s&p global platts top 250

TRANSCRIPT

www.platts.com

China – the big questionsThe new economic scenarios. What they mean for

crude demand. And are the data giving the true picture

Greetings from the GulfWhat the changing shape of Middle Eastern

market share reveals about Asia’s energy dynamics

S&P Global Platts Top 250Global energy company rankings – in a tumultuous year

PLUS: INDIA – THE NEW DRIVER • INDONESIA GASOLINE • PETCHEMS • US CRUDE – AND MORE

Asia & the New Oil Landscape

Autumn 2016

Every dawn brings with it new opportunity & every new opportunity - A unique set of risk.

themes of today’s Commodity and Energy Trading Industry. With the growing need to address

GLOBAL THOUGHT LEADERSHIP. DELIVERED.

InsightAutumn 2016

ISSN 2153-1528 (print)ISSN 2153-1536 (online)

Publisher

Murray Fisher, 720-264-6644

murray.fi [email protected]

Editor

Maurice Geller

Production Manager

Nelson Sprinkle

Designer

Constantina Bertsoukli

Production Offi ce

Platts Insight Magazine

1800 Larimer, Suite 2000

Denver, CO 80202

Global Director, Conferences

and Strategic Media

Steven McCarthy, 857-383-5727

Advertising Sales Manager

Robin Mason, 631-642-2600

Article Reprints and Permissions:

The YGS Group, +1 717-505-9701, ext

Subscribe free at:

http://marketing.platts.com/forms/

SMSInsightSubscribe

S&P Global Platts

20 Canada Square, 9th Floor

London, E14 5LH, UK

President:

Imogen Joss

VP Finance:

Hywel Thomas

Global Head of Content:

Martin Fraenkel

Global Head of Oil Content:

Dave Ernsberger

Global Editorial Director, Gas,

Power, Coal and Petrochemicals:

Simon James Thorne

Content Director, Asia:

Sarah Cottle

ContentsAutumn 2016

A matter of projection ............................................................................... 6What are the implications of a slowing economy

for Chinese oil demand? Choose your scenario

China’s true crude demand ..................................................................... 10It may be higher than it appears, with

the fi gures skewed by incomplete data

Infrastructure angst ............................................................................... 16The stumbling block for China’s

blossoming independent ‘teapot’ refi neries

Changing shape of Persian Gulf .............................................................. 19Dramatic shifts in Middle Eastern market share

as producers compete to meet Asia’s needs

Driving force ........................................................................................... 22All eyes are on India as the new motor

behind global oil demand in coming years

Stormy waters ........................................................................................ 26Boom times led to a ship-shopping spree

but now the tanker market may be swamped

US crude migration ................................................................................ 32 What has happened since the lifting of the US

export ban – and where are the barrels going?

Petchems strives to keep its edge .......................................................... 38Cheap feedstocks meant beautiful margins

for Asian players but that may soon be eroded

Gasoline goes into reverse ..................................................................... 42Weak fundamentals and excess supplies

have tarnished last year’s ‘King of the Barrel’

Indonesia’s refi ning industry .................................................................. 46Developments are fi nally taking off – which

may not be good news for oil product exporters

Myanmar’s roadblock ............................................................................. 49Failure to tackle surging energy demand

could prove an expensive obstacle to growth

S&P GLOBAL PLATTS TOP 250 ................................................................. 52The 15th annual global energy rankings,

as a price shakeout sparks industry upheaval

Cover Photo: ©shutterstock/chuyuss

“People say believe half of what you see, some or none of what you hear,” goes the Motown anthem. And much of this special APPECissue of Insight magazine involves intense scrutiny of Asian economic and energy scenarios and the assumptions underlying them as wellas the implications for crude and oil products demand.

Skepticism may turn momentarily to disbelief almost elsewherein this issue, even for those inured to the wild price action and volatility of the past year or two. Witness the Top 250 feature –our 15th annual global energy company rankings with perhaps the most dramatic shifts to date. I won’t say any more here – read on.But the list of biggest movers – up as well as down – is particularly eye-opening.

This is also our inaugural APPEC issue – to tie in with an event that, since its inception in 1985, has grown to become one of Asia’s most important oil industry forums. The acquisition of APPEC by S&P Global Platts refl ects our commitment to providing up-to-date industry intelligence and deepening the insights and attendance base thatthe oil community has come to expect from this event.

And it comes at a particularly signifi cant time for the industry. As one of our authors says – and proceeds to demonstrate – the importance of the region to global oil demand over the next fi ve years could not be more clear. Equally, it’s hardly going out on a limb to suggest those fi ve years will throw up as many challenges as they do opportunities.

But ultimately what one can bank on, for markets and businessesto survive and thrive, is a capacity for innovation, adaptability, resilience – and trust.

In the end, pace Marvin Gaye, as Mariel Hemingway said toWoody Allen at the end of Manhattan, “You have to have a littlefaith in people.”

Editor’s Letter

Maurice Geller

Editorial Director,

Central Editing Desk,

EMEA,

S&P Global Platts

PlattsOil AnalyticsSo much of your success lies in understanding the space betweenprice and value. It’s where you’ve always found us, talking to themarket every day, gathering data and publishing our price assessments.

To meet market demand, we’re taking our analysis of this world evenfurther, not just of the transactional side of price but also the supplychain dynamics shaping it.

Building on the insights our editors and analysts already share with you,we’re expanding our data sets and analytical tools to give you even greatercoverage of oil industry verticals and the trade-fl ows between them.

With S&P Global Platts facilitating connected thinking across tradingprice and supply chain infl uences, this wider context of value helps youfurther develop your own view and seize the opportunity you fi nd there.

Platts China Oil Analytics | Platts cFlow | Platts Ocean Intelligence | Platts Well Economics Analyzer

www.platts.com

ANALYTICSANALYTICS

China Economy

6 Platts Insight Autumn 2016

Where China is heading – a matter of projectionWhat is the likely extent of a slowing economy – and its implications for Chinese oil demand?

As crude demand falls in the OECD over the next fi ve years, oil demand will increasingly be driven by Asia. The importance

of the region to global oil demand over the next fi ve years could not be more apparent – witness the International Energy Agency’s expectations of incremental global oil demand over the period 2015-2021(Chart 1).

The IEA expects global demand to grow by 7.2 million b/d by from 2015 to 2021. While demand from India, the Middle East and other non-OECD Asian countries is expected to account for 4.1 million b/d or 57% of total incremental demand, it is China that will be in everyone’s sights over the six years 2015-2021. With uncertainties over the sustainability of China’s economic growth, there are questions over whether China can really be expected to account for a third or 2.4 million b/d of newcrude demand.

China’s economy has performed remarkably well since 2000 with growth rates averaging 9.5%. However, much of this growth has been built on giving state-owned enterprises (SOEs) access to easy credit where it has been funneled into the real estate, infrastructure and heavy industry sectors. This has resulted insignifi cant misallocation of capital

and overcapacity across many industrial sectors and which has become a drag on the economy.

We can identify three narratives that are used to explain the Chinese macro-economy:

• “Hard Landing” – offi cial numbers can’t be trusted and are thought to be suspect. The “true” growth rate as measured by metrics like railway cargo volume and electricity consumption is more like 2% to 3%;

• “It’s still largely under control” – There may be problems, but the Chinese authorities have a great track record in managing the economy;

• “Extend and pretend” – Growth is probably close to the offi cial number but this is being propped up by credit which is unsustainable.

At S&P Global, our view is that the “extend and pretend” narrative is closest to the actual situation on the ground with credit continuing to grow faster than nominal GDP (Chart 2).

While consumption, which in China is not primarily driven by debt, is holding up well, credit continues to be channeled into the increasingly unproductive state-owned sector where there are fewer and fewer opportunities for productive investment. While we do not think that the Chinese economy is in imminent danger of a macro shock or

Sebastian Lewis

Content Director, China,

S&P Global Platts

China Economy

Autumn 2016 Platts Insight 7

rapid slowdown in growth, we do believe that this strategy of continuing to prop up growth with credit is unsustainable.

In order to rein in credit growth and bring the economy on to a more sustainable path the government needs to engage in structural reform targeted at the state-owned sector so that it becomes more productive and requires less credit. This would result in an economy with a smaller state-owned sector, with growth being driven by the larger (and more productive) private sector. It would also entail considerable social costs as the government removes

overcapacity and overemployment in the state sector. This would also mean the government accepting a lower, but more sustainable, rate of growth, something that thus far it seems unwilling to do. (Lower growth would mean for example abandoning Premier Xi Jinping’s much publicized “China Dream” of doubling 2010 GDP by 2020.)

The government has laid out plans for structural reform in the latest fi ve year plan (2016-2020) however the implementation has been slow and radical reform does not seem to be on the cards. That said, we believe the

government has fi scal and external reserve cushions and effective policy levers to support growth and fi nancial stability at least in the short to medium term. Given this we expect China to continue to grow at around 6% for the next three years.

Earlier this year S&P Global Ratings published a paper which examined a hypothetical “hard downside” economic scenario in which the government sharply constrains lending to SOEs in order to accelerate the rebalancing of the economy which inadvertently triggers a sharp slowdown in growth as the private sector adopt a wait and see attitude towards investment and consumer spending fails to pick up from current levels. In this “hard downside” scenario Chinese GDP growth slows to an average annual 3.4% over 2017-2020 from 6% in our baseline projection.

We have modelled Chinese oil demand to see how it performs under our baseline, low growth and “hard downside” scenarios. We use an approach to modelling oil demand based on projecting historical trends in per capita GDP and per capita over the period 2010–2015 into the future. Our economic assumptions and resulting forecasts for Chinese crude demand are given in the table and chart (Table 1, Chart 3).

Our base case sees Chinese oil demand rise to 13.3 million b/d by 2020, or 2.2 million b/d of new incremental demand over the fi ve year period 2016-2020.This is in line with 2020 oil demandas forecast by the IEA of 13.2 millionb/d in its 2016 Medium Term Oil Market Report. This is hardly surprising as the economic assumptions from the IMF that the the Paris-based agency usesto forecast medium term oil demandare very similar to the base casegrowth rates produced by our S&P Global economists.

IEA PROJECTED GROWTH IN OIL DEMAND 2015�2021 & SHARE OF GLOBAL GROWTH

Source: ΙΕΑ

-1

0

1

2

3

ChinaOther AsiaMiddle EastIndiaAfricaRoWOECD

(million b/d)

-14%

11% 13%15%

18%

24%

33%

Chart 1

CHINA: CREDIT GROWTH VS NOMINAL GDP GROWTH

Source: S&P Global

-10

0

10

20

30

40

50

60

70

2015201420132012201120102009200820072006

(%) Aggregate FinancingCumulative difference Nominal GDP

Chart 2

©shutterstock/LIUSHENGFILM

Autumn 2016 Platts Insight 9

Oil demand slips slightly in the downside scenario to 13.2 million b/d by 2020. Or 100,000 b/d less incremental demand 2016-2020 than the base case. In the hard downside case demand falls sharply, reaching only 12.5 million b/d by 2020, around 800,000 b/d around 800,000 b/d lower than the base case.

Forecasting oil demand in the “hard downside” case is made more diffi cult because this scenario assumes a heavy contraction in fi xed investment like construction, and infrastructure which is more oil intensive than consumption which includes consumer goods and services. The “hard downside” assumes that fi xed investment falls to 32% of GDP in 2020 from 43% in 2016. We have taken account of this by modelling the historical relationship between oil demand and both investment and consumption components of GDP and projecting these into 2017-2020. In this scenario growth in investment is negative and consumption growth falls in the initial years with consumption growth improving from 2019 onwards. Using these assumptions we fi nd that demand growth falls by more than half compared to the base case, reaching only slightly more than 12.0 million b/d by 2020, around 1.2 million b/d down on the base case.

But any rapid fall in Chinese growth would have signifi cant knock-on effects to the global economy. A decline in Chinese investment and a substantially depreciated yuan would see a slowdown in Chinese imports. Given that China’s imports only account for only around 3% of global GDP this would actually be a relatively minor shock to the global economy but would be most keenly felt by economies like Taiwan and Korea with high trade exposure to China.

Much more signifi cant would be the effect that this would have on global business and consumer confi dence. In our “hard downside” scenario, we see

global growth impacted via lower global investment, capital outfl ows from emerging economies and the depreciation of their currencies. Investors and banks around the world would become more risk-adverse, provoking a liquidity squeeze in emerging economies similar to that seen in 2008-2009 with milder liquidity stresses occurring in developed economies. This “hard downside” scenario for China would see an annual shortfall in global GDP of just under 1% over 2017-2020 (or a cumulative 3.8%).

In terms of impact on global oil demand, this lower global growth scenario would see global oil demand fall by at least 1.8 million b/d compared to our base case and indeed we believe the decline could be even greater if much of the fall in oil demand is as a result of a pullback in investment in emerging markets especially in Asia which will be more impacted by any China “hard downside” than regions like Europe and North

America which will feel less of an impact as well as being less oil intensive. At the same time this demand shock would also result in dramatically lower prices for oil and other commodities which would be positive for oil and commodity importers. We do stress however that this hard downside scenario is a tail-risk analysis. As such, it is neither part of S&P Global base-case nor even our downside view about the Chinese economy and oil demand.

The Chinese state has suffi cient fi scal reserves and control over the fi nancial sector that it can step in and ensure enough credit is supplied to the economy to support growth if it starts to falter (at least in the short term). However this will just be delaying the inevitable reforms that must take place if China is not to succumb to a prolonged period of low growth. Or in the words of Laozi (Lao Tzu) the ancient Chinese philosopher and founder of Daoism (Taoism) “If you do not change direction, you may end up where you are heading”.

CHINESE OIL DEMAND UNDER THREE GROWTH SCENARIOS

Source: S&P Global, IEA, Platts

0

2

4

6

8

10

12

14

2020201920182017

(million b/d) DownsideBase case Hard downside

Chart 3

REAL GDP BASELINE, LOW & HYPOTHETICAL “HARD DOWNSIDE” SCENARIOS (%)

2017 2018 2019 2020Base Case 6.1 6.0 6.0 6.0Downside 5.8 5.7 5.7 5.7Hard Downside 2.5 2.6 3.6 5.0

Source: S&P Global

Table 1

China Economy

©shutterstock/Hung Chung Chih

Autumn 2016 Platts Insight 11

Playing by numbers: China’s true demandCrude demand may be higher than it appears with figures skewed by incomplete data

Anyone monitoring headline oil demand data in China would have noticed that growth this year has decelerated

signifi cantly from the heady rate of 2015, when low oil prices encouraged consumption at the pump while the ongoing economic transition to consumption-led expansion boosted transport fuels such as gasoline andjet fuel.

In 2016, apparent oil demand during the fi rst six months contracted slightly by 0.6%. In contrast, it spiked 5.8% in 2015 – the strongest growth rate since the end of the global fi nancial crisis. Strength was seen particularly in the light ends with gasoline’s apparent demand surging 9%.

What has put thebrakes on growth?

The Chinese government does not release consumption data on oil. S&P Global Platts, as well as other agencies looking at China, uses a proxy for oil demand by adding domestic production – comprising refi nery runs released by the National Bureau of Statistics – to net imports of oil products, data for

which is made available by the General Administration of Customs.

Calculations based on these data put apparent oil demand at 11.15 million b/d during the fi rst half, a 0.6% decline year on year. Yet crude oil imports this year have upended expectations and risen nearly 900,000 b/d, or 13.6%, over the period. This incremental volume is nearly equal to the growth in crude imports in 2014 and 2015 combined.

If crude imports are so strong and demand appears to have weakened, does it imply a signifi cant volume of crude going into stocks?

On the contrary, Platts believes apparent demand to be higher because independent refi ners have raised their processing rates signifi cantly this year, but this has not been captured by the offi cial statistics.

The NBS reported that total refi nery runs in China over the fi rst half rose just 1.9% or nearly 200,000 b/d to 10.73 million b/d. However, data collected by Platts and JYD Commodities Hub, a domestic data provider, shows that over 600,000 b/d of additional crude oil was processed by independent refi ners

Yen Ling Song

Senior Analyst,

S&P Global Platts

China Demand

12 Platts Insight Autumn 2016

during the fi rst half comparedwith the same period of 2015. Theserefi ners have raised their run ratesfrom an average of 39% over January to June last year, to 54% in the fi rsthalf of 2016 and this has been thedirect result of the government deregulating the refi ning sectorand allowing independent refi nersto import crude oil.

Before this, they were offi cially banned from importing crude oil and mainly relied on crudes that were available in the domestic market, supplemented with imported fuel oil. The restrictions on their feedstock posed cost challenges which constrained their operations. But after the government awarded 1.2 million b/d of new crudeoil import rights to independent refi ners since the second half of last year, these refi ners have now been able to boost utilization to record levels, with some even claiming to be running at 80%to 100%.

Since the deregulation, independent refi ners have made a big impact on global markets, accounting for at least three quarters of the growth in China’s crude oil imports this year and opening up a new avenue for foreign traders and crude suppliers to do business in China in an area traditionally dominated by a handful of state-owned companies.

In previous years independent refi ners largely operated under the radar and typically accounted for less than 10% of China’s refi nery runs. Incentivized by the newly acquired crude import quotas to compete on a level playing fi eld, this year they have, in true David and Goliath fashion, leveraged their nimbleness, small scale and fl exibility to seize market share from the state-owned giants by undercutting them on price.

Independent refi ners have likely doubled their crude processing volumes in the last year, according to Platts estimates. Faced with heated competition, the state-owned companies have raised their exports of oil products by some 70% to a record high level of 680,000 b/d. Dominant refi ner Sinopec, the largest by capacity in Asia, reported a 3% decline in refi nery runs in the fi rst half of this year.

So why is data from independent refi ners not being captured by the offi cial statistics? Independent refi ners have been notorious for going to great lengths to minimize payment on taxes. Because of the way consumption taxes are structured in the country – different

tax amounts are levied on various oil products and crude oil, while exemptions can be applied under certain conditions – companies have been creative at fi nding loopholes to avoid paying some consumption taxes. This, coupled with hitherto poor oversight by offi cials, has resulted in tax avoidance among independent refi ners becoming a fairly widespread yet covert practice for many years.

But sources explain that the NBS collates domestic production of commodities by looking at tax submissions, known in China as fapiao. These are invoices issued for every kind of payment made in China and are used by the government to monitor tax payments. So if tax payments are avoided, then the NBS will not be able to tally production accurately.

This is key to understanding why there is such a big difference between the growth in crude oil imports and the apparent oil demand fi gure this year.

If independent refi neries were included in the calculation, that would raise refi nery runs by at least 400,000 b/d

CHINA’S APPARENT OIL DEMAND

Sources: National Bureau of Statistics, General Administration of Customs, Platts China Oil Analytics

0

2

4

6

8

10

12

DecNovOctSepAugJulJunMayAprMarFebJan

(million b/d) 2014 2015 2016

If tax payments

are avoided, then

the NBS will not be able

to tally production

accurately

China Demand

Autumn 2016 Platts Insight 13

this year, meaning apparent demand would likely have increased by 3%, rather than a 0.6% contraction if calculated using the offi cialgovernment data.

This would be closer in line with Platts China Oil Analytics’ original forecast of 2% growth for apparent oil demand in China in 2016. Macroeconomic data

also support this rate of growth. GDP growth in China in the second quarter came in at 6.7%, unchanged from the fi rst three months of the year but stronger than market expectations. Secondary sector nominal GDP – an indication of expansion in the industrial and manufacturing sectors – rose to 4.8% year-to-date in the second quarter, the strongest pace of growth

since late 2014. Credit also continues to fl ood the economy, with total social fi nancing rising by nearly $1.5 trillion in the fi rst half.

S&P Global Ratings, a sister divisionof Platts, in July raised its forecast for China’s GDP growth in 2016 to 6.6%,up from its previous forecast of 6.4%.

©shutterstock/tolotola

China Demand

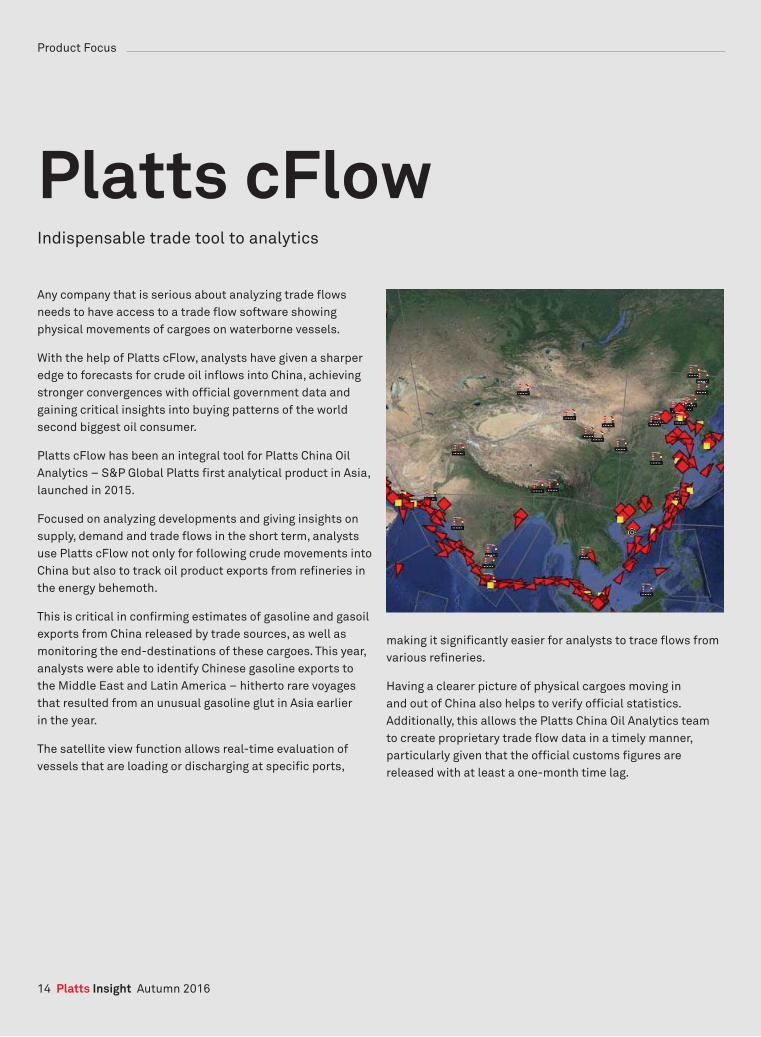

Platts cFlowIndispensable trade tool to analytics

Any company that is serious about analyzing trade fl ows needs to have access to a trade fl ow software showing physical movements of cargoes on waterborne vessels.

With the help of Platts cFlow, analysts have given a sharper edge to forecasts for crude oil infl ows into China, achieving stronger convergences with offi cial government data and gaining critical insights into buying patterns of the world second biggest oil consumer.

Platts cFlow has been an integral tool for Platts China Oil Analytics – S&P Global Platts fi rst analytical product in Asia, launched in 2015.

Focused on analyzing developments and giving insights on supply, demand and trade fl ows in the short term, analysts use Platts cFlow not only for following crude movements into China but also to track oil product exports from refi neries in the energy behemoth.

This is critical in confi rming estimates of gasoline and gasoil exports from China released by trade sources, as well as monitoring the end-destinations of these cargoes. This year, analysts were able to identify Chinese gasoline exports tothe Middle East and Latin America – hitherto rare voyages that resulted from an unusual gasoline glut in Asia earlierin the year.

The satellite view function allows real-time evaluation of vessels that are loading or discharging at specifi c ports,

making it signifi cantly easier for analysts to trace fl ows from various refi neries.

Having a clearer picture of physical cargoes moving inand out of China also helps to verify offi cial statistics. Additionally, this allows the Platts China Oil Analytics teamto create proprietary trade fl ow data in a timely manner, particularly given that the offi cial customs fi gures are released with at least a one-month time lag.

Product Focus

14 Platts Insight Autumn 2016

Platts cFlowConnecting the dots you can see – and the dots you can’t

Gaining a deeper, richer understanding of today’s waterborne commodities marketrequires more than simply connecting the dots on a satellite map. To completethe picture, you need to combine real-time vessel location information with the latest news, market data, trends, prices, insight and analysis.

Platts cFlow is a trade fl ow analytics service that helps you join up your tradingideas with dynamic market fundamental-driven information to make more informedtrading and operational decisions. With Platts cFlow you can view, monitor and analyzethe key factors affecting the supply chain and impacting prices such as vessel movement, cargo data and freight bunker pricing information.

For more information visit www.platts.com/products/cfl ow

www.platts.com

ANALYTICSANALYTICS

16 Platts Insight Autumn 2016

Infrastructure angstThe biggest stumbling block for China’s blossoming independent ‘teapot’ refineries

Several independent Chinese refi ners have joined the export bandwagon this year butmust overcome signifi cant

infrastructure challenges to have a smooth and profi table ride.

So far in 2016, 10 independent refi ners have won quotas to export 1.255 million mt of refi ned products. As of July, they have exported around 200,000 mt.

The independent “teapot” refi neries, as they are often called, refer to those that have not been built by state-owned oil majors CNOOC, Sinopec, PetroChina and Sinochem – though CNOOC and Sinochem later acquired stakes in some of these refi neries to meet their own strategic needs.

Exporting products is a new business for them given that until early last year, they were not even allowed to process imported crudes and relied either on domestic crude or imported fuel oilfor feedstock.

But a lot has changed in the last year since Beijing deregulated crude imports and allowed the independents to start processing imported grades. With ample feedstock choice and availability, these refi ners have boosted run rates and production and have surplus products available for export.

Too much, too soon?

But all these opportunities may have come a little prematurely.

Lack of adequate pipeline, storage and port infrastructure has added greatly to their cost of doing business and solving those problems is key to securing their long-term profi tability.

Infrastructure bottlenecks have led to a heavy reliance on trucks to transport crude and products.

An estimated three out of every four independent refi neries in Shandong province have to rely either in part or entirely on trucks to transport crude and/or oil products, according to Platts China Oil Analytics.

Companies like Chambroad Petrochemical, Fuhai Petrochemical, Yatong Petrochemical and Qingyuan Petrochemical have set up trucking businesses, each with a vehicle fl eet ranging from 100 to 400.

Oceana Zhou

Senior Writer, Oil,

S&P Global Platts

Ports are also

under pressure with the

rise in refi ning activity

in the region

China Independents

Autumn 2016 Platts Insight 17

The high land freight costs take a big bite out of the refi ners’ margins. To illustrate, the point-to-point transportation cost of state-owned refi ners who own ports, storage tanks and an extensive crude and oil product pipeline network is half that compared with transportation via trucks.

These trucks are loaded with 30 mt tanks, a standard size that has in recent years been strictly regulated by the local government.

When Hongrun Petrochemical exported its fi rst gasoline cargo in April this year, the 35,000 mt parcel had to be transported on over a thousand trucks before it could be loaded and shipped out of Laizhou port, more than 200 km northeast of its refi nery in Qingzhou city.

Similarly, Chambroad Petrochemical spent at least Yuan 3.2 million ($500,000) to send the cargo from its refi nery in Zibo to Laizhou port.

Freight for sending gasoline to the ports is around Yuan 160/mt ($2.88/barrel),

Shang Xinkai, trading manager with Chambroad, told S&P Global Plattsin March.

One advantage of road transport however, is that it provides fl exibility for independent refi neries to send their oil products to various parts of China.

Some independent refi ners sell their products as far away as Yunnan province in southwest China, about 2,500 km from Shandong, but transportation cost is also high at about Yuan 600/mt ($12.31/b), according to an offi cial at Zibo-based Wonfull Petrochemical.

Ports are also under pressure with the rise in refi ning activity in the region.

Qingdao Port, which oversees the busiest Huangdao port and the new Dongjiakou port, is currently the largest in China in terms of annual cargo turnover, but it is one of only two in Shandong that can receive VLCCs. Not surprisingly, it has been hit the hardest.

Since the third quarter of last year,

congestion has become routine at the port. Early this year when the independent refi ners imported a wave of crude cargoes, vessels waited between three weeks to a month before they could discharge at Qingdao.

A VLCC that is in the Qingdao queue for 25 days may incur additional costs of more than $2 million, or $1/b, to be borne by the buyer of the cargo, according to a trading source with Chinaoil.

Projects underway

Given the urgent need to improve transport links, plans are underway to build more pipelines.

One major project many companies are eagerly awaiting is the 400,000 b/d Yanzi pipeline, which will run from Yantai port in northern Shandong, to Zibo in the central part of the province.

Construction of the pipeline was completed in July 2016 but it is stillnot clear when the pipeline will begin operations as several approvals arestill pending.

This would be the second crude oil pipeline to be freely available to independent refi ners. The fi rst is the existing 400,000 b/d Huangwei pipeline which connects Huangdao port in Qingdao with Weifang city, another refi ning hub in central Shandong.

Separately, the port of Qingdao has proposed a plan to construct a pipeline to connect its new VLCC berth in Dongjiakou, adjacent to Huangdao, with Weifang and Dongying.

But these projects will not materialize overnight as they are capital intensive and require long lead times, especially

China Independents

18 Platts Insight Autumn 2016

as they span multiple districts and municipal areas, from which approvals must be sought. In addition, pipelines may involve numerous partners and getting alignment from all stakeholders often leads to delays.

The outlook for oil products is even more dire as there are only a couple of pipelines and those too are dedicated to specifi c refi neries.

Key to survival

It is hard to generalize how independent refi ners continue to make money and operate despite their additional operational costs as each of them has a unique plan and mode of survival. Moreover, as these refi ners test the

international markets, their aims and ambitions vary. Some see the higher costs incurred to export products as an investment in the future as they look to shed their traditional reputation of being producers of sub-quality products made from fuel oil.

This goes beyond economics and is related more to getting the experience of exporting products and creating a brand name for themselves. It helps them show their products are acceptable to international buyers.

Moreover, it is not just the independent refi ner who is keen to make a mark in the export market. Trading houses are just as keen to build relationships with them and offer them advantageous deals.

Trafi gura has been one of the most active companies. Besides supplying foreign crude it has also been the offtaker of a number of gasoline cargoes exported by these refi ners.

Sources said Trafi gura has struck a tolling deal with Luqing Petrochemical in particular to sell the refi nery crude feedstock and buy the gasoline processed. This can be seen as an example of the trading houses abilityto help independent refi neries toexport barrels.

But this does not mean there will be a big outfl ow of oil products from the independent refi neries. A sustainable rise in exports will ultimately depend on margins, and that is linked to having the right infrastructure.

Yellow Sea

Bohai Bay

CHINA

Henan

Shandong

Hebei

Ridong pipeline

Yanzi pipeline

Donghuang pipeline

Huangwei pipeline

Laichang pipeline

Proposed Dongwei pipeline

Port

Qingdao

Dongjiakou

Rizhao

Yantai

Laizhou

Longkou

Dongying

Dongying

Zibo

Weifang

Heze

Dezhou

Source: Platts China Oil Analytics

MAJOR PORTS AND PIPELINES IN SHANDONG

China Independents

Autumn 2016 Platts Insight 19

Changing shape of Gulf’s market shareMixed results from Middle East producers show intense competition to meet China’s needs

The Middle East has been losing its share of global crude oil sales to Asia’s biggest energy consumer, despite near-record

output for at least the past year by key Persian Gulf producers.

The surprising trend, which began in 2013, is masked by large monthly fl uctuations in oil trade, but is revealed by analysis of Chinese customs data on imports of crude oil by source country.

The data show Chinese imports of Persian Gulf and other Middle East crudes growing in volume to average 3.364 million b/d in 2015 from 2.943 million b/d in 2013 for a 14.3% increase over two years. However, the Middle East’s share of total Chinese crude imports fell over the same period by more than fi ve percentage points to 50.9% from 56.3%, meaning that other suppliers, including Russia, Angola and Brazil, have been outperforming their Middle East counterparts in boosting crude sales to China. New exportersare also joining the fray – even theUS, which has started selling crudeto China.

The market-share downturn continued in the fi rst fi ve months of this year,

dragging the Middle East’s share of Chinese crude imports below 50% mark for the fi rst time in years. (Fig.1)

That surely casts doubt on the effectiveness of the Saudi-led strategy, to which key Arab oil producers from the Persian Gulf region have adhered since late 2014, of maintaining high output to protect their share of the global market instead of defending prices. China is by far the biggest oil consumer in the Asia-Pacifi c region, which for years has been the key export market for Persian Gulf producers.

In 2015, China consumed 559.7 million mt (11.24 million b/d) of crude oil and refi ned petroleum products, according to BP in the latest issue of its Statistical Review of World Energy, amounting to more than a third of total oil consumption in the Asia-Pacifi c region last year.

A closer look at Chinese imports reveals that, among the large Persian Gulf producers, Saudi Arabia has suffered the biggest erosion of its share of the Chinese oil market. That fell to 14.9% in 2015 from 19.6% two years earlier, accompanied by a nearly 9% decline in export volumes to China. The sales volumes rebounded in the fi rst fi ve

Tamsin Carlisle

Senior Editor,

Oil News and Analysis,

S&P Global Platts

Middle East Supply

20 Platts Insight Autumn 2016

months of 2016 to average more than 1 million b/d for the fi rst extended period since 2013, but even that failed to arrest a further decline in market share to 14.2%.

Iran, as it struggled under international sanctions targeting its petroleum sector, saw the Gulf region’s second largest fall in market share of crude sales to China in 2013-15 with a drop of nearly two percentage points to 7.9% from 9.8%. Despite the January lifting of the most economically damaging

sanctions, Iran saw its share of Chinese crude imports slip further in January-May 2016, to 7.7%.

The region’s other major oil producers have fared better with loss of marketshare since 2013 amounting to less than a percentage point each forthe UAE and Oman – the largestArab oil producer from outside OPEC.Iraq and Kuwait have managed toincrease both oil export volumes to China and their respective market shares, although not enough to offset

completely the corresponding Saudi and Iranian declines.

Iraq provided a steady 9.3% of Chinese crude imports between 2013 and 2015 and in the fi rst fi ve months of 2016 achieved a slight increase to 9.5%.That was backed by an almost 50% increase in export volumes to China over the past two-and-a-half years which may be due, at least in part, to Chinese state-controlled company involvement in projects to boost output from some of Iraq’s largest oil fi elds. Those include the giant BP-operatedRumaila fi eld where China National Petroleum Co. holds a 46.4% stake in the development.

Kuwait, which exports less than halfas much oil to China as neighboring Iraq, has achieved the region’s best results in terms of percentage gainsin its crude sales to the big Asian consumer. Volumes are up nearly 65%, while market share has climbed to 4.2%from 3.6%. Kuwait strives to maintain close commercial and trade ties with China and is a partner in a project to build a refi nery and petrochemicals complex in China’s Guangdong province. However, the project has faced a series of delays.

Overall, the mixed results from Middle East producers exporting to China suggest the Gulf region’s major exporters may be competing as intensely with each other as well as with other international producers to supply China’s oil needs.

Elsewhere in the Asia-Pacifi c region, Japan, with a mature economy, has increased its crude imports from most major oil producers in the Persian Gulf region, including Saudi Arabia and Iran . Both have gained market share there

CHINESE OIL IMPORTS BY SOURCE

Source: Platts

0

5

10

15

20

YemenQatarKuwaitUAEIranOmanIraqSaudi Arabia

(%) 2013 2014 2015 Jan-May 2016

INDIA OIL IMPORTS BY COUNTRY, 2016

Source: Platts

0.0

0.2

0.4

0.6

0.8

1.0

1.2

UAESaudi ArabiaQatarOmanKuwaitIraqIranEgypt

(million b/d) Jan Feb Mar Apr

Fig1.

Fig2.

Middle East Supply

Autumn 2016 Platts Insight 21

since 2013. Over the same period, only Oman has seen a signifi cant drop in its share of Japan’s oil market. However, that market is smaller than China’s and likely to expand slowly at best in coming years.

If some Middle East producers are losing ground in the crowded Chinese market, they still have a chance closer to home to grab a chunk of the rapidly emerging Indian oil market, which so far this year has been importing around 2.8 million b/d of crude from Middle East producers to feed its large refi neries. That compares with about 3.6 million b/d of Middle East oil imports by China and 2.9 million b/d by Japan in the January-May period (Fig.2).

“We’re already ahead of China in economic growth. The brightest spotin the global economic landscape is India,” the spokesman for India’s ruling BJP, Narendra Taneja, told S&P Global

Platts earlier this year in an interview in Doha in which he said India’s government planned to pursue domestic and international petroleum-sector partnerships with Persian Gulf oil and gas producers.

“We are doing everything possible to deepen our energy ties with the region’s oil producers, particularly Saudi Arabia and Iran,” he said.

A barrier for some could be that India wants equity in any international upstream oil and gas ventures in which it participates, even in the Gulf region where most of the biggest producers –Saudi Arabia, Kuwait, Iraq and Iran –offer only service contracts. However, India already has close to $20 billion invested in Iran and is taking a good look at the country’s oil and gas exploration and production sector for further opportunities, Taneja said.

“We would be most interested in buying equity in oil fi elds,” he said, referring broadly to international investment plans. “Our strategy is to invest in equity oil and equity gas so we could bring the oil and gas to India.”

Speaking at an industry event in Doha, Taneja said he favored oil prices in the range of $40-58/b as the sweet spot that would be good for consumers and producers and would stimulate the global economy. At such prices most Middle East upstream oil projects could still offer attractive returns, while many outside the region would struggle.

From a Middle East oil producer’s perspective, if oil prices were tostay in Taneja’s favored range, it just might be worth opening up to equity investment by a trade partner eager to buy more crude.

©shutterstock/vahitdag

Middle East Supply

India Demand

22 Platts Insight Autumn 2016

Driving force: India moves into top gear The nation’s thirst for oil is a key factor behind global demand growth this year and next

It’s neither a knee-jerk reactionto feeble oil prices nor atemporary upsurge on theback of seasonal swings.

Taking a deeper look at India’s ballooning oil demand trajectory over the last year or so clearly points to one thing – that growth is holding up on the back of fundamentals and structural factors, and this is sending a strong signal to world markets that the momentum is here to stay.

The BJP government’s clearly focused policies for the oil sector, strong and sustained GDP growth, a huge push towards making India a manufacturing hub and rising disposable incomes are all playing crucial roles in helping accelerate India’s oil consumption into top gear.

The International Energy Agency in its July report said that India’s thirst for oil will be a key factor driving global oil demand growth this year and next year. It expects India’s oil demand to rise by 280,000 b/d in 2017, closely followedby China.

Buoyant Indian demand growth and strong government policy initiatives have

raised the interest level of international companies to make inroads into India’s retail oil sector. Highlighting that, India’s Petroleum Minister Dharmendra Pradhan in June said that companies such as Saudi Aramco and Total have expressed interest in setting up retail fuel stations in India.

India’s oil products demand grew 8.5% in 2015 from 2014 levels to 177 million mt, or 3.81 million b/d, as gasoline, LPG and naphtha saw double-digit growth in consumption. And in the fi rst half of 2016, India’s overall oil products demand surged 11.1% to 97.62 million mt, or 4.2 million b/d. The IEA expects total Indian oil products demand to average 4.3 million b/d in 2016.

With the country dependent on imported crudes, LNG and LPG for meeting a large chunk of demand, the petroleum ministry, led by Pradhan, is taking steps to strengthen relationships with key suppliers. Pradhan has visited countries such as Iran, Qatar and Russia to boost energy ties with them.

The ‘make in India’ dream

One of the brightest spots on which the world oil market is banking its hopes

Sambit Mohanty

Senior Editor,

Asia Oil News & Analysis,

S&P Global Platts

India Demand

Autumn 2016 Platts Insight 23

on India is the government’s ‘Make in India’ initiative – which aims to boost the share of the manufacturing sector in GDP from 15% to as high as 25%by 2022.

This is expected to give a huge liftto demand for industrial fuels. In addition, the push to build more highways and expand road infrastructure is expected to ignite demand for transport fuels.

“In this new era of slower Chinese growth, a new contender has emerged: India, which in 2015 was the main driver of non-OECD oil demand growth,” the Oxford Institute for Energy Studies said in research paper published earlierthis year.

“In addition to the boost from low oil prices, structural and policy-driven changes are underway which could result in India’s oil demand ‘taking off’ in a similar way to China’s during the late 1990s, when Chinese oil demand was at levels roughly equivalent to current Indian oil demand,” the institute added.

Galloping gasoline

Gasoline continues to gain ground since late 2014 when a removal of subsidies on diesel triggered a massive shift towards gasoline-driven vehicles in the passenger cars segment. With the transport sector accounting for almost 40% of India’s oil demand, gasoline sales in the domestic market rose nearly 15% in 2015 to 21.1 million mt.

And the momentum continues this year. Gasoline consumption in the fi rst half of 2016 grew nearly 13% to 11.63 million mt.

In the 2015-16 fi scal year to end-March,

India’s domestic automobile sales were 20.47 million units, a growth of nearly 4% from the previous year’s 19.72 million units, according to data from the Society of Indian Automobile Manufacturers.

And expectations are growing that as disposable incomes rise, the shift in ownership would take place in favor of passenger cars, from two-wheelers, leading to rising consumption of transport fuels, the Oxford Institute study said.

Diesel sales were up 5% to 72.7million mt in 2015, which is seen as substantial given the large base. And as the manufacturing push continued, diesel demand growth picked up in the fi rst half of 2016, rising 7.8% to 39.59million mt.

Market participants are of the view that despite gasoil losing out to gasoline in the passenger vehicle segment, strong demand from the industrial sector will more than offset the losses.

Clean fuels surge

As New Delhi steps up efforts to promote LPG as a cooking fuel across the country, demand continues to grow at a healthy pace, rising by close to 10% in the fi rst half of the year to 10.06 million mt.

“The government’s drive to increase total LPG dealerships by 60% should keep LPG demand growth above 8% year on year here on,” Credit Suisse said in a research note, adding that while LPG penetration was as high as 88% in urban India, it was only about 20% in rural India. A raft of government initiatives propelled LPG

consumption to a record high of 1.84 million mt in March, up more than 14% year on year, leading analysts to believe that growth is expected to hover close to double-digit levels as New Delhi intensifi es its push towards cleaner fuels.

In its drive towards making 2016 the “year of LPG consumers,” India’s BJP-led government has set an ambitious target to open 10,000 new LPG dealerships across the country this year, in addition to the 16,000 that already exist.

New Delhi also has ambitious plans to provide additional subsidies to create 50 million new connections among lower-income families, with another15 million being added this year.

With LPG domestic demand growing at a much faster rate than output, the country, where refi ners fi nd it more profi table to focus on middle distillates rather than boosting LPG output, will be increasingly dependent on imports to meet its incremental consumption growth.

Petchems powers ahead

Domestic demand for naphtha witnessed the sharpest growth among all oil products in 2015, and is set to increase further in the coming years as India pushes forward to become a manufacturing hub.

Naphtha consumption, which accounts for about 7% of the country’s overall oil products demand, surged more than 18% in 2015 to 12.96 million mt, surpassing the growth rate of 15% seen for gasoline in 2015. In the fi rst half of 2016, naphtha demand rose 11% to 6.94 million mt.

24 Platts Insight Autumn 2016

Consumption of naphtha has been rising because of increased appetitefor its use as a gasoline-blendingstock, surging demand from the petrochemicals sector and pockets of demand from the fertilizer sector.

In addition, changing lifestyles promoting hygiene and packaging alongside infrastructure growth promoting smart city programs could take petrochemicals growth abovethe current GDP growth rate. This will support naphtha consumption in abig way.

But despite this, India is expected to remain a net naphtha exporter over the next four to fi ve years as expansion plans in the pipeline can only absorb a part of the surplus the country is currently producing.

“While the bulk of the growth in Indian oil demand so far has been in the transportation and power sectors,an important aspect for oil products demand going forward could be the potential change to industrial fuel demand,” the Oxford Institutestudy said.

When other key Asian consumers, like China, are witnessing a slowdown, India’s galloping growth certainly offers a ray of hope.

And there is every reason to remain optimistic about the Indian growth story which is just starting to take off – but it is ultimately dependent on the continuation of the strong government policy initiatives that have been launched, for a happy ending.

India Demand

©shutterstock/monotoomono

Shipping

26 Platts Insight Autumn 2016

Global tanker market set for stormy watersBoom times led to a ship-shopping spree – but excess tonnage may outstrip demand

The global tanker market had a sort of dream run in 2015 with freight rates offering handsome returns to ship owners. Come

2016, the tanker market is on the cusp of a marked change in fortune.

When the market is good, ship owners tend to get overambitious and excitable and end up placing orders for new ships. This in turn skews the supply dynamics and causes massive tonnage overhang in the market.

The market is expecting a storm toward the end of the year. The modest increase in global demand to move oil – or provide fl oating storage – will not be able to soak up the tonnage.

“It is likely to be a bit of a bumpy ride for the rest of the year and early 2017 as the order book for both crude and product tankers gets delivered,” said Erik Nikolai Stavseth, a Norway-based shipping analyst with Arctic Securities.

The order book deliveries are not evenly spaced out over several years and this implies that there will be a surge in deliveries in the near-term that willadd to the downward pressure onfreight rates.

More than half of the crude tanker order book is due for delivery over the next 12 months and will likely outstrip demand for a period of time, Stavseth said.

It is not surprising to see why shipping companies took the plunge and went on a ship-shopping spree. Daily earnings on the key Persian Gulf-to-Japan route for VLCCs briefl y reached above $100,000 late last year. As the earnings were moving northwards over the last two years, orders for construction and purchase of new ships poured in but deliveries always come with a lag. Now as ships are fi nally being delivered, VLCC earnings for the same route have plunged, estimated at around $17,000/day and analysts say they are yet to bottom out.

The growth in demand to move oil and oil products has not kept pace with the incremental new buildings. Expansion in crude supply from OPEC members is expected to slow down from 0.8-0.9 million b/d this year to 0.4-0.5 million b/d next year.

Crude export sales in Latin America and West Africa are in decline; in recent years, the tankers market benefi ted from longer voyages from the Caribbean and West Africa to North Asia.

Sameer Mohindru

Senior Editor,

Asia Shipping,

S&P Global Platts

Shipping

Autumn 2016 Platts Insight 27

Longer voyages keep ships occupied for an extended duration, thereby tightening the tonnage supply. Not any more. Analysts point toward cash-crunched Venezuela where drilling activity is at historical lows. Idle ships from Latin America are ballasting to West Africa in search of cargoes.

“This is creating a ripple effect of oversupply over the broader seaborne trade,” Morgan Stanley said in a report in July.

While the existing fl eet is struggling to fi nd business, the new ship buildings have been ordered.

An additional 1 million b/d of crude trade typically translates into incremental demand for 30-35 VLCCs, which can load cargoes of up to 2 million mt each. However, the supply is expected to increase by at least 45 VLCCs this year and another 35 VLCCs in 2017. The corresponding increase in supply over the last three years was around 13-15 VLCCs annually, according to industry estimates.

If most of the order book gets delivered, and the world continues to have near-zero demolition, the crude tanker fl eet could expand by as much as 8% in deadweight ton terms this year, these estimates show.

Interestingly, the order book is being fi nanced by export credits or by companies who have access to the capital market and so the normalbanking market, which bore the brunt of the ongoing global recession, has only been a marginal contributor to this boom in new buildings, said Dagfi nn Lunde, Chairman of Executive Ship Management, or ESM, and a Netherlands-basedshipping consultant.

“Unfortunately, ship owners have a talent for shooting themselves in the foot,” said Ralph Leszczynski, research director at Bancosta, an Italian shipping brokerage and consultancy.

The second half of this year andlikely most of 2017 will probablybe disappointing for VLCC owners,who will need to weather a storm, Leszczynski said.

In 2014 and 2015, trade fl ows for crude increased because importers rushed to

take advantage of lower prices. However, now with storage tanks full in many locations, importers have cut down on buying, in line with their refi ning requirements. And while crude prices are drastically lower than the $100-plus/b that seemed the norm even two years ago, they’ve recovered signifi cantly from the mid-$20s lows seen in January, eroding the incentive to buy more volumes.

“The tanker party seems to be over for now as global stock building of oil is

DIRTY TANKER FLEET SIZE

Sources: Arctic Securities

0

100

200

300

400

500

2018e2017e2016e2015201420132012

(million deadweight)

VLCC

Suezmax

Aframax

Other

DIRTY TANKER FLEET NEW DELIVERIES

Sources: Arctic Securities*For 2016 the vessel count is for already delivered and scheduled deliveries whereas 2017 and 2018 are projections

0

30

60

90

120

150

180

2018e2017e2016e2015201420132012201120102009

(number of vessels)

Aframax

Suezmax

VLCC

28 Platts Insight Autumn 2016

tapering off,” said Jarle Hammer, a Norway-based veteran shipping researcher and consultant. The total global commercial stocks of oil and oil products are close to 6 billion barrels which is equivalent to more than two months of demand, he said. In addition, there are also strategic reserves in various countries as well as crude and refi ned products in sea transit that account for volumes equivalent to a month of demand, said Hammer, who is also a lecturer in maritime economics.

Chartering ships to store crude was another avenue of demand in recent years, which has tapered off signifi cantly.

“Trading activity declined as contango in crude prices has disappeared,”Fotis Giannakoulis, a New York-based shipping analyst with MorganStanley said.

When crude prices are in contango, traders make purchases from the physical market and use ships to store it for sales in subsequent months. During backwardation, traders buy futures contracts from derivatives market and there is no incremental demand for ships. Instead, the market draws down on inventories. Hammer said currently less than two days’ worth of global demand for oil and oil products is on fl oating storage.

“It is illogical to expect the volumes of trade that we saw last year to continue forever,” said Leszczynski.

Problem of plentyfor product tankersThe supply pressure that we see in crude tankers is manifesting itself in product tankers as well, where the fl eet grew by 7% last year and is projected to

grow by another 8% in 2016. Deliveries and fl eet growth have already begun to spike in 2015 with close to 10 million dwt of deliveries compared with just 7 million dwt in 2014 and 6 million dwt in 2013. Another 14 million dwt of deliveries are either done or scheduled to take place during the rest of this year, according to industry estimates.

“There is a strong link between the two markets. It is rare to have a crude tankers’ market on fi re when product tankers’ rates are low and vice versa,” Arctic Securities’ Stavseth said.

Daily earnings from a Long Range I product tanker that typically carries around 55,000 mt cargoes on theMiddle East to East Asia routes are currently around $12,000/day, down 70% year-on-year.

In the last two years, refi neries in China, the Middle East and India pushed up their capacity utilization to take advantage of lower crude prices.

Europe’s naphtha exports to Northand Southeast Asia are expected to decline by close to 50% this year

CLEAN TANKER FLEET NEW DELIVERIES*

Sources: Arctic Securities*For 2016 the vessel count is for already delivered and scheduled deliveries whereas 2017 and 2018 are projections

0

40

80

120

160

2018e2017e2016e2015201420132012201120102009

(number of vessels) LR 2 LR 1 MR Handy

EXISTING FLEET AND ORDERBOOK

Sources: Arctic Securities

0

300

600

900

1200

1500

1800

HandyMRLR 1LR 2AframaxSuezmaxVLCC

(number of vessels) Existing fleet Orderbook

Shipping

Autumn 2016 Platts Insight 29

due to poor demand and lack of price competitiveness, according to market estimates. China is struggling to sell off its surplus gasoil and gasoline and even trying to send shipments to the Americas. Europe is fl ush with gasoil, hitting cargo movement prospects from the Middle East refi neries. The US is likely to move more cargoes of cheaper LPG, which is an alternative feedstock for petrochemical plants, via a widened Panama Canal and thus hitting demand for products tankers which move naphtha.

“High products inventories and low refi nery runs have kept chartering activity at low levels intensifying the seasonal weakness in rates,” the Morgan Stanley report said.

An interesting aside to these developments is that should the downside in the market continue as is expected, “Some companies will be squeezed to sell off their ships giving a fi llip to the second-hand tankers sales market though it may not happen quickly,” said Dagmar’s Lunde.

Sunny days again forthe tanker market?

And yet… further out, the outlook for the tankers market gives some grounds for optimism. For once, the order book for deliveries is not large in the near term and when they are complete, rates are expected to bottom out.

“Contracting activity for more ships is now fairly modest,” said Hammer. Echoing the same sentiment, Bancosta’s Leszczynski said, “It is expected to be smoother sailing again for owners from 2018 onwards as fortunately we are seeing very few new newbuilding orders now and there are quite a number of older units which are approaching an age where they will fi nd very diffi cult to get approvals for trade.”

From the costs side, sharply lower bunker prices have provided a tremendous cushion and ensured that the fall in freight rates does not dent owners’ earnings as much as was the case two years ago. This also explains relatively higher returns for ship owners

currently compared with earlier years, when bunker prices were expensive.The 380 CST grade bunker price on a delivered basis in Singapore was at $209.50/mt as of August 3 compared with $270/mt a year earlier and $606/mt two years ago, according to S&P Global Platts data.

Analysts are also optimisticabout the prospects of a revivalin product tankers.

The large volumes of crude in storage near refi ning facilities will need to be processed sooner or later. The general trend is of refi ning capacity to be built in the Middle East, India and China, away from many other end-users of middle distillate products such as Australia, West Africa and Latin America, where refi ning capacities are scarce, uncompetitive and closing down. This will add to demand for longer voyages and thereby help absorb part of the expanded fl eet, arguably justifying some of the shopping spree that owners have been indulging in.

©shutterstock/Oleksandr Kalinichenko

Shipping

Product Focus

Aviation spending analysisAirlines look to streamline competitive fuel spending and risks in a low-cost environment

In a relatively low-price fuel environment, many in the aviation industry are looking to capture the best buying opportunities and manage risk competitively. Followinga substantial period of hedging losses, airlines are now carefully looking ahead to consider the most effi cientoptions for buying and hedging in order to best weatherfuture volatility.

The gains made by airlines that were not heavily hedgedhave now largely been realized. The challenge airlines are currently facing is to plan ahead, managing risk and costs now the majority of airlines are exposed to the benefi ts of cheaper jet fuel.

In turn, airlines will need to watch as Asian oil markets continue to evolve and adapt to the rebalancing of crude

and refi ned product markets. Chinese refi ners in particular are changing dynamics as more and more barrels of jet fuel are being exported alongside Chinese airlines expandinginto international markets.

In light of this changing landscape, Platts has beenworking collaboratively with the aviation industry tobetter understand its needs and deliver a solution that provides essential market intelligence by combining its benchmark assessments, market and fundamentalinsights, and analytics.

Through the collaboration of more than 30 airlines, air freight and jet fuel distributors, the Platts Jet Fuel Dashboard curates the most important data and information, providing a tool to quickly understand the essential intelligence Platts offers. The result is a tool which allows customers to:

• Quickly identify historical trends • Watch the market evolve throughout the day • Anticipate buying/selling opportunities in the future

Aviation clients currently beta-testing the Jet Fuel Dashboard appreciate the ability to quickly review trendsand developments in the market to identify purchasing opportunities, evaluate contract pricing and manage risk.

Transforming the way the industry engages with Platts data, information and analysis, Platts is working to integrate the insights it provides to help clients identify opportunities, whether that is by monitoring and projecting shifts in global trade fl ows (cFlow), anticipating crude oil product economics (Platts Well Economics Analyzer) or analyzing patters in jet fuel markets (Platts Jet Fuel Dashboard).

30 Platts Insight Autumn 2016

Looking fora clear picture of China’s oil supply and demand?Platts China Oil Analytics covers all the analysis, news, and data relating to China’s oil balance. Its in-depth reports and insights, delivered by our team of analysts, gives you a winning edge and the short and medium-term forecasts can help you develop robust strategies. And all that comes in a single online intuitive analytical tool.

An exclusive interactive refi nery map enables you to look at a macro view, or focus on agranular perspective – capturing everything from import and export volumes to refi nerycapacities and turnaround. You can quickly drill down to the information that’s relevantto you and access our extensive historical database. Packed with supply and demand data from well-respected regional and national named sources, you can download and integrate it into your models to compare our data with yours.

Get a truly informed picture of the factors affecting China’s Oil balance.

For more information visit www.platts.com/products/china-oil-analytics

Platts China Oil Analytics

www.platts.com

ANALYTICSANALYTICS

©shutterstock/Sergii Tverdokhlibov

US Crude Exports

Autumn 2016 Platts Insight 33

US crude migration

in a holding patternThe US export ban has been lifted – but who actually wants the oil and what will they pay?

Think of the fi rst months of the lifting of the US ban on exporting crude oil as resembling online dating, but

with a bit more money at stake.

When the US Congress, seemingly outof the blue, approved the export of US crude oil in late 2015, it caught the industry by surprise. Companies and industry groups for years had been pushing for lifting the ban, imposed in 1975 in the wake of the fi rst oil crisis. But calling the pace of change in the US Congress “glacial” would be an insult to the speed of glaciers – yet suddenly, there it was: the end of the export ban,a compromise between the Obama administration and the Republican-controlled Congress as part of a broader deal on taxes and spending. As the Wall Street Journal noted, the end to the ban would have been considered “unthinkable” just a few months earlier.

And then the question faced oil producers: who is going to buythis oil and at what price?

The raw numbers so far don’t tell much of a story. Monthly fi gures, released by the Energy Information Administration

two months after the fact, showed US crude exports in April were 591,000 b/d and then 662,000 b/d in May. The latter fi gure is the highest ever, and it wasn’t just a stampede of oil headed to Canada, where as long as they met certain conditions, exports had never been banned. The May total of 308,000 b/d to Canada was a little on the low side compared with recent trends.

But the May report did show the evidence of deals rumored in themarket months ago, to Curacao (2 million barrels), the Dutch refi ning centers (3.4 million barrels) and a number of other European countries, such as 1.1 million barrels to the UK. China took a half million barrels in May. Reportedly, the grade was Poseidon, an offshore Louisiana Gulf Coast crude.

That is a small slice of data. In the actual market, S&P Global Platts market reporters are fi nding a fair number of deals but nothing thatcould yet be called a pattern. It’sonline dating again: testing out a number of possible opportunitiesbut fear of making a commitment.

Some of the deals that have been done

John Kingston

Director,

S&P Global

34 Platts Insight Autumn 2016

show the creativity of global oil traders. For example, while most of the trades have been done on a FOB Gulf Coast basis, the trading fi rm of Gunvor bought a cargo to be delivered into the Caribbean side of the pipeline that runs across the Panama Canal, in essence giving it maximum fl exibility to put it through to the other side of the canal or ship it somewhere on the eastern side of that route.

Other sales have run the gamut. A quantity of DSW – domestic sweet, the blend that comes out of the delivery point of Cushing, Oklahoma – was bid into a PetroPeru tender. (It didn’t win, but PetroPeru gave it a long look). Trade sources were reporting months ago that Latin American countries were taking cargoes, and the evidence of that started showing up in the May data: Colombia for a half-million barrels, and Peru for 330,000 barrels.

One ironic trade: Alaskan North Slope crude reportedly has been sold to Japan. In the ’90s, BP spent plenty of time and money lobbying for a change in the regulations to allow the export of ANS to Asia. The idea was that crude

moving on a foreign-fl agged vessel to Asia made more economic sense than putting it on a more expensive Jones Act ship to California (and into the early ’90s, the US Gulf Coast). When that permission was fi nally granted, sales of ANS, mostly to Taiwan, had their online dating period…and promptly fl opped. (Data shows a brief spike of US crude exports to Asia for a few months in the fi rst half of 1999). Why it would work now when it didn’t then is unclear, but there simply isn’t the ANS production anymore (1.1 million b/d then vs. less than 500,000 b/d now) to make this a signifi cant stream, even if the economics work.

Will those economics work for other US crude grades? In a report being prepared for Platts Analytics, Al Troner, long-time industry observer and President of Asia Pacifi c Energy Consulting, notes several other key factors that he says contributes to forecasting “modest expectations” of US crude exports. The tight spread between Brent and WTI – which opened up 2014 at more than $12 and was about $3 at the end of the year, and has been consistently less than $2 for most

of 2016 – discourages exports. Buying crude at a WTI-related price and selling into a Brent-linked market would have been easy when that spread reached $27, as it did by autumn 2011. But with crude-by-rail and numerous pipeline projects having fl attened that spread, the slam dunk arbitrage of a few years ago – albeit one that couldn’t legally be traded – is long gone. Traders will need to pick their opportunities when they fi nd them, and they might not necessarily be obvious.

And what of condensates, the fi rst break in the wall against the long-time ban on US crude oil exports? A Commerce Department decision in June 2014 to allow the export of processed condensate – a fi nding which concluded that processed condensate was essentially a refi ned product, not crude – helped lead to a signifi cant jump in condensate exports from the port of Corpus Christi, not far from the condensate-rich fi elds of the Eagle Ford shale. Full-year data shows the Corpus Christi port exported 2.6 million mt of condensate for all of 2014, but at the halfway point this year was on track only to export 2.3 million mt. Still, that would be more than the 2.1 million tons exported last year.

Still, too much focus on the ending of the US crude ban tends to obscure the fact that the shale revolution that led to the opening of US crude exports continues to provide an enormous level of exports of other products. Crude may be getting all the attention, but the biggest exports are being racked up in other products, which were never banned.

LPG exports are at the top of that list. US LPG exports rose to a record 1.139 million b/d in May, the third month this year that they had topped the 1 million

US CRUDE OIL EXPORTS

Sources: EIA

2013 2014 2015 20160

100

200

300

400

500

600

700(’000 b/d)

US Crude Exports

Autumn 2016 Platts Insight 35

b/d mark. China, Japan and Latin America were the largest destinations. Three years ago – to take a snapshot comparison – US LPG exports in April 2013 stood at 310,000 b/d. Ten years ago, they were fewer than 100,000 b/d.

LPG exports took another signifi cant step forward in early August whenthe fi rst ethane cargo was scheduledto be shipped out of the Gulf Coast.The US is long on ethane – one of the only countries in the world with that distinction – which has led to a

signifi cant decline in its price relativeto other feedstocks used to make propylene, such as naphtha. The US surplus in ethane effectively became stranded, because exporting it traditionally has been seen as problematic; it needs to be chilled, not to the temperatures needed for LNG but still in a process that adds costs. (The surplus would get consumed by leaving it in the natural gas stream, known as ethane rejection, so it was burned for its BTUs rather than cracked for its feedstock value). But Sunoco Logistic’s

Marcus Hook facility near Philadelphia exported its fi rst ethane in March, and Enterprise Product Partners, at its new facility in Morgan Point, Texas, is joining Sunoco Logistics with its 200,000 b/d ethane export terminal on the Gulf Coast.

US refi ned products exports have continued to soar, not slowed at all by reduced US crude production. Flip through an Energy Information Administration table of refi nery operating rates, and you’ll fi nd that for the last few years, refi nery utilization month-by-month has for the most part been steadily at a higher level than in the corresponding month a year earlier. And some of that push has been needed to supply growing US gasoline demand, which – depending on what data stream you look at – appears to be running anywhere from 2% to 3% more than a year earlier.

EIA data shows US gasoline exports have been solidly above 500,000 b/d since the end of last year, with a record surge to 722,000 b/d in February. Distillate exports are consistently running at more than 1.2 million b/d, a level that is down slightly from the record-breaking levels of late 2013, but is still among the highest months ever recorded. Overall, fi nished petroleum product exports from the US in the fi rst months of this year continued to hover just under the 3 million b/d level, not far from the record months, reached a few times, where product exports crossed the 3.1 million b/d mark. Exports in May once again broke through the 3 million b/d mark.

When the elimination of the crude oil ban was agreed upon at the end of 2015, it was only the fi rst of two steps that occurred in rapid succession that drove home to world energy markets the

US LPG EXPORTS

Sources: EIA

2013 2014 2015 20160

200

400

600

800

1000

1200(’000 b/d)

US TOTAL PETROLEUM NET IMPORTS

Sources: EIA

2004 2006 2008 2010 2012 2014 20160

2

4

6

8

10

12

14(million b/d)

US Crude Exports

36 Platts Insight Autumn 2016

changing role of the US in hydrocarbon trade. That’s because at the end of February, the US – or more specifi cally, Cheniere Energy – shipped out the fi rst cargo of LNG from the Gulf of Mexico. (It wasn’t the fi rst LNG export from the US; LNG has been shipped out of ConocoPhillips’ Kenai Peninsula in Alaska for many years and resumed in 2015 after a yearlong shutdown).

But there was one other cargo after that list was compiled, signifi cant because of where it was going – somewhere in Asia, destination unclear at press time – and how it got there. When the Shell-controlled Maran Gas Apollonia left the Gulf Coast on July 19, it headed to Asia through the expanded Panama Canal, the fi rst LNG carrier to make the passage through there. LNG tankers were too large to fi t through the canal before its expansion.

The exports that have fl owed out of the US so far have come solely from Cheniere’s terminal, though approval has been granted to other terminals.

But in late July, the tough market conditions that any potential exporters face claimed a victim when Shell said it would hold off on a fi nal investment decision for its approved LNG export facility in Lake Charles, Louisiana. It was the second time that Shell took such a decision that month; just a few weeks earlier, Shell put on hold a decision on its Canadian West Coast LNG project in Kitimat, BC.

Just like the narrowing of the Brent/WTI spread, the tighter gap between North American natural gas prices and the global price of LNG looms as a factor in many of these decisions. As noted, WTI exports looked like they’d be tremendously profi table when Brent/WTI was at $27 – even if nobody thought that spread was going to stay there, where it was going to settle as a new norm could still have been a spur to profi table exports. Similarly, the gap between Henry Hub and the Platts Asian-based JKM marker, at the start of 2014, was about $14-$15/Mcf. By this spring, it was less than $2.50 (though it

has risen recently). The easy profi ts of a $14 spread mostly disappear with that kind of movement. The list of approved export projects is almost certainly longer than the list of those that will actually operate.