southern copper corporation highlights · metal market copper molybdenum • 92% of world reserves...

TRANSCRIPT

Southern Copper Corporation HighlightsSouthern Copper Corporation Highlights

Southern Copper Corporation Highlights

January 2009January 2009

0

Safe Harbor Statement

This presentation contains ‘‘forward-looking statements,’’ as defined by federalsecurities laws, with respect to our financial condition, results of operations andbusiness, and our expectations or beliefs concerning future events. Thesestatements include words such as, but not limited to, ‘‘expect,’’ ‘‘anticipate,’’‘‘believe,’’ ‘‘intend,’’ ‘‘plan,’’ ‘‘seek,’’ ‘‘forecast,’’ ‘‘estimate,’’ ‘‘continue,’’ ‘‘may,’’believe, intend, plan, seek, forecast, estimate, continue, may,‘‘will,’’ ‘‘would,’’ ‘‘could,’’ ‘‘likely,’’ and similar expressions. These forward-lookingstatements reflect management’s current expectations and assumptions regardingf t t d ti d fi i l f d b d tlfuture events and operating and financial performance and are based on currentlyavailable information. However, actual results are subject to risks anduncertainties, which could cause actual results to differ materially from thosecontained in the forward-looking statements.

Many risks and uncertainties are inherent in the copper industry. Others are moreMany risks and uncertainties are inherent in the copper industry. Others are morespecific to our operations. Additional information about risks and uncertainties thatcould affect our future results are contained in our SEC filings, including our

t F 8 K 10 Q d 10 K d i t ti t t t F S 3

1

reports on Forms 8-K, 10-Q, and 10-K and a registration statement on Form S-3relating to our proposed public offering of common stock.

I. Introduction

2

Management Presenters

Presenters TitlePresentersRaúl Jacob

TitleManager of Financial Planning & IR

3

Corporate Structure

79.1%

20 9%

Public Float

20.9%

99.29 % 99.95 %

SCC Peru Branch Minera México

4

Metal Market

MolybdenumCopper

• 92% of world reserves and productioncapacity are concentrated in: Mexico, Peru,USA, China, and Chile.

• Slowdown in demand due to concernsabout industrial production.

• Supply constraints and cash cost• Demand largely driven by special steelalloys consumption.

pp yincreases.

• Strong long-term fundamentals fromBRIC’s and N-11.BRIC s and N 11.

Molybdenum PricesLME CopperCash Price vs. Inventories

1,000,000.00 $4.50

600,000.00

700,000.00

800,000.00

900,000.00

$2.50

$3.00

$3.50

$4.00

$15$20$25$30$35$40$45

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

$0.50

$1.00

$1.50

$2.00

$0$5

$1020

00/0

1/07

2001

/01/

07

2002

/01/

07

2003

/01/

07

2004

/01/

07

2005

/01/

07

2006

/01/

07

2007

/01/

07

2008

/01/

07

5

-

,

$0.00

01/0

5/00

04/0

4/00

07/1

1/00

10/0

9/00

01/0

9/01

04/0

9/01

07/1

2/01

10/1

6/01

01/2

2/02

04/2

2/02

07/2

4/02

10/2

1/02

01/2

3/03

04/2

3/03

07/2

2/03

10/1

7/03

01/2

1/04

04/2

0/04

07/2

0/04

10/1

5/04

01/2

1/05

04/2

5/05

07/2

5/05

10/2

1/05

01/2

4/06

04/2

5/06

07/2

5/06

10/2

0/06

01/2

3/07

04/2

4/07

07/2

4/07

10/2

2/07

01/2

2/08

04/2

2/08

07/2

3/08

10/2

1/08

3 month price US$ per ton Registered inventories in tons

2 2 2 2 2 2 2 2 2

FOB North America price US$ per lb

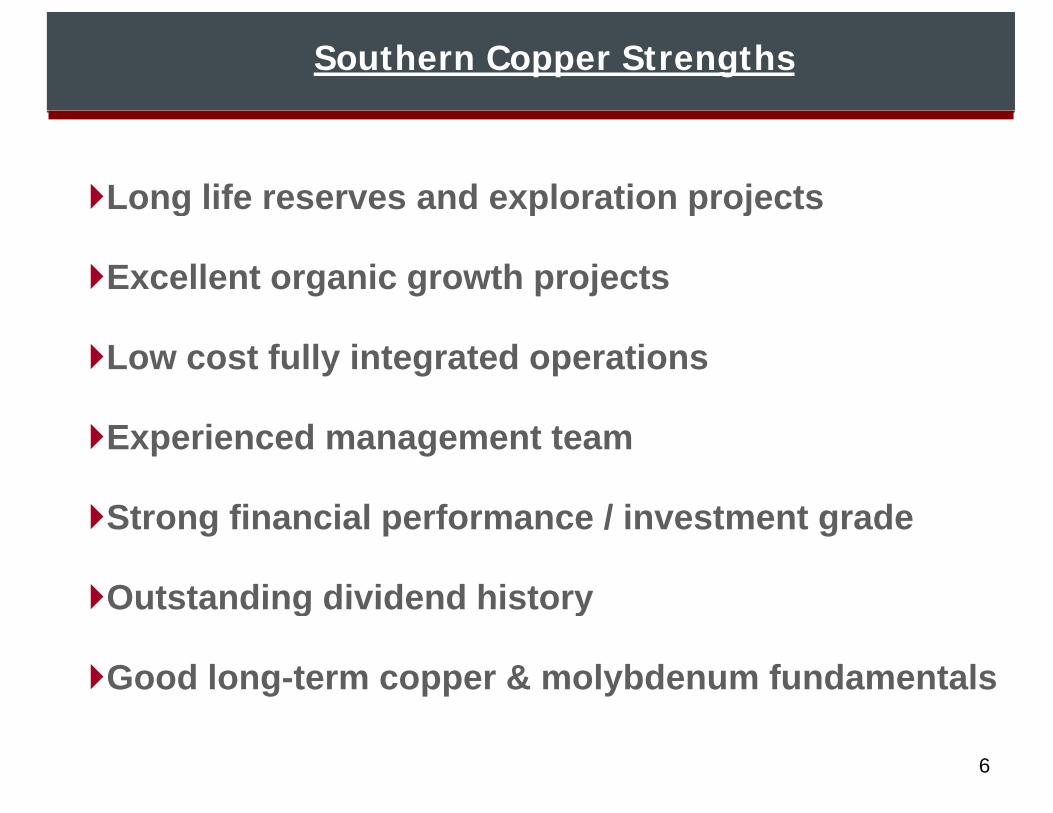

Southern Copper Strengths

Long life reserves and exploration projectso g e ese es a d e p o at o p ojects

Excellent organic growth projects

Low cost fully integrated operations

Experienced management team

St fi i l f / i t t dStrong financial performance / investment grade

Outstanding dividend historyOutstanding dividend history

Good long-term copper & molybdenum fundamentals

6

II. Overview of Operations

7

Company Overview

MexicoCopper Reserves 1: 49.1 mmtFor December 2008 La CaridadCananeaFor December 2008

Copper Production: 489 ktSales: $ 4,851 M

Santa Barbara

Charcas

Santa Eulalia

El Arco

Buenavista

San Martin

Peru

EBITDA: $ 2,557 MCash Cost: $ 0.34 / lb. Taxco

San Luis PotosiAngangueo

e u

Mines

Key#2 copper company by reserves 2

#7 copper producer 3Smelters and Refineries

Projects

#7 copper producer #8 copper smelter 3

Tantahuatay

Ilo

Cuajone

Toquepala

Los ChancasTia Maria

Source: Company FilingsNotes: 1 Copper contained in reserves based on US$1.20 per pound of copper as of December 31, 2007

8

2 Based on available companies reports3 CRU

Long Life Reserves

First largest copper reserves of any publicly traded company

Long life reserves with strong capacity expansion plansLong-life reserves with strong capacity expansion plans

69 9

Main Copper Reserves SCC Copper Reserves

50.3 49.150

60

38.2

49.1

69.9

40

50

60

70

d in

rese

rves

(Mt)

42%

29%SEC

40.0

25.622.9

30

40

er R

eser

ves

(Mt)

0

10

20

30

Cop

per C

onta

ine

2006

200717.3 16.512.1 10.2

0

10

20

Cop

pe

00.90 1.20 2.664

Copper prices ($/lb)

Source Annual Rep. 10K 10K 20F Annual Rep. 20F Reserve Rep. Annual Rep. Annual Rep.

0

Cod

elco

SC

C

FCX

BH

P B

illito

n

Ang

loA

mer

ican

Rio

Tin

to

Xst

rata

CV

RD

-Inco

Ant

ofag

asta

9

Period 06/12/31 07/12/31 07/12/31 07/06/30 07/12/31 07/12/31 07/06/30 07/12/31 07/12/31Cu Price N/A $1.20 $1.20 $2.00 N/A $2.31 N/A N/A N/A

Low Cost Operations

Cash Costs per pound of Copper Produced Net of By-Products

Management focus on cost efficiency

Low Cost Drivers

0 6 Management focus on cost efficiencySignificant low cost SX-EW productionHigh quality reservesStrong by-product credits – 12M08:

0.44

0 18

0.340.4

0.6

/lb)

– molybdenum (16% of revenues) – zinc (4% of revenues)– silver (4% of revenues)– gold & others (3% of revenues)

0.18

0.03

0.16

-0.13

0

0.2

(US$

/

Cost Structure Operating Cash Cost per Pound of Copper Produced

gold & others (3% of revenues)– sulphuric acid (4% of revenues)

-0.22003 2004 2005 2006 2007 2008

pp

Operating Materials

16%

FuelMaintenance

Other12%

1.01

1.281.38

1.71

1.20

1.50

1.80

) Fuel12%

Energy31%

Labor14%

15%0.74 0.85

0.30

0.60

0.90

(US

$/lb

)

10As of December 31, 2008 As of December 31, 2008

0.002003 2004 2005 2006 2007 2008

Low Cost of Operations

SCC’s cash cost as per Brook Hunt estimates is in the bottom quartile of global copper producers

High quality reserves, large scale open-pit mines, low cost SX-EW production, strong by-products credits, and management focus on cost efficiency are among SCC’s key low cost drivers

Top 8 Lowest Cash Cost Copper Producers1 Top 10 Lowest Cash Cost Copper Minesites1,2

100 0

80.0

100.0

5.116.6 18.1 18.4

79.9

40.0

80.0

54 0 57 066.0

86.040.0

60.0

c/lb

)

(82 7)(62.9)

(29.9)(22.7)

(80.0)

(40.0)

0.0

(c/lb

)(2.0)

39.754.0 57.0

(10.8)(16 8)

0.0

20.0

(c

(174.5)

(145.3)

(82.7)

(200.0)

(160.0)

(120.0)

(16.8)

-40.0

-20.0

SCC

Anto

faga

sta

Rio

Tin

to

Cod

elco

BHP

Billit

on

Xstra

ta

Angl

oAm

eric

an

Free

port

Sier

rita

Bing

ham

Can

yon

Anta

min

a

La C

arid

ad

Los

Pela

mbr

es

Bagd

ad

Toqu

epal

a

Chu

quic

amat

a

Cua

jone

OK

Tedi

Can

anea

11

Source: Based on companies reportsNotes:1 Excludes minesites/facilities with annual Cu production less than 100 Mlbs. As of 12/31/07.2 Operating cost net of by-product credits

B

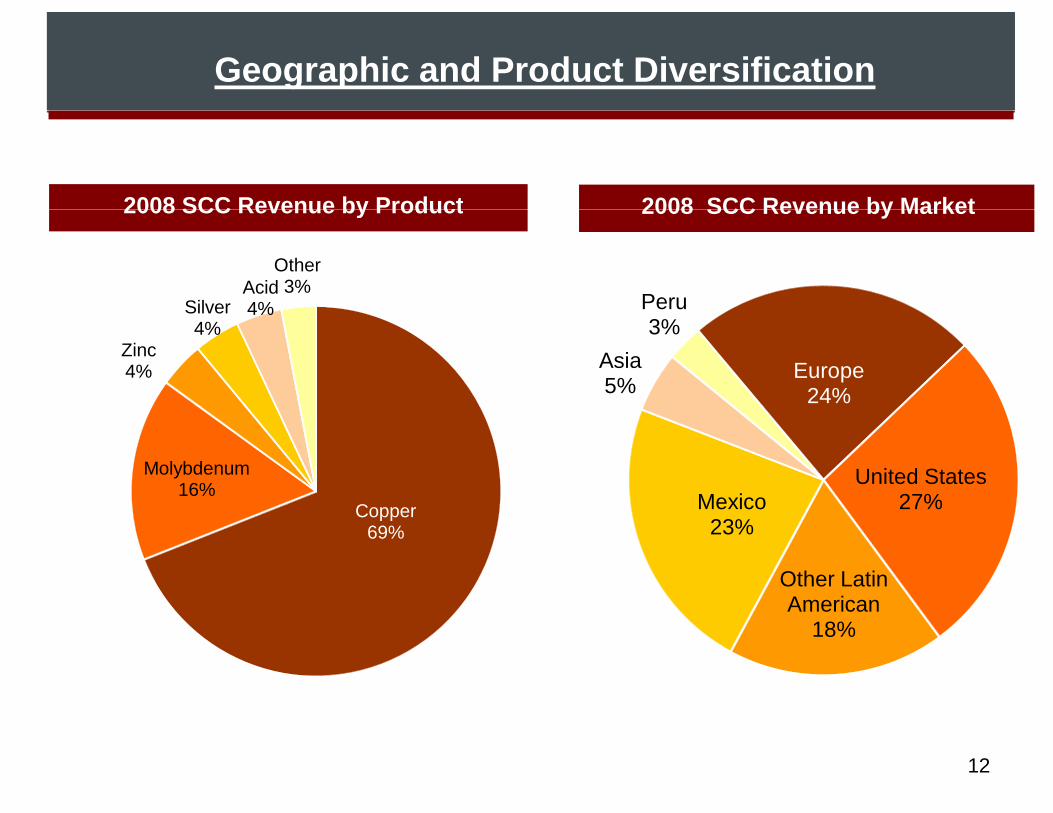

Geographic and Product Diversification

2008 SCC Revenue by Product 2008 SCC Revenue by Market2008 SCC Revenue by Product 2008 SCC Revenue by Market

SilverAcid 4%

Other 3%

Peru

Zinc 4%

Silver 4%

4%

Europe24%

Asia5%

Peru3%

Molybdenum19%

C

Molybdenum 16% United States

27%MexicoCopper 69%

27%

Other Latin American

Mexico23%

American18%

12

Expansion Projects

Tía María SX EW / Copper Ilo Metallurgical Operations ExpansionLBE for Operations: 4Q - 2010Annual Copper Production: 120 ktpyEstimated Capex: $934 M

LBE for Operations: 2012Additional Concentrates from Cuajone & Toquepala, 445 ktpyS lt i f 1 2 MTPY tToquepala Concentrator Expansion

LBE for Operations: 2011Annual Production: Copper = 100

Smelter expansion from 1.2 MTPY to 1.8 MTPYCopper Anode production: 325 ktpy to 490 ktpyktpy; Moly = 3.1 ktpy

Estimated Capex: $600 M

490 ktpyCopper Cathode production: From 280 ktpy to 360 ktpyEstimated Capex: $200 MCuajone Concentrator Expansion Estimated Capex: $200 M

LBE for Operations: 2012Annual Production: Copper = 50 ktpy Moly = 0.7 ktpy

j

y pyEstimated Capex: $374 M

Additi l C P d ti 270 kt C $2 1B13LBE : Last Best Estimate

Additional Copper Production : 270 ktpy; Capex : $2.1B

Tia Maria Project

Estimated Capex : US $934 M120,000 MT of copperSX EW Cathodes per yearLBE for Operations :

14

2010, for 18 years

Tia Maria: New Operating Unit Overview

Key Metals: Copper

SX EW Plant Capacity: 120 ktpy

Key Operating DataHighlightsLocated at 100 Km north of Ilo, PeruAnnual production of 120 ktpy of copper SX-EW Plant Capacity: 120 ktpyAnnual production of 120 ktpy of copperCash cost estimated at ¢ 70-80 per Lb

Life of mine : 18 years

ExpansionResource Information

Possible concentrator after 2021, when sulfide resources are reached

Resource: 2.5 MT of contained copper

Average Copper Grade: 0.39%

Stripping Ratio: 1.00x

15Source: SCCNote:(1) Reserves based on US$0.90 per pound of copper.

III. Financial Overview

16

SCC Financial Summary

(US$ MM) 2005 2006 2007 2008Copper Price (LME) US$ per pound 1.67 3.05 3.23 3.16Income Statement:Net Revenues $4,089 $5,460 $6,086 $4,851EBITDA 2,335 3,316 3,766 2,557EBITDA Margin 57% 61% 62% 53%Interest Expense 109 113 123 116Interest Expense 109 113 123 116Net Income 1,400 2,038 2,216 1,407Balance Sheet Statement:Cash & Equivalents $876 $1,023 $1,409 $717Total Assets 5,688 6,376 6,581 5,730Total Debt 1 1,172 1,528 1,450 1,290Total Liabilities 2,349 2,696 2,716 2,331Total Shareholders' Equity 3,326 3,667 3,848 3,385Cash Flow Statement:Capital Expenditures 2 $471 $456 $316 $517F C h Fl 3 1 193 1 604 2 388 1 204Free Cash Flow 3 1,193 1,604 2,388 1,204Key Credit RatiosNet Debt / EBITDA 0.1x 0.2x 0.01x 0.2xEBITDA / Interest Expense 21 4 29 3 30 6 22 0

17

EBITDA / Interest Expense 21.4 29.3 30.6 22.0

1 Includes short-term and long-term debt including current portion2 Includes capitalized stripping costs until 20053 Free Cash Flow defined as net cash from operating activities less capital expenditures

Solid Financial Performance

Among the highest EBITDA margins and strongest leverage ratios in the metals & mining industry

2007 EBITDA Margin (%) Net Debt/ 2007 EBITDA (x)2007 EBITDA Margin (%) / ( )

72%Antofagasta-0.7xAntofagasta

62%Southern Copper 0.01xSouthern Copper

46%

46%

Freeport

Anglo American

0.5x

0.4x

Anglo American

BHP Billiton

46%BHP Billiton

p

1.0x

0.7x

Xstrata

FCX

42%Rio Tinto2.7xCVRD - Inco

18Source: SCC; Company Reports

39%Xstrata 3.2xRio Tinto

Focus on Total Return to Investors

Current Dividend Yield1 (%) 3-Year Share Price Performance1 (%)

Disciplined approach to creating shareholder value

12.1%Southern Copper39% Southern Copper

7.4%

8.9%

Freeport

Antofagasta

14%

23%

Antofagasta

BHP Billiton

5.6%

6.8%

Anglo American

Rio Tinto

-36%

13%

Anglo American

CVRD

3.3%

4.6%

BHP Billiton

CVRDIn 2008, SCC paid

US$1.7 Billion

US$ 1.94 per share

-53%

-53%

Xstrata

Rio Tinto

0.0%

0 0% 2 0% 4 0% 6 0% 8 0% 10 0% 12 0% 14 0%

Xstrata -57%

-60% -40% -20% 0% 20% 40% 60%

Freeport

19

Source: Bloomberg; Company FilingsNote:1 Regular and special dividends declared over last twelve months by record date

divided by current share price as of December 31, 2008 (SCC = US$16.06)1 As of December 31, 2008

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 60% 40% 20% 0% 20% 40% 60%

Capital Expenditure Forecast (US$M)

$107

$199$1,200

$800

$1,000

$940

$1,200$600

$517$393

$780

$250$200

$400

$250$0

2008 2009E 2010E 2011E 2012E 2013E

20Source: SCC

SCC Debt Amortization Schedule

Millions of USD as of December 31, 2008

SCC is evaluating the best financing option for its projects.

$1,000

$56

$200

$0 $10 $10 $10 $10 $10$

2008 2009 2010 2011 2012 2013 2015 2028 2035

21

Mitsui Yankee Bonds 10 & 30 year Bonds

IV. Appendix

22

Estimated Production Capacity Growth

(Ktpy)1,579 1,579

1,3421,276

1,086

970 116

190

66

237

920820

120

50100

116

700

2008 Full CapacityProduction

2010 - Tía MaríaSX EW (120 ktpy

Cu)

2012 - ToquepalaConcentrator

Expansion (100ktpy Cu)

2012 - CuajoneConcentrator (33

ktpy Cu) + SX EW(17 ktpy Cu)

2014 - LosChancas SX EW

(100 ktpy Cu) 2011- Angangueo (16

ktpy Cu)

2014 - El Arco SXEW +

Concentrator (190ktpy Cu)

2014 - Cananea SXEW +

ConcentratorExpansion (66

ktpy Cu)

2016 - NewCananea

Concentrator (160ktpy Cu) 2013 -

Buena Vista Mine

2016 - TotalProduction

ktpy Cu) ktpy Cu) Buena Vista Mine(22 ktpy Cu)

1D 1D 2P 2P 2P 2P

2014 20162008

Stage

2010 - 2012

1D

23Source: SCC

Other Expansion Projects

El Arco (SX EW + Concentrator) Los Chancas (SX EW + Concentrator)

LBE for Operations: 2014Annual Copper Production: SX-EW = 35 ktpy; Conc.= 155 ktpy

LBE for Operations: 2014Annual Copper Production: SX-EW = 20 ktpy Conc = 80 ktpySX EW 35 ktpy; Conc. 155 ktpy

Annual Gold Production= 81 kozpyEstimated Capex: $1,800 M

SX EW 20 ktpy Conc. 80 ktpyAnnual Moly= 4.7 ktpyEstimated Capex: $1,200 M

LBE for Operations: 2014

Angangueo

Capacity 2000 tpd (Cu, Zn, Ag).Annual Copper Production: 16 ktpyEstimated Capex: $145 M

$24Source: SCC LBE : Last Best Estimate

Additional Copper Production : 306 ktpy; Capex : $1.9B

Operational Update - Cananea Minesite

Key Metals: Copper

Concentrator Capacity: 77 ktpd

Operating Statistics (2008) HighlightsLargest mine in MexicoFourth largest copper mine worldwide in Concentrator Capacity: 77 ktpd

SX-EW Plant Capacity: 55 ktpy

Copper Production: 16 kt

Fourth largest copper mine worldwide in terms of reserves (similar to Escondida)Recent LOM study shows operations th h 2070 U i d itthrough 2070 Unique deposit: no evidence of decline in ore grades at deeper stratas

Reserve Information (2007)

Reserves (1): 19.0 MT

ExpansionSeveral projects underway or planned to increase production to an estimated 66kt

Average Copper Grade:

Sulfide: 0.577%

Leachable Materials: 0.267%

per year:- SX-EW III 33 ktpy- Concentrator expansion 33 ktpy

Production (kt)

Stripping Ratio: 2.23x

p pyMolybdenum circuit, 4 ktpyPossible second expansion to increase capacity by an additional 160 ktpy

173 175 164 99

25

capacity by an additional 160 ktpySource: SCCNote:(1) Reserves based on US$1.20 per pound of copper.

99

162004 2005 2006 2007 2008

Operational Update - Caridad MinesiteOperating Statistics (2008)

Key Metals: Copper, Mo, Au, Ag

Concentrator Capacity: 90 ktpd

Highlights

p y p

SX-EW Plant Capacity: 22 ktpy

Copper Production: 119 kt

Molybdenum Production: 7 28 kt

Second largest mine in Mexico

Recent LOM study shows operations

through 2044Molybdenum Production: 7.28 kt

Increasing Mo grades with depth

potentially allows conversion of

operations to a copper equivalent mine

Reserve Information (2007)

Reserves (1): 5.2 MToperations to a copper equivalent mine

ExpansionP t ti l t i d

Average Copper Grade:

Sulfide: 0.348%

Leachable Materials: 0.161%Potential to increase copper and

molybdenum recoveries

Future moly plant expansion due to Production (kt)

Stripping Ratio: 1.73x

higher ore grade

132 144 125 119

26Source: SPCCNote:(1) Reserves based on US$1.20 per pound of copper.

69

2004 2005 2006 2007 2008

Operational Update - Cuajone MinesiteOperating Statistics (2008)

HighlightsKey Metals: Copper, Mo

Concentrator Capacity: 87 ktpdSecond largest copper mine in Peru

Leachable ore sent to Toquepala by

pipeline

Concentrator Capacity: 87 ktpd

Copper Production: 196kt

Molybdenum Production: 4.4 ktpipeline

LOM study shows expanded

operations through 2038

h l bd b d d

Reserve Information (2007)

Reserves (1): 9.1 MTAverage Copper Grade:

High molybdenum by-product credits

Expansion

g ppSulfide: 0.566%Leachable Materials: 0.584%

Stripping Ratio: 2.36xp

Concentrator expansion underway:

– Copper : +50 ktpy

M l bd 700 t

Production (kt)

– Molybdenum : +700 tpy194

164 174 182

196

27Source: SPCC(1) Reserves based on US$1.20 per pound of copper. Includes sulfur ore reserves

and in-pit leachable reserves.

2004 2005 2006 2007 2008

Operational Update - Toquepala Minesite

Key Metals: Copper, Mo

Concentrator Capacity: 60 ktpd

Highlights

Thi d l t i i P

Operating Statistics (2008)

Concentrator Capacity: 60 ktpd

SX-EW Plant Capacity: 56 ktpy

Copper Production: 153 kt

Third largest copper mine in Peru

LOM study shows expanded operations

through 2036Molybdenum Production: 4.7 ktHigh molybdenum by-product credits

Installation of crusher / conveyor

system for leachable ore in operation

Reserves Information (2007)

Reserves (1): 16.0 MTy p

Expansion

Average Copper Grade:Sulfide: 0.598%Leachable Materials: 0.195%

Concentrator & SX EW expansion

underway: Production (kt)

Stripping Ratio: 5.07x

– Copper : +100 ktpy

– Molybdenum : +3.1 ktpy

203 194 188 178 153

28Source: SPCC(1) Reserves based on US$1.20 per pound of copper. Includes sulfur ore reserves

and in-pit leachable reserves.

203 194 188 178 153

2004 2005 2006 2007 2008

Operational Update - Caridad Metallurgical Complex

Highlights

Consists of a smelter, electrolytic copper

Operating Statistics (2008)

Smelter capacity: 1,000 ktpy

refinery, precious metal refinery and a

copper rod plant

10th largest copper smelter worldwide

Anode capacity: 300 ktpy

Cathode production: 140 kt10th largest copper smelter worldwide

8th largest copper refinery worldwide

World-class facilities commissioned in

1997 09

Rod plant capacity: 150 ktpy

Copper rod production: 76 kt

1997-09

Plans for a 600 Megawatt coal-fired

Gold production: 666 kg

Silver production: 136 tons

Sulfuric acid production: 578 ktpower facility by 2012, to be built and

operated by an independent power

producer.

Sulfuric acid production: 578 kt

producer.

29

Operational Update - Ilo Metallurgical Complex

Operating Statistics (2008)

Smelter Capacity: 1,200 ktpy

Highlights

Consists of a smelter, anode plant, Smelter Capacity: 1,200 ktpy

Copper Anode Production(1): 307 kt

Cathode Capacity: 280 ktpy

electrolytic plant and precious metals

plant

6th largest copper smelter worldwideCathode Production: 249 kt

Silver Production: 92 tons

G ld P d ti 153 k

g pp

9th largest copper refinery worldwide

Record production in 2005

Long term power supply agreement Gold Production: 153 kgLong-term power supply agreement

with Enersur until 2017

Expansion

Ilo modernization completed in 1Q07

- 2¢/lb reduction in cash cost

Sulfuric acid production increased- Sulfuric acid production increased

from 0.35 to 1.1 million tons

Potential to further increase capacity

30

- Smelter: 1,800kt/y

- Refinery: 360kt/y(1) Blister production has been replaced by anode production as of January 2006.

SLP Metallurgical Complex: Overview

Operating Statistics (2008)Highlights

Assets consist of copper smelter and zinc Zinc refinery capacity: 105 ktpyrefinery

One of the most cost-efficient zinc refineries

in the world

Zinc refinery capacity: 105 ktpy

Zinc production: 107 kt

Copper concentrate f d itin the world

Expansion

feed capacity: 230 ktpy

Copper concentrate feed: 41 ktPossible 55kt/y expansion of the zinc

refinery underwayCopper blister production: 19 kt

31

Comparable Company AnalysisSouthern Copper Antofagasta Codelco Freeport

Data as of: LTM 12/31/2008 LTM 06/30/2008 12/31/2007 LTM 12/31/2008Current Rating Ba1 / BBB- / BB+ -- / -- / -- Aa3 / A / -- B1 / B+ / --

I St t tIncome StatementNet Revenues $4,851 $4,292 $16,988 $17,796EBIT 2,202 2,902 8,548 (12,710) EBIT Margin 45% 68% 50% -(71%)EBITDA $2,557 $2,986 $7,853 (11,202) EBITDA Margin 53% 70% 46% -(63%)Interest Expense $116 $16 $245 $584Net Income 1,407 2,232 2,982 (11,341)

Balance SheetCash & Equivalents $717 $2,349 $2,074 $872Total Assets 5,730 6,527 15,058 23,271 Total Debt 1,290 214 4,354 7,351 Net Debt 573 (2,135) 2,280 6,479 Total Liabilities 2,331 1,111 10,309 16,153 Minority Interest 14 1,018 3 1,328 Total Shareholders' Equity 3,385 5,416 4,744 5,790

Credit RatiosTotal Debt / EBITDA 0.5x 0.1x 0.6x (0.66x)N t D bt / EBITDA 0 20 (0 7) 0 3 (0 6)

32

Net Debt / EBITDA 0.20 (0.7) 0.3 (0.6) EBITDA / Interest Expense 22.0 186.6 32.1 (19.2)

Source: Companies filings

Summary of Reserves Data 1

The table below details SCC’s copper and molybdenum reserves as of December 31, 2007 Cuajone Toquepala Cananea La Caridad Total Immsa 2

Mineral Reserves (Peru) (Peru) (Mexico) (Mexico) Open-Pit Mines (Mexico)

Mineral Reserves

Metal Prices:

Copper ($/lb.) $1.20 $1.20 $1.20 $1.20 $1.20 $1.20

Molybdenum ($/lb.) $9.00 $9.00 $9.00 $9.00 $9.00 $9.00

Sulfide ore reserves (000's of tons) 1,594,589 1,940,206 2,511,484 932,191 6,978,470 40,781

Average Grade:

Copper 0.566% 0.598% 0.577% 0.348% 0.550% 0.490%

Molybdenum 0.020% 0.036% - 0.026% 0.028% -

Leachable Materials

R i t k (000' f t ) 20 701 940 502 704 587 513 291 2 179 081 Reserves in stock (000's of tons) 20,701 940,502 704,587 513,291 2,179,081 -

Average copper grade 0.482% 0.143% 0.127% 0.252% 0.167% -

In-pit reserves (000's of tons) 10,902 2,117,946 1,670,689 1,189,125 4,988,662 -

Average copper grade 0 584% 0 195% 0 267% 0 161% 0 212% - Average copper grade 0.584% 0.195% 0.267% 0.161% 0.212%

Total leachable reserves (000's of tons) 31,603 3,058,448 2,375,276 1,702,416 7,167,743 -

Average copper grade 0.517% 0.179% 0.225% 0.188% 0.198% -

Copper contained in ore reserves (000's of tons) 39,089 15,732 18,952 5,159 48,932 200

33

Source: SCCNotes:1 Reserves based on long-term price assumptions of US$1.20 per pound of copper and US$9.00 per pound of molybdenum.2 The Immsa Unit includes the Charcas, Santa Bárbara, San Martin, Santa Eulalia and Taxco mines. 3 Copper contained in ore reserves for open-pit mine is (I) the product of sulfide ore reserves and the average copper grade plus (ii) the product of in-pit leachable reserves

and the average grade of copper. Copper contained in ore reserves for underground mines is the product of sulfide ore reserves and the average copper grade.

pp ( ) 9,089 15,732 18,952 5,159 48,932 200

Debt Breakdown

US$ MM as of December 31, 2008 Type Maturity Amount Interest Rate

Yankee Bonds9.25% Senior Unsecured Bonds Unsecured 2028 / bullet $56 9.25%

Sub-total $56

Unsecured Notes6.375% Notes due 2015 1 Unsecured 2015 / bullet $200 6.375%7.50% Notes due 2035 1 Unsecured 2035 / bullet $1,000 7.50%

Sub-total $1,200

OtherS / $ O % %Mitsui bank credit agreement Secured 2013 / amortizing $50 LIBO + 1.250%=aprox. 3.57%

Sub-total $50

Total Debt $1,306

34Source: SCC1 At face value