southern charter entrepreneur school module 1

TRANSCRIPT

Entrepreneur Program

Investment planning 101

Investing in an Annuity

Presented by

Mark Thompson

Investment Planning 101

Investing in an Annuity for retirement income

Module Objective -

1) Understand and know your client fully, draft a balance sheet.

2) Establish and agree on your clients risk profile and financial needs,

3) More specifically his income requirement, is it reasonable?

4) Explain and agree on available annuity options in simple terms,

5) Explain and agree on the tax and investment strategy going forward,

6) Recommend the most cost effective investment platform that your

client trusts and is comfortable with.

7) Summarise your discussions and agreements in a written signed

proposal

Case study – John Retires

After meeting with the client we gain the following information:

– John had 30yrs service with last employer

– Offered consulting work

– Small bond on the house R35 500

– Small Debt on the car R12 325

– Married to Joy - who is a practicing private beautician

– Post retirement medical aid paid for by the company

– John loves sailing, Joy loves cooking in Italy!

– Available Pension Fund capital after tax free cash withdrawal of R 2 810 031

– John requires an income of R12 000pm

– Interest / Guaranteed rate 15%

Case Study - John Retires > Gaining further

information

To gain a further understanding of John‘s needs and potential risks

We do a SWOT analysis on our client, enquire and note;

• Strengths - Strong balance sheet? EG no debt, or debt?

ability to work and earn an income?

• Weakness - Health? Maybe overweight? Not fit? Enough income?

Extra drain on income?

• Opportunities - Has a skill which adds value? May work longer, travel? re-locate? Potential future income?

• Threats - Consider Inflation, political uncertainty, financial scams!

At this stage, what conclusions can you

draw about John? What type of guy is he?

Conservative risk averse? Or Risk taker?

Conclude and agree on income required

and risk profile.

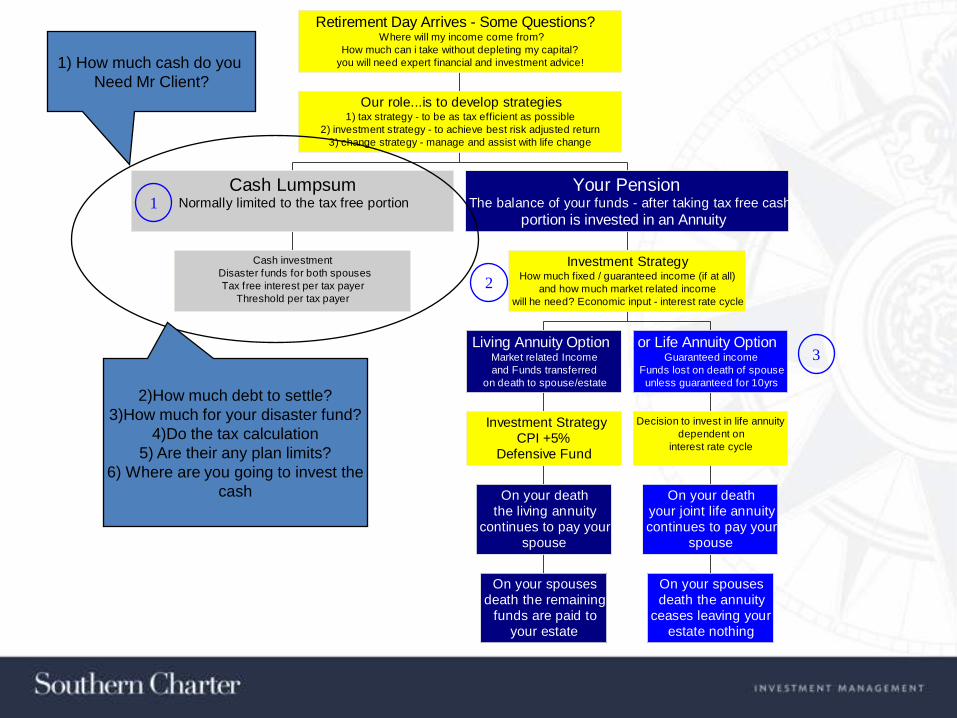

Cash investment

Disaster funds for both spouses

Tax free interest per tax payer

Threshold per tax payer

Cash LumpsumNormally limited to the tax free portion

On your spousesdeath the remaining

funds are paid toyour estate

On your deaththe living annuity

continues to pay yourspouse

Investment StrategyCPI +5%

Defensive Fund

Living Annuity OptionMarket related Income

and Funds transferred

on death to spouse/estate

On your spousesdeath the annuity

ceases leaving yourestate nothing

On your deathyour joint life annuitycontinues to pay your

spouse

Decision to invest in life annuity

dependent on

interest rate cycle

or Life Annuity OptionGuaranteed income

Funds lost on death of spouse

unless guaranteed for 10yrs

Investment StrategyHow much fixed / guaranteed income (if at all)

and how much market related income

will he need? Economic input - interest rate cycle

Your PensionThe balance of your funds - after taking tax free cash

portion is invested in an Annuity

Our role...is to develop strategies1) tax strategy - to be as tax efficient as possible

2) investment strategy - to achieve best risk adjusted return

3) change strategy - manage and assist with life change

Retirement Day Arrives - Some Questions?Where will my income come from?

How much can i take without depleting my capital?

you will need expert financial and investment advice!

1

2

3

At this stage you may wish

to take your client through

this schematic

Cash investment

Disaster funds for both spouses

Tax free interest per tax payer

Threshold per tax payer

Cash LumpsumNormally limited to the tax free portion

On your spousesdeath the remaining

funds are paid toyour estate

On your deaththe living annuity

continues to pay yourspouse

Investment StrategyCPI +5%

Defensive Fund

Living Annuity OptionMarket related Income

and Funds transferred

on death to spouse/estate

On your spousesdeath the annuity

ceases leaving yourestate nothing

On your deathyour joint life annuitycontinues to pay your

spouse

Decision to invest in life annuity

dependent on

interest rate cycle

or Life Annuity OptionGuaranteed income

Funds lost on death of spouse

unless guaranteed for 10yrs

Investment StrategyHow much fixed / guaranteed income (if at all)

and how much market related income

will he need? Economic input - interest rate cycle

Your PensionThe balance of your funds - after taking tax free cash

portion is invested in an Annuity

Our role...is to develop strategies1) tax strategy - to be as tax efficient as possible

2) investment strategy - to achieve best risk adjusted return

3) change strategy - manage and assist with life change

Retirement Day Arrives - Some Questions?Where will my income come from?

How much can i take without depleting my capital?

you will need expert financial and investment advice!

1

2

3

1) How much cash do you

Need Mr Client?

2)How much debt to settle?

3)How much for your disaster fund?

4)Do the tax calculation

5) Are their any plan limits?

6) Where are you going to invest the

cash

Retirement Funds - new retirement and death tables

Taxable income from lump sum benefits

Rate of Tax

0 - R315 000 0%

R315 001 - R630 000 R0 plus 18% of taxable income in excess of R315 000

R630 001 - R945 000 R56 700 plus 27% of taxable income in excess of R630 000

R945 001 R141 750 plus 36% of taxable income in excess of R945 000

Effective date - 1 March 2011

Note - Applies to involuntary retrenchment retirement benefits and severance benefits

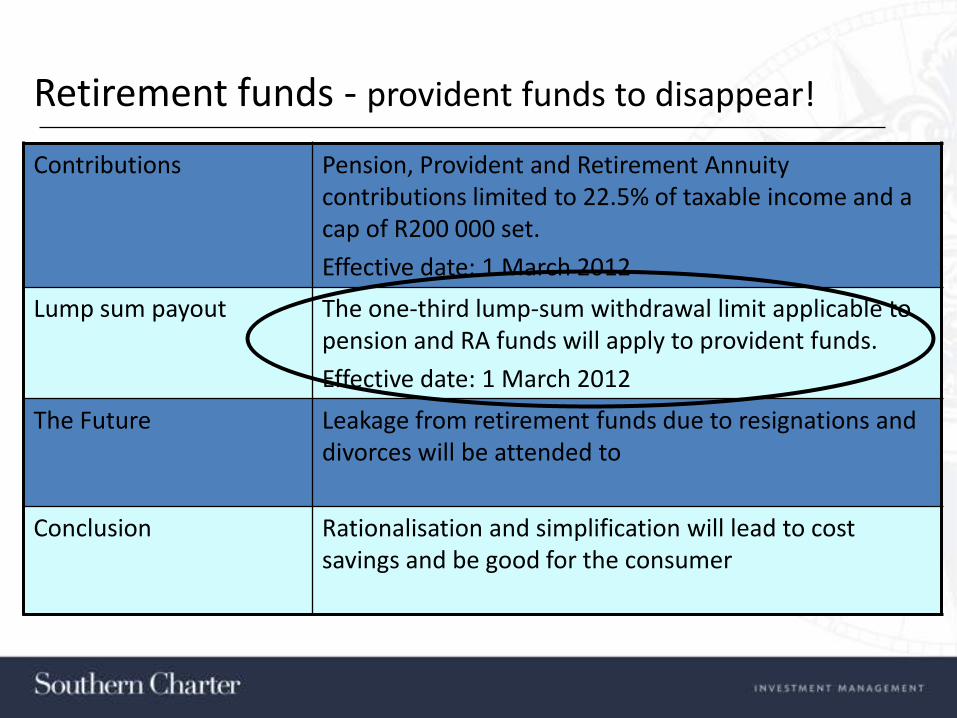

Retirement funds - provident funds to disappear!

Contributions Pension, Provident and Retirement Annuity contributions limited to 22.5% of taxable income and a cap of R200 000 set.

Effective date: 1 March 2012

Lump sum payout The one-third lump-sum withdrawal limit applicable to pension and RA funds will apply to provident funds.

Effective date: 1 March 2012

The Future Leakage from retirement funds due to resignations and divorces will be attended to

Conclusion Rationalisation and simplification will lead to cost savings and be good for the consumer

Cash investment

Disaster funds for both spouses

Tax free interest per tax payer

Threshold per tax payer

Cash LumpsumNormally limited to the tax free portion

On your spousesdeath the remaining

funds are paid toyour estate

On your deaththe living annuity

continues to pay yourspouse

Investment StrategyCPI +5%

Defensive Fund

Living Annuity OptionMarket related Income

and Funds transferred

on death to spouse/estate

On your spousesdeath the annuity

ceases leaving yourestate nothing

On your deathyour joint life annuitycontinues to pay your

spouse

Decision to invest in life annuity

dependent on

interest rate cycle

or Life Annuity OptionGuaranteed income

Funds lost on death of spouse

unless guaranteed for 10yrs

Investment StrategyHow much fixed / guaranteed income (if at all)

and how much market related income

will he need? Economic input - interest rate cycle

Your PensionThe balance of your funds - after taking tax free cash

portion is invested in an Annuity

Our role...is to develop strategies1) tax strategy - to be as tax efficient as possible

2) investment strategy - to achieve best risk adjusted return

3) change strategy - manage and assist with life change

Retirement Day Arrives - Some Questions?Where will my income come from?

How much can i take without depleting my capital?

you will need expert financial and investment advice!

1

2

3

1)How much income does Southern Charter Financial

Services need?

2) Is it reasonable? Will he deplete his capital?

3) Discuss our investment strategy

4) Agree on objective - Yes?

5) Discuss where we are in the interest rate

cycle.

Asset Allocation is

EverythingOngoing research indicates that:

92% of performance comes from Asset Allocation,

6% from stock picking, and 2% from market timing

Determinants of Performance - Brinson et al Financial Analysts Journal

LO

NG

TE

RM

(L

AS

T 6

0Y

RS

)

AN

NU

AL

ISE

D R

EA

L R

ET

UR

N

Achieving Optimal Asset Allocation on the Efficient Frontier

In the worst market in living memoryPeriod - One year ending 30th September 2009

Southern Charter

Defensive +3.61%

Southern Charter

Balanced -8.79%

Southern Charter

Growth - 13.28%

JSE All Share

Index - 25.72%

Fund Ranking

1/54

3/40

1/17

Our Asset Allocation strategy Protects on the Downside

Prudential Low Equity Category

Prudential Medium Equity Category

Prudential High Equity Category

Personal FinanceSource

Our funds have delivered

JSE beating returns since

inception

Cash investment

Disaster funds for both spouses

Tax free interest per tax payer

Threshold per tax payer

Cash LumpsumNormally limited to the tax free portion

On your spousesdeath the remaining

funds are paid toyour estate

On your deaththe living annuity

continues to pay yourspouse

Investment StrategyCPI +5%

Defensive Fund

Living Annuity OptionMarket related Income

and Funds transferred

on death to spouse/estate

On your spousesdeath the annuity

ceases leaving yourestate nothing

On your deathyour joint life annuitycontinues to pay your

spouse

Decision to invest in life annuity

dependent on

interest rate cycle

or Life Annuity OptionGuaranteed income

Funds lost on death of spouse

unless guaranteed for 10yrs

Investment StrategyHow much fixed / guaranteed income (if at all)

and how much market related income

will he need? Economic input - interest rate cycle

Your PensionThe balance of your funds - after taking tax free cash

portion is invested in an Annuity

Our role...is to develop strategies1) tax strategy - to be as tax efficient as possible

2) investment strategy - to achieve best risk adjusted return

3) change strategy - manage and assist with life change

Retirement Day Arrives - Some Questions?Where will my income come from?

How much can i take without depleting my capital?

you will need expert financial and investment advice!

1

2

3Annuity Option Strategy

Discuss and explain both annuity options

Pros and cons and get agreement

On the risks of both options.

Decide and recommend a course

of action taking the clients

Feelings into account

How old is your wife?

Do you want to leave anything

To your kids?

Lets talk about beneficiaries

Living Annuities

• Beneficiary choice on death of annuitant: Annuity or lump sum

• lump sum proceeds received or accrued from a living annuities will be taxed according to the retirement tax tables

• No minimum drawdown required - maximum remains 17.5%

• Only natural persons as beneficiaries. EG no Trusts

Solve the following Case Studies

• Problem One - John retires when interest rates are high {15%} Inflation 10%

• Problem Two - John retires today

• Problem Three - identify what documentation is needed to be professional and compliant in both instances

• Problem Four - What else would you suggest?

We are with you for the long haul!

A wealth creation partnership.

Liv ing Lif e

Annuity Annuity Total

Opening Inv estment 2,310,031 500,000 2,810,031

Total all Fees -322,712 -322,712

Total Pension Paid -1,515,472 -779,926 -2,295,398

Total Capital Growth 1,890,646 0 1,890,646

Closing Inv estment 2,362,493 500,000 2,862,493

Current

Monthly Income 13,499 6,239 19,738

Variable Fixed

Portion Portion

Guaranteed

Case Study - John

• Case study - John Retires 10yrs later

Retirement Capital R2 862 493Gross Retirement Income - R19 653pmJohn has R180 000 in his Money Market accountJoy has R280 000 in her Money Market accountJoy still consults as a beautician

John and Joy maintained and improved their lifestylethey still live in Constantia, drive the same cars, and travel overseas once a year!

Southern Charter Financial Services (Pty) Ltd. is an Authorised Financial Service

Provider.

The content of this presentation and any information provided may be of a general nature

and may not be based on any analysis of the investment objective financial situation or

particular needs of the client. (as defined in the Financial Advisory Intermediary Services

Act) As a result, there may be limitations as to the appropriateness of any information

given. It is therefore recommended that the client first obtain the appropriate legal, tax,

investment or other professional advice and formulate an appropriate investment strategy

that would suit the risk profile of the client prior to acting upon such information and to

consider whether any recommendation is appropriate considering the client’s own

objectives and particular needs.

Any opinions, statements and any information made, whether written, oral or implied are

expressed in good faith.