southeastern asset management & longleaf partners funds€¦ · 1 year 5 year 10 year since...

TRANSCRIPT

Intelligent Investing in an Uncertain Environment

Southeastern Asset Management &Longleaf Partners Funds

November 2016

Before investing in any Longleaf Partners fund, you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. For a current Prospectus and Summary Prospectus, which contain this and other important information, visit longleafpartners.com. Please read the Prospectus and Summary Prospectus carefully before investing. RISKS

The Longleaf Partners Funds are subject to stock market risk, meaning stocks in the Funds may fluctuate in response to developments at individual companies or due to general market and economic conditions. Also, because the Funds generally invest in 15 to 25 companies, share values could fluctuate more than if a greater number of securities were held. Mid-cap stocks, held particularly in the Partners Fund, may be more volatile than those of larger companies. Smaller company stocks, held particularly in the Small-Cap Fund, may be more volatile than those of larger companies. Particularly for the International Fund and Global Fund, investing in non-U.S. securities may entail risk due to non-US economic and political developments, exposure to non-US currencies, and different accounting and financial standards. These risks may be higher when investing in emerging markets.

Funds distributed by ALPS Distributors, Inc.

The statements and opinions expressed are those of the author and are as of the date of this report.

Longleaf US Fund Disclosures

2LLP000559Expiring 1/31/17

Longleaf US Fund DisclosuresAverage annual total returns for the Funds and their benchmarks for the one, five, and 10-year and since inception periods endedSeptember 30, 2016 are as follows:

Returns reflect reinvested capital gains and dividends but not the deduction of taxes an investor would pay on distributions or share redemptions. Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Longleaf Partners Funds may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting longleafpartners.com

The total expense ratios for the Longleaf Partners Funds are: Longleaf Partners Fund 0.93%, Longleaf Small-Cap Fund 0.91%, Longleaf Partners International Fund 1.28%, Longleaf Partners Global 1.54%. The Partners and Small-Cap Funds’ expense ratios are subject to a fee waiver to the extent a Fund’s normal annual operating expenses exceed 1.5% of average annual net assets.The Longleaf International Fund’s expense ratio is subject to a fee waiver to the extent the Fund’s normal annual operating expenses exceed 1.75% of average annual net assets. The Longleaf Global Fund’s expense ratio is subject to a fee waiver to the extent the Fund’s normal annual operating expenses exceed 1.65% of average annual net assets.

1 Year 5 Year 10 Year Since InceptionPartners Fund (04/08/87) 24.80% 11.39% 3.77% 10.44%S&P 500 15.43 16.37 7.27 9.48Small-Cap Fund (02/21/89) 24.09% 16.49% 8.70% 11.05%Russell 2000 15.47 15.82 7.07 9.38International Fund (10/26/98) 16.86% 6.65% 1.41% 7.17%MSCI EAFE 6.52 7.39 1.82 4.06Global Fund (12/27/12) 25.74% na na 5.75%MSCI World 11.36 na na 9.23

3

Longleaf US Fund Disclosures

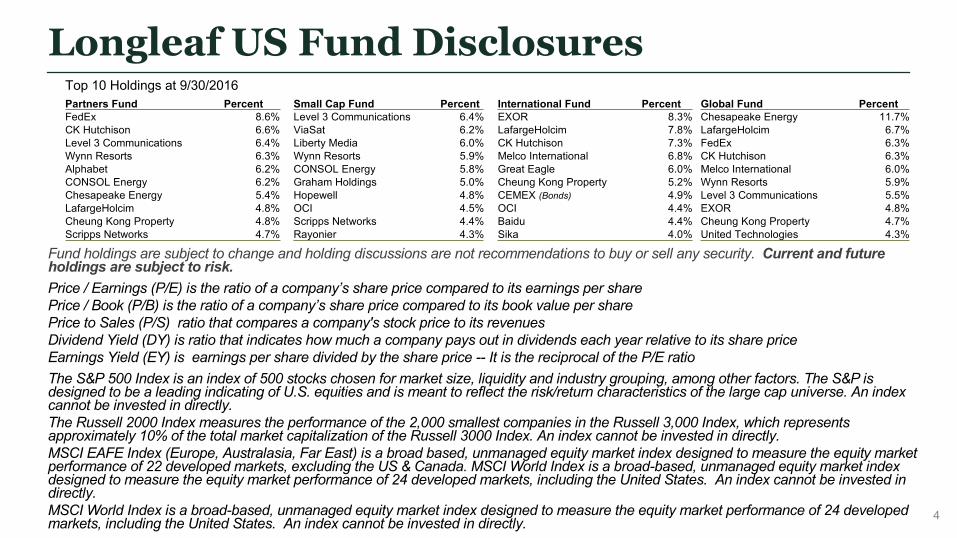

Fund holdings are subject to change and holding discussions are not recommendations to buy or sell any security. Current and future holdings are subject to risk. Price / Earnings (P/E) is the ratio of a company’s share price compared to its earnings per sharePrice / Book (P/B) is the ratio of a company’s share price compared to its book value per sharePrice to Sales (P/S) ratio that compares a company's stock price to its revenuesDividend Yield (DY) is ratio that indicates how much a company pays out in dividends each year relative to its share priceEarnings Yield (EY) is earnings per share divided by the share price -- It is the reciprocal of the P/E ratioThe S&P 500 Index is an index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. The S&P isdesigned to be a leading indicating of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. An index cannot be invested in directly. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3,000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. An index cannot be invested in directly.MSCI EAFE Index (Europe, Australasia, Far East) is a broad based, unmanaged equity market index designed to measure the equity market performance of 22 developed markets, excluding the US & Canada. MSCI World Index is a broad-based, unmanaged equity market indexdesigned to measure the equity market performance of 24 developed markets, including the United States. An index cannot be invested in directly.MSCI World Index is a broad-based, unmanaged equity market index designed to measure the equity market performance of 24 developed markets, including the United States. An index cannot be invested in directly.

Top 10 Holdings at 9/30/2016Partners Fund Percent Small Cap Fund Percent International Fund Percent Global Fund PercentFedEx 8.6% Level 3 Communications 6.4% EXOR 8.3% Chesapeake Energy 11.7%CK Hutchison 6.6% ViaSat 6.2% LafargeHolcim 7.8% LafargeHolcim 6.7%Level 3 Communications 6.4% Liberty Media 6.0% CK Hutchison 7.3% FedEx 6.3%Wynn Resorts 6.3% Wynn Resorts 5.9% Melco International 6.8% CK Hutchison 6.3%Alphabet 6.2% CONSOL Energy 5.8% Great Eagle 6.0% Melco International 6.0%CONSOL Energy 6.2% Graham Holdings 5.0% Cheung Kong Property 5.2% Wynn Resorts 5.9%Chesapeake Energy 5.4% Hopewell 4.8% CEMEX (Bonds) 4.9% Level 3 Communications 5.5%LafargeHolcim 4.8% OCI 4.5% OCI 4.4% EXOR 4.8%Cheung Kong Property 4.8% Scripps Networks 4.4% Baidu 4.4% Cheung Kong Property 4.7%Scripps Networks 4.7% Rayonier 4.3% Sika 4.0% United Technologies 4.3%

4

Our Global Research Team

5

Memphis, TNMason Hawkins, CFA

Staley Cates, CFA

Ross Glotzbach, CFA

Jim Thompson, CFA

Lowry Howell, CFA

Brandon Arrindell, CFA

SingaporeKen Siazon

Manish Sharma, CFA

Yaowen Zhang

LondonScott Cobb

Josh Shores, CFA

John Woodman

David Vyravipillai

Naser Bashir, CFA

Introduction Gwin Myerberg

Southeastern Progress Report Mason Hawkins

U.S. Investment Highlights Ross Glotzbach

Asian Investment Highlights Ken Siazon

European Investment Highlights Josh Shores

Q & A Global Research Team

Agenda

6

Capital Gains Distribution

Per Share % Long-Term

Partners Fund $0.5312 100%

Small-Cap Fund 4.855 97

International Fund -- --

Global Fund -- --

Distributed on November 16, 2016

7

Southeastern Progress ReportMason Hawkins

9

Southeastern Asset Management, Inc.We are long-term, concentrated, engaged, intelligent, partnership investors

Long-Term Investing A 5 year expected investment time horizon

Concentrated Investing 20 or fewer holdings

Engaged Investing Collaborate with our boards and managements to build long-term value per share growth

Intelligent Investing Investments must qualify quantitatively and qualitatively

Partnership Investing Collectively our associates and affiliates are the largest shareholder group in funds advised by Southeastern

Our Global Research Team

10

Memphis, TNMason Hawkins, CFA

Staley Cates, CFA

Ross Glotzbach, CFA

Jim Thompson, CFA

Lowry Howell, CFA

Brandon Arrindell, CFA

SingaporeKen Siazon

Manish Sharma, CFA

Yaowen Zhang

LondonScott Cobb

Josh Shores, CFA

John Woodman

David Vyravipillai

Naser Bashir, CFA

Year-To-Date PerformanceLongleaf Partners Funds and Indices (1/1/16 to 10/31/16)

*Inflation +10% is based on CPI (not seasonally adjusted) as of 9/30/16

Returns reflect reinvested capital gains and dividends but not the deduction of taxes an investor would pay on distributions or share redemptions. Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting longleafpartners.com. 11

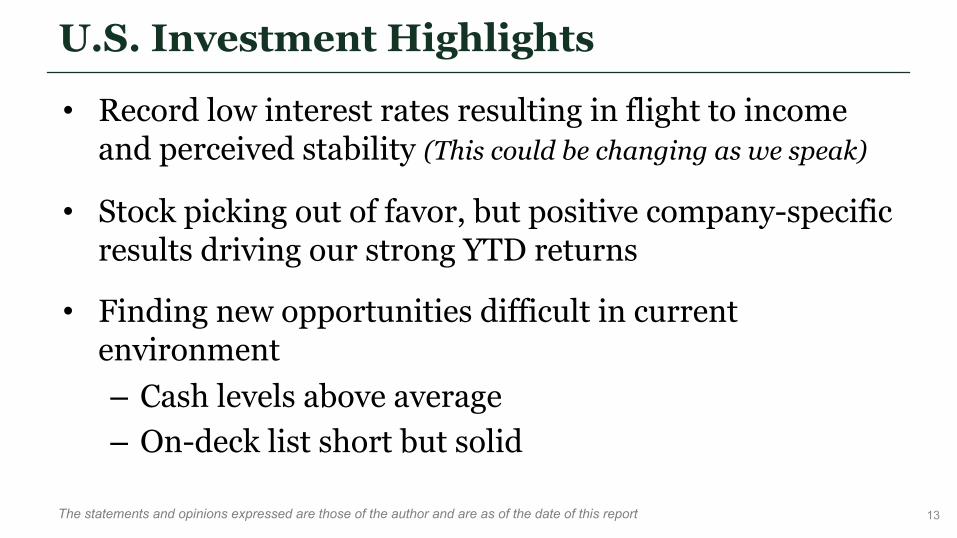

U.S. Investment HighlightsRoss Glotzbach

U.S. Investment Highlights

• Record low interest rates resulting in flight to income and perceived stability (This could be changing as we speak)

• Stock picking out of favor, but positive company-specific results driving our strong YTD returns

• Finding new opportunities difficult in current environment– Cash levels above average– On-deck list short but solid

The statements and opinions expressed are those of the author and are as of the date of this report 13

$20 - 30Value Range:

$7.40Closing Price: (11/13/15)

$62.20Closing Price: (11/13/15)

Valuations Last November

$120+Value Range:

Is Stock Picking Dead?We disagree with this sentiment and have been rewarded for our discipline over the last year

The Dying Business of Picking StocksMONDAY, OCTOBER 17, 2016

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security.

14

Company Specifics Driving Strong ReturnsOur positive performance over the last year is a result of strong management actions and improving industry dynamics

Total Return 15-November-15 to 15-November-16

15

CONSOL Energy

Wynn Resorts

S&P 500

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security.Past performance does not guarantee future results and current circumstances may not be comparable.

Inde

x Va

lue

24.7% 23.2%27.3%

0%

30%

Partners Fund Global Fund Small-Cap Fund

Current Position and OpportunityCash Balance at 10/31/16

Historical Cash Balance U.S. Sample Account12/31/1987 to 10/31/16 (monthly)

Limited Market Opportunity

25%High-Priced

25%Low-P/E/Low Quality

50%Opportunities

Average 10.5%

-5

0

5

10

15

20

25

30

35

1987

1989

1990

1991

1992

1993

1994

1996

1997

1998

1999

2000

2001

2003

2004

2005

2006

2007

2008

2010

2011

2012

2013

2014

2015

Perc

ent o

f Por

tfolio

The statements and opinions expressed are those of the author and are as of the date of this reportPast performance does not guarantee future results and current circumstances may not be comparable.

The chart shows monthly cash balance for Southeastern’s largest US Equity account.

16

Asian Investment HighlightsKen Siazon

Asian Investment Highlights• Asia remains most attractively valued region, in our

view, despite strong recent performance

• Positive company-specific results driving our strong YTD performance

• Investment opportunities in Japan and potential volatility resulting from – Fear of higher interest rates – Post-U.S. election uncertainty – Emerging Market weakness

18

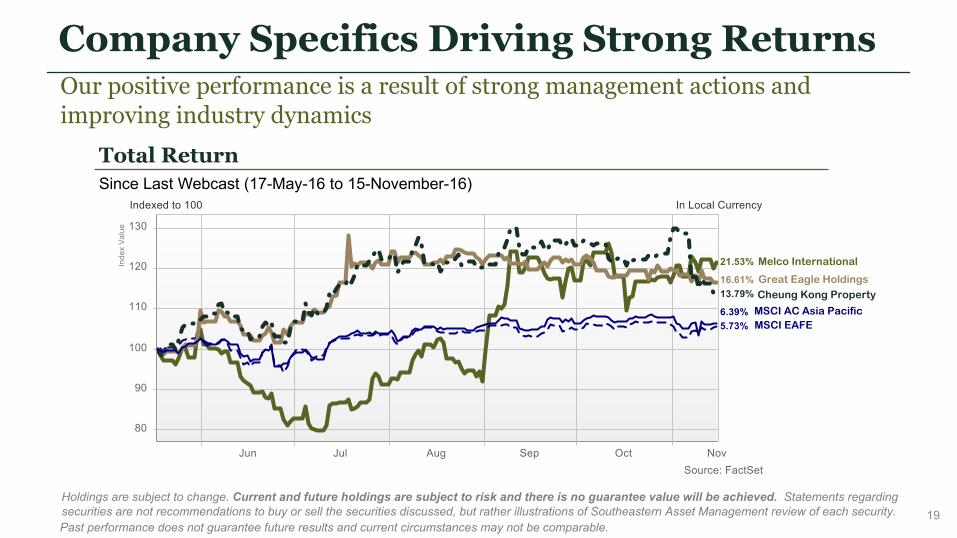

Our positive performance is a result of strong management actions and improving industry dynamics

Total Return Since Last Webcast (17-May-16 to 15-November-16)

Company Specifics Driving Strong Returns

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security. 19

Melco International

Great Eagle HoldingsCheung Kong Property

MSCI AC Asia PacificMSCI EAFE

Past performance does not guarantee future results and current circumstances may not be comparable.

Inde

x Va

lue

0

50

100

150

200

250

300

350

Private Domestic Transaction PricesHang Seng Property Index

Historic Disconnect

Global Financial CrisisSARS

Hong Kong property companies trade at significant discounts to underlying NAVs, and smart operators are selling property into private price strength

Hong Kong Real Estate

Source: Ratings and Valuation Department (Government of Hong Kong) Monthly Supplement dated September 30; FactSet

Historic Disconnect Significant disconnect between real estate and stock prices

Date Property Est. Gross Yield (%)

Rate (HK$/sq.ft)

Sep-16 Golden Centre 2.0 28,000Sep-16 Kwun Tong View 3.5 12,949Jul-16 One Harbour Gate (East) ~3.0 15,957May-16 China Overseas Building 2.2 22,092May-16 Wheelock House 3.2 30,216Jan-16 Dah Sing Financial Center 2.3 23,641Nov-15 Massmutual Tower 1.6 36,187Nov-15 One Harbour Gate (West) 3.0 14,885Sep-15 Park Building 3.0 6,869

Average 2.6 21,200

Real Estate Transactions Deals are pricing at or below 3% gross rental yields

Source: Morgan Stanley, September 20, 2016

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security.

20

Inde

x Va

lue

(Inde

xed

to 1

00 in

Jan

200

0)

Hong Kong Property Prices vs. Hang Seng Property Index

Current Position and OpportunityCash Balance at 31-October-2016

P/V (“price to value”) is a calculation that compares the prices of the stocks in a portfolio to Southeastern’s appraisal of their intrinsic values. The ratio represents a single data point about a Fund and should not be construed as something more. P/V does not guarantee future results, and we caution investors not to give this calculation undue weight. Past performance does not guarantee future results and current circumstances may not be comparable.

CountriesLTM

Price to Book

NTM Price to

Earnings

NTM Earnings

Yield

LTM Dividend

Yield

Bond Yield

Earnings Yield / Bond

YieldPrice to Sales

Hong Kong 1.1 10.1 9.9 2.1 1.3 7.5 1.0

Korea 1.1 10.2 9.8 1.5 1.8 5.3 0.6

Singapore 1.1 13.2 7.6 3.8 2.1 3.6 1.5

Japan 1.2 14.0 7.1 2.1 0.0 -155.1 0.7

Germany 1.7 13.2 7.6 2.7 0.3 28.1 0.7

UK 1.7 14.7 6.8 3.4 1.2 5.5 1.2

Australia 1.8 15.8 6.3 4.2 2.5 2.5 1.7

US 2.6 17.4 5.7 2.0 2.2 2.7 1.7

China 2.9 20.2 5.0 0.9 2.8 1.8 2.1

Global Market ValuationsAt 10-November-2016

LTM – Last 12 Months, NTM – Next 12 MonthsSource: FactSet

U.S. Election Volatility

21

Inde

x C

losi

ng P

rice

24.7% 23.2%

0%

30%

International Fund Global Fund

Mid - 60s%P/V Mid - 60s%

European Investment HighlightsJosh Shores

European Investment Highlights

• Investing within our circle of competence with ownership mentality being rewarded

• Positive company-specific results driving our strong YTD performance

• In our view, Europe remains more inefficient with wider stock dispersion and broad macro uncertainty

• Cash represents opportunity for next qualifiers

23

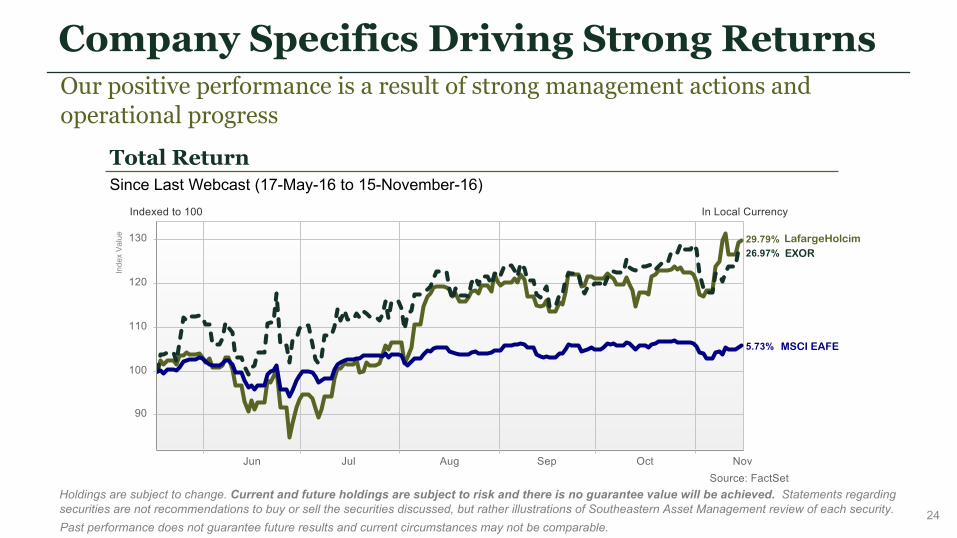

Company Specifics Driving Strong ReturnsOur positive performance is a result of strong management actions and operational progress

Total Return Since Last Webcast (17-May-16 to 15-November-16)

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security. 24

LafargeHolcimEXOR

MSCI EAFE

Past performance does not guarantee future results and current circumstances may not be comparable.

Inde

x Va

lue

Current Position and Opportunity

Past performance does not guarantee future results and current circumstances may not be comparable.

Global Market ValuationsAt 10-November-2016

LTM – Last 12 Months, NTM – Next 12 MonthsSource: FactSet

CountriesLTM

Price to Book

NTM Price to

Earnings

NTM Earnings

Yield

LTM Dividend

Yield

Bond Yield

Earnings Yield /

Bond YieldPrice to Sales

Hong Kong 1.1 10.1 9.9 2.1 1.3 7.5 1.0

Singapore 1.1 13.2 7.6 3.8 2.1 3.6 1.5

Japan 1.2 14.0 7.1 2.1 0.0 -155.1 0.7

Germany 1.7 13.2 7.6 2.7 0.3 28.1 0.7

UK 1.7 14.7 6.8 3.4 1.2 5.5 1.2

US 2.6 17.4 5.7 2.0 2.2 2.7 1.7

China 2.9 20.2 5.0 0.9 2.8 1.8 2.1

France 1.5 14.4 7.0 3.5 0.7 10.2 0.9

Spain 1.4 14.3 7.0 4.1 1.4 5.0 1.1

Italy 1.0 13.3 7.5 3.6 1.9 3.9 0.5

25

• Leading businesses with owner operators growing values

• Our constructive engagement supporting value recognition

• Cash as opportunity for next qualifiers

Cash Balance at 10-October-2016

24.7% 23.2%

0%

30%

International Fund Global Fund

Q & ABrandon Arrindell

Q&A with Our Global Research Team

27

Memphis, TNMason Hawkins, CFA

Staley Cates, CFA

Ross Glotzbach, CFA

Jim Thompson, CFA

Lowry Howell, CFA

Brandon Arrindell, CFA

SingaporeKen Siazon

Manish Sharma, CFA

Yaowen Zhang

LondonScott Cobb

Josh Shores, CFA

John Woodman

David Vyravipillai

Naser Bashir, CFA

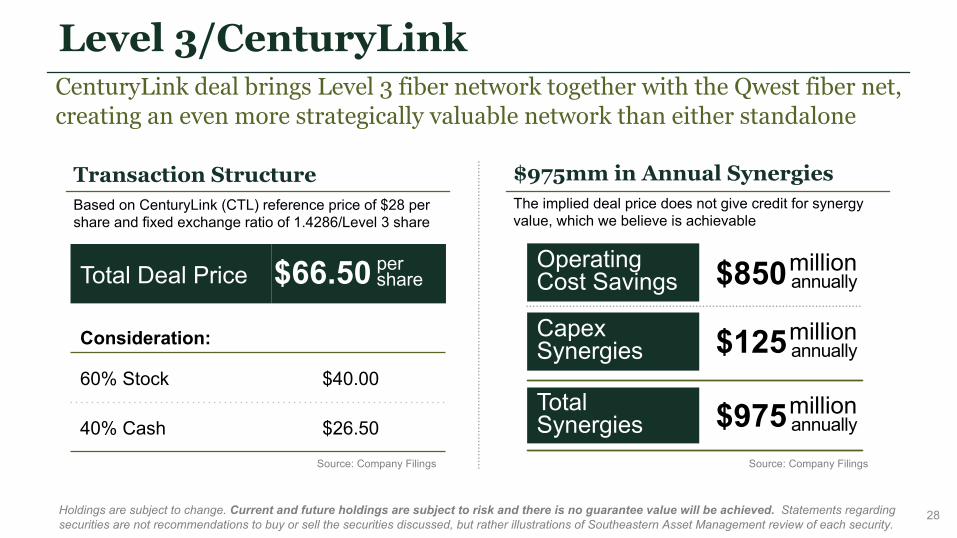

Level 3/CenturyLinkCenturyLink deal brings Level 3 fiber network together with the Qwest fiber net, creating an even more strategically valuable network than either standalone

Transaction StructureBased on CenturyLink (CTL) reference price of $28 per share and fixed exchange ratio of 1.4286/Level 3 share

$975mm in Annual SynergiesThe implied deal price does not give credit for synergy value, which we believe is achievable

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security.

Total Deal Price pershare

Consideration:

60% Stock $40.00

40% Cash $26.50

Capex Synergies

million annually

Total Synergies

million annually

Operating Cost Savings

million annually$850

$125

$975 Source: Company Filings Source: Company Filings

$66.50

28

0

2

4

6

8

10

0

20

40

60

80

100

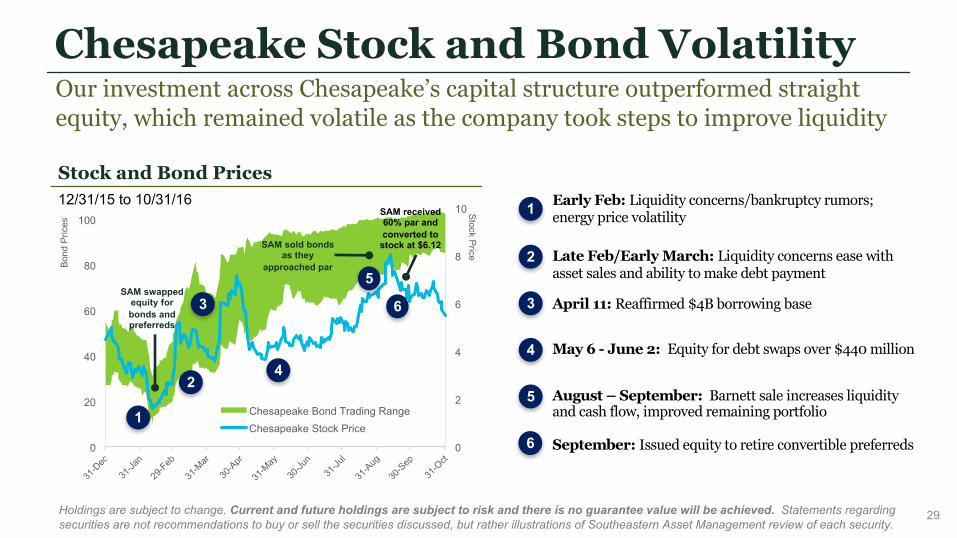

Chesapeake Bond Trading RangeChesapeake Stock Price

Chesapeake Stock and Bond VolatilityOur investment across Chesapeake’s capital structure outperformed straight equity, which remained volatile as the company took steps to improve liquidity

Stock Price

Bond

Pric

es

Stock and Bond Prices 12/31/15 to 10/31/16

1

2

3

4

5

Early Feb: Liquidity concerns/bankruptcy rumors; energy price volatility

Late Feb/Early March: Liquidity concerns ease with asset sales and ability to make debt payment

April 11: Reaffirmed $4B borrowing base

May 6 - June 2: Equity for debt swaps over $440 million

August – September: Barnett sale increases liquidity and cash flow, improved remaining portfolio

September: Issued equity to retire convertible preferreds

1

2

3

4

5

6

6SAM swapped

equity for bonds and preferreds

SAM sold bonds as they

approached par

SAM received 60% par and converted to

stock at $6.12

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security.

29

Chesapeake Debt Reduction“We have substantially improved our capital structure … we have taken measures to provide excess liquidity to address the remaining maturities of our debt through 2018” – Doug Lawler, CEO

Company press release dated October 5, 2016

YTD Decrease in Debt Maturing Over Next 5 Years

$5.1 BillionDebt dueafter 20202

$2.9 BillionDebt duethrough 2020

~$8.0 BillionTotal

Source: FactSet; Company Filings

1. Estimated future debt level based on filings since June 30, 20162. Does not include $1.5 billion term loan facility or $100 million

revolving credit

9/30/161

$0.38 B

$1.89 B

$0.88 B

$1.10 B $1.13 B

$0.00 B

$0.66 B $0.67 B$0.50 B

$1.10 B

2016 2017 2018 2019 2020Includes

2037(puttable in 2017)

Includes2038

(puttable in 2018)

12/31/15: Total 5 Year Maturities = $5.4B

9/30/161: Total 5 Year Maturities = $2.9B

Holdings are subject to change. Current and future holdings are subject to risk and there is no guarantee value will be achieved. Statements regarding securities are not recommendations to buy or sell the securities discussed, but rather illustrations of Southeastern Asset Management review of each security.

30