· pdf fileby sonia baldeira, iwona hovenko and yi zhu. page 6 oil. ... compensation has not...

TRANSCRIPT

March 28, 2016 Bloomberg Brief Economics Asia 2

INSIDE

BIG PICTURE. Prime Minister Modi's second anniversary as premier is approaching and many reform ambitions remain far from realized. By Enda Curran and Unni Krishnan. Page 3

OUTLOOK. Benign inflation and a prudent government deficit target for the next financial year provide scope for more easing by India’s central bank. By Tamara Henderson. Page 4

THE BUDGET. A demonstration of fiscal prudence should pay dividends in the form of lower borrowing costs. By Tamara Henderson. Page 5

INFRASTRUCTURE. India faces a similar challenge to China a decade ago: building a nationwide transport network as well as entire cities, schools and hospitals. By Sonia Baldeira, Iwona Hovenko and Yi Zhu. Page 6

OIL. India looks like Japan, whose woefully inadequate oil reserves made it the world's biggest energy importer for decades. By David Fickling. Page 7

RUPEE OUTLOOK. Where economic reforms go, the currency may follow. By Subhadip Sircar. Page 8

CREDIT OUTLOOK. Indian firms will issue a record amount of local currency bonds again this year as fiscal discipline aims to allow the central bank to cut rates. By Divya Patil. Page 9

EQUITIES. Investors withdrew a net $100 million from India-focused ETFs during the last 12 months. By Puneet Saxena and Kartik Palaniappan. Page 10

M&A. Local banks are rising up the country's league table. By George Smith Alexander and Anto Antony. Page 11

REAL ESTATE. Piramal Enterprises' real estate unit has its sights on distressed assets discarded by indebted businesses and banks. By Bhuma Shrivastava. Page 12

VENTURE CAPITAL. The fundraising party may be winding down. By Saritha Rai. Page 13

BUSINESS OF SPORT. The Indian Premier League of cricket is producing revenues and economic impact to rival professional leagues in developed markets. By Colin Simpson. Page 14

Samit Vartak, chief investment officer at SageOne Q&A. Investment Advisors, discusses investment opportunities created by the new budget. By Suzy Waite. Page 15

BIG PICTURE

March 28, 2016 Bloomberg Brief Economics Asia 3

BIG PICTURE

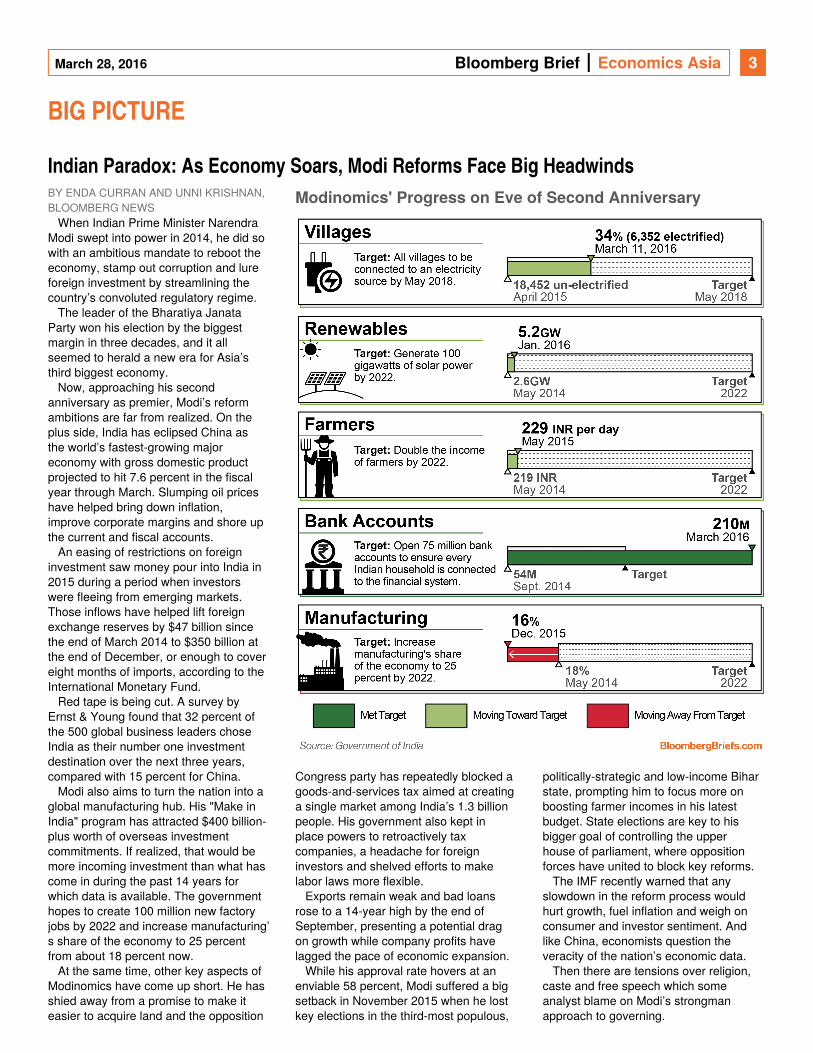

Indian Paradox: As Economy Soars, Modi Reforms Face Big HeadwindsBY ENDA CURRAN AND UNNI KRISHNAN, BLOOMBERG NEWS

When Indian Prime Minister Narendra Modi swept into power in 2014, he did so with an ambitious mandate to reboot the economy, stamp out corruption and lure foreign investment by streamlining the country’s convoluted regulatory regime.

The leader of the Bharatiya Janata Party won his election by the biggest margin in three decades, and it all seemed to herald a new era for Asia’s third biggest economy.

Now, approaching his second anniversary as premier, Modi’s reform ambitions are far from realized. On the plus side, India has eclipsed China as the world’s fastest-growing major economy with gross domestic product projected to hit 7.6 percent in the fiscal year through March. Slumping oil prices have helped bring down inflation, improve corporate margins and shore up the current and fiscal accounts.

An easing of restrictions on foreign investment saw money pour into India in 2015 during a period when investors were fleeing from emerging markets. Those inflows have helped lift foreign exchange reserves by $47 billion since the end of March 2014 to $350 billion at the end of December, or enough to cover eight months of imports, according to the International Monetary Fund.

Red tape is being cut. A survey by Ernst & Young found that 32 percent of the 500 global business leaders chose India as their number one investment destination over the next three years, compared with 15 percent for China.

Modi also aims to turn the nation into a global manufacturing hub. His "Make in India" program has attracted $400 billion-plus worth of overseas investment commitments. If realized, that would be more incoming investment than what has come in during the past 14 years for which data is available. The government hopes to create 100 million new factory jobs by 2022 and increase manufacturing’s share of the economy to 25 percent from about 18 percent now.

At the same time, other key aspects of Modinomics have come up short. He has shied away from a promise to make it easier to acquire land and the opposition

Congress party has repeatedly blocked a goods-and-services tax aimed at creating a single market among India’s 1.3 billion people. His government also kept in place powers to retroactively tax companies, a headache for foreign investors and shelved efforts to make labor laws more flexible.

Exports remain weak and bad loans rose to a 14-year high by the end of September, presenting a potential drag on growth while company profits have lagged the pace of economic expansion.

While his approval rate hovers at an enviable 58 percent, Modi suffered a big setback in November 2015 when he lost key elections in the third-most populous,

politically-strategic and low-income Bihar state, prompting him to focus more on boosting farmer incomes in his latest budget. State elections are key to his bigger goal of controlling the upper house of parliament, where opposition forces have united to block key reforms.

The IMF recently warned that any slowdown in the reform process would hurt growth, fuel inflation and weigh on consumer and investor sentiment. And like China, economists question the veracity of the nation’s economic data.

Then there are tensions over religion, caste and free speech which some analyst blame on Modi’s strongman approach to governing.

OUTLOOK

Modinomics' Progress on Eve of Second Anniversary

March 28, 2016 Bloomberg Brief Economics Asia 4

OUTLOOK

India Inflation, Budget Provide Scope for Rate CutBY TAMARA HENDERSON, BLOOMBERG INTELLIGENCE ECONOMIST

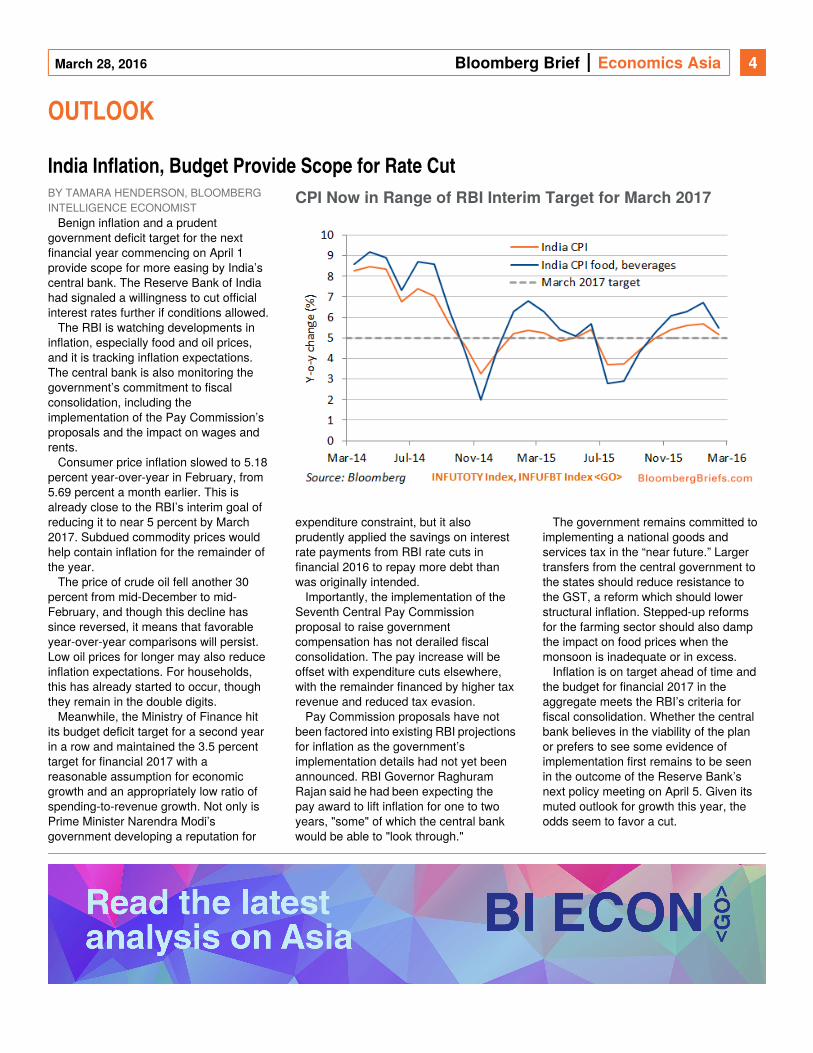

Benign inflation and a prudent government deficit target for the next financial year commencing on April 1 provide scope for more easing by India’s central bank. The Reserve Bank of India had signaled a willingness to cut official interest rates further if conditions allowed.

The RBI is watching developments in inflation, especially food and oil prices, and it is tracking inflation expectations. The central bank is also monitoring the government’s commitment to fiscal consolidation, including the implementation of the Pay Commission’s proposals and the impact on wages and rents.

Consumer price inflation slowed to 5.18 percent year-over-year in February, from 5.69 percent a month earlier. This is already close to the RBI’s interim goal of reducing it to near 5 percent by March 2017. Subdued commodity prices would help contain inflation for the remainder of the year.

The price of crude oil fell another 30 percent from mid-December to mid-February, and though this decline has since reversed, it means that favorable year-over-year comparisons will persist. Low oil prices for longer may also reduce inflation expectations. For households, this has already started to occur, though they remain in the double digits.

Meanwhile, the Ministry of Finance hit its budget deficit target for a second year in a row and maintained the 3.5 percent target for financial 2017 with a reasonable assumption for economic growth and an appropriately low ratio of spending-to-revenue growth. Not only is Prime Minister Narendra Modi’s government developing a reputation for

expenditure constraint, but it also prudently applied the savings on interest rate payments from RBI rate cuts in financial 2016 to repay more debt than was originally intended.

Importantly, the implementation of the Seventh Central Pay Commission proposal to raise government compensation has not derailed fiscal consolidation. The pay increase will be offset with expenditure cuts elsewhere, with the remainder financed by higher tax revenue and reduced tax evasion.

Pay Commission proposals have notbeen factored into existing RBI projectionsfor inflation as the government’s implementation details had not yet been announced. RBI Governor Raghuram Rajan said he had been expecting the pay award to lift inflation for one to two years, "some" of which the central bank would be able to "look through."

The government remains committed to implementing a national goods and services tax in the “near future.” Larger transfers from the central government to the states should reduce resistance to the GST, a reform which should lower structural inflation. Stepped-up reforms for the farming sector should also damp the impact on food prices when the monsoon is inadequate or in excess.

Inflation is on target ahead of time and the budget for financial 2017 in the aggregate meets the RBI’s criteria for fiscal consolidation. Whether the central bank believes in the viability of the plan or prefers to see some evidence of implementation first remains to be seen in the outcome of the Reserve Bank’s next policy meeting on April 5. Given its muted outlook for growth this year, the odds seem to favor a cut.

THE BUDGET BY TAMARA HENDERSON, BLOOMBERG INTELLIGENCE ECONOMIST

CPI Now in Range of RBI Interim Target for March 2017

March 28, 2016 Bloomberg Brief Economics Asia 5

THE BUDGET BY TAMARA HENDERSON, BLOOMBERG INTELLIGENCE ECONOMIST

Modi Keeps Targeted Spending in CheckThe government’s spending plans

remain prudent. Total expenditures are projected to increase by 10.8 percent, which is in line with the 11 percent baseline assumption for nominal GDP growth. This is also 4.7 percentage points below the anticipated increase in receipts excluding borrowing. If the government carries through on its plan, the extent to which expenditures exceed revenues excluding borrowing will fall to 37 percent.

Infrastructure projects will need to take a back seat to other spending, including measures to support the farm sector. Space must also be created to fund the Seventh Central Pay Commission’s recommendation for a substantial increase in government compensation. As such, plan expenditures on the revenue account are slated to increase by 20.5 percent in FY2017. By comparison, plan expenditures on the capital account will increase just 2.9 percent next year. This follows an increase of 35.4 percent in FY2016.

Non-plan expenditures, which include more uncertain spending such as interest

payments and subsidies, are targeted to rise by 9 percent, the same increase as in FY2016 and FY2015. Large interest payments and subsidies, which account for 25 percent and 14 percent of total expenditures respectively, continue to limit room for maneuver. Rate cuts by the

Reserve Bank of India would help keepborrowing costs in check and adequate rainfall during the southwest monsoon would help reduce the government’s food subsidy bill, though the government does not appear to be putting too much weight on such possibilities.

Ministry of Finance Gets More Aggressive With Revenue PlansThe Ministry of Finance expects

receipts excluding borrowing to grow by 15.5 percent, almost twice the pace of realized collections it estimates for the previous financial year.

The pace of receipts envisioned for next year is also 4.5 percentage points above the government’s 11 percent baseline assumption for nominal GDP growth — much more aggressive than the budget plan for FY2016.

The lion’s share of the increase in receipts is to come from tax revenues. The government will further widen the tax base with a host of measures to reduce tax evasion, including the introduction of taxes at the source for high value transactions. Additionally, “the likely implementation of GST [goods and services tax] in the near future” is seen boosting indirect tax collections.

Asset sales in the current financial year fell short of plans because of financial

market volatility. Disinvestment is slated to pick up in FY2017, with capital receipts

excluding loan recoveries and borrowings projected to double to 0.6 trillion rupees.

INFRASTRUCTURE

Expenditures Breakdown

Hitting Revenue Goals Is Key to Budget Success

March 28, 2016 Bloomberg Brief Economics Asia 6

INFRASTRUCTURE

India's Thirst for Infrastructure Paves Way for Building SpreeBY SONIA BALDEIRA AND IWONA HOVENKO, BLOOMBERG INTELLIGENCE ANALYSTS

India faces a similar challenge to that faced by China a decade ago: building a nationwide transport network as well as entire cities, schools and hospitals. Projects include the 1,428-km Delhi to Mumbai highway. India's government is promoting this expansion with favorable government policy initiatives.

India produced 219 kilograms of cement per capita compared with 1,721 kilograms in China in 2015, according to Bloomberg Intelligence. The gap in cement production and consumption is expected to narrow in the next decade, as India's population grows faster. Since 2010, the country's population has risen 6.7 percent, compared with 2.4 percent for China.

India is likely to be among the fastest-growing building materials markets in 2016. Government measures to boost affordable housing demand and infrastructure construction should

underpin growth. A stable rupee and subdued inflation are also helping. The background for investment is also favorable, though curbed by relatively

high interest rates. LafargeHolcim forecasts India's cement demand will increase by 5 percent a year, reaching 311 million metric tons in 2018.

Steel Output Growth May Accelerate on Government SpendingBY YI ZHU, BLOOMBERG INTELLIGENCE ANALYST

India may also ramp up crude-steel output as the government pushes ahead with infrastructure and affordable housing projects.

Capacity will rise to 142 million tons by 2017, up more than 40 percent from 2014, according to the five-year plan for 2012-2017. Output growth has slowed in the past four years, mainly due to delays in securing environmental clearances for projects. India plans to increase capacity to 300 million tons by 2025.

Indian steel companies can now import high-quality iron ore at about the same cost as lower-quality, domestic feedstock, thanks to falling global prices. The situation is hurting Indian miners whileboosting margins at the nation's steel mills.

India had raised export duties on iron ore, motivated by concerns about the availability of the raw materials for its

steelmakers. The country became a net-importer of iron ore in July 2014. The

export tax will be scrapped according to the government's latest federal budget.

OIL

China's Cement Demand Towers Above Others

Iron-Ore Imports Overtook Exports in July 2014

March 28, 2016 Bloomberg Brief Economics Asia 7

OIL

India's Coming Oil Drought Will Dwarf China's ShortfallBY DAVID FICKLING,BLOOMBERG GADFLY

Watching the development of India, there's often an assumption the country will follow China's path. For commodity exports, China "is not the only game in town," Australia's resources minister Josh Frydenberg said in a February speech, citing forecasts of India's burgeoning demand for power, steel, and coal.

Here's one area where the two countries could scarcely be more different: oil.

Geography accounts for much of the contrast. China isn't just a big consumer of oil: Thanks to ample onshore and offshore reserves, it was the world's fourth-biggest crude producer after the United States, Saudi Arabia and Russia in 2014, according to BP. By adding nearly a million barrels a day of local output over the past 15 years, Beijing has been able to maintain a relatively manageable crude deficit and soften the impact of its burgeoning demand on the rest of the world.

India looks a lot more like Japan, whose woefully inadequate oil reserves made it the world's biggest energy importer for decades. India was the 20th-biggest oil producer in 2014, according to BP, and looks since to have slipped one further place back, behind the U.K. Domestic output has dropped about 14 percent since 2011, according to data from the Ministry of Petroleum. Over that same 15-year period when China was adding a million barrels of daily output, India put on just 169,000.

Oil accounts for about a third of India's imports and two-thirds of its budget deficit, equivalent to 9 percent of gross domestic product in 2013, according to

. That's a PricewaterhouseCoopersdrag on the economy, and in the long term the situation is likely to worsen.

India will become the world's third-biggest car market by 2019, adding furtherpressure from consumers. Under a scenario where Modi's "Make in India" manufacturing policies lift Indian GDP by 6.8 percent a year (compared with the 7.1 percent pace it's averaged since 2000,

and China's 9.6 percent rate over the same period), the International Energy Agency projects oil demand will hit 7.1 million barrels a day by 2030, with only 0.4 million barrels provided by domestic production.

Trade in refined products will reduce the daily import demand to about 5.4 million barrels in 2030, according to the IEA, but that's still equivalent to more than half of Saudi Arabia's output. And it will continue

to rise: By 2040, the gap between demand and domestic production will hit 9.4 million barrels a day, about 50 percent bigger than China's deficit in 2014. With capital spending on new oilfields on hold thanks to depressed prices and a global glut that may not be cleared until 2021, that's enough to give any oil executive sleepless nights.

This column does not necessarily reflect the

opinion of Bloomberg LP and its owners.

RUPEE OUTLOOK

Thirsty: India's Oil Imports Moved Ahead of Japan's

Plugging the Gap: Oil Import Demand Will Only Rise

March 28, 2016 Bloomberg Brief Economics Asia 8

RUPEE OUTLOOK

Modi's Path on Reform Is Next Crucial Test for Slumping CurrencyBY SUBHADIP SIRCAR,BLOOMBERG FIRST WORD

Prime Minister may Narendra Modihave taken the first steps to calm investors by presenting a fiscally prudent budget. How he manages to push through reforms will be the next crucial test in the rupee's fortunes.

While the U.S. Fed's rate-hike trajectory remains a key to emerging market currency performance, foreign investors are keeping a close watch on how India navigates a volatile global environment.

As the Modi government approaches two years in office, key reforms are outstanding. The much-delayed goods and services tax and the land legislation bill are in legislative limbo as the government lacks the necessary numbers to push through the bills in the upper house of parliament. Bad loans in state-run banks have been piling up, leading to concerns on lenders holding back on loans which may hurt the nascent economic recovery.

Modi also faces key elections in four states during the next two months, none in areas where his party is a traditional force. His Bharatiya Janata Party will try to regain some political ground after recent losses in Delhi and Bihar states.

A loss would not only hamper Modi's aim of gaining majority in the upper house of parliament, but also hurt the political will to undertake bolder reforms.

The rupee has spent most of 2016 languishing near the bottom of the Asian currency heap, coming perilously close to its record low of 68.845 to the dollar seen in the taper-tantrum days of August 2013.

Most foreign banks including Goldman and had outperform ratings Sachs ANZ

on the currency at the start of the year. This was based on the attractiveness of the carry trade, strong macro fundamentals — like a shrinking current-account deficit and easing inflation — as well as a credible central bank.

The rupee recovered some losses after the government stuck to its fiscal consolidation plan in the budget. It is forecast to trade at 68.90 to the dollar in the fourth quarter of this year, improving to 68 by 2017, according to a median

survey of Bloomberg forecasters as of March 9.

Technically, a bearish shift in momentum indicators on monthly charts suggests the rupee could fall to its 21-month moving average in coming months, according to Bloomberg currency strategist Andrew Robinson.

And regulatory, political and external risks remain. The Reserve Bank of India has been adding to forex reserves, while

referring to the rupee's overvalued realeffective exchange rate compared to its to trading peers. Rajan said last month that he would encourage some rupee depreciation to combat inflation.

Another potential worry is the conclusion of Rajan's term in office this September. His deft management of monetary policy has won praise. Any changing of the guard will be a potential source of investor worry.

BONDS

Rupee May Fall to 21-Month Moving Average

Indian Currency Tipped as a Leading EM Performer

March 28, 2016 Bloomberg Brief Economics Asia 9

BONDS

Rupee Bond Issuance Seen Extending Record Run in 2016BY DIVYA PATIL,BLOOMBERG FIRST WORD

Indian companies will continue their runof issuing record amounts of local currencybonds this year as Prime Minister

's fiscal discipline aims to Narendra Modiprovide the central bank room to cut interest rates.

The government last month said the budget gap will narrow as targeted to 3.5 percent of gross domestic product in the year starting April 1, the smallest since 2008. The administration's fiscal prudence opens room for Reserve Bank of India to cut benchmark rates by 50 basis points this year, according to Axis

, the top arranger for rupee bonds Banksince 2008.

"As growth and investments pick up pace in the economy, more companies will look to borrow from the bond market," said , head of Shashi Kant Rathiinvestments and capital markets at Axis, who expects issuance to rise to a record 5trillion rupees in 2016. "Top rated companies will find it easier to refinance high cost debt in the bond market."

Infrastructure-related issuance is seen rising this year as RBI in September allowed banks to partially enhance credit ratings on corporate bonds issued by companies, in turn enabling borrowers to access funds from the bond market on better terms.

India's state-run Life Insurance Corp.will also set up a fund to help improve credit ratings of bonds sold by infrastructure companies, the government announced in its federal budget last month.

Axis's Rathi expects issuers to borrow from the bond market only while the spread between yields on company notes and banks' lending rate remains wide. Some bankers say the shrinking gap is prompting some issuers to temporarily choose loans.

Though local-currency onshore issuance is seen rising, the same isn't true for rupee bonds issued by Indian firms in the overseas market. Not one company has sold the so-called Masala bonds, named after spices found in Indian curries, as investors demand premiums

for liquidity and currency risks.

RBI in September had allowed offshore rupee bond sales to help wean companies off foreign debt and provide financing for Modi's $1 trillion wish list of infrastructure projects.

Bankers said guidelines on green bonds, municipal bonds, and primary

market offerings on electronic platforms will also boost the onshore rupee bond market to an all-time high this year. They expect issuance to remain robust and atypical borrowers to continue tapping the market as a revival is seen in the Indian economy.

EQUITIES

Local Issuance Expected to Hit New High

* Estimate by Axis Bank

Shrinking Rate Gap Between Bonds, Bank Loans

* Difference in yield between State Bank of India's base rate and the average on secondary prices for AAA-rated rupee-denominated bonds with a three-year maturity.

March 28, 2016 Bloomberg Brief Economics Asia 10

EQUITIES

Exchange-Traded Fund Investors Cool on India ProspectsInvestors pulled out a net $100 million

from India-focused exchange-traded funds listed outside the country in the past year, according to data compiled by Bloomberg.

The funds have seen outflows in eight of the past nine months as global investors have withdrawn money from emerging markets including India. Except for October, the outflow has been consistent since June 2015.

The WisdomTree India Earnings Fund had the most outflow, $570 million, during the 12 months to March 15.

The iShares MSCI India fund received by far the most inflows, a net $1.09 billion.

— Puneet Saxena, application specialist,

Bloomberg LP, and Kartik Palaniappan, analytics,

Bloomberg LP

India Stocks Face Valuation Headwinds Compared With Other BRICsIndia equities seem overvalued

compared with the benchmark indexes of the other countries that make up BRICs.

A decline in earnings among India's biggest companies has contributed to the surge in the Nifty 50's price-to-earnings ratio: it has soared to more than 20x from about 15x two years ago, according to data compiled by Bloomberg.

The equity benchmarks of Russia and China trade at lower multiples. Russia, which vies with Saudi Arabia as the world's largest oil producer, has by far the cheapest stock market of the four BRIC nations. It has benefited from the 40 percent-plus rally in crude prices this year.

— Kartik Palaniappan, analytics, Bloomberg LP

The articles on this page were written by Bloomberg LP employees who may be involved in the selling of the Bloomberg Professional Service and edited by the News department. To suggest ideas or provide feedback, contact the editor, Stew Hawkins, at [email protected].

M&A

Net ETF Flows for the Year to March 15

Fundamentally Challenged

The valuation score above is a composite measure comprised of equally weighted B/P, E/P and dividend yield values that have been Z-scored relative to the average of the basket. It shows India's Nifty 50 is 0.75 of a standard deviation below the average — it's more expensive than the other indexes. Bloomberg Professional subscribers can use the function to analyze how MRVIndia's stock market valuation compares with its peers.

March 28, 2016 Bloomberg Brief Economics Asia 11

M&A

Citigroup's Slide in League Table Shows Rise of Local Bankers BY GEORGE SMITH ALEXANDER AND ANTO ANTONY, BLOOMBERG NEWS

Citigroup Inc. is no longer India’s top investment banker. A local firm that ended a partnership with Morgan Stanley more than eight years ago became No. 1 in 2015, marking the decline of foreign advisers who’ve led the market for more than a decade.

After topping the M&A league table the prior two years, the U.S. lender tumbled to fourth position, dislodged by JM Financial Ltd. and Axis Capital Ltd.

India-based investment banks have been honing their skills in forging mergers and acquisition deals at a time their overseas rivals have either closed their businesses in the South Asian country or have been cutting senior positions. Royal Bank of Scotland Group Plc shut down its India advisory unit, while Morgan Stanley, UBS Group AG and Bank of America Corp. scaled back their operations in the last five years.

“We are like the Goldman Sachs of India,” Vishal Kampani, managing directorof JM Financial, said in an interview earlier this month. “Having a team which saw almost no churn for 15 years helped us institutionalize relationships and gives bandwidth to deliver on complex deals on the ground unlike foreign players.”

Following the global financial crisis of 2008, deals and equity offerings by Indian companies slowed as economic growth cooled. Some advisers lowered their fees to chase work. Many foreign banks’ advisory units responded by reducing workforce and flying in senior bankers from Hong Kong and Singapore when needed, Dharmesh Mehta, chiefexecutive officer and managing director of Axis Capital, said in an interview in his office. As business picks up, clients are turning to experienced bankers on the ground, with whom they’ve had long-term relationships, he said.

“Competition from foreign banks is decreasing day by day,” he said. “We don’t see any foreign bank dominating the market this year.”

Fees were at $516 million in 2015 versus an average $580 million in the five years starting 2011, according to data

JM Financial Topped 2015 Adviser League Table by Share

2015 RANK

2014 RANK

FIRMMARKET SHARE

TOTAL DEAL VALUE ($m)

AVERAGE DEAL VALUE ($m)

DEAL COUNT

1 3 JM Financial Ltd 38% 24,788 2,066 12

2 13 Axis Bank Ltd 33% 21,483 1,790 12

3 12 Macquarie 29% 19,097 9,549 2

4 1 Citi 10.7% 6,954 632 11

5 31 Credit Suisse 6.9% 4,476 560 8

6 4 BofA Merrill Lynch 6.8% 4,441 1,110 4

7 25 Morgan Stanley 6.6% 4,312 479 9

8 21 JP Morgan 5.8% 3,754 417 9

9 10 Kotak Mahindra Bank 5.1% 3,309 236 14

10 9 Ernst & Young 4.6% 2,992 77 39Source: Bloomberg

provided by Freeman Consulting, a New York-based research firm.

That is just 4 percent of the $12.9 billion investment banks generated in the rest of Asia ex-Japan in 2015, Freeman estimates.

Deal making in the country is predicted to grow further in the current year as stressed Indian companies restructure businesses and dispose of assets to bolster their balance sheets.

Last year “was dominated by a few large intra-group restructurings amounting

to over $23 billion of M&A ,” Ravi Kapoor,head of corporate andinvestment banking for Citigroup in India said in an e-mail. Citi advised 13 announced deals valued at about $8 billion in 2015, most of which were focused on M&A transactions between unrelated parties aggregating about $6 billion, he said.

"Stressed companies selling off assets and restructuring operations remains flavor of the season and we have an edge over foreign firms there,” Kampani said.

REAL ESTATE

India M&A Deal Count Rose to a Record in 2015

March 28, 2016 Bloomberg Brief Economics Asia 12

REAL ESTATE

Goldman-Backed 'Nimble Gorilla' Targets Distressed Assets BY BHUMA SHRIVASTAVA,BLOOMBERG NEWS

Ajay Piramal is a man on a shopping mission. His firms are training their sights on distressed assets discarded by indebted businesses and banks struggling with bad loans.

His unlisted real estate unit, recently flush with cash from Warburg Pincusand , is looking to buy Goldman Sachsland parcels from distressed developers, a month after Piramal Enterprisesannounced a $893 million fund to buy soured loans. The group’s investment arm is financing builders, who in turn can buy or co-develop projects with their troubled peers.

“My father says we should be like a nimble gorilla so you are able to move quickly, but at the same time you should have the capital to move,” Anand

, the group’s executive director Piramaland scion who manages the real estate business, said in an interview in Mumbai. “It’s a good time to be in the market.”

Rich pickings may come through for the Piramal conglomerate as Indian developers’ cash flow from operations fall short of their finance costs and lenders, desperate to recover dues, tighten screws demanding repayment. Saddled with distressed assets at a 14-year high, banks in Asia’s third-largest economy have reported record losses amid pressure from regulators to clean up.

Piramal Realty will “look at good, prime parcels of land with a clean title” from distressed developers and is already in talks for as many as five deals, Piramal said. Disputes over land ownership are common in India, with cases dragging because of litigation for decades.

Sellers are becoming “more amenable now” toward deals to overcome financial stress, which may continue for another year at least, Piramal said. “Capital is always a source of competitive advantage.”

Goldman Sachs acquired a minority stake in the company for $150 million in August, about a month after Warburg Pincus pumped in 18 billion rupees ($268 million). The company has about 10 million square feet under development in

Mumbai and plans to invest 160 billion rupees in the next four years.

Builders are selling assets as they streamline operations driven by both strategy and distress, according to

managing director for Shobhit Agarwal,capital markets at property broker Jones

. “Developers are Lang LaSalle Indiaturning to these big boys because they have both the money and the market trust to make sales plus command a premium,” Agarwal said.

As smaller local builders struggle with byzantine approvals processes, high cost of financing, dwindling sales and drying cash flows, private equity firms are stepping in, lured by the prospect of acquiring property at deep discounts from down-and-out developers.

KKR said last month that it will invest in two Mumbai projects by . Sunteck RealtySingapore sovereign wealth fund in GICDecember invested 19.9 billion rupees in a joint-venture housing project in central Delhi with India’s largest developer, .DLF

Piramal Fund Management, the family’s real-estate funding vehicle, is distributing as much as 150 billion rupees to about 10 developers that are in a position to buy land or collaborate with

struggling competitors.The listed Piramal Enterprises

announced setting up a 60 billion-rupee Piramal India Resurgent Fund with the specific mandate of acquiring soured loans, according to a post-earnings presentation in February. Piramal declined to share any details about the new fund or the sectors it’ll focus on.

Lenders struggling to recover soured loans have weighed on credit in the India. Loans to commercial real estate segment grew 5.9 percent to 1.7 trillion rupees in 2015, less than half of the 14.8 percent growth the year earlier, data compiled by the Reserve Bank of India.

RBI Governor has Raghuram Rajanset banks a March 2017 deadline to tidy their balance sheets while India’s top court directed the RBI last month to share a list of the country’s largest defaulters in the past five years.

“The squeeze is also coming in because of the banks,” Piramal said. “If banks are able to push developers to accept more reasonable valuations, then groups like us can step in. I think it’s happening.”

— With assistance from Anto Antony, Pooja

Thakur and Sterling Wong

VENTURE CAPITAL

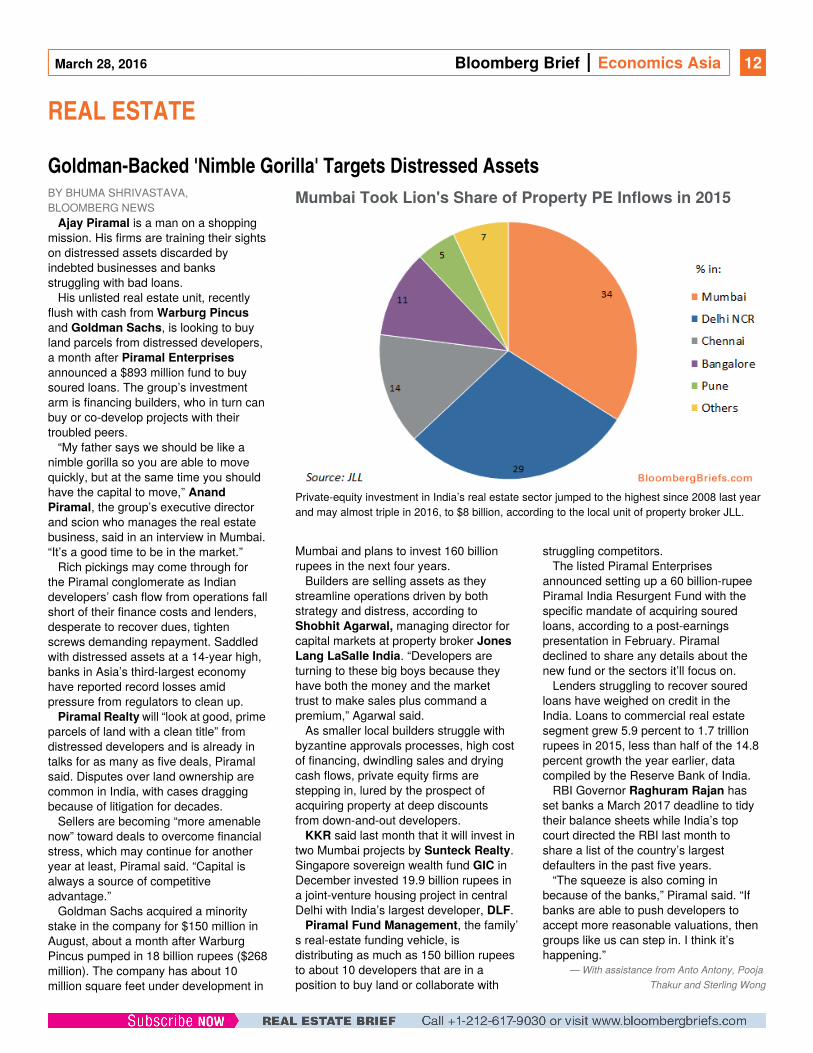

Mumbai Took Lion's Share of Property PE Inflows in 2015

Private-equity investment in India’s real estate sector jumped to the highest since 2008 last year and may almost triple in 2016, to $8 billion, according to the local unit of property broker JLL.

March 28, 2016 Bloomberg Brief Economics Asia 13

VENTURE CAPITAL

Flipkart's Mark-Down Augurs Lean Times for Tech StartupsBY SARITHA RAI, BLOOMBERG NEWS

Cash-hungry Indian startups like FlipkartPvt. are discovering the fundraising party’swinding down.

The e-commerce company became one of the most prominent Asian startups to have its valuation slashed by a high-profileinvestor. Sending ripples through the industry, a Morgan Stanley fund marked down its value by more than a quarter to $11 billion, less than a year after the company clinched a $15 billion valuation.

That’s an unexpected setback for Flipkart: it’s currently seeking to raise about $1 billion, according to a person familiar with the matter. India’s top online retailer by sales is the largest of a crop of startups craving capital to battle Amazon.com Inc. and Snapdeal for a slice of the world’s second-most populous country. It didn’t respond to an e-mail requesting comment.

Beyond eight-year-old Flipkart,entrepreneurs and venture capital investors are bracing for leaner times and more down-to-earth valuations after two years of frenzied deal-making. A deceleration in funding could in turn quicken the failure rate among smaller, ill-prepared startups.

“The global market is seeing several flat or down rounds. There is no doubt that there will be more discussions and pressure around valuation of Indian startups, given what Morgan Stanley recently did,” said Ash Lilani, co-founder and managing partner of venture firm Saama Capital, which has backed startups including Snapdeal and Paytm Mobile Solutions Pvt. It’s since exited Snapdeal.

“Only the strongest will survive. The weak — those who do not have a solid business model but still managed to raise money — will wither away,” he said. “The companies with the right model, the leaders in the pack will continue to raise money but at realistic levels.”

Smaller startups are already feeling the heat as “investors sit on their hands,” said Ravi Gururaj, founder and chief executive officer of digital locker startup QikPod, backed by Flipkart among others.

Largest VC Fundraisings in India Dominated by Flipkart

DATE COMPANY LEAD VC(S) RAISED ($m)

July 29, 2014 Flipkart GIC Pte Ltd 1,000

Dec. 21, 2014 Flipkart Qatar Investment Authority 700

July 27, 2015 Flipkart Steadview Capital Management 700

Aug.18, 2015 Jasper Infotech (Snapdeal) Alibaba Group Holding, Foxconn Technology Group 500

Sept. 15, 2015 ANI Technologies (Ola) Falcon Edge Capital LP 500

April 16, 2015 ANI Technologies (Ola) DST Global 400

July 10, 2013 Flipkart Sofina SA 360

Oct. 27, 2015 ReNew Power Ventures Abu Dhabi Investment Authority 265

Oct. 28, 2014 ANI Technologies (Ola) SoftBank Group Corp 210

May 26, 2014 Flipkart DST Global 210Source: Bloomberg

Companies that are burning cash fast will have to tighten their belts and re-position. “There is going to be a market detox. It is a healthy sign.”

Investment in Indian technology firms had slowed from the peaks of 2015 even before the filing in which the same Morgan Stanley fund also marked down other prominent holdings like lodging service Airbnb Inc. and Dropbox Inc. Deals fell 46 percent and venture investment slid 18 percent in the final three months of 2015 from the previous quarter, when Indian startups raised $1.5 billion via 114 deals, according to CB Insights and KPMG.

That mirrored a global slump. Venture investment in startups around the world dropped about 30 percent in the fourth quarter compared with the previous one, according to CB Insights. And there was an increase in “down rounds,” when funds are raised at a lower valuation than in previous financings. During the last three months of the year, 26 percent of mature startups raised money at lower valuations than in earlier rounds, according to a study by law firm Fenwick & West LLP.

“Clearly, the euphoric times are over and we are now moving into a consolidation phase,” said Vishal Gondal, CEO and founder of Mumbai-based GOQii, which makes wearable fitness bands and was one of the few to get

funding recently: $13.4 million from investors including China’s Cheetah Mobile. “It is now about the survival of the fittest.”

Indian startups have enjoyed an unprecedented funding boom over the past two years as global investors vied to grab a piece of a rapidly growing economy with a surging mobile population. The country has overtaken the U.S. in smartphone usage with about 220 million users, according to Counterpoint Research.

Much of the mania has centered on an e-commerce market expected to grow an annual average of 44 percent to $75 billion by 2020 from $12 billion currently, according to Forrester Research. Flipkart has funding from Tiger Global Management and Accel Partners, among others, becoming in 2014 the only Indian startup to have raised $1 billion in a single round. Snapdeal won over Japan’s SoftBank Group Corp. and Alibaba Group Holding Ltd., while Paytm drew Alibaba.

A reality check may be around the corner. Flipkart and Snapdeal — battling Amazon on their home turf — have spent heavily on advertising and deep discounting. Losses at the three companies in the year ending March will come to at least 50 billion rupees ($745 million), Kotak Institutional Equities estimated in a Feb. 5 report.

BUSINESS OF SPORT

March 28, 2016 Bloomberg Brief Economics Asia 14

BUSINESS OF SPORT

A Cricket Tournament That's in a Financial League of its Own BY COLIN SIMPSON, BLOOMBERG BRIEF EDITOR

Many of the world’s top cricketers will gather in India next month to compete in a league that didn’t exist 10 years ago yet now contributes billions of rupees to the country’s economy.

The VIVO Indian Premier League 2016 features eight franchise teams representing cities across the country competing in 60 matches in the explosive Twenty20 short-duration version of the game. The IPL follows on from the ICC World Twenty20, a competition featuring national teams that is currently approaching its climax in India.

Though the IPL season lasts only a few weeks — this year’s tournament runs from April 9 to May 29 — the top-level international players taking part are lavishly rewarded. At February’s player auction, Australian Shane Watson attracted the highest bid, $1.4 million, to play for the Royal Challengers Bangalore team this year.

The players are not the only ones to benefit. A report on the economic impact of last year’s IPL season produced by KPMG Sports Advisory Services found that the event contributed 11.5 billion rupees ($172 million) to India’s GDP. Another report, by the American Appraisal valuation services company, last year put the overall value of the IPL as a business at $3.5 billion, up 9 percent from 2014.

The authors of the KPMG study used an input-output model, a method that takes into account the links between the different parts of an economy. Input-output models involve the use of economic multipliers, factors that determine the total amount of spending generated by an injection of money. Their use is based on the idea that increased spending has knock-on effects that result in even greater total spending.

The direct economic impact of the IPL season, including spending on travel, accommodation, food and beverages, team outfits and equipment, promotional activities and the cost of staging matches, was put at 5.7 billion rupees.

The total output impact — once the multiplier effect of this spending across the Indian economy was taken into account — was 26.5 billion rupees. The

report says three groups drove the economic impact of the competition — spectators, the franchises and the organizers.

"Direct impact creates demand in the supply chain of businesses that are directly engaged with stakeholder groups," says the report, which was commissioned by the Board of Control for Cricket in India, the governing body that runs the league. "The total economic output impact could be expressed as the sum of direct impacts and ripple effects."

"There are plenty of benefits to many industries," Prabhudev Konana, a professor at the University of Texas who has written about the IPL, said in an email. "These include the hospitality, media, garment — from branded T-shirts, et cetera — sectors and some security and cleaning services. State governments benefit from sales tax revenues."

However, he said there were downsides such as increases in traffic congestion and pollution, disruption of day-to-day life in busy cities and security concerns.

Until recently, top-level cricket was always played at a leisurely pace over four or, in the case of the international matches known as "Tests," five days.

This style of play requires batsmen with patience and a mastery of defensive shots. International matches lasting a single day began in 1971, and the first Twenty20 fixture was played in 2003.

Twenty20 matches typically last little more than three hours and entertain spectators with big-hitting thrills and rapid scoring. The first IPL season took place in 2008, and the competition was an immediate hit in a country that is crazy about cricket. Broadcasting and sponsorship cash poured in.

"The IPL has skewed the way domestic cricket is valued in India," according to Lawrence Booth, the editor of Wisden Cricketers’ Almanack, an annual publication that has been chronicling the game since 1864 and is known as the bible of cricket. "Before the IPL, if you were a young Indian cricketer your ambition would probably be to play Test cricket for India. Now with Twenty20, that's where the money is and you’d think as a young player, ’my ambition is to get very rich very quickly so I’m going to practice all the shots that will make me a Twenty20 star’," he said in a phone interview.

The IPL has been dogged bycontroversy — top teams Chennai Super Kings and Rajasthan Royals were last year suspended for two years following an illegal betting and match-fixing scandal.

"The IPL seems to overcome corruption scandals," said Booth. "The players consider it the number one Twenty20 tournament in the world, the money seems endless and the fans just lap it up."

Q&A

The Input-Output Modeling Process

March 28, 2016 Bloomberg Brief Economics Asia 15

Q&A

Opportunity for Hedge Funds in Financials, Agriculture, Says SageOne CIO Vartak

India's new budget creates opportunities in the

financial and agriculture sectors, says Samit

, chief investment officer at Mumbai-based Vartak

Vartak, whose SageOne Investment Advisors.

firm advises Singapore-based Lighthouse

Canton's two India-focused hedge funds, spoke

to Bloomberg's Suzy Waite on March 1.

Q: How do you view the new budget?A: The budget has taken care of a lot of things, like the banking sector. State-run banks have $100 billion worth of non-performing assets. Considering most of these banks are levered 10 or 11 times, even if part of those assets go bad, that's a significant hit to the equity and therefore to the capital adequacy ratio. Recapitalization is needed and the budget will put $4 billion toward public sector banks. In addition, the Reserve Bank of India announced changes in revaluing reserves, foreign assets and deferred tax, which has given banks more room to increase lending. The government's adherence to a strict 3.5 percent fiscal deficit gives the RBI room to reduce interest rates. This is the back-bone of the capex cycle if it has to start in India.

Q: What else did the budget address?A: Rural infrastructure and agriculture. The government is going to help the farmers, the largest population in India, by insuring their crops.

Q: What should the government's priority be at this stage?A: They need to reduce interest rates. Most loans are available at 11 percent to 13 percent, which is really really high. Indian GDP has been around 7 percent with inflation of 7 percent, so the economy has grown at 14 percent on average in the past few decades. With those growth rates, borrowing at 11 to 12 percent is acceptable. But when the economy is growing at 5 percent, very few companies can afford to pay that interest, so why would anyone borrow? Sticking to a strict 3.5 percent of fiscal deficit will help.

Q: What opportunities are there forhedge funds?

A: One is on the financial side. There have been a lot of worries due to the huge amount of non-performing assets. If the non-performing asset issue is resolved, a lot of companies are trading at 0.2 times book and 0.3 times book, so as an investor, that's reduced a huge risk. If the government is able to recapitalize and create demand on the other side, it will solve the issue.

Q: Where are the other opportunities?A: Agriculture. Not many farmers make profits. Either there's a drought or floods which destroys the crop. Now the government will provide farmers protection if their crops are destroyed by covering expenses. A lot of farmers will come forward and start farming. That will impact farming inputs, whether its fertilizer, pesticide or seeds. Another is low-ticket-sized basic necessity items, like cookware and undergarments. Rural housing finance is another way to play these markets once demand starts picking up. The government has announced huge incentives for people who buy a house for below $70,000. The government is also trying to boost affordable housing in rural areas and there are mortgage companies that fund these rural houses that cost $20,000 to $30,000. The risk of non-performing assets is low and the growth is high.

Q: What would you avoid?Any area where there is a lot of A:

government spending but no barriers to entry and huge competition. A lot of funds rushed to invest directly in road building

companies or airport construction companies, and got their hands burned. Our ground research shows there are currently 15 bids for the [National Highway Authority of India] road building engineering procurement and construction project. It is extremely competitive and the pricing is rock bottom, so there is no incentive for road builders. You won't make much money and you are bidding at a level where commodity prices are low.

Q: How do you go short in India?A: There are 7,000 listed stocks in India, and only 173 are available to short, mainly big companies like JP Associates. We find it is much better to short the Nifty 50, which includes commodity players, miners, infrastructure companies, and private and public banks which are funding infrastructure. The Nifty 50 is very liquid, so it's a good short, but you can't expect it to work short-term. As a hedge fund, the biggest issue in India is there is not apples to apples shorting. There are a lot of long opportunities.

Q: Is now a good time to invest in India?A: Current valuations are close to 20 times, which is above average, so we expect further correction over the next six to 12 months. We don't know when it will happen, but given the structural changes the government has done in terms of subsidy flow, financial inclusion and resource allocation, India will be one of the most attractive destinations once these changes start showing results.

Age: 42Hometown: MumbaiProfessional background: PwC Consulting, DeloitteHobbies: Cricket, social work (forestation and supporting primary education in India)Favorite cuisine: Chinese and local MaharashtrianFavorite book: The Power of Positive ThinkingFavorite quote: “Every problem has in it the seeds of its own solution. If you don't have any problems, you don't get any seeds” — Norman Vincent PealeFavorite holiday spot: New York City

March 28, 2016 Bloomberg Brief Economics Asia 16

CONTACTS

Managing Editor

Jennifer Rossa

+1-212-617-8074

Editors

Nathaniel E. Baker

Paul Smith

James Crombie

Jennifer Bernstein

Colin Simpson

Stew Hawkins

Reporter

Suzy Waite

Graphic Designer

Pekka Aalto

Subscribe to the Briefs on the

Bloomberg Terminal at BRIEF<GO>

Bloomberg BriefExecutive Editor

Brian Bremner

Managing Editor

Arijit Ghosh

New Delhi Bureau Chief

Sunil Jagtiani

Mumbai Bureau Chief

Sam Nagarajan

Editors

Daniel Ten Kate

Reporters

Enda Curran

Unni Krishnan

Anto Antony

George Smith Alexander

Divya Patil

Bhuma Shrivastava

Saritha Rai

Subhadip Sircar

Bloomberg NewsDirector of Research – Global

David Dwyer

Director of Research – Asia

Tim Craighead

Economist – India

Tamara Henderson

Read in-depth economic analysis on the

Bloomberg Terminal at BI ECON<GO>

Yvette Romero

Matthew Traum

+1-212-617-4671

Lori Husted

+1-717-505-970

Christopher Konowitz

+1-212-617-4694

Bloomberg Intelligence

Bloomberg Rankings

Economics Terminal Sales

Reprints & Permissions

Advertising

© 2016 Bloomberg LP. All rights reserved. This newsletter and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Please contact our reprints group listed left for more information.

Interested in learning more about the Bloomberg terminal? Contact [email protected] or +91-22-6120-3963 for a free demo.Sunny Chhabria at sc