solid transformation progress in 2016 · pdf fileabb 800xa dcs applications to identify...

TRANSCRIPT

ABB LTD, ZURICH, SWITZERLAND, MARCH 10, 2017, FULL-YEAR AND Q4 2016 RESULTS (RESTATED)

ABB delivers growth in fourth quarterSolid transformation progress in 2016Ulrich Spiesshofer, CEO; Eric Elzvik, CFO

This presentation includes forward-looking information and statements including statements concerning the outlook for ourbusinesses. These statements are based on current expectations, estimates and projections about the factors that may affectour future performance, including global economic conditions, and the economic conditions of the regions and industries thatare major markets for ABB Ltd. These expectations, estimates and projections are generally identifiable by statementscontaining words such as “expects,” “believes,” “estimates,” “targets,” “plans,” “outlook” or similar expressions.

There are numerous risks and uncertainties, many of which are beyond our control, that could cause our actual results to differmaterially from the forward-looking information and statements made in this presentation and which could affect our ability toachieve any or all of our stated targets. The important factors that could cause such differences include, among others:

– business risks associated with the volatile global economic environment and political conditions– costs associated with compliance activities– market acceptance of new products and services– changes in governmental regulations and currency exchange rates, and– such other factors as may be discussed from time to time in ABB Ltd’s filings with the U.S. Securities and Exchange

Commission, including its Annual Reports on Form 20-F.

Although ABB Ltd believes that its expectations reflected in any such forward-looking statement are based upon reasonableassumptions, it can give no assurance that those expectations will be achieved.

This presentation contains non-GAAP measures of performance. Definitions of these measures and reconciliations betweenthese measures and their US GAAP counterparts can be found in the ‘Supplemental reconciliations and definitions’ section of“Financial Information” under “Quarterly results and annual reports” on our website at www.abb.com/investorrelations

Important notices

March 10, 2017 Slide 2

Q4 and full-year 2016 performance

Next Level transformation

Outlook and priorities 2017

March 10, 2017 Slide 3

Agenda

Full-year and Q4 2016

March 10, 20171On a comparable basis; 2Operational EPS growth is in constant currency (2014 foreign exchange rates) ; 3Excluding unique events operational EBITA margin improved 10 bpsSlide 4

FY 2

016

Operational EPS

$1.29+4%2

$3.1 bn+2%

Revenues Free cash flow

$33.4 bn-5%1

$33.8 bn-1%1

12.4 %+50 bps

Operational EBITA margin

Orders

Q4

2016

Operational EBITA margin

11.7 %-20 bps3

Base orders Revenues

$8.3 bn+3%1

$6.9 bn-1%1

$9.0 bn+1%1

Orders

Q4 2016: ABB delivers growth

March 10, 20171On a comparable basis; 2WCP: White Collar Productivity; 3NWC: Net Working Capital Slide 5

Stage 3 of Next Level Strategy launched – committed to unlocking value

Profitable Growth

Relentless Execution

Business-led Collaboration

+3%1 order growth reflects strong orders in Power Grids, strong growth in US & China +9%1

Revenues grew1; positive contribution by Power Grids and Electrification Products

Launched ABB AbilityTM – significant interest, momentum building

Op. EBITA impacted ~30 bps by default of a large distributor and foreign currency losses

Process Automation op. EBITA margin up 130 bps and Power Grids up 90 bps

WCP2 on track to meet $1.3 bn savings; NWC3 as % of revenues reduced 160 bps

Improved country and account collaboration

Global business service centers operational; ramped up >2,500 people

Successful launch of ABB brand campaign

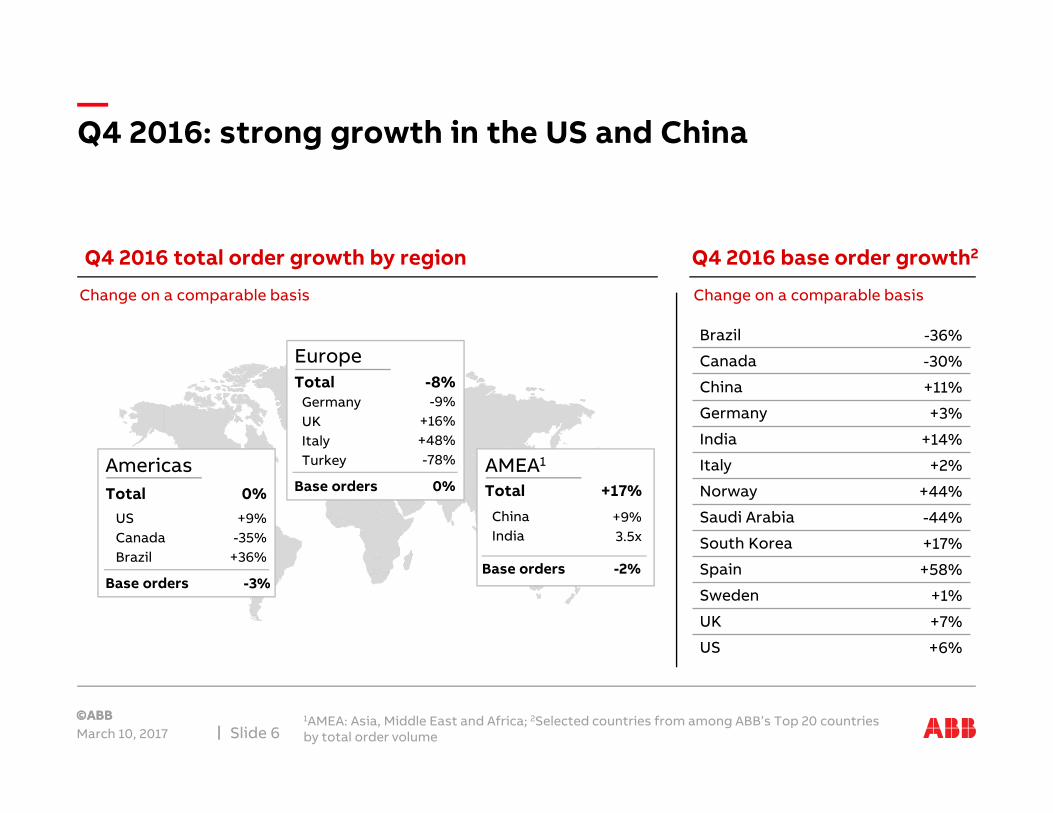

Q4 2016: strong growth in the US and China

March 10, 20171AMEA: Asia, Middle East and Africa; 2Selected countries from among ABB’s Top 20 countries by total order volume Slide 6

Q4 2016 total order growth by region Q4 2016 base order growth2

Change on a comparable basis

Brazil -36%

Canada -30%

China +11%

Germany +3%

India +14%

Italy +2%

Norway +44%

Saudi Arabia -44%

South Korea +17%

Spain +58%

Sweden +1%

UK +7%

US +6%

Change on a comparable basis

Americas

Base orders

USCanadaBrazil

Total+9%

-35%+36%

ChinaIndia

+9%3.5x

Europe

Base orders

GermanyUKItalyTurkey

Total-9%

+16%+48%-78%

-3%

0%

AMEA1

0%

-8%

Base orders

Total

-2%

+17%

Q4 2016: Power Grids orders

March 10, 2017 UHVDC: Ultra-High-Voltage Direct Current; HVDC: High-Voltage Direct CurrentSlide 7

>$840 million, 3 continents

India USA Brazil Philippines

Raigarh-Pugalur 800kV Sylmar converter station Pacific Intertie power link

National Grid Corp of Philippines

Belo Monte

UHVDC system India

Integrate renewable & conventional power over long distances at low losses

Upgrade HVDC station includes ABB AbilityTM to monitor, control & protect

Advanced fault registration & remote control

Design, supply & commission transformers

Support power infrastructure upgrade

800kV ultra-high voltage converter transformers

Integrate clean power from hydro over long distance

Reliable, efficient electricity to 80 mn people

Improves operational efficiency and reliability

Improve grid reliability and increase power capacity

Efficient and safe UHVDC conversion with low losses

$75 mn$640 mn $100 mn $27 mn

Key figures

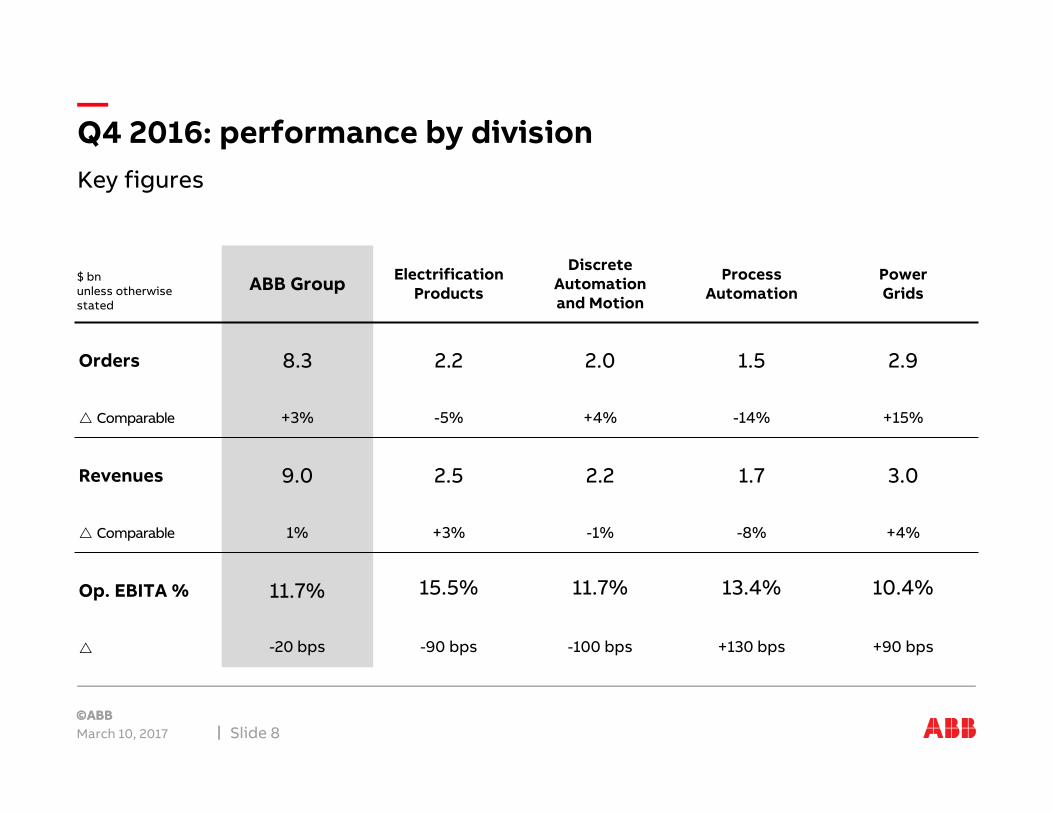

Q4 2016: performance by division

March 10, 2017 Slide 8

ABB Group Electrification Products

Discrete Automation and Motion

Process Automation

Power Grids

Orders 8.3 2.2 2.0 1.5 2.9

Comparable +3% -5% +4% -14% +15%

Revenues 9.0 2.5 2.2 1.7 3.0

Comparable 1% +3% -1% -8% +4%

Op. EBITA % 11.7% 15.5% 11.7% 13.4% 10.4%

-20 bps -90 bps -100 bps +130 bps +90 bps

$ bnunless otherwise stated

Net savings

Net volume

OtherProject margins

Mix ForexOp. EBITAQ4 2015

Op. EBITAQ4 2016

Q4 2016: Operational EBITA margin bridge

March 10, 2017 Slide 9

Operational EBITA bridge Q4 2015 to Q4 2016, $ mn

11.9% op. EBITA margin

11.7% op. EBITA margin

1,057

+32-21

-8 -132+111 -26

(e.g. Distributor

default; operational

currency losses)

1,0571,101

Large distributor default and Egyptian currency losses impacted op. EBITA margin ~30 bps

Q4 2016: Operational EBITA to net income bridge

March 10, 2017 = indicating against expectationsSlide 10

Q4

2016

1,057

Q4

2015

425

-68-38

-67

-92-73

+13-54 -12

-47

-194

PPA amortization

Op. EBITA

Restructuring related

Changes in pre-acquisition

estimates

Non-operational

Pension

South Korea

Finance netOther Disc. ops & minority interest

Net income

FX/ timing

differences

Tax

1,101

204

-531-73

-8 -12-54

-76-42 -35-66

0

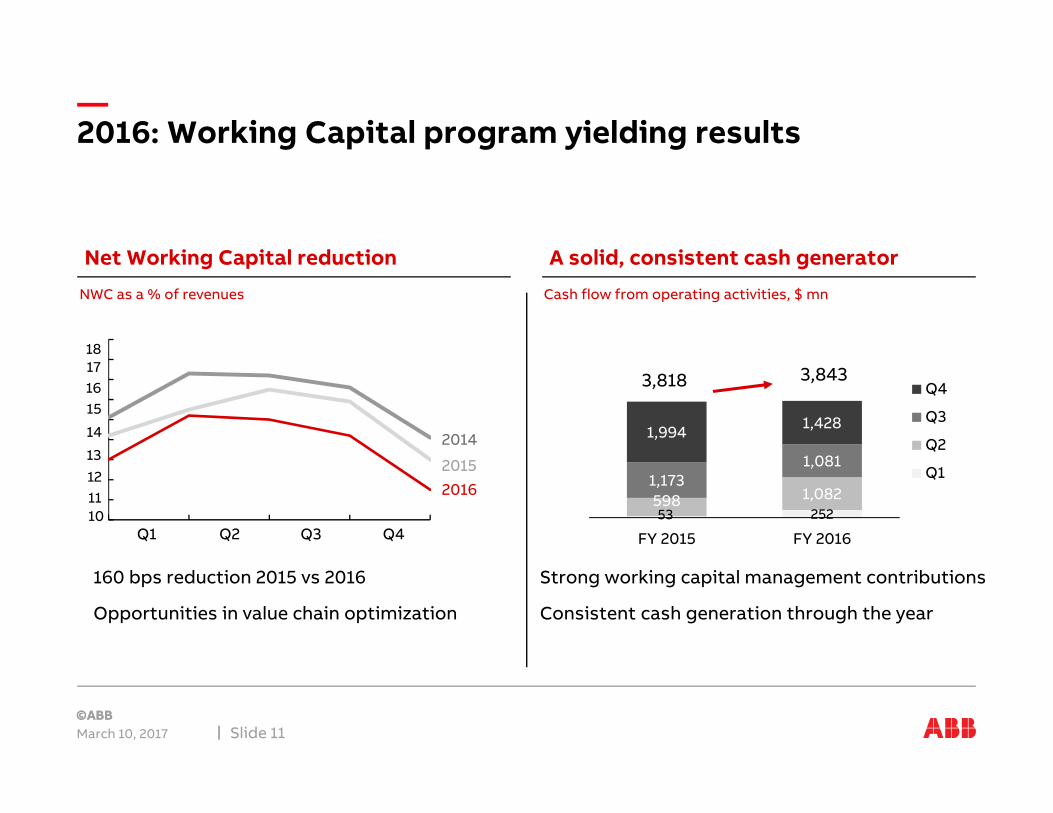

2016: Working Capital program yielding results

March 10, 2017 Slide 11

Net Working Capital reduction A solid, consistent cash generator

15

14

13

181716

101112

Q2 Q3 Q4

2014

20152016

Q1

NWC as a % of revenues

53 252598 1,082

1,1731,081

1,994 1,428

0

1000

2000

3000

4000

5000

FY 2015 FY 2016

Q4

Q3

Q2

Q1

Strong working capital management contributions

Consistent cash generation through the year

Cash flow from operating activities, $ mn

3,8433,818

160 bps reduction 2015 vs 2016

Opportunities in value chain optimization

Next Level transformation

March 10, 20171PIE: Penetration, Innovation, Expansion; 2F&B: Food and BeverageSlide 12

Growth momentum building (i.e. PIE1) in key markets

Double digit growth in F&B2, robotics

Launch of ABB AbilityTM, 3 partnerships

Strategic portfolio review Power Grids completed

Power Grids transformation delivered

Delivered +$1 bn normal cost savings

Delivered ~$550 mn of WCP gross savings

Reduced working capital ~$550 mn

>70k people on performance / compensation system

Simpler, customer-focused organization

Unified brand and brand migration

Lack of organic growth focus

Underperforming units

Fat, inefficient white collar organization

Inadequate cash culture

Static, lack of accountability

Complex organizational setup

Fragmented brand landscape

Starting point 2013 2016 achievements

Profitable Growth

Relentless Execution

Business-led Collaboration

ABB ready to deliver on growth – Next Level Stage 3

Four actions

Next Level Stage 3 – committed to unlocking value

March 10, 2017 Slide 13

Delivering attractive shareholder returns

Business-led Collaboration

2

4

Profitable Growth

Accelerating momentum in operational excellence

1

Relentless Execution 3

Strengthening the global ABB brand

Driving growth in four market-leading entrepreneurial divisions

Quantum leap in digital

ANNOUNCED OCTOBER 4TH, 2016

Operational as of January 1, 2017

Four market-leading entrepreneurial divisions

March 10, 2017 Slide 14

1

Electrification Products

g g

Robotics and Motion

Industrial Automation

Power Grids

…electrification of all consumption points

…robotics and intelligent motion solutions

…industrial automation

…a stronger, smarter and greener grid

Partner of choice for… Actions ….

Combine all electrification components Investment in growth platforms (renewables, EV charging, power quality)

Simplified and focused portfolio Driving growth in robotics

Driving digitalization across industry sectorsDriving service offering

Focus on high growth, digitalization, “Power Up” transformationPrune niche non-core & grow with de-risked business model

Position

#2 in electrification

#1 in motion

#2 in robotics

#1 in process control

#1 in T&D

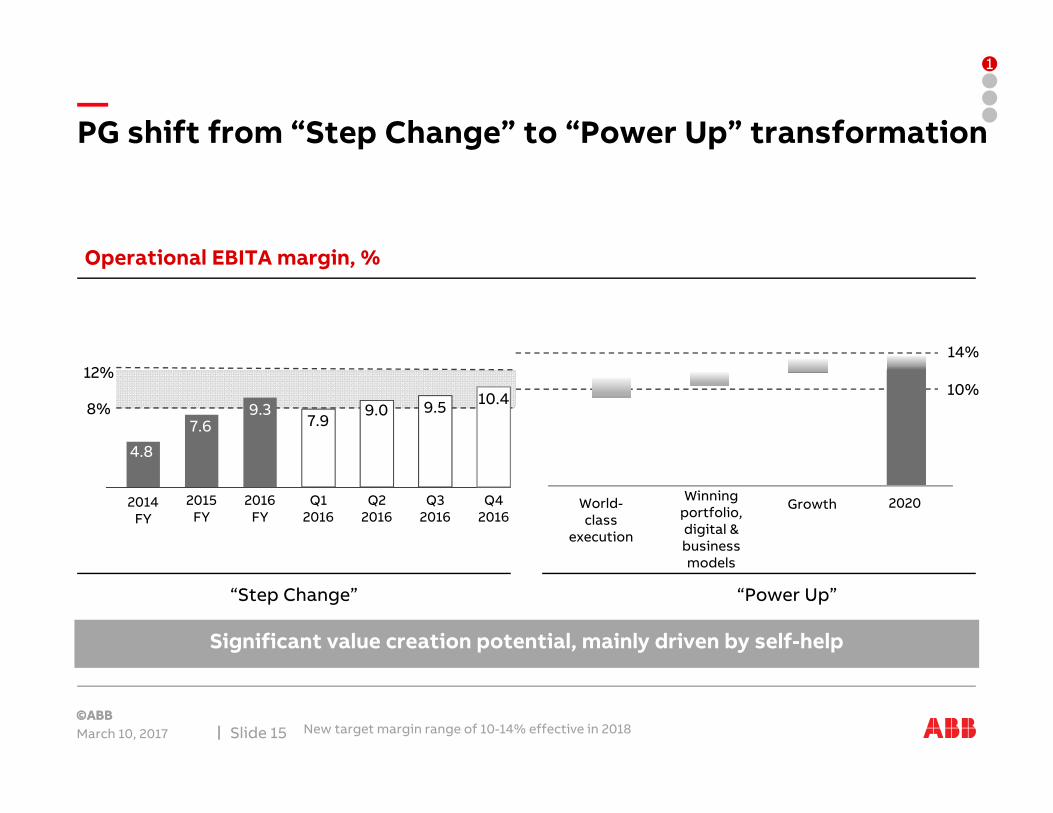

PG shift from “Step Change” to “Power Up” transformation

March 10, 2017 New target margin range of 10-14% effective in 2018Slide 15

Significant value creation potential, mainly driven by self-help

2020Growth2015 FY

Q1 2016

Winning portfolio, digital & business models

World-class

execution

Q22016

Q32016

Q42016

Operational EBITA margin, %

2016 FY

“Step Change” “Power Up”

1

10%12%

8%7.6

9.07.9

9.5 10.49.3

2014 FY

4.8

14%

One common offering for digital end-to-end solutions

Quantum leap in digital: launch of ABB AbilityTM

March 10, 2017 Slide 16

Digital ABB offering across all businesses

2

Driving growth by:

Integrating

Penetrating

Replicating

ABB AbilityTM – creating value for customers

March 10, 2017 Slide 17

2

Leading robot simulation & offline programming software

Virtual commissioning

Discrete manufacturing processes across major verticals

Reduced risk, shorter installation time,

elimination of down-time

ABB 800xA DCS

Applications to identify problems, adapt software

& control strategy

Identify mechanical issues

Extensive O&G domain expertise with control system

Faster commissioning and operational efficiency

Wireless communication network aggregating multiple

applications through an integrated digital

distribution system

Global market leader in grids

Deliver safe, reliable power and reduce end customers’

energy consumption

Robot Studio (14,000 users/week)

Ormen Lange gas field, Norske Shell

Central Hudson Gas & Electric Distribution Grid, USA

Digital solution

Domain expertise

Customer value

Plan / design Build Operate

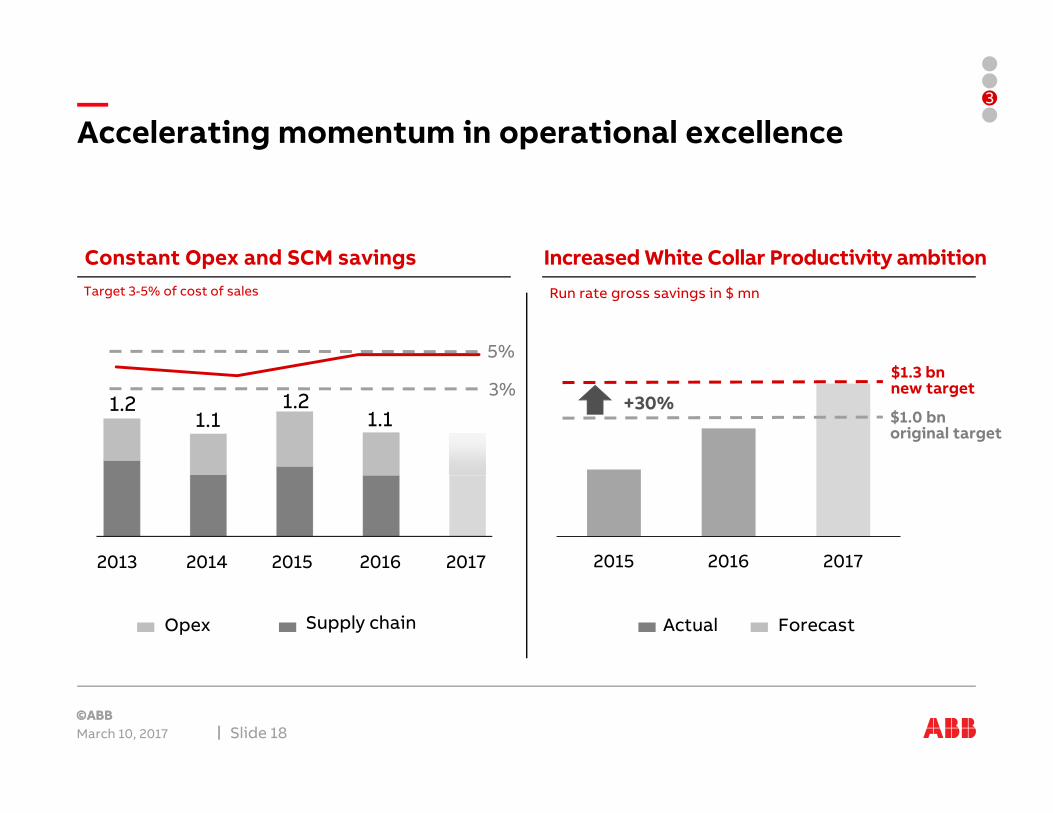

Accelerating momentum in operational excellence

March 10, 2017 Slide 18

3

Run rate gross savings in $ mn

Constant Opex and SCM savings Increased White Collar Productivity ambition

1.2

Supply chainOpex

1.21.1

2013 2014 2015 2016

1.1

2015 2016 2017

$1.0 bnoriginal target

$1.3 bnnew target

+30%

Actual Forecast

3%

5%

Target 3-5% of cost of sales

2017

0.71.5 1.3

3.0

2014 2015 2016 2017-201

11.6%

12.7%13.4%

13.8%

2013 2014 2015 2016

Returned $2.9 bn of cash to shareholders in 2016

Committed to delivering attractive shareholder returns

March 10, 20171Planned; 2Dividend divided by year end share priceSlide 19

in $ bn

Improved free cash flow, strong cash conversion

Share repurchase volume

2.6 2.9

94% 110%156% 161%

2013 2014 2015 2016

Dividend per share (CHF)

Dividend yield2

0.73.7% 3.6% 3.0% 3.4% 4.1%

2011 2012 2013 2014 2015 2016

0.7

4

0.7

2

0.7

0

0.6

8

0.6

5 0.7

6

3.5%

3.0 3.1

Jan’16 Mar’17

Share price

Improving cash return on investment

15

20

25

Outlook – short term market conditions

March 10, 20171Including automotive, food & beverage, machinerySlide 20

Pioneering technology

Utilities Industry Transport & Infrastructure

Globally

T&D: positive drivers, policy support

Solar and Wind: continued growth

Conventional Power: fewer coal capacity additions, gas stable

Discrete & hybrid industries1: investment remains positiveOil & Gas: bottoming onshore, further decline offshoreMining & metals: persistent overcapacity, bulk metal capacity clean-up

Transportation: rail growing, specialty ships strong, cargo vessels challenged

Construction: solid with downside risk

China: growth in T&D, robotics and buildings, process difficult

India: growth across sectors

Middle East: political instability. Infrastructure challenges

US: T&D positive, industrials remain mixed, political uncertainty

Canada: stable; O&G bottoming

Brazil: Flat off of severe contraction

Northern & Central Europe: moderate growth overall, impact of Brexit 2017

Southern Europe: mixed, strong growth in Spain, Italy slow, Turkey affected by political events

Africa, Middle East and Asia Americas Europe

2017 priorities

March 10, 2017 Slide 21

Profitable Growth

Relentless Execution

Business-led Collaboration

Drive organic growth through PIE, expand technology leadership

Drive ABB AbilityTM momentum through customer base and within every business unit

Ready for disciplined inorganic moves and partnerships

Deliver White Collar Productivity and Working Capital programs

Drive Leading Operating Model, Supply Chain Management and Quality programs

Live new performance culture and performance systems

Tap “growth collaboration” opportunities in countries and accounts

Drive high performance culture with newly shaped organization and leadership team

Continue strengthening the global ABB brand

Why own ABB

March 10, 2017 Slide 22

Pioneering technology leader

Strong positions in attractive markets

Efficient balance sheet; generating attractive returns for shareholders

Clear transformation agenda driving operational EPS and CROI

Committed to unlocking value

Key figures Q4 2016

March 10, 2017 Slide 24

Q4 2016 Q4 2015 Change

$ mn unless otherwise indicated $ Local currency Comparable

Orders 8,277 8,262 0% +2% +3%Order backlog (end December) 22,981 24,121 -5% -2% -1%

Revenues 8,993 9,242 -3% 0% +1%

Operational EBITA 1,057 1,101 -4% -2%

as % of operational revenues

11.7% 11.9% -0.2 pts.

Income from operations 678 347 +95%

as % of revenues 7.5% 3.8% +3.7 pts

Net income 425 204 +108%Basic earnings per share ($) 0.20 0.09 +115%

Cash flow from operating activities 1,428 1,994 -28%

Key figures 2016

March 10, 2017 Slide 25

FY 2016 FY 2015 Change

$ mn unless otherwise indicated $ Local currency Comparable

Orders 33,379 36,429 -8% -5% -5%Order backlog (end December) 22,981 24,121 -5% -2% -1%

Revenues 33,828 35,481 -5% -2% -1%

Operational EBITA 4,191 4,209 0% +2%

as % of operational revenues

12.4% 11.9% +0.5 pts.

Income from operations 2,897 3,049 -2%

as % of revenues 8.8% 8.6% +0.2 pts

Net income 1,899 1,933 -2%Basic earnings per share ($) 0.88 0.87 +2%

Cash flow from operating activities 3,843 3,818 +1%

Third party base orders by division

March 10, 2017 Slide 26

Q4 2016 Q4 2015 % Change

Third-party base orders $ mn Comparable

Electrification Products 2,051 2,158 -2%

Discrete Automation and Motion 1,820 1,779 +5%

Process Automation 1,285 1,309 0%

Power Grids 1,692 1,864 -7%

Corporate and Other 12 12

Total Group 6,860 7,122 -1%

Order backlog by division

March 10, 2017 Slide 27

Q4 2016 Q4 2015 Change

Order backlog (end December) $ mn $ Comparable

Electrification Products 2,612 2,872 -9% -5%

Discrete Automation and Motion 4,078 4,232 -4% 0%

Process Automation 5,258 6,036 -13% -10%

Power Grids 12,437 12,502 -1% +4%

Corporate and Other(incl. Inter-division eliminations)

-1,404 -1,521

Total Group 22,981 24,121 -5% -1%

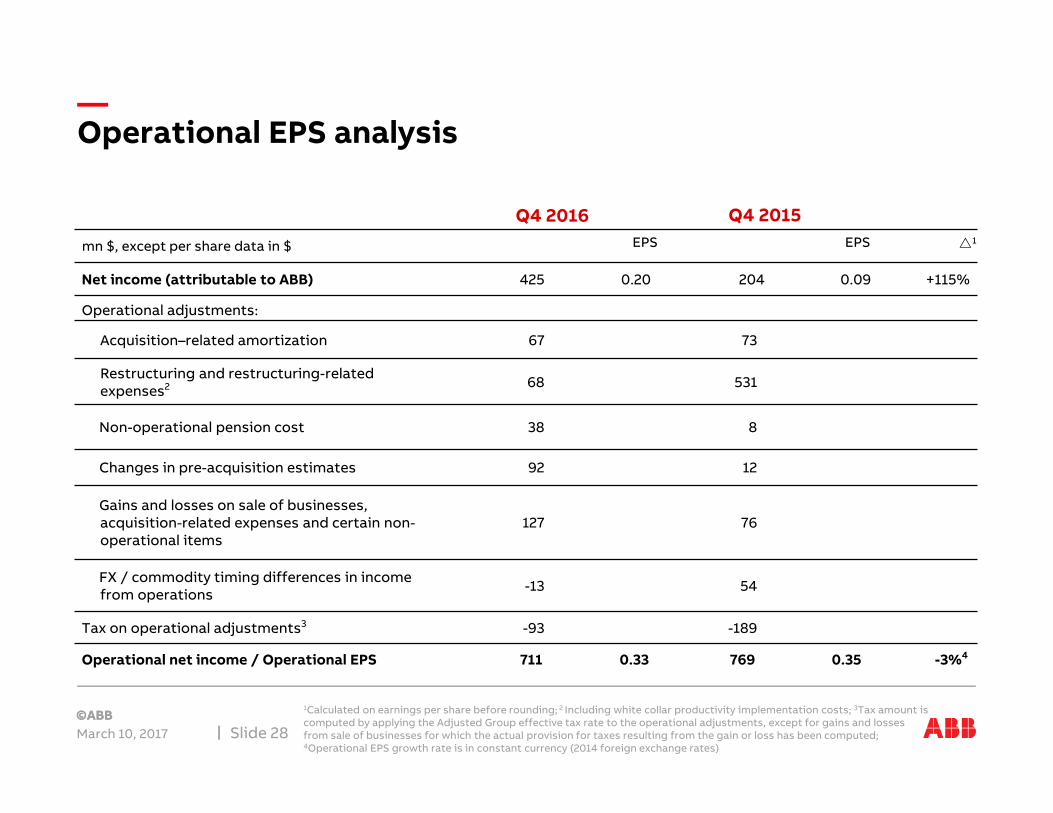

Operational EPS analysis

March 10, 2017

1Calculated on earnings per share before rounding; 2 Including white collar productivity implementation costs; 3Tax amount is computed by applying the Adjusted Group effective tax rate to the operational adjustments, except for gains and losses from sale of businesses for which the actual provision for taxes resulting from the gain or loss has been computed; 4Operational EPS growth rate is in constant currency (2014 foreign exchange rates)

Slide 28

Q4 2016 Q4 2015mn $, except per share data in $ EPS EPS 1

Net income (attributable to ABB) 425 0.20 204 0.09 +115%

Operational adjustments:

Acquisition–related amortization 67 73

Restructuring and restructuring-related expenses2 68 531

Non-operational pension cost 38 8

Changes in pre-acquisition estimates 92 12

Gains and losses on sale of businesses, acquisition-related expenses and certain non-operational items

127 76

FX / commodity timing differences in income from operations -13 54

Tax on operational adjustments3 -93 -189

Operational net income / Operational EPS 711 0.33 769 0.35 -3%4

Operational EPS analysis – full year

March 10, 2017

1Calculated on earnings per share before rounding; 2 Including white collar productivity implementation costs; 3Tax amount is computed by applying the Adjusted Group effective tax rate to the operational adjustments, except for gains and losses from sale of businesses for which the actual provision for taxes resulting from the gain or loss has been computed; 4Operational EPS growth rate is in constant currency (2014 foreign exchange rates)

Slide 29

FY 2016 FY 2015mn $, except per share data in $ EPS EPS 1

Net income (attributable to ABB) 1,899 0.88 1,933 0.87 +2%

Operational adjustments:

Acquisition–related amortization 279 310

Restructuring and restructuring-related expenses2 543 674

Non-operational pension cost 38 19

Changes in pre-acquisition estimates 131 21

Gains and losses on sale of businesses, acquisition-related expenses and certain non-operational items

173 120

FX / commodity timing differences in income from operations 40 16

Tax on operational adjustments3 -320 -295

Operational net income / Operational EPS 2,783 1.29 2,798 1.26 +4%4

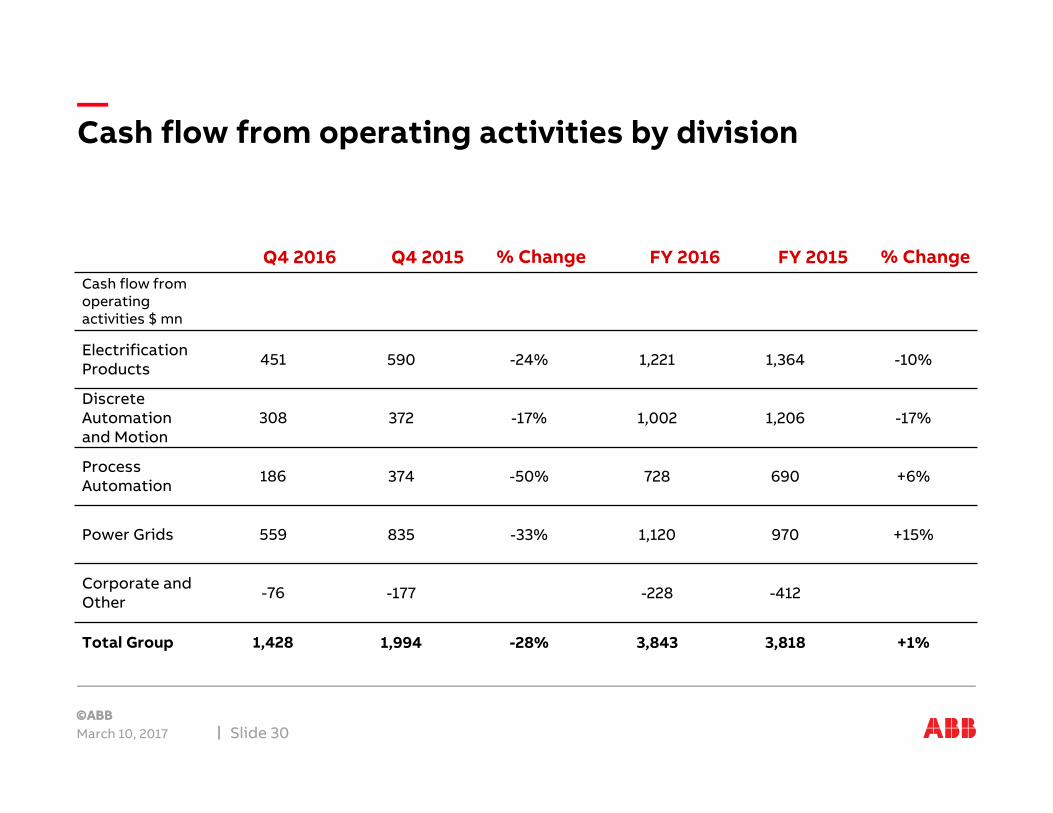

Cash flow from operating activities by division

March 10, 2017 Slide 30

Q4 2016 Q4 2015 % Change FY 2016 FY 2015 % ChangeCash flow from operating activities $ mn

Electrification Products 451 590 -24% 1,221 1,364 -10%

Discrete Automation and Motion

308 372 -17% 1,002 1,206 -17%

Process Automation 186 374 -50% 728 690 +6%

Power Grids 559 835 -33% 1,120 970 +15%

Corporate and Other -76 -177 -228 -412

Total Group 1,428 1,994 -28% 3,843 3,818 +1%

Status 2015 – 2020 financial targets

Group Targets

March 10, 2017

1Average annual revenue growth on a like-for-like basis over 6 years, base year 2014; 2Target is on a full-year basis; 3CAGR = Compound annual growth rate, base year is 2014 and assuming constant exchange rates; 4Temporary reduction possible in the event of larger acquisitions

Slide 31

Status as of December 2016 unless otherwise stated Group Status

Revenue growth1 3 – 6% 0%

Operational EBITA %2 11 – 16% 12.4%

Operational EPS growth CAGR3 10 – 15% 4%

FCF conversion to net income >90% 161%

CROI %4 Mid-teens 14.1%

White Collar Productivity program costs

March 10, 2017 Slide 32

$ mn

Originalguidance

New guidance 2015 2016 2017

Total Cost 1,200-1,250

1,020-1,070 420 370 ~230

Restructuring and related expenses 850-900 ~520 370 140 ~10

Program implementation 350 500 50 230 220

$ mn Original target

New target 2015 2016 2017 2018

Gross savings (run rate end of 2017) 1,000 1,300

Gross savings (incremental y-o-y) ~25 >550 450 300

Q4 2016

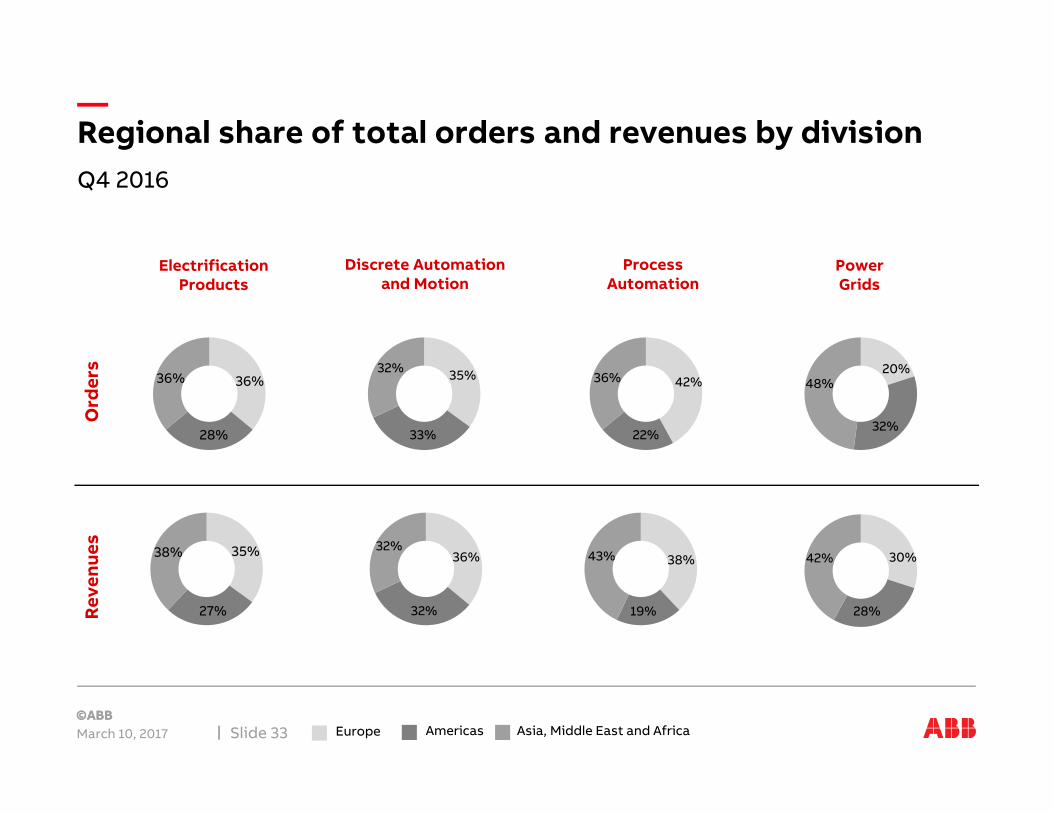

Regional share of total orders and revenues by division

March 10, 2017 Slide 33

Ord

ers

Reve

nues

Electrification Products

36% 36%

28%

38% 35%

27%

Discrete Automation and Motion

32% 35%

33%

32%36%

32%

Process Automation

36% 42%

22%

43% 38%

19%

Power Grids

48%20%

32%

42% 30%

28%

Europe Americas Asia, Middle East and Africa

Q4 2016

Electrification Products

March 10, 2017 Slide 34

Ord

ers

Total orders reflects lower large orders in the systems business compared with the same period a year ago. Positive order development in China and India could not offset declines in the US, Canada and the United Kingdom.

Op.

EB

ITA

&

mar

gin

Operational EBITA margin was impacted by the default of a Turkish distributor and Egyptian operational currency losses resulting collectively in a 90 basis points decline to 15.5 percent. Excluding these charge operational EBITA margin would have been steady in the quarter.

Reve

nues

Revenues grew 3 percent in the quarter as a result of the execution of the systems backlog and higher demand in building products.

In $ mn, y-o-y change comparable

1 2

-5%

2,340 2,157

Q4 2015 Q4 2016

1 2

+3%

2,459 2,462

Q4 2015 Q4 2016

1 2

15.5%

403 382

16.4%

Q4 2015 Q4 2016

Q4 2016

Discrete Automation & Motion

March 10, 2017 Slide 35

Total orders grew 4 percent as continued strong demand patterns in robotics and light industry more than offset the impacts from capex declines in process industries such as oil and gas.

Operational EBITA margin declined 100 basis points compared with the same quarter a year ago mainly impacted by lower margins in solar, unfavorable mix and low capacity utilization.

Revenues were steady reflecting order execution and strong demand from light industries.

In $ mn, y-o-y change comparable

1 2

+4%

1,984 2,013

Q4 2015 Q4 2016

1 2

-1%

2,288 2,211

Q4 2015 Q4 2016

1 2

11.7%

291 260

12.7%

Q4 2015 Q4 2016

Ord

ers

Op.

EB

ITA

&

mar

gin

Reve

nues

Q4 2016

Process Automation

March 10, 2017 Slide 36

Total orders were 14 percent lower as a result of continued capital expenditure reduction in the process industries.

Operational EBITA margin increased 130 basis points to 13.4 percent due to positive mix and successfully implemented cost reduction and productivity measures.

Revenues declined 8 percent as higher service revenues could not offset declines in mining and oil and gas.

In $ mn, y-o-y change comparable

1 2

-14%

1,796 1,520

Q4 2015 Q4 2016

1 2

-8%

1,926 1,737

Q4 2015 Q4 2016

1 2

13.4%

235 231

12.1%

Q4 2015 Q4 2016

Ord

ers

Op.

EB

ITA

&

mar

gin

Reve

nues

Q4 2016

Power Grids

March 10, 2017 Slide 37

Total orders were 15 percent higher compared with the same quarter a year ago due to a significant increase in large contract awards.

Operational EBITA margin increased by 90 basis points to 10.4 percent, mainly driven by higher revenues, improved productivity, solid project execution and continued cost savings.

Revenues increased 4 percent due to steady execution of a healthy order backlog.

In $ mn, y-o-y change comparable

1 2

+15%

2,628 2,879

Q4 2015 Q4 2016

1 2

+4%

3,107 3,042

Q4 2015 Q4 2016

1 2

10.4%

293 318

9.5%

Q4 2015 Q4 2016

Ord

ers

Op.

EB

ITA

&

mar

gin

Reve

nues

Q1 2016 Proforma – new structure

March 10, 2017 Note: best estimate, subject to changeSlide 38

ABB Group Electrification Products

Roboticsand Motion

Industrial Automation

Power Grids

Orders($ mn) 9,253 2,506 2,088 1,838 3,307

Revenues($ mn) 7,903 2,289 1,873 1,664 2,518

Operational EBITA($ mn)

951 307 286 202 198

Operational EBITA margin (%)

12.1% 13.5% 15.3% 12.0% 7.9%

FY 2016 Proforma – new structure

March 10, 2017 Note: best estimate, subject to changeSlide 39

ABB Group Electrification Products

Roboticsand Motion

Industrial Automation

Power Grids

Orders($ mn) 33,379 9,775 7,868 6,041 11,232

Revenues($ mn) 33,828 9,916 7,915 6,778 10,975

Operational EBITA($ mn)

4,191 1,458 1,224 865 1,021

Operational EBITA margin (%)

12.4% 14.7% 15.4% 12.7% 9.3%

FY 2015 Proforma – new structure

March 10, 2017 Note: best estimate, subject to changeSlide 40

ABB Group Electrification Products

Roboticsand Motion

Industrial Automation

Power Grids

Orders($ mn) 36,429 10,606 8,285 7,525 12,205

Revenues($ mn) 35,481 10,272 8,201 7,431 11,621

Operational EBITA($ mn)

4,209 1,519 1,290 908 877

Operational EBITA margin (%)

11.9% 14.8% 15.7% 12.2% 7,6%

More information available at ABB Investor Relations

March 10, 2017 Slide 41

Name Telephone E-Mail

Alanna AbrahamsonHead of Investor Relations +41 43 317 3804 [email protected]

Beat Fueglistaller +41 43 317 4144 [email protected]

Ruth Jaeger +41 43 317 3808 [email protected]