social security anna’s baseshop training for financial professional use only

TRANSCRIPT

Social Security

Anna’s Baseshop Training

For Financial Professional use only

Life Expectancy Considerations

Life Expectancy Upon Retirement at 65

Male age 6550% chance of living to 85

25% of living to 93

Female Age 65 50% chance of living to 87

25% chance of living to 95

Couple of age 65

At lease one person has a 50% chance of living to 93

At lease one person has a 25% chance of living to 97

Source: Annuity 2000 Mortality Table.

Just the Facts73% of those collecting Social Security Retirement benefit are receiving reduced

amounts

>76% of all women

>71% of all men

15.5% increase over the past 5 years in those over age 85 collecting benefits

>4.8Million

In 2006

>1,203,834 recipients age 90 or older

>256,319 recipients age 95 or older

>45,000 recipients 100 or older

-39,000 women

-6,000 men

Source: Social Security Administration's annual statistical supplement 2008

Millions Face Shrinking Social Security Payments

The trustees who oversee Social Security are projecting there won't be a cost of living adjustment (COLA) for the next two years. That hasn't happened since automatic increases were adopted in 1975.

Social Security Taxes Wages

To be fully insured, a worker needs 40 credits. A maximum of 4 credits can be earned per year

It takes approximately 10 years of working to become fully insured.

3 Months before your birthday, you should received a Social Security Statement estimating what your retirement benefits will be

You should verify the earnings record to ensure its accuracy since your benefit is based on that.

When Should Benefits be Collected

Individuals can elect to receive: Reduced benefits at as early as age 62 Full benefits at fully retirement age –or- Increased benefits, if benefits are delayed beyond

fully retirement age.

Full Retirement age is increasing to age 67. Depending on the year of birth, your client’s full retirement age can be anywhere between age 65 and 67

Year Born Full Retirement age

1937 or early 65

1938-1942 65+2 months for every year after 1937 until 1953

1943-1954 66

1955-1959 66+2 months for every year after 1954 until 1960

1960 and later 67

Early Retirement Benefits: If Clients are fully insured, they can collect Benefit as early as the first full month the recipient attains age 62

What’s the cost

Fully Retirement age Monthly Benefit reduction

65 20%

66 25%

67 30%

What if the Client Works During Retirement?

2009 Limit

Under full retirement age >$1 of benefits withheld for every $2 in earnings above the limit

$14,160/year

Year individual reaches full retirement age

>$1 of benefits withheld for every $3 in earnings above the limit for months prior to attaining full retirement age

$37,680/year

Month individual reached full retirement age and beyond

>Reduction no longer applies

Unlimited

Only own wages are considered. Spouse’s wages are not considered.

Request for Withdrawal of Application

Complete Withdrawal of Application form Indicate reason for withdrawal request

Wait for SSA approval

Repay all benefits, including spousal benefits, paid to date (If work again)

Reapply when ready to begin collecting benefits

Delayed Retirement Credit

Year of Birth Yearly Increase to age 70

1939-1940 7.0%

1941-1942 7.5%

1943 or later 8.0%

If you delay collecting benefits beyond your full Retirement Age, you Will Receive an increase in your Primary Insurance Amount.

This DRC is in addition to the Cost of Living Adjustment. 2008 COLA: 5.8%

Spousal & Survivor Benefits

>Spouse is eligible to receive the higher of whatever benefit he/she may haveEarned on his/her own record, or half of Primary Worker’s Primary InsuranceAmount (PIA)>Spouse cannot collect on Primary Worker’s record until the Primary files for Benefits. (The Primary can file and elect to suspend benefits).>A Surviving spouse will receive 100% of the primary’s benefit at full retirementAge. However, reduced benefits can begin s early as age 60

Age Monthly Benefit

Age Monthly Benefit

Spousal Benefit

Adjusted Spousal Benefit

Survivor Benefit

62 $416 62 $1,614 $406 $1,862

66 $552 66 $2,257 $1,129 $577 $2,257

70 $729 70 $3,042 $400 $3,042

Wife’s Earning History Husband’s Earning History

Strategically Taking Social SecurityTwo High Wage Earners

Wife’s Earning History Husband’s Earning History

Age Monthly

BenefitAge Monthly

BenefitSpousal Benefit

Survivor Benefit

62 $1,650 62 $1,682 $1,879

66 $1,353 66 $2,277 $1,139 $2,277

70 $1,786 70 $3,048 $3,048

If the wife waits until FRA to collect benefits, she can file for spousal benefits onlyAnd allow her own to continue to grow. She would receive $1,139. Than at age 70.She would apply to start collecting her own benefit in Lieu of Spousal, and Receive $1,786.

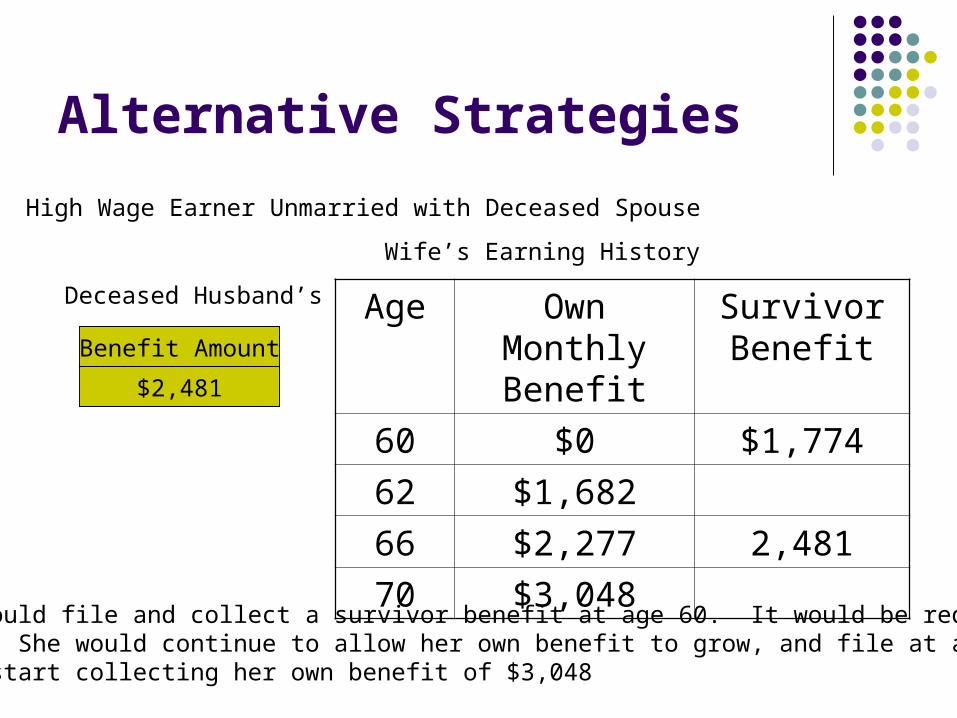

Alternative Strategies

High Wage Earner Unmarried with Deceased Spouse

Deceased Husband’s

Benefit Amount

$2,481

Age Own Monthly Benefit

Survivor Benefit

60 $0 $1,774

62 $1,682

66 $2,277 2,481

70 $3,048

Wife’s Earning History

Wife could file and collect a survivor benefit at age 60. It would be reduced by28.5%. She would continue to allow her own benefit to grow, and file at age70 to start collecting her own benefit of $3,048

What if the Individual has Younger Children?

Who can collect benefits when you retire?

You Your Spousal Your Unmarried Child

Age 62 or older 1. Age 62 or over

2. Any age, if caring for your child who is under 16 or disabled before 22

Under 18, or up to 19 if in high school, or any age if disabled before 22

Divorced Spouse A divorced spouse can apply for benefits on a

work’s record if Had been married to worker for at lease 10 years Has been divorced for at lease 2 years* Is at lease age 62 Is unmarried –and- Not eligible for an equal or higher benefit on his or her own

record, or on someone else’s record.The ex-spouse has to be at lease age 62, but not required to

have filed.

* 2 years does not apply if the individual was eligible for spousal benefit at the time of divorce.

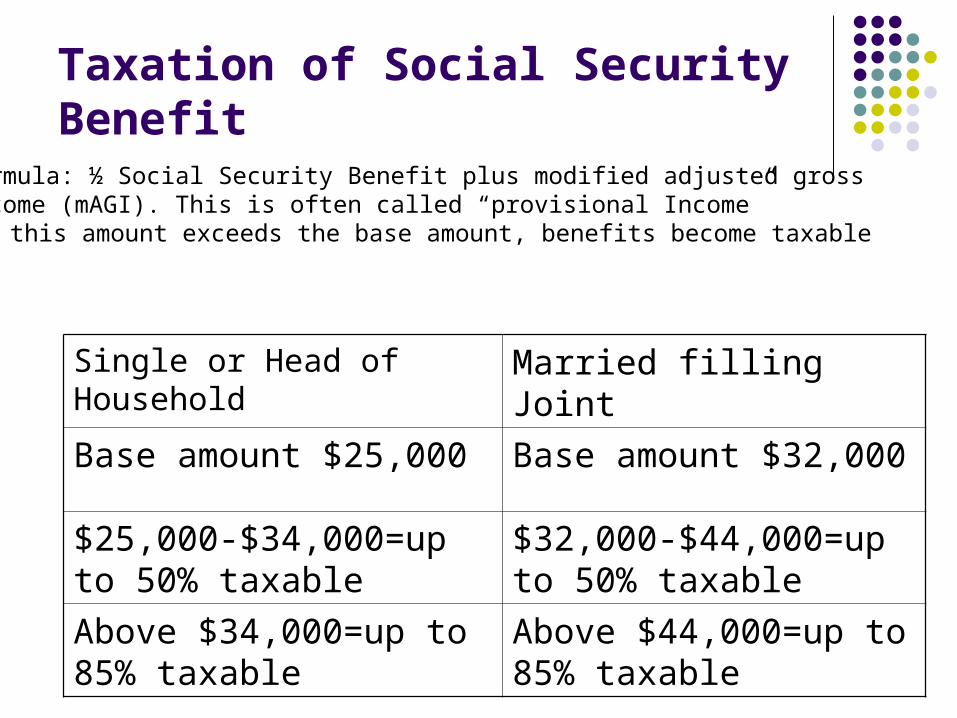

Taxation of Social Security Benefit

Single or Head of Household Married filling Joint

Base amount $25,000 Base amount $32,000

$25,000-$34,000=up to 50% taxable

$32,000-$44,000=up to 50% taxable

Above $34,000=up to 85% taxable

Above $44,000=up to 85% taxable

1. Formula: ½ Social Security Benefit plus modified adjusted grossincome (mAGI). This is often called “provisional Income”

2. If this amount exceeds the base amount, benefits become taxable

Government Pension Offset (GPO)

If your are covered by a pension under the civil retirement system rather thanSocial Security, your spousal and/or survivor benefits will be reduced throughA Government Pension Offset.

Spouse benefits and Survivor benefit will be reduce by 2/3 of the amount of Your pension.

Wife’s Pension

Monthly Pension

$1,500

Gov’t Pen. Offset

$1,000

Age Monthly Benefit

Spousal Benefit

Adj. Spousal Benefit

Adj. Survivor Benefit

62 $1,614 $862

66 $2,257 $1,129 $129 $1,257

70 $3,042 $2,042

Husband’s Earning History

Additional Resource

Social Security Administration www.ssa.gov

Internal Revenue Service

www.IRS.gov

2009 Guide to Social Security