sni report

TRANSCRIPT

Trey Thompson May 7, 2013 Scripps Networks Interactive, Inc. Summary

I rate shares of SNI a buy, with an aggressive

suitability. The 12-‐month target price for the stock is

$81.00 which implies a ~16% upside potential, along

with a modest 0.90% dividend yield. I believe that SNI

is well positioned to continue gaining market share

with its leading portfolio of lifestyle-‐oriented

networks. Additionally, the company’s strong balance

sheet will allow for continued timely investments and

acquisitions to expand its global footprint. Risks to

this rating include a decline in audience ratings for the

networks and the potential for slowing growth, which could cause the earnings multiple

applied to the stock to contract.

Company Description

Scripps Networks Interactive (SNI) is one of the leading developers of lifestyle-‐

oriented content for television and Internet. They have operations domestically, as well as

in the U.K., European Union, Middle East, Africa, and the Asia-‐Pacific regions. Revenue is

derived principally from advertising sales, affiliate fees, and ancillary sales, including

licensing of consumer products. Operating costs are primarily programming expenses,

BUY GICS Sector: Consumer Discretionary Sub-‐Industry: Broadcasting & Cable Key Statistics Ticker SNI Price (05/03/2013) $69.31 52-‐Week Range: $49-‐70 Shares Outstanding: 148.38 Market Cap*: 10.28 Beta: 1.06 Avg. Daily Volume* 0.822 Dividend/Yield: $0.60/0.90% Payout Ratio (ttm): 13.45% LT Debt*: $1.385 LT Debt/Equity: 0.76 12-‐Month Target Price: $81.00 3-‐5 Yr. Est. Growth Rate: 11% P/E 2013E EPS: 19.15x P/B (mrq): 5.45x ROE (ttm): 36.47% *All numbers in billions-‐ ex per share data

employee costs, and sales and marketing expenses. SNI became a publicly trade company

as the result of a separation from The E.W. Scripps Company on July 1, 2008.

SNI has two reporting segments: Lifestyle Media and Corporate & Other. The

Lifestyle Media segment includes National television networks, Food Network, Home and

Garden Television (HGTV), Travel Channel, DIY Network (DIY), Cooking Channel, and Great

American Country (GAC). This segment also includes websites and other media that are

associated with the aforementioned brands. The Corporate & Other operating segments

includes results from International brands including: Food Network UK, UKTV (50%

owned) and Canadian networks.

Subsidiary Breakdown: Scripps Networks, LLC Delaware Television Food Network, G.P. (69% owned) Delaware TCM Sub, LLC (65% owned) Delaware Travel Channel, LLC (65% owned) Delaware Scripps Networks International Limited (Travel Channel International)

England and Wales

Lightdragon Limited England and Wales

Source: Scripps Networks Interactive 2012 Annual Report

Investment Rationale/Risk:

I think that SNI is reasonably priced given its favorable growth outlook and strong financial

position. The following items may have a significant impact on my outlook for the stock

performance.

Catalysts:

-‐ International expansion opportunities. SNI has been aggressively increasing

spending to grow the operations of its international subsidiaries. In April 2012, they

acquired Travel Channel International, which has already had a positive impact on

earnings. SNI has a solid balance sheet that should allow it to capitalize on other

international acquisitions should the opportunity present itself.

-‐ Affiliate contract renewals. SNI routinely negotiates and enters in to multi-‐year

distribution agreements with various cable and satellite operators. As consumer

loyalty to programs and ratings increase, SNI should be able to negotiate more

favorable terms for these contracts.

-‐ Share repurchase Program. SNI has authorized a $1bn share repurchase program.

SNI repurchased $150mm worth of shares in 1Q 2013, leaving approximately $750

million in the program. This should be a positive catalyst for the stock, as the

reduced share base coupled with rising revenue should lead to strong EPS growth.

Risks:

-‐ A slowdown in economic conditions would reduce corporate advertising and

marketing budgets. This would negatively impact advertising rates for SNI and other

broadcasting and cable networks. Advertising sales account for ~69% of total

revenue.

-‐ Rating declines. Changes in consumer preferences and behavior occur frequently.

SNI must constantly adapt programming to fit these changing tastes and support

continued strong ratings. A failure to adapt to changing preferences could lead to

lower ratings, henceforth lower advertising sales and less favorable affiliate fees.

-‐ Negative performance of equity method investments. SNI has substantial

investments in companies that it accounts for using the equity method. Since SNI is

not responsible for the day-‐to-‐day operations of these companies, there

performance is largely out of management’s control.

Industry Position/Environment

The broadcasting and cable subsector has performed well over recent years after

recovering from the economic downturn. In 2012, the sector returned 44.7% versus 13.7%

for the S&P 1500. The industry is experiencing several challenges to their traditional

operating model, primarily; the introduction of video-‐on-‐demand (VOD) and other Internet

based media delivery systems. There have been many legal battles and media attention

drawn to this issue, but overall, the actual impact has been minimal. However, this issue is

not going away and there will likely be increased pressure on the industry to accept the

VOD concept.

Advertisement spending across the industry has been very strong in recent years

and is projected to continue. 1 This has been lead by the auto industry, a historical top

spender, which has finally recovered to pre-‐recession levels of spending. There continues

1 Source: S&P Capital IQ Industry Report

to be a slow return of M&A activity within the industry over the past few years, and there is

the potential for further consolidation.2

Strengths/Weaknesses

SNI has done a great job of building brand loyalty with its portfolio of leading

network programming. Advertising space on SNI networks is particularly desirable to

advertisers because SNI delivers content that focuses on specifically defined topics of

interest. According to the company, SNI viewers have the highest level of discretionary

spending among all cable/satellite networks. These factors both lead to higher ratings and

affiliate fees for the company.

Cable and satellite programming has been gaining significant market share from

traditional (over-‐the-‐air) broadcasting television. This trend has increased the amount of

cable/satellite subscriptions and has allowed Scripps and other cable/satellite networks to

increase their viewership base. In addition, cable/satellite networks receive affiliate fees

(subscription fees) from cable and satellite operators. These fees can help smooth out

earnings volatility since they are multi-‐year contracts. This is an advantage over traditional

broadcasting companies that do not receive such fees. Affiliate fees accounts for roughly

30% of SNI revenue.

As mentioned earlier, one of the challenges for broadcasting and cable companies

has been increased competition from VOD and Internet-‐based content delivery. By

integrating network content throughout television, Internet, print, and mobile media, SNI

has capitalized on this trend before many of its peers. This should remain a competitive

advantage in the medium-‐term as other competitors adapt their own strategies.

2 S&P NetAdvantage

One weakness is that only 5% of SNI revenue comes internationally. This means that

almost all of the revenue generated comes from domestic ad spending and affiliate fees.

Additionally, within its domestic network portfolio, the vast majority of sales comes from

food and home lifestyle programming. If viewer interest wanes in these two categories, SNI

could see a large decrease in advertising revenue. Within this weakness lies their biggest

opportunity as well.

Opportunities/Threats

Scripps Network’s biggest growth opportunity lies in international markets.

Currently, only about 5% of total revenues are derived internationally. However, in recent

years, the company has made several investments to increase its international footprint.

These investments include UKTV (50% owned) and Travel Channel international. A healthy

balance sheet and strong free cash flow should allow SNI to make further timely

investments and acquisitions internationally as opportunities arise.

The greatest threat to SNI is the fact that ~69% of its sales are derived from

advertising sales. The price that advertisers pay SNI is contingent upon the rating their

programs receive from Nielsen Media Research. In turn, these rating are based on the

number of viewers, and the “attractiveness” of those viewers to advertisers (i.e. income,

age, gender, ect). In other terms, 69% of SNI revenue is based on how many viewers they

have watching their programming.

Earnings Analysis

SNI has shown strong revenue and earnings growth over the past four years driven

by increasing advertising sales and affiliate fees. Top line revenue has increased from

$1.3bn in 2008 to $2.3bn in 2012. Meanwhile, earnings have increased from $24mm in

2008 to $681mm last year, a 110% 4-‐year CAGR, reflecting efforts to reduce costs and

streamline operations.

Source: Scripps Networks Interactive 2012 Annual Report

SNI has been able to maintain gross margins in the low to mid 40% range, which is the best

in the industry. SNI also generates industry-‐leading return on equity (ROE), averaging in

the high 20% range over the past few years.

Source: S&P Capital IQ

3

In the food category, Food Network finished

the year ranked ninth among all ad-supported

cable networks, maintaining its command of

the genre. It was the most-watched year ever

for the network.

Contributing to the network’s positive audience

trends is the enduring popularity of programs

like Chopped, Iron Chef America, Restaurant:

Impossible and Food Network Star. The

network picked up tremendous audience gains

with breakout hits like Restaurant Stakeout

with New York restaurateur Willie Degel and

competition shows, including Rachael vs. Guy

and Worst Cooks in America with Anne Burrell.

And we’re pushing for even stronger

momentum in 2013.

This year at Food Network, we’re celebrating

20 years of defining a wildly popular television

genre and shaping the nation’s, and now the

world’s, conversation about food. There’s no

doubt that Food Network is an iconic power

brand and will be for decades to come.

We’re seeing continued success with our

flanker brands, DIY Network and Cooking

Channel. DIY Network finished the year on

a high note with record ratings and strong

growth in primetime audience, driven by The

Vanilla Ice Project, the new Bronson Pinchot

Project and the ever-popular Crashers series

— all favorites of our avid fan base of home

improvement enthusiasts. And at Cooking

Channel, viewership rose steeply with new

shows, such as Not My Mama’s Meals with

Bobby Deen and Symon’s Suppers with

Michael Symon, driving audience numbers.

FINANCIAL HIGHLIGHTS*

Q!Total Revenue"!

Q!Total Segment Profit

*Excludes discontinued operations for all periods presented.

Q!Segment Revenue"!

Q!Segment Profit

+15% 4-YEAR REVENUE CAGR

$1,315 $1,367

$1,883$2,072

$583 $571$835

$977

$2,307

$1,041

08 09 10 11 12

36% Food Network

34% HGTV

12% Travel Channel

10% DIY Network, Cooking Channel, GAC

5% Digital

3% International and Other

CONSOLIDATED REVENUE BY BRAND

CONSOLIDATED OPERATING RESULTS*

(Dollars in millions)

LIFESTYLE MEDIA

(Dollars in millions)

+15% 4-YEAR REVENUE CAGR

(Dollars in millions) 2012 2011 2010

CONSOLIDATED

Operating revenues $ 2,307 $ 2,072 $ 1,883

Income from continuing operations 681 473 398

LIFESTYLE MEDIA

Segment operating revenues $2,256 $ 2,045 $ 1,867

Segment profit 1,136 1,050 904

Segment profit margin 50% 51% 48%

*Excludes discontinued operations for all periods presented.

Segment profit is used by the company’s chief operating decision makers to evaluate its business segments. See page F-37 of the company’s Form 10-K.

$1,312 $1,367

$1,867$2,045

$632 $637$904

$1,050

$2,256

$1,136

08 09 10 11 12

-20

-10

0

10

20

30

40

36

38

40

42

44

46

48

Dec12 Dec11 Dec10 Dec09 Dec08 Dec07 Dec06 Gross Margin Return on Equity (%)

Gross Margin

ROE

For 1Q 2013, the most recently reported quarter, SNI reported EPS of $0.72 vs.

expectations of $0.74. The EPS miss was primarily due to unfavorable tax adjustments

totaling $7.8 million or $0.05 per share. Consolidated revenues of $594mm, were up 11%

from the same period last year. This was driven by an 11% increase in both advertising

sales and affiliate fees. SNI reported a very strong advertising market with Food, Retail,

and financial companies spending the most for the quarter. The robust increase in affiliate

fees was the result of a digital distribution deal with Amazon, Inc. This is a good example of

SNI capitalizing on new digital media trends.

SNI also announced they repurchased 2.4 million shares for $150 million during the

quarter, which leaves ~$750mm left in the current repurchase program. SNI generated

$268 million in cash from operating activities and reported cash reserves of $421mm.

One of the biggest positives, in my opinion, was the increase in revenues YoY for

smaller networks in the SNI portfolio. Most notably, the Cooking channel and Great

American Country (GAC) with 32.7% and 28.2% increases respectively. Although these

sizeable increases are coming from a relatively small base, it is nonetheless a step in the

right direction for SNI to grow the diversity of their revenue streams.

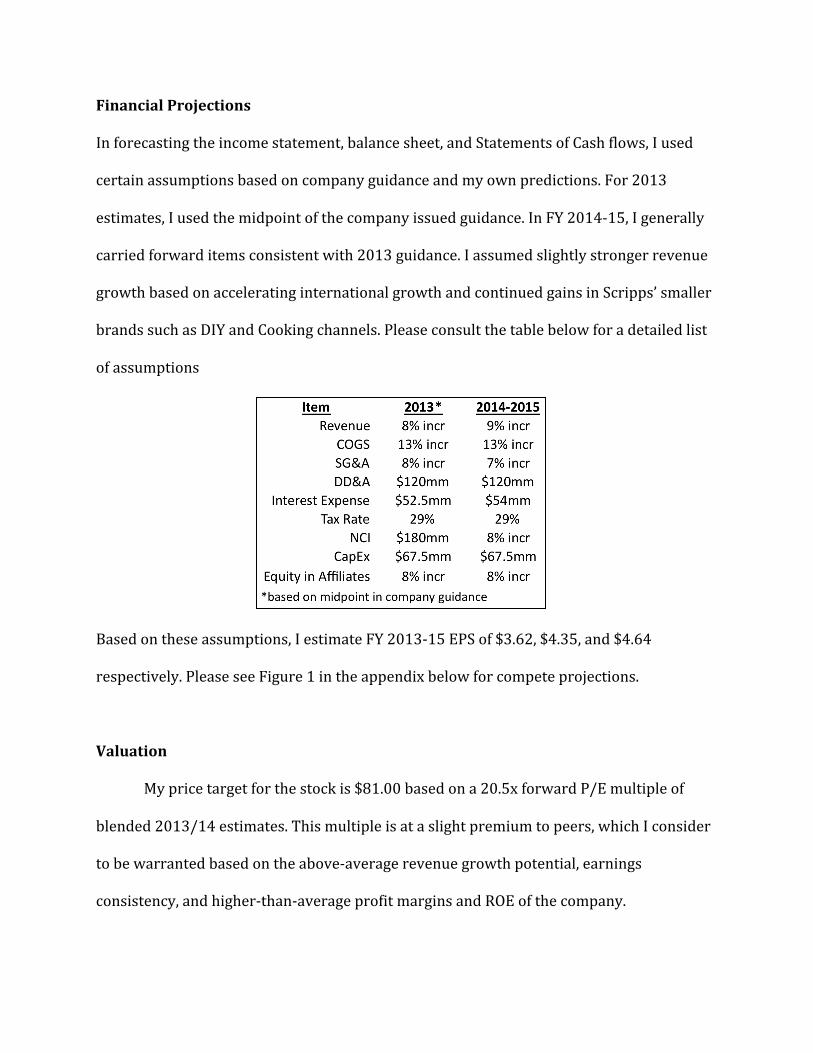

Financial Projections

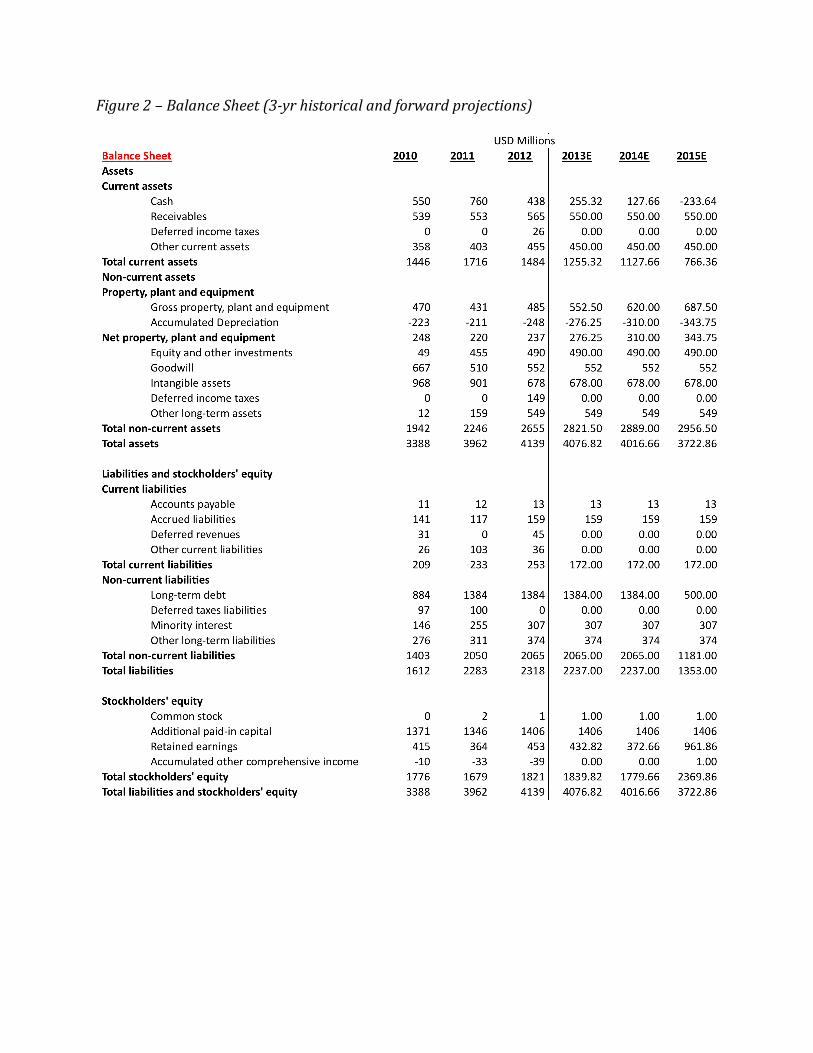

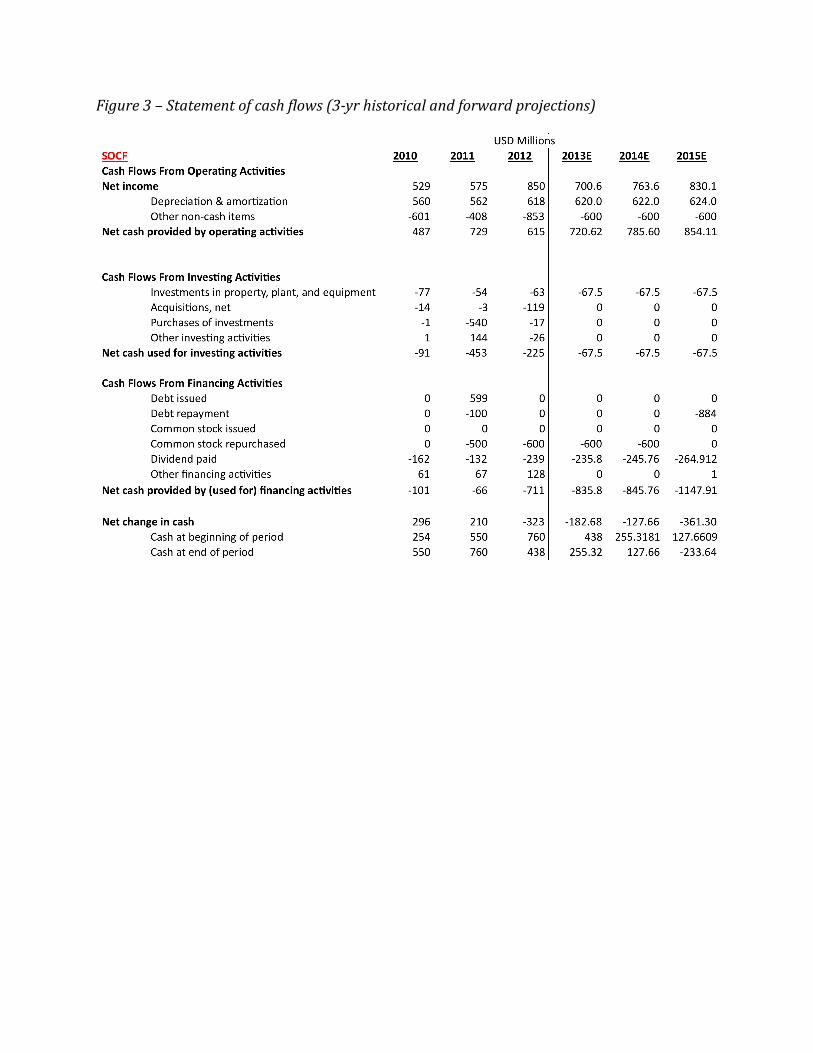

In forecasting the income statement, balance sheet, and Statements of Cash flows, I used

certain assumptions based on company guidance and my own predictions. For 2013

estimates, I used the midpoint of the company issued guidance. In FY 2014-‐15, I generally

carried forward items consistent with 2013 guidance. I assumed slightly stronger revenue

growth based on accelerating international growth and continued gains in Scripps’ smaller

brands such as DIY and Cooking channels. Please consult the table below for a detailed list

of assumptions

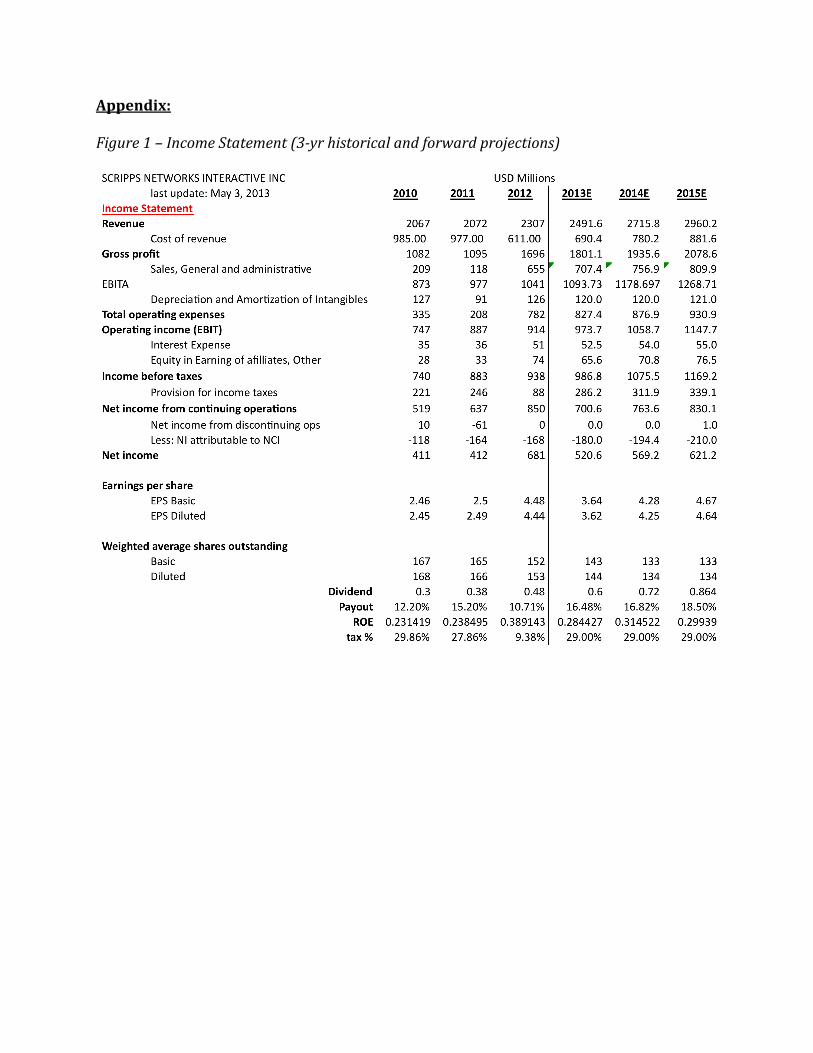

Based on these assumptions, I estimate FY 2013-‐15 EPS of $3.62, $4.35, and $4.64

respectively. Please see Figure 1 in the appendix below for compete projections.

Valuation

My price target for the stock is $81.00 based on a 20.5x forward P/E multiple of

blended 2013/14 estimates. This multiple is at a slight premium to peers, which I consider

to be warranted based on the above-‐average revenue growth potential, earnings

consistency, and higher-‐than-‐average profit margins and ROE of the company.

In deriving the 20.5x P/E multiple, I first divided the peer group in two, and selected

stocks that traded at P/E multiples above the median of 17.5x forward 2013/14 blended

estimates. Then, I averaged the P/E of these companies to come up with what amounts to

an ‘average premium multiple’. Please note that I excluded the NFLX from the premium

multiple as the P/E was well over 100x and distorted the average.

I view this as a relatively conservative estimate since I believe that SNI is the best

company within the cable and broadcasting subsector. I choose to value the company using

relative valuation mainly because growth rates far exceeded the cost of capital for the

foreseeable future. This makes it difficult to come up with an accurate terminal value for

the DDM and DCF.

Appendix:

Figure 1 – Income Statement (3-yr historical and forward projections)

Figure 2 – Balance Sheet (3-yr historical and forward projections)

Figure 3 – Statement of cash flows (3-yr historical and forward projections)

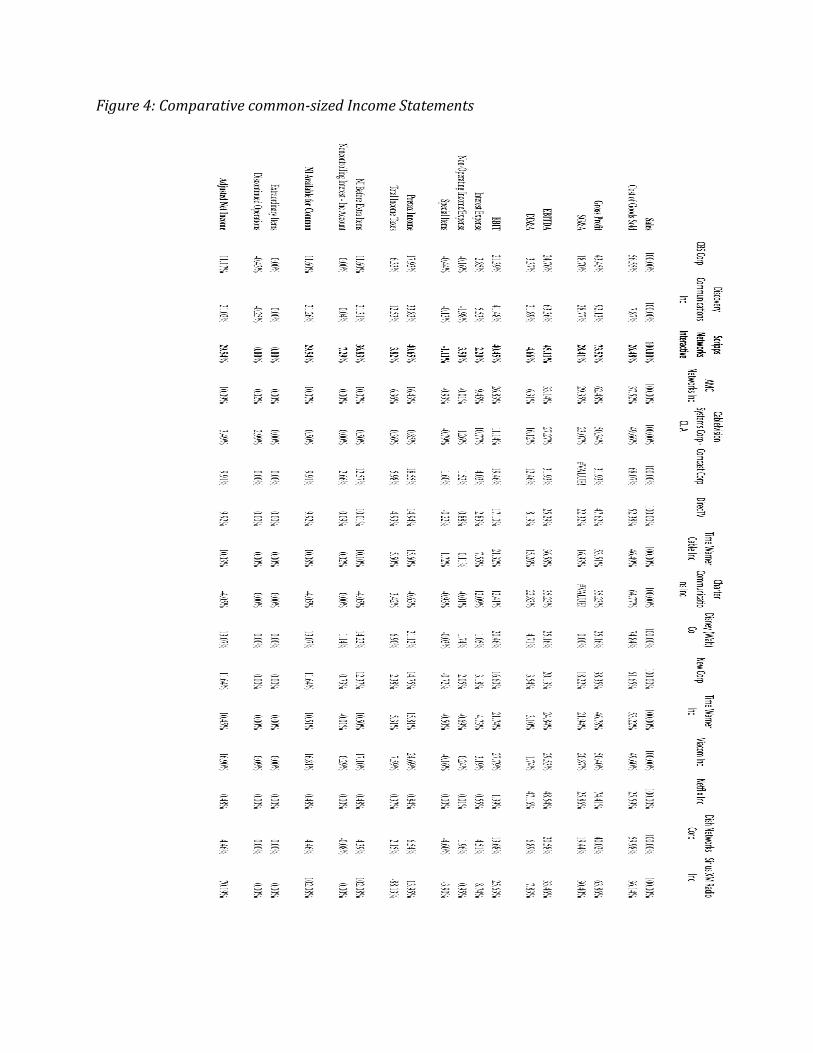

Figure 4: Comparative common-sized Income Statements

Figure 5: Comparative Analysis