sme internationalization and finance in asia€¦ · · 2015-07-16sme internationalization and...

TRANSCRIPT

SME Internationalization and Finance in AsiaAn Empirical Exploration

Ganeshan Wignaraja

Advisor

Asian Development Bank

Manila

16 July 20151

Introduction and Contents1.

2

• Motivation: Policy spotlight on the role of SMEs to promote jobs and inclusive growth in Asia

• Open question: how to encourage SME internationalization and financing in Asia?

• Contents:

1. SMEs in supply chain trade and characteristics of firms

2. SME finance and characteristics of bank borrowers

3. Policy Implications and conclusion

• Focus on Southeast Asia and PRC

SMEs Make up the Majority of Firms in Asia

3

62.258.5

48.0

89.7

56.5

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Asia Europe and CentralAsia

Latin America and theCaribbean

Middle East and NorthAfrica

Sub-Saharan Africa

Distribution of Enterprise Sizes across Regions (%)

Small Medium Large

Note: SME are firms with less than 100 employees. Uses recent data from the World Enterprise Surveys.Asia refers to Afghanistan, Bangladesh, Bhutan, PRC, Indonesia, Kazakhstan, Kyrgyz Republic, the Lao PDR, Nepal, Pakistan, the Philippines, Sri Lanka, Tajikistan, Timor-Leste, Uzbekistan, and Viet Nam. Source: ADB–OECD Study on Enhancing Financial Accessibility for SMEs: Lessons from recent crises. Philippines: Asian Development Bank, 2013

SMEs Contribute Much to Economic Activity but Less to Trade in Asia

4

Note: SME definition varies by country.Use most recently available data* percent of the private nonfarm GDP in 2008** estimateSource: Various statistical agencies (ASEAN SME data, Business in Asia, DTI Philippines, PRC Ministry of Industry and Information Technology, European Commission fact sheet, Small Business and Entrepreneurship Council)

49.4

79

70

40

35

40

77.0

97.2

61.0

77.9

58.9

87.5

70.2

0 50 100

United…

Germany

Pakistan

Banglade…

Sri Lanka

India

Vietnam

Indonesia

Philippines

Thailand

Malaysia

Korea,…

Japan

SME share of total employment (%)

46

53.8

30

22.5

52

17

40.0

57.8

35.7

38.7

31.9

49.4

50.0

0 50 100

United States *

Germany

Pakistan

Bangladesh

Sri Lanka

India

Vietnam

Indonesia

Philippines

Thailand

Malaysia

Korea, Republic of

Japan

SME Contribution to GDP (%)

33.7

55.9

25

11.3

20

40

20.0

15.8

20.0

29.5

19

30.9

53.8

0 20 40 60

United States *

Germany

Pakistan

Bangladesh

Sri Lanka

India

Vietnam

Indonesia

Philippines

Thailand

Malaysia

Korea, Republic of

Japan

SMEs share of total exports (%)

**

SMEs in Supply Chain Trade2.

5

Rise of Factory Asia, but Concentrated in Some Asian Economies

Note: Supply chain trade is defined as trade in parts and components using the gross trade approach of Athukorala (2011) .

6

0.1

0.1

0.8

0.0

0.0

0.0

0.2

0.8

1.0

1.1

1.7

2.0

2.7

4.8

7.9

25.0

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Sri Lanka

Pakistan

India

Brunei Darussalam

Lao People's Dem. Rep.

Myanmar

Cambodia

Indonesia

Philippines

Viet Nam

Singapore

Thailand

Malaysia

Rep. of Korea

Japan

China

Sou

th A

sia

ASE

AN

East

Asi

aShare of world supply chain exports,

2001-2013 (%)

2001-2004

2005-2008

2009-2013

ASEAN accounted for 9.3% of world supply chain trade over the period 2009-2013

Peoples Rep. of

7

SMEs and Large Firms in Supply Chain Trade in Southeast Asia*

• SME engagement varies by economy. Large firms dominate.

22.0

46.2

29.6

20.1

6.3

21.4

72.1

82.4

91.1

51.1 52

64.6

0

10

20

30

40

50

60

70

80

90

100

All Countries Malaysia Thailand Philippines Indonesia Viet Nam

%

Role of large firms and SMEs in supply chains

SMEs in supply chains as apercentage of all SMEs

Large firms in supply chains asa percentage of all large firms

Source: Wignaraja, G., (2015), “Factors Affecting Entry into Supply Chain Trade: An Analysis of Firms in Southeast Asia” Asia and the Pacific Policy Studies, March

Note: * Direct exporters and tier 1 suppliers only. Tier 2 suppliers excluded.

What Explains Entry into Supply Chain Trade in Southeast Asia?

8

• Various attempts to measure supply chain trade (e.g. trade in value added) but little on the characteristics of firms in supply chains in Asia

• Wignaraja (2015) examines 5,900 firms in 5 Southeast Asian economies (Malaysia, Thailand, Philippines, Indonesia and Vietnam). World Bank data collected by random sampling

• Main findings: Firm heterogeneity matters Higher SME engagement in some economies but large firms dominate Apart from firm size, technological capabilities, skills, access to credit

and foreign ownership affect whether firms join supply chains Tackling residual supply-side and policy constraints can further firms,

including SMEs, joining supply chains Caution about use of cluster policies and selective interventions to

promote SME engagement in supply chains

8

Factors Influencing Joining Supply Chain Trade in Southeast Asian Firms

VariableAll firms in Supply Chains SMEs in Supply Chains

Sign Significance Sign Significance

Firm Size + 1% + 1%

Firm Size squared - 1%

Firm Age - 10% - 10%

Firm ISO certified + 1% + 1%

Firm has Patents + 1% + 1%

GM has degree + 5% +

GM’s experience + +

Workers have HS education

+ 1% + 1%

Foreign Ownership + 1% + 1%

Access to Credit + 1% + 10%

Country Dummies -/+ 1-10% +/- 1-5%

*Dependent variable is binary: 1 if part of production network, 0 otherwise.9

10

Affordable and High Quality Support Systems Are Important

Source: Wignaraja (2013).

SMEs Face Many Barriers, Including Access to Finance

11Source: Wignaraja, G., (2015), “Factors Affecting Entry into Supply Chain Trade: An Analysis of Firms in Southeast Asia” Asia and the Pacific Policy Studies, March

SMEs Access to Finance3.

12

SME Credit Gap is Severe in Asia

13

Note: Credit gap” is the difference between formal credit provided to SMEs and total estimated potential need for formal credit based on McKinsey & Co. estimates. Uses the IFC Enterprise Finance Gap Database (2011)Source: From the IFC report “Closing the Credit Gap for Formal and Informal MSMEs” (2013)

In South and East Asia and the Pacific approximate 9 million of all formal SMEs do not have sufficient access to finance (IFC, 2013).

14

SME Credit Gap Varies Across Asia

Note: “Credit gap” is the difference between formal credit provided to SMEs and total estimated potential need for formal credit based on McKinsey & Co. estimates. Source; IFC Enterprise Finance Gap Database (2011).

Region CountryTotal Credit Gap (US $

Billions)

Average Credit value Gap per Enterprise

(US$)

ASE

AN

Singapore 7.1 856,000

Brunei Darussalam 7.2 736,000Malaysia 8 126,000

Thailand 11.8 126,000

Philippines 2 59,000

Cambodia 0.4 50,000

Vietnam 4.3 42,000

Indonesia 11.8 29,000Lao PDR 0.2 13,000

East

Asi

a Hong Kong 10.2 733,000Republic of Korea 28.5 503,000PRC 62.7 44,000

Sou

th A

sia

Sri Lanka 0.1 54,000India 3.4 54,000

Pakistan 2.9 51,000Bangladesh 1.8 17,000

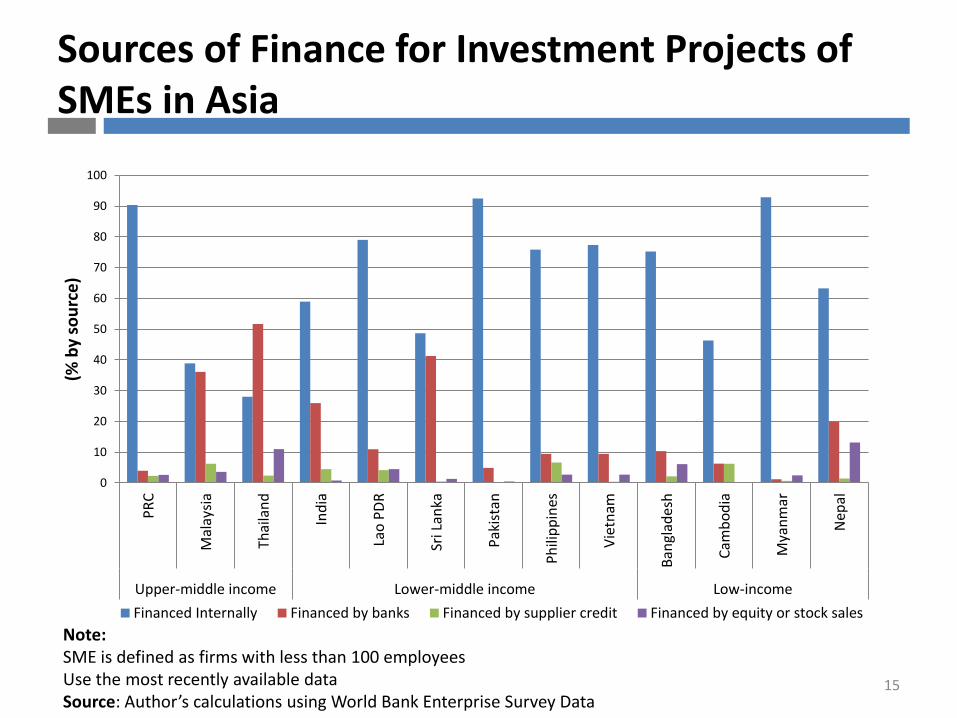

Sources of Finance for Investment Projects of SMEs in Asia

15

Note: SME is defined as firms with less than 100 employeesUse the most recently available dataSource: Author’s calculations using World Bank Enterprise Survey Data

0

10

20

30

40

50

60

70

80

90

100

PR

C

Mal

aysi

a

Thai

lan

d

Ind

ia

Lao

PD

R

Sri L

anka

Pak

ista

n

Ph

ilip

pin

es

Vie

tnam

Ban

glad

esh

Cam

bo

dia

Mya

nm

ar

Nep

al

Upper-middle income Lower-middle income Low-income

(% b

y so

urc

e)

Financed Internally Financed by banks Financed by supplier credit Financed by equity or stock sales

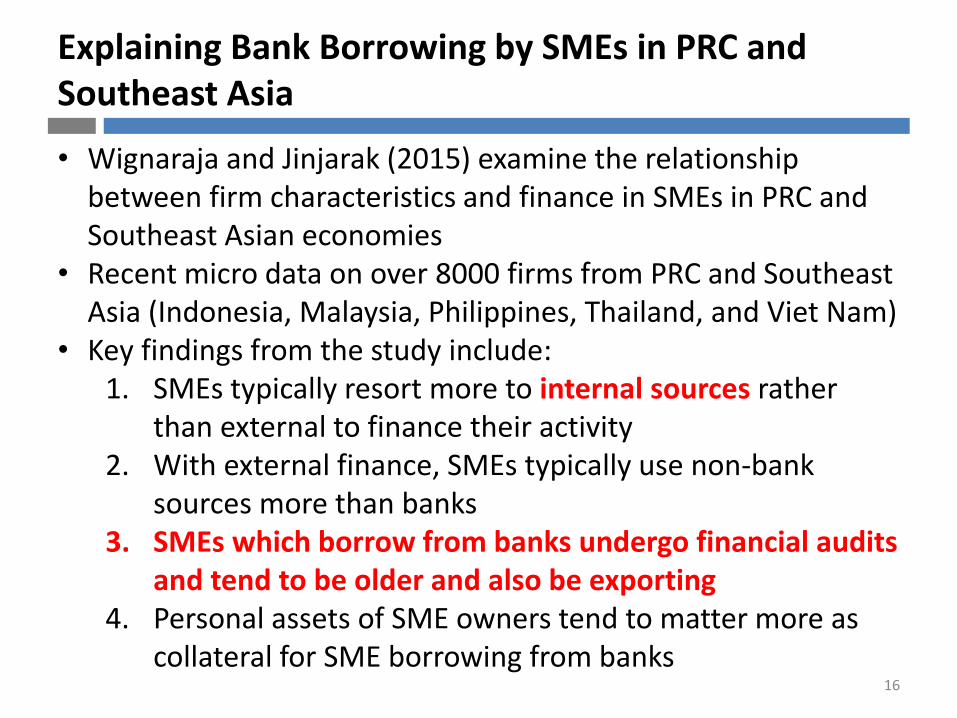

Explaining Bank Borrowing by SMEs in PRC and Southeast Asia

• Wignaraja and Jinjarak (2015) examine the relationship between firm characteristics and finance in SMEs in PRC and Southeast Asian economies

• Recent micro data on over 8000 firms from PRC and Southeast Asia (Indonesia, Malaysia, Philippines, Thailand, and Viet Nam)

• Key findings from the study include:1. SMEs typically resort more to internal sources rather

than external to finance their activity2. With external finance, SMEs typically use non-bank

sources more than banks3. SMEs which borrow from banks undergo financial audits

and tend to be older and also be exporting4. Personal assets of SME owners tend to matter more as

collateral for SME borrowing from banks16

17

Influence of Firm Characteristics on Bank Borrowing

Y = Bank

Borrowing (%

working capital)

Firm Size (number of employees)

≤ 25 > 25 & ≤ 100 > 100 & 250 ≤ > 250

Firm age .52 .37 .49 .30

(.21)** (.14)*** (.16)*** (.13)**

Export participation .30 .15 .12 .10

(.09)*** (.05)*** (.05)** (.05)**

Foreign ownership -21.77 -29.83 -15.42 -21.93

(8.51)** (4.23)*** (4.60)*** (3.94)***

Managerial experience -.52 -.45 .10 .28

(.22)** (.15)*** (.19) (.16)*

Financial audit 9.37 1.27 3.97 8.89

(4.30)** (3.16) (4.58) (4.46)**

ISO certification -18.23 -11.54 -6.88 -1.26

(6.60)*** (3.18)*** (3.99)* (4.03)

Labor Intensive 5.44 9.13 20.11 17.07

Industries (5.53) (4.67)* (6.76)*** (6.50)***

Capital Intensive 16.12 12.62 20.14 2.52

Industries (5.01)*** (4.13)*** (6.16)*** (6.05)

constant -73.61 -26.43 -38.62 -22.15

(6.26)*** (5.31)*** (8.00)*** (8.08)***

Pseudo R-sq. .01 .01 .01 .01

observations 2,859 2,729 1,336 1,156

Note: This table reports regression results of lender type (dummy dependent variable) on firm characteristics (control variables) for firms at different sizes. The estimation method is Probit. The analysis pools firm observations across PRC, Malaysia, Thailand, Indonesia, Philippines, and Viet Nam. Standard errors are in parentheses; *** (**, *) denotes statistical significance at 1 (5, 10) percent level.Source: Wignaraja and Jinjarak (2015).

18

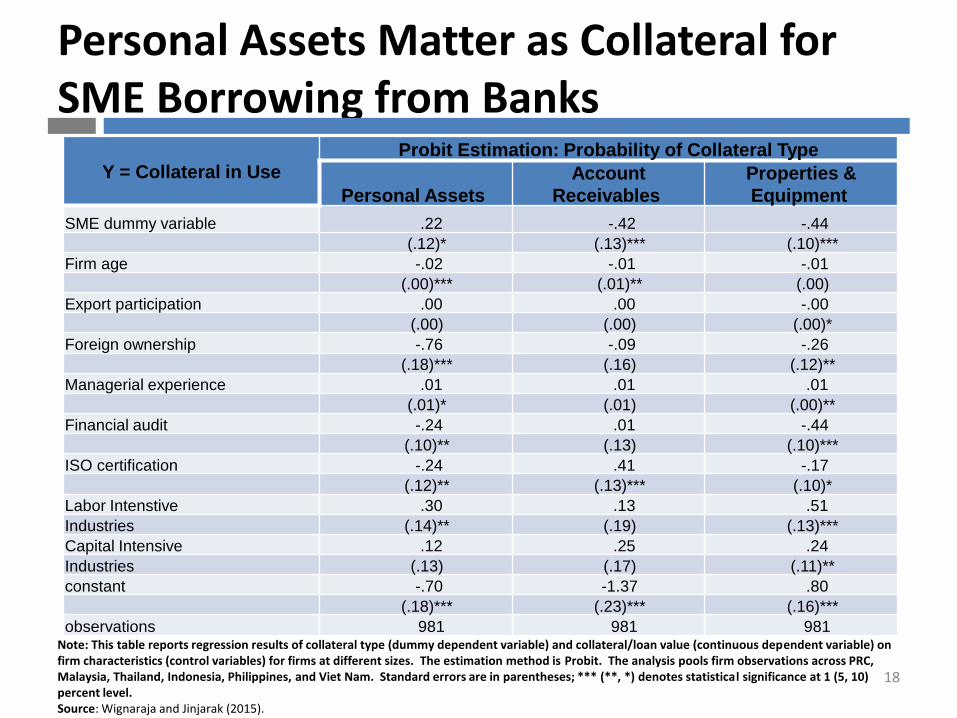

Personal Assets Matter as Collateral for SME Borrowing from Banks

Y = Collateral in Use

Probit Estimation: Probability of Collateral Type

Personal Assets

Account

Receivables

Properties &

Equipment

SME dummy variable .22 -.42 -.44

(.12)* (.13)*** (.10)***

Firm age -.02 -.01 -.01

(.00)*** (.01)** (.00)

Export participation .00 .00 -.00

(.00) (.00) (.00)*

Foreign ownership -.76 -.09 -.26

(.18)*** (.16) (.12)**

Managerial experience .01 .01 .01

(.01)* (.01) (.00)**

Financial audit -.24 .01 -.44

(.10)** (.13) (.10)***

ISO certification -.24 .41 -.17

(.12)** (.13)*** (.10)*

Labor Intenstive .30 .13 .51

Industries (.14)** (.19) (.13)***

Capital Intensive .12 .25 .24

Industries (.13) (.17) (.11)**

constant -.70 -1.37 .80

(.18)*** (.23)*** (.16)***

observations 981 981 981 Note: This table reports regression results of collateral type (dummy dependent variable) and collateral/loan value (continuous dependent variable) on firm characteristics (control variables) for firms at different sizes. The estimation method is Probit. The analysis pools firm observations across PRC, Malaysia, Thailand, Indonesia, Philippines, and Viet Nam. Standard errors are in parentheses; *** (**, *) denotes statistical significance at 1 (5, 10) percent level.Source: Wignaraja and Jinjarak (2015).

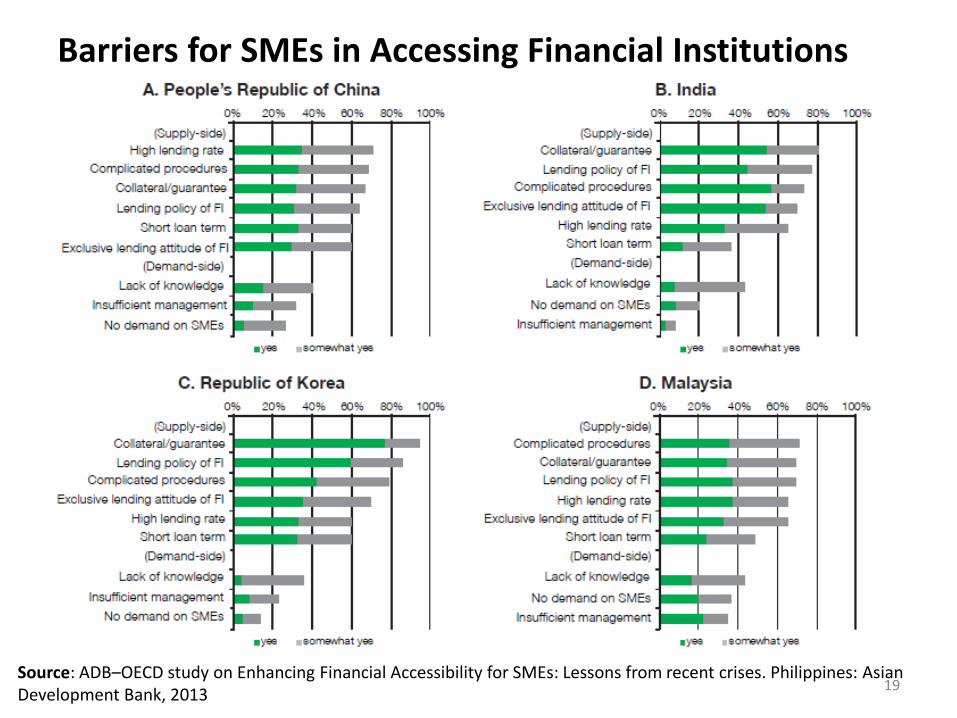

Barriers for SMEs in Accessing Financial Institutions

19Source: ADB–OECD study on Enhancing Financial Accessibility for SMEs: Lessons from recent crises. Philippines: Asian Development Bank, 2013

Policy Implications and Conclusion4.

20

Policy Implications

21

• No one size fits all solution to SME internationalization and finance in Asia

• Sustain open trade regimes, invest in traditional and ICT infrastructure, and streamline business regulations

• Affordable and high quality technical, marketing and other business support are useful to develop SMEs

• Develop a sound and effective financial system

Support bank privatization

Facilitate entry of reputable foreign financial firms

Foster stock and bond market development

Ensure adequate macroprudential regulation and capacity

Policy Implications

22

• Increase financial access for SMEs Introduce better credit rating and databases

Expand partial credit guarantees

Introduce innovative schemes to expand collateral

Scale up microfinance and link it to the financial system at large

Promote technology (e-finance) and alternative delivery (mobile banking)

Support private equity, venture capital and angel financing

Teach financial literacy from school onwards

Conclusion

23

• Firm-level analysis useful to explore links between trade, finance and SMEs

• SMEs important in Asia but are underrepresented in exports and supply chain trade SMEs that join supply chain trade are bigger, build technological capability

and skills, have greater access to credit and some foreign ownership

• The credit gap is severe - about 9 million Asian SMEs affected

• SMEs typically rely on internal or non-bank sources of finance for their activity

• SME characteristics influence bank borrowing Older, financially audited, exporting SMEs tend to borrow from banks Personal assets of SMEs matter as collateral

• No panacea for SME internationalization or financing

24

Selected References

• Wignaraja, G., (2015), “Factors Affecting Entry into Supply Chain Trade: An Analysis of Firms in Southeast Asia” Asia and the Pacific Policy Studies, March http://onlinelibrary.wiley.com/doi/10.1002/app5.78/full

• Wignaraja, G., and Jinjarak, Y., (2015). “Why SMEs Do Not Borrow from Banks? Evidence from People’s Republic of China and Southeast Asia”. ADBI Working Paper, No. 509. Tokyo: Asian Development Bank Institute. Available at: http://www.adbi.org/files/2015.01.09.wp509.why.do.sme.not.borrow.from.banks.pdf

• Jinjarak, Y., Mutuc, P.J., and Wignaraja, G. (2014), “Does Finance Really Matter for the Participation of SMEs in International Trade?” ADBI Working Paper, No. 470. Tokyo: Asian Development Bank Institute. Available at: http://www.adbi.org/files/2014.03.28.wp470.finance.matter.smes.trade.pdf

• Yoshino, N., Morgan, P. and Wignaraja, G. (2015), “Financial Education in Asia: Assessment and Recommendations”, Asian Development Bank Institute Working Papers No. 534, http://www.adb.org/sites/default/files/publication/161053/adbi-wp534.pdf