sm finaltooba iqbal

TRANSCRIPT

INSTITUTE OF BUSINESS MANAGEMENT

Researching ‘Firm level Strategy and Competitiveness’ for Sanofi Aventis Pakistan 2012

4/18/2012

Enterprise:Sanofi-Aventis Pakistan Ltd.Plot 23, Sector-22, Korangi Industrial Area,Karachi-74900, Pakistan

Research Partners:Syed Adnan Ali (Senior Product Manager)0321-2162306Omair Siddiqui (Assistant Product Manager)0333-2169734

Name of IoBM researchers:Ayena Maqbool (9098)Humaira Akhter (8970)Tuba Iqbal (8725)Naureen Ansari (8696)Nashaf Hashimi (9442)Mashal Balani (9824)

This research instrument is used for researching the Business Strategy of Sanofi Aventis Pakistan: its external and internal researched environment, its competitors and its strategic implementation framework.

LETTER OF TRANSMITTAL

April 18, 2012

Mr. Javaid Ahmed

Institute of Business Management, Karachi.

Respected Sir,

This is the term report on “Researching firm level strategy and competitiveness for Sanofi

Aventis 2012”.

The objective of the report was to research the business strategy of Sanofi Aventis Pvt. Ltd, its

vision and mission, its current strategies, its external and internal researched environment, blue

ocean strategy and evaluation of its strategic options.

The report has been completed after the perpetual hard work and determination of past 2 months.

If you have any additional questions, we would be pleased to answer them.

Thanking you.

Sincerely,

Ayena Maqbool (9098)

Humaira Akhter (8970)

Tuba Iqbal (8725)

Naureen Ansari (8696)

Mashal Balani (8924)

Nashaf Hashimi (9442)

LETTER OF AUTHORIZATION

April 18, 2012

Dear Reader,

As students of IoBM, we have been authorized by Mr. Javaid Ahmed to prepare a term report on

“Researching firm level strategy and competitiveness for Sanofi Aventis 2012”, for the course of

Strategic Management to be submitted on April 18, 2012

The preparation of this term report required us to perform a thorough analysis of the

pharmaceutical industry of Pakistan and formulate new strategies for Sanofi Aventis Pvt. Ltd. by

carrying out internal company and external environment analysis, along with the issues involving

strategic leadership and implementation in the company.

We would like to thank our course instructor; Mr. Javaid Ahmed for all the informative sessions

that he delivered through-out the semester which greatly enhanced our practical management

skills. We are extremely grateful for his guidance on this term report.

We would also like to thank Mr. Adnan Ali (Senior Product Manager) and Mr. Omair Siddiqui

(Assistant Product Manager) at Sanofi Aventis Pakistan Pvt. Ltd. for their co-operation in this

research project.

Sincerely,

Ayena Maqbool (9098)

Humaira Akhter (8970)

Tuba Iqbal (8725)

Naureen Ansari (8696)

Mashal Balani (8924)

Nashaf Hashimi (9442)

Contents

LITERATURE REVIEW.........................................................................6

CHAPTER # 1....................................................................................17

INDUSTRY STRUCTURE & MACRO-ENVIRONMENTAL ANALYSIS

........................................................................................................17

OVERVIEW OF PHARMACEUTICAL INDUSTRY IN PAKISTAN............18

PORTER’S 5 FORCES & PEST ANALYSIS FOR PAKISTAN

PHARMACEUTICAL INDUSTRY.............................................................22

INTRODUCTION OF COMPANY.............................................................31

MISSION STATEMENT...........................................................................36

ANALYSIS OF SANOFI’S MISSION STATEMENT..................................36

RECOMMENDED MISSION STATEMENT FOR SANOFI AVENTIS.......37

VISION STATEMENT..............................................................................37

EXTERNAL FACTOR EVALUATION MATRIX.........................................38

COMPANY AND COMPETITOR ANALYSIS............................................40

CHAPTER # 2....................................................................................41

INTERNAL COMPANY VALUE CHAIN ANALYSIS............................41

INTERNAL VALUE CHAIN ANALYSIS....................................................42

CORE COMPETENCIES OF SANOFI AVENTIS......................................48

STRATEGIC COST MANAGEMENT PROCESSES OF SANOFI AVENTIS

.................................................................................................................49

FINANCIAL RATIO TRENDS OF SANOFI AVENTIS..............................50

INTERNAL FACTOR EVALUATION MATRIX..........................................52

CHAPTER # 3....................................................................................54

STRATEGY ANALYSIS AND RECOMMENDATIONS.........................54

GENERIC STRATEGY FOR SANOFI AVENTIS.......................................55

TOWS MATRIX OF SANOFI AVENTIS....................................................56

INTERNAL EXTERNAL MATRIX OF SANOFI AVENTIS........................58

SPACE MATRIX FOR SANOFI AVENTIS................................................60

GRAND STRATEGY MATRIX FOR SANOFI AVENTIS:...........................63

BCG MATRIX FOR SANOFI AVENTIS....................................................65

MATRIX ANALYSIS & TOWS SUMMARY...............................................66

QUANTITATIVE STRATEGIC PLANNING MATRIX FOR SANOFI

AVENTIS..................................................................................................67

SELECTED STRATEGY FOR SANOFI AVENTIS.....................................70

CHAPTER # 4....................................................................................71

BLUE OCEAN STRATEGY................................................................71

BLUE OCEAN STRATEGY FOR SANOFI AVENTIS................................72

CHAPTER # 5....................................................................................74

STRATEGIC LEADERSHIP & IMPLEMENTATION..........................74

STRATEGIC LEADERSHIP MODEL FOR SANOFI AVENTIS..................75

THE FOUR INTERNAL HURDLES TO STRATEGY IMPLEMENTATION77

BIBLIOGRAPHY.................................................................................79

LITERATURE REVIEW

Strategy

Strategy is the direction and scope of an organization over the long-term which

achieves advantage for the organization through its configuration of resources within a

challenging environment, to meet the needs of markets and to fulfill stakeholder expectations.

Strategic Management

Strategic management is a field that deals with the major intended and emergent

initiatives taken by general managers on behalf of owners, involving utilization of resources, to

enhance the performance of firms in their external environments. It entails specifying the

organization's mission, vision and objectives, developing policies and plans, often in terms of

projects and programs, which are designed to achieve these objectives, and then allocating

resources to implement the policies and plans, projects and programs. A balanced scorecard is

often used to evaluate the overall performance of the business and its progress towards

objectives. Recent studies and leading management theorists have advocated that strategy needs

to start with stakeholders expectations and use a modified balanced scorecard which includes all

stakeholders.

Strategic Management Steps

a) Formulation

The stage of the strategic management process that involves planning and decision

making that leads to the establishment of the organization’s goals and of a specific

strategic plan.

b) Implementation

This stage of strategic management involves the use of managerial and organizational

tools to direct resources towards achieving strategic outcomes.

c) Evaluation

1

The final stage in strategic management is strategy evaluation and control. All strategies

are subject to future modification because internal and external factors are constantly

changing. In the strategy evaluation and control process managers determine whether the

chosen strategy is achieving the organization's objectives.

S trategic Management Framework

Certain strategic tools have

been used for analyzing the company

in focus throughout our research. For

external analysis, porter’s five forces

followed by PEST analysis have

been done which followed the

external factor evaluation (EFE) and

competitor profile matrix (CPM) for

relative positioning of the firm. Then

we have performed an Internal Audit

of the firm by examining the Value Chain Activities and determining the strengths and

weaknesses with respect to the company’s performance internally. This has been supported by an

Internal Factor Evaluation Matrix (IFE). Then with the help of all these we have tried to locate

the company in Porters Generic map and defined where the company is and where it should be to

gain a sustainable competitive advantage. This section of the report emphasises on defining each

and every tool that we have used in our report, along with relevant examples and figures chosen

from various sources.

Vision Statement

A vision statement is sometimes called a picture of your company in the future but it’s so

much more than that. Your vision statement is your inspiration, the framework for all your

strategic planning. In other words, a vision is a statement about what an organization wants to

become.

2

Mission Statement

A mission statement is a brief description of a company's fundamental purpose. A

mission statement answers the question, "Why do we exist?" A Mission Statement defines the

purpose of the organizations existence and its primary objectives. Its prime function is internal –

to define the key measure or measures of the organization's success – and its prime audience is

the leadership team and stockholders.

Porter’s Five Forces

Porter's five forces analysis is a framework for industry analysis and business strategy

development formed by Michael E. Porter of Harvard Business School in 1979. The most

influential analytical model for assessing the nature of competition in an industry is Michael

Porter's Five Forces Model, which is described below:

Porter explains that there are five forces that determine industry attractiveness and long-

run industry profitability. These five "competitive forces" are

3

i. Threat of New Entrants

New entrants to an industry can raise the level of competition, thereby reducing its

attractiveness. The threat of new entrants largely depends on the barriers to entry. High entry

barriers exist in some industries (e.g. shipbuilding) whereas other industries are very easy to

enter (e.g. estate agency, restaurants). Key barriers to entry include

• Economies of scale

• Capital / investment requirements

• Customer switching costs

• Access to industry distribution channels

• The likelihood of retaliation from existing industry players.

ii. Threat of Substitutes

The presence of substitute products can lower industry attractiveness and profitability

because they limit price levels. The threat of substitute products depends on:

• Buyers' willingness to substitute

• The relative price and performance of substitutes

• The costs of switching to substitutes

When the threat of substitutes is high, industry profitability suffers. Substitute products or

services limit an industry’s profit potential by placing a ceiling on prices. If an industry does not

distance itself from substitutes through product performance, marketing, or other means, it will

suffer in terms of profitability—and often growth potential.

iii. Bargaining Power of Suppliers

Suppliers are the businesses that supply materials & other products into the industry.

Supplier power is a mirror image of the buyer power. As a result, the analysis of supplier power

4

typically focuses first on the relative size and concentration of suppliers relative to industry

participants and second on the degree of differentiation in the inputs supplied. If suppliers have

high bargaining power over a company, then in theory the company's industry is less attractive.

The bargaining power of suppliers will be high when:

• There are many buyers and few dominant suppliers

• There are undifferentiated, highly valued products

• Suppliers threaten to integrate forward into the industry

• Buyers do not threaten to integrate backwards into supply

• The industry is not a key customer group to the suppliers

iv. Bargaining Power of Buyers

The bargaining power of buyers is greater when:

• There are few dominant buyers and many sellers in the industry

• Products are standardized

• Buyers threaten to integrate backward into the industry

• Suppliers do not threaten to integrate forward into the buyer's industry

• The industry is not a key supplying group for buyers

Buyer power is one of the two horizontal forces that influence the appropriation of the

value created by an industry. The most important determinants of buyer power are the size and

the concentration of customers. Other factors are the extent to which the buyers are informed and

the concentration or differentiation of the competitors. Kippenberger (1998) states that it is often

useful to distinguish potential buyer power from the buyer's willingness or incentive to use that

power, willingness that derives mainly from the “risk of failure” associated with a product's use.

v. Intensity of Rivalry

5

The intensity of rivalry, is the most obvious of the five forces in an industry, helps

determine the extent to which the value created by an industry will be dissipated through head-

to-head competition. High rivalry limits the profitability of an industry. The degree to which

rivalry drives down an industry’s profit potential depends, first, on the intensity with which

companies compete and, second, on the basis on which they compete. The intensity of rivalry is

greatest if competitors are numerous or are roughly equal in size and power. In such situations,

rivals find it hard to avoid poaching business. Industry growth is slow, Exit barriers are high, and

rivals are highly committed to the business and have aspirations for leadership.

Pest Analysis

PEST analysis stands for "Political, Economic, Social, and Technological analysis" and

describes a framework of macro-environmental factors used in the environmental

scanning component of strategic management.

The Pest Model

PEST is the acronym for Political, Economic, Social and Technological factors.

The internal environment is composed of the internal customers, which are the employees of the

organization, the internal policies, mission and vision. However, the external environment is a

broad category which has been divided into micro environment and macro environment. The

micro environment is made of factors such as the customers, suppliers, distributors, competitors

etc whereas; factors making up the macro environment include political, economic, social and

technological forces.

i. Political Factors

Political factors include government regulations such as employment laws, environmental

regulations and tax policy. Other political factors are trade restrictions and political stability.

They refer to the degree of intervention of government in the economy. There are certain formal

6

and informal rules laid down by the government which every organization has to abide by in

order to sustain its operations in a particular country. Important political factors include:

ii. Economic Factors

These affect the cost of capital and purchasing power of an organization. Economic

factors include economic growth, interest rates, inflation and currency exchange rates.

Economic factors are those which have a direct impact on the capital loss of organizations and

purchasing power of customers.

iii. Social Factors

Social factors are cultural aspects and demographic variables which are closely linked to

the market potential and customers’ needs. These include age distribution, attitude towards

health and environment, education, leisure activities, attitude towards career, changing lifestyle,

gender role etc.

iv. Technological Factors

Technology is what drives the phenomena of globalization. It provides competitive

advantage to firms. Major technological factors include rate of technological innovation, rate of

obsolesce of technology, technological development, new technological platforms, diffusion of

technology etc. Technology reduces costs, improves quality and leads to innovation. It can

benefit consumers as well as the organizations providing the products.

External Factor Evaluation

External Factor Evaluation (EFE) matrix method is a strategic-management tool often

used for assessment of current business conditions. The EFE matrix is a good tool to visualize

and prioritize the opportunities and threats that a business is facing. External factors assessed in

7

the EFE matrix are the ones that are subjected to the will of social, economic, political, legal, and

other external forces.

Internal Factor Evaluation

Internal Factor Evaluation (IFE) matrix is a strategic management tool for auditing or

evaluating major strengths and weaknesses in functional areas of a business. IFE matrix also

provides a basis for identifying and evaluating relationships among those areas. The Internal

Factor Evaluation matrix or short IFE matrix is used in strategy formulation. Internal factors

include management, manpower, machine, material and money.

Competitive Profile Matrix

Competitive profile matrix is essential tool used in strategic management process, it

contain all the important critical success factors of industry. Success factor can vary from

industry to industry, every industry consider different success factor, all the companies in CPM

are measured on same scale by considering the same success factor.

Critical success factors are extracted after deep analysis of external and internal

environment of the firm. Obviously there are some good and some bad for the company in the

external environment and internal environment. The higher rating show that firm strategy is

doing well to support this critical success factors and lower rating means firm strategy is lacking

to support the factor.

Michael Porter’s Generic Strategies

i. Cost Leadership Strategy

Cost leadership is perhaps the clearest of the three generic strategies. In it, a firm sets out

to become the low-cost producer in its industry. The firm has a broad scope and serves many

industry segments, and may even operate in related industries -- the firm's breadth is often

8

important to its cost advantage. The sources of cost advantage are varied and depend on the

structure of the industry

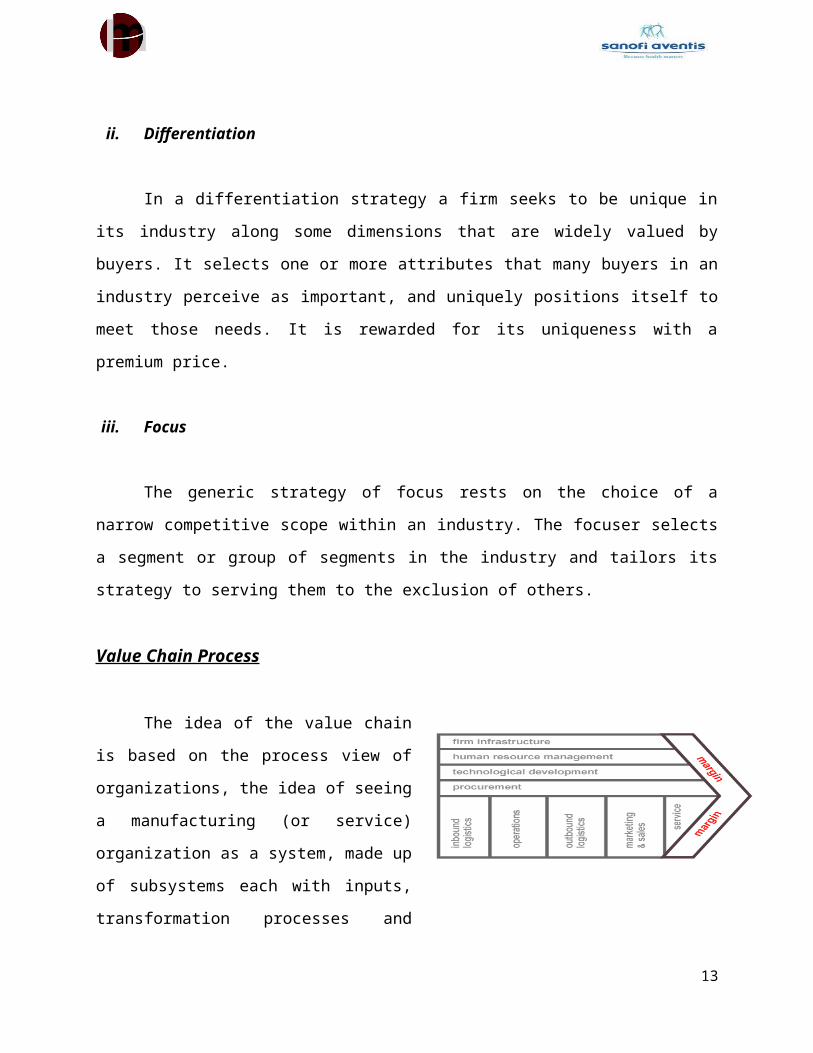

ii. Differentiation

In a differentiation strategy a firm seeks to be unique in its industry along some

dimensions that are widely valued by buyers. It selects one or more attributes that many buyers

in an industry perceive as important, and uniquely positions itself to meet those needs. It is

rewarded for its uniqueness with a premium price.

iii. Focus

The generic strategy of focus rests on the choice of a narrow competitive scope within an

industry. The focuser selects a segment or group of segments in the industry and tailors its

strategy to serving them to the exclusion of others.

Value Chain Process

The idea of the value chain is based on

the process view of organizations, the idea of

seeing a manufacturing (or service) organization

as a system, made up of subsystems each with

inputs, transformation processes and outputs.

Most organizations engage in hundreds, even

thousands, of activities in the process of

converting inputs to outputs. These activities can

be classified generally as either primary or support activities that all businesses must undertake

in some form.

According to Porter (1985), the primary activities are:

• Inbound Logistics - involve relationships with suppliers and include all the activities

required to receive, store, and disseminate inputs.

9

• Operations - are all the activities required to transform inputs into outputs (products

and services).

• Outbound Logistics - include all the activities required to collect, store, and

distribute the output.

• Marketing and Sales - activities inform buyers about products and services, induce

buyers to purchase them, and facilitate their purchase.

• Service - includes all the activities required to keep the product or service working

effectively for the buyer after it is sold and delivered.

Secondary activities are:

• Procurement - is the acquisition of inputs, or resources, for the firm.

• Human Resource management - consists of all activities involved in recruiting,

hiring, training, developing, compensating and (if necessary) dismissing or laying

off personnel.

• Technological Development - pertains to the equipment, hardware, software,

procedures and technical knowledge brought to bear in the firm's transformation of

inputs into outputs.

• Infrastructure - serves the company's needs and ties its various parts together, it

consists of functions or departments such as accounting, legal, finance, planning,

public affairs, government relations, quality assurance and general management.

Core Competencies

A core competence is the result of a specific unique set of skills or production techniques

that deliver value to the customer. Such competences empower an organization to access a wide

variety of markets. Executives should estimate the future challenges and opportunities of the

business in order to stay on top of the game in varying situations. . A core competence should be

"competitively unique"

10

Strategic Cost Management

Strategic cost management can be defined as" scrutinizing every process within your

organization, knocking down departmental barriers, understanding your suppliers' business, and

helping improve their processes"

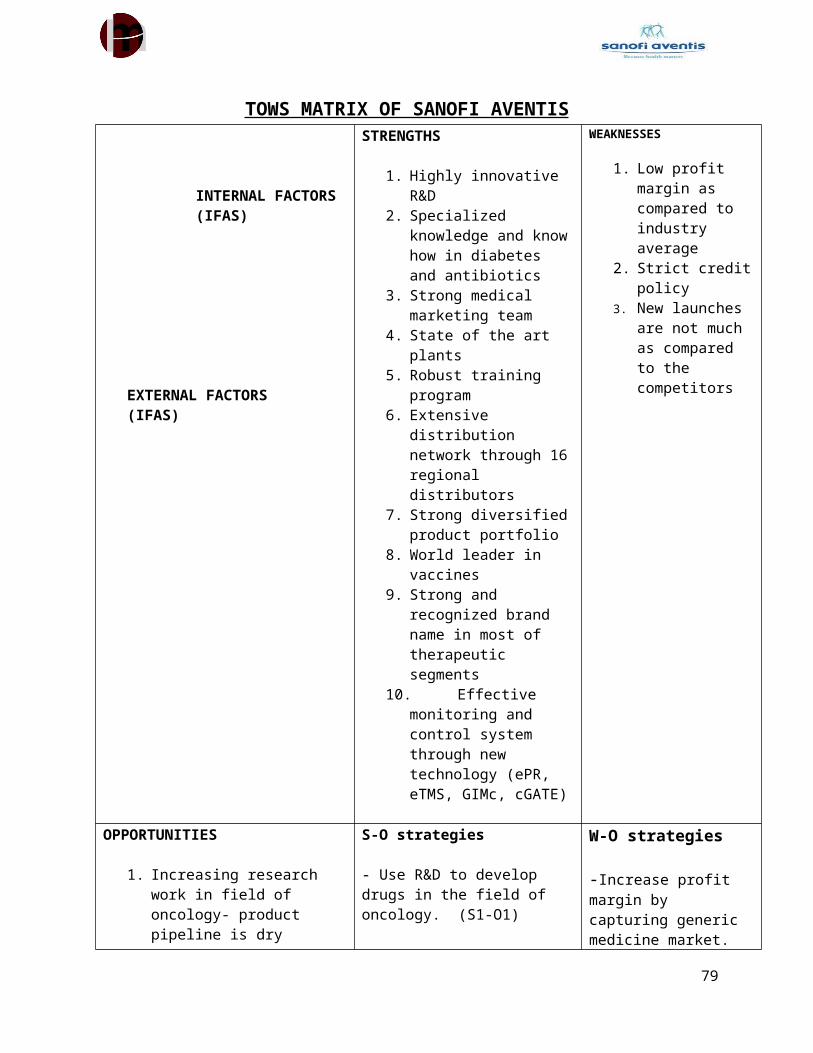

TOWS Matrix

TOWS Analysis is a variant of

the classic business tool, SWOT

Analysis. TOWS and SWOT are

acronyms for different arrangements of

the words Strengths, Weaknesses,

Opportunities and Threats. By analyzing

the external environment (threats and

opportunities), and your internal

environment (weaknesses and strengths),

you can use these techniques to think

about the strategy of your whole organization, a department or a team. You can also use them to

think about a process, a marketing campaign, or even your own skills and experience.

BCG Matrix

This helps the company allocate resources and is used as an analytical tool in brand

marketing, product management, strategic management, and portfolio analysis.

These groups are explained below:

Dogs: Low Market Share / Low Market Growth

In these areas, your market presence is weak,

so it's going to take a lot of hard work to get noticed.

You won't enjoy the scale economies of the larger

11

players, so it's going to be difficult to make a profit. And because market growth is low, it's

going to take a lot of hard work to improve the situation.

Cash Cows: High Market Share / Low Market Growth

Here, you're well-established, so it's easier to get attention and exploit new opportunities.

It's only worth expending a certain amount of effort, because the market isn't growing, and your

opportunities are limited.

Stars: High Market Share / High Market Growth

Here you're well-established, and growth is exciting! There should be some strong

opportunities here, and you should work hard to realize them.

Question Marks (Problem Child): Low Market Share / High Market Growth

These are the opportunities no one knows what to do with. They aren't generating much

revenue right now because you don't have a large market share. But, they are in high growth

markets so the potential to make money is there.

Internal External (IE) Matrix

IE stands for Internal external as the name suggest that it’s based upon internal and

external factors of the organization. The IE is an important strategic tool which comes under

the portfolio management considered much similar to BCG Matrix. The IE matrix used to plot

the organization divisions in nine cell diagram, each cell has some meaning associated which

suggests strategies. The IE matrix is a continuation of the EFE matrix and IFE matrix models. In

summarize way it can be defined as the strategic management tool which is used to analyze the

current position of the divisions and suggest the strategies for the future for the better results.

12

The IE matrix can be divided into three

major regions that have different strategy

implications.

Cells I, II, and III suggest the “grow and

build” strategy. This means intensive and

aggressive tactical strategies. Your strategies

should focus on market penetration, market

development, and product development.

From the operational perspective, a

backward integration, forward integration, and horizontal integration should also be

considered.

Cells IV, V, and VI suggest the “hold and maintain” strategy. In this case, your tactical

strategies should focus on market penetration and product development.

Cells VII, VIII, and IX are characterized with the harvest or exit strategy. If costs for

rejuvenating the business are low, then it should be attempted to revitalize the business.

In other cases, aggressive cost management is a way to play the end game.

GRAND STRATEGY MATRIX

Based on four important elements of rapid

market growth, slow market growth, strong

competitive position, and weak competitive

position, Grand Strategy Matrix has been emerged

into a dominant tool in formulating cross-functional

strategies. To simplify the job of identification and

selection of best fitting strategy the elements of the

Grand Strategy Matrix actually form a four quadrant

13

Matrix where relevant organizations in the analysis are positioned. Instead of different

organizations a firm with many divisions can plot its divisions across Grand Strategy Matrix for

the sake of devising best suited strategy for each division.

SPACE MATRIX

The SPACE matrix is a management tool used to analyze a company. It is used to

determine what type of a strategy a company should undertake. It focuses on strategy

formulation especially as related to the competitive position of an organization. The

SPACE matrix is constructed by plotting calculated values for the competitive advantage

(CA) and industry strength (IS) dimensions on the X axis. The Y axis is based on the

environmental stability (ES) and financial strength (FS) dimensions.

QUANTITATIVE STRATEGIC PLANNING MATRIX (QSPM)

Quantitative Strategic Planning Matrix (QSPM) is a high-level strategic

management approach for evaluating possible strategies. Quantitative Strategic Planning

Matrix or a QSPM provides an analytical method for comparing feasible alternative

actions. The QSPM method falls within so-called stage 3 of the strategy formulation

analytical framework. When company executives think about what to do, and which way

to go, they usually have a prioritized list of strategies. If they like one strategy over another one,

they move it up on the list. This process is very much intuitive and subjective. The QSPM

method introduces some numbers into this approach making it a little more "expert" technique.

Blue Ocean Strategy:

Blue oceans denote all the

industries not in existence today—the

unknown market space, untainted by

14

+1

+3

+2-6 -5 -4 -3 -2 -1

-6-5

-4-3

-2-1

+1

+2

+3

+4

+5

+6

ES

CA

IS

Defe n

si veC

omp

e titi ve

Ma

rket

De

velo

pm

en

t

Ma

rket

Pe

ne

tratio

n

Pro

du

ct

De

velo

pm

en

t

Ho

rizon

tal

Int e

grat io

n

Div

estu

re

Liq

uid

at io

n

Ma

rket

De

velo

pm

en

t

Ma

rket

Pe

ne

trati

on

Pro

du

ct

dev

elop

me

nt

Fo

rwa

rd

int e

grat i

on

Ba

ckw

a rd

in

t eg

rat io

n

Ho

rizon

ta

l in

t eg

rat io

n

Co

nce

nt

ric

int e

grat i

on

Re

tren

ch

men

t

Co

nce

ntric

d

iversifi ca

tion

Ho

rizon

tal

Div

ersif ic

ation

Co

ng

lom

erat e

d

iversifi ca

tion

Div

estu

re / L

iqu

ida

t ion

Co

nce

ntric

D

ivers

if icatio

n

Ho

rizon

tal

Div

ersif ic

ation

Co

ng

lom

erat e

D

ivers

if icatio

n

Jo

i nt V

en

ture

s

competition. In blue oceans, demand is created rather than fought over. There is ample

opportunity for growth that is both profitable and rapid. There are two ways to create blue

oceans. In a few cases, companies can give rise to completely new industries, as eBay did with

the online auction industry. But in most cases, a blue ocean is created from within a red ocean

when a company alters the boundaries of an existing industry. As will become evident later, this

is what Cirque did. In breaking through the boundary traditionally separating circus and theater,

it made a new and profitable blue ocean from within the red ocean of the circus industry. The

main factor of blue ocean strategy is to create value (value innovation).

Tipping Point Leadership

The theory of tipping points, which has its roots in epidemiology, is well known; it

hinges on the insight that in any organization, once the beliefs and energies of a critical mass of

people are engaged, conversion to a new idea will spread like an epidemic, bringing about

fundamental change very quickly. The theory suggests that such a movement can be unleashed

only by agents who make unforgettable and unarguable calls for change, who concentrate their

resources on what really matters, who mobilize the commitment of the organization’s key

players, and who succeed in silencing the most vocal naysayers.

15

CHAPTER # 1

INDUSTRY STRUCTURE & MACRO-ENVIRONMENTAL ANALYSI S

16

OVERVIEW OF PHARMACEUTICAL INDUSTRY IN PAKISTAN

Pakistan’s Pharmaceutical industry is a rapidly growing industry which is highly

competitive and challenging as well, thus contributes significantly to the national economy. At

the time of independence in 1947, there were hardly any pharmaceutical companies in Pakistan.

The foundation of the pharmaceutical industry of Pakistan was formally laid in 1950 with the

establishment of local subsidiaries of foreign firms and formulation of imported raw material

based medicines by local entrepreneurs.

The pharmaceutical sector is also one of the most organized and regulated sectors of

Pakistan; the companies are fully documented and the prices of the medicines are set by the

government by giving an upper cap. There are 2 associations of the pharmaceutical

manufacturers:

• Pakistan Pharmaceutical Manufacturers Association (PPMA)

• Pharma Bureau (PB)

As of today there are about 600 Pharmaceutical companies operating in Pakistan out of

which 386 are operating units and among them, 30 are MNCs producing the drugs (Aamir and

Zaman, 2011). National companies comprise of the majority 55% of the companies in the

industry and the fact is that this has risen over the years depicting an encouraging sign for the

local investors. The top 50 companies have 82% of the market share. The Pakistani

Pharmaceutical industry is growing at an annual growth rate of 11%, which is more than the

annual global growth rate of 8%. 80% of the local demand is met domestically while 20% is met

through imports.

. As of 2012, the total export value of Pakistani-manufactured medicines around the

world stood at $400 million. The pharmaceutical industry is focusing to an Export Vision of USD

500 Million by 2013. In the meantime, exports are also likely to be boosted by new regional and

global opportunities.

17

Major Players in Industry

Name Market Share

Gsk 11.6%

Abbott Lab 7.9%

Highnoon Labs 6.3%

Getz Pharma 3.9%

Sanofi Aventis 3.8%

Roche 3.1%

Source: (Aamir and Zaman, 2011)

RESEARCH IN PHARMACEUTICAL SECTOR:

Pakistan’s contribution to pharmaceutical research is very limited despite the fact that we

are the world’s sixth largest country in terms of population. In Pakistan, most research is being

done in oncology, hepatitis, cardiovascular diseases, infectious diseases, respiratory diseases,

diabetes and thrombocytopenia.

The major chunk of the research work is done by the MNCs in Pakistan, whereas in

India, the national pharmaceutical companies have the majority contribution in the Research and

18

Some Key Statistics Of The Industry

Registered drugs 47000

Registered molecules 1100

R&d expenditures 1% of profit

Average growth rate 11%

Market share of multinational

companies

45%

Market share of local companies 55%

Market leader Glaxosmithkline

development. Most of the companies only allocate about 1% - 2% of the total budget for the

research and development. The major hurdle in research in local pharmaceutical companies was

the lack of government interest. Without government support, the private sector cannot use even

its available expertise to develop new products

Key Trends & Developments

Leaders of Pakistan's pharmaceutical industry have condemned the cabinet's recent

unanimous decision to grant Most Favoured Nation (MFN) trading status to India. While the

decision will benefit Indian trade to Pakistan, including the export of medicines to Pakistan -

ultimately enforcing competitive pressure on the local pharmaceutical industry, BMI (Business

Monitor International) believes the agreement will be of significant benefit to patients,

improving their access to affordable medicines.

According to BMI the creation of six Drug Regulatory Authorities and the replication of

operations by the authorities will create inefficiencies in the drug approvals process in Pakistan,

which will not sit well with local or multinational drug makers. Furthermore, the shift from one

regulatory authority to six will lead to more bureaucracy, increasing drug maker’s operational

costs. (Pakistan Pharmaceuticals and Healthcare Report Q2 2012)

Challenges Faced By the Pharmaceutical Industry Of Pakistan

No doubt that the Pakistan pharmaceutical market is growing at a steady rate but there are certain

challenges which pose a great threat to the industry.

The first major challenge which the pharmaceutical industry faces is the total government

control on the prices of all the enlisted products

Import of raw material which costs a lot of precious foreign exchange

Rapid devaluation of the rupee against the major currencies, due to which the profit

margins are shrinking

Increasing cost of manpower and energy

19

Low R&D expenditure, which can lead to the suffering of the masses for not conducting

sufficient research on the newly emerging diseases in the Pakistani environment

Political instability is another major factor which is emerging as the major challenge to

the pharmaceutical industry, because of discontinuation of the policies

Last but not the least, the deteriorating law and order situation, due to which most of

companies have suffered in terms of sales and also lack of reach to the customers in the

affected areas

Market access is challenging and operational risks are high

Although Pakistan’s pharmaceutical and healthcare sectors are expanding and evolving

rapidly, about half the population has no access to modern medicines like in Baluchistan and

Khyber Pakhtunkhwua. Clearly this presents an opportunity, but much more work needs to be

done by the government and industry's stakeholders. The value of pharmaceuticals sold in 2007

exceeded US$1.4bn, which equates to per capita consumption of less than US$ 10 per year and

value of medicines sold is expected to exceed US$2.3 B by 2012.

20

PORTER’S 5 FORCES & PEST ANALYSIS FOR PAKISTAN PHARMACEUTICAL INDUSTRY

THE THREAT OF NEW ENTRANT Yes (+) No (-)

1. Do large firms have a cost or performance advantage in your segment of the industry?

2. Are there any proprietary product differences in your

industry?

3. Are there any established brand identities in your industry?

4. Do your customers incur any significant costs in

switching suppliers?

5. Is a lot of capital needed to enter your industry? 6. Is serviceable used equipment expensive? 7. Does the newcomer to your industry face difficulty in

accessing distribution channels?

8. Does experience help you to continuously lower costs? 9. Does the newcomer have any problems in obtaining the

necessary skilled people, materials or supplies? 10. Does your product or service have any proprietary

features that give you lower costs?

11. Are there any licenses, insurance or qualifications that are difficult to obtain?

12. Can the newcomer expect strong retaliation on entering

the market?

The table above suggests that the barriers to entry in the pharmaceutical industry of

Pakistan are quite high in case of setting up a totally new pharmaceutical company. This is

because the existing firms in the industry have achieved economies of scale through increasing

their capital intensity while the setup costs would be very high for the new entrants as expensive

state-of-the-art machinery is required for operations in the pharmaceutical industry. Also, new

firms find it very difficult to acquire licenses and other qualifications from the regulatory bodies.

Moreover, the major portion of the market share is held by a few firms. These well

established firms make it tough for new firms to enter into the industry, because of the strong

21

brand image that these firms have in the market. Thus this low threat of new entrants makes it a

favorable point for the industry.

P - Factors like deteriorated law and order situation and approval from Ministry of Health

increases barriers to entry. Prices of medicines are dictated and regulated by MoH so it is also

lowering down the threat of new entrants. MFN status to India will increase the threats of new

entrants as in the form of importers and Indian Pharmaceutical industry will likely to pose great

threat on the existent pharmaceutical industry of Pakistan.

E - The industry is growing rapidly but the prices of raw materials which are usually imported

from foreign countries are increasing because of rupee depreciation. It is unlikely for the

pharmaceutical companies to put the burden on consumers in the form of higher prices as the

prices are being controlled by MoH. The high rate of inflation is also decreasing the threat of

new entrants.

S - No significant effect

T - High technology is required to manufacture drugs and that requires large amount of capital

investment which is again an obstacle for new entrants. Moreover, the technical equipments are

also very expensive which increase the barriers to entry.

Low Moderate High

22

P

E

T

BARGAINING POWER OF BUYERS Yes (+) No (-)

1. Are there a large number of buyers relative to the number of firms in the business?

2. Do you have a large number of customers, each with

relatively small purchases?

3. Does the customer face any significant costs in switching suppliers?

4. Does the buyer need a lot of important information? 5. Is the buyer aware of the need for additional information? 6. Is there anything that prevents your customer from taking

your function in-house?

7. Your customers are not highly sensitive to price. 8. Your product is unique to some degree or has accepted

branding.

9. Your customers’ businesses are profitable 10. You provide incentives to the decision makers.

The primary customers of pharmaceutical companies are the doctors of the country, who

then help to increase the general consumption of that medicinal drug by prescribing it to their

patients i.e. the general public. If the pharmaceutical industry of Pakistan is growing at a rate of

12.9% annually, then naturally the demand is coming from the grass root level. So, there is large

number of buyers relative to the number of existing firms in the business. There is not much cost

associated with customers switching suppliers, however, there is an enormous amount of

information that the customers need about the products; also these customers are aware of the

additional information needed.

The customers are price sensitive for certain brands but ready to buy some brands at any

price because of their life-saving characteristic. Also, the existing products are unique to some

degree and have accepted branding. Overall, the bargaining power of buyers is low, making the

industry structure attractive.

P - No significant effect.

23

EST

E - Government of Pakistan has only provided Rs 40 billion for both health and education

sectors in the fiscal budget and also the minimum wage rate is also considerably low in the

country. These factors tend to increase the bargaining power of buyers as they are forced to opt

for low performing, cheap substitutes available in the form of homoeopathic drugs etc.

.

S – Because of increase in awareness of health related issues, people are becoming more health

conscious. They are getting more concerned about the medicines that are being prescribed to

them. As a result, doctors prescribe medicines of only those companies whose products are

superior in quality and have a good history. This factor tends to increase the bargaining power of

buyers.

T - With the advancement of information and technology, more and more researches about new

diseases and their cures are being conducted. All this information is being provided to the

doctors, who are keeping themselves updated through various seminars, journals, etc, and are

becoming more concerned about the quality of the products. This factor is also increasing the

bargaining power of buyers.

24

Low Moderate High

THREAT OF SUBSTITUTES Yes (+) No (-)

1. Substitutes have performance limitations that do not completely offset their lowest price. Or, their performance is not justified by their higher price.

2. The customer will incur costs in switching to a substitute. 3. Your customer has no real substitute. 4. Your customer is not likely to substitute.

The threat of substitutes is low in this industry as there are no real substitutes of the

products in the pharmaceutical industry. Availability of the herbal and homeopathic medicines,

does affect the products a bit but these medicines have significant performance limitation. Due to

the threat of different new diseases people are less willing to take chances with homeopathic and

herbal medicines and follow the instructions of their doctors.

P - No significant effect.

E – Availability of substitutes such as homeopathic, herbal products and home remedies at

cheaper prices, gives rise to threat of substitutes. In Pakistan there are a large number of people

who are not economically strong and cannot afford the medicines so they tend to move towards

the homeopathic and herbal medicines that are much cheaper. This factor increases threat of

substitutes.

S – The low literacy rate and lack of awareness sometimes make people move towards

homeopathic medicines. This factor also increases threat of substitutes.

T - No significant effect.

Low Moderate High

25

E

S

BARGAINING POWER OF SUPPLIERS Yes (+) No (-)

1. My inputs are standard rather than unique or differentiated.

2. I can switch between suppliers quickly and cheaply. 3. My suppliers would find it difficult to enter my business

or my customers would find it difficult to perform my function in-house.

4. I can substitute inputs readily. 5. I have many potential suppliers. 6. My business is important to my suppliers. 7. My cost of Purchases has no significant influence on my

overall costs.

In order to remain competitive in the pharmaceutical industry, the inputs used by each

company, such as various chemicals are mostly unique & differentiated and therefore cannot be

easily substituted. The company goes through a complicated process of selecting its suppliers in

order to make sure the quality of inputs match the company’s specific criteria so this is a costly

process for companies, and therefore they do not switch between suppliers and intend to stick to

limited amount of suppliers who pass their selection criteria. Thus, all these factors contribute to

moderately high bargaining power of suppliers.

P - No effect

E - The major inputs are imported from foreign countries like at Sanofi, raw materials are

majorly imported from France and Germany. So the rupee depreciation and rise in inflation

would increase the cost of raw materials in the industry and hence adversely affecting the

industry structure and due to the price control by Ministry of Health, it is not possible for

companies to shift the burden of cost on consumers. This factor increase the bargaining power of

suppliers.

S - No significant effect

26

T - In order to come up with innovative, differentiated, and superior quality products,

pharmaceutical companies demand for superior quality and state-of-the-art supplies. This factor

tends to reduce the bargaining power of suppliers.

E

T

Low Moderate High

THREAT OF RIVALRY Yes (+) No (-)

1. The industry is growing rapidly. 2. The industry is not cyclical with intermittent overcapacity. 3. The fixed costs of the business are relatively low portion

of total costs.

4. There are significant product differences and brand identities between the competitors.

5. The competitors are diversified rather than specialized. 6. It would not be hard to get out of this business because

there are no specialized skills and facilities or long-term contract commitments etc.

7. My customers would incur significant costs in switching to a competitor.

8. My product is complex and requires a detailed

understanding on the part of my customer.

9. My competitors are all of approximately the same size as I am.

The pharmaceutical industry is growing at a rate of 12.9% annually and is highly

competitive. The ratio of MNC and national companies is 54% and 46% respectively. There are

noteworthy product differences and brand identities in the pharmaceutical industry. Also it is not

easy to exit in the industry since there are long-term commitments and specialized needed. The

consumers (general public) do not incur any significant costs in switching to competitors

products but usually the decision is influenced by the doctor’s prescription. The products are

27

PES

complex and require total compliance to international standards. This analysis shows that the

rivalry among existing competitors in the industry is moderate.

P - Due to the decision of MFN status to India, the pharmaceutical companies are threatened to

lose their market share and thus this factor can bring rivalry among competitors.

E - Since companies can’t pass the burden on the consumers and the cost of producing drugs is

also increasing so they try to get the market shares by aggressive marketing practices which in

resultant is increasing the rivalry among competitors.

S - The changing trend towards higher consumer awareness about health issues, diseases, and

drugs require the companies to come up with innovative products and market them extensively.

This factor tends to increase the rivalry in the industry.

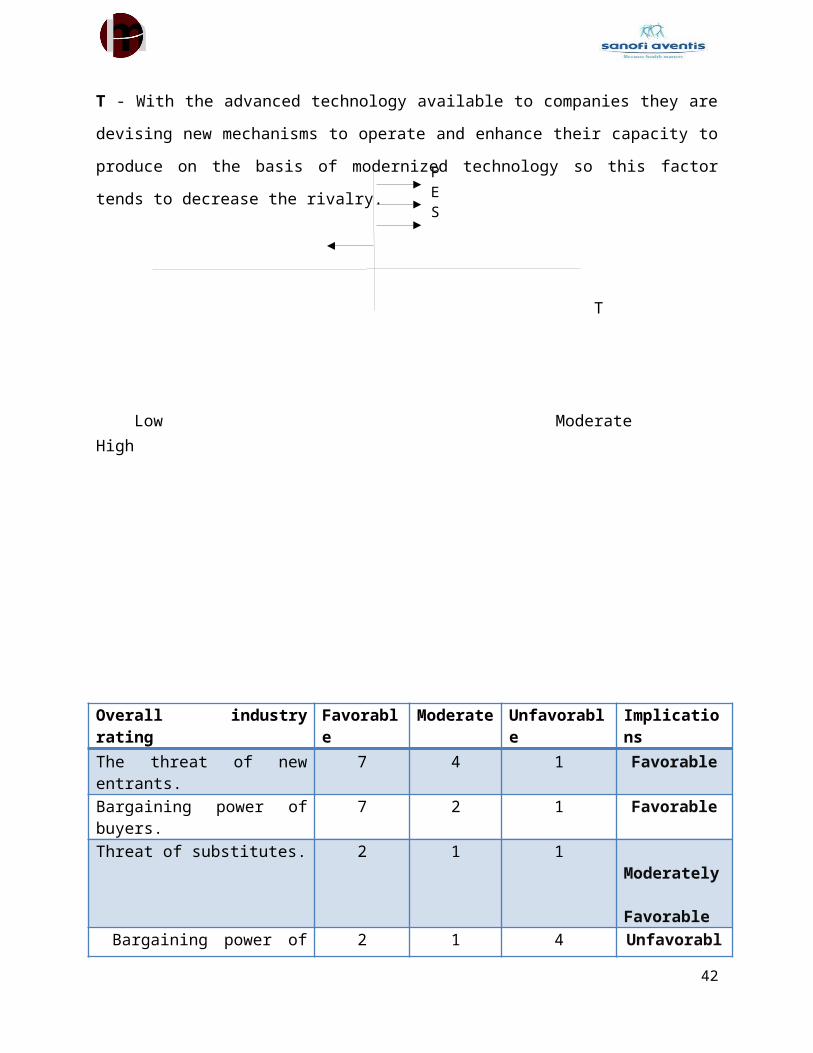

T - With the advanced technology available to companies they are devising new mechanisms to

operate and enhance their capacity to produce on the basis of modernized technology so this

factor tends to decrease the rivalry.

T

Low Moderate High

28

Overall industry rating Favorable Moderate Unfavorable Implications

The threat of new entrants. 7 4 1 Favorable

Bargaining power of buyers. 7 2 1 Favorable

Threat of substitutes. 2 1 1 ModeratelyFavorable

Bargaining power of suppliers.

2 1 4 Unfavorable

Intensity of rivalry among competitors.

3 2 4 Moderately favorable

Total 21 10 11 Favorable

29

INTRODUCTION OF COMPANY

Group Profile

Sanofi is a diversified global healthcare leader, focused on patients’ needs, researching

and developing medicines and vaccines to help improve the lives of the greatest possible number

of people. The company’s growth is attributable to a regional approach to business operations,

backed by a comprehensive portfolio of innovative products, mature prescription medicines,

consumer health products, generics, vaccines as well as animal health. By virtue of its

commitments, Sanofi constantly adapts its development model to the world’s emerging human

and economic problems.

Corporate Profile

The company was incorporated on December 8, 1967 as Hoechst Pakistan Limited.

Manufacturing of pharmaceuticals and specialty chemicals started in 1973. In 1977 the company

went public and was listed on the Karachi Stock Exchange. Agrochemical formulation started in

1985. In 1996, the Agriculture business was spun off into a separate legal entity called AgrEvo

Pakistan (Private) Limited, and the following year, Specialty Chemicals business was sold to

Clariant Pakistan Limited. Hoechst Pakistan Limited changed its name to Hoechst Marion

Roussel (Pakistan) Limited in June 1996, and the core business was then restricted to

pharmaceutical activities. In December 1999, Hoechst AG & Rhone Poulenc S.A. globally

merged their life sciences business into a new company known as Aventis S.A. The name of the

company in Pakistan was changed to Aventis Pharma (Pakistan) Limited in November 2000. In

line with the amalgamation globally, Aventis Pharma (Pakistan) Limited was merged locally

with Rhone Poulenc Rorer Pakistan (Private) Limited and the company changed it’s name to

Aventis Limited from April 2003. During 2004 Aventis S.A. was acquired by sanofi synthelabo

to form a company called sanofi-aventis S.A. Consequently in September 2005 the name of the

company was changed to sanofi-aventis Pakistan limited. In 2011, sanofi-aventis changed its

identity to Sanofi. However, the legal entity continues to remain the same i.e sanofi-aventis

30

Pakistan limited. Today, Sanofi is the 6th largest pharmaceutical company in Pakistan with a

market share and growth rate of 4.1% (2010: 4.5%) and 16% (2010: 19.3%) respectively. Today,

Sanofi S.A. France, is one of the world’s leading diversified healthcare companies offering

medicines, consumer healthcare products, generics and animal health products.

Therapeutic Areas

The company focuses on 7 major therapeutic areas to address the health needs of the greatest number

Cardiovascular

Vaccines

Thrombosis

Internal medicine

Metabolic disorders

Central nervous system

Oncology

Corporate Structure

31

Top products

Business Development

Sanofi Pakistan has set a vision to reach Rs. 15 billion mark by the year 2015. The

Business Development function will play a pivotal role in making this vision a reality by

preparing to build a strong inorganic growth platform in the form of pre-launch planning for new

product launches and new business additions to existing and new markets. Additionally,

diversification of portfolio; identification of new channels and geographies for business

expansion and external alliances and partnerships are all strategies which will help move towards

this vision.

Corporate Social Responsibility

32

Sanofi’s approach to Corporate Social Responsibility (CSR) inspires all its activities

while focusing on four main dimensions: Addressing patients’ needs - Patient Ensuring ethical

integrity in business and research - Ethics Promoting social commitments - People Limiting the

Group’s impact on the environment – Planet

Ethics & Compliance

Ethics is an integral part of the culture at sanofi-aventis Pakistan & guides the behavior

and conduct of all employees enabling them to meet objectives efficiently, transparently and

fairly. To keep in line with the changing industry dynamics, a new Code of Ethics was launched

during the year. Employees were given extensive training on the new code, which was launched

both in english and urdu languages.

33

Core Business Values

At sanofi-aventis, values define their ethics and serve as the moral compass of the

company. They are the DNA of the company and distinguish us from other companies. Values

are how they all think, act and feel. It is the values they hold that make them the people and the

company they are. Therefore, values define what they do and how they behave. These are the

values that every member of sanofi-aventis, in every continent, in every country, in every part of

the organisation, lives day to day.

34

InnovationForward-ThinkingWe encourage our people and partners to embrace creative solutions and excel through entrepreneurship.

Confidence

Standing OutWe are confident; standing up for what we believe in and pursuing our goals passionately. Always resilient, we dare to challenge the norm.

Respect

Embracing DifferenceWe recognise and respect the diversity and needs of our people, patients and partners, ensuring transparent and constructive interactions through mutual trust.

Solidarity

Socially ResponsibleWe are united in shared responsibility for our actions, our people, the wellbeing of our patients and in achieving a sustainable impact on the environment.

IntegrityActing EthicallyWe commit to maintain the highest ethical and quality standards without compromise.

MISSION STATEMENT

Sanofi’s mission includes:

• Create value by rapidly launching and successfully marketing innovative pharmaceuticals

that satisfy unmet medical needs in large patient populations.

• Focus commercial resources on strategic brands to drive sales growth and maximize the

value of existing and new global brands.

• Aggressively recruit and retain top talent, enhancing our capabilities in drug innovation

and commercialization.

ANALYSIS OF SANOFI’S MISSION STATEMENT

Determining the essential components in the company’s mission statement

Customer Yes

Product and Services Yes

Market Yes

Technology No

Survival, Growth, Profit Yes

Philosophy No

Self concept Yes

Concern for public Yes

Concern for employees Yes

35

Recommended statements for missing components:

1. Technology

Sanofi aims to utilize state of the art technology to make the organization technologically

efficient and for effective business operations.

2. Philosophy

Sanofi aims to provide best of them to customers and create values for themselves.

RECOMMENDED MISSION STATEMENT FOR SANOFI AVENTIS

“Create value by rapidly launching and successfully marketing innovative pharmaceuticals that

satisfy unmet medical needs in large patient populations. Focus commercial resources on

strategic brands to drive sales growth and maximize the value of existing and new global brands.

Aggressively recruit and retain top talent, enhancing our capabilities in drug innovation and

commercialization. It aims to utilize best of their resources to make the organization

technologically efficient and for effective business operation and provide best of them to

customers and create values for themselves.”

VISION STATEMENT

To become a diversified healthcare leader, focused on patients’ needs

Valued by patients & healthcare providers

Sought-after as an employer

Respected by the scientific community & our competitors

36

EXTERNAL FACTOR EVALUATION MATRIX

Critical Success Factors Weight Rating

Weighted

Score

Opportunities

Increasing research work in field of oncology- product

pipeline is dry 0.08 2 0.16

Pakistan pharmaceutical is US $2billion industry with

growth rate of 12.9% per annum. 0.05 4 0.20

Pakistan's high population growth rate 0.04 3 0.12

Emergence of new diseases 0.05 3 0.15

Some affected markets are not completely catered 0.05 2 0.10

Growing market of blood and blood forming organs 0.06 2 0.12

Growth in generic sector 0.1 3 0.30

Threats

Rising cost of production due to high inflation (10.8%)

and devaluation of local currency 0.09 3 0.27

Aggressive competition by local companies due to their

ability to launch new products in short time. 0.08 2 0.16

40-50% fake and Counterfeit drugs available in market 0.06 2 0.12

MFN status to India opens up avenues for Indian

pharmaceutical companies to Pakistan 0.04 1 0.04

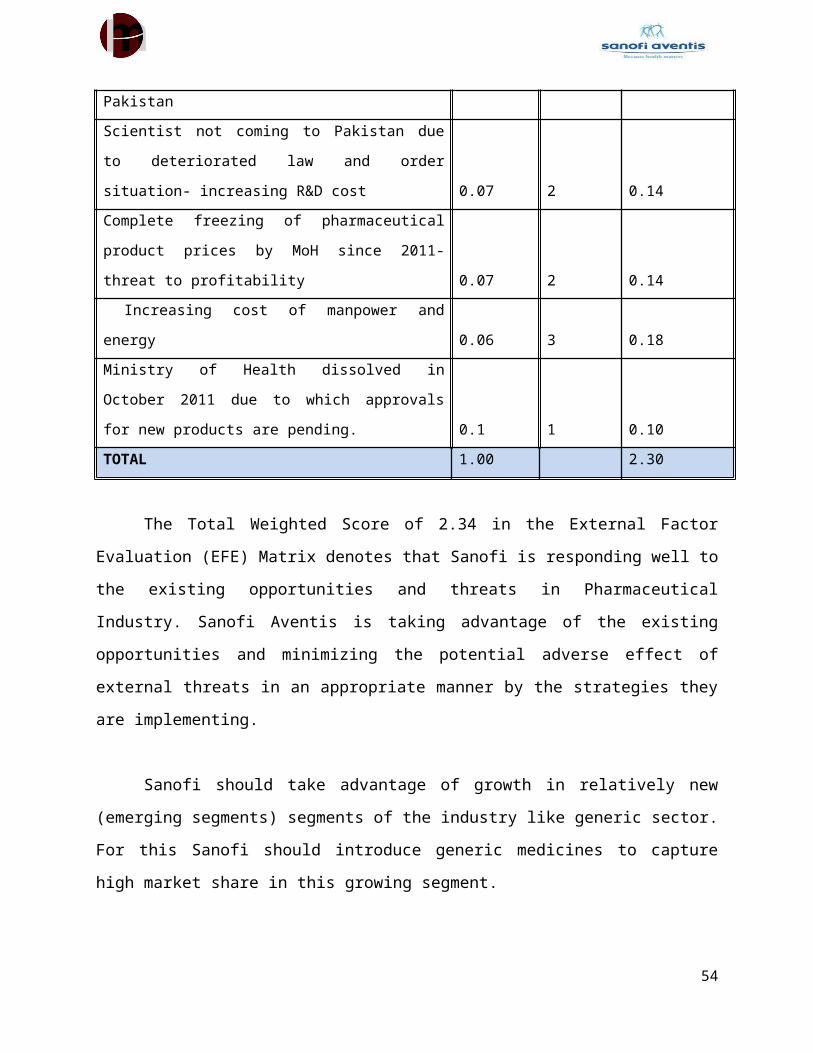

Scientist not coming to Pakistan due to deteriorated law

and order situation- increasing R&D cost 0.07 2 0.14

Complete freezing of pharmaceutical product prices by

MoH since 2011- threat to profitability 0.07 2 0.14

Increasing cost of manpower and energy 0.06 3 0.18

Ministry of Health dissolved in October 2011 due to

which approvals for new products are pending. 0.1 1 0.10

TOTAL 1.00 2.30

37

The Total Weighted Score of 2.34 in the External Factor Evaluation (EFE) Matrix

denotes that Sanofi is responding well to the existing opportunities and threats in Pharmaceutical

Industry. Sanofi Aventis is taking advantage of the existing opportunities and minimizing the

potential adverse effect of external threats in an appropriate manner by the strategies they are

implementing.

Sanofi should take advantage of growth in relatively new (emerging segments) segments

of the industry like generic sector. For this Sanofi should introduce generic medicines to capture

high market share in this growing segment.

Moreover Sanofi should guard against the threat of the rising costs due to high inflation

(10.8% - as reported in March 2012) and devaluation of local currency. In the face of rising

economic instability and exchange rate fluctuation, Sanofi should try to build partnerships with

low cost suppliers particularly within Asia in order to reduce the cost of imports of raw

materials.

38

COMPANY AND COMPETITOR ANALYSIS

Key players in Pakistan’s pharmaceutical industry include Glaxo Smith Kline, Sanofi

Aventis, Abbott and Getz Pharma.

Sanofi Aventis GSK Abbott Getz

Critical Weighte

d Weighte

d Weighte

d Weighte

d

Success Factors Weigh

t Rating Score Rating Score Rating ScoreRatin

g Score Product Quality 0.20 3 0.60 4 0.80 4 0.80 4 0.80Investment in R&D 0.15 4 0.60 4 0.60 3 0.45 3 0.45Financial Position 0.15 2 0.30 4 0.60 3 0.45 4 0.60Global Expansion 0.20 4 0.80 4 0.80 4 0.80 3 0.60Market share 0.10 2 0.20 4 0.40 3 0.30 2 0.20Distribution 0.10 3 0.30 4 0.40 4 0.40 3 0.30Positive brand image 0.05 4 0.20 4 0.20 4 0.20 4 0.20Promotion 0.05 3 0.15 3 0.15 3 0.15 2 0.10

Total 1.00 3.15 3.95 3.55 3.25

The overall position of Sanofi is fine. However, it needs to improve its financial position.

The profit margins are considerably lower than the industry average. Sanofi needs to introduce

new products and diversify its product line by capturing untapped markets in order to increase

and improve their overall financial position. Also, Sanofi should not compromise on its quality

as this would make them lose their customer base. The pharmaceutical companies do not have

any other option to increase their market share except for building a strong customer base which

can be achieved b providing the customers good quality products.

39

CHAPTER # 2

INTERNAL COMPANY VALUE CHAIN ANALYSIS

40

INTERNAL VALUE CHAIN ANALYSIS

Support activities:

i. Firm Infrastructure:

For meeting global standards, Sanofi realizes the importance of a good infrastructure. Its

plants that are based in Karachi and Wah Cantt provide highest standard of quality and

innovative pharmaceutical products.

Haemaccel Plant, which is the first blood plasma substitute manufacturing facility

in Pakistan has a capacity of over 2 million bottles per year. This plant is a result

of transfer of state-of-the-art German technology to Pakistan.

Claforan Plant is considered as one most modern facility in the entire Asia Pacific

region equipped with online filling and packaging operation and has a dedicated

quality control laboratory meeting international standards. In order to avoid cross

contamination, the technical area of the plant is installed with air handling units

separately.

Oral Liquid Plant is a highly sophisticated, state of the art facility complying with

the latest GMP and HSE standards. All manufacturing and cleaning activities are

handled here. The packaging suite is integrated and has steaming manufacturing

suite and comprising high-speed compact line installed by Marchesisni from Italy.

Pharma Manufacturing Plant has an extensive granulation, compression and

blistering operations allowing production of more than 1.5 billion tablets and

capsules per year.

ii. Human Resource Management:

Sanofi takes pride in the excellence of their human assets and teams who are committed

towards the organizational success. The employees are professionally trained, motivated

workforce, working as a team in an environment, which recognizes and rewards performance,

41

innovation and creativity. The human resource policies, developmental programs and

promotion/incentive activities all revolve around creating an exemplary team. At Sanofi the

following concerns pertains to HR:

Sanofi not only recruits experienced talent but also provides opportunities to

potential talent, young university graduates. The company also takes part in job

fairs in the leading business schools of the country. The new recruits also undergo

a comprehensive orientation program which helps in enhancing and improving

their understanding of the company, business and future outlook.

Sanofi invests heavily in the training and developments of its employees. The

year 2011 saw a number of programs dedicated to human talent recognition,

development and career progression. The company imparted total training of 3394

days to 2022 employees focusing on improving managerial, personal and

functional effectiveness. Some of the training programs included:

• Licensed 2 Sell – a global initiative rolled out to all sales team (150

employees).

• Extensive training on technical aspects and sales certification process.

• Business Management Certification Program to 45 employees.

• New Product Training to around 200 employees.

• District Managers’ training for new/promoted DMs to develop their

capabilities.

• Participation of Sanofi Pakistan’s employees as facilitators in ‘Evolve’

(a regional program to coach young High Potentials from different

affiliates)

• Mapping for Leadership, an advanced leadership program for all

supervisors including the Management Committee.

• W2E, (Way to Excellence) a customized, technical program for

enhancing in-clinic performance of the sales force.

42

iii. Technology:

Sanofi-Aventis continues with its policy to invest more and more in IT and keeps on

upgrading their machinery and related infrastructure, thereby enhancing management decision

making. Some of their innovations include:

Genzyme: Applying the most advanced technology to treat rare diseases. The

recent acquisition of Genzyme, a global leader in biotechnology, brings access to

the most advanced technologies in life science, strengthening Sanofi’s reputation

as a global center for excellence in rare diseases.

A tetravalent vaccine to prevent dengue fever - Dengue fever is the second most

widespread endemic tropical diseases after malaria. No specific treatment exists

for this disease, and developing a vaccine is extremely challenging. Based on an

innovative biotechnology approach, Sanofi is working on an advanced tetravalent

vaccine for dengue. From 2010-2011 the under-developed vaccine has progressed

to the next phase of development.

iBGStar - The iBGStar is the first blood glucose meter that connects to a

Smartphone. This compact device allows independent diabetes management for

people with diabetes. With its innovative features and ease of use, the iBGStar

won the prestigious red dot design award 2011 in the category of life science and

medicine.

The organization has managed to eliminate manual work as much as possible. Some of

their business process projects have been very successful which include:

eTMS system - It manages sales force monitoring, performance, incentives,

primary and secondary sales consolidation had several enhancements such as:

ePR (Electronic Purchase Requisition system) - It is used to automate and

simplify approval process, improve documentation and internal controls. The

system integrates with SAP to ensure budget controlling as well.

43

eAED (Electronic Approval) - Used for projects of higher financial values.

Projects can be transparently reviewed and approved by regional management and

corporate teams.

cGate - A portal for their sales force with communication highlights, email, and

electronic daily call reporting that automates field expenses re-imbursement and

KPI calculation. Results of electronic daily calls are cross referenced with our

secondary sales and as a result steers our marketing and sales planning process.

GIMc - A global change management system, which is a paperless change

management system for industrial processes. The system is GMP compliant and

improves control and documentation. It also saves time in accessing change

requests or to check status.

iv. Procurement:

Sanofi ensures procurement of high quality inputs that comply with the highest social,

ethical and environmental standards. By 2011, around 1880 suppliers were evaluated.

Primary activities:

i. Inbound Logistics:

Before choosing the suppliers, a thorough and extensive evaluation of suppliers is done in

order to select the most experienced and competent suppliers who provide high quality raw

material as per the quality requirement of the company. A major portion of the raw material

purchased, comes from Germany and France. Sanofi also manages its process of movement of

raw materials from suppliers to warehouse effectively.

ii. Operation:

All the developmental activities carried out at Sanofi are managed and conducted

intelligently, scientifically and methodically and are in full compliance with the cGMP

44

guidelines. Its ongoing strategy is to increase investment in technology. Sanofi has a better

managed quality control department which ensures that all products meet the quality standards

and certifications. It has warehouses where products are properly stocked and maintained with

due diligence.

iii. Outbound Logistics:

Sanofi has a world-class, state-of-the-art pharmaceutical warehouses situated in Wah

Cantt and Karachi. Sanofi distributes its stocks directly to different institutions like doctors,

government and private hospitals, dispensaries by experienced distributors. It receives stocks

from WAH Warehouse and KARACHI Warehouse and sell that to Retailers and Wholesalers in

local market through their 16 Regional Distributors. Sale is done to all Institutions including

Government and Private Hospitals all over the country. It is done directly by the company but

supplied through 12 Institutional Agents.

Goods flows chart

iv. Marketing &

45

Sales:

Information regarding the proper use of medicine is provided by Sanofi through its well

marketed channels and promotional marketing strategies. The changing customer needs are well

understood by the marketing department of Sanofi which is well equipped with expert marketers.

Marketing of medicine is usually through seminars and conferences which introduces and

explains the benefits of medicine and their importance with changing consumer needs. This is

done through marketing representatives with strong mission to achieve the objectives. Since

there are large numbers of products, each product requires a different marketing strategy. This

ultimately requires huge investment and promotion budget on marketing which Sanofi is already

doing.

v. Services:

Sanofi provides after sales service by asking their customers for any help regarding

detailed description of a particular product or helping their consumers gather sufficient number

of consumers so that they can deliver their message to them and thus can create profits for them

by catering to the greater number of people.

46

CORE COMPETENCIES OF SANOFI AVENTIS

1. Highly innovative Research & Development

Sanofi has built a revitalized R&D organization which is focused on meeting unmet

needs of the patients and delivering truly innovative solutions. The R&D team of Sanofi is

composed of highly qualified and trained scientists, pharmacists, chemists and engineers who not

only identify novel mechanism of actions but they also transform innovative concepts into

effective treatments. The products made by this team comply to the internationally accepted

standards of quality, purity, efficacy and safety.

2. Specialized knowledge and know how in key sectors i.e. in Diabetes and Antibiotics

Sanofi is a very well established French multinational company in the market of diabetes

and anti-biotic. They are very strong in these sectors and also have a first mover advantage. They

have led the field in insulin manufacturing as well as in diabetes research and development for

88 years: from the first manufacture of insulin through to the development of Lantus which they

launched a little over a decade ago.

47

STRATEGIC COST MANAGEMENT PROCESS ES OF SANOFI AVENTIS

Sanofi Aventis does not use Activity Based accounting system. Costing is done

departmental wise by a team of accountants that are hired by the company. It includes the

following costs:

i. Operational Costs (warehousing, manufacturing & workforce)

Sanofi has a state of the art plant which is continuously improved and upgraded; the cost

incurred for advancement and maintenance is high. The corporation is continuously transforming

the business to meet the challenges that lie ahead. Sanofi also has a large pool of highly skilled

labor force which has to be looked after.

ii. Raw Material Cost

Sanofi outsources the raw materials for production out of which majority of raw materials

are imported from abroad mainly Germany and France. This increases the transportation

expenses of 3rd party contractors, and eventually increases overall costs for Sanofi. They can do

backward integration with their suppliers and increase partnership locally as well as

internationally which can also reduce cost of raw material as the price hike of raw material is

increasing globally.

iii. Distribution and marketing Cost

Sanofi distributes its products all over Pakistan which is done through different channels,

of distribution. The organization’s marketing department is active and launches new campaigns

to create awareness. It also conducts seminars and workshops. Sanofi controls the transportation,

distribution and marketing costs effectively. Distribution and marketing expenses have increased

as a % of net sales from 17.8% to 18.4% this year. The increase is attributable to the

pharmaceuticals business activities with increased spending on advertising and promotional

activities coupled with higher utility, traveling & conveyance, handling, freight & transportation

48

costs, adverse exchange parity impact relating to imported items, depreciation charge and the

impact on account of general inflation. The increase was offset by reduced selling expenses

especially commission expenses pertaining to the vaccines tender business.

FINANCIAL RATIO TRENDS OF SANOFI AVENTIS

Financial Ratio Trend Analysis

The growth rate of Sanofi for 2011 was 16% (Business Recorder, 2011) where as average

growth rate of industry was 11%. This shows that Sanofi is growing at a much better rate

than the market.

Total sales including both pharmaceutical and vaccine sales of the company grew by

23.7%. This was mainly driven by volume growth of key pharmaceutical brand and

exploration and materialization of growth opportunities (which included licenses

acquired for certain pharmaceutical products as well as new line extension for Amaryl,

Falgyl and Taxotere family.

The major concern uncovered by the ratios is that the operating and net profitability of

this company is very low when compared with the industry average, indicating that other

49

INDICATOR SANOFI AVENTIS INDUSTRY AVERAGE

Inventory Turnover 3.9 Times 5.29 Times

Current Ratio 1.1 Times 1.9 Times

Net Profit Margin 3.0% 6.62%

Return On Assets 5.2% 10.16%

Operating Margin 7% 12.25%

Growth 16% 11%

companies are making a better return on their investment and earning more profits due to

more sales & lesser cost structures. Sanofi has to increase its profitability as it seems

there is still untapped potential in the market which the company is forgoing. The data

suggest that the company has to curtail it expenses, in order to compete aggressively in

the Pharmaceutical industry and increase their profit share.

Inventory Turnover is lower than the industry average indicating that it is taking more

days to sell the inventory so an action needs to be taken here.

50

INTERNAL FACTOR EVALUATION MATRIX

Critical Success Factors Weight RatingWeighted