slides for chapter 6: external adjustment in small and...

TRANSCRIPT

Slides for Chapter 6:

External Adjustment in Small and Large Economies

International Macroeconomics

Schmitt-Grohe Uribe Woodford

Columbia University

May 1, 2016

1

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

A Graphical Approach to Studying External Adjustment in

Small and Large Economies

We will derive a current account schedule: CAt = CA(rt; . . . ). This

will be helpful to analyze adjustment in the current account to

macroeconomic disturbances.

2

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Recall the Investment Schedule from Chapter 5:

I1 = I( r1; A2,− +

. . . )

I1

r1

← I(r1;A2)

3

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Shifter of the Investment Schedule

• A2 ↑, then schedule shifts up and to the right

4

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Introduce the Savings Schedule Results of Chapters 3 and 5 imply...

S1 = S( r1; Q1 Q2,+ + −

. . . )

S1(r1;Q1,Q2)

S

r1

5

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Shifters of the Savings Schedule

• Q1 ↑, S(r) shifts right.

• Q2 ↑, S(r) shifts left.

6

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

The Current Account Schedule

CA = S − I

CA(r) = S(r)− I(r)

7

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Draw the savings and investment schedule in the same graph:

Given r, horizontal difference gives: S − I, which is the current

account.

S(r1, Q

1)

I(r1)

S, I

r1

rc

ra

rb

(a)

CA(r1)

r1

CA0

rc

ra

rb

(b)

8

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

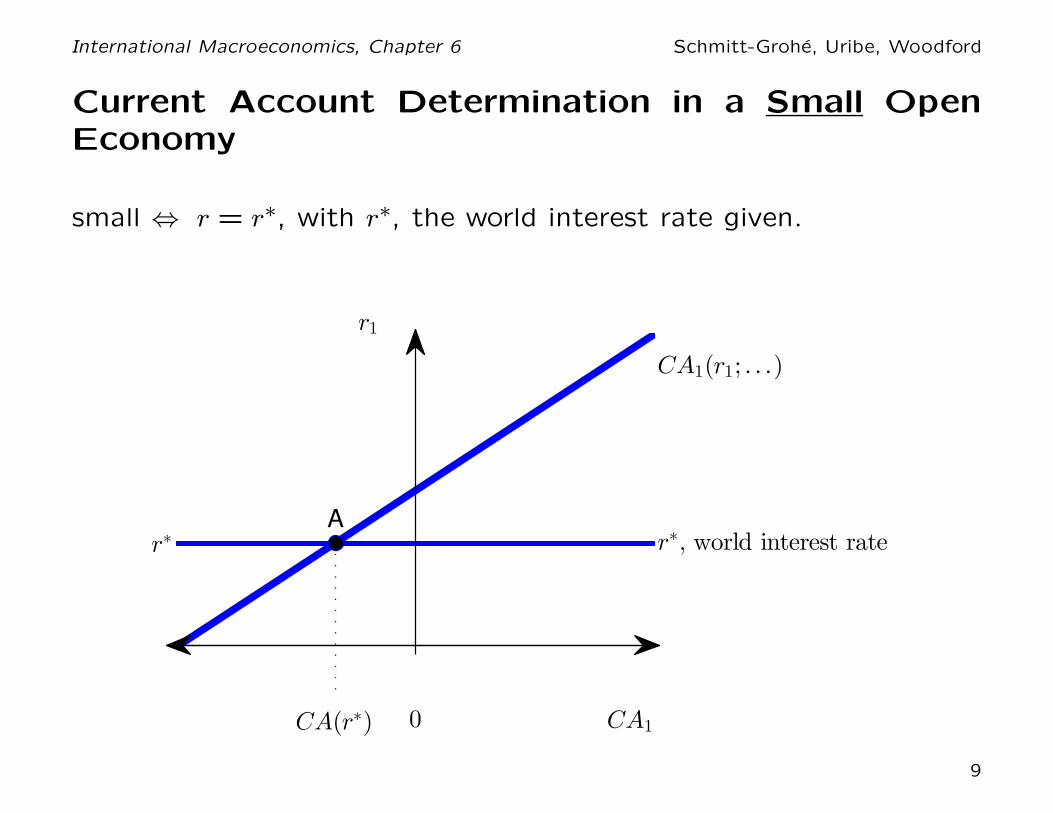

Current Account Determination in a Small OpenEconomy

small ⇔ r = r∗, with r∗, the world interest rate given.

A

CA(r∗)

CA1(r1; . . .)

r∗, world interest rater∗

CA10

r1

9

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Now use the graphical apparatus to analyze current account adjustment

to:

1. An increase in the world interest rate, r∗ ↑.

2. A temporary output shock, Q1 ↑.

3. A future productivity shock, A2 ↑.

4. Expected future terms of trade depreciation.

10

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

1.) Current account adjustment to an increase in the world

interest rate

CA(r1, Q

1)

CA0

r*o

CA1

r*1

r1

CA0

11

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

2.) Current account adjustment to a temporary increase in

output

S(r1, Q

0

1) S(r

1, Q

1

1)I(r

1)

S, I

r1

r*

So

1S

1

1Io

1

ro

c

r1

c

(a)

CA(r1, Q

1

0)

CAo

1

CA(r1, Q

1

1)

CA1

1

r1

CA0

r*

(b)

12

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

3.) Current account adjustment to a future increase in productivity

So(r

1, Q

1)

S1(r

1, Q

1)I

o(r

1) I

1(r

1)

S, I

r1

r*

So

1S

1

1Io

1I1

1

ro

c

r1

c

(a)

CAo(r

1, Q

1)

CAo

1

CA1(r

1, Q

1)

CA1

1

r1

CA0

r*

(b)

13

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

4.) Expected future terms of trade depreciation.

S(r1, Q

0

1) S(r

1, Q

1

1)I(r

1)

S, I

r1

r*

So

1S

1

1Io

1

ro

c

r1

c

(a)

CA(r1, Q

1

0)

CAo

1

CA(r1, Q

1

1)

CA1

1

r1

CA0

r*

(b)

14

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Current Account Determination in a

Small Open Economy with

an Interest Rate Risk Premium

15

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

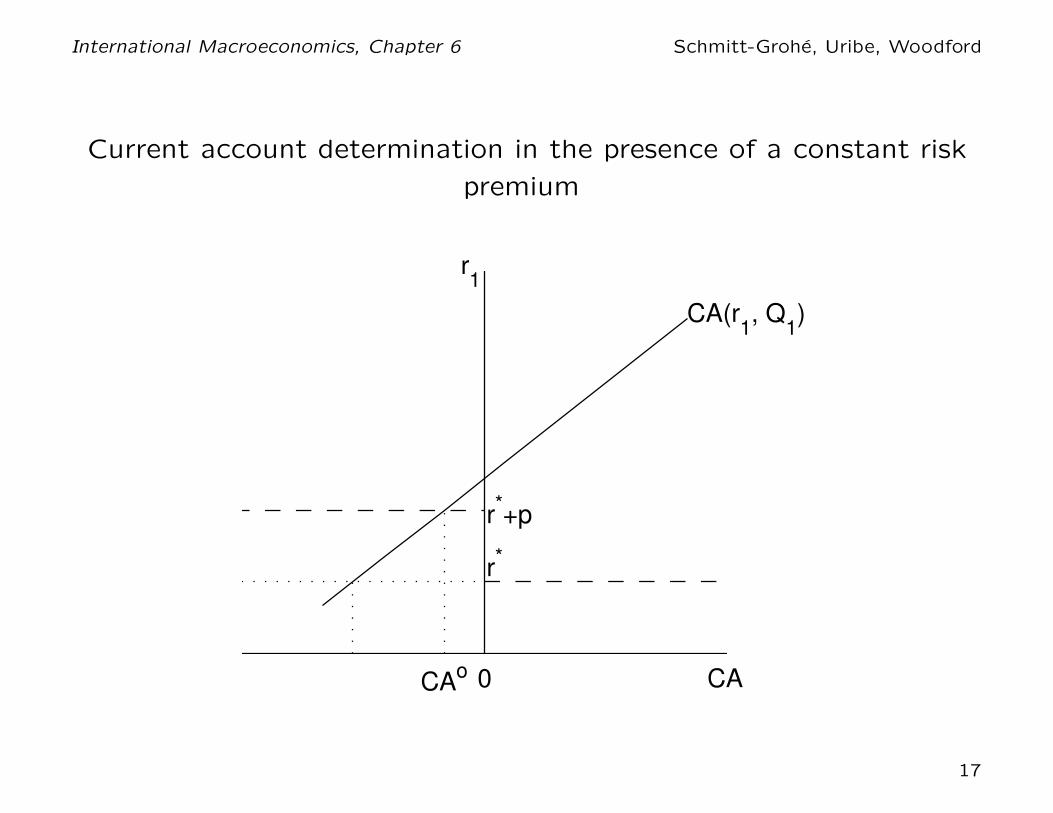

r1 = country interest rate

r∗ = world interest rate

Typically, r1 >> r∗ for emerging market debtors. Why? Because of

positive country risk premia.

p ≡ r1 − r∗ = country risk premium

or

r1 =

{

r∗ + p if country is a debtorr∗ if country is a creditor

16

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Current account determination in the presence of a constant risk

premium

CA(r1, Q

1)

r*

CAo

r*+p

r1

CA0

17

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Current account determination in the presence of an increasing risk

premium

CAo(r

1, Q

1)CA

1(r

1, Q

1)

r*

r*+p(−CA)

CA0

1CA

1

1

r1

CA0

18

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Equilibrium in a Large Open Economy

large → r 6= r∗.

Instead r is such that

CA(r) + CAROW(r) = 0

ROW = rest of the world

19

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Current account determination in a large open economy

CAUSCA

US′

CARW

AC

BD

D′

r

CAUS0CA

RW

20

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Bernanke’s Global Saving Glut Hypothesis

Ben S. Bernanke, “The Global Saving Glut and the U.S. Current

Account Deficit,” Homer Jones Lecture, St. Louis, Missouri, April

14, 2005.

21

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

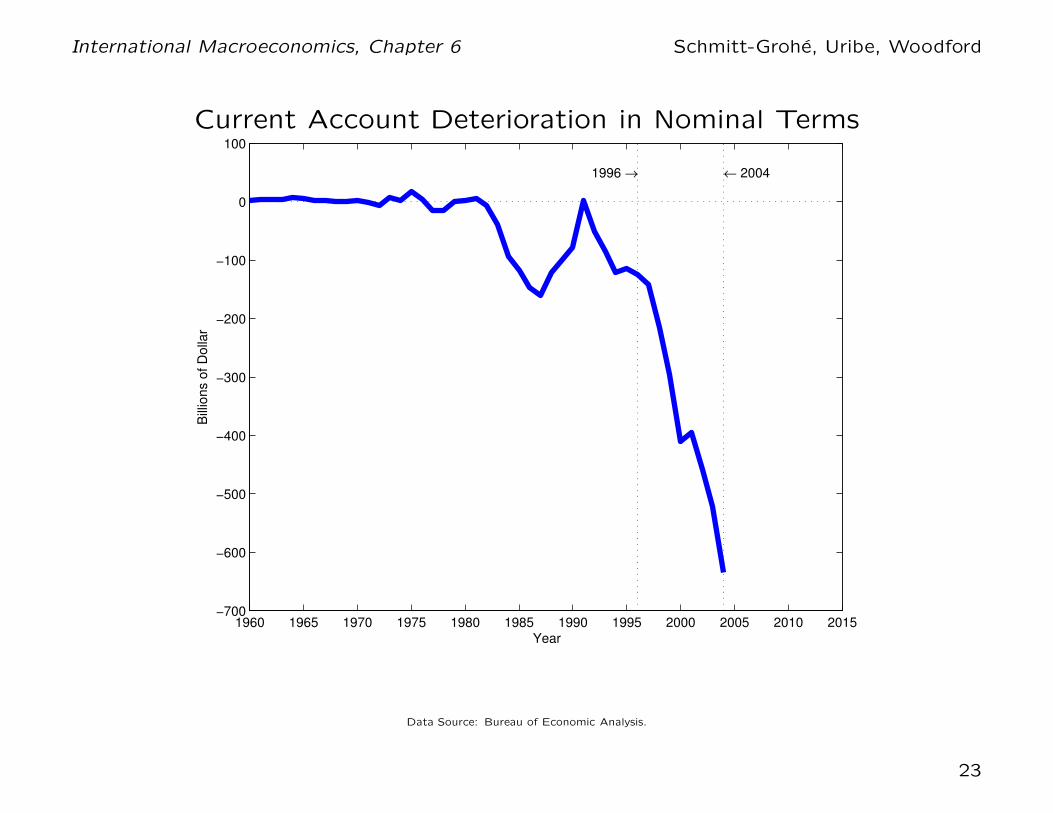

Bernanke observes that between 1996 and 2004 the U.S. current

account has greatly deteriorated:

CA ($ bn) CA/GDP (in %)

1996 -125 -1.52000 -411 -4.02004 -634 -5.2

Note. These numbers differ slightly from those reported in Bernanke’s speech, because the

numbers in the table are revised numbers from the March 19, 2015 release.

22

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Current Account Deterioration in Nominal Terms

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015−700

−600

−500

−400

−300

−200

−100

0

100

1996 → ← 2004

Bill

ions o

f D

olla

r

Year

Data Source: Bureau of Economic Analysis.

23

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

While not quite as dramatic as in nominal terms, current account

deterioration also large in real terms ...

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015−6

−5

−4

−3

−2

−1

0

1

2

1996 → ← 2004

Pe

rce

nt

of

GD

P

Year

Data Source: Bureau of Economic Analysis.

24

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Bernanke then asks what accounts for this dramatic CA deterioration.

He suggests two alternative explanations:

• Hypothesis 1: (“Made in the U.S.A.”) The CA deterioration

primarily reflects developments inside the United States and is independent

of developments in other parts of the world.

• Hypothesis 2: (Global Saving Glut) The CA deterioration was due

to external factors, that is, due to developments in the rest of the

world (and hence not under U.S. control).

25

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

“Made in the U.S.A.” Hypothesis

The U.S. decided to save less and invest more ⇒ U.S. current

account schedule shifts up and to the left.

Why? Financial innovation induced low private savings rates and

over-investment in residential housing.

Global Saving Glut Hypothesis:

Over the past decade there was a significant increase in the global

supply of savings— a global saving glut ⇒ current account schedule

of the rest of the world shifts down and left

Why? (1) Emerging markets are accumulating foreign reserves to

prepare for future crises and avoid the experience of the 1990s. (2)

Export-led growth (brought about via exchange rate manipulation

— undervalued currency). (3) Foreign (developed) countries are

saving more in preparation for an aging population.

26

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

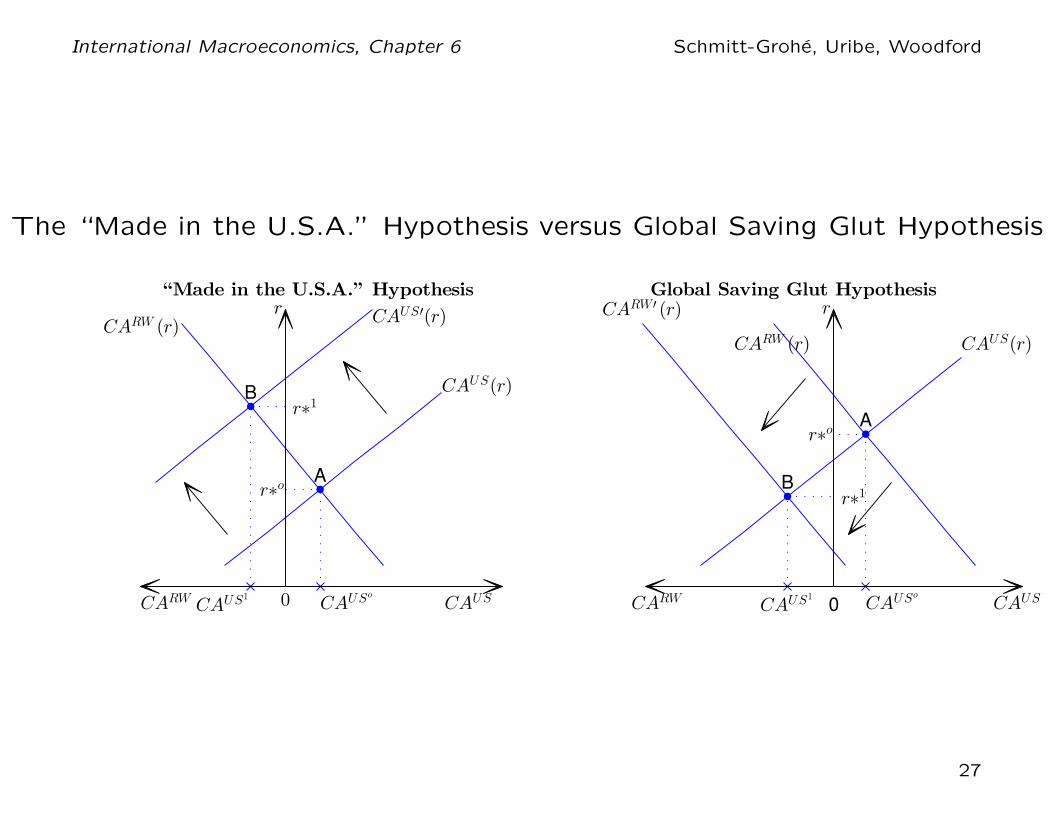

The “Made in the U.S.A.” Hypothesis versus Global Saving Glut Hypothesis

CAUS(r)CARW (r)

CARW′ (r)

A

CAUSo

r∗o

B

CAUS1

r∗1

r

CAUS0CARW

Global Saving Glut Hypothesis

CAUS(r)

CAUS′(r)CARW (r)

A

CAUSo

r∗o

B

CAUS1

r∗1

r

CAUS0CARW

“Made in the U.S.A.” Hypothesis

27

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

How can we tell the Global Saving Glut Hypothesis and the

“Made in the U.S.A.” Hypothesis apart?

Both hypothesis imply that the U.S. current account deteriorates.

BUT

the global savings glut hypothesis predicts that interest rates fall

whereas the “Made in the U.S.A.” hypothesis predicts that interest

rates rise.

So we can use the observed behavior of interest rates to tell the two

hypotheses apart.

28

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

How to construct the real interest rate?

rt = real rate between period t and t + 1

it = nominal interest rate between t and t + 1

πt+1 ≡ Pt+1/Pt = gross rate of inflation between t and t + 1

Et = expectations operator conditional on information in period t

Use the Fisher equation,

1 + rt =(1 + it)

Etπt+1,

which says that the real rate equals the nominal rate minus expected

inflation.

it measured by 1-year Treasury rate.

29

πt measured by annual CPI inflation rate.

How to measure expected inflation, Etπt+1? We assume that πt+1 =

Etπt+1 for simplicity.

Alternatively, one could run a regression of 1/πt on its own lags.

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

The World Real Interest Rate: 1994-2004

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010−2

−1

0

1

2

3

4

Year

Perc

ent per

year

1996 → ← 2004

Note. The world real interest rate is approximated by the difference between the rate on 1-year U.S. Treasury securities and 1-year ex post CPI inflation.

30

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

The World Real Interest Rate: 1992-2012

1995 2000 2005 2010−1

0

1

2

3

4

Year

Perc

ent per

year

Note. The world real interest rate is approximated by the difference between the rate on 10-year U.S. Treasury securities and 10-year expected inflation.

30

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

The figure shows that real interest rates fell, which is consistent

with the Global Savings Glut Hypothesis and inconsistent with the

“Made in the U.S.A.” hypothesis.

31

International Macroeconomics, Chapter 6 Schmitt-Grohe, Uribe, Woodford

Finally, can the Saving Glut Hypothesis be used to rationalize the

improvement in the U.S. current account after 2006? The argument

would go as follows. After 2006 the rest of the world decided to

save less and invest more, hence the CA schedule of the ROW

would have shifted up and to the right. As a result the CA balance

of the U.S. would have improved. What would have happened to

interest rates? They should have gone up. However, this is not what

happened, interest rates fell even further during the Great Recession,

suggesting that a subsiding of the savings glut is not the reason for

the improvement in the U.S. current account post 2006.

32