slide number #1 © 2007 nan mckay & associates cara gillette what’s new in public housing? ©...

TRANSCRIPT

Slide Number #1

© 2007 Nan McKay & Associates

Cara Gillette

What’s New What’s New

in Public Housing?in Public Housing?

© 2007 Nan McKay & Associates

Slide Number #2

© 2007 Nan McKay & Associates

Today’s Update TopicsToday’s Update Topics

Asset ManagementThe New PHAS – What We KnowNew HUD Procurement HandbookHUD’s Administrative Reform Initiative and Refinement of Income and RentCivil Rights Monitoring

Slide Number #3

© 2007 Nan McKay & Associates

Asset ManagementAsset Management

Slide Number #4

© 2007 Nan McKay & Associates

How the New Model WorksHow the New Model Works

We’ll walk through the model to help you understand why this is a fundamental shift for public housing programs

Slide Number #5

© 2007 Nan McKay & Associates

OverviewOverview

The new formula:• Requires PHAs with 250 or more PH units to transition

to PBM• Is based on HUD’s multifamily industry• Will force the PH program to become more property-

based to ensure the viability of each property

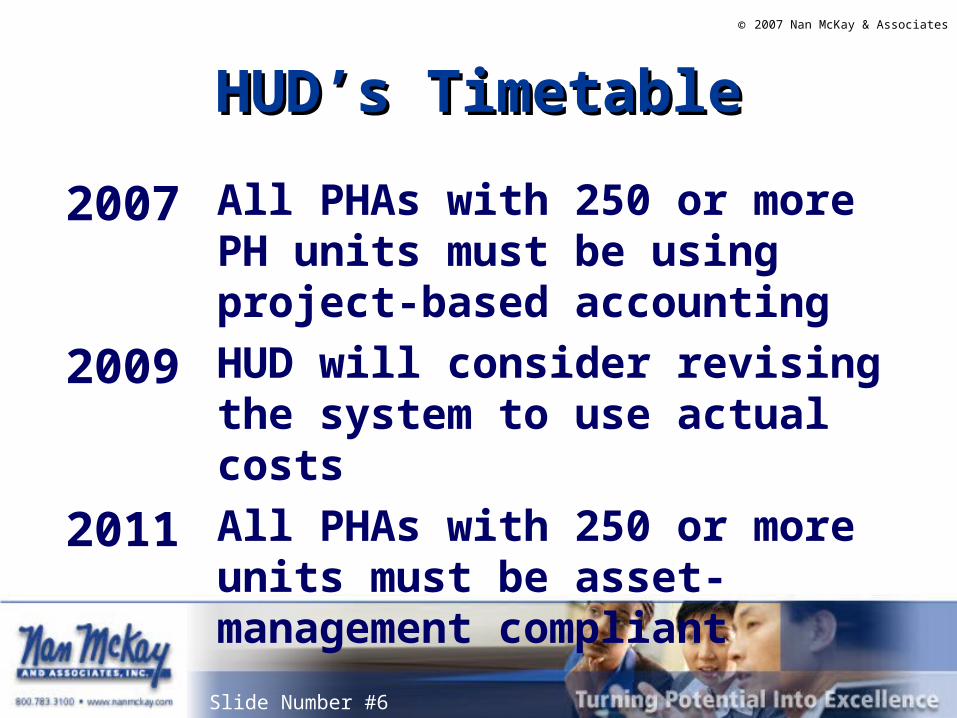

Slide Number #6

© 2007 Nan McKay & Associates

HUD’s TimetableHUD’s Timetable

2007 All PHAs with 250 or more PH units must be using project-based accounting

2009 HUD will consider revising the system to use actual costs

2011 All PHAs with 250 or more units must be asset-management compliant

Slide Number #7

© 2007 Nan McKay & Associates

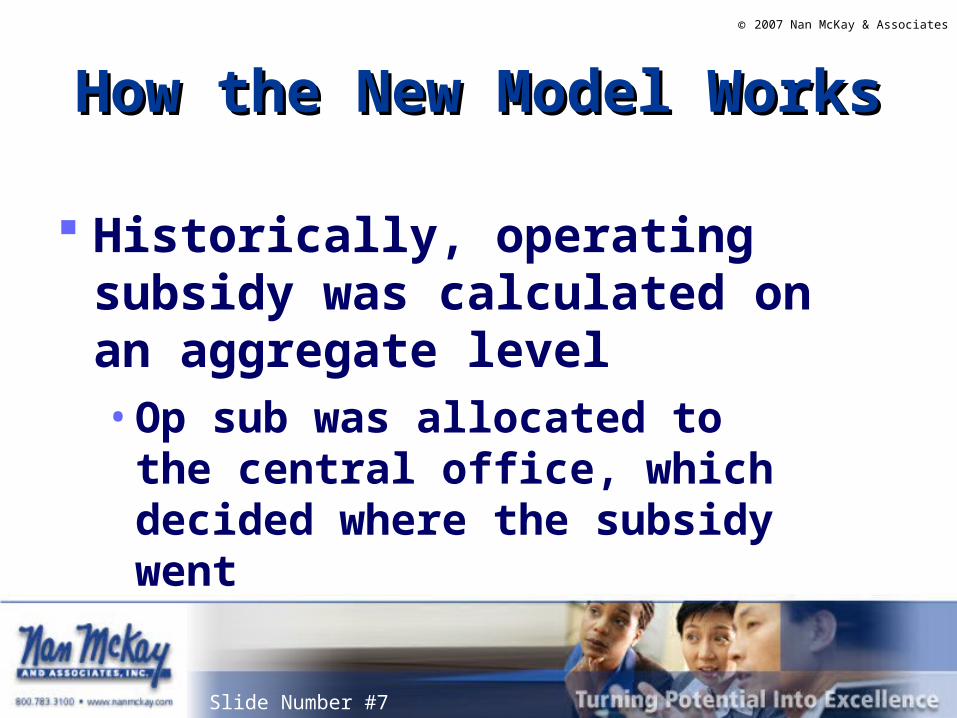

How the New Model WorksHow the New Model Works

Historically, operating subsidy was calculated on an aggregate level• Op sub was allocated to the central

office, which decided where the subsidy went

Slide Number #8

© 2007 Nan McKay & Associates

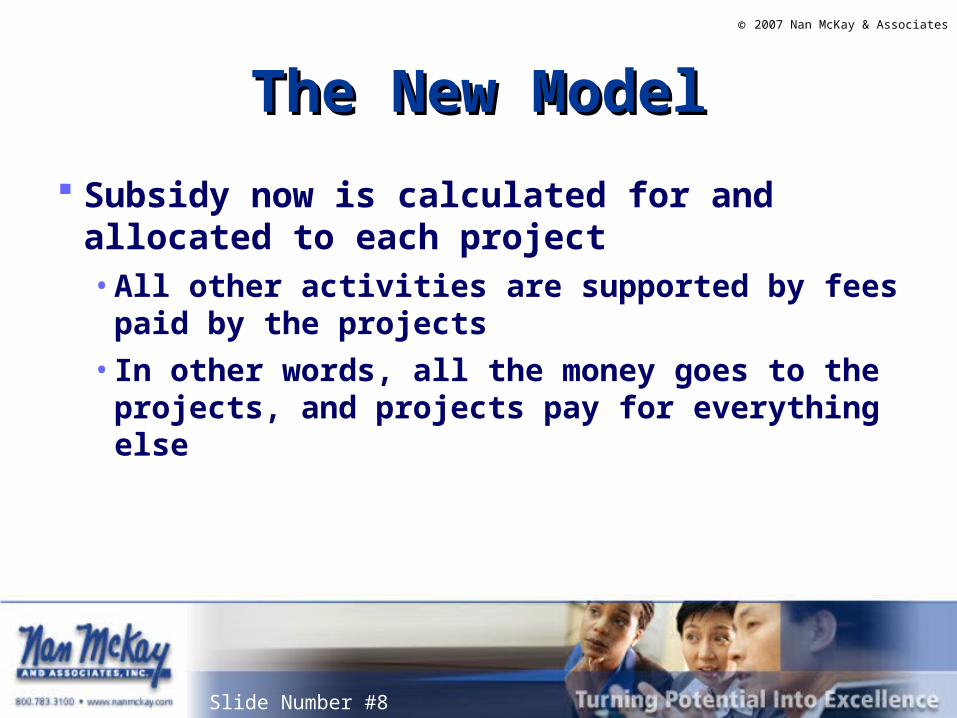

The New ModelThe New Model

Subsidy now is calculated for and allocated to each project• All other activities are supported by fees paid by

the projects• In other words, all the money goes to the projects,

and projects pay for everything else

Slide Number #9

© 2007 Nan McKay & Associates

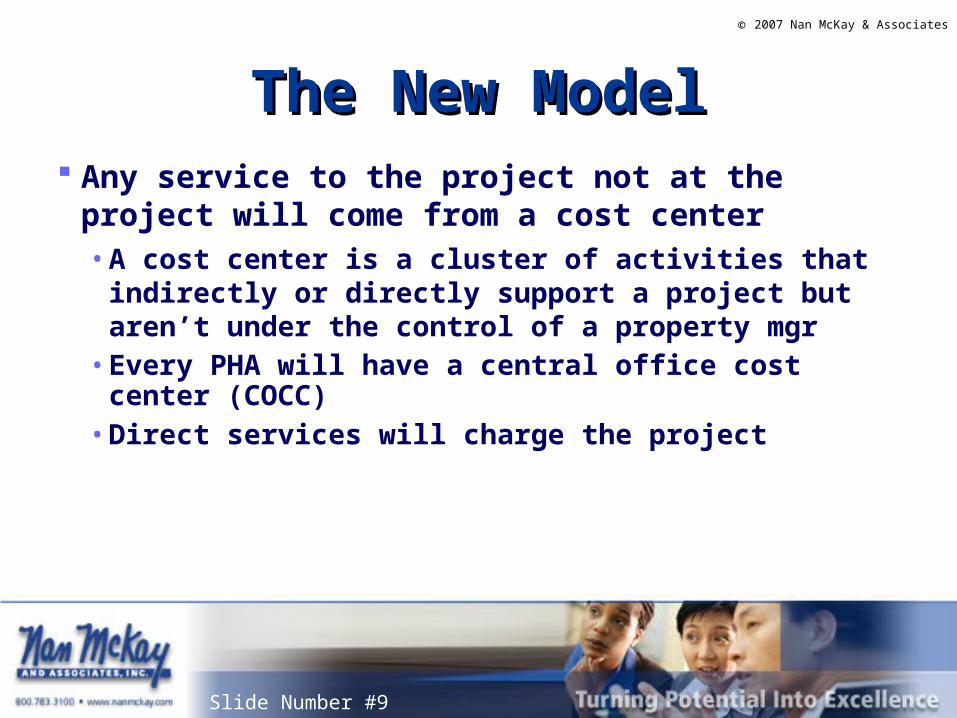

The New ModelThe New Model Any service to the project not at the project will come

from a cost center• A cost center is a cluster of activities that indirectly or

directly support a project but aren’t under the control of a property mgr

• Every PHA will have a central office cost center (COCC)• Direct services will charge the project

Slide Number #10

© 2007 Nan McKay & Associates

Compliance with Asset Compliance with Asset ManagementManagement

Best definition of compliance so far is in Notice 2006-14(HA)• Guidance on

successful conversion for stop-loss agencies

Slide Number #11

© 2007 Nan McKay & Associates

The Deal with Stop-LossThe Deal with Stop-Loss

PHAs who are losing operating subsidy in the new formula can stop the loss by early conversion to asset management

Slide Number #12

© 2007 Nan McKay & Associates

Stop-Loss ProvisionStop-Loss Provision

The deadline is October 15, 2007 If PHA demonstrates conversion by that date,

the reduction of subsidy will be stopped at 5% of the difference for CY 2007 That means that 95% of the PUM difference will

be added to the lower op sub level under the final rule

Slide Number #13

© 2007 Nan McKay & Associates

Stop-Loss ProvisionStop-Loss Provision

The added subsidy will continue to be received by the PHA each calendar year that the PHA remains in compliance with the asset management requirements• This means that the PHA must be in

compliance each year or go back to the original loss

Slide Number #14

© 2007 Nan McKay & Associates

Attachment 1• Attachment B of this document adds some

requirements for year two deadline• We’ll weave these in when we discuss the

stop-loss kit

Stop-Loss Notice PIH 2007-16Stop-Loss Notice PIH 2007-16

Stop-Loss ProvisionStop-Loss Provision

The stop-loss kit is an important document because it’s a template for stop-loss agencies • And a roadmap for all

other agencies• HUD to issue 2nd year

stop-loss kit soon

Slide Number #16

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

1. Project-based accounting• Monthly operating statements for each project – revenues and

expenses vs. budget levels, including all fees from COCC and CFG

• Must reasonably reflect the financial performance of each project

Sum of operating statements = total PH

Slide Number #17

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

1. Project-based accounting second year: Project-specific balance sheets not required

Slide Number #18

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

2. Project-based management• Property management services are arranged

or provided in the best interest of the property considering needs, cost, and responsiveness, relative to local market standards

Slide Number #19

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

3. Central office cost center (COCC)• All central office fees must be reasonable• COCC must operate on the allowable fees and other

permitted reimbursements from its PH and S8 programs

• In other words, the COCC must support itself

Slide Number #20

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

3. Central office (COCC) second year:• PHA may not fund the COCC with:

Sale of assets acquired with PH funds Amounts from Capital Fund other than

permitted (e.g., can’t use “Management Improvement” funds to pay for general accounting staff)

Funds from state or local governments

Slide Number #21

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

4. Centralized services• Centralized services that directly support

projects are funded using a fee-for-service approach or through other allowable charge-backs

• Each project is charged for actual services received

• Must be reasonable compared to local market

Slide Number #22

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Review of project performance• PHA systematically reviews financial,

physical, and management performance of each project, and identifies non-performing properties

Slide Number #23

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Review of project performance – a non-performing property has:

• PHAS physical score below 70• Significant crime and drug problems• Below 95% occupancy• TARS that exceed 7% of monthly rent roll

FAQ clarifies this means rent…

Slide Number #24

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Review of project performance – a non-performing property has:

• PHAS grade of “D” or below for vacant unit turnaround and work orders

• Utility consumption more than 120% of agency average

• Other major management problemsTurnaround = D more than 30 daysWOs = D more than 40 days

Slide Number #25

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

5. Non-performing property second year:• Significant drug and crime as defined by

Uniform Crime Reporting = exceeds the surrounding community by 120%

• For any projects identified as non-performing, PHA has management plan with set of recommendations and measurable goals

Slide Number #26

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

6. Capital planning• Physical needs assessment and a five-year

plan for each project Five-year plan needs to consider revenue

sources, market, tenancy, and project needs• PHA demonstrates commitment to long-range

energy consumption reduction

Slide Number #27

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

7. Risk management responsibilities related to regulatory compliance

• PHA not carrying out responsibilities if: Designated troubled under PHAS Any outstanding FHEO findings or voluntary

compliance agreement not implemented…

Slide Number #28

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

7. Regulatory noncompliance if:• No current energy audit…• Outstanding IG audit findings w/no progress• Not in compliance with ACOP• Unsatisfactory progress under RHIIP/RIM• PIC (50058) reporting rate under 95%• Any other major compliance deficiency

Slide Number #29

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

7. Regulatory noncompliance:• Stop-Loss FAQs, published 9/1/06 clarifies:

Regulatory compliance is agency-wide for now

• But at some point it will be analyzed by project

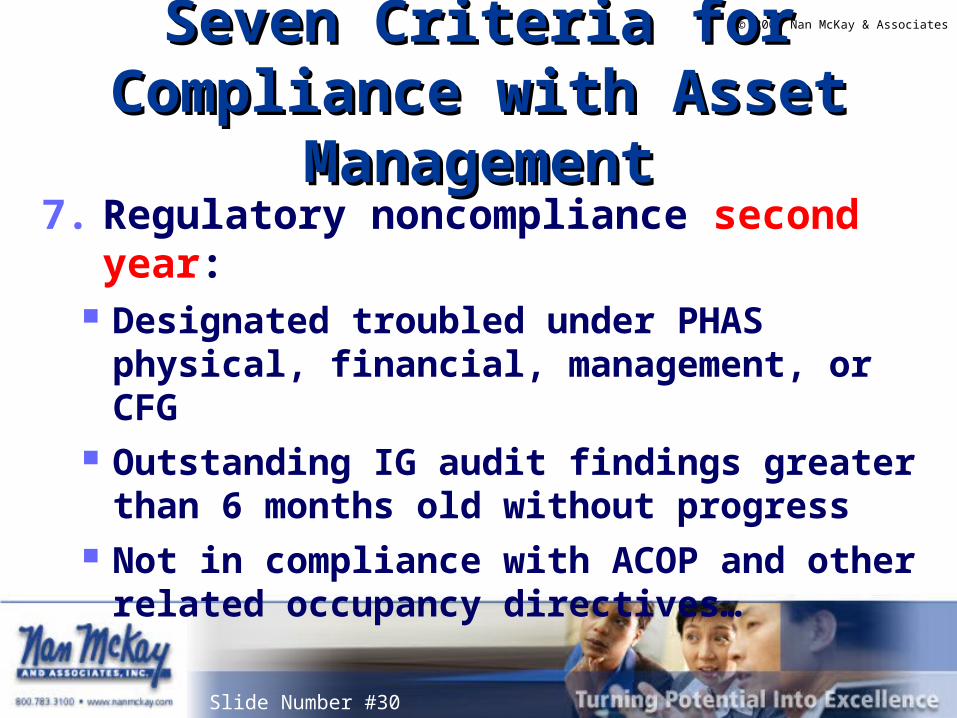

Slide Number #30

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

7. Regulatory noncompliance second year: Designated troubled under PHAS physical,

financial, management, or CFG Outstanding IG audit findings greater than 6

months old without progress Not in compliance with ACOP and other related

occupancy directives…

Slide Number #31

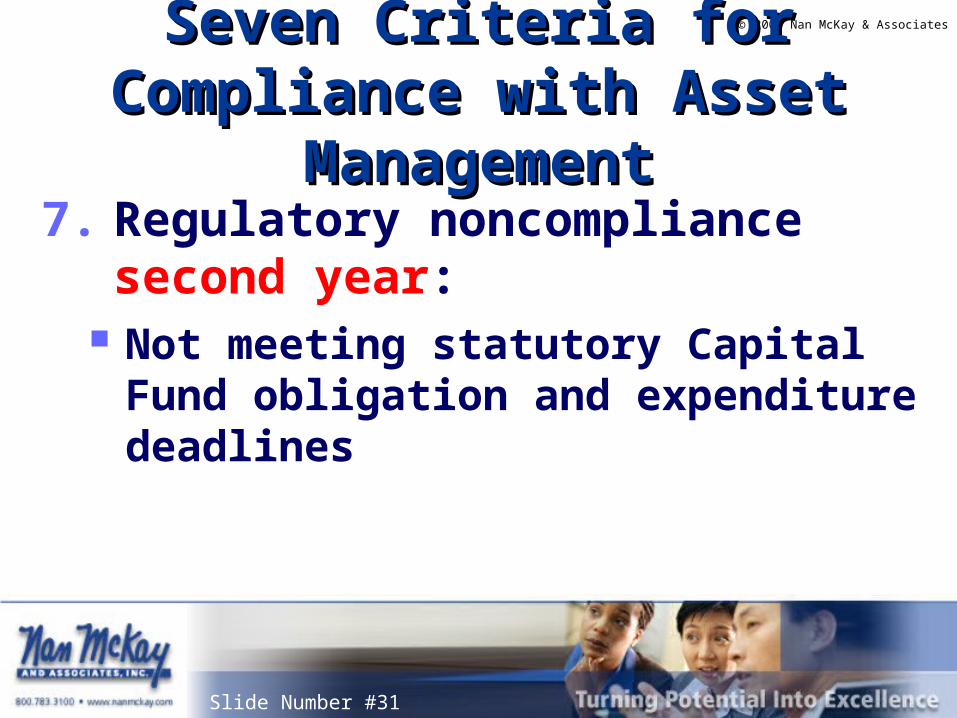

© 2007 Nan McKay & Associates

Seven Criteria for Compliance Seven Criteria for Compliance with Asset Managementwith Asset Management

7. Regulatory noncompliance second year: Not meeting statutory Capital Fund obligation

and expenditure deadlines

Slide Number #32

© 2007 Nan McKay & Associates

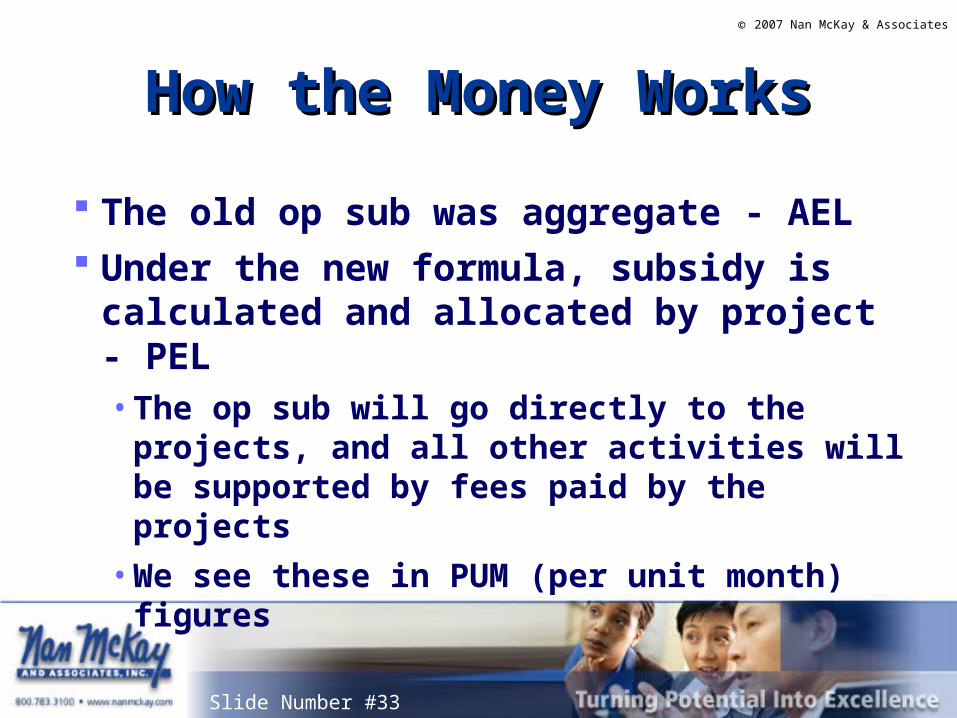

Follow the MoneyFollow the Money

How the op sub is calculated and allocated is driving these fundamental changes

Slide Number #33

© 2007 Nan McKay & Associates

How the Money WorksHow the Money Works

The old op sub was aggregate - AEL Under the new formula, subsidy is

calculated and allocated by project - PEL• The op sub will go directly to the projects,

and all other activities will be supported by fees paid by the projects

• We see these in PUM (per unit month) figures

Slide Number #34

© 2007 Nan McKay & Associates

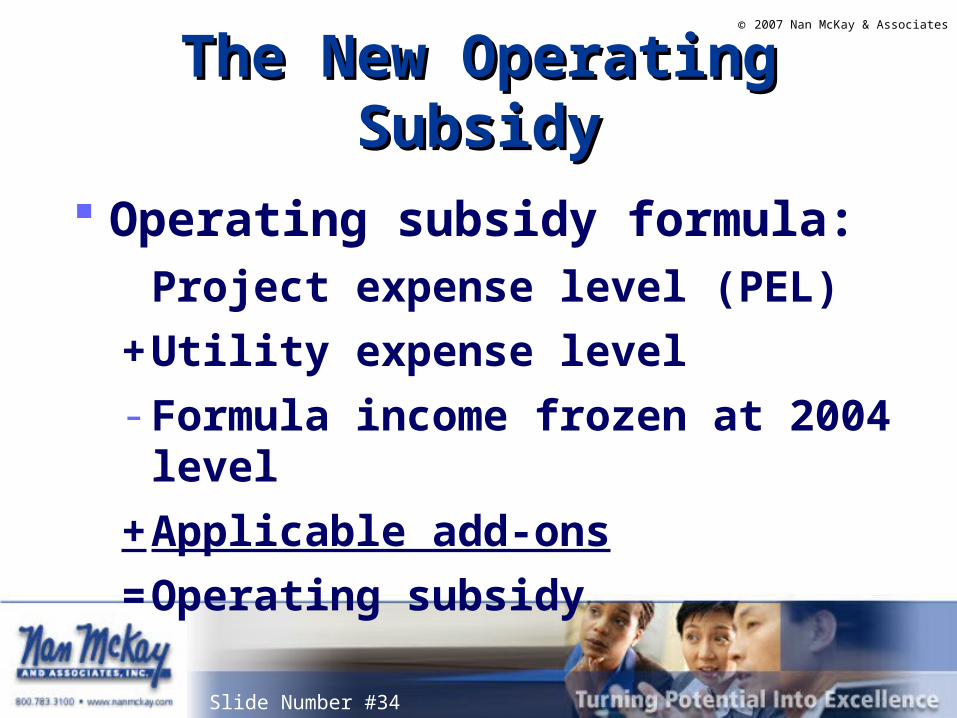

The New Operating SubsidyThe New Operating Subsidy

Operating subsidy formula:Project expense level (PEL)

+ Utility expense level- Formula income frozen at 2004 level

+ Applicable add-ons

= Operating subsidy

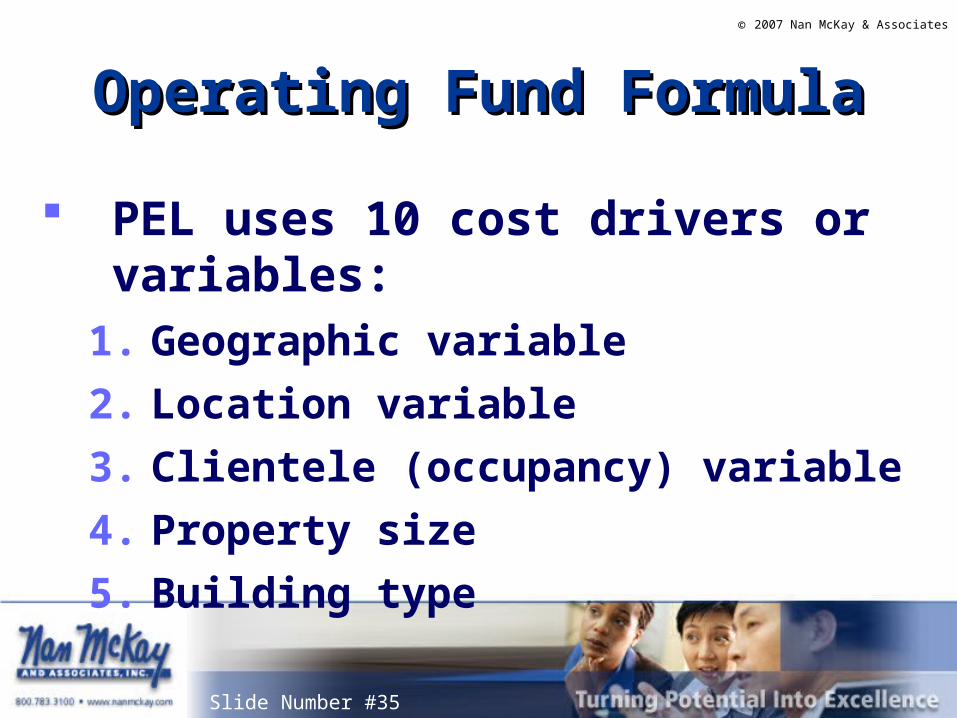

Slide Number #35

© 2007 Nan McKay & Associates

Operating Fund FormulaOperating Fund Formula

PEL uses 10 cost drivers or variables:1. Geographic variable

2. Location variable

3. Clientele (occupancy) variable

4. Property size

5. Building type

Slide Number #36

© 2007 Nan McKay & Associates

Operating Fund FormulaOperating Fund Formula

PEL uses 10 cost drivers or variables:6. Bedroom mix (unit size)

7. Percent assisted

8. Property age

9. Neighborhood poverty

10. Ownership type

Slide Number #37

© 2007 Nan McKay & Associates

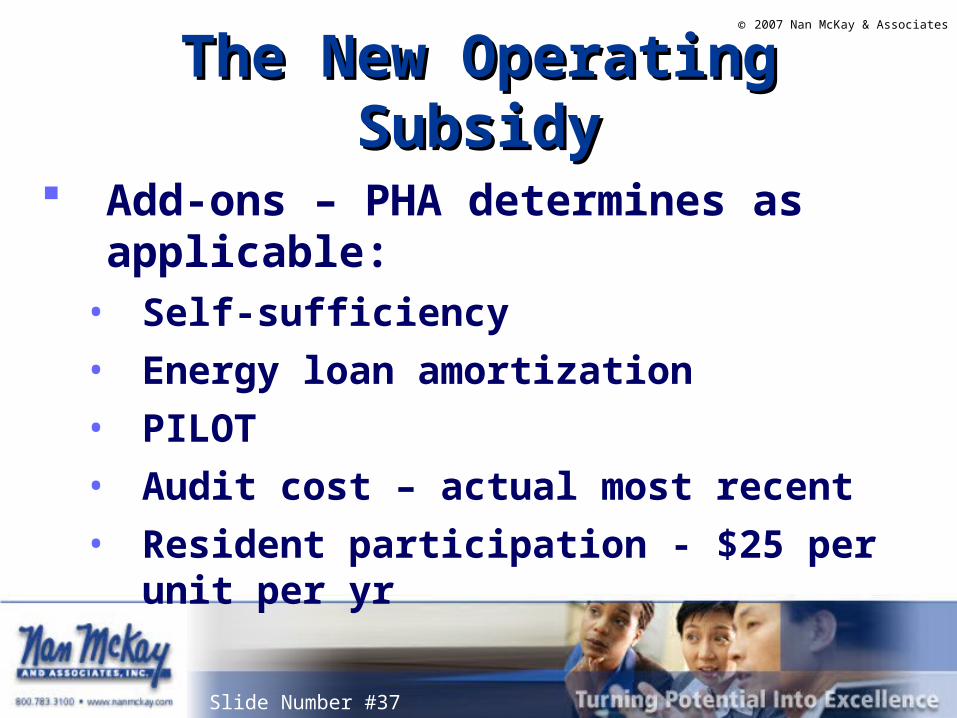

The New Operating SubsidyThe New Operating Subsidy

Add-ons – PHA determines as applicable:• Self-sufficiency• Energy loan amortization• PILOT• Audit cost – actual most recent• Resident participation - $25 per unit per yr

Slide Number #38

© 2007 Nan McKay & Associates

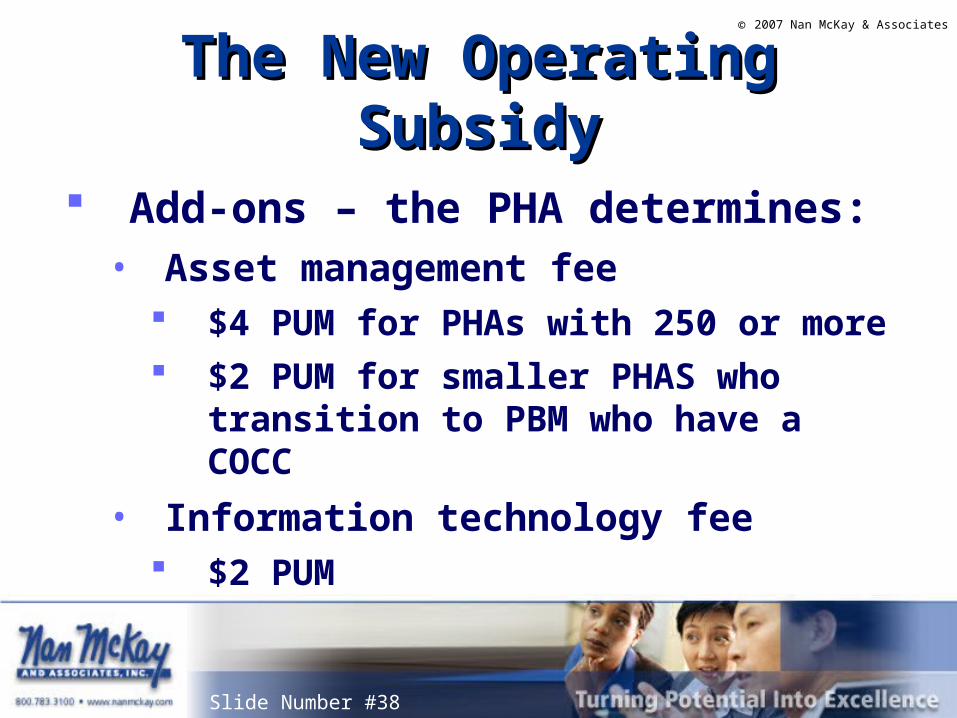

The New Operating SubsidyThe New Operating Subsidy

Add-ons – the PHA determines:• Asset management fee

$4 PUM for PHAs with 250 or more $2 PUM for smaller PHAS who transition to

PBM who have a COCC

• Information technology fee $2 PUM

Slide Number #39

© 2007 Nan McKay & Associates

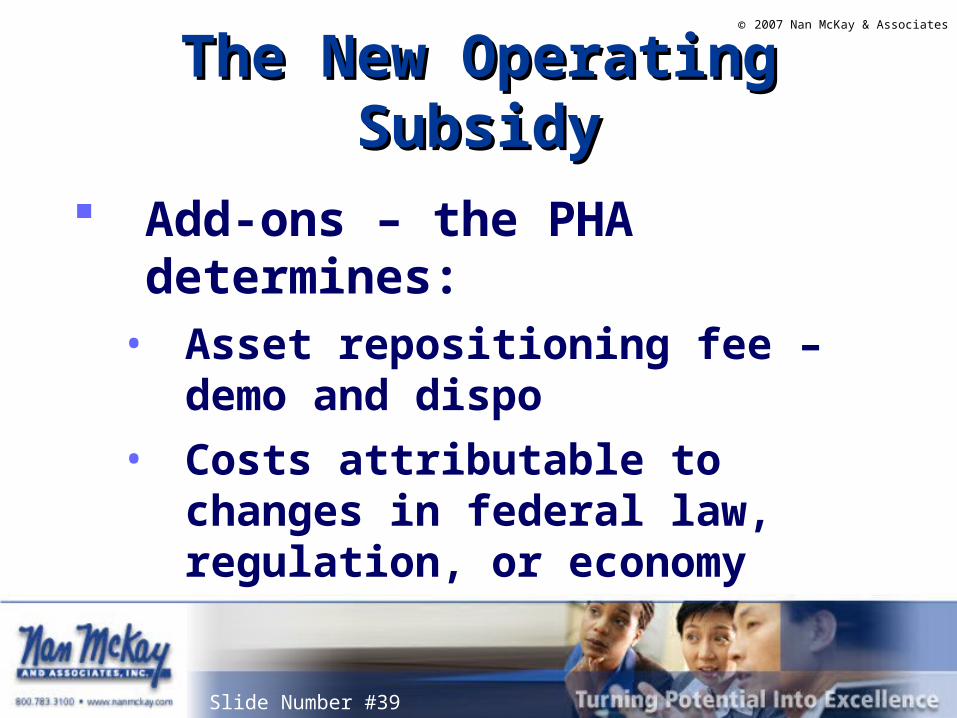

The New Operating SubsidyThe New Operating Subsidy

Add-ons – the PHA determines:• Asset repositioning fee – demo and dispo• Costs attributable to changes in federal

law, regulation, or economy

Slide Number #40

© 2007 Nan McKay & Associates

The New Operating SubsidyThe New Operating Subsidy

Approved vacancies – still get op sub:• Units undergoing mod (if on schedule)• Units approved for resident services• Units in court litigation• Units undergoing casualty loss settlement• Units vacant due to disaster (federal or

state)…

Slide Number #41

© 2007 Nan McKay & Associates

The New Operating SubsidyThe New Operating Subsidy

Approved vacancies – still get op sub:• Units vacant due to changing market

conditions• Limited vacancies, up to 3%

The PHA will enter types of vacancies into PIC

Slide Number #42

© 2007 Nan McKay & Associates

CostsCosts

Slide Number #43

© 2007 Nan McKay & Associates

CostsCosts

All budgeted costs and expenses will fall into one of three general categories: Direct or frontline cost (at the project) Central office cost center (COCC)

• Indirect services and allocated services Other cost centers (optional)

Slide Number #44

© 2007 Nan McKay & Associates

AMPAMP Frontline, or direct, costs of the AMP:

• Personnel costs of staff assigned to project• Repair and maintenance costs including

supplies, contracted repairs, make-readies, preventive maintenance, etc.

• Utility costs• Costs related to the site office – phones, office

supplies, computers, postage, etc…

Slide Number #45

© 2007 Nan McKay & Associates

AMP Frontline (Direct) CostsAMP Frontline (Direct) Costs

These are expenses of the project:• Advertising including procurement and

employment notices• Costs of employee recruiting and screening• PILOT• Insurance (allocated)• Legal fees

Slide Number #46

© 2007 Nan McKay & Associates

AMP Frontline (Direct) CostsAMP Frontline (Direct) Costs

These are expenses of the project:• Fees paid to the central office• Audit costs (allocated)

PHA should allocate a reasonable share of the audit cost to each AMP, COCC, and program

• Vehicle expense for site-based vehicles

Slide Number #47

© 2007 Nan McKay & Associates

Cost CentersCost Centers

Any service provided to the project that doesn’t reside at the project will need to come from a cost center

• The projects will pay for the direct services that don’t reside at the project

Slide Number #48

© 2007 Nan McKay & Associates

Cost CentersCost Centers

A cost center is a cluster of activities that indirectly or directly support an AMP but aren’t under the direct control of a property manager• Every PHA will have at least one cost center,

the central office cost center (COCC)• Centralized maintenance may also probably be

a cost center

Slide Number #49

© 2007 Nan McKay & Associates

Central Office Cost Center Central Office Cost Center (COCC)(COCC)

The COCC is the PHA’s collection of indirect costs of operation - all programs

COCC will have its own column on FDS We’ll talk about the fees the COCC

charges to the projects a bit later

Slide Number #50

© 2007 Nan McKay & Associates

COCC ActivitiesCOCC Activities• Executive director• Human resources• Regional PH mgmt• Corporate legal• Finance • IT• Risk management

• Centralized (if not an optional service center) Procurement Maintenance Work orders Inspections

Slide Number #51

© 2007 Nan McKay & Associates

Other Cost (Service) CentersOther Cost (Service) Centers

Maintenance is an example of services that may need to be provided directly to projects that are centrally located and charged based on time spent or actual work performed

Slide Number #52

© 2007 Nan McKay & Associates

Other Cost (Service) CentersOther Cost (Service) Centers

How to organize maintenance is an important PBM decision• A PHA can decide to organize maintenance:

Decentralized – front line• Supervised by the property manager

CentrallyA mix

Slide Number #53

© 2007 Nan McKay & Associates

Other Cost (Service) CentersOther Cost (Service) Centers

If the PHA uses centralized maintenance, will be required to use fee-for-service method when charging the project• Project can only be charged for actual

services providedCould be a single blended hourly rate, separate

hourly rates for various activities, or flat fee – must be reasonable

Slide Number #54

© 2007 Nan McKay & Associates

Centralized Maintenance Centralized Maintenance

For all centralized maintenance staff providing direct services, the PHA can charge up to the market rate• Even if it’s above what the

technician is actually paid

May charge for actual materials used as well as labor

Slide Number #55

© 2007 Nan McKay & Associates

Centralized MaintenanceCentralized MaintenanceHow Much Can the PHA Charge?How Much Can the PHA Charge?

Sally is a maintenance worker $62.26 Wages

$17.50 Benefits (45%)

$79.76 Hourly rate

If the market rate is $100, the hourly charge could be $100, regardless of what Sally is paid

Slide Number #56

© 2007 Nan McKay & Associates

Other FunctionsOther Functions

Charging back to the project• Where it’s cost-effective,

PHA can prorate across projects the cost of centralized staff who perform frontline functions

Slide Number #57

© 2007 Nan McKay & Associates

Charging Back to the ProjectCharging Back to the Project

These are called front line allocated costs• For example, collecting rent centrally,

employee handing rent collection, as well as direct costs, could be charged back to applicable projects on any reasonable basis

Slide Number #58

© 2007 Nan McKay & Associates

Charging Back to the ProjectCharging Back to the Project

Two exceptions to charging projects for centralized staff performing frontline functions:• Can’t charge projects for cost of a centralized

supervisor• Can’t charge projects cost of centralized staff

handling procurement

Slide Number #59

© 2007 Nan McKay & Associates

Update – Centralized Update – Centralized WarehouseWarehouse

FAQ December 1, 2006 If a warehouse at the COCC is for

“storerooms” of scattered sites, with HUD approval, this can be an eligible frontline cost

Slide Number #60

© 2007 Nan McKay & Associates

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project:• Central waiting lists, screening, leasing and

occupancy – PHAs can prorate costs direct costs of these functions to the AMPs, including supervisory personnel The proration can be based on the number of units

leased at a project, average turnover at a project, or other reasonable allocation method

Slide Number #61

© 2007 Nan McKay & Associates

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project:• Resident programs – PHA can prorate

centralized resident programs across projects on a reasonable basis, including supervisory staff

Slide Number #62

© 2007 Nan McKay & Associates

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project:• Protective services – PHAs can charge

centralized protective services, either in-house or through local law enforcement, including supervisory staff

• HUD eventually wants these tracked by project

Slide Number #63

© 2007 Nan McKay & Associates

Charging Back to the ProjectCharging Back to the Project

HUD will allow charging back to project:• Work order processing

Although it is the norm in multifamily housing to handle work order processing on site, a PHA may charge the cost of centralized work order processing only if the PHA can document/justify that the cost pro rated is reasonable and necessary

Slide Number #64

© 2007 Nan McKay & Associates

Shared Resource CostsShared Resource Costs

- What if there is PHA personnel who provide services both to the projects and the central office cost center?

Slide Number #65

© 2007 Nan McKay & Associates

Shared Resource CostsShared Resource Costs

HUD recognizes it may not make economic sense to have full-time staff dedicated to a specific project• In this case the PHA may establish a

reasonable method to spread these personnel costs to the AMPS that receive the service

Slide Number #66

© 2007 Nan McKay & Associates

Shared Resource CostsShared Resource Costs Shared resource costs are distinguished

from front line prorated costs in that the services being shared are limited to a few projects as opposed to being pro rated across all projects• An example of a shared resource cost might

be a maintenance person assigned to and paid for by two projects

Slide Number #67

© 2007 Nan McKay & Associates

Shared Resource CostsShared Resource Costs

- For PHA staff who provide services both to the projects and the central office cost center, the PHA must separate the amount of time spent on providing services to the projects and the central office cost center, based on a reasonable methodology

Slide Number #68

© 2007 Nan McKay & Associates

Shared Resource CostsShared Resource Costs

- The time spent by the staff on projects must be at an hourly rate that does not exceed the reasonable hourly fee for the service

Slide Number #69

© 2007 Nan McKay & Associates

Fees Allowed under PBMFees Allowed under PBM

Slide Number #70

© 2007 Nan McKay & Associates

Fees Allowed under PBMFees Allowed under PBM

Fees the projects will pay to the COCC:• Property management fees• Bookkeeping fees• Asset management fees• Capital fund management fees

Slide Number #71

© 2007 Nan McKay & Associates

Fees Allowed under PBMFees Allowed under PBM

Property management fee• Is “reasonable fee” paid by project to COCC

for project oversight• HUD has established some “reasonability”

guidelines Notice: Guidance on Implementation of Asset

Management, issued Sept 6, 2006

Slide Number #72

© 2007 Nan McKay & Associates

Fees Allowed under PBMFees Allowed under PBM

Management fee – “reasonable”• Based on multifamily fee (annual letter from

field office); or • 80th percentile as established by HUD; or• Other compelling data of local market

Might include fees paid pay the PHA for private management of other properties

Updated April 10, 2007Updated April 10, 2007

Slide Number #74

© 2007 Nan McKay & Associates

Fees Allowed under PBMFees Allowed under PBM

Management fee• Based on units leased (occupied units and

approved vacancies, but not the 3% limited vacancies) using average monthly lease-up rateStop-loss FAQs (question 12) says that the

PHA can use either the first day or last day of the month (but must be consistent)

Slide Number #75

© 2007 Nan McKay & Associates

Fees Allowed under PBMFees Allowed under PBM

Bookkeeping fee• An extension of the management fee• For accounting for project funds, charged to

the project from the COCC• Based on occupied units and allowable

vacancies• HUD will consider $7.50 PUM reasonable

Slide Number #76

© 2007 Nan McKay & Associates

Fees Allowed under PBMFees Allowed under PBM

Asset management fee• Fee paid by project to COCC for oversight of

portfolio • Based on total ACC• Must be reasonable, not to exceed $10 PUM• Only paid if the project has excess cash flow

(no limit first year)

Slide Number #77

© 2007 Nan McKay & Associates

Update – Asset Mgmt FeeUpdate – Asset Mgmt Fee

Per PIH Notice 2007-9(HA), issued 4/10/07• In the 1st year of PBM, there is no excess cash

requirement for the payment of the fee• In the 2nd year, each project must have excess

cash to pay the asset management fee• In the 3rd and subsequent years, excess cash

must equal one month of operating expenses to pay the asset management fee

Slide Number #78

© 2007 Nan McKay & Associates

Capital Fund Management Capital Fund Management FeeFee

Fee may be up to 10% of the CFG including replacement housing funds• The fee is paid by each AMP from CFG

proceeds

HUD is still defining the way the fee will be earned

Slide Number #79

© 2007 Nan McKay & Associates

The New PHAS – What We KnowThe New PHAS – What We Know

Per notice published Sept 6, 2006:• Under the first year of

project-based management, PHAs will receive a transitional score under the new PHAS

Slide Number #80

© 2007 Nan McKay & Associates

The New PHASThe New PHAS

Changes being considered:• Inspections under project-based PHAS may be

scheduled in the last three months of an agency’s fiscal year

• Projects that receive a score of 80 or higher will only be inspected every two years

Slide Number #81

© 2007 Nan McKay & Associates

The New PHASThe New PHAS

HUD is expected to issue a new physical inspection scoring notice specific to project-based PHAS

The central office or non-public housing projects will not be included in the financial assessment

Slide Number #82

© 2007 Nan McKay & Associates

The New PHASThe New PHAS

PHAs will be required to submit financial statements at the project level so that the financial condition of each AMP can be measured• Two of the indicators, Current Ratio and

Months Expendable Fund Balance, will be used to determine if a property/AMP is fiscally healthy

Slide Number #83

© 2007 Nan McKay & Associates

The New PHASThe New PHAS

The Management Operations Indicator is expected to be significantly changed under project based PHAS• Form HUD 9834, which is used by HUD for on

site multifamily management reviews, may be used a guide

Slide Number #84

© 2007 Nan McKay & Associates

The New PHASThe New PHAS

Management Operations Indicator• Will cover the area of tenant selection,

assignments, lease and grievance and tenant participation

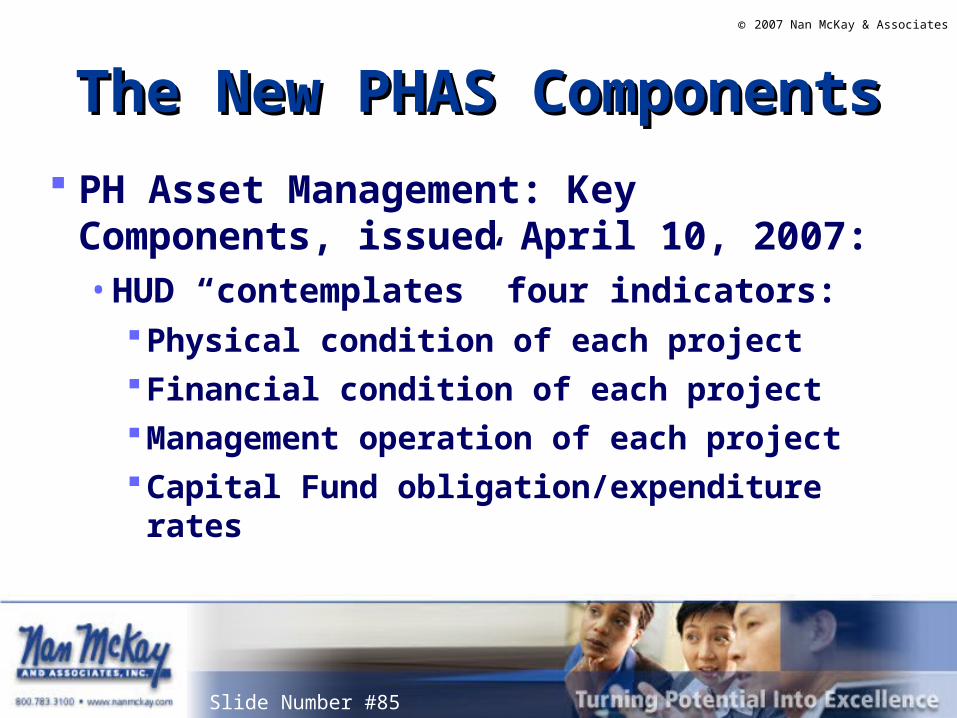

Slide Number #85

© 2007 Nan McKay & Associates

The New PHAS ComponentsThe New PHAS Components

PH Asset Management: Key Components, issued April 10, 2007:• HUD “contemplates” four indicators:

Physical condition of each projectFinancial condition of each projectManagement operation of each projectCapital Fund obligation/expenditure rates

Slide Number #86

© 2007 Nan McKay & Associates

The New PHAS AssessmentThe New PHAS Assessment

• Physical condition – Independent inspector (current practice)

• Financial condition – Principally, the AMP’s financial liquidity

• Management operations – Onsite management reviews will eliminate self-certifications and submissions

• Capital Fund – obligation and expenditure rates

Slide Number #87

© 2007 Nan McKay & Associates

Measuring PerformanceMeasuring Performance

Accountability and responsibility• Clear articulation of responsibilities is

needed• Performance of properties will need to be

more closely tied to performance evaluation of staff

• Effective supervision and quality control is a must in making this work

Slide Number #88

© 2007 Nan McKay & Associates

HUD’s New Procurement HandbookHUD’s New Procurement Handbook

Transmittal is Attachment 2

Slide Number #89

© 2007 Nan McKay & Associates

HUD Handbook 7460.8 REV 2HUD Handbook 7460.8 REV 2

Applies specifically to public housing agencies for the operation of public housing

Is not applicable to Indian Housing Authorities or the operation of the Section 8 Housing Choice Voucher Program

Slide Number #90

© 2007 Nan McKay & Associates

HUD Handbook 7460.8 REV 2HUD Handbook 7460.8 REV 2

Also, does not apply to income generated by the Central Office Cost Center (COCC) – not considered Federal program income• Management fees• Bookkeeping fees• Asset management fees

Governed by local & State requirements, if applicable

Slide Number #91

© 2007 Nan McKay & Associates

Delegation of AuthorityDelegation of Authority

Under PBM, more decentralization of procurement function is expected

Policy required for delegation of procurement authority• Limits of authority in terms of dollar value each PHA

classification may make• Other limitations, e.g., types of contracts an individual may

award

Slide Number #92

© 2007 Nan McKay & Associates

Delegation of AuthorityDelegation of Authority

Delegation policy should also be clear if individual staff may further re-delegate any of his/her authority – and how much!

Training for site staff is important• Individual staff will be binding the PHA legally

Slide Number #93

© 2007 Nan McKay & Associates

What Has Been StreamlinedWhat Has Been Streamlined

Increase in the small purchase threshold from $25,000 to $100,000

The establishment of a micro-purchase threshold of $2,000, requiring only one reasonable quote

The use of “incorporation by reference” of mandatory contract clauses into bid specifications and contracts…

Slide Number #94

© 2007 Nan McKay & Associates

What Has Been StreamlinedWhat Has Been Streamlined

Elimination of any required forms for small purchases, with the exception of applicable maintenance and construction contracts exceeding $2,000

The use of a simplified contract for construction work that does not exceed $100,000…

Slide Number #95

© 2007 Nan McKay & Associates

What Has Been StreamlinedWhat Has Been Streamlined

Elimination of requirement to conduct a separate cost/price analysis when obtaining products or services of a commercial nature

Ability of PHAs to “self-certify” that their procurement systems satisfy the requirements of 24 CFR 85.36, thereby eliminating the need for prior HUD approval for most change orders and non-competitive purchases

Slide Number #96

© 2007 Nan McKay & Associates

Developing a Procurement PolicyDeveloping a Procurement Policy

New handbook includes language PHA’s procurement policy should include

Slide Number #97

© 2007 Nan McKay & Associates

Procurement Policy Should Procurement Policy Should IncludeInclude

Statement on access by public to certain information

Clear wording on ethical behavior

Slide Number #98

© 2007 Nan McKay & Associates

Procurement Policy Should Procurement Policy Should IncludeInclude

Procurement methods used by PHA• Petty cash• Small purchase (include dollar level)• Sealed bids• Competitive proposals• Noncompetitive proposals• Cooperative purchasing agreements

Slide Number #99

© 2007 Nan McKay & Associates

Procurement Policy Should Procurement Policy Should IncludeInclude

Conditions for cost & price analysis Methods of solicitation to be used for various levels of

procurement Bonding requirements for construction contracts over $100,000 Contractor qualifications & duties Different types of contracts the PHA will use

Slide Number #100

© 2007 Nan McKay & Associates

Procurement Policy Should Procurement Policy Should IncludeInclude

Identification of required contract clauses Types of specifications the PHA will use Process for filing an appeal Assistance available for small and other types of businesses Required Board approval of policy Delegation of contracting authority

Slide Number #101

© 2007 Nan McKay & Associates

Procurement Policy Should Procurement Policy Should IncludeInclude

Disposition policy (may also be a stand alone policy)

Self-certification (if applicable)

Slide Number #102

© 2007 Nan McKay & Associates

Ethics in Public ContractingEthics in Public Contracting

New handbook emphasizes ethics PHA must have a written code of standards

that governs performance of employees who engage in award & administration of contracts

Included in the PHA’s procurement policy

Slide Number #103

© 2007 Nan McKay & Associates

Ethics in Public ProcurementEthics in Public Procurement

PHA’s procurement policy should prohibit any employee from participating in the selection of a vendor or award of a contract if a conflict – real or perceived – would be involved

Page 7-25

Slide Number #104

© 2007 Nan McKay & Associates

Ethics in Public ProcurementEthics in Public Procurement

Also recommended that policy prohibit employees who participate in the procurement process from accepting gifts, gratuities, favors or kickbacks from current or potential vendors or contracts

Page 7-25

Slide Number #105

© 2007 Nan McKay & Associates

Ethics in Public ProcurementEthics in Public Procurement

Penalties should be established & included in policy for those employees who breach ethical standards• Oral or written warnings/reprimands• Suspension with/without pay• Termination of employment• Dismissal from the office or agency position

Slide Number #106

© 2007 Nan McKay & Associates

HUD Administrative Reform HUD Administrative Reform InitiativeInitiative

Slide Number #107

© 2007 Nan McKay & Associates

HUD’s Administrative Reform HUD’s Administrative Reform InitiativeInitiative

On July 12, HUD will launch first meeting to focus on non-statutory administrative requirements that might be streamlined to• Better support transition to asset mgmt• Ensure consistency with norms in multifamily

Slide Number #108

© 2007 Nan McKay & Associates

Administrative Reform – 10 AreasAdministrative Reform – 10 Areas

Occupancy Capital Fund and

Agency Plans Resident involvement

and self-sufficiency General monitoring

Development and asset repositioning

Homeownership General management Financial management Systems Structure

Slide Number #109

© 2007 Nan McKay & Associates

Proposed Rule – Rent RefinementProposed Rule – Rent Refinement

Attachment 3 Issued June 19, 2007

• Applies to public housing and HCV

• Purpose is to make EIV mandatory and more functional

Slide Number #110

© 2007 Nan McKay & Associates

Proposed Rule Would:Proposed Rule Would:

Require all family members, regardless of age, to disclose and document SSNs

Require PHAs to get proof of citizenship or legal status

Change definition of annual income from anticipated future income to actual income received

Slide Number #111

© 2007 Nan McKay & Associates

Civil Rights Monitoring Civil Rights Monitoring

Slide Number #112

© 2007 Nan McKay & Associates

Civil Rights-Related Reviews Civil Rights-Related Reviews

11/9/2006 & 3/1/2007 – Federal Register Notices 6/13/2007 – Final civil rights review documents

posted on www.hudclips.org• Joint effort by PIH and FHEO to increase oversight of

fair housing issuesTwo checklists – attachment A & B

Slide Number #113

© 2007 Nan McKay & Associates

Attachments A & BAttachments A & B

• PIH is planning to conduct civil rights monitoring reviews of 20 PHAs in fiscal year 2007 (i.e., before September 30, 2007)

• Focus is on reasonable accommodation and LEP issues

• Data collected helps HUD evaluate PHA compliance with civil rights and fair housing laws and regulations

Slide Number #114

© 2007 Nan McKay & Associates

Attachment AAttachment A

Attachment A – will be completed by a PIH reviewer• Will be completed as part of on-site

comprehensive/consolidated reviews• PIH reviewer completes form and sends it to FHEO

for review

Slide Number #115

© 2007 Nan McKay & Associates

Attachment AAttachment A

The PIH reviewer does not analyze the answers to the checklist• However, FHEO “will…take appropriate action, if

necessary” depending on the responses of the PIH reviewer• This form leaves some discretion to the reviewer and FHEO

as to what is reported

Slide Number #116

© 2007 Nan McKay & Associates

Attachment AAttachment A

Three main fair housing topics covered:• Notice of fair housing rights to participants• General fair housing and civil rights

violations and compliance issues• LEP

Slide Number #117

© 2007 Nan McKay & Associates

Attachment A - NoticeAttachment A - Notice

Questions 1-5:• FH poster must be displayed• PHA Agency Plans, policies, regulations and rules need to be

posted and available to the public as well as participants• Notice to participants regarding how to file a fair housing

complaint

Slide Number #118

© 2007 Nan McKay & Associates

Attachment A – General FHAttachment A – General FH

Very broad criteria that is being examine:• (Part II) “Is there anything else that is related to civil

rights or fair housing that should be noted…?”• Form suggests for PIH reviewers to gather

information from “media reports” and “racial/ethnic tensions” complaints at developments

Slide Number #119

© 2007 Nan McKay & Associates

Attachment A - LEPAttachment A - LEP

Asks about LEP four-factor test and asks PIH reviewer to send in a copy of the analysis• Requests copy of LAP• Inquires into bi-lingual staff• Inquires into contracts for language services

Slide Number #120

© 2007 Nan McKay & Associates

Attachment BAttachment B

Checklist purpose “serves as an alert to PIH and FHEO to certain PHA practices regarding Section 504”• Unlike A, this form is completed by the PHA and is

collected by PIH during its on-site review• Results are referred to FHEO for follow-up

Slide Number #121

© 2007 Nan McKay & Associates

Attachment BAttachment B

Specific questions regarding:• Section 504 coordinator• Units meeting UFAS-accessibility standards• Distribution of accessible units• Reasonable accommodation policy/process

Including how/when RA policy is given to applicants and residents

Slide Number #122

© 2007 Nan McKay & Associates

Attachment BAttachment B

Final question is very broad:• “What other rules or policies has the PHA

implemented that affect persons with disabilities?”• Be prepared to show affirmative steps the PHA has

taken to market to and support people with disabilities in the community

Slide Number #123

© 2007 Nan McKay & Associates

Attachments A & BAttachments A & B

These forms have expiration date of 2010 LEP and disability support are issues

HUD/FHEO is taking very seriously Show good faith efforts and take affirmative

action – make a plan to deal with these issues!

Slide Number #124

© 2007 Nan McKay & Associates

Attachment BAttachment B

Additional inquiry into:• Service animals• Deposits• TTY• Alternative forms of communication• Mobility support, voucher exts, FMR exceptions for HCV

applicants/participants

Slide Number #125

© 2007 Nan McKay & Associates

SummarySummary

Q &A