slide 5.1 statements of cash flows chapter 5. slide 5.2 by the end of this chapter, you should be...

TRANSCRIPT

Slide 5.1

Statements of cash flows

Chapter 5

Slide 5.2

By the end of this chapter, you should be able to:

• prepare a statement of cash flows in accordance with IAS 7;

• analyse a statement of cash flows;

• critically discuss their strengths and weaknesses.

Objectives

Slide 5.3

Cash Flow Statement

Cash Flow Statement is a summary of a business’s cash receipts and cash payments, over a certain period of time – usually one year.

It shows the cash that has come from and/or gone to sources external (outside) to the business.

Slide 5.4

Cash Flow Statement

The Cash Flow Statement classifies the sources of cash in terms of: cash flows from operations (operating activities), cash flows from investing activities, and cash flows from financing activities. The Cash Flow Statement has two main purposes: measuring a business’s financial health, and explaining the relationship between the Income

Statement prepared under accrual accounting and the actual movement in cash from operations.

Slide 5.5

Cash Flow Statement

Why is it important? Cash is the lifeblood of an entity. A business cannot

survive without cash. Cash, not reported profit, pays the bills.

A business’s ability to raise cash through financing activities is dependent upon its ability to generate cash from operations.

Creditors and shareholders are not keen to invest in a business that does not generate enough cash from operations to assure prompt payment of maturing liabilities, interest, and dividends.

Slide 5.6

Cash Flow Statement

The Cash Flow Statement is designed to assist stakeholders to assess: the ability of a business to generate positive cash

flows in future periods both the cash and non-cash aspects of the business’s

investing and financing transactions for the period The Cash Flow Statement reports the business’s

investments in such assets as plant and equipment. ….. more

Slide 5.7

Cash Flow Statement

the business’s ability to meet its obligations and to pay dividends

Shareholders are interested in receiving dividends on their investment. Creditors (lenders and suppliers) want to receive their payments on time.

reasons for differences between the amount of profit for the period and the related net cash flow from operations

a business’s cash balance can decrease when its profit for the period is high (e.g. through large debt repayments), and cash can increase when profit for the period is low (e.g. through borrowing or sales of non-current assets).

Slide 5.8

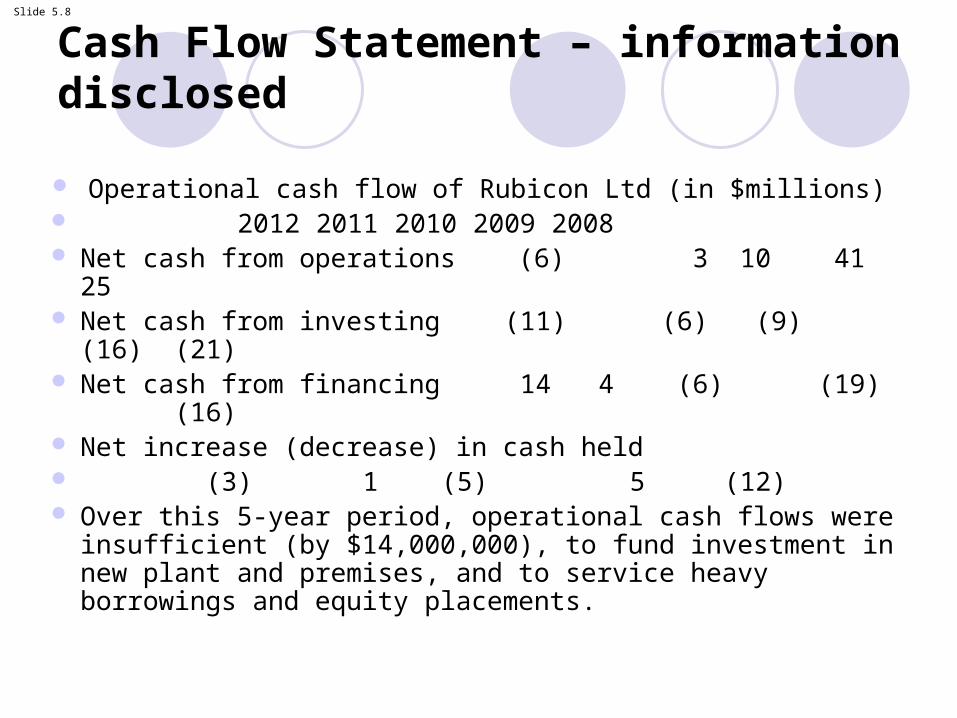

Cash Flow Statement – information disclosed

Operational cash flow of Rubicon Ltd (in $millions) 2012 2011 2010 2009 2008 Net cash from operations (6) 3 10 41 25 Net cash from investing (11) (6) (9) (16) (21) Net cash from financing 14 4 (6) (19) (16) Net increase (decrease) in cash held (3) 1 (5) 5 (12) Over this 5-year period, operational cash flows were insufficient

(by $14,000,000), to fund investment in new plant and premises, and to service heavy borrowings and equity placements.

Slide 5.9

Cash Flow Statement

IAS 7 requires the cash flow information to be classified by its major sources and dispositions, namely its operating , investing and financing activities.

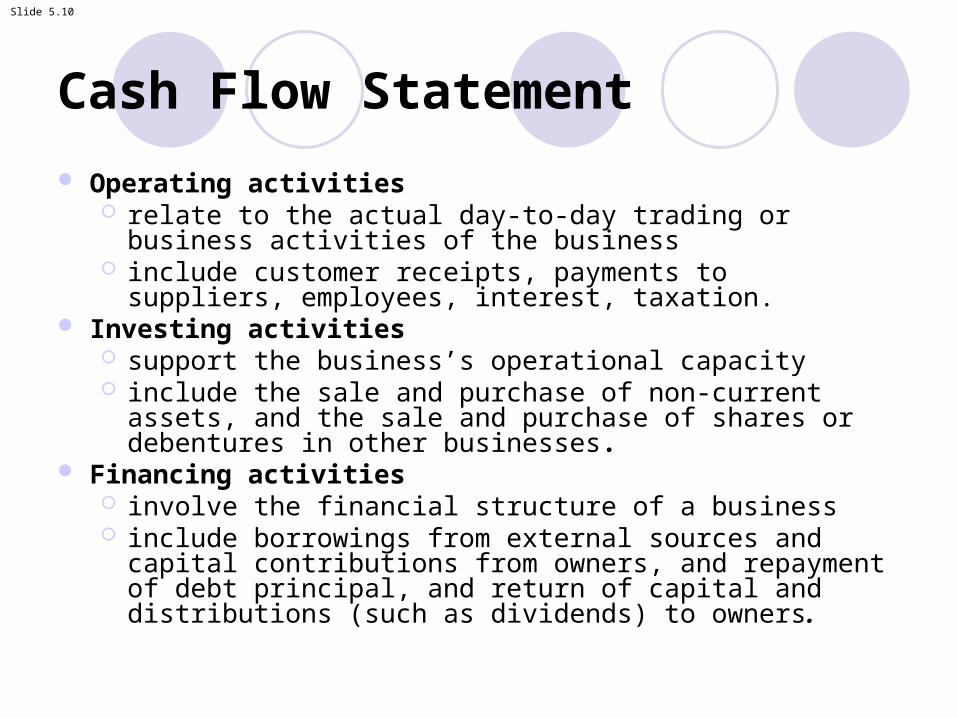

Slide 5.10

Cash Flow Statement

Operating activities relate to the actual day-to-day trading or business activities of

the business include customer receipts, payments to suppliers, employees,

interest, taxation. Investing activities

support the business’s operational capacity include the sale and purchase of non-current assets, and the

sale and purchase of shares or debentures in other businesses.

Financing activities involve the financial structure of a business include borrowings from external sources and capital

contributions from owners, and repayment of debt principal, and return of capital and distributions (such as dividends) to owners.

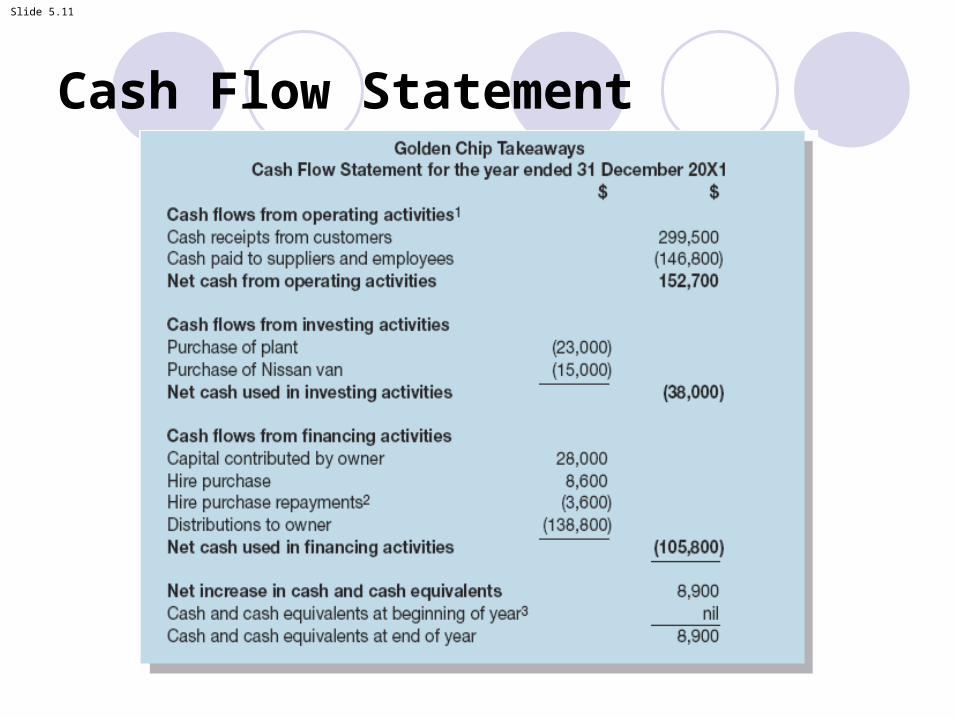

Slide 5.11

Cash Flow Statement

Slide 5.12

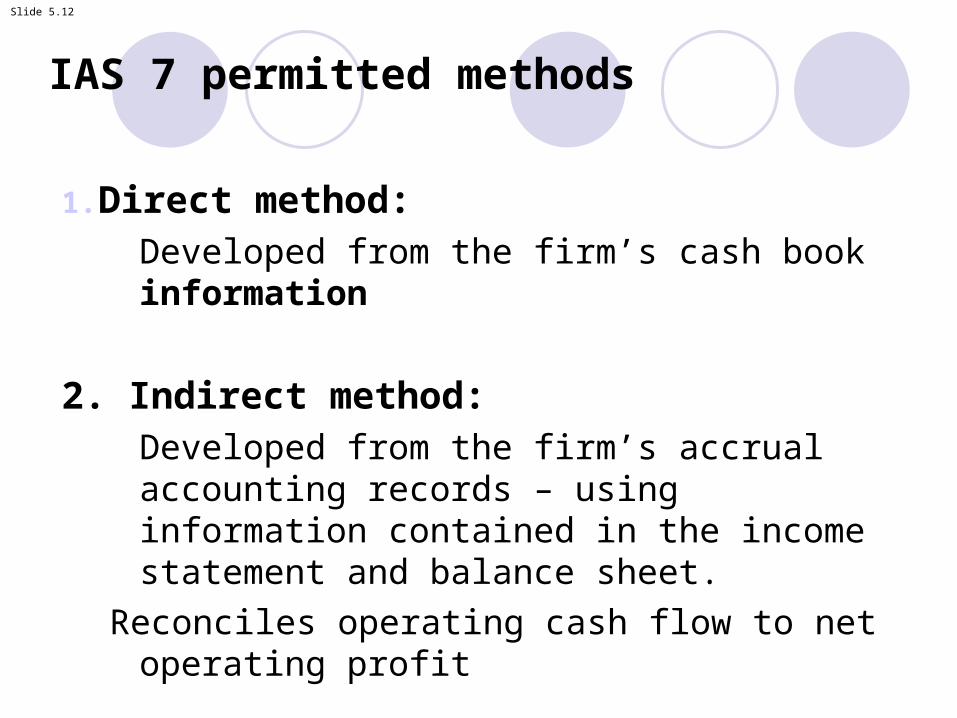

IAS 7 permitted methods

1. Direct method:Developed from the firm’s cash book information

2. Indirect method:Developed from the firm’s accrual accounting records – using information contained in the income statement and balance sheet.

Reconciles operating cash flow to net operating profit

Slide 5.13

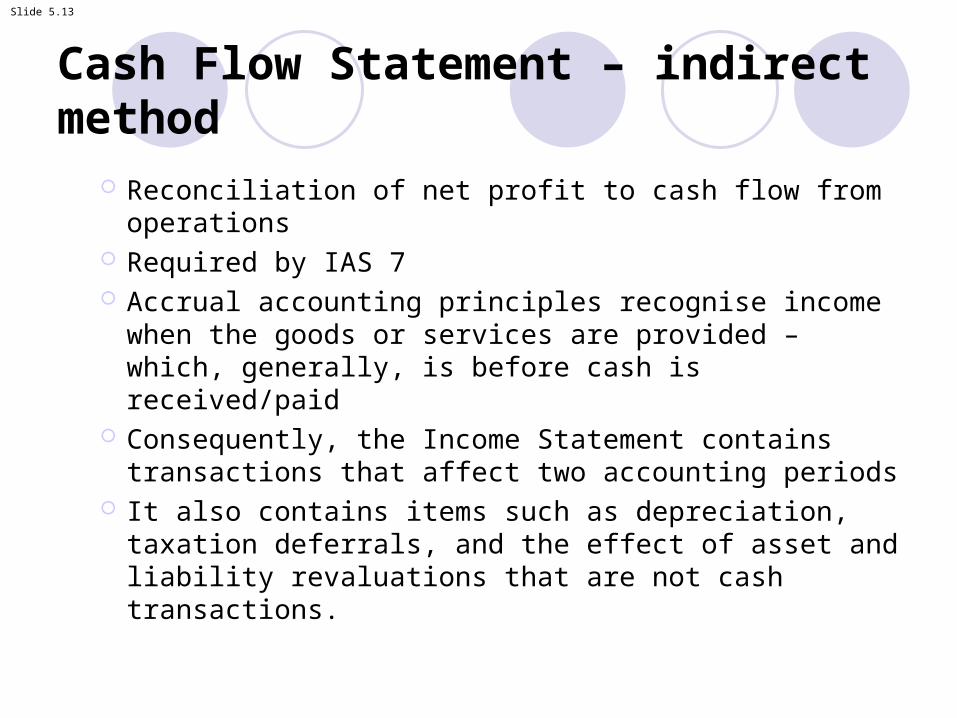

Cash Flow Statement – indirect method

Reconciliation of net profit to cash flow from operations Required by IAS 7 Accrual accounting principles recognise income when

the goods or services are provided – which, generally, is before cash is received/paid

Consequently, the Income Statement contains transactions that affect two accounting periods

It also contains items such as depreciation, taxation deferrals, and the effect of asset and liability revaluations that are not cash transactions.

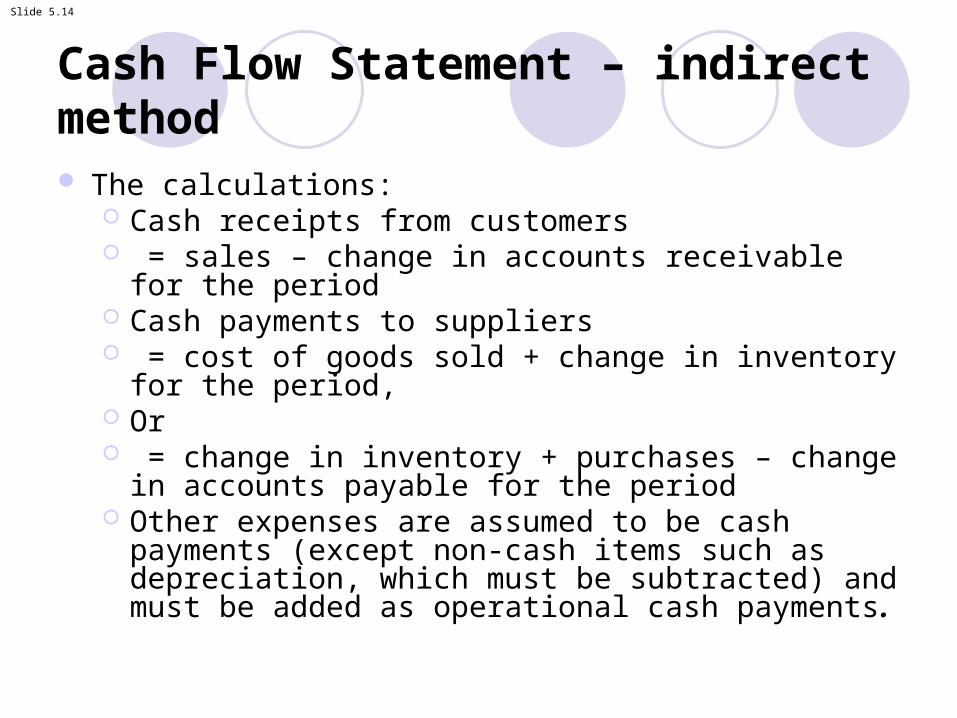

Slide 5.14

Cash Flow Statement – indirect method The calculations:

Cash receipts from customers = sales – change in accounts receivable for the period Cash payments to suppliers = cost of goods sold + change in inventory for the

period, Or = change in inventory + purchases – change in

accounts payable for the period Other expenses are assumed to be cash payments

(except non-cash items such as depreciation, which must be subtracted) and must be added as operational cash payments.

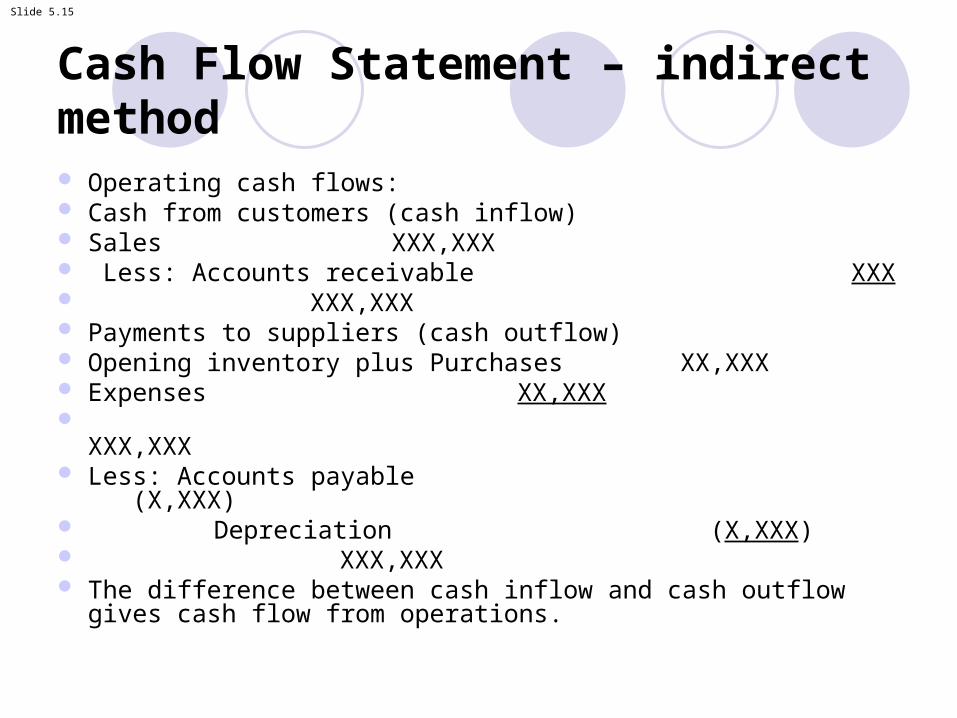

Slide 5.15

Cash Flow Statement – indirect method Operating cash flows: Cash from customers (cash inflow) Sales XXX,XXX Less: Accounts receivable XXX XXX,XXX Payments to suppliers (cash outflow) Opening inventory plus Purchases XX,XXX Expenses XX,XXX XXX,XXX Less: Accounts payable (X,XXX) Depreciation (X,XXX) XXX,XXX The difference between cash inflow and cash outflow gives

cash flow from operations.

Slide 5.16

Cash Flow Statement – indirect method

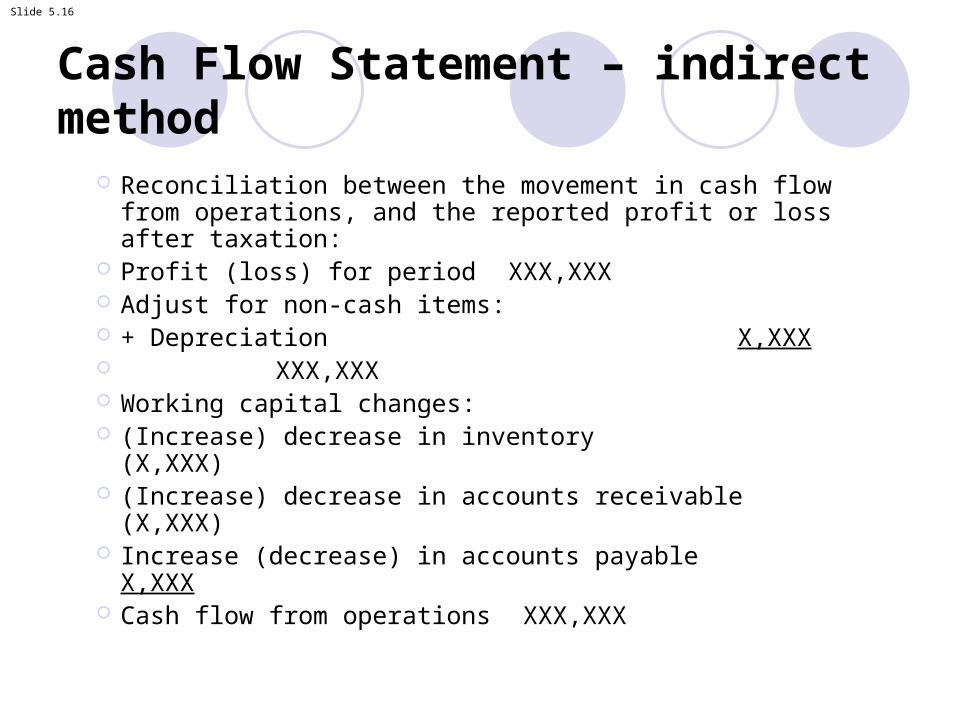

Reconciliation between the movement in cash flow from operations, and the reported profit or loss after taxation:

Profit (loss) for period XXX,XXX Adjust for non-cash items: + Depreciation X,XXX XXX,XXX Working capital changes: (Increase) decrease in inventory (X,XXX) (Increase) decrease in accounts receivable (X,XXX) Increase (decrease) in accounts payable X,XXX Cash flow from operations XXX,XXX

Slide 5.17

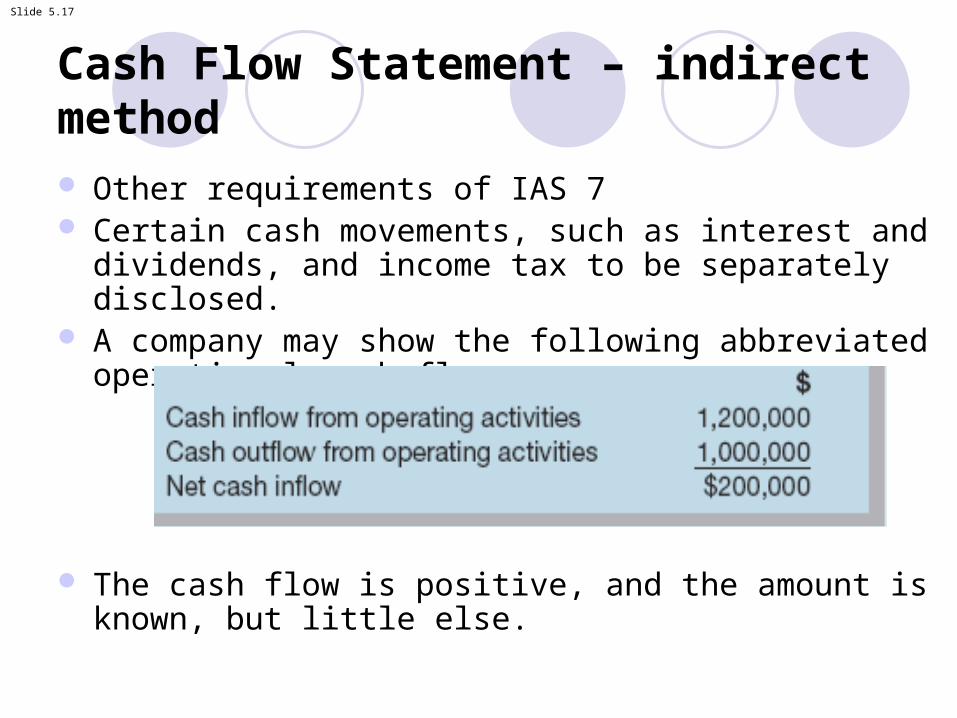

Cash Flow Statement – indirect method Other requirements of IAS 7 Certain cash movements, such as interest and dividends,

and income tax to be separately disclosed. A company may show the following abbreviated operational

cash flows:

The cash flow is positive, and the amount is known, but little else.

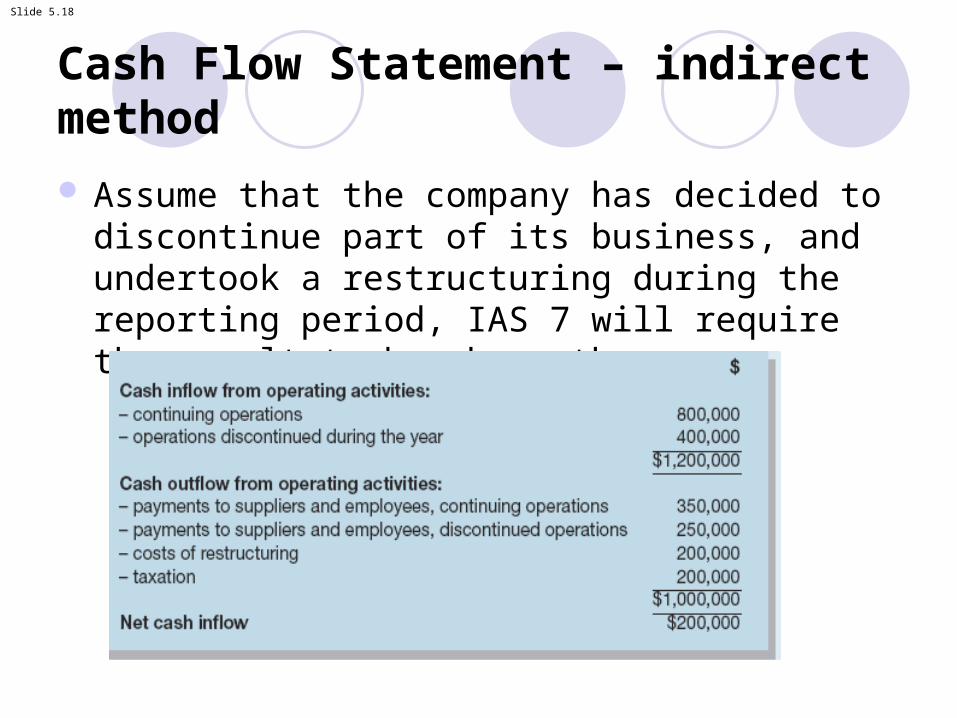

Slide 5.18

Cash Flow Statement – indirect method

Assume that the company has decided to discontinue part of its business, and undertook a restructuring during the reporting period, IAS 7 will require the result to be shown thus:

Slide 5.19

Step approach to preparation of a statement of cash flows – indirect method

Step 1:

Calculate differences in the Balance Sheets and note whether to treat under Operating activities, Investing activities, Financing activities or as a cash equivalent.

Slide 5.20

Steps 2 and 3

Step 2: Identify any items in the income statement for the year

after earnings before interest and tax (EBIT) (also known as profit before interest and tax (PBIT)), to be entered under operating, investing or financing activities.

Step 3: Refer to the PPE schedule to identify any acquisitions,

disposals and depreciation charges that affect the cash flows.

Slide 5.21

IAS 7 format – indirect method

• Cash flow from operating activities

• Cash generated from operations

• Cash flows from investing activities

• Cash flows from financing activities

• Net increase in cash and cash equivalents.

Slide 5.22

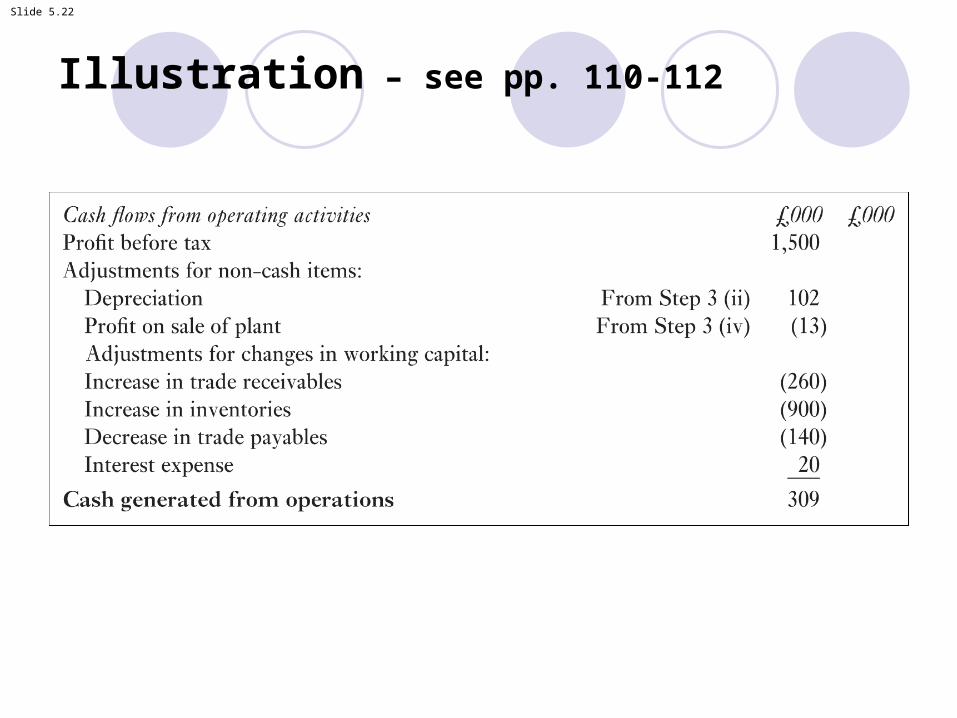

Illustration – see pp. 110-112

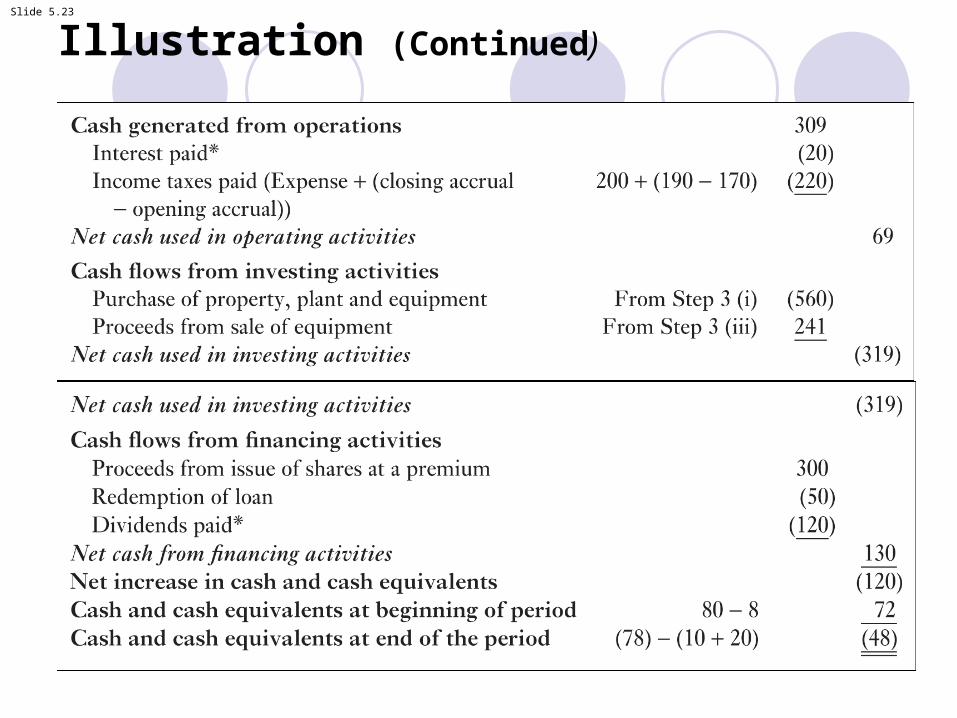

Slide 5.23

Illustration (Continued)

Slide 5.24

Methods of presenting cash flows from operating activities

Direct method

Indirect method.

Slide 5.25

The direct method

Reports cash inflows and outflows directlyStarts with the major categories of gross cash

receipts and paymentsCash flows such as receipts from customers and

payments to suppliers are stated separately within the operating activities.

Slide 5.26

Indirect method

Starts with profit before tax

Highlights differences between operating profit and net cash flow from operating activities

Indicates quality of earnings

Able to estimate future cash flows and adjust for accruals.

Slide 5.27

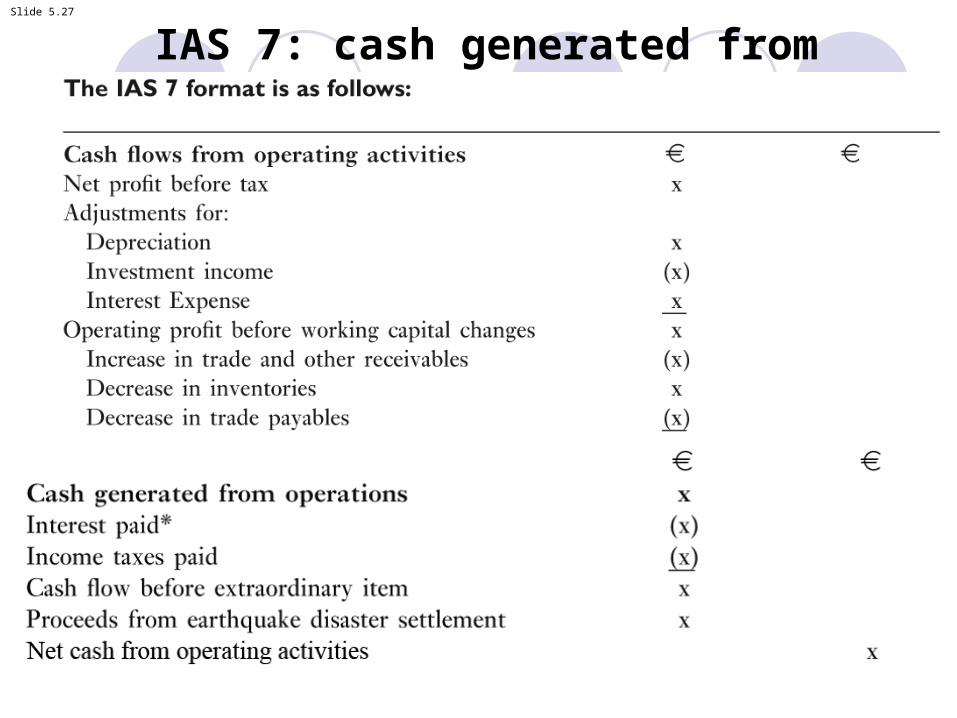

IAS 7: cash generated from operations

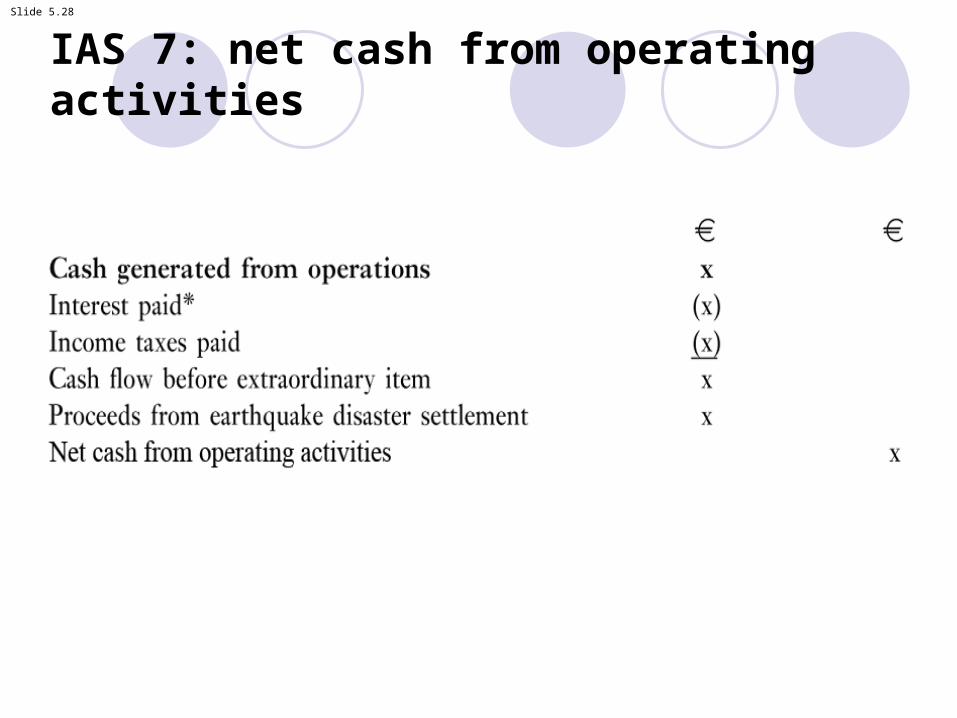

Slide 5.28

IAS 7: net cash from operating activities

Slide 5.29

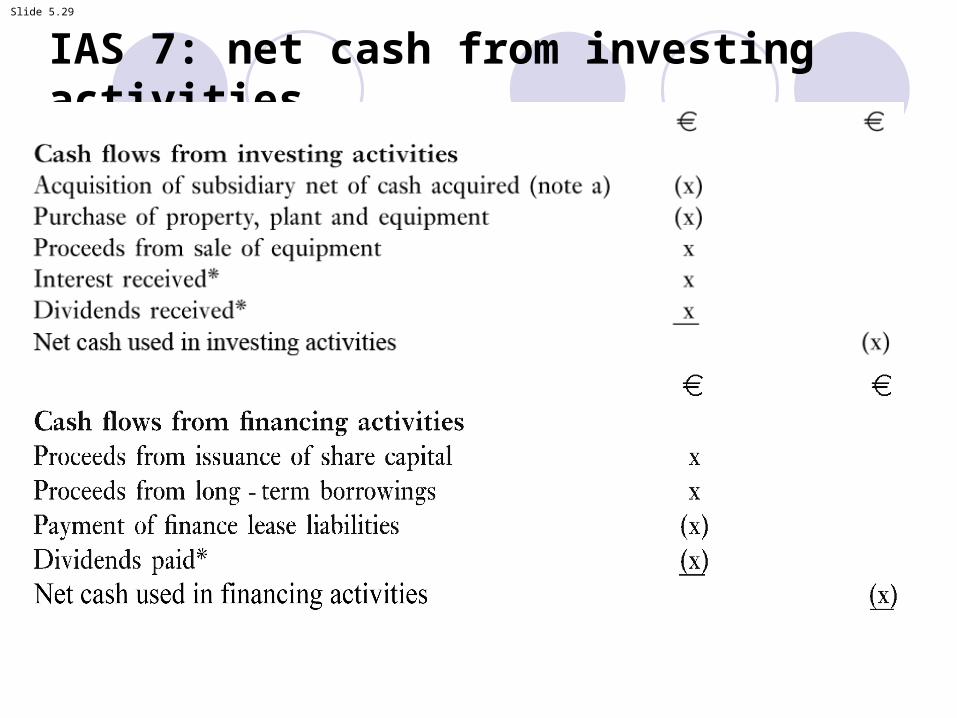

IAS 7: net cash from investing activities

Slide 5.30

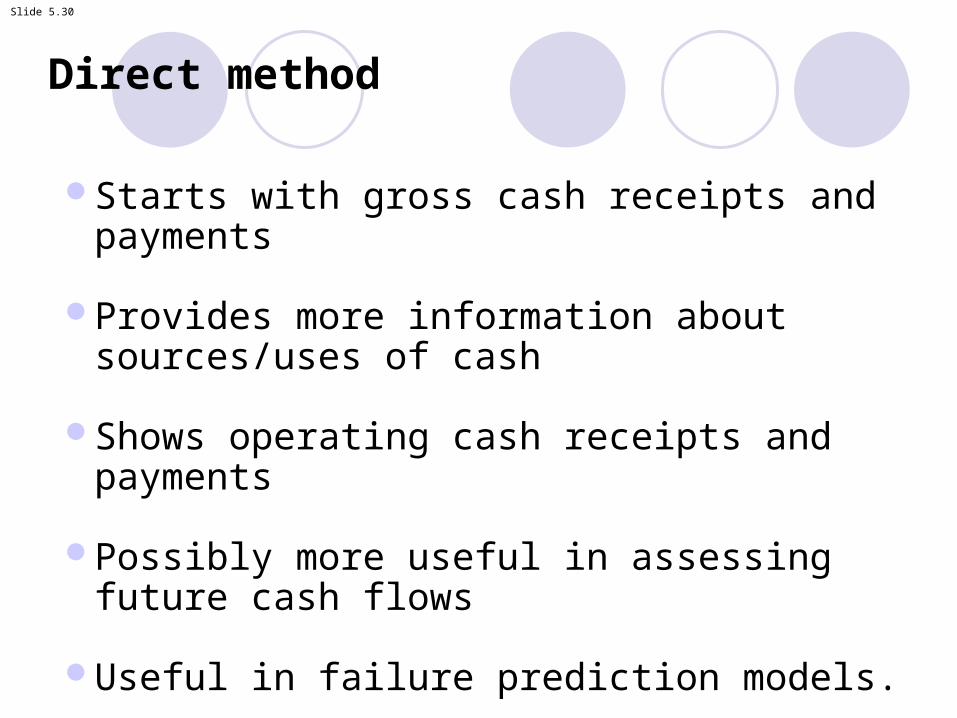

Direct method

Starts with gross cash receipts and payments

Provides more information about sources/uses of cash

Shows operating cash receipts and payments

Possibly more useful in assessing future cash flows

Useful in failure prediction models.

Slide 5.31

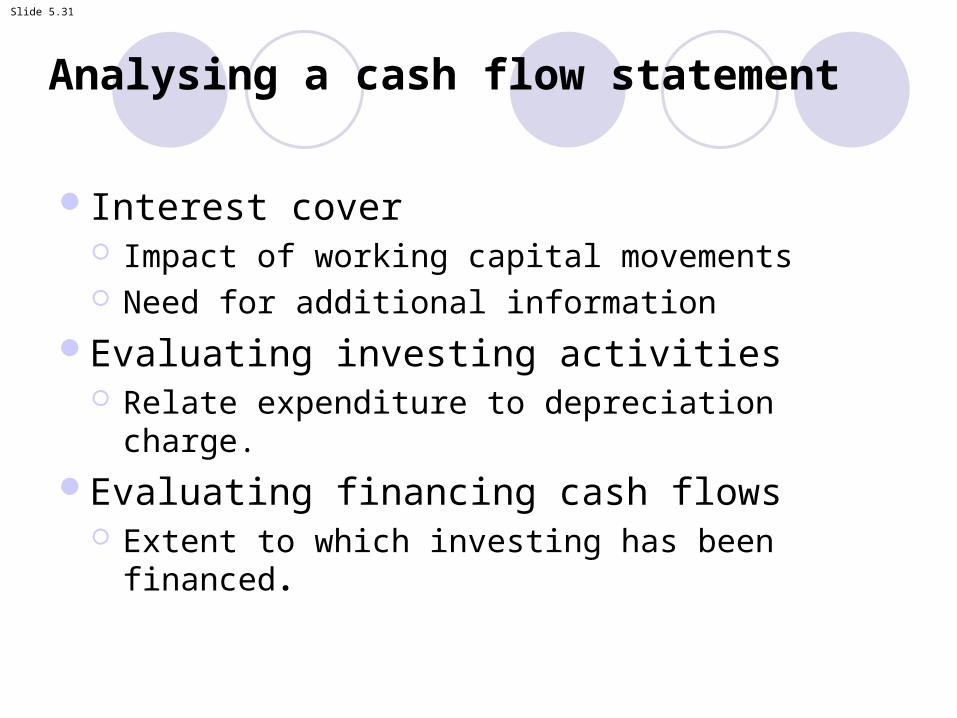

Analysing a cash flow statement

Interest cover Impact of working capital movements Need for additional information

Evaluating investing activities Relate expenditure to depreciation charge.

Evaluating financing cash flows Extent to which investing has been financed.

Slide 5.32

Discussion

Do you agree or disagree with the following statements: The cash flow statement is the link between profitability

and viability All companies should be required to report using the

indirect format.

Slide 5.33

Discussion (Continued)

Do you agree or disagree with the following statements:The format of the cash flow statement should be left to the discretion of managementThe requirement to standardise the CFS format indicates a lack of trust in management.

Slide 5.34

Review questions

1. Explain the information that a user can obtain from a cash flow statement that cannot be obtained from the current or comparative statements of financial position.

4. Many people preferred the direct method for cash flow preparation, but IAS 7 did not require it. Discuss possible reasons for allowing choice and the effectiveness of the IASC’s encouragement to companies to use the direct method.

7. A negative free cash flow is always a sign of a company in trouble. Discuss.