slide 12.1 pauline weetman, financial and management accounting, 5 th edition © pearson education...

TRANSCRIPT

Slide 12.1

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Chapter 12

Ownership interest

Slide 12.2

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Non-current (fixed) assets

plus

Current assets

minus

Current liabilities

minus

Liabilities due after one year

equals

Ownership Interest[Share capital plusReserves of past profits]

Structure of a statement offinancial position

Slide 12.3

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Statement of financial position of Safe and Sure plc

370.4464.3Equity holders’ funds

340.8431.615Retained earnings

4.64.614Revaluation reserve

5.58.513Share premium accountReserves

19.519.612Called-up share capitalCapital and

£m£m

Year 6Year 7Notes

Slide 12.4

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Issue of shares at the date of incorporation

When company first comes into existence:

• it issues shares to the owners,

• who become shareholders.

• Each share has a named value

• which is called its nominal value (par value)

Slide 12.5

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Certificate number 24516

Public Company plcSHARE CERTIFICATE

This is to certify that

J A Smith

is the registered owner of 100,000 ordinary shares of 25 pence each,

Signed P McDowall

Company Secretary

Given under Seal of the Company the 15th day of August 1985

J JonesW BrownDirectors

Share certificate

Slide 12.6

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

J A Smith has paid £25,000 to the company. That is the limit of this person's liability if the

company fails.The company issues 100,000 shares to J A

Smith at a price of 25 pence each. The shares represent the ownership interest in the company.

Assets – Liabilities = Ownership interest

Increase in cash

£25,000

Increase in nominal valueof shares£25,000

Share certificate (Continued)

Slide 12.7

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Some time later…

• Company has traded profitably: Company wishes to raise as much funds as possible.

• Will issue shares at their market value.

• Nominal value remains the same, the market value may be quite different.

• Nominal value 25 pence but the shares are selling in the market at 80 pence each.

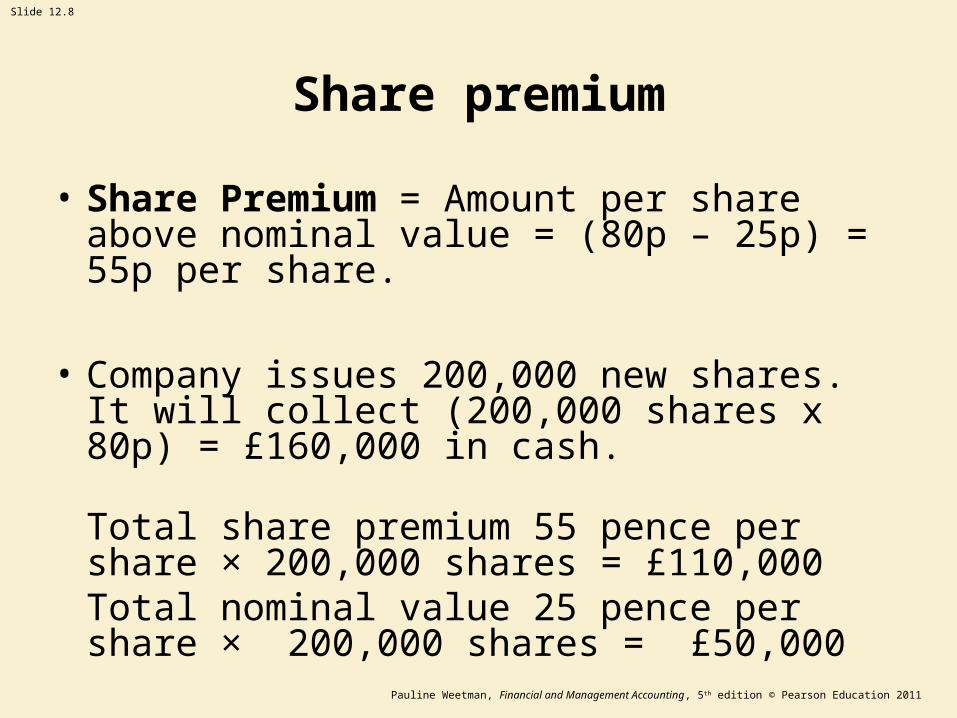

Slide 12.8

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Share premium

• Share Premium = Amount per share above nominal value = (80p – 25p) = 55p per share.

• Company issues 200,000 new shares. It will collect (200,000 shares x 80p) = £160,000 in cash.

Total share premium 55 pence per share × 200,000 shares = £110,000Total nominal value 25 pence per share × 200,000 shares = £50,000

Slide 12.9

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Share premium (Continued)

Increase in nominal valueof shares £50,000

and increase in sharepremium £110,000

Increase in cash £160,000

Assets – Liabilities = Ownership interest

Slide 12.10

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Revaluation

Hotel cost is £560,000. The hotel is run successfully for a period of three years and at the end of that period a professional valuer confirms that the hotel, if sold, would probably result in sale proceeds of £620,000.

The directors of the company may wish to tell shareholders about this increased market value of the company's (fixed) asset.

Slide 12.11

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Revaluation – choices

1. Keep the reported value at £560,000 (the historical cost) but include a note to the statement of financial position explaining that the market value is £620,000.

2. Alternative treatment is to RECOGNISE in financial statements the increase in value. But not a realised profit.

Slide 12.12

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Recognise increase in value – not ‘realised’

Increase in revaluation reserve as part of the ownership interest

£60,000

Increase in value of non-current (fixed) asset

£60,000

Assets – Liabilities = Ownership Interest

Slide 12.13

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Foreign currency gains & losses

Gains or losses resulting from changes in the rates of exchange with regard to assets held and liabilities owed and denominated in a different currency.

• Loans $6m when rate of exchange is £1 = $2Liability expressed in £ = (6 × 1/2) = £3m

• Rate of exchange changes to £1 = $3 Liability expressed in £ = (6 × 1/3) = £2m

Slide 12.14

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Foreign currency (Continued)

• Assets – Liabilities↓ = Ownership interest↑ Gain of £1m but not a realised gain

Slide 12.15

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Example

• A company, Office Owner Ltd, is formed on 1 January Year 1 by the issue of 4m ordinary shares of 25 pence nominal value each.

• The cash raised from the issue is used on 2 January to buy an office block which is rented to a customer for an annual rent of £50,000. The tenant carries all costs of repairs.

• The company's administration costs for the year are £10,000.

• At the end of the year the office block is valued by an expert at £1,015,000.

• On the last day of the year the company issues a further 2m ordinary shares at a price of 40 pence each, to raise cash for expansion plans in Year 2.

Slide 12.16

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Date Transaction or event Effect on Effect on

Year 1 Assets Ownership interest

Jan. 1 Issue of shares at nominal value

Increase asset of cash Increase share capital at nominal value

Jan. 2 Purchase of office block

Increase asset property.Decrease asset of cash

No impact

Jan.–Dec.

Rent received Increase asset of cash Revenue of the period

Jan. –Dec.

Administration costs Decrease asset of cash Expense of the period

Dec. 31 Revaluation of asset Increase asset of property

Increase ownership interest by revaluation

Dec. 31 Issue of further shares Increase asset of cash Increase share capital at nominal value and increase share premium

Analysis of transactions for Year 1

Table 12.1 Office Owner Ltd – analysis of transactions for Year 1

Increase asset of cash

Slide 12.17

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Date Transaction Cash Office SC S,Prem Ret. Rev

Year 1 £000’s £000’s £000’s £000’s £000’s £000’s

Jan 1 Issue of shares 1,000 1,000

Jan 2 Purchase of office block

(1,000) 1,000

Jan-Dec

Rent received 50 50

Jan –Dec

Administration costs

(10) (10)

Dec 31 Revaluation of asset

15 15

Dec 31 Issue of further shares

800 500 300

840 1,015 1,500 300 40 15

1,855 1,855

Analysis of transactions for Year 1 (Continued)

Table 12.2 Office Owner Ltd – spreadsheet of transactions for Year 1

Slide 12.18

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Office Owner Ltd £000’s

Fixed asset: Office block 1,015

Current asset: Cash 840

Net assets 1,855

Share capital 1,500

Share premium 300 Reserves

Revaluation reserve 15

Retained earnings 40

1,855

Balance sheet at end of year Year 1

Slide 12.19

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Additional primary financial statements

(A) IASB standards: Statement of changesin equity.

(B) UK ASB standards: Statement of total recognised gains and losses (STRGL).

Slide 12.20

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Statement of changes in equity

Must report

(a) Profit or loss for the period

(b) Items of income and expense for the period required to be reported directly through equity

(c) Effects of changes in accounting policies and correction of errors.

A statement reporting (a) + (b) + (c) also called a statement of comprehensive income.

Slide 12.21

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Statement of changes in equity (Continued)

Must also report

(d) Transactions with equity holders (e.g. dividend).

(e) Retained earnings at start and end of period.

(f) Explanation of changes in each class of equity.

A statement showing (a) to (f) is called a statement of changes in equity.

Slide 12.22

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

UK Statement of total recognised gains and losses (STRGL)

• Statement that helps to bridge the gap between income statement (profit and loss account) and balance sheet.

• STRGL shows the extent to which shareholders’ funds have increased or decreased from the various gains and losses of the period.

• Income statement (profit and loss account) only reports realised profits (the results of transactions with third parties.)

Slide 12.23

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

STRGL (Continued)

Income statement (profit and loss account) only reports realised profits (the results of transactions with third parties.)

Add to this unrealised gains and losses, e.g.

• Revaluations of fixed assets.

• Effect of exchange rates on foreign currency translation.

Slide 12.24

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

UK movements in shareholders’ funds

Shows all changes in shareholders’ funds. Could include:

• Issue of new shares.

• Repurchase and cancellation of shares.

• Profit of the period.

• Dividends of the period.

• Effect of exchange rates on foreign currency translation.

• Revaluations of fixed assets.

Slide 12.25

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dividends

Reward to the owner (usually cash)Questions:1. Does the company have sufficient cash to pay

a dividend?2. Has the company made sufficient profits (increase in ownership interest) to justify a dividend?The decision is taken by the Directors.It is approved by shareholders at Annual General Meeting.

Slide 12.26

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dividends paid

Might be:

• Dividend proposed for previous year, now paid.

• Interim dividend as part of dividend for current year,

A ↓ – L = OI ↓

Decrease in asset of cash,

Decrease in ownership interest reported in income statement (profit and loss account).

Slide 12.27

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Final dividend

• At end of accounting year, after profits have been calculated, directors decide whether to pay a final dividend and, if so, how much.

• This is not a liability because it has not been approved by shareholders. It is a proposal from directors.

• The proposal to pay the dividend is reported as an item in the directors’ report.

Slide 12.28

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Issue of further shares (1)

Capitalisation issue (Bonus issue or Scrip issue)

A company decides to increase the number of shares with no change to assets or liabilities.

Slide 12.29

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Capitalisation issue

• Share price tends to outperform the market after the announcement of a capitalisation issue.

• There tends to be an acceptable range of prices for listed shares. £20 per share maximum. Increase number of shares, to scale down the price per share.

• Capitalisation issue is often made out of reserves (of retained profits). Message given to shareholders that these are now part of the long-term funds of the company. No longer available to cover the payment of dividends.

Slide 12.30

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Issue of further shares (2)

Rights issueWhen a public (quoted) company raises finance by the issue of shares, this is normally done by way of a ‘rights issue’. This gives existing shareholders the choice of subscribing for new shares in the company and so maintain their proportional shareholding in the company.The issue price is set at below the current market price of the shares.

Slide 12.31

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Capitalisation issue

Assume that Office Owners Ltd wishes to make a 1 for 5 capitalisation issue.

Share capital is 6 million 25 p shares Nominal value £1.5 million

New shares:

6,000,000/5 = 1,200,000

Nominal value:

1,200,000 × 25 p = £300,000

Slide 12.32

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Increase in share capital £300,000decrease in reserves £300,000

Assets – Liabilities = Ownership interest

Capitalisation issue (Continued)

Slide 12.33

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Date Transaction or event

Cash Office block

Share capital

Share premium

Retained earnings

Reval’n reserve

£000’s £000’s £000’s £000’s £000’s £000’s

At 1 Jan Yr 2

Balance sheet values

840 1,015 1,500 300 40 15

Jan 1 for 5 capitalis-ation issue

300 (300)

840 1,015 1,800 nil 40 15

1,855 1,855

Capitalisation issue in Jan Year 2

Slide 12.34

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Rights issue

Company has 400 million shares in issue of nominal value 25 pence per share. It wishes to issue a further 100 million shares.

This means a rights issue of 1 for 4,

for example, a holder of 8,000 shares will be given the right to subscribe for 2,000 new shares.

Slide 12.35

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Rights issue (Continued)

A shareholder who does not wish to invest any more in the company is able to sell the ‘rights’.

Assume an issue price of 150 pence per share.

This is split for accounting purposes into the nominal value of 25 pence and the premium of 125 pence.

Slide 12.36

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Rights issue (Continued)

• In terms of the accounting equation the effect of the rights issue on the balance sheet is:

• Total cash raised by the issue £1.5 x 100 million shares = £150m

• Nominal value of shares issued will be 25 pence × 100 million shares = £25m

• Share premium on issue of shares will be £1.25 × 100 million shares = £125m.

Slide 12.37

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

increase in share capital £25mincrease in share premium £125m

Increase in cash £150m

Assets – Liabilities = Ownership interest

Rights issue (Continued)

Slide 12.38

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

(a) At the end of the month it is found that the roof has been leaking and rainwater has damaged goods worth £500.

Year-end adjustments

Expense of £500 for inventory (stock) damaged

Inventory (stock) decreases by £500

Assets – Liabilities = Ownership interest

Slide 12.39

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

(b) The business uses gas to heat a water boiler and it is estimated that consumption for the month amounts to £80.

Year-end adjustments (Continued)

Ownership interest =Liabilities – Assets

Expense of £80 for gas consumed

Obligation to pay for gas consumed £80

Slide 12.40

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Illustration

• See Supplement to Chapter 12 in the book

Slide 12.41

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Chapter 12

Bookkeeping supplement

Slide 12.42

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

DEBIT ENTRIES CREDIT ENTRIES

Left-hand side of the equation

Asset Increase Decrease

Right-hand side of the equation

Liability Decrease Increase

Ownership interest Expense Revenue

Capital withdrawn Capital contributed

Debit and credit entries

Slide 12.43

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Expense of £500 for inventory (stock) damaged

Inventory (stock) decreases by £500

Ownership interest= Assets – Liabilities

(a) At the end of the month it is found that the roof has been leaking and rainwater has damaged goods worth £500.

Year-end adjustments

Slide 12.44

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dr Cost of goods sold £500Cr Inventory (stock) of goods £500

Year-end adjustments (Continued)

Slide 12.45

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

(b) The business uses gas to heat a water boiler and it is estimated that consumption for the month amounts to £80.

Year-end adjustments (Continued)

Assets

Expense of £80 for gas consumed

Obligation to pay for gas consumed £80

Ownership interest = Liabilities –

Slide 12.46

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Dr Expense of gas £80 Cr Accruals £80

Year-end adjustments (Continued)

Slide 12.47

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Illustration

• See Supplement to Chapter 12 in the book

Slide 12.48

Pauline Weetman, Financial and Management Accounting, 5th edition © Pearson Education 2011

Current assets

Inventory (stock) 7,500

Cash at bank 6,400

CA 13,900

CL Accruals (80)

Net current assets 13,820

Extract from balance sheet