sl. no. topic detailed explanations - tax, law & audit classes · his liabilities as a...

TRANSCRIPT

Page | 1

© Siddharth Agarwal. All Rights Reserved.

Sl. No. Topic Detailed Explanations 1 Company Audit Section 139 & 143

2 Liabilities Liabilities of Auditors – Expanded

3 Tax Audit Section 44AB, 44AD, Form 3CD

4 GST Audit New Topic added in syllabus.

5 NBFC Audit Audit Report of NBFC Expanded

6 Audit Report SA 700, 701, 705, 706 – only Amended portion.

Page | 2

© Siddharth Agarwal. All Rights Reserved.

Topic Detailed Explanation Rotation of Auditors

Principle Rule as per Companies (Audit and Auditors) Rules, 2014 as amended via Companies (Audit and Auditors) 2nd Amendment Rules, 2017

Rule 5: Class of Companies - For the purposes of sub-section (2) of section 139, the class of companies shall mean the following classes of companies excluding one person companies and small companies: (a) all unlisted public companies having paid up share capital of rupees 10 crore or

more; (b) all private limited companies having paid up share capital of rupees 20 50 crore

or more; (c) all companies having paid up share capital of below threshold limit mentioned

in (a) and (b) above, but having public borrowings from financial institutions, banks or public deposits of rupees 50 crores or more.

.

Auditor’s Report on Internal Financial Controls

Section 143(3)(i) – Exemption Notification from Auditor’s Report on Internal Financial Controls Section 143(3)(i), shall not apply to a private company:- (i) which is a OPC or a small company; or (ii) which has turnover < ` 50 cr. as per latest audited financial statement or which has

aggregate borrowings from banks or financial institutions or anybody corporate at any point of time during the financial year < ` 25 Cr.

A CA acts as an authorized representative of his clients and attends before the Income Tax Authorities or the Appellate Tribunal. His liabilities as a representative under the Income Tax Act are given below –

I Tax Act, 1961 Details

Section 288(4) No Person shall be qualified to represent an assesse u/s 288(1) under following cases:

Auditor's Liabilities under the Income Tax, 1961

Under Section 288 Unders Section 278Under Rule 12A of

the Income Tax RulesUnder Section 271J

Page | 3

© Siddharth Agarwal. All Rights Reserved.

I Tax Act, 1961 Details

(a) who has been dismissed or removed from Government service after the 01.04.1938

For all times in the case of a person referred to in clause(a),

(b) Who has been convicted of an offence connected with any income tax proceeding or on whom a penalty has been imposed under this Act, other than a penalty imposed on him u/s 271(1)(ii) or Section 272A(1)(d)

For such time as the Principal Chief Commissioner or Chief Commission or Principal Commissioner or Commissioner may, by order determine in the case of a person referred to in clause (b),

(c) who has become an insolvent For the period during which the insolvency continues in the case of a person referred to in clause (c),

(d) who has been convicted by a court for an offence involving fraud

And for a period of 10 years from the date of conviction in the case of a person referred to in clause (d).

Section 288(5) In the following cases a CA is prohibited from representing his clients before the Income Tax Authorities: a. he has been convicted of any offence under the Income Tax Law; or b. he has been found guilty of professional misconduct by the ICAI.

Section 278: Where a CA makes or induces any persons to deliver false documents, accounts or statements to the Income Tax Authorities, relating to income chargeable to tax which he knows to be false or does not believe to be true, then the punishment shall be as follows:

If tax, Interest & Penalty evaded > ` 25 Lacs

6 Months ≤ Rigorous Imprisonment ≤ 7 years AND FINE

If tax, Interest & Penalty evaded ≤ ` 25 Lacs

3 Months ≤ Rigorous Imprisonment ≤ 2 years AND Fine

Rule 12A of Income Tax Rules 1962

Under this rule a Chartered Accountant who as an authorised representative has prepared the return filed by the assessee, has to furnish to the Assessing Officer, the particulars of accounts, statements and other documents supplied to him by the assessee for the preparation of the return. Where the Chartered Accountant has conducted an examination of such records, he has also to submit a report on the scope and results of such examination. The report to be submitted will be a statement within the meaning of Section 277 of the Income Tax Act. Thus if this report contains any information which is false and which the Chartered Accountant either knows or believes to be false or untrue, he would be liable to rigorous imprisonment which may extend to seven years and to a fine.

Section 271J As per new section inserted by the Finance Act, 2017 if an accountant or a merchant banker or a registered valuer, furnishes incorrect information in a report or certificate under any provisions of the Act or the rules made thereunder, the Assessing Officer or

Page | 4

© Siddharth Agarwal. All Rights Reserved.

I Tax Act, 1961 Details

the Commissioner (Appeals) may direct him to pay a sum of ` 10,000 for each such report or certificate by way of penalty.

Section 44AB - AUDIT OF ACCOUNTS OF CERTAIN PERSONS CARRYING ON BUSINESS OR PROFESSION.

S. No. Condition Condition in Detail

1 Turnover > ` 100 lacs Every person carrying on business shall, if his total sales turnover or gross

receipts, as the case may be, in business exceeds ` 100 lakhs in any previous year.

Note: Provided that this section is not applicable to the person, who opts for presumptive taxation Scheme under Section 44AD and his total sales or turnover does not exceed ` 2 crores.

2 Gross Receipts from

Profession > ` 50 lacs Every person carrying on profession shall, if his gross receipts, in profession

exceed ` 50 lakhs in any previous year,

3 Assessee not falling under Section 44AE, 44BB, 44BBB

Every person carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section

44AE or section 44BB or section 44BBB as the case may be, and he has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, in any previous year,

4 Assesses not falling under Section 44ADA

Every person carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits and gains of such person under section 44ADA, and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his profession and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year.

5 Assessee not falling under Section 44AD

Every person carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section 44AD, and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his business and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year

Note: 1. Section 44AD 5 years in a row.

Section 44AD (4) of the Income Tax Act, 1961 states that where an eligible assessee declares profit for any Previous Year in accordance with the provisions of this section 44AD and he declares profit for any of the 5 Assessment Years relevant to the Previous Year succeeding such Previous Year not in

Page | 5

© Siddharth Agarwal. All Rights Reserved.

accordance with the provisions of sub-section (1) of section 44AD, he shall not be eligible to claim the benefit of the provisions of this section for 5 Assessment Years subsequent to the Assessment Year relevant to the Previous Year in which the profit has not been declared in accordance with the provisions of sub-section (1) of section 44AD.

2. Higher threshold for non-audit of accounts for assessees opting for presumptive taxation under

section 44AD: Section 44AB makes it obligatory for every person carrying on business to get his accounts of any previous year audited if his total sales, turnover or gross receipts exceed ` 1 crore. However, if an eligible person opts for presumptive taxation scheme as per section 44AD(1), he shall not be required to get his accounts audited if the total turnover or gross receipts of the relevant previous year does not exceed ` 2 crore. The CBDT, has vide its Press Release dated 20th June, 2016, clarified that the higher threshold for non-audit of accounts has been given only to assessees opting for presumptive taxation scheme under section 44AD.

3. Reduction in the existing rate of deemed profit under section 44AD in respect of amounts/receipts

through banking channel/digital means [Press Release, dated 19-12-2016] Under the existing provisions of section 44AD of the Income-tax Act, 1961, in case of certain assessees (i.e. an individual, HUF or a partnership firm other than LLP) carrying on any business (other than transportation, agency, brokerage and commission) and having a turnover of Rs.2 crore or less, the profit is deemed to be 8% of the total turnover. In order to achieve the Government’s mission of moving towards a less cash economy and to incentivise small traders / businesses to proactively accept payments by digital means, with effect from A.Y. 2017-18 the existing rate of deemed profit of 8% under section 44AD of the Act has been reduced to 6% in respect of the amount of total turnover or gross receipts received through banking channel/digital means i.e., by an A/c payee cheque/bank draft or use of ECS through a bank A/c during the previous year or before the due specified in section 139(1) in respect of that previous year.

Clause 31 (a) Particulars of each loan or deposit in an amount exceeding the limit specified in section 269SS taken

or accepted during the previous year: (i) name, address and permanent account number (if available with the assessee) of the lender or

depositor; (ii) amount of loan or deposit taken or accepted; (iii) whether the loan or deposit was squared up during the previous year; (iv) maximum amount outstanding in the account at any time during the previous year; (v) whether the loan or deposit was taken or accepted by cheque or bank draft or use of electronic

clearing system through a bank account; (vi) in case the loan or deposit was taken or accepted by cheque or bank draft, whether the same

was taken or accepted by an account payee cheque or an account payee bank draft.

*(These particulars needs not be given in the case of a Government company, a banking company or a corporation established by a Central, State or Provincial Act.)

Page | 6

© Siddharth Agarwal. All Rights Reserved.

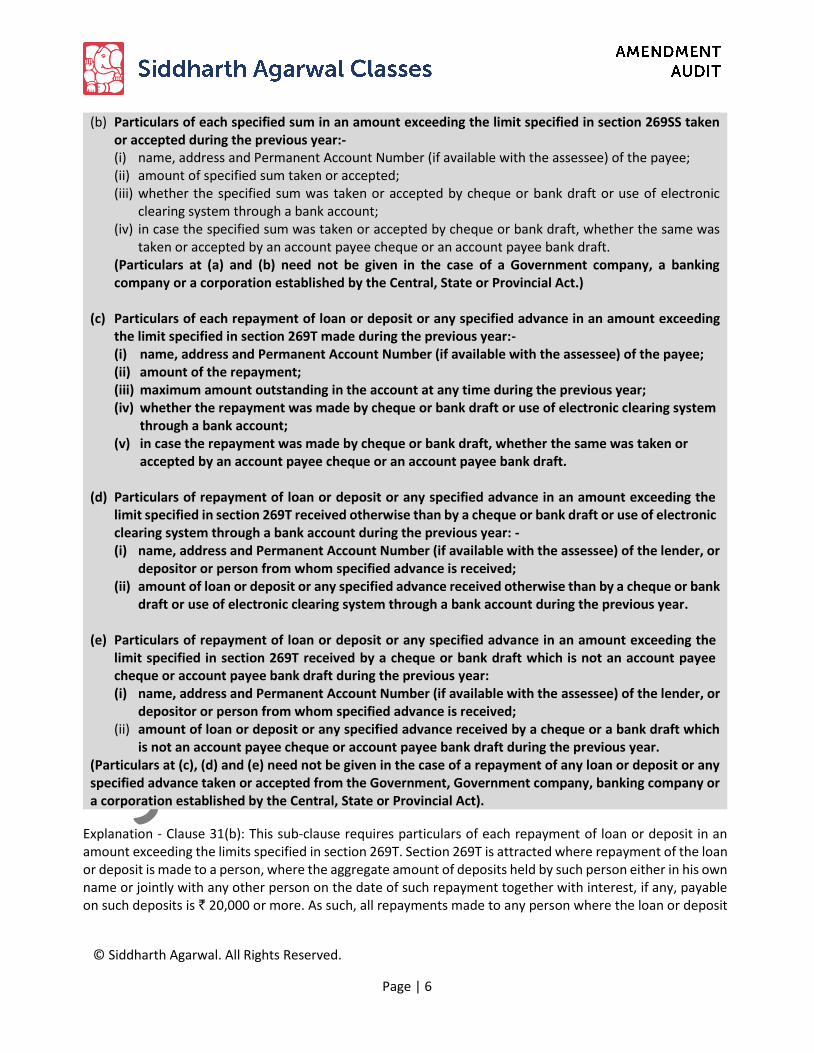

(b) Particulars of each specified sum in an amount exceeding the limit specified in section 269SS taken or accepted during the previous year:- (i) name, address and Permanent Account Number (if available with the assessee) of the payee; (ii) amount of specified sum taken or accepted; (iii) whether the specified sum was taken or accepted by cheque or bank draft or use of electronic

clearing system through a bank account; (iv) in case the specified sum was taken or accepted by cheque or bank draft, whether the same was

taken or accepted by an account payee cheque or an account payee bank draft. (Particulars at (a) and (b) need not be given in the case of a Government company, a banking company or a corporation established by the Central, State or Provincial Act.)

(c) Particulars of each repayment of loan or deposit or any specified advance in an amount exceeding

the limit specified in section 269T made during the previous year:- (i) name, address and Permanent Account Number (if available with the assessee) of the payee; (ii) amount of the repayment; (iii) maximum amount outstanding in the account at any time during the previous year; (iv) whether the repayment was made by cheque or bank draft or use of electronic clearing system

through a bank account; (v) in case the repayment was made by cheque or bank draft, whether the same was taken or

accepted by an account payee cheque or an account payee bank draft. (d) Particulars of repayment of loan or deposit or any specified advance in an amount exceeding the

limit specified in section 269T received otherwise than by a cheque or bank draft or use of electronic clearing system through a bank account during the previous year: - (i) name, address and Permanent Account Number (if available with the assessee) of the lender, or

depositor or person from whom specified advance is received; (ii) amount of loan or deposit or any specified advance received otherwise than by a cheque or bank

draft or use of electronic clearing system through a bank account during the previous year. (e) Particulars of repayment of loan or deposit or any specified advance in an amount exceeding the

limit specified in section 269T received by a cheque or bank draft which is not an account payee cheque or account payee bank draft during the previous year: (i) name, address and Permanent Account Number (if available with the assessee) of the lender, or

depositor or person from whom specified advance is received; (ii) amount of loan or deposit or any specified advance received by a cheque or a bank draft which

is not an account payee cheque or account payee bank draft during the previous year. (Particulars at (c), (d) and (e) need not be given in the case of a repayment of any loan or deposit or any specified advance taken or accepted from the Government, Government company, banking company or a corporation established by the Central, State or Provincial Act).

Explanation - Clause 31(b): This sub-clause requires particulars of each repayment of loan or deposit in an amount exceeding the limits specified in section 269T. Section 269T is attracted where repayment of the loan or deposit is made to a person, where the aggregate amount of deposits held by such person either in his own name or jointly with any other person on the date of such repayment together with interest, if any, payable on such deposits is ` 20,000 or more. As such, all repayments made to any person where the loan or deposit

Page | 7

© Siddharth Agarwal. All Rights Reserved.

along with interest is ` 20,000 or more are to be reported under this sub-clause, even though the amount of repayment may be less than ` 20,000. The tax auditor should verify such repayments and report accordingly.

Definition of “Audit” has been as per section 2(13) of the CGST Act, 2017 is given below:

“audit” means the examination of records, returns and other documents maintained or furnished by the registered person under this Act or the rules made thereunder or under any other law for the time being in force to verify the correctness of turnover declared, taxes paid, refund claimed and input tax credit availed, and to assess his compliance with the provisions of this Act or the rules made thereunder.”

GST envisages three types of Audit. 1. Audit of accounts [Section 35(5) read alongwith section 44(2) and rule 80] 2. Audit by Tax Authorities wherein the Commissioner or any officer authorised by him, can undertake audit

of any registered person for such period, at such frequency and in such manner as may be prescribed. [Section 65 and rule 101]

3. Special Audit wherein the registered person can be directed to get his records including books of account examined and audited by a chartered accountant or a cost accountant during any stage of scrutiny, inquiry, investigation or any other proceedings; depending upon the complexity of the case. [Section 66 and rule 102]

Topic Detailed Explanation Audit of Accounts [Section 35(5) read alongwith section 44(2) and rule 80]

As per sub-section 5 of section 35 read alongwith section 44(2) and rule 80 of the CGST Rules, 2017 stipulates as follows:

Every registered person must get his accounts audited by a Chartered Accountant or a Cost Accountant if his aggregate turnover during a FY exceeds ` 2 crores.

Such registered person is required to furnish electronically through the common portal along with Annual Return a copy of: 1. Audited annual accounts A Reconciliation Statement, duly certified, in prescribed FORM GSTR-9C.

GST AUDIT

Audit by GST Tax Authorities

General Audit

Special Audit

Audit by Professionals

To File Returns+Audited Accounts + Reconcilation

Statements

Page | 8

© Siddharth Agarwal. All Rights Reserved.

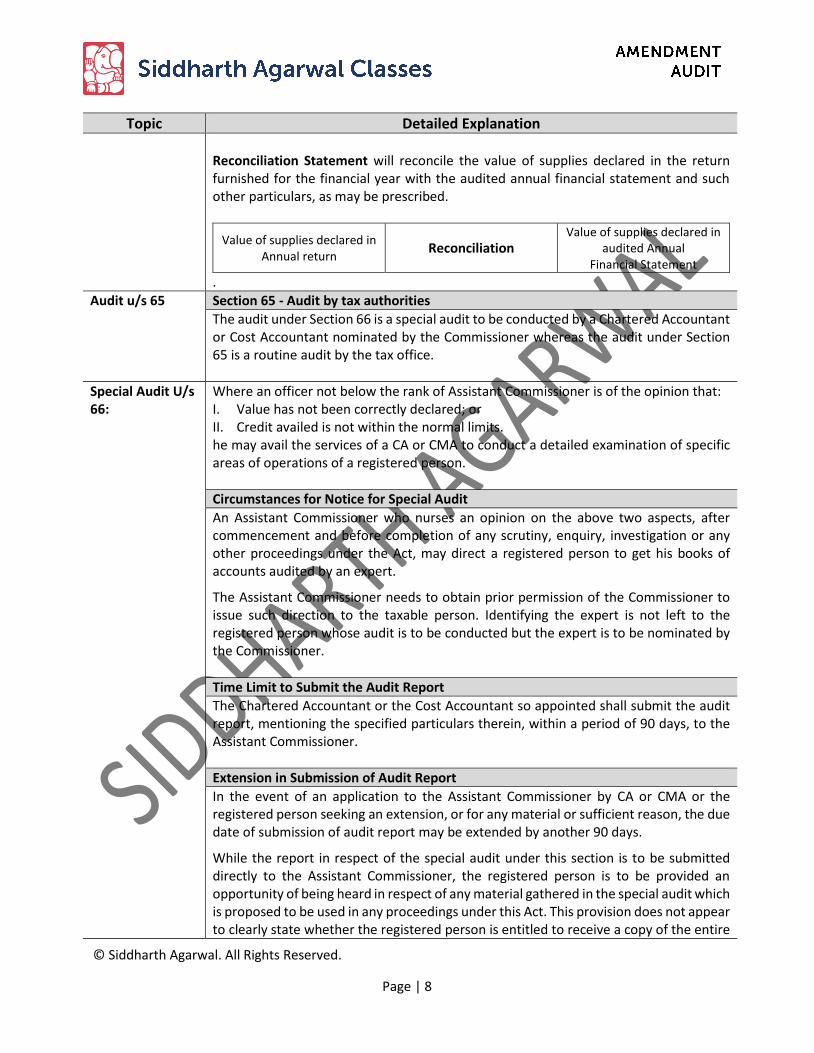

Topic Detailed Explanation Reconciliation Statement will reconcile the value of supplies declared in the return furnished for the financial year with the audited annual financial statement and such other particulars, as may be prescribed.

Value of supplies declared in Annual return

Reconciliation Value of supplies declared in

audited Annual Financial Statement

.

Audit u/s 65 Section 65 - Audit by tax authorities

The audit under Section 66 is a special audit to be conducted by a Chartered Accountant or Cost Accountant nominated by the Commissioner whereas the audit under Section 65 is a routine audit by the tax office.

Special Audit U/s 66:

Where an officer not below the rank of Assistant Commissioner is of the opinion that: I. Value has not been correctly declared; or II. Credit availed is not within the normal limits. he may avail the services of a CA or CMA to conduct a detailed examination of specific areas of operations of a registered person.

Circumstances for Notice for Special Audit

An Assistant Commissioner who nurses an opinion on the above two aspects, after commencement and before completion of any scrutiny, enquiry, investigation or any other proceedings under the Act, may direct a registered person to get his books of accounts audited by an expert.

The Assistant Commissioner needs to obtain prior permission of the Commissioner to issue such direction to the taxable person. Identifying the expert is not left to the registered person whose audit is to be conducted but the expert is to be nominated by the Commissioner.

Time Limit to Submit the Audit Report

The Chartered Accountant or the Cost Accountant so appointed shall submit the audit report, mentioning the specified particulars therein, within a period of 90 days, to the Assistant Commissioner.

Extension in Submission of Audit Report

In the event of an application to the Assistant Commissioner by CA or CMA or the registered person seeking an extension, or for any material or sufficient reason, the due date of submission of audit report may be extended by another 90 days.

While the report in respect of the special audit under this section is to be submitted directly to the Assistant Commissioner, the registered person is to be provided an opportunity of being heard in respect of any material gathered in the special audit which is proposed to be used in any proceedings under this Act. This provision does not appear to clearly state whether the registered person is entitled to receive a copy of the entire

Page | 9

© Siddharth Agarwal. All Rights Reserved.

Topic Detailed Explanation audit report or only extracts or merely inferences from the audit. However, the observance of the principles of natural justice in the proceedings arising from this audit would not fail the taxable person on this aspect.

Expenses for Examination and Remuneration for Audit

The expenses for examination and audit including the remuneration payable to the auditor will be determined and borne by the Commissioner.

As in the case of audit under section 65, no demand of tax, even ad interim, is permitted on completion of the special audit under this section. In case any possible tax liability is identified during the audit, procedure under section 73 or 74 as the case may be is to be followed.

While conducting the audit, the auditor is authorized to: 1. Verify books & records 2. Returns & statements 3. Correctness of turnover, exemptions & deductions 4. Rate of tax applicable in respect of supply of goods and/or services 5. The input tax credit claimed/availed/unutilized and refund claimed.

Some of the best practices to be adopted for GST audit among others could be: The evaluation of the internal control viz-a-viz GST would indicate the area to be focused. This could be done by verifying: 1. The Statutory Audit report which has specific disclosure needs in regard to maintenance of record, stock

and fixed assets. 2. The Information System Audit Report and the Internal Audit Report. 3. Internal Control Questionnaire designed for GST compliance.

(a) The use of generalised audit software to aid the GST audit would ensure modern practice of risk based audit are adopted.

(b) The reconciliation of the books of account or reports from the ERP’s to the return is imperative. (c) The review of the gross trial balance for detecting any incomes being set off with expenses. (d) Review of purchases/expenses to examine applicability of Reverse Charge applicable to

goods/services. The foreign exchange outgo reconciliation would also be necessary for identifying the liability of import of services.

(e) Quantitative reconciliation of stock transfer within the State or for supplies to Job Workers under exemption.

(f) Ratio analysis could provide vital clues on areas of non-compliance.

Form GST ADT - 04 [See Rule 102(2)]

Reference No.: Date:

Page | 10

© Siddharth Agarwal. All Rights Reserved.

To, -------------------------------------------- GSTIN ……………………………… Name ……………………………… Address ………………………….. Information of Findings upon Special Audit Your books of account and records for the F.Y………………..…. has been examined by ………….………….. (chartered accountant/cost accountant) and this Audit Report is prepared on the basis of information available/documents furnished by you and the findings /discrepancies are as under :

Short payment of Integrated Tax Central Tax State/UT Tax Cess

Tax

Interest

Any other Amount

[Upload pdf file containing audit observation] You are directed to discharge your statutory liabilities in this regard as per the provisions of the Act and the rules made thereunder, failing which proceedings as deemed fit may be initiated against you under the provisions of the Act.

Signature ..................................... Name ……………………………………….. Designation ……………………….........

Meaning of Aggregate Turnover as defined u/s 2(6) of the CGST Act:

Includes Values of All Outward Supplies

Taxable Supplies

Exempt Supplies

Exports

Inter-State supplies of persons having the same PAN be computed on all India basis

Excludes the following:

CGST

SGST

UTGST

IGST

Compensation Cess

Value of inward supplies on which tax is payable under Reverse Charge basis.

Page | 11

© Siddharth Agarwal. All Rights Reserved.

Topic Detailed Explanation Material to be included in the Auditor’s report to the Board of Directors

The auditor’s report on the accounts of a non-banking financial company shall include a statement on the following matters, namely- (A) In the case of ALL non-banking financial companies:

1. Whether the company has obtained a Certificate of Registration (COR) from the Bank.

2. In case of a company holding COR issued by the RBI, whether that company is entitled to continue to hold such COR in terms of its Principal Business Criteria (Financial asset/income pattern) as on March 31 of the applicable year.

3. Whether the NBFC is meeting the required net owned fund requirement as laid down by RBI.

(B) In the case of a non-banking financial companies accepting/holding public

deposits: 1. Whether the public deposits accepted by the company are within the limits

admissible to the company as per the provisions of the Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 2016;

2. Whether the public deposits held by the company in excess of the quantum of such deposits permissible to it are regularised in the manner provided in the said Directions;

3. Whether the non-banking financial company is accepting "public deposit” without minimum investment grade credit rating from an approved credit rating agency;

4. Whether the capital adequacy ratio as disclosed in the return has been correctly determined and whether such ratio is in compliance with the minimum CRAR prescribed therein;

5. Whether the company has violated any restriction on acceptance of public deposit as provided in Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 2016;

6. Whether the company has defaulted in paying to its depositors the interest and/or principal amount of the deposits after such interest and/or principal became due;

7. Whether the company has complied with the prudential norms on income recognition, accounting standards, asset classification, provisioning for bad and doubtful debts, and concentration of credit/investments as specified in the Directions issued by the RBI;

8. Whether the company has complied with the liquid assets requirement as prescribed by the Bank in exercise of powers under section 45-IB of the RBI Act and whether the details of the designated bank in which the approved securities are held is communicated to the office concerned of the Bank in terms of NBS 3;

9. Whether the company has furnished to the RBI within the stipulated period the return on deposits as specified in the NBS 1;

10. Whether the company has furnished to the RBI within the stipulated period the quarterly return on prudential norms as specified in the Non-Banking Financial Company Returns (Reserve Bank) Directions, 2016;

Page | 12

© Siddharth Agarwal. All Rights Reserved.

Topic Detailed Explanation 11. Whether, in the case of opening of new branches or offices to collect deposits or

in the case of closure of existing branches/offices or in the case of appointment of agent, the company has complied with the requirements contained in the Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 2016.

(C) In the case of a non-banking financial company not accepting public deposits: Apart from the aspects enumerated in (A) above, the auditor shall include a statement on the following matters, namely: - 1. Whether the Board of Directors has passed a resolution for non-acceptance of

any public deposits; 2. Whether the company has accepted any public deposits during the relevant

period/year; 3. Whether the company has complied with the prudential norms relating to income

recognition, accounting standards, asset classification and provisioning for bad and doubtful debts;

4. Whether the capital adequacy ratio as disclosed in the return submitted to the Bank in form NBS-7, has been correctly arrived at and whether such ratio is in compliance with the minimum CRAR prescribed by the Bank;

5. whether the non-banking financial company has been correctly classified as NBFC Micro Finance Institutions (MFI) as defined in the Non-Banking Financial Company – Non-Systemically Important Non-Deposit taking Company (Reserve Bank) Directions, 2016.

(D) In the case of a company engaged in the business of non-banking financial institution not required to hold CoR subject to certain conditions: Apart from the matters enumerated in (A)(I) above where a company has obtained a specific advice from the RBI that it is not required to hold CoR from the Bank, the auditor shall include a statement that the company is complying with the conditions stipulated as advised by the RBI.

Reasons to be stated for unfavourable statements

Where, in the auditor’s report, the statement regarding any of the items referred above is unfavourable or qualified, the auditor’s report shall also state the reasons for such unfavourable or qualified statement, as the case may be. Where the auditor is unable to express any opinion on any of the items referred above, his report shall indicate such fact together with reasons therefor.

Page | 13

© Siddharth Agarwal. All Rights Reserved.

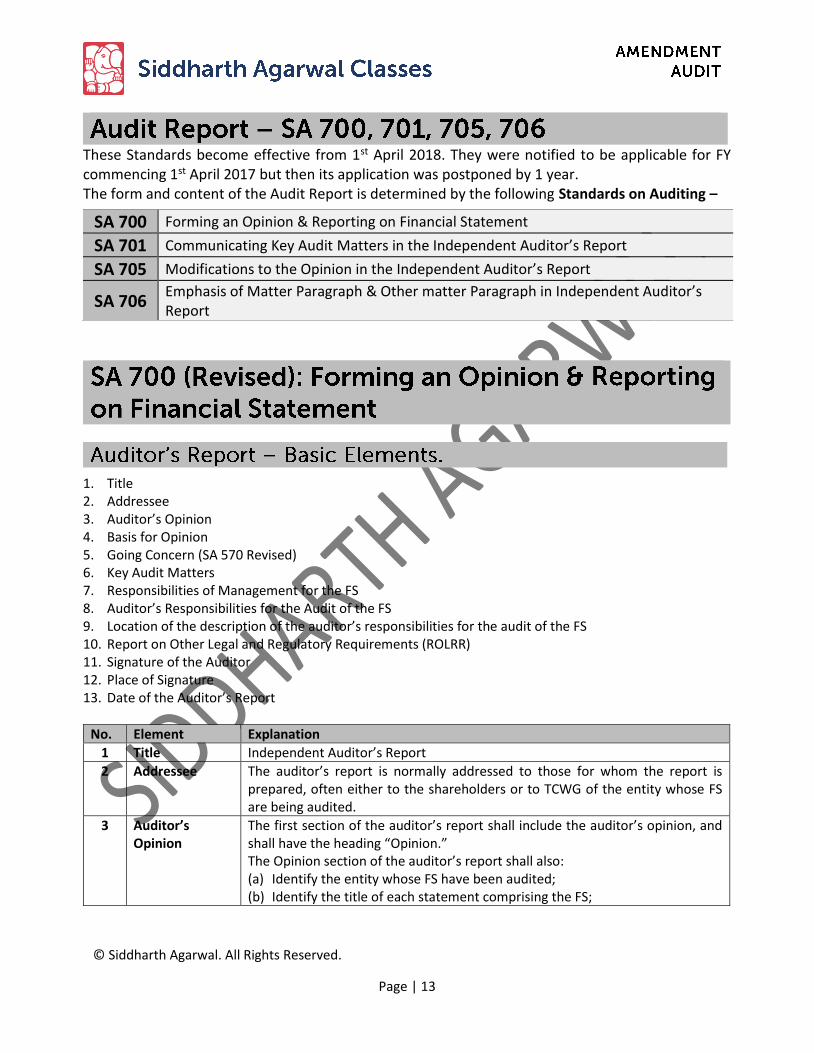

These Standards become effective from 1st April 2018. They were notified to be applicable for FY commencing 1st April 2017 but then its application was postponed by 1 year. The form and content of the Audit Report is determined by the following Standards on Auditing –

SA 700 Forming an Opinion & Reporting on Financial Statement

SA 701 Communicating Key Audit Matters in the Independent Auditor’s Report

SA 705 Modifications to the Opinion in the Independent Auditor’s Report

SA 706 Emphasis of Matter Paragraph & Other matter Paragraph in Independent Auditor’s Report

1. Title 2. Addressee 3. Auditor’s Opinion 4. Basis for Opinion 5. Going Concern (SA 570 Revised) 6. Key Audit Matters 7. Responsibilities of Management for the FS 8. Auditor’s Responsibilities for the Audit of the FS 9. Location of the description of the auditor’s responsibilities for the audit of the FS 10. Report on Other Legal and Regulatory Requirements (ROLRR) 11. Signature of the Auditor 12. Place of Signature 13. Date of the Auditor’s Report

No. Element Explanation

1 Title Independent Auditor’s Report

2 Addressee The auditor’s report is normally addressed to those for whom the report is prepared, often either to the shareholders or to TCWG of the entity whose FS are being audited.

3 Auditor’s Opinion

The first section of the auditor’s report shall include the auditor’s opinion, and shall have the heading “Opinion.” The Opinion section of the auditor’s report shall also: (a) Identify the entity whose FS have been audited; (b) Identify the title of each statement comprising the FS;

Page | 14

© Siddharth Agarwal. All Rights Reserved.

No. Element Explanation

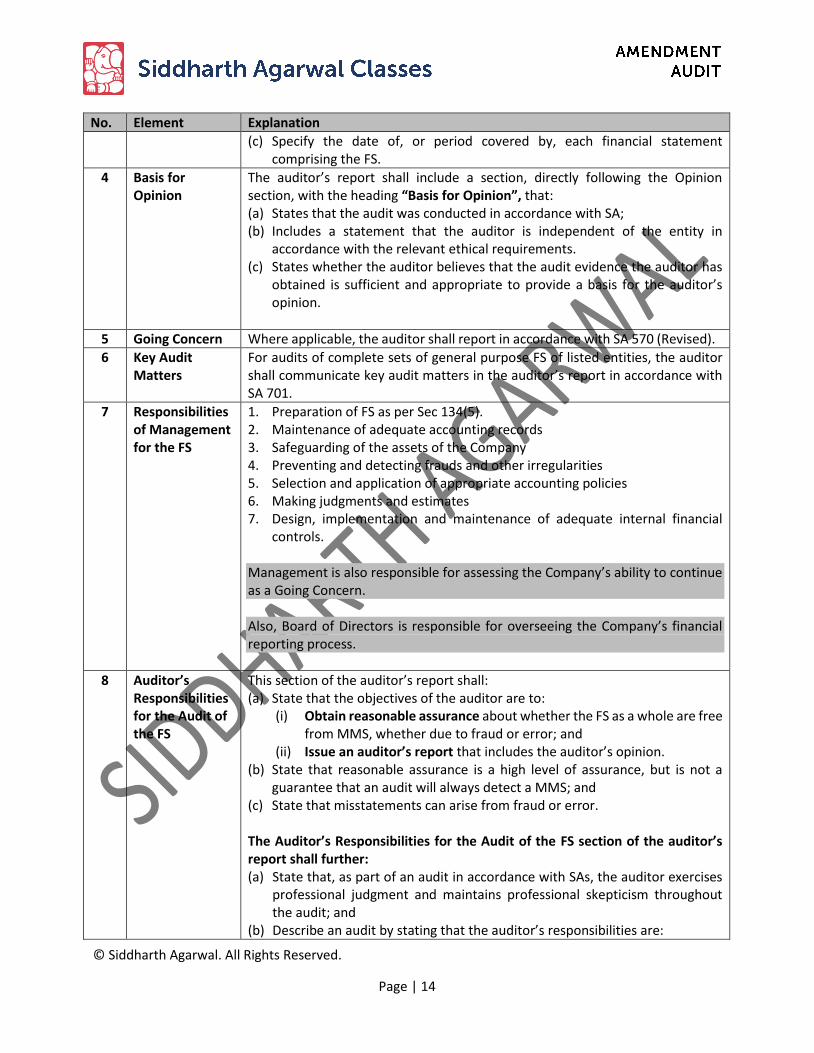

(c) Specify the date of, or period covered by, each financial statement comprising the FS.

4 Basis for Opinion

The auditor’s report shall include a section, directly following the Opinion section, with the heading “Basis for Opinion”, that: (a) States that the audit was conducted in accordance with SA; (b) Includes a statement that the auditor is independent of the entity in

accordance with the relevant ethical requirements. (c) States whether the auditor believes that the audit evidence the auditor has

obtained is sufficient and appropriate to provide a basis for the auditor’s opinion.

5 Going Concern Where applicable, the auditor shall report in accordance with SA 570 (Revised).

6 Key Audit Matters

For audits of complete sets of general purpose FS of listed entities, the auditor shall communicate key audit matters in the auditor’s report in accordance with SA 701.

7 Responsibilities of Management for the FS

1. Preparation of FS as per Sec 134(5). 2. Maintenance of adequate accounting records 3. Safeguarding of the assets of the Company 4. Preventing and detecting frauds and other irregularities 5. Selection and application of appropriate accounting policies 6. Making judgments and estimates 7. Design, implementation and maintenance of adequate internal financial

controls. Management is also responsible for assessing the Company’s ability to continue as a Going Concern. Also, Board of Directors is responsible for overseeing the Company’s financial reporting process.

8 Auditor’s Responsibilities for the Audit of the FS

This section of the auditor’s report shall: (a) State that the objectives of the auditor are to:

(i) Obtain reasonable assurance about whether the FS as a whole are free from MMS, whether due to fraud or error; and

(ii) Issue an auditor’s report that includes the auditor’s opinion. (b) State that reasonable assurance is a high level of assurance, but is not a

guarantee that an audit will always detect a MMS; and (c) State that misstatements can arise from fraud or error. The Auditor’s Responsibilities for the Audit of the FS section of the auditor’s report shall further: (a) State that, as part of an audit in accordance with SAs, the auditor exercises

professional judgment and maintains professional skepticism throughout the audit; and

(b) Describe an audit by stating that the auditor’s responsibilities are:

Page | 15

© Siddharth Agarwal. All Rights Reserved.

No. Element Explanation

(i) To identify and assess the risks of MMS of the FS, whether due to fraud or error; to design and perform audit procedures responsive to those risks; and to obtain audit evidence that is sufficient and appropriate to provide a basis for the auditor’s opinion. The risk of not detecting a MMS resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

1. To identify and assess the risks of MMS of the FS. 2. To design and perform audit procedures in response to those

risks. 3. To obtain sufficient and appropriate audit evidence.

(ii) To obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances.

(iii) To evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

(iv) To conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern.

Communication with TCWG (a) State that the auditor communicates with TCWG regarding the planned

scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control;

(b) For audits of FS of listed entities, state that the auditor provides TCWG with a statement that the auditor has complied with relevant ethical requirements regarding independence; and

(c) For audits of FS of listed entities and any other entities for which KEY AUDIT MATTERS are communicated in accordance with SA 701, state that, from the matters communicated with TCWG, the auditor determines those matters that were of most significance in the audit of the FS of the current period and are therefore the key audit matters.

9 Location of the description of the auditor’s responsibilities for the audit of the FS

The description of the auditor’s responsibilities for the audit of the FS required by paragraphs 38–39 shall be included. (i) Within the body of the auditor’s report; (ii) Within an appendix to the auditor’s report, in which case the auditor’s

report shall include a reference to the location of the appendix; or (iii) By a specific reference within the auditor’s report to the location of such a

description on a website of an appropriate authority.

Page | 16

© Siddharth Agarwal. All Rights Reserved.

No. Element Explanation

10 ROLRR This Contains Auditors Comments on the matters u/s 143(3) and reference to Annexure on CARO and Annexure on Internal Financial Controls.

11 Signature Signature. Membership Number, Firm Registration number, Firm Name, Partner name.

12 Place City where it is signed.

13 Date Date upto which Auditor has considered subsequent events.

When expressing an unmodified opinion (UO) on FS, the auditor’s opinion shall use one of the following phrases, which are regarded as being equivalent: (a) In our opinion, the accompanying FS are present fairly, in all material respects, in accordance with the

applicable FRF; or (b) In our opinion, the accompanying FS give a true and fair view of in accordance with the applicable FRF.

Definition of Key audit matters— Those matters that, in the auditor’s professional judgment, were of most significance in the audit of the FS of the current period. Key audit matters are selected from matters communicated with TCWG.

The purpose of communicating key audit matters is to enhance the communicative value of the auditor’s report by providing greater transparency about the audit that was performed. Communicating key audit matters provides additional information to intended users of the FS (“intended users”) to assist them in understanding those matters that, in the auditor’s professional judgment, were of most significance in the audit of the FS of the current period. Communicating key audit matters may also assist intended users in understanding the entity and areas of significant management judgment in the audited FS.

Two types of Opinion Language

Presented fairly, in all material aspects.

True and Fair View

Page | 17

© Siddharth Agarwal. All Rights Reserved.

This SA applies to audits of complete sets of general purpose FS of LISTED ENTITIES and circumstances when the auditor otherwise decides to communicate key audit matters in the auditor’s report. This SA also applies when the auditor is required by law or regulation to communicate key audit matters in the auditor’s report. However, SA 705 (Revised) prohibits the auditor from communicating key audit matters when the auditor disclaims an opinion on the FS,

The objectives of the auditor are to determine key audit matters and, having formed an opinion on the FS, communicate those matters by describing them in the auditor’s report.

The auditor shall determine, from the matters communicated with TCWG, those matters that required significant auditor attention in performing the audit. In making this determination, the auditor shall take into account the following: (a) Areas of higher assessed risk of MMS, or significant risks identified in accordance with SA 315. (b) Significant auditor judgments relating to areas in the FS that involved significant management judgment,

including accounting estimates that have been identified as having high estimation uncertainty. (c) The effect on the audit of significant events or transactions that occurred during the period.

The auditor shall determine which of the matters determined in accordance with paragraph 9 were of most significance in the audit of the FS of the current period and therefore are the key audit matters.

The auditor shall describe each key audit matter, using an appropriate subheading, in a separate section of the auditor’s report under the heading “Key Audit Matters,” unless the circumstances in paragraphs 14 or 15 apply. The introductory language in this section of the auditor’s report shall state that: (a) Key audit matters are those matters that, in the auditor’s professional judgment, were of most

significance in the audit of the FS [of the current period]; and (b) These matters were addressed in the context of the audit of the FS as a whole, and in forming the

auditor’s opinion thereon, and the auditor does not provide a separate opinion on these matters.

The auditor shall not communicate a matter in the Key Audit Matters section of the auditor’s report when the auditor would be required to modify the opinion in accordance with SA 705 (Revised) as a result of the matter.

Communicating key audit matters in the auditor’s report is in the context of the auditor having formed an opinion on the FS as a whole. Communicating key audit matters in the auditor’s report is not: (a) A substitute for disclosures in the FS that the applicable FRF requires management to make, or that are

otherwise necessary to achieve fair presentation;

Page | 18

© Siddharth Agarwal. All Rights Reserved.

(b) A substitute for the auditor expressing a modified opinion when required by the circumstances of a specific audit engagement in accordance with SA 705 (Revised);

(c) A substitute for reporting in accordance with SA 570 (Revised) when a material uncertainty exists relating to events or conditions that may cast significant doubt on an entity’s ability to continue as a going concern; or

(d) A separate opinion on individual matters.

Placement of Basis for Modified Opinion paragraph As shown in SA 700 above.

Placement of an EMP paragraph. 1. When the EMP relates to the applicable FRF, the auditor may consider it necessary to place the paragraph

immediately following the Basis of Opinion section to provide appropriate context to the auditor’s opinion.

2. When a Key Audit Matters (KAM) section is presented in the auditor’s report, an EMP may be presented either directly before or after the KAM section, based on the auditor’s judgment as to the relative significance of the information included in the Emphasis of Matter paragraph.

Placement of an OMP paragraph. 1. Other Matter paragraph should be placed after the “Auditor’s Responsibility” Section in the Auditor’s

Report. 2. When an OMP is included to draw users’ attention to a matter relating to Other Reporting

Responsibilities addressed in the auditor’s report, the paragraph may be included in the Report on Other Legal and Regulatory Requirements section.