skf half-year results 2014 tom johnstone, president and ceo 15 july 2014

TRANSCRIPT

SKF Half-year results 2014Tom Johnstone, President and CEO

15 July 2014

© SKF Group 15 July 2014

Examples of new business

• Envision Energy, China Strategic long-term partnership

• A customer in the automation industry Roller screw electromechanical cylinder

• Dongfang Electric New Energy Equipment Main shaft bearings

• Aurizon, Australia Service contract

• A customer in the oil and gas industry Asset management services

• Bosch Service, Brazil SKF’s vehicle aftermarket product range

Slide 2

© SKF Group 15 July 2014

Highlights

• Inauguration of SKF Campus and SKF North East Asia Distribution Centre in Shanghai.

• New SKF Solution Factory in Nieuwegein in the Netherlands.

• Events during the quarter:- SKF Wind Farm Management Conference in Berlin

- SKF Life Cycle Management Conference in Buenos Aires- SKF Asset Management Conference in Prague

Slide 3

© SKF Group 15 July 2014

Customer awards

Slide 4

• Best Technical and Service Award 2013 – Envision Energy, China

• Supplier Excellence Award 2013 – National Oilwell Varco (NOV), USA

• Premium Supplier Award – Joy Global Underground Mining LLC, USA

• Marine Supplier of the year Award 2014 – Rolls-Royce Marine

• Excellent Supplier Award – ABB Marine, China

• Supplier Certification of Appreciation – Nissan, China

• Quality Gold Award 2013 – Yamaha Motor Company

• The Qualitas Award – Fiat/Chrysler, Argentina

© SKF Group 15 July 2014

New products and solutions

Slide 5

SKF Wireless MicroVibe

SKF Wireless Machine Condition Sensor

SKF @ptitude Connect

SKF Shaft Alignment Tool

Low friction grease for hub bearing units

SKF Gear Bearing Unit

Floating piston

Electric grease transfer pump

SKF Tachometer

Low torque operator valve solution

Turbulo BlueMon emission monitoring system

© SKF Group 15 July 2014

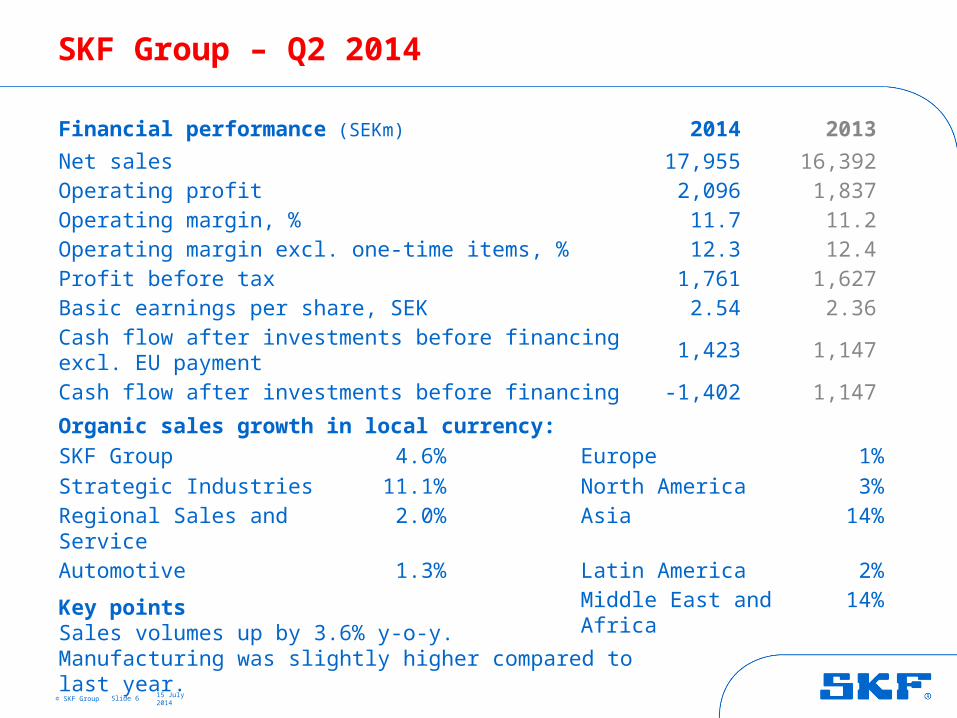

SKF Group – Q2 2014

Slide 6

Financial performance (SEKm) 2014 2013

Net sales 17,955 16,392Operating profit 2,096 1,837Operating margin, % 11.7 11.2Operating margin excl. one-time items, % 12.3 12.4Profit before tax 1,761 1,627Basic earnings per share, SEK 2.54 2.36Cash flow after investments before financing excl. EU payment 1,423 1,147Cash flow after investments before financing -1,402 1,147

Organic sales growth in local currency:

SKF Group 4.6% Europe 1%

Strategic Industries 11.1% North America 3%Regional Sales and Service 2.0% Asia 14%

Automotive 1.3% Latin America 2%Middle East and Africa 14%

Key pointsSales volumes up by 3.6% y-o-y.Manufacturing was slightly higher compared to last year.

© SKF Group 15 July 2014

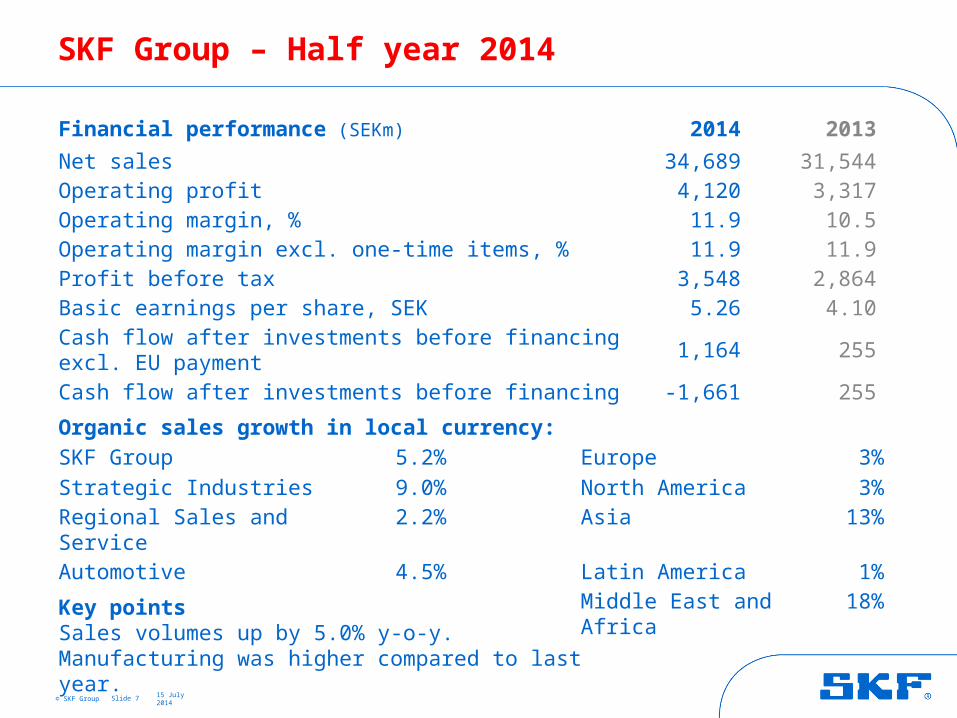

SKF Group – Half year 2014

Slide 7

Financial performance (SEKm) 2014 2013

Net sales 34,689 31,544Operating profit 4,120 3,317Operating margin, % 11.9 10.5Operating margin excl. one-time items, % 11.9 11.9Profit before tax 3,548 2,864Basic earnings per share, SEK 5.26 4.10Cash flow after investments before financing excl. EU payment 1,164 255Cash flow after investments before financing -1,661 255

Organic sales growth in local currency:

SKF Group 5.2% Europe 3%

Strategic Industries 9.0% North America 3%Regional Sales and Service 2.2% Asia 13%

Automotive 4.5% Latin America 1%Middle East and Africa 18%

Key pointsSales volumes up by 5.0% y-o-y.Manufacturing was higher compared to last year.

© SKF Group 15 July 2014

Organic sales growth in local currency

Slide 8

% changey-o-y

2012 2013 2014

© SKF Group 15 July 2014

Organic sales growth in local currency

Slide 9

% y-o-y

Structure in 2012: 0.4%Structure in 2013: 2.5%Structure in 2014: 4.2%

-2.5%

-0.7%

5.2%

© SKF Group 15 July 2014

Sales development by geographyOrganic growth in local currency Q2 2014 vs Q2 2013

Slide 10

Europe1%

Asia/Pacific14%

Middle East& Africa

14%

LatinAmerica

2%

NorthAmerica

3%

© SKF Group 15 July 2014

Sales development by geographyOrganic growth in local currency YTD 2014 vs YTD 2013

Slide 11

Europe3%

Asia/Pacific13%

Middle East& Africa

18%

LatinAmerica

1%

NorthAmerica

3%

© SKF Group 15 July 2014

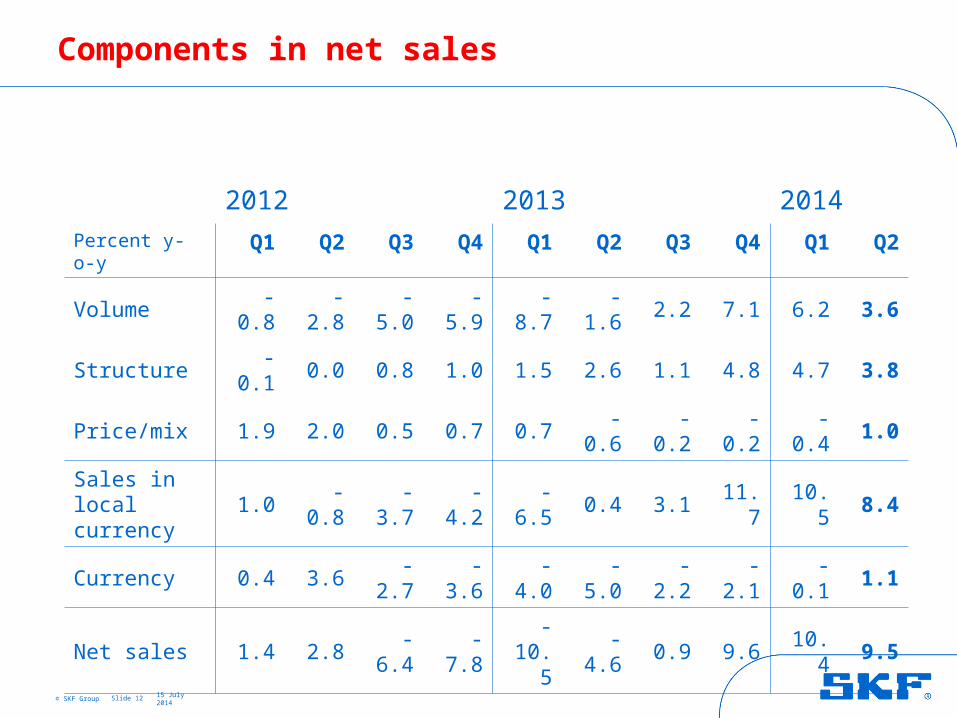

Components in net sales

Slide 12

2012 2013 2014

Percent y-o-y Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Volume -0.8 -2.8 -5.0 -5.9 -8.7 -1.6 2.2 7.1 6.2 3.6

Structure -0.1 0.0 0.8 1.0 1.5 2.6 1.1 4.8 4.7 3.8

Price/mix 1.9 2.0 0.5 0.7 0.7 -0.6 -0.2 -0.2 -0.4 1.0

Sales in local currency

1.0 -0.8 -3.7 -4.2 -6.5 0.4 3.1 11.7 10.5 8.4

Currency 0.4 3.6 -2.7 -3.6 -4.0 -5.0 -2.2 -2.1 -0.1 1.1

Net sales 1.4 2.8 -6.4 -7.8 -10.5 -4.6 0.9 9.6 10.4 9.5

© SKF Group 15 July 2014

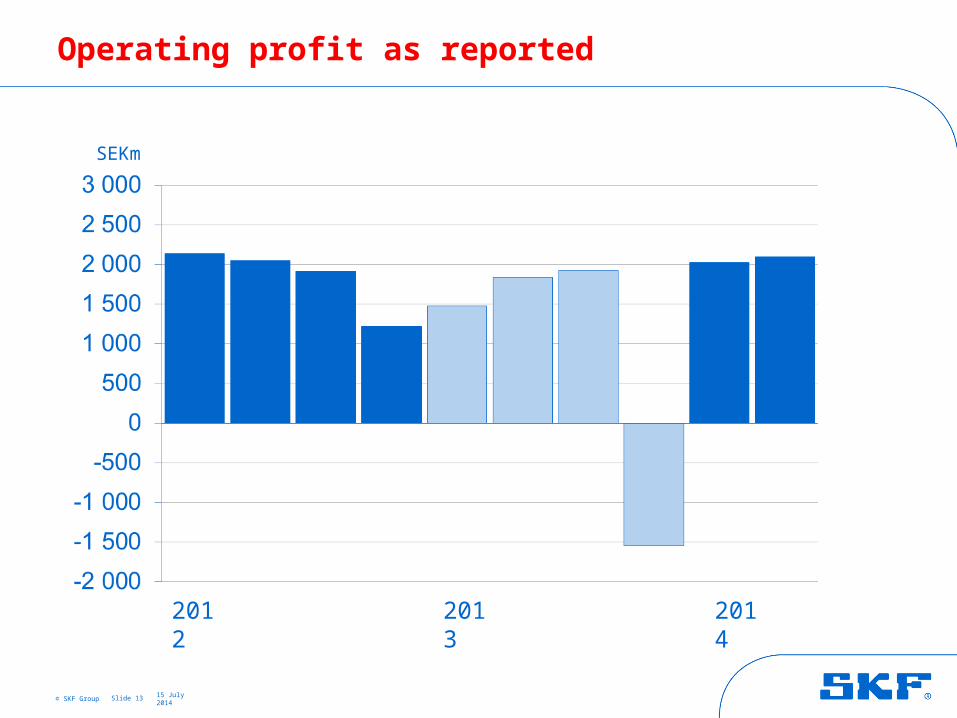

Operating profit as reported

Slide 13

SEKm

2012 2013 2014

© SKF Group 15 July 2014

Operating profit excluding one-time items

Slide 14

SEKm

2012 2013 2014

© SKF Group 15 July 2014

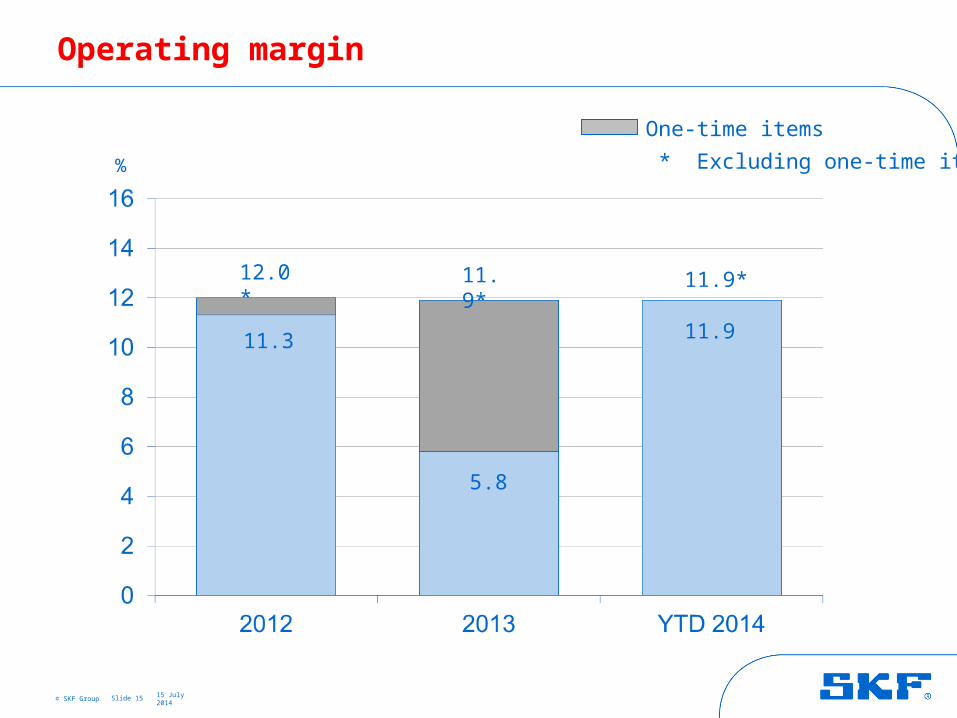

Operating margin

Slide 15

%

5.8

11.3

12.0* 11.9*

One-time items

* Excluding one-time items

11.9*

11.9

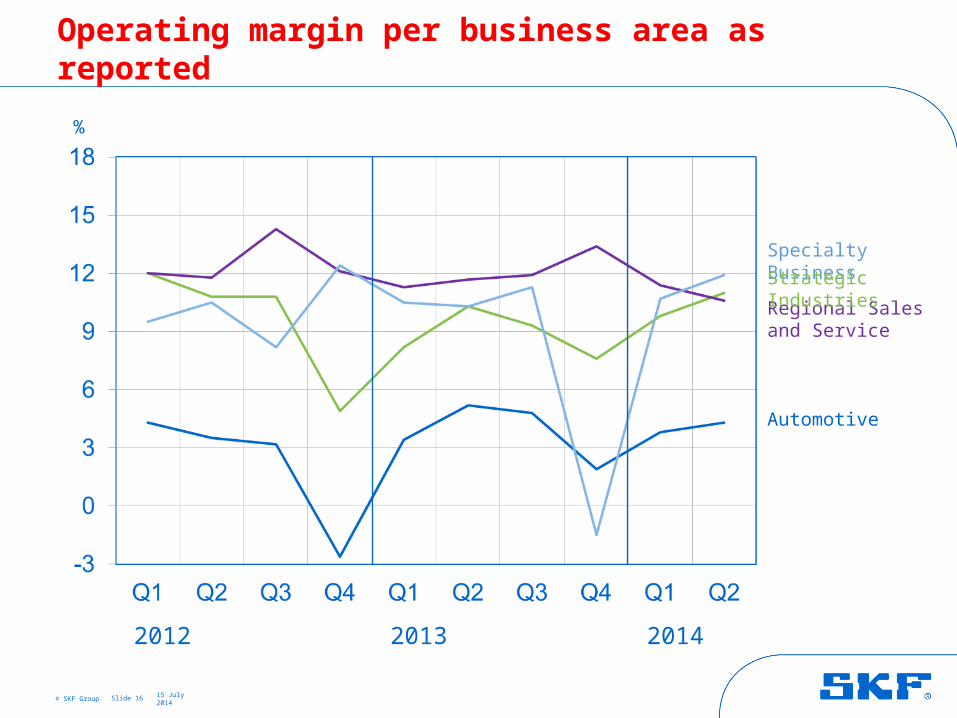

© SKF Group 15 July 2014Slide 16

Regional Salesand Service

Specialty Business

Automotive

%

2012 2013 2014

Operating margin per business area as reported

Strategic Industries

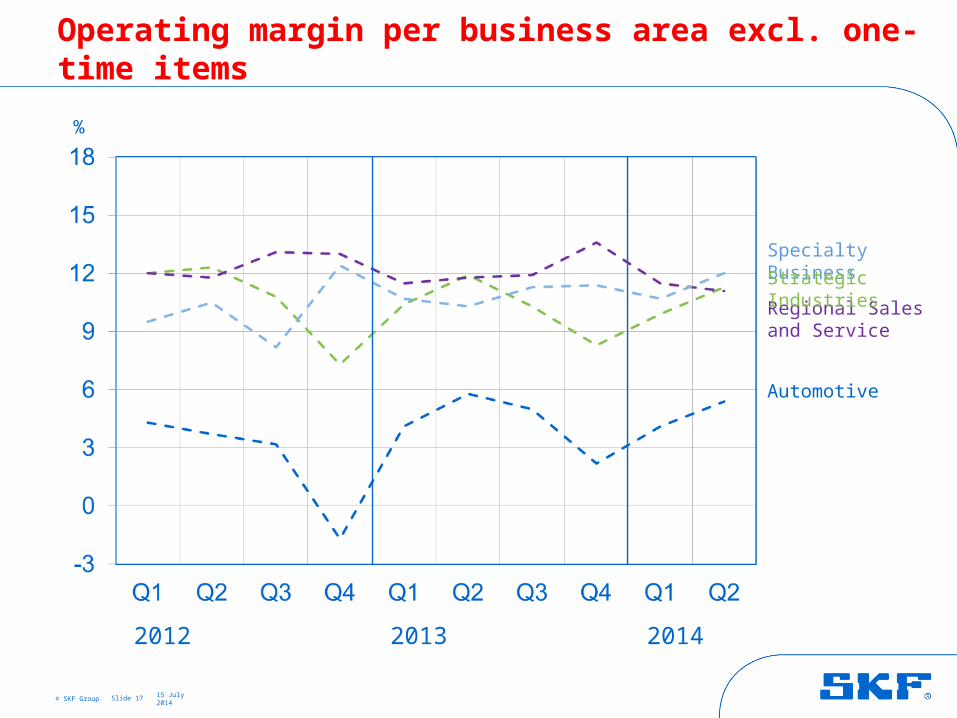

© SKF Group 15 July 2014Slide 17

Regional Salesand Service

Specialty Business

Automotive

%

2012 2013 2014

Operating margin per business area excl. one-time items

Strategic Industries

© SKF Group 15 July 2014

SKF’s programme to improve efficiency and reduce cost

Slide 18

Q4/12 Q1/13 Q2/13 Q3/13 Q4/13 2013 Q1/14 Q2/14 Total

Cost taken 200 250 190 0 50 490 0 100 790

People affected 530 410 320 0 130 860 0 170 1,560

Q1/13 Q2/13 Q3/13 Q4/13 2013 Q1/14 Q2/14 2014

Restructuring 15 35 75 75 200 70 50 120

S&A 50 50 50 50 200 0 0 0

Purchasing 100 100 100 100 400 60 100 160

Total 165 185 225 225 800 130 150 280

Restructuring, SEKm:

Realized gross savings from total programme, SEKm:

Full year gross saving 150 100 80 0 40 220 0 100 470

Giving future gross savings, SEKm:

vs 2012 vs 2013

Note: Run rate Q2 2014 SEK 1,340 million vs 2012.

© SKF Group 15 July 2014

Operating profit bridge, Q2 2014

Slide 19

+1601,837

+160 2,096+134

+150 +70 -120-295

SEKm

Q2 2013 Q2 2014Volumes excl.

Specialty

Business

Specialty

Business

Savings One-time items

Currencies R&D, inflation etc.

Price/mix

© SKF Group 15 July 2014

Operating profit bridge, half year 2014

Slide 20

+4003,317

+604,120+240

+280

+440 -220-397

SEKm

Q2 2013 Q2 2014Volumes excl.

Specialty

Business

Specialty

Business

Savings One-time items

Currencies R&D, inflation etc.

Price/mix

© SKF Group 15 July 2014

Net working capital as % of annual sales

Slide 21

%

2012 2013 2014

Target: 27%

© SKF Group 15 July 2014

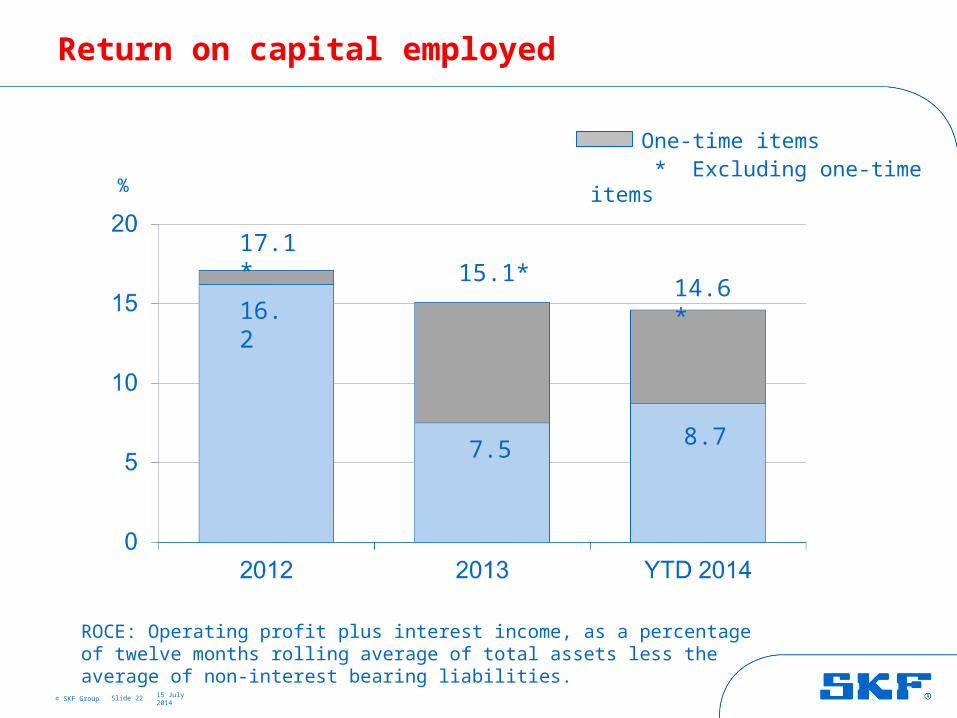

Return on capital employed

Slide 22

%

14.6*

7.5 8.7

16.2

17.1*15.1*

One-time items * Excluding one-time items

ROCE: Operating profit plus interest income, as a percentage of twelve months rolling average of total assets less the average of non-interest bearing liabilities.

© SKF Group 15 July 2014

Cash flow, after investments before financing

Slide 23

SEKm

2012 2013 2014

Excl. acq. and div.: 1) Q3 2012 SEK 1,707 million2) Q1 2013 SEK -69 million3) Q3 2013 SEK 871 million4) Q4 2013 SEK 1,170 million

Excl. EU payment 5) Q2 2014 SEK 1,423 million

4) 5)

© SKF Group 15 July 2014

Net debt

Slide 24

SEKm

2012 2013 2014

AB SKF, dividend paid (SEKm):2012 Q2 2,5042013 Q2 2,5302014 Q2 2,530

Cash out fromacquisitions (SEKm):

2012 Q3 8292013 Q1 8232013 Q4 7,900

Net debt: Loans and net provisions for post-employment benefits less short-term financial assets excluding derivatives.

EU payment (SEKm):

2014 Q2 2,825

© SKF Group 15 July 2014

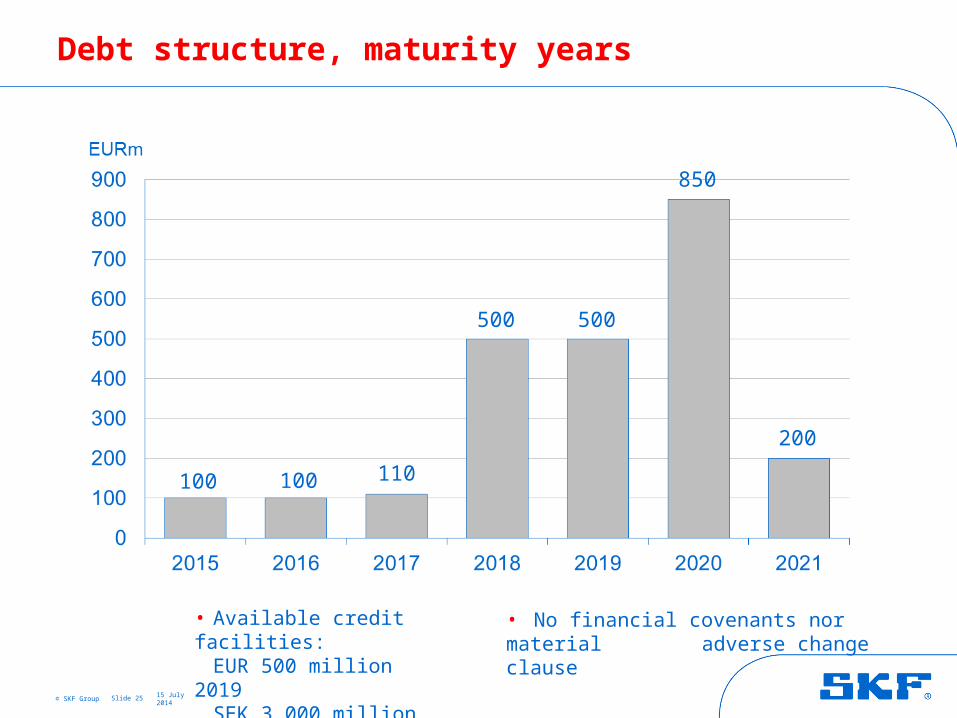

Debt structure, maturity years

Slide 25

• Available credit facilities:EUR 500 million 2019SEK 3,000 million 2016

SEK 3,000 million 2017

• No financial covenants nor material adverse change clause

200

100 100 110

500 500

850

© SKF Group 15 July 2014

July 2014: SKF demand outlook Q3 2014

Slide 26

Demand compared to the third quarter 2013

The demand for SKF’s products and services is expected to be slightly higher for

the Group and North America, higher for Asia, relatively unchanged for Europe

and slightly lower for Latin America. It is expected to be higher for Strategic

Industries and relatively unchanged for Regional Sales and Service and

Automotive.

Demand compared to the second quarter 2014

The demand for SKF’s products and services is expected to be relatively

unchanged for the Group and Europe. It is expected to be slightly higher for

North America and Asia and slightly lower for Latin America. For Strategic

Industries it is expected to be slightly higher and for Regional Sales and Service

and Automotive it is expected to be relatively unchanged.

Manufacturing

Manufacturing is expected to be slightly higher year over year and relatively

unchanged compared to the second quarter.

© SKF Group 15 July 2014

SKF demand outlook Q3 2014, main regions

Share of net sales 2013

Europe 42%

Asia Pacific 24%

North America 24%

Latin America 7%

Total

Q3 2014 vs Q3 2013

+/-

++

+

-

+

Slide 27

Sequential trend for Q3 2014

© SKF Group 15 July 2014

SKF demand outlook Q3 2014, main business areas

Share of net sales 2013

StrategicIndustries

29%

Regional Sales and Service

39%

Automotive 27%

Total

Q3 2014 vs Q3 2013

++

+/-

+/-

+

Slide 28

Sequential trend for Q3 2014

© SKF Group 15 July 2014

SKF sequential volume trend Q3 2014, Industries

Slide 29

6% Aerospace

5% Energy

4% Railway

2% Two-wheelers and Electrical

29% Industrial distribution

14% Cars and light vehicles

13% Industrial, heavy, special and off-highway

11% Vehicle service market

11% Industrial, general

5% Trucks

Share of net sales 2013

© SKF Group 15 July 2014

Guidance for the third quarter 2014*

Slide 30

• Tax level: around 30%

• Financial net for the third quarter:Around SEK -230 million

• Currency impact on operating profit versus 2013Q3: SEK +50 millionFull year: SEK -70 million

• Additions to PPE: Around SEK 1.6 billion for 2014

* Guidance is approximate and based on current assumptions and exchange rates.

© SKF Group 15 July 2014

SKF’s priorities

Slide 31

Sustainable profitable growth• Expand the platform concept• Exploit the asset life cycle approach• Develop new products and grow SKF BeyondZero portfolio• Extend and grow second brands• Acquisitions

Investments & Innovation • New and existing facilities• Research and development• IT systems and mobility

Cost reduction• Business Excellence• Consolidation of manufacturing• Optimization and productivity improvements• Reduction in purchasing costs

Capital efficiency• Fixed capital• Net working capital

© SKF Group 15 July 2014

Cautionary statement

Slide 32

This presentation contains forward-looking statements that are based on the current expectations of the management of SKF.

Although management believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those implied in the forward-looking statements as a result of, among other factors, changes in economic, market and competitive conditions, changes in the regulatory environment and other government actions, fluctuations in exchange rates and other factors mentioned in SKF's latest annual report (available on www.skf.com) under the Administration Report; “Important factors influencing the financial results", "Financial risks" and "Sensitivity analysis”.

© SKF Group 15 July 2014