sino-russian quest for influence in west asia: decrypyting the future- syrian footwold

DESCRIPTION

This paper attempts to decode the underlying forces shaping the Sino-Russian motives in the Gulf region in general and active involvement in Syria in particular. It highlights various possible aspects that could give some insight why these remotely located countries have become so active in the Syrian quagmire. Various aspects and its future implications and possible alliances under new circumstances are delineated in this paper. This paper has been written nine months earlier.TRANSCRIPT

Sino-Russian Quest in the Gulf: Decrypting Future Dynamics

Syria as a Footstep

Zakir Hussain

Research Fellow

Indian Council of World Affairs Sapru House, Barakhamba Raod

New Delhi -110 001

Since the outbreak of the Arab Spring the authoritarian regimes in the Arab world find it

tough to claim their legitimacy, both in the eyes of the world and their own public. After the

fall of Ben Ali in Tunisia, Hoosni Mubarak in Egypt, Ali Abdullah Saleh in Yemen, and the

protest movement in Bahrain and the blood end of Gaddafi in Libya, the issue of regime

change in Syria have taken a wholly different turn. The rebel groups, around 30 in number,

agitating for regime change has not been able to boot out the five-decade-old house of Asad

from power, despite some Arab countries’ open insistence on arming the rebels.1 On the

external front, the situation has polarized into a big and diverse “policy stand” fight. Unlike in

the case of Iraq and Libya, this time around Russia and China have taken a stand totally

different from that of the US-Western alliance. Both have so far maintained status quo ante by

providing strong “diplomatic”2 cover to the Bashar al-Asad regime by vetoing twice to the

resolutions introduced by the US-West-Arab League in the UN Security Council against the

al-Asad regime. However, the resolution introduced in the UN General Assembly came up

with a totally different mandate: 137 countries for, 12 against, with 17 abstentions, called on

Bashar al-Asad “to immediately put an end to all human rights violations and attacks against

civilians”.3 Saudi King Abdullah also gave a call to the Asad regime to step down and expressed

anguish to the Russian Prime Minister Medvedev that Saudi Arabia “will never abandon its

religious and moral obligations towards what’s happening” in Syria.4

What made Russia and China create history by vetoing the resolutions twice? Why has Syria

become “core” to their West Asia policy? Is it a vindication of their Libya policy faux pas5 or a

protest note against the West or is an attempt to assert their positions in evolving new world

order? Myriad analogies might be drawn but a deeper analysis brings out some insights why

there is so much resonance and dissonance on Syria and Iran. Is Domino theory coming back

or is it the return of cold war 3.0.6

1 Saudi Arabia and Qatar lobby hard to arm the rebel groups to fight against the Basher regime.

2 For a detailed discussion see Zakir Hussain, Decoding the Syrian Blast, http://www.icwa.in/pdfs/VBzh.pdf

3 UN Adopts Resolution against Assad; gets Support from India, The Hindustan Times, 17 February 2012.

http://www.hindustantimes.com/world-news/NorthAmerica/India-votes-for-Syria-resolution-in-

UNGA/Article1-812884.aspx. 4 Jonathan Schanzer, Saudi Arabia Is Arming the Syrian Opposition: What could possibly go wrong?, February

27, 2012 The Foreign Policy.

.http://www.foreignpolicy.com/articles/2012/02/27/saudi_arabia_is_arming_the_syrian_opposition?page=full 5 For a detailed discussion see Zakir Hussain, Decoding the Syrian Blast, http://www.icwa.in/pdfs/VBzh.pdf

6 In the last six decades three phases of ‘cold war’ has seen. The first started with a tacit confrontation between

the former USSR and the US, thereafter a phase of detente occurred. Subsequently new dynamics in the form of

second cold war emerged when Chain and the US came together after the Vietnam War to curb the Soviet

influence. Now, this is the third phase of the cold war when Russia and Chain returned to experiment their

policy against the western dominance and prevent the possibility of insinuation of “localized” version of cold

war, may be termed as Cold War 3.0.

I: Russian Roulette in Syria and Iran

Russia’s Return to Strategic Configuration in the Region

After the fall of Saddam Hussein in Iraq, the current Syrian regime is the last standing

Ba’athist-communist dispensation in the region, providing the last ideological foothold to

Russia in West Asian politics. Both the US and Russia have in West Asia pursued a “two leg”

policy. The US had maintained Iran and Saudi Arabia, while the former USSR, Iraq and Syria.7

However, after the end of the cold war and the beginning of the Arab Spring, both exogenous

powers have lost one leg each in the region and the current diplomatic struggle seems to be

the continuation of restoring the past “two leg” policy in the region, i.e. Iran and Syria for

Russian influence and Saudi Arabia and Iraq to the US and its allies.8 The analysts like Cohen

believe:

“Flush with oil cash, Putin chose to confront the West and the Arab world over Syria and Iran. Together with China, he imposed two vetoes in the U.N Security Council against the Syrian sanctions...Moscow would like to see the US power so diminished in the Middle East and Europe that America could not act without Russian permission.” 9

Geo-Strategic Compulsions

Syria offers Russia a significant strategic foothold in the region. Syria’s Tartus port provides

Russia access to the warm water port of the Mediterranean Sea. The Mediterranean Sea also

provides direct access to Syria from the disturbed regions of Russia like Dagestan and

Chechnya. It is believed that if the hardliners/Islamists, whose presence is expected to

increase after US withdrawal from Iraq, succeed in toppling the al-Asad regime, would extend

and intensify their support, both ideologically and in resources, to the rebels groups active in

the disturbed regions of Russia. The deteriorating security condition in Syria has already

convinced Russia to take proactive policy steps towards Damascus. Recently, there is news in

rife that Russia has replaced its ships deployed in November 2011 at the Tartus port in

Mediterranean Sea by sending Black Sea fleet’s Iman tanker. Although Russia has denied any

such deployments, the UN Security Council has termed this move as “a bomb” bound to

“create certain serious repercussion” in the region and beyond.10

Arms Market

7 Other countries where the former USSR maintained its presence in the region were Yemen.

8 This author believes that due several reasons the new trifurcated Iraq (Sunni Iraq, Shia Iraq and Kurd Iraq) has

minimised the geo-strategic positions of both Iran and Saudi Arabia in the region. 9 Ariel Cohen (2012) How the US Should deal with Putin’s Russia”, Issue Brief, No. 3530, March 7, The

Heritage Foundation. 10

Kirit Radia and Rym Momtaz, Russian Anti-Terror Troops Arrive in Syria, March 20,

2012.http://news.yahoo.com/russian-anti-terror-troops-arrive-syria-164035966--abc-news.html

Syria and Iran are also lucrative arms markets for Russia. Since the Islamic Revolution in Iran

(1979) as well as due to Syria’s sustained support to Iran, the US and the major European

countries have imposed an arms embargo over both. Russia has benefited from this market for

its weapons, joined later on by China as well. According to Richard F. Grimmett, a veteran

international security specialist at the Congressional Research Service in Washington, “from

2007 to 2010, the value of Russian arms deals with Syria more than doubled – $4.7 billion from

$2.1 billion – compared with 2003 to 2006”.11 It is noted that before al-Asad’s crackdown, 50 per

cent of the Syrian arms market was captured by Russia, 30 per cent by China and North Korea

and 20 per cent by Iran.12 Despite stiff opposition to stop arms supply to Syria by the US-West,

the Russian Deputy Defence Minister Anatoly Antonov said “Russia will abide by the existing

contracts to deliver weapons to Syria”. He added that “Russia enjoys good, strong military

technical cooperation with Syria, and we see no reason to reconsider it”.13

Data reveal that Syria is the largest Russian arms buyer in West Asia. According to Richard

Galpin, BBC World Correspondent, approximately “10 percent of Russia’s global arms sales go

to Syria.”14 Since the crisis started in the region, Syria concluded $3.5 billion arms deal with

Russia. The arms deal involves the supply of two Bastion anti-ship missile systems with 72

Yakhont supersonic missiles, the prototype of the Indo-Russian BrahMos Missile.15 16

Regarding Iran, between 1995 and 2005, Russia supplied 70 percent of the Iranian arms

purchase. Effectively, the arms relations between Russia and Iran existed even before the end

of the Cold War. Between 1989 and 1991, according to Alla (2006), the Soviet Union signed

major arms deal with Iran; it supplied Iran MIG-29 and SU-24 fighter aircraft missiles, S-200

11

David M. Herszenhorn, “For Syria, Reliant on Russia for Weapons and Food, Old Bonds Run Deep”,

February 18, 2010. The New York Times. http://www.nytimes.com/2012/02/19/world/middleeast/for-russia-and-

syria-bonds-are-old-and-deep.html?pagewanted=all 12

Thomas Grove and Erika Solomon, “Russia boosts arms sales to Syria despite world pressure, Reuters”,

February 21, 2012. http://www.reuters.com/article/2012/02/21/us-syria-russia-arms-idUSTRE81K13420120221 13

Russia Says Arms Sales to Syria Will Continue Despite Uproar, The Moscow Times, march 14, 2012.

:http://www.themoscowtimes.com/news/article/russia-says-arms-sales-to-syria-will-continue-despite-

uproar/454617.html#ixzz1pMSOBn9l 14

Richard Galpin, “Russian Arms Shipments Bolster Syria’s Embattled Assad”, The BBC News Middle East,

January 30, 2012.http://www.bbc.co.uk/news/world-middle-east-16797818 15

Vladimir Radyuhin, “Russian arms deal with Syria stays despite clashes”, The Hindu, November 13, 2011

http://www.thehindu.com/news/international/article2624802.ece 16

Since the crisis started in the Gulf, an arm race has also started. US, Russia have signed billions’ dollar arms

deal with their respective allies. For instance, US made commitment to supply $30 billion worth of arms sales to

Saudi Arabia, nearly $11.5 billion to Iraq and $3.5 billion to the UEA by supplying it the THAAD (Theatre

High Altitude Area Defense)- the only system designed to destroy short- and intermediate-range ballistic

missiles both inside and outside the Earth's atmosphere. Jim Wolf, “ U.S. in $3.5 billion arms sale to UAE amid

Iran tensions”, December 31, 2011, The Reuters. http://www.reuters.com/article/2011/12/31/us-usa-uae-iran-

idUSTRE7BU0BF20111231

air defence complexes, three diesel submarines, and hundreds of tanks and armoured vehicles

as well as various munitions.17

Inelasticity of Iran’s Nuclear Urge and Creation of Huge Enriched Fuel Market in West Asia

Iran’s nuclear programme, in both cases either for military purposes or civilian uses, offers

huge incentives to Russia to supply that country both enriched fuel and uranium.18

Technologically, Iran has low nuclear capability. Russia and other countries will be the

choicest partners of Iran to furnish enriched nuclear fuel, reactors and other nuclear

equipment. Iran had earlier approached Russian, Argentine, Brazilian, Chinese and Pakistani

companies either for completion of work on the Bushehr reactors or to acquire research

reactors.19

In its recent report, October 2011, the IAEA has indirectly underlined the role of a Russian

nuclear expert20 in developing and assisting the Iranian nuclear programme:

Strong indications that the development by Iran of the high explosives initiation system, and its development of the high speed diagnostic configuration used to monitor related experiments were assisted by the work of a foreign expert. [The expert] was not only knowledgeable in these technologies... (but) worked for much of his career with this technology in the nuclear weapon programme of the country of his origin.21

In case Iran succeeds in developing nuclear capability, it will generate a different kind of

atmosphere in the region. Foremost, it will drastically transform the political and security

architecture of the region. Second, it will reduce the US preponderance in the region. As a

result, the small but resource-rich countries might evolve a different foreign policy mechanism

and, possibly, they would likely maintain an “equidistance” policy between the US-Israel and

Iran. Third, it will wage a “psychological” war on Saudi Arabia and force the Kingdom to

develop its own nuclear capability, a growing desire that could expansively be noticed among

17

Kassianov Alla (2006) Russian Weapons Sales to Iran: Why they are unlikely to Stop, PONARS Policy Memo

427, http://csis.org/files/media/csis/pubs/pm_0427.pdf. 18

Another country which would likely to share the Iranian nuclear pie will be Kazakhstan, sitting over 16 per

cent global uranium deposits. 19

Asli Bali, “The US and the Iranian Nuclear Impasse”, MER241, http://www.merip.org/mer/mer241/us-

iranian-nuclear-impasse. The Iranian nuclear programme for peaceful purposes was established in 1957 under

US supervision. In 1974, the Shah announced a target of 23,000 MWe of nuclear capacity to free up oil and gas

for export. At Darkhovin, two French companies started building two 910 MWe units; however, after the

Islamic Revolution not only the French but almost all the Western countries denied nuclear assistance to Iran. In

1992, the Iranian government signed an agreement with China to build two 300 MW reactors at Darkhovin, but

after US intervention, “China withdrew before construction started”. 20

The US-based Institute for Science and International Security (ISIS) has identified Vycheslav Danilenko, a

Russian scientist, as the expert.20

Danilenko is reported to have been living in Iran for the last five years. 21

http://www.straitstimes.com/BreakingNews/World/Story/STIStory_734076.html.

the Saudi thinkers.22 Again, the Saudi nuclear quest might be opposed by the US-Israel. This

may force Saudi Arabia to clamber aboard the Russian/Chinese boat, which again might not

be liked by the US to lose Saudi Arabia. The US has to placate the Saudi monarch by doing

some extra security adventure in the region as well as soothe the pride as well as help

maintain the legitimacy of the Arab Gulf monarchs.

In case, the US support Saudi Arabia to go nuclear, the region will witness some likely

ramifications: (i) Collapse of NPT (Non-Proliferation Treaty) will be imminent as both Saudi

Arabia and Iran are the signatories of the treaty; (ii) Owning nuclear technology may became a

case of national pride; consequently, other regional powers like Turkey, Egypt might also

attempt for developing nuclear capabilities; (iii) The region would generate huge markets for

enriched fuels, nuclear reactors and equipments; and Russia, China and other uranium rich

countries would enter the Middle East enriched nuclear fuel market. Going by the IAEA

information, eighteen Middle East countries have already applied for Nuclear Power Plant

(NPP). This may trigger a new dynamics of enriched fuel market in the world. 23

Energy Dynamics

Another significant point of Russian interest in the Persian Gulf might be “energy”. Russia and

Iran are two hydrocarbon giants. Their combined reserves of oil account approximately for 15

per cent of world reserves: Russia, 214 billion barrels (15 per cent) and Iran 137 billion barrels

(9.9 per cent). Their combined natural gas deposits exceed 40 per cent of the global deposits:

Russia 24 per cent (44.8 trillion cubic metres – tcm) and Iran 16 per cent (29.6 tcm). At the

current reserve/production ratio, their shelf lives of gas deposits are estimated to be more

than 21.4 and 88.4 years respectively.24

Besides this, both countries have a significant say in the global production of oil and gas. In

recent years, Russia has emerged as a top oil-producing and –exporting country, even ahead of

Saudi Arabia. It contributes around 12.9 per cent (10.2 million barrels per day–mbd) oil to the

22

Perkovich, et al (2005) have also listed Saudi Arabia under “Intention Suspected but no Weapon Programmee

identified”, page 20, table 1.1., George Perkovich, et.al. (2005) Universal Compliance: A Strategy For Nuclear

Security, Carnegie Endowment for International Peace., Washington, USA.

Jason Burke, “Saudi Arabia worries about stability, security and Iran”, The Guardian, June 29, 2011.

http://www.guardian.co.uk/world/2011/jun/29/saudi-arabia-prince-turki-arab-spring-iran; HRH Prince Turki

AlFaisal, A Tour d' Horizon of the Saudi Political Seas

December 15, 2011. http://idsa.in/keyspeeches/ATourdHorizonoftheSaudiPoliticalSeas . 23

Hussain, Zakir GCC Going Nuclear: Motives and Implications, Middle East Studies, Marine Corps

University, Virginia, USA Monograph, (forthcoming). 24

BP Annual Report, 2011.

http://www.bp.com/liveassets/bp_internet/globalbp/globalbp_uk_english/reports_and_publications/statistical_en

ergy_review_2011/STAGING/local_assets/pdf/statistical_review_of_world_energy_full_report_2011.pdf.

total world oil production, while Iran contributes approximately 5.2 per cent, nearly 4.2 mbd

to the total 82 mbd demand in the world.25

In both cases, either Russia and Iran cooperate with each other or remain isolated, Russian

Federation will largely benefit in international energy market.

Possible Scenarios

Scenario I – Non-Alliance: A mishap in the Persian Gulf, including an attack on Iran, would

massively benefit Russia. Oil prices will shoot up. The spare capacities with Saudi Arabia, the

UAE, Kuwait, Libya and Venezuela, accounting for 80 per cent of world spare capacity, can

compensate to the loss of the Iranian oil (3 mbd, 3 per cent) but they cannot cover up the

Russian share, which stands at nearly 12.9 per cent. According to Andrew E. Kramer, “Analysts

estimate that Iran jitters have added $5 to $15 a barrel to the global price of oil, which means

an extra $35 million to $105 million a day for the Russian industry.”26 Quoting Jesse Mercer, a

senior oil analyst based in Houston with PFC Energy, Kramer notes, “‘It is good for Putin. In

US when oil prices go up, the President’s ratings go down. In Russia, it’s the opposite’. The

extra money has [already] helped [Russia] further subsidize domestic energy consumption,

tempering down inflation.”27 Russia also enjoys the advantages of pipelines; its oil is of similar

quality as that of Iran. So Russia can easily cater for Iran’s European and Asian customers.

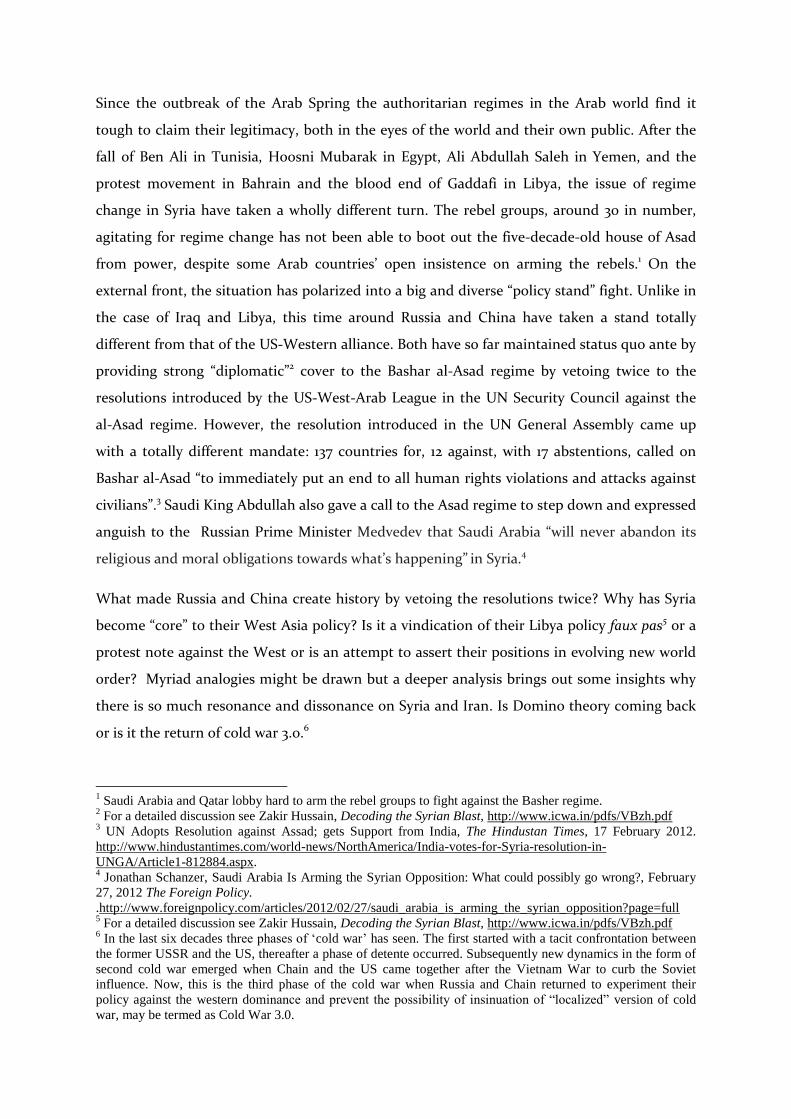

Figure 1 shows the top Russian oil importing countries of Asia and Europe.

25

Ibid. 26

Andrew E. Kramer, “An Iranian Oil Embargo and a Russian Oil Boom”, 16 February 2012, New York Times

News Service. 27

Ibid.

Figure 1: Direction of the Russian Crude Oil Export, Region & Major Countries, 2009.

Source: Energy Information Administration, USA.

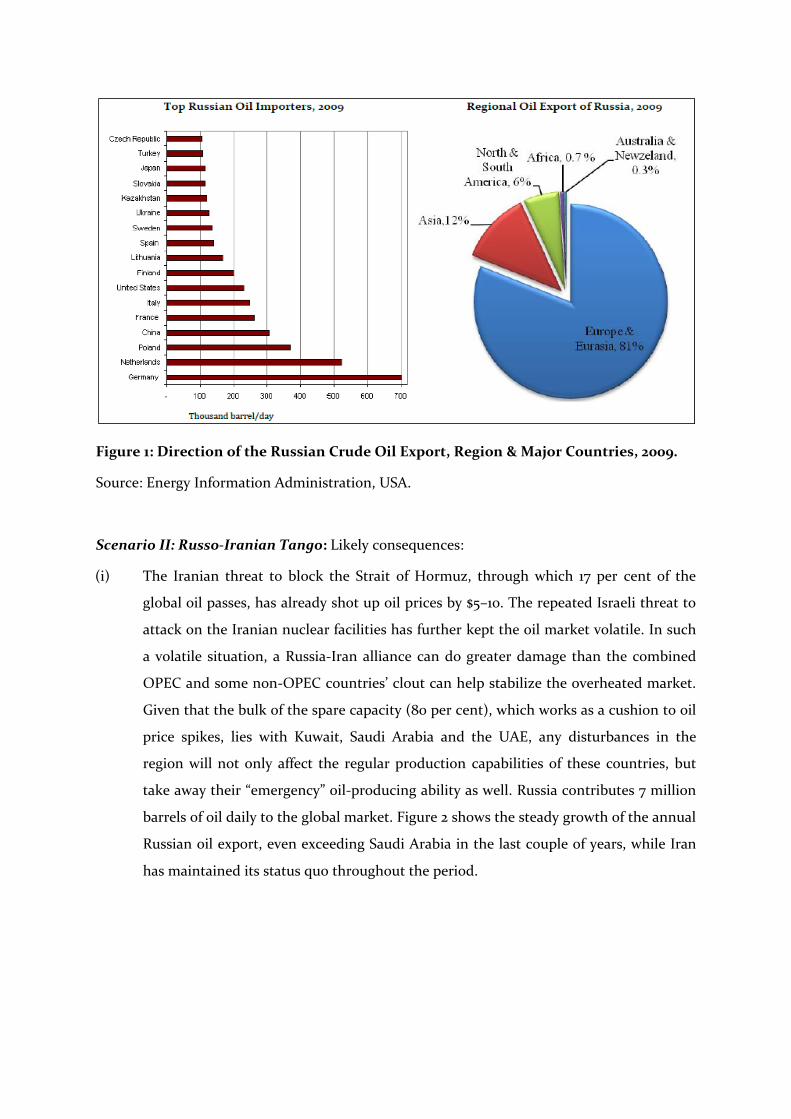

Scenario II: Russo-Iranian Tango: Likely consequences:

(i) The Iranian threat to block the Strait of Hormuz, through which 17 per cent of the

global oil passes, has already shot up oil prices by $5–10. The repeated Israeli threat to

attack on the Iranian nuclear facilities has further kept the oil market volatile. In such

a volatile situation, a Russia-Iran alliance can do greater damage than the combined

OPEC and some non-OPEC countries’ clout can help stabilize the overheated market.

Given that the bulk of the spare capacity (80 per cent), which works as a cushion to oil

price spikes, lies with Kuwait, Saudi Arabia and the UAE, any disturbances in the

region will not only affect the regular production capabilities of these countries, but

take away their “emergency” oil-producing ability as well. Russia contributes 7 million

barrels of oil daily to the global market. Figure 2 shows the steady growth of the annual

Russian oil export, even exceeding Saudi Arabia in the last couple of years, while Iran

has maintained its status quo throughout the period.

Note: Net export reached at by substracting total oil production from total consumption. Figure 2. Net Oil Export by Four Major Oil Producing Countries, 1965-2010 (in million tonnes)

Source: BP, 2011.

20 In the medium to long term, it might be tough for the OPEC and some of the non-

OPEC countries to stabilize and save the world from another “oil shock”.28 Due to huge

investment requirements and long gestation period in petroleum industry, the

traditional suppliers won’t be able to increase output at short notice. The international

oil and gas market is already operating on a tight margin. Besides this, the

hydrocarbon industry already is facing the crunch of investment capital and investors

are not readily available to invest in insecure and new regions. According to World

Energy Outlook 2011, in order to meet the energy demand by 2035, the global energy

sector needs an investment capital of nearly $38 trillion; and out of total 51 per cent,

28

“Oil and Gasoline”, New York Times, 29 December 2011,

http://topics.nytimes.com/top/news/business/energy-environment/oil-petroleum-and-

gasoline/index.html?inline=nyt-classifier

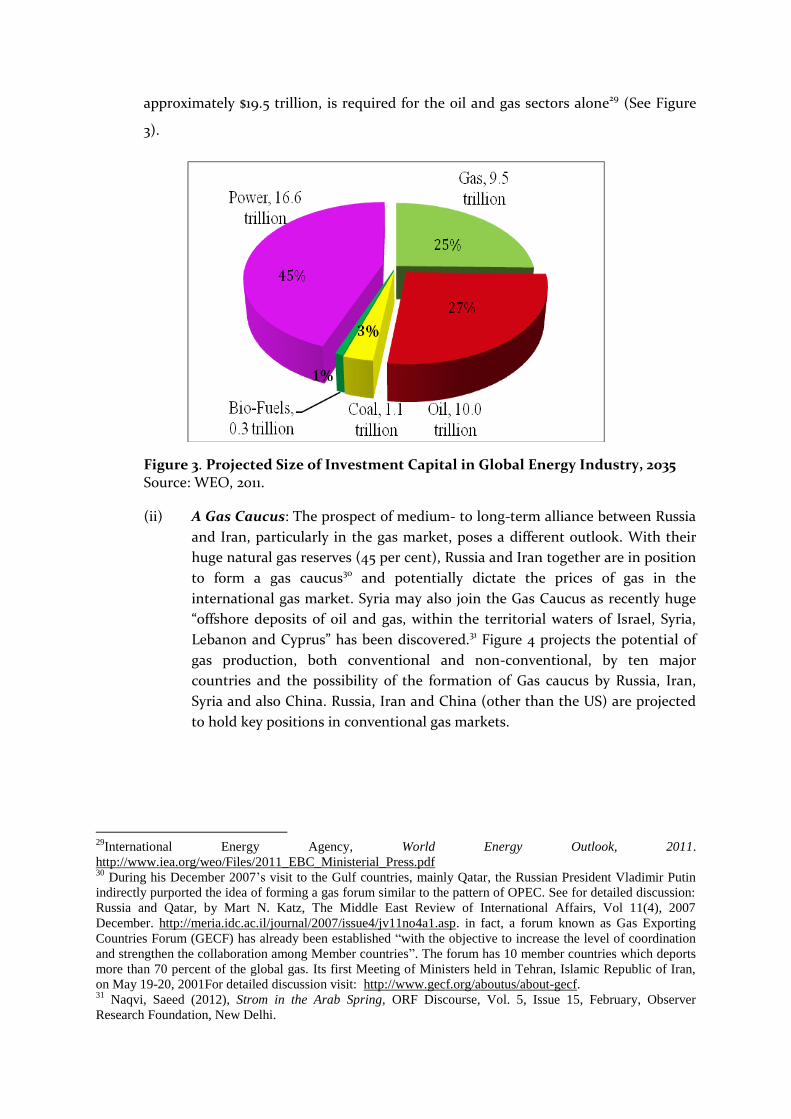

approximately $19.5 trillion, is required for the oil and gas sectors alone29 (See Figure

3).

Figure 3. Projected Size of Investment Capital in Global Energy Industry, 2035 Source: WEO, 2011.

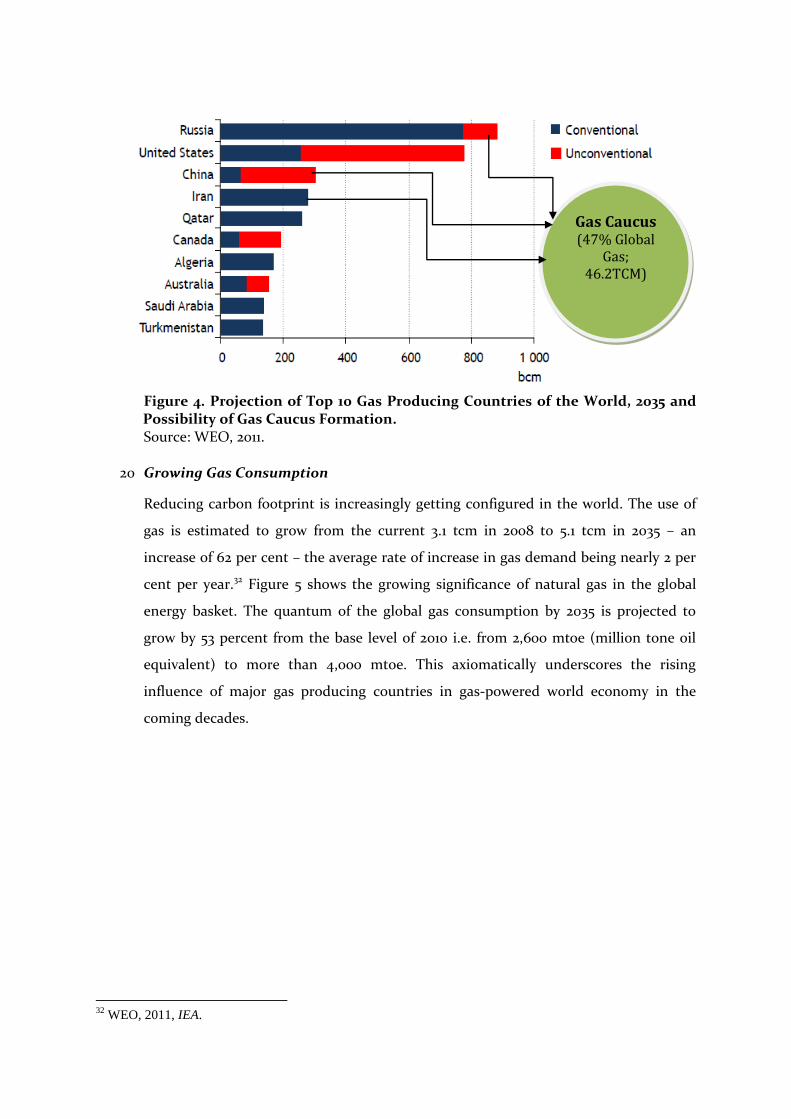

(ii) A Gas Caucus: The prospect of medium- to long-term alliance between Russia

and Iran, particularly in the gas market, poses a different outlook. With their

huge natural gas reserves (45 per cent), Russia and Iran together are in position

to form a gas caucus30 and potentially dictate the prices of gas in the

international gas market. Syria may also join the Gas Caucus as recently huge

“offshore deposits of oil and gas, within the territorial waters of Israel, Syria,

Lebanon and Cyprus” has been discovered.31 Figure 4 projects the potential of

gas production, both conventional and non-conventional, by ten major

countries and the possibility of the formation of Gas caucus by Russia, Iran,

Syria and also China. Russia, Iran and China (other than the US) are projected

to hold key positions in conventional gas markets.

29

International Energy Agency, World Energy Outlook, 2011.

http://www.iea.org/weo/Files/2011_EBC_Ministerial_Press.pdf 30

During his December 2007’s visit to the Gulf countries, mainly Qatar, the Russian President Vladimir Putin

indirectly purported the idea of forming a gas forum similar to the pattern of OPEC. See for detailed discussion:

Russia and Qatar, by Mart N. Katz, The Middle East Review of International Affairs, Vol 11(4), 2007

December. http://meria.idc.ac.il/journal/2007/issue4/jv11no4a1.asp. in fact, a forum known as Gas Exporting

Countries Forum (GECF) has already been established “with the objective to increase the level of coordination

and strengthen the collaboration among Member countries”. The forum has 10 member countries which deports

more than 70 percent of the global gas. Its first Meeting of Ministers held in Tehran, Islamic Republic of Iran,

on May 19-20, 2001For detailed discussion visit: http://www.gecf.org/aboutus/about-gecf. 31

Naqvi, Saeed (2012), Strom in the Arab Spring, ORF Discourse, Vol. 5, Issue 15, February, Observer

Research Foundation, New Delhi.

Figure 4. Projection of Top 10 Gas Producing Countries of the World, 2035 and Possibility of Gas Caucus Formation. Source: WEO, 2011.

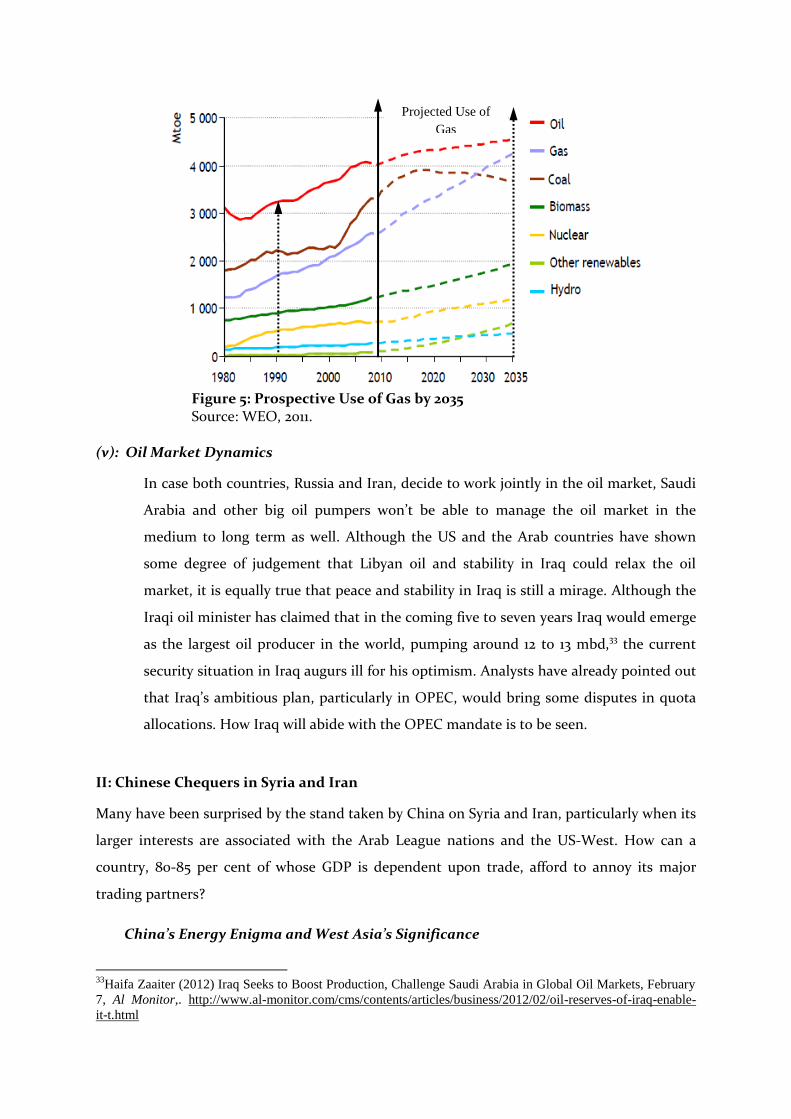

20 Growing Gas Consumption

Reducing carbon footprint is increasingly getting configured in the world. The use of

gas is estimated to grow from the current 3.1 tcm in 2008 to 5.1 tcm in 2035 – an

increase of 62 per cent – the average rate of increase in gas demand being nearly 2 per

cent per year.32 Figure 5 shows the growing significance of natural gas in the global

energy basket. The quantum of the global gas consumption by 2035 is projected to

grow by 53 percent from the base level of 2010 i.e. from 2,600 mtoe (million tone oil

equivalent) to more than 4,000 mtoe. This axiomatically underscores the rising

influence of major gas producing countries in gas-powered world economy in the

coming decades.

32

WEO, 2011, IEA.

Gas Caucus (47% Global

Gas; 46.2TCM)

Figure 5: Prospective Use of Gas by 2035 Source: WEO, 2011.

(v): Oil Market Dynamics

In case both countries, Russia and Iran, decide to work jointly in the oil market, Saudi

Arabia and other big oil pumpers won’t be able to manage the oil market in the

medium to long term as well. Although the US and the Arab countries have shown

some degree of judgement that Libyan oil and stability in Iraq could relax the oil

market, it is equally true that peace and stability in Iraq is still a mirage. Although the

Iraqi oil minister has claimed that in the coming five to seven years Iraq would emerge

as the largest oil producer in the world, pumping around 12 to 13 mbd,33 the current

security situation in Iraq augurs ill for his optimism. Analysts have already pointed out

that Iraq’s ambitious plan, particularly in OPEC, would bring some disputes in quota

allocations. How Iraq will abide with the OPEC mandate is to be seen.

II: Chinese Chequers in Syria and Iran

Many have been surprised by the stand taken by China on Syria and Iran, particularly when its

larger interests are associated with the Arab League nations and the US-West. How can a

country, 80-85 per cent of whose GDP is dependent upon trade, afford to annoy its major

trading partners?

China’s Energy Enigma and West Asia’s Significance

33

Haifa Zaaiter (2012) Iraq Seeks to Boost Production, Challenge Saudi Arabia in Global Oil Markets, February

7, Al Monitor,. http://www.al-monitor.com/cms/contents/articles/business/2012/02/oil-reserves-of-iraq-enable-

it-t.html

Projected Use of

Gas

Since China became a net importer of petroleum products in 1993, and net oil importer in

1996, energy security has occupied centre-stage in China’s foreign policy. Since then, the

central theme of China’s diplomacy has been targeting the energy-rich regions across the

world in general and the energy-rich Gulf, Africa and Central Asia, in particular. By the end of

2010, China had only 2 billion tonnes of proven oil reserves, which is only 1.1 per cent of the

global reserve34, while its consumption is growing by leaps and bounds. Although China is a

significant oil producer with an output of 202 million tonnes in 2010, almost 4.06 mbd, the

quotient of its self-sufficiency has drastically declined, from 102 per cent in 1993 to 45 per cent

in 2010 and at the given reserves/production ratio its reserves are capable of meeting only ten

years’ requirements.35 In 2010, China imported almost 239 million tonnes oil, up from 2.92

million tonnes in 2003. This scissors-like gap between domestic supply and demand has forced

the Chinese government to abandon its traditional goal of energy self-sufficiency and look

abroad for energy resources.36 A forecast reveals that by 2030 domestic oil production will be

able to meet less than 20 per cent – 3 mbd of the total daily oil consumption of 14.5 mbd.37

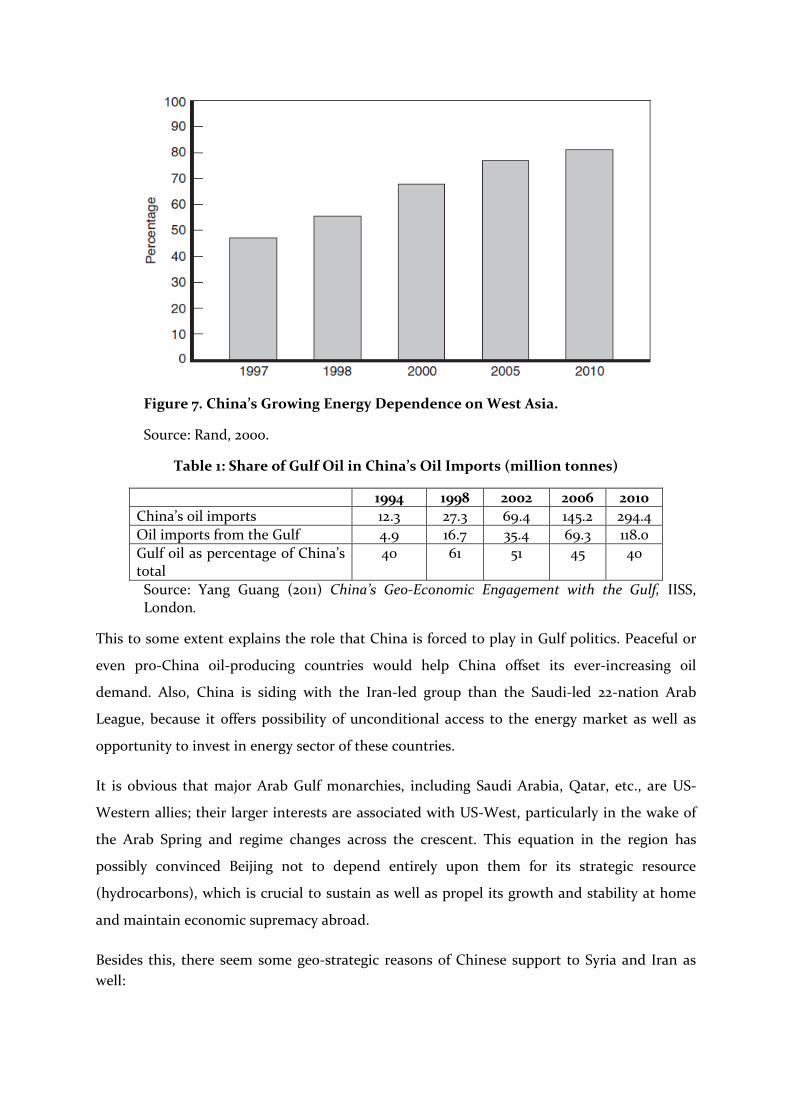

No country which is dependent for the bulk of its oil and gas requirements from outside

sources can ignore West Asia in general and the Persian Gulf in particular. About 67 per cent

of the global oil and more than 45 per cent of the gas are deposited in West Asia38, while in the

Persian Gulf, around 2/3 of the proven oil reserves (674 billion barrels) and 35 percent gas

(1,923 Tcf). 39 As a result, China’s fast growing economy is increasingly tied to the Gulf

countries for its energy needs.40 According to Raja Almarzodi Albdami, director of the Saudi-

based Institute of Diplomatic Studies, “58 percent of China’s oil imports currently come from

the Middle East region, and by 2015 this share will increase to 70 percent”.41 Figure 6 shows

that over the period 2015–2030, China’s domestic ability to meet its oil requirements will

34

BP Annual report, 2011. 35

Ibid. 36

Downs, Erica Strecker, China’s Quest for Energy Security, Santa Monica, CA: RAND Corporation, 2000,

http://www.rand.org/pubs/monograph_reports/MR1244. 37

Ibid. 38

For a detailed discussion see Zakir Hussain (viewpoint, 17 February 2012), Iran Crisis and India’s foreign

Policy Predicament. http://www.icwa.in/pdfs/VBIndiaIran.pdf 39

Persian Gulf Oil and Gas Exports Fact Sheet: http://www.parstimes.com/library/persian_gulf_doe_2003.pdf 40

Afshin Molavi (2011) Parsing the Reality and Promise of Gulf-Asia Engagement, papaer presented at IISS

Geo-Economics and Strategy programme, London. 41

Economic Intelligence Unit (2011), GCC Trade and Investment Flows: The Emerging-market Surge, EIU

Limited.

significantly decline, while its consumption continues booming. By 2030, China will be

importing 79 percent of the total oil from outside sources it consumes.42

Figure 6. Current and Projected China’s Oil Production and Import, 2008–2030 (mbd) Source: Julie Jiang and Jonathan Sinton (2011) Overseas Investments by Chinese National Oil Companies: Assessing the drivers and impacts, International Energy Agency, Paris.

Figure 7 and Table 1 reveal China’s growing energy dependence on West Asia in general and the Gulf energy market in particular. 43

42

Julie Jiang and Jonathan Sinton (2011) Overseas Investments by Chinese National Oil Companies: Assessing

the drivers and impacts, International Energy Agency, Paris. 43

Other major countries through which China resources its oil needs (May 2010) are Angola ($22.7 billion),

Russia ($8.8 billion), Sudan ($6.5 billion), Kazakhstan ($5.5 billion) and Libya ($4.453 billion). Country-wise

we also notice that over the period China has shifted the focus of its oil import in the Gulf countries. In 1999,

Oman supplied 13.7 per cent of China’s crude imports, followed by Yemen (11.3 per cent), Iran (10.8 per cent),

and Saudi Arabia (6.8 per cent). However, after one decade the situation changed. In May 2010, Saudi Arabia

toped the position, supplying oil worth of $25.5 billion, followed by Iran ($12 billion), Oman ($9.07 billion),

Iraq ($6.26 billion) and Kuwait ($5.46 billion). We also notice that during this period China also targeted other

oil-rich countries in different parts of the world. Angola, Russia, Sudan, Kazakhstan and Libya were also

brought under the Chinese energy radar.

Domestic

Production

Net Import

Figure 7. China’s Growing Energy Dependence on West Asia.

Source: Rand, 2000.

Table 1: Share of Gulf Oil in China’s Oil Imports (million tonnes)

1994 1998 2002 2006 2010

China’s oil imports 12.3 27.3 69.4 145.2 294.4

Oil imports from the Gulf 4.9 16.7 35.4 69.3 118.0

Gulf oil as percentage of China’s total

40 61 51 45 40

Source: Yang Guang (2011) China’s Geo-Economic Engagement with the Gulf, IISS, London.

This to some extent explains the role that China is forced to play in Gulf politics. Peaceful or

even pro-China oil-producing countries would help China offset its ever-increasing oil

demand. Also, China is siding with the Iran-led group than the Saudi-led 22-nation Arab

League, because it offers possibility of unconditional access to the energy market as well as

opportunity to invest in energy sector of these countries.

It is obvious that major Arab Gulf monarchies, including Saudi Arabia, Qatar, etc., are US-

Western allies; their larger interests are associated with US-West, particularly in the wake of

the Arab Spring and regime changes across the crescent. This equation in the region has

possibly convinced Beijing not to depend entirely upon them for its strategic resource

(hydrocarbons), which is crucial to sustain as well as propel its growth and stability at home

and maintain economic supremacy abroad.

Besides this, there seem some geo-strategic reasons of Chinese support to Syria and Iran as

well:

“China has vested interests in a good relationship with Iran... [Its] priorities in Iran go beyond economic interests. Strong bilateral relations help to counter U.S. dominance in the Middle East and increase Beijing’s strategic leverage. China sees Iran’s influence in the Middle East and Central Asia as useful to advancing its political, economic and strategic agenda in that region”.44

China seems to hedge at least 10 to 20 per cent of its oil and gas by betting on Tehran. China is

also shrewd enough to squeeze Iran and sign long-term energy contracts at concessional rates,

particularly at this juncture.45 There are also possibilities that China might strike a deal to use

its currency, Rinminbi, to pay the oil bills and encourage counter non-oil trade with Tehran

similar on the pattern of Tehran and New Delhi signed the agreement.46

In the coming decades, Asia will be the largest energy market of the Gulf countries. The

energy requirements in both China and India are growing at a rate of 6 per cent per annum,

which is commensurate to their economic growth. On account of these realities, the major

Gulf countries are perhaps not in position to annoy Beijing. Rather we notice that despite

Chinese support to Syria and Iran, the energy interaction between Saudi Arabia and China has

increased. During the recent Chinese Premier, Wen Jiabao’s visit to Saudi Arabia, after a gap of

almost three decades, Saudi Aramco and Chinese Sinopec inked a joint venture, Yanbu

Aramco Sinopec Refining Co. Ltd (YASREF), to establish a $8.4 billion refinery at Yanbu, Saudi

Arabia. The YASREF will begin production in the second half of 2014, processing 400,000

barrels of heavy crude oil a day. At the occasion, the Saudi Aramco President and CEO Khalid

Al-Falih said, “This is the fourth joint venture between our two enterprises [Armco &

Sinopec]... YASREF takes its rightful place next to out two downstream companies in China’s

Fujian Province, and our in-Kingdom upstream joint venture, Sino-Saudi Gas Ltd.”47 He also

pointed out that Sinopec was Saudi Aramco’s largest crude oil customer. The YASREE will

create 1,200 direct s and over 5000 indirect job opportunities.48 Saudi Arabia has also invested

in Chinese refineries and petrochemical units.

44

The Iran Nuclear Issue: The View from Beijing, Asia Briefing N°100, Beijing/Brussels, International Crisis

Group, 17 February 2010.

http://www.crisisgroup.org/~/media/Files/Middle%20East%20North%20Africa/Iran%20Gulf/Iran/b100%20The

%20Iran%20Nuclear%20Issue%20The%20View%20from%20Beijing.pdf 45

Indira A.R. Lakshmanan and Gopal Ratnam, “China Gets Cheaper Iran Oil as U.S. Pays Tab for Hormuz

Patrols”, 13 January 2012, http://www.bloomberg.com/news/2012-01-12/china-gets-cheaper-iran-oil-as-u-s-

pays-tab-for-hormuz-patrols.html 46

Ibid.; See: Sujay Mehdudia, ‘Iran agrees to accept payment in rupee”, The Hindu, March 3, 2012. 47

Siraj Wahab , “Aramco, Sinopec sign SR32bn Yanbu refinery deal”, The Arab News, Jan 15, 2012.

http://arabnews.com/economy/article563458.ece 48

Siraj Wahab , “Aramco, Sinopec sign SR32bn Yanbu refinery deal”, The Arab News, Jan 15, 2012.

http://arabnews.com/economy/article563458.ece

Besides Russia, Iraqis are also determined to hone their oil production capabilities. In this

atmosphere, Saudi Arabia and OPEC will not be able to dictate the terms of the energy market

at least for a half to one decade. At the same time, the “golden gas” era will emerge in the

world market. Consequently, the Arab Gulf, spearheaded by the Saudi Arabia, possibly will not

be able to dictate the terms in the energy market in general and with China in particular.

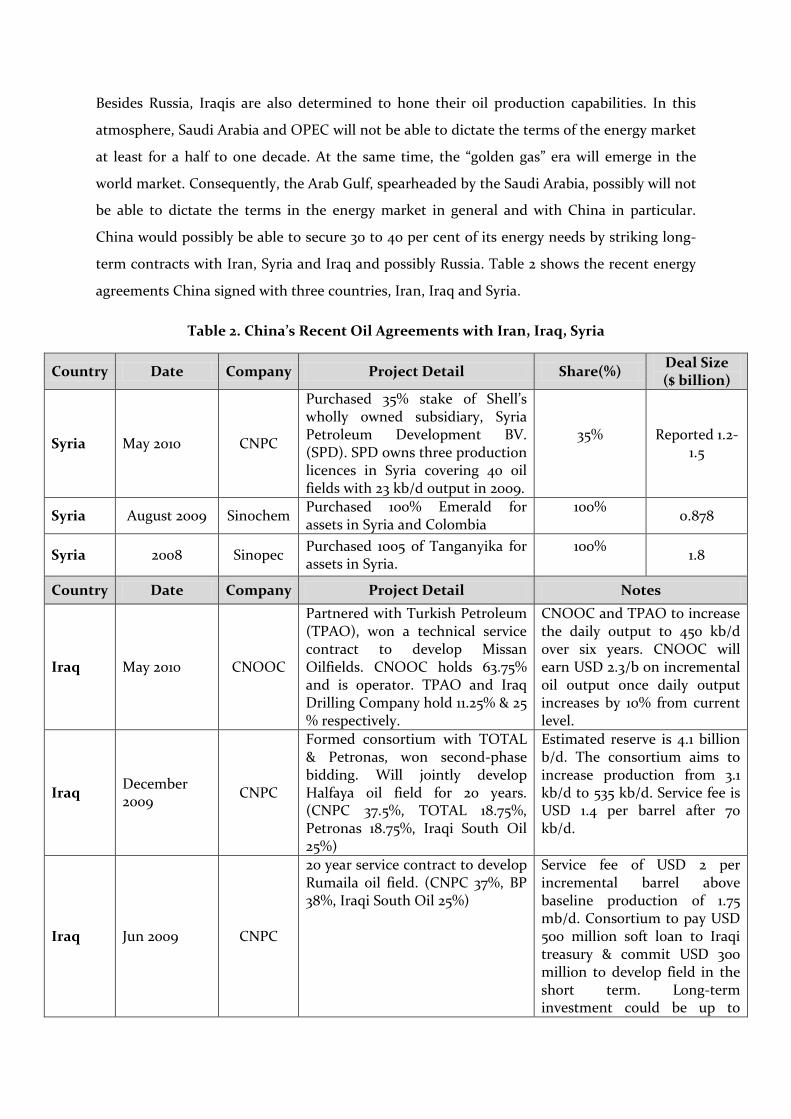

China would possibly be able to secure 30 to 40 per cent of its energy needs by striking long-

term contracts with Iran, Syria and Iraq and possibly Russia. Table 2 shows the recent energy

agreements China signed with three countries, Iran, Iraq and Syria.

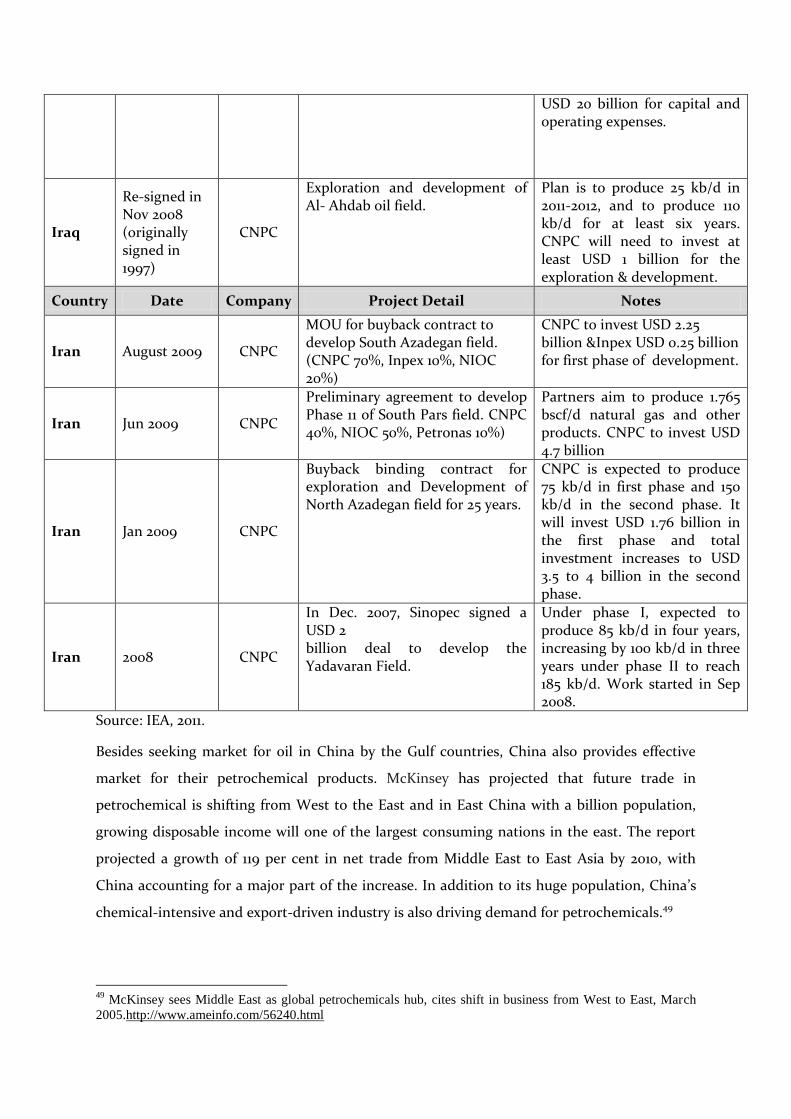

Table 2. China’s Recent Oil Agreements with Iran, Iraq, Syria

Country Date Company Project Detail Share(%) Deal Size ($ billion)

Syria May 2010 CNPC

Purchased 35% stake of Shell’s wholly owned subsidiary, Syria Petroleum Development BV. (SPD). SPD owns three production licences in Syria covering 40 oil fields with 23 kb/d output in 2009.

35%

Reported 1.2-1.5

Syria August 2009 Sinochem Purchased 100% Emerald for assets in Syria and Colombia

100%

0.878

Syria 2008 Sinopec Purchased 1005 of Tanganyika for assets in Syria.

100%

1.8

Country Date Company Project Detail Notes

Iraq May 2010 CNOOC

Partnered with Turkish Petroleum (TPAO), won a technical service contract to develop Missan Oilfields. CNOOC holds 63.75% and is operator. TPAO and Iraq Drilling Company hold 11.25% & 25 % respectively.

CNOOC and TPAO to increase the daily output to 450 kb/d over six years. CNOOC will earn USD 2.3/b on incremental oil output once daily output increases by 10% from current level.

Iraq December 2009

CNPC

Formed consortium with TOTAL & Petronas, won second-phase bidding. Will jointly develop Halfaya oil field for 20 years. (CNPC 37.5%, TOTAL 18.75%, Petronas 18.75%, Iraqi South Oil 25%)

Estimated reserve is 4.1 billion b/d. The consortium aims to increase production from 3.1 kb/d to 535 kb/d. Service fee is USD 1.4 per barrel after 70 kb/d.

Iraq Jun 2009 CNPC

20 year service contract to develop Rumaila oil field. (CNPC 37%, BP 38%, Iraqi South Oil 25%)

Service fee of USD 2 per incremental barrel above baseline production of 1.75 mb/d. Consortium to pay USD 500 million soft loan to Iraqi treasury & commit USD 300 million to develop field in the short term. Long-term investment could be up to

USD 20 billion for capital and operating expenses.

Iraq

Re-signed in Nov 2008 (originally signed in 1997)

CNPC

Exploration and development of Al- Ahdab oil field.

Plan is to produce 25 kb/d in 2011-2012, and to produce 110 kb/d for at least six years. CNPC will need to invest at least USD 1 billion for the exploration & development.

Country Date Company Project Detail Notes

Iran August 2009 CNPC

MOU for buyback contract to develop South Azadegan field. (CNPC 70%, Inpex 10%, NIOC 20%)

CNPC to invest USD 2.25 billion &Inpex USD 0.25 billion for first phase of development.

Iran Jun 2009 CNPC

Preliminary agreement to develop Phase 11 of South Pars field. CNPC 40%, NIOC 50%, Petronas 10%)

Partners aim to produce 1.765 bscf/d natural gas and other products. CNPC to invest USD 4.7 billion

Iran Jan 2009 CNPC

Buyback binding contract for exploration and Development of North Azadegan field for 25 years.

CNPC is expected to produce 75 kb/d in first phase and 150 kb/d in the second phase. It will invest USD 1.76 billion in the first phase and total investment increases to USD 3.5 to 4 billion in the second phase.

Iran 2008 CNPC

In Dec. 2007, Sinopec signed a USD 2 billion deal to develop the Yadavaran Field.

Under phase I, expected to produce 85 kb/d in four years, increasing by 100 kb/d in three years under phase II to reach 185 kb/d. Work started in Sep 2008.

Source: IEA, 2011.

Besides seeking market for oil in China by the Gulf countries, China also provides effective

market for their petrochemical products. McKinsey has projected that future trade in

petrochemical is shifting from West to the East and in East China with a billion population,

growing disposable income will one of the largest consuming nations in the east. The report

projected a growth of 119 per cent in net trade from Middle East to East Asia by 2010, with

China accounting for a major part of the increase. In addition to its huge population, China’s

chemical-intensive and export-driven industry is also driving demand for petrochemicals.49

49

McKinsey sees Middle East as global petrochemicals hub, cites shift in business from West to East, March

2005.http://www.ameinfo.com/56240.html

China also seeks to import energy-intensive goods like phosphate and aluminium, which the

GCC states can produce 30 percent50 more cheaply. The process of aluminium smelting, for

instance, requires large amounts of oil... Given the strong synergies to be gained by either side,

McKinsey predicts GCC oil exports to China will grow by an average of 3.7 per cent per annum

through 2030.51

China’s Economic Leverage: Trade & Finance Related Issues

China is well aware of its economic strengthen in the Gulf market. Although China’s trade and

commercial relations with the Gulf countries picked up after 1993, when China entered as a

net oil importer to the Gulf energy market, its size and volume has grown unparallel to any

other long term trading partners. Over a period of two decades, Chinese goods have carved a

solid niche in the GCC market, which China thinks will, more or less, continue in the coming

decades.

Since 2000, Chinese exports to the GCC have increased more than seven-fold, while trade

flows to the other way have increased five-fold...Total capital flows between the GCC and

China tallied around $32 billion in 2006.52 Between 2003 and 2005, bilateral trade between the

two countries registered a growth of 71 percent, from $16.9 billion to $33.8 billion. Again in

2007, it grew to $58 billion, with Chinese imports amounting to $30 billion and export to GCC

reaching $27.7 billion, which again grew to $70 billion in 2008.53 Looking at the growing

prospects of trade, commerce, and investment between the Gulf region and China, both sides

inaugurated the Federation of GCC Chambers of Commerce and Industry (FGCCC Chambers).

During his visit to three GCC countries, Saudi Arabia, Qatar and the UEA, the Chinese

Premier Wen Jibao expressed the hope to conclude the Free Trade Agreement between the

second largest energy consuming nation, China, and the GCC. The FTA will lower tariff

barriers and would stimulate more trade by opening the gateway to a wider range of goods

and services. This will also bolster GCC’s non-oil trade to China, particularly petrochemicals,

aluminium and other goods at competitive rates. The consulting group McKinsey predicts that

by 2020, total trade flows between China and the Middle East could climb to between $350

billion and $500 billion in real terms, which means at least a six-fold increase.54 China is

50

Jaap B. Kalkman, Laurent Nordin, and Ahmed YahiaMoving energy-intensive industries to the Gulf February

2007: https://www.mckinseyquarterly.com/Moving_energy-intensive_industries_to_the_Gulf_1921#Exhibit3 51

“China Gulf Economic Relations”, http://www.cfr.org/china/china-gulf-economic-relations/p16398 52

Lee Hudson Teslik (2008) China-Gulf Economic Relations, Council on Foreign Relations, June 4.

http://www.cfr.org/china/china-gulf-economic-relations/p16398 53

FGCC Chambers inaugurates agency in China, February 08 - 2009

http://www.ameinfo.com/184108.html 54

Mckensey Report

expected to be the GCC’s most important economic partner by 2020, according to a report by

the Economist Intelligence Unit (EIU).55

China also found the Gulf market as an attractive destination for its growing trade and

investment potentials. The current rise in oil prices has assigned massive oil wealth to these

Gulf investors and China is courting their investment. The chances of quid pro quo have

encouraged China to tag its energy with trade and investment policies in the Gulf. According

to the McKinsey report, in the five years to 2010, Asia is likely to require about $1 trillion of

foreign direct investment, and China alone will consume more than half of that total.56

This has convinced the Chinese authorities that the GCC countries, particularly the private

investors, will not be able to revisit their economic policies towards China. China with its deep

purse and suitable technology has also invested large amounts in GCC countries. The GCC

countries under their “Look East” policy have also found the Chinese market an attractive

destination for their investment.

China’s Asian Ordeal – Shifting Attention

Going by the current power dynamics in the Asia-Pacific region, China has declared its three

core interests to include Tibet, Taiwan and South China Sea. With regard to Tibet, new Prime

Minister in exile Dr Lobsang Sangay, a Harvard law scholar, has been appointed57, who may

provide an effective political leadership in the post-Dalai Lama period as the Dalai Lama

himself views Tibet movement as a political issue than a spiritual one. In Taiwan, the pro-

unification government has lost the election and Taiwan wants to maintain its independent

identity. In the South China Sea, China has suffered humiliation in the East Asia Summit

(EAS). There were also reports of China staking its claim in the disputed zone and not

adhering to the Declaration of the Code of Conduct in South China Sea.

Matters have been further complicated by the proactive policy announcements of the US in

the Pacific region that the current century will be the “Century of Pacific”. Further, the

announcement of establishing a base at Darwin under Anzus Treaty, deploying 2,500

mariners, has provided strength to the small countries of South East Asia, against a possible

threat from the rising power of China in the region. This might have definitely perturbed the

55

Andy Sambidge, 9 May 2011, “China set to be GCC's top trade partner in 2020”,

http://www.arabianbusiness.com/china-set-be-gcc-s-top-trade-partner-in-2020-398790.html 56

Barton Dominic, Kito de Boer, and Gregory P. William (2006), “The New Silk Road: Opportunities for Asia

and the Gulf”, Mckinsey on Economics: Commentary, McKensey Quarterly, July 2006. 57

Tibet's first prime minister: the challenges ahead, The

Telegraph:http://www.telegraph.co.uk/news/worldnews/asia/tibet/8688146/Tibets-first-prime-minister-the-

challenges-ahead.html

Chinese thinkers. According to the Zambells (2012), “China’s support for Iran serves as a check

against Washington in response to the U.S. military presence in East Asia and its constellation

of allies and partners surrounding Chinese territory.”58

On account of these developments in the Asia-Pacific region, China and Russia may have

forged some common cause to resist the US-West combined onslaught in the Persian Gulf and

set an example of resistance. It may be that the two countries have come closer for tactical

gains, although there may not be a long-term alliance, because they have their own policy

differences on a number of issues. China and Russia may also want the US and its allies to

bleed on the West Asian front: this will keep the US engaged there, stymieing its ability to

open the Pacific front against China. The two decades’ long US engagement in West Asian

imbroglio has enormously benefitted China. China has already acquired the synonyms of

economic superpower, with $1.15 trillion worth of US treasuries in its bag, while the US

economy has turned the largest indebted country in the world: its debt-GDP ratio stands at

100 per cent, i.e. $15 trillion, leading the US economy to fall into a “low growth trap”.59

Tibet: China’s Achilles’ Heel

Last but not the least reason for China’s adamant support to Syria and Iran seems to be “home

grown”. The growing demand for independence by the Tibetans and the disturbed region in

Xinjiang and Uighurs is gradually building pressure on the Chinese authorities. Tibet is

becoming the Achilles’ heel of the Chinese authorities. Can China afford a second Tiananmen

Square, is big question mark. The world situation has drastically changed since that massacre

of pro-democracy students. On account of the Arab Spring, the Tibetan monks have also

intensified their passive resistance and increasing number of cases of self-immolation by the

Tibetan monks is being noticed. This might also be one of the reasons for the stiff Chinese

stand in the Gulf region and support to Syria and Iran.

III: Sino- Russian Priorities and Prospects

The alliance between Russia and China in West Asia indicates some policy stand of theirs in

the region and beyond. After the end of the cold war, West Asia is the only place left in the

58

Chris Zambelis, “China’s Persian Gulf Diplomacy Reflects Delicate Balancing Act”, China Brief, Vol 12 (4)

February 21, 2012. The Jamestown Foundation:

http://www.jamestown.org/single/?no_cache=1&tx_ttnews%5Btt_news%5D=39029&tx_ttnews%5BbackPid%5

D=13&cHash=2a0d1f93a94480e3a687c82e8085bdf4 59

Low growth trap is a state, where the economy fails to grow because of high debt-GDP ratio, particularly

when its crosses 90% of the GDP. During a study, it was noted that in 1990s, the Japanese economy witnessed a

90 % debt-GDP ratio, hence, Japan witnessed

world where great-power rivalry is still active. However, after the end of Saddam Hussein and

the sweeping changes brought about by the Arab Spring, Russo-Chinese influence in the

Persian Gulf has started waning significantly.

The demand for regime change in Syria, agitation against the potential Iranian nuclear threat

and the bogey of “Shiite Spring” in the Gulf, has considerably altered the geo-politics of the

region. The delisting of Syria from Russia’s sphere of influence will not only take away Russia’s

strategic warm water foothold but also oust it completely from the region. If the opposition in

Syria achieves success, Russia’s disturbed areas like Chechnya-Ingushia and Dagestan may

come in for more serious attacks by the hardliners.

Although China has no such obvious high geo-strategic stakes in the region, some of its

“prime” national interests such as energy security, trade and investment opportunities are

important. In alliance with Iran, China likely wants to hedge its long-term energy supply from

Iraq as well. Association with Russia may also be helpful to China to nurture bonhomie on

Central Asian issues and bring both the countries to work, share and shape the “evolving”

future world order.

The Russia-China alliance in West Asia, although seems for the immediate reason of providing

“diplomatic cover” to the al-Asad regime in the UN, it is possible that their alliance is tactically

imbued with laying down the foundation of a future global order. They also want to make sure

that their presence in global affairs counts, so that they may not lose their allies forever.

The portents are that the game started in West Asia will endure in other parts of the world.

Russia and China are aware of that change is destined; however, they are trying to maintain

and secure their interest to such an extent that their own growth and stability may not be

jeopardized.

In a broader setting, the Syrian episode seemly purports an intended move of China and

Russia to set a foreign policy precedent to effectively hedge their national interests,

particularly in the regions harbouring their national interests and prevent the possibility of

insinuation of “localised” version of cold war in the 21st century. The likely areas of the

beginning of localised version of cold war seems to be the West Asia, the Pacific region and

next the African Continent. The present Syrian case looks nothing but a “preventive

diplomatic” actuation of the two powers against the US-West and its allies.

Whatever may be the outcome of this stalemate, but one thing is definite that the post- Basher

era may vandalise Syria to an extent that geo-strategically it might not be significant for it to

play any decisive or strategic role in the foreseeable future in the region. The dismemberment

of the country on ethnic and sectarian lines, similar to Iraq, may also not be ruled out. This

will, nonetheless, satisfy the major powers; however, the region will hardly be able to heel up

with its territorial scars.

About the author Dr. Zakir Hussain is Research Fellow at Indian Council of World Affairs, Sapru House, New Delhi, India. He has a vast experience on Gulf issues, including the political economy, geopolitics and geostrategic affairs of the region. This paper has been written nine months earlier. Due to some reason it could not be put on the web. Misnomer: Views expressed in this monograph are of the author, ICWA has nothing to do with the author personal opinion.