singapore’s experience in economic development · 2017-07-14 · singapore’s experience in...

TRANSCRIPT

Singapore’s Experience in Economic Development

Panama Conference

Where the World Meets

24 Feb 2011

by Philip YeoSpecial Advisor for Economic Development,

Prime Minister's Office, Government of Singapore

and

Chairman, SPRING Singapore

• Early accounts showed Singapore has been a trading post since 13th century.

• Modern Singapore was founded in 1819 by Sir Stamford Raffles o Spore became centre of govt for

the British Straits Settlements and later a Crown Colony

o Blossomed as a free port trading with India, China, Europe and US

• Occupied by Japan during WWII from 1942-45

• Continued to be key trading hub through and after the war

• Attained self-government in 1959, joined Malaysia in 1963 and finally became an independent nation in 1965

Singapore: A Free Port from 1819

2

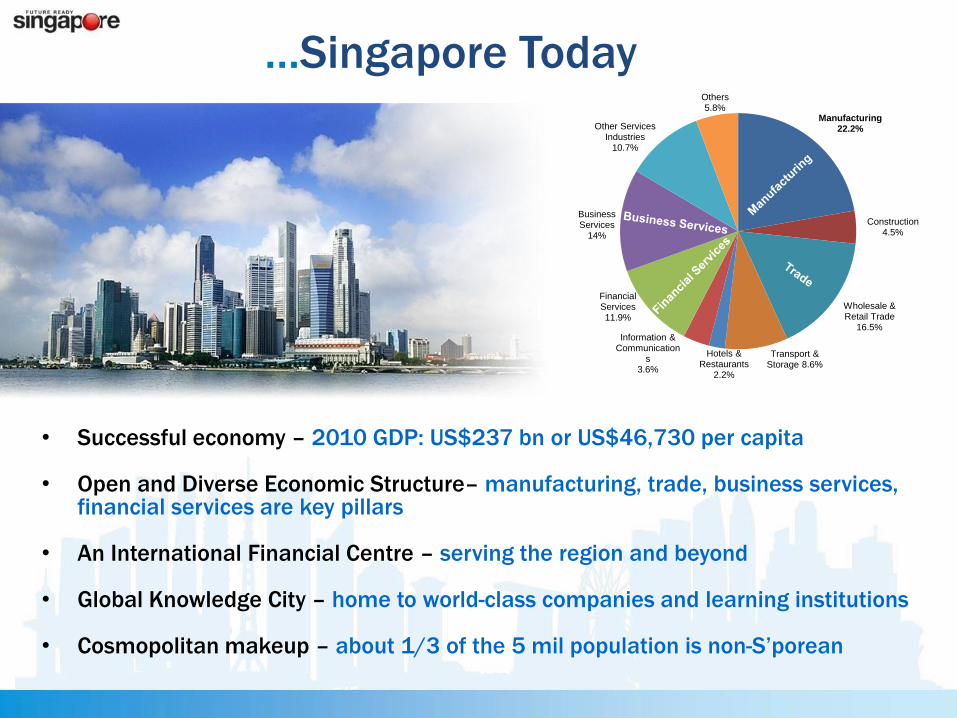

Singapore …Singapore Today

• Successful economy – 2010 GDP: US$237 bn or US$46,730 per capita

• Open and Diverse Economic Structure– manufacturing, trade, business services, financial services are key pillars

• An International Financial Centre – serving the region and beyond

• Global Knowledge City – home to world-class companies and learning institutions

• Cosmopolitan makeup – about 1/3 of the 5 mil population is non-S’porean

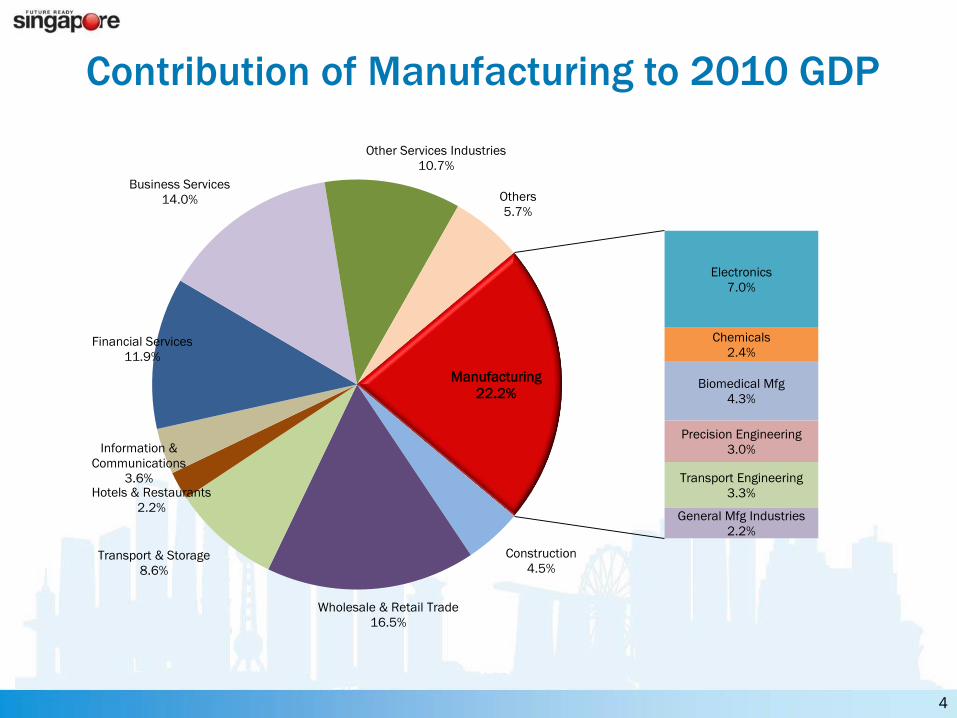

Manufacturing 22.2%

Construction 4.5%

Wholesale & Retail Trade

16.5%

Transport & Storage 8.6%

Hotels & Restaurants

2.2%

Information & Communication

s 3.6%

Financial Services 11.9%

Business Services

14%

Other Services Industries

10.7%

Others5.8%

Construction

4.5%

Wholesale & Retail Trade

16.5%

Transport & Storage

8.6%

Hotels & Restaurants

2.2%

Information &

Communications

3.6%

Financial Services

11.9%

Business Services

14.0%

Other Services Industries

10.7%

Others

5.7%

Electronics

7.0%

Chemicals

2.4%

Biomedical Mfg

4.3%

Precision Engineering

3.0%

Transport Engineering

3.3%

General Mfg Industries

2.2%

Manufacturing

22.2%

Contribution of Manufacturing to 2010 GDP

4

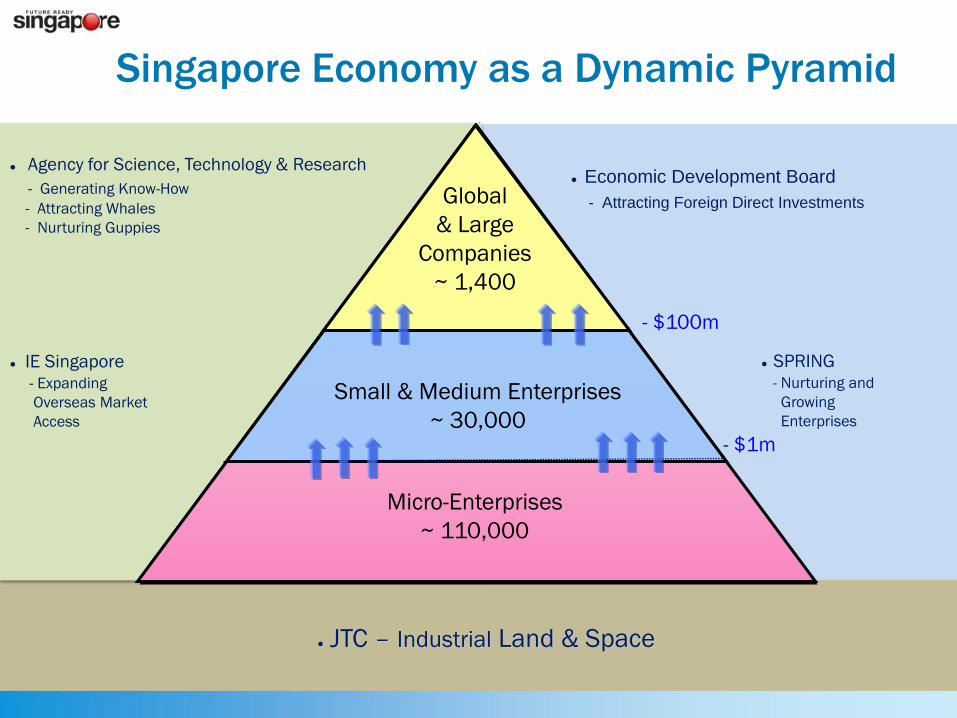

● Agency for Science, Technology & Research

- Generating Know-How

- Attracting Whales

- Nurturing Guppies

● IE Singapore

- Expanding

Overseas Market

Access

● Economic Development Board

- Attracting Foreign Direct Investments

Small & Medium Enterprises

~ 30,000

Micro-Enterprises

~ 110,000

Global

& Large

Companies

~ 1,400

● SPRING

- Nurturing and

Growing

Enterprises

- $1m

- $100m

● JTC – Industrial Land & Space

Singapore Economy as a Dynamic Pyramid

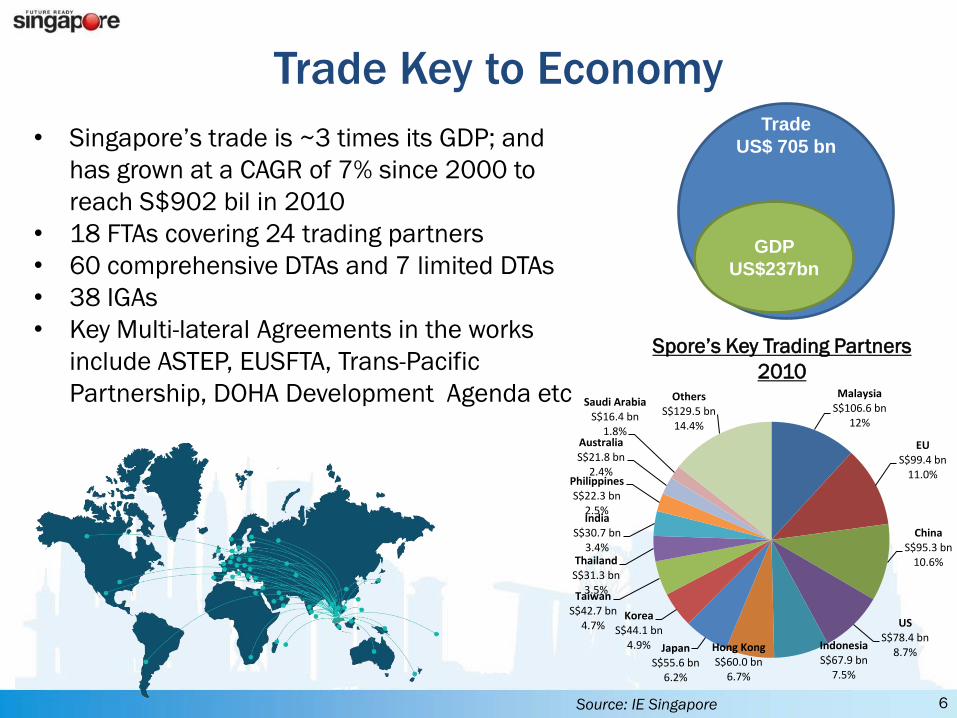

Trade

US$ 705 bn

GDP

US$237bn

• Singapore’s trade is ~3 times its GDP; and

has grown at a CAGR of 7% since 2000 to

reach S$902 bil in 2010

• 18 FTAs covering 24 trading partners

• 60 comprehensive DTAs and 7 limited DTAs

• 38 IGAs

• Key Multi-lateral Agreements in the works

include ASTEP, EUSFTA, Trans-Pacific

Partnership, DOHA Development Agenda etc

Trade Key to Economy

6

MalaysiaS$106.6 bn

12%

EUS$99.4 bn

11.0%

ChinaS$95.3 bn

10.6%

US S$78.4 bn

8.7%IndonesiaS$67.9 bn

7.5%

Hong KongS$60.0 bn

6.7%

Japan S$55.6 bn

6.2%

KoreaS$44.1 bn

4.9%

TaiwanS$42.7 bn

4.7%

ThailandS$31.3 bn

3.5%

IndiaS$30.7 bn

3.4%

PhilippinesS$22.3 bn

2.5%

AustraliaS$21.8 bn

2.4%

Saudi Arabia S$16.4 bn

1.8%

OthersS$129.5 bn

14.4%

Spore’s Key Trading Partners

2010

Source: IE Singapore

Top Container Ports in the World

2009 2010

1 Singapore, 25.9M TEU Shanghai, 29.1M TEU

2 Shanghai, 25.0M TEU Singapore, 28.4M TEU

3 Hong Kong, 20.9M TEU Hong Kong, 23.5M TEU

4 Shenzhen, 18.3M TEU Shenzhen, 22.5M TEU

5 Busan, 12.0M TEU Ningbo, 13.1M TEU

6 Guangzhou, 11.2M TEU Busan, 13.0M TEU

7 Dubai, 11.2M TEU Guangzhou, 12.6M TEU

8 Ningbo, 10.5M TEU Qingdao, 12.0M TEU

9 Qingdao, 10.3M TEU Dubai, 11.6M TEU

10 Rotterdam, 9.8M TEU Rotterdam 11.1M TEU

• The Port of Singapore has prospered in tandem with growth in global trade.

• Ranks amongst the busiest ports in the world:o World's #1 port by shipping tonnage

since 1986

o World's #1 container port in 2005 -2009

o World's #1 trans-shipment port

o World's #1 bunkering port since 1988

o World's #1 port by cargo tonnage until 2005, and in 2008

• Trans-shipment accounts for bulk of Singapore’s volume. Wide variety of cargo types, with multiple destinations

Singapore Port

7

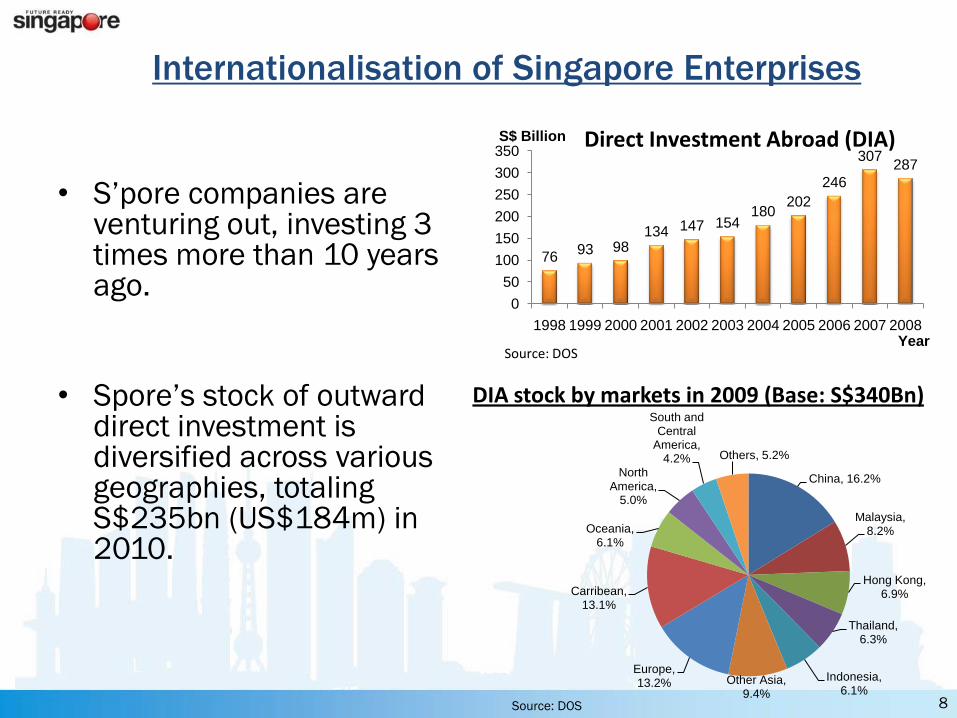

• S’pore companies are venturing out, investing 3 times more than 10 years ago.

• Spore’s stock of outward direct investment is diversified across various geographies, totaling S$235bn (US$184m) in 2010.

Internationalisation of Singapore Enterprises

8

7693 98

134 147 154180

202

246

307287

0

50

100

150

200

250

300

350

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

S$ Billion

Year

Direct Investment Abroad (DIA)

Source: DOS

China, 16.2%

Malaysia, 8.2%

Hong Kong, 6.9%

Thailand, 6.3%

Indonesia, 6.1%

Other Asia, 9.4%

Europe, 13.2%

Carribean, 13.1%

Oceania, 6.1%

North America,

5.0%

South and Central

America, 4.2% Others, 5.2%

Source: DOS

DIA stock by markets in 2009 (Base: S$340Bn)

Development of Singapore Industries

9

0

1960

5000

10000

15000

20000

25000

30000

35000

40000

1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008

GD

P/C

ap

ita

(U

S$

)

2000s:

Innovation Intensive

90s:

Technology Intensive

80s:

Capital Intensive

70s:

Skills Intensive

60s:

Labour Intensive

GDP per capita

80x in 50 years

Industrial Development Strategies

10

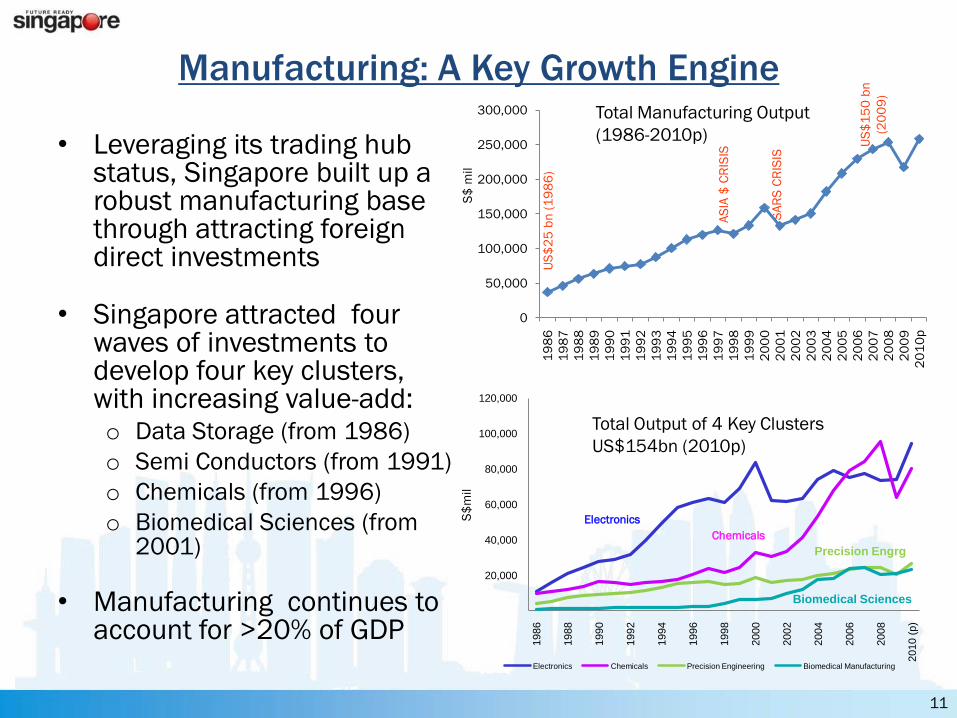

• Leveraging its trading hub status, Singapore built up a robust manufacturing base through attracting foreign direct investments

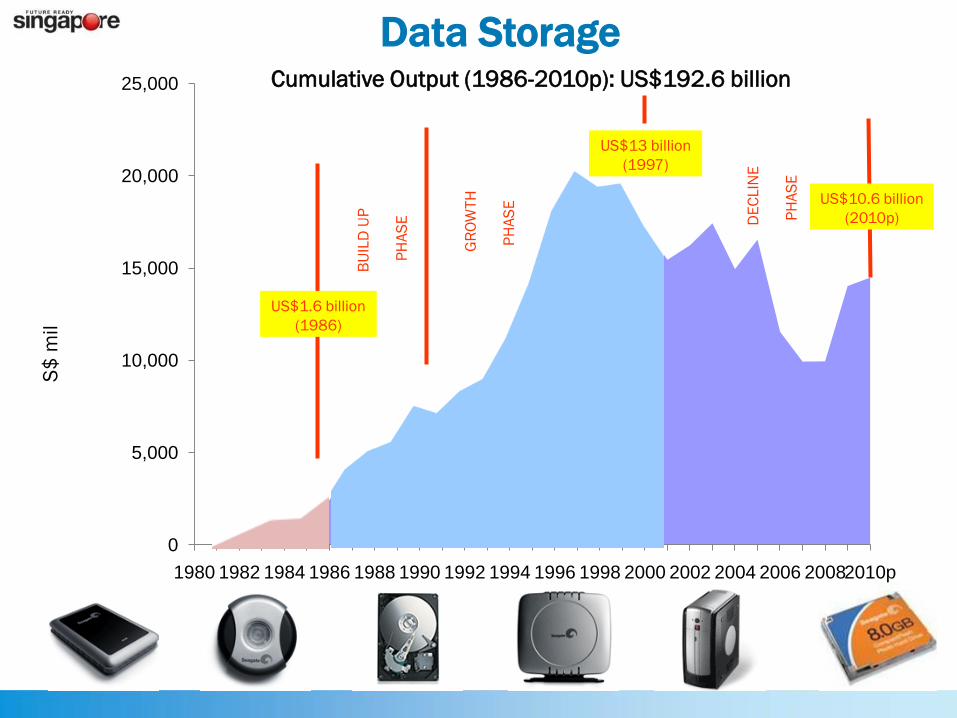

• Singapore attracted four waves of investments to develop four key clusters, with increasing value-add:o Data Storage (from 1986)

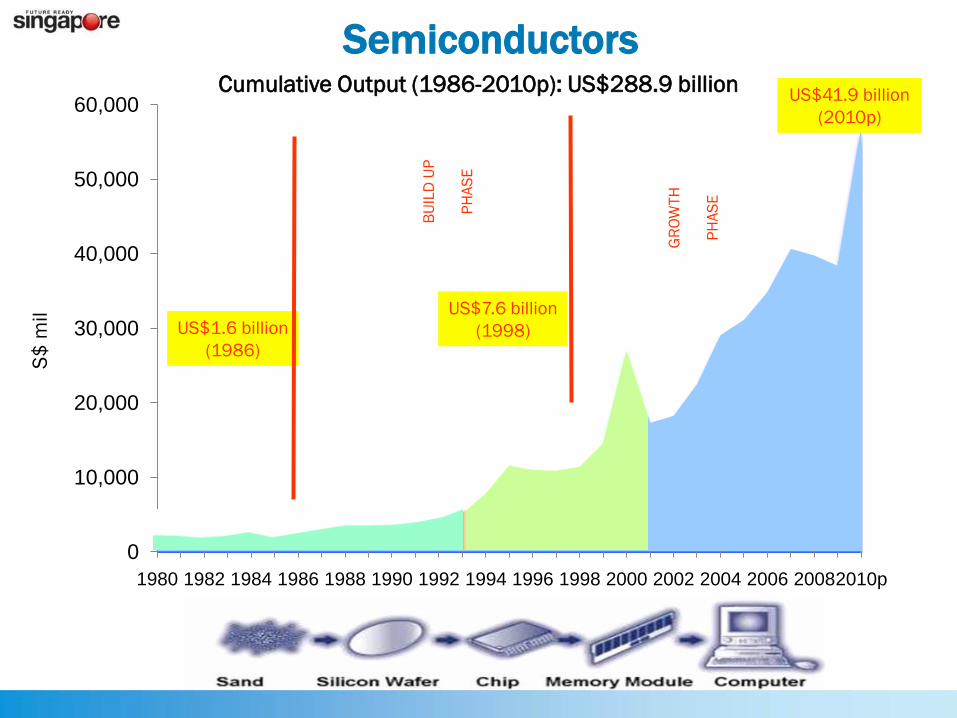

o Semi Conductors (from 1991)

o Chemicals (from 1996)

o Biomedical Sciences (from 2001)

• Manufacturing continues to account for >20% of GDP

Manufacturing: A Key Growth Engine

US

$2

5 b

n (

19

86

)

AS

IA $

CR

ISIS

SA

RS

CR

ISIS

US

$1

50

bn

(20

09

)

S$

mil

Total Manufacturing Output

(1986-2010p)

Total Output of 4 Key Clusters

US$154bn (2010p)

20,000

40,000

60,000

80,000

100,000

120,000

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010 (

p)

Electronics Chemicals Precision Engineering Biomedical Manufacturing

Biomedical Sciences

Precision Engrg

Electronics

Chemicals

S$

mil

11

0

50,000

100,000

150,000

200,000

250,000

300,000

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

p

Cumulative Output (1986-2010p): US$192.6 billion

0

5,000

10,000

15,000

20,000

25,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 20082010p

DE

CLIN

E

PH

AS

E

US$10.6 billion

(2010p)

S$

mil

GR

OW

TH

PH

AS

E

BU

ILD

UP

PH

AS

E

US$1.6 billion

(1986)

US$13 billion

(1997)

Data Storage

0

10,000

20,000

30,000

40,000

50,000

60,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 20082010p

Cumulative Output (1986-2010p): US$288.9 billion

S$

mil

US$1.6 billion

(1986)

BU

ILD

UP

PH

AS

E

US$7.6 billion

(1998)

GR

OW

TH

PH

AS

E

US$41.9 billion

(2010p)

Semiconductors

5,000

10,000

15,000

20,000

25,000

30,000

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010p

GR

OW

T

H

PH

AS

E

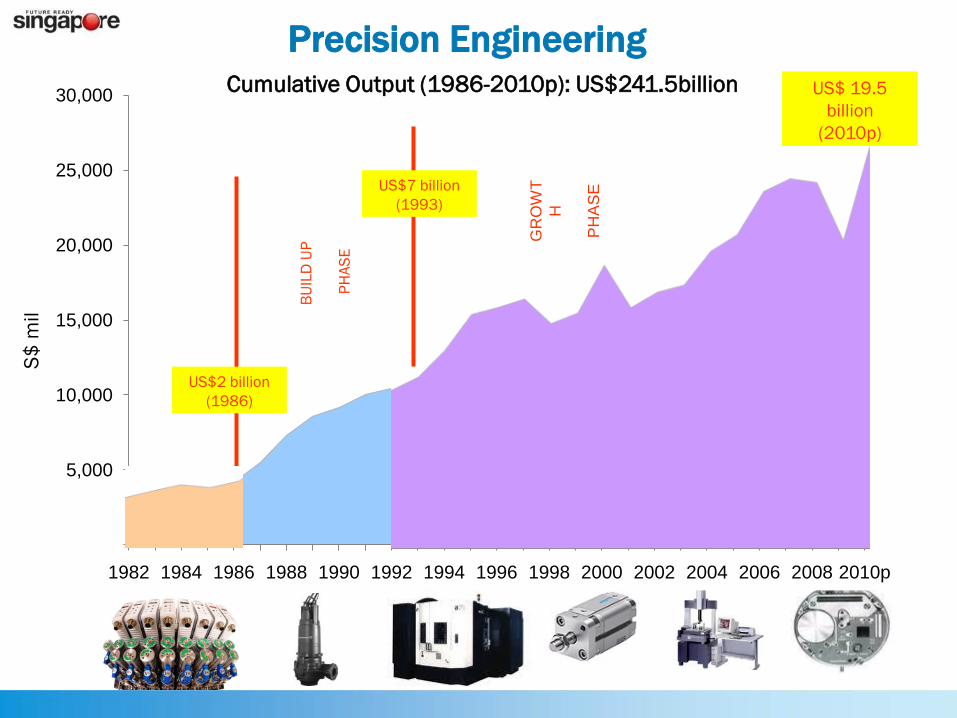

Cumulative Output (1986-2010p): US$241.5billion

US$2 billion

(1986)

BU

ILD

UP

PH

AS

E

US$7 billion

(1993)

US$ 19.5

billion

(2010p)

S$

mil

Precision Engineering

S$ m

il

0

20,000

40,000

60,000

80,000

100,000

120,000

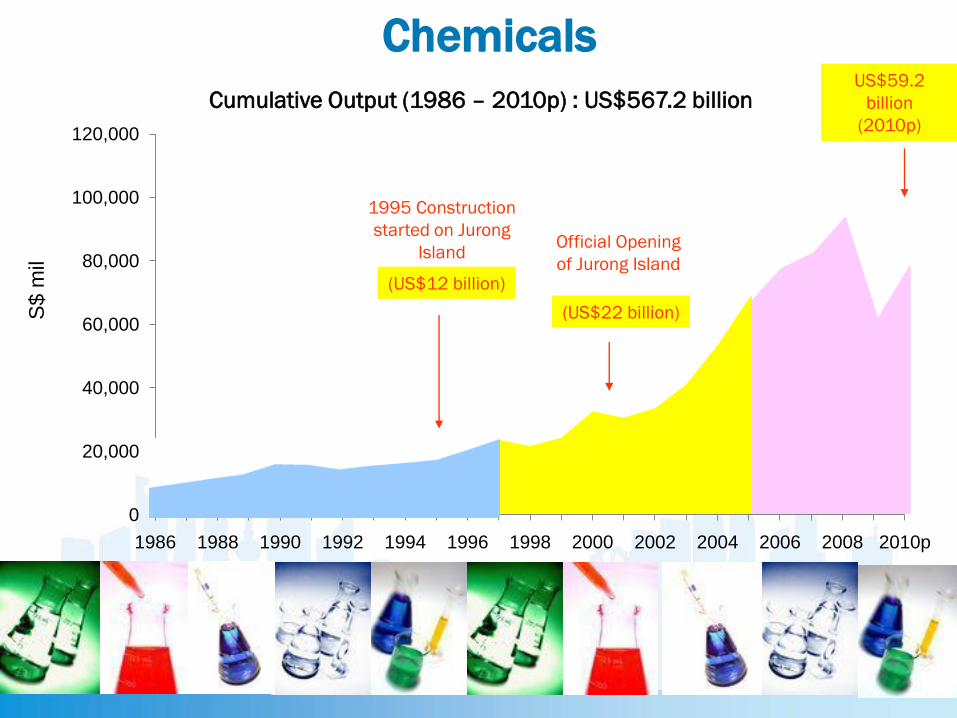

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010p

1995 Construction

started on Jurong

Island

(US$12 billion)

Official Opening

of Jurong Island

(US$22 billion)

US$59.2

billion

(2010p)

Chemicals

Cumulative Output (1986 – 2010p) : US$567.2 billion

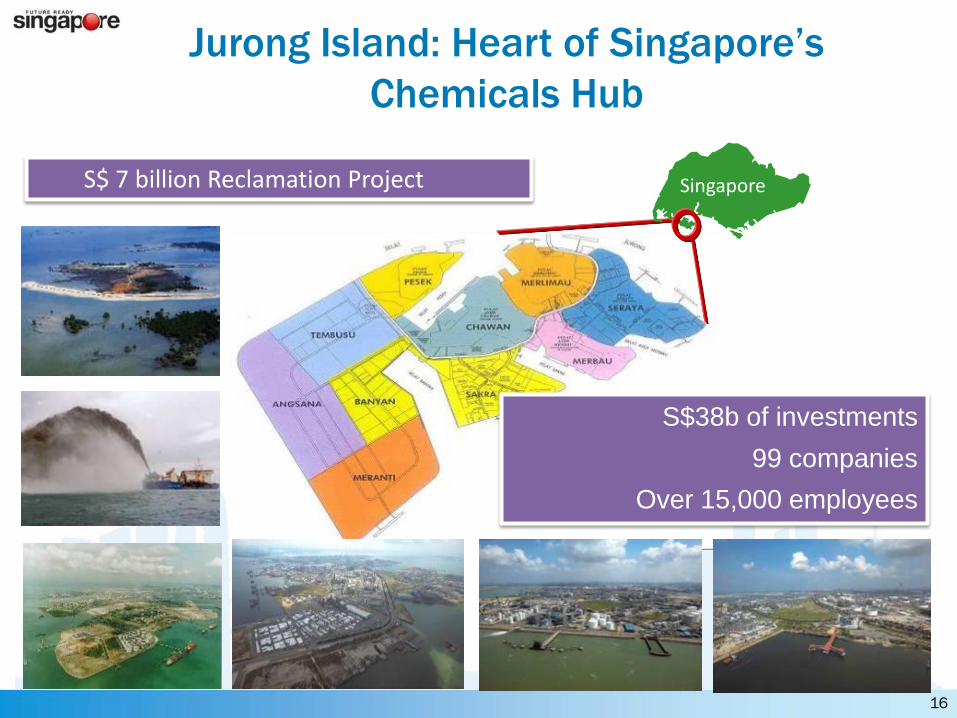

SingaporeS$ 7 billion Reclamation Project

S$38b of investments

99 companies

Over 15,000 employees

Jurong Island: Heart of Singapore’s

Chemicals Hub

16

0

5,000

10,000

15,000

20,000

25,000

30,000

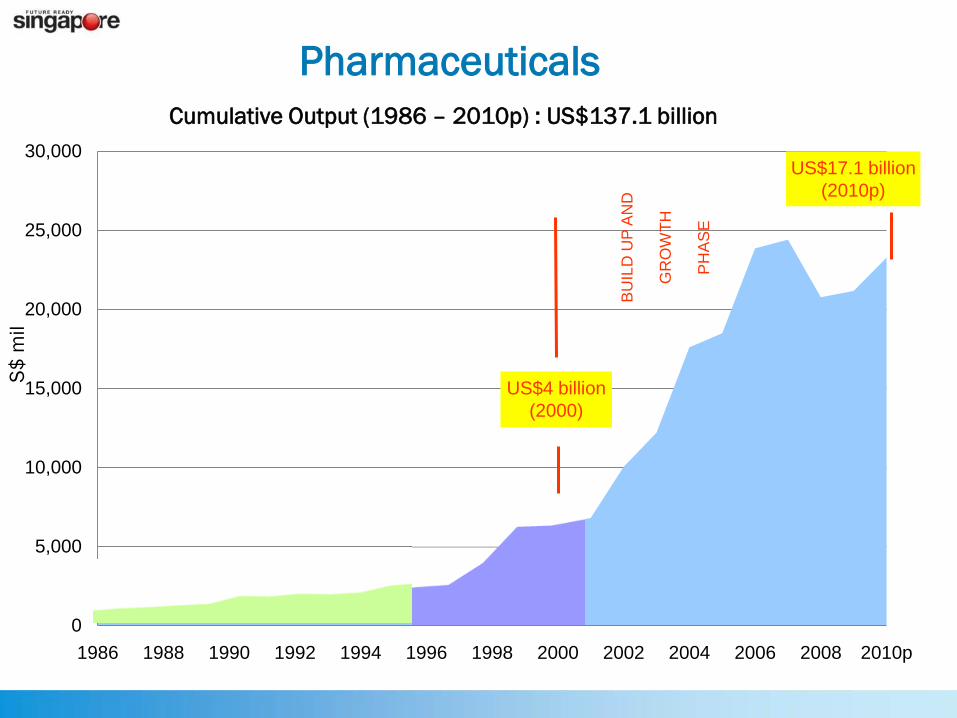

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010p

US$4 billion

(2000)

BU

ILD

UP

AN

D

GR

OW

TH

PH

AS

E

US$17.1 billion

(2010p)

Cumulative Output (1986 – 2010p) : US$137.1 billion

Pharmaceuticals

S$

mil

18

Tuas Pharma Park

Developing Singapore as a Global

Hub for Knowledge and Innovation

19

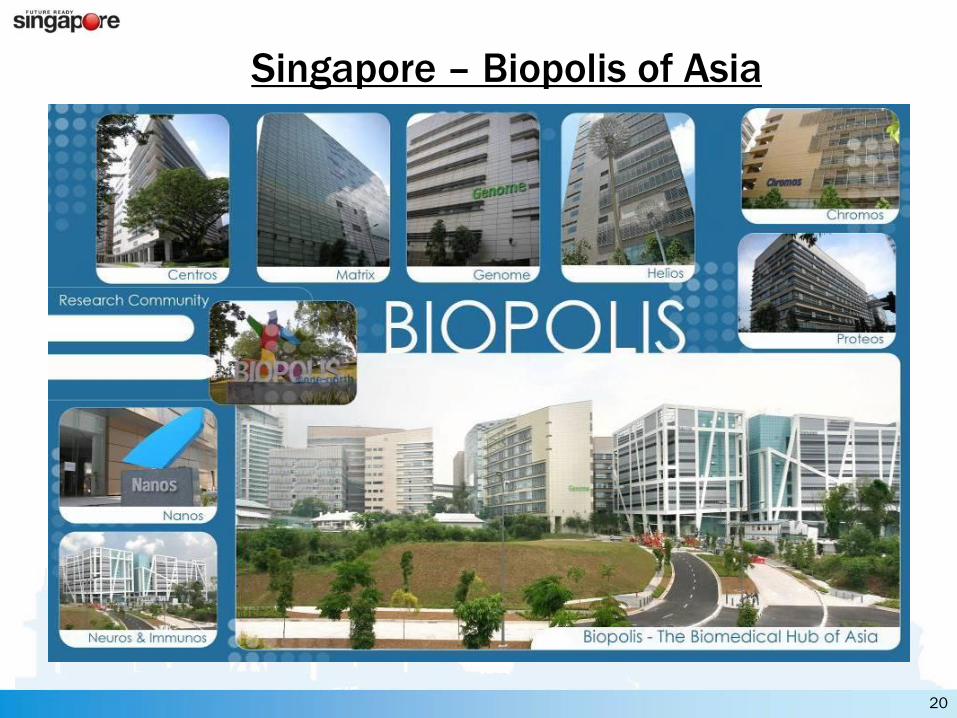

Singapore – Biopolis of Asia

20

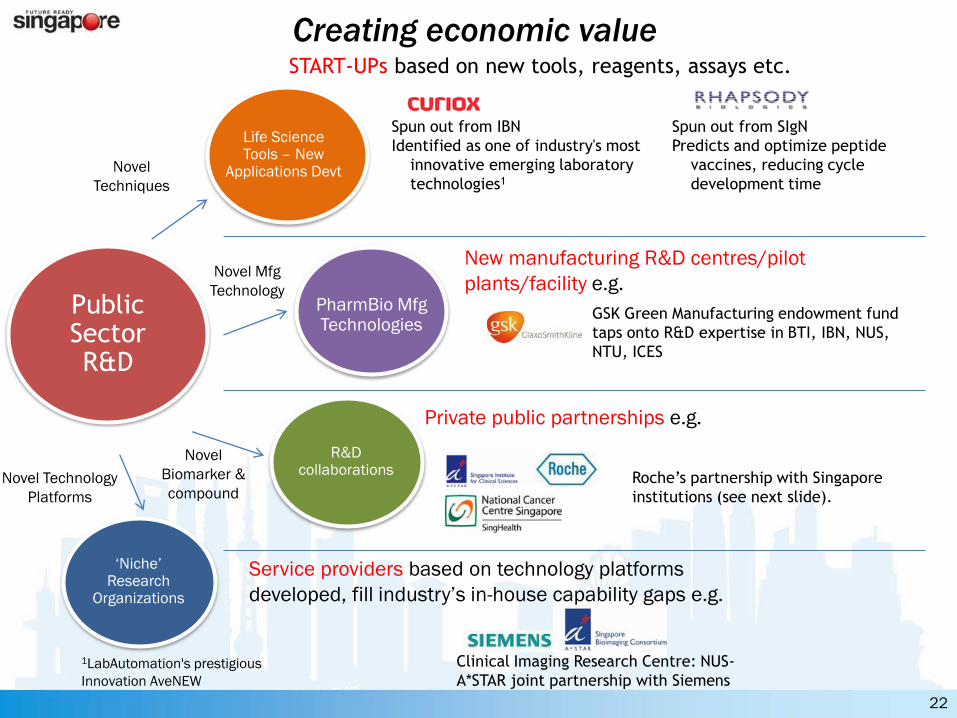

Creating economic value

22

Public Sector R&D

Novel

Techniques

Life Science Tools – New

Applications Devt

‘Niche’ Research

Organizations

Novel Technology

Platforms

New manufacturing R&D centres/pilot

plants/facility e.g. PharmBio Mfg Technologies

Novel Mfg

Technology

1LabAutomation's prestigious

Innovation AveNEW

Spun out from IBN

Identified as one of industry's most

innovative emerging laboratory

technologies1

Spun out from SIgN

Predicts and optimize peptide

vaccines, reducing cycle

development time

GSK Green Manufacturing endowment fund

taps onto R&D expertise in BTI, IBN, NUS,

NTU, ICES

Service providers based on technology platforms

developed, fill industry’s in-house capability gaps e.g.

Roche’s partnership with Singapore

institutions (see next slide).

R&D collaborations

Novel

Biomarker &

compound

START-UPs based on new tools, reagents, assays etc.

Private public partnerships e.g.

Clinical Imaging Research Centre: NUS-

A*STAR joint partnership with Siemens

Fusionopolis Facilities

Fitness Gym & Pool

Retail and F&B Podium

SharedConference Rooms

one-north MRT Station

Business andResearch Space

Skybridges and SkyGardens

Serviced Work-Live Apartments

500-seatExperimental Performance Theatre

23

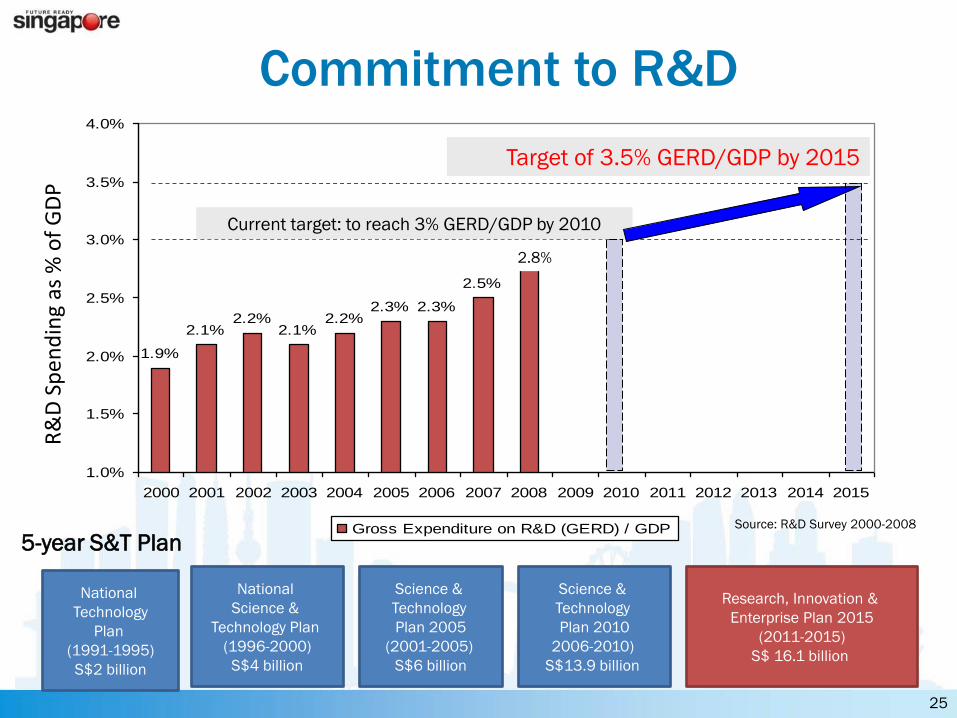

1.9%

2.1%2.2%

2.1%2.2%

2.3% 2.3%

2.5%

2.8%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Gross Expenditure on R&D (GERD) / GDP Source: R&D Survey 2000-2008

R&

D S

pe

nd

ing

as %

of

GD

P

Science &

Technology

Plan 2010

2006-2010)

S$13.9 billion

Science &

Technology

Plan 2005

(2001-2005)

S$6 billion

National

Science &

Technology Plan

(1996-2000)

S$4 billion

National

Technology

Plan

(1991-1995)

S$2 billion

5-year S&T Plan

Current target: to reach 3% GERD/GDP by 2010

Research, Innovation &

Enterprise Plan 2015

(2011-2015)

S$ 16.1 billion

Target of 3.5% GERD/GDP by 2015

2.8%

Commitment to R&D

25

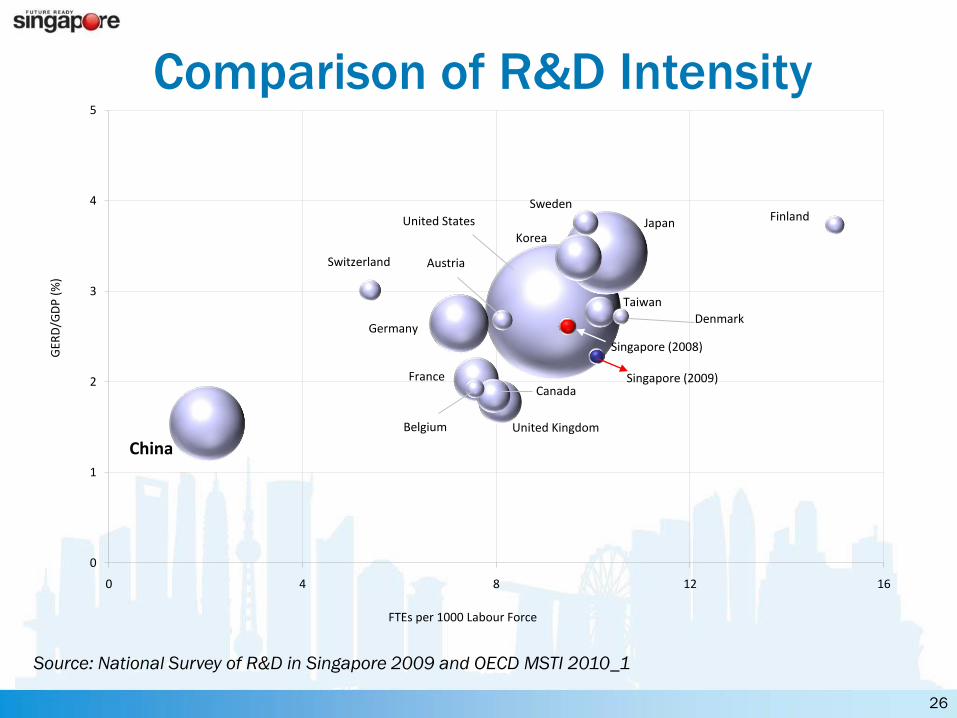

Comparison of R&D Intensity

Source: National Survey of R&D in Singapore 2009 and OECD MSTI 2010_1

United States Japan

Germany

Korea

France

United Kingdom

Canada

Taiwan

Sweden

Switzerland Austria

Belgium

Finland

Singapore (2009)

Denmark

Singapore (2008)

0

1

2

3

4

5

0 4 8 12 16

GER

D/G

DP

(%

)

FTEs per 1000 Labour Force

China

26

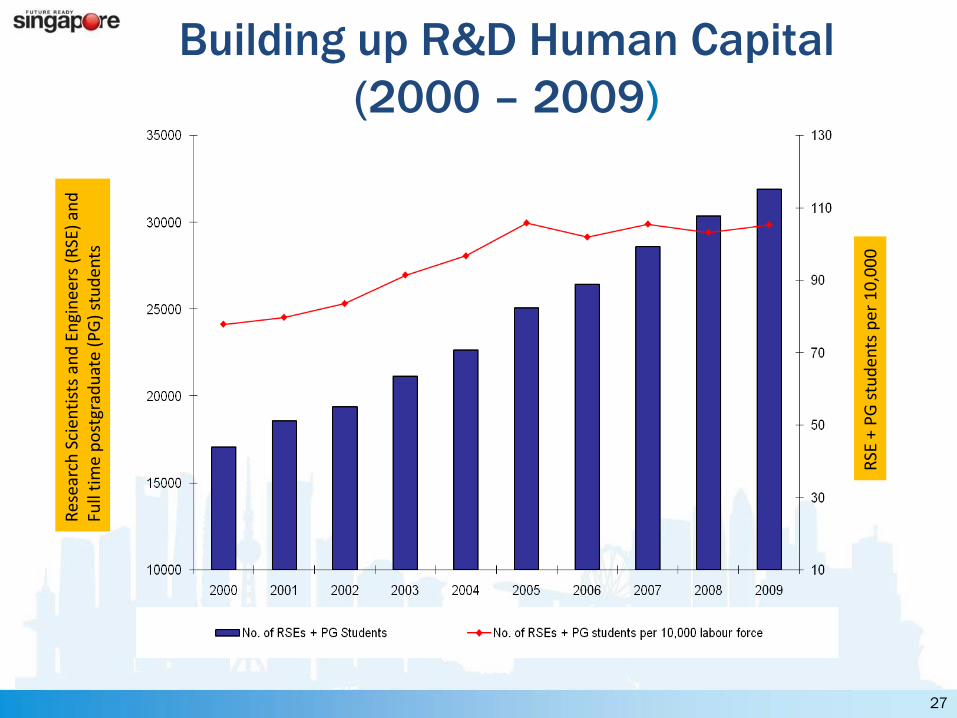

Res

earc

h S

cien

tist

s an

d E

ngi

nee

rs (

RSE

) an

dFu

ll ti

me

po

stgr

adu

ate

(PG

) st

ud

ents

RSE

+ P

G s

tud

ents

per

10

,00

0

Building up R&D Human Capital

(2000 – 2009)

27

Prof David

Townsend

Head of PET and SPECT

Group, SBIC

Dr Stephen

Cohen

Acting Exec Dir,

IMCB

Attracting International

Scientific Talent

Dr Edison Liu

Exec Dir, GIS

Dr Davor Solter

PI, IMB

Sir David Lane

Chief Scientist

Dr Birgitte Lane

Exec Dir, IMB

Dr Phil Ingham

Dy Dir, IMCB

Dr Jean Paul

Thiery

Dy Dir, IMCB

Dr Edward Holmes

Executive Dy Chmn (TCSG),

BMRC &

Chmn, NMRC

Dr Judith

Swain

Exec Dir, SICS

Dr Philippe

Kourilsky Chairman,

SIgN

Prof Peter Gluckman

PI, SICS

Sir George Radda

Chmn, BMRC

Dr Jackie Ying

Exec Dir, IBN

Dr Alan Colman

Exec Dir, SSCC

Dr Dale Purves

Exec Dir, NRP

Dr Frank

Eisenhaber

Director, BII

Prof Paola

Castagnoli

Scientific Dir,

SIgN

Prof Charles

Zukoski

Chmn, SERC

Dr Sydney Brenner

Scientific Adviser,

A*STAR

Dr Keith Carpenter

Exec Dir, ICES

Prof Dim-Lee

Kwong

Exec Dir, IME

Prof Stephen Quake

Consultant

Dr David Srolovitz

Exec Dir, IHPC

Dr Alex Matter

Director, ETC

Dr Pantelis

Alexopoulis,

Exec Dir, DSI

29

Guppy – 0.03 meters

Human Capital –

Train 1,000 PhD Guppies

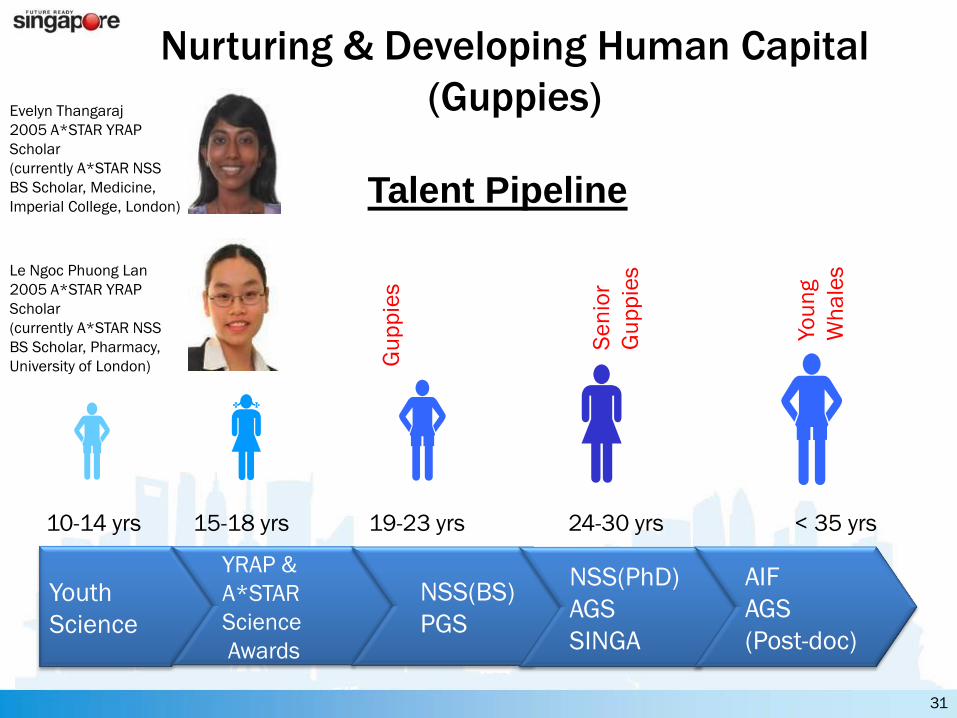

30

Youth

Science

YRAP &

A*STAR

Science

Awards

NSS(BS)

PGS

NSS(PhD)

AGS

SINGA

AIF

AGS

(Post-doc)

10-14 yrs < 35 yrs15-18 yrs 19-23 yrs 24-30 yrs

Talent Pipeline

Gu

pp

ies

Se

nio

r

Gu

pp

ies

Yo

un

g

Wh

ale

sLe Ngoc Phuong Lan

2005 A*STAR YRAP

Scholar

(currently A*STAR NSS

BS Scholar, Pharmacy,

University of London)

Evelyn Thangaraj

2005 A*STAR YRAP

Scholar

(currently A*STAR NSS

BS Scholar, Medicine,

Imperial College, London)

Nurturing & Developing Human Capital

(Guppies)

31

MIT

Physics

(Malaysia)

Stanford

Chemical Engineering

(Shanghai)

MIT

Bio Engineering

(Hong Kong)

Stanford

Computer Science

(India)

MIT

Chemical Engineering

(Vietnam)

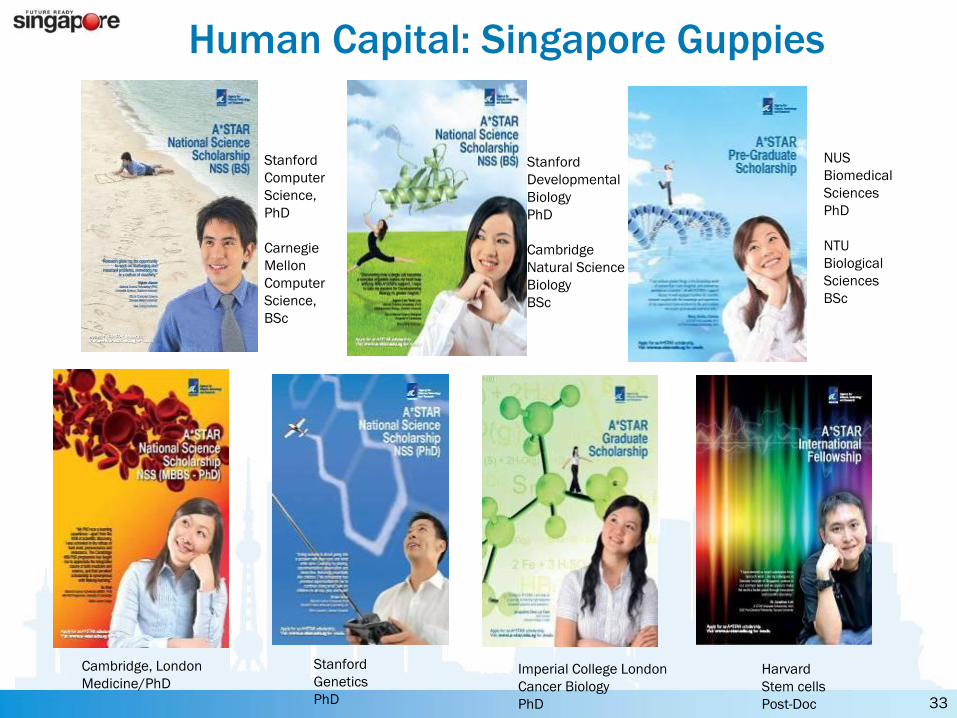

Human Capital: International Guppies

32

Harvard

Stem cells

Post-Doc

Stanford

Computer

Science,

PhD

Carnegie

Mellon

Computer

Science,

BSc

Stanford

Developmental

Biology

PhD

Cambridge

Natural Science

Biology

BSc

Cambridge, London

Medicine/PhD

Stanford

Genetics

PhD

Imperial College London

Cancer Biology

PhD

NUS

Biomedical

Sciences

PhD

NTU

Biological

Sciences

BSc

Human Capital: Singapore Guppies

33

Singapore as a Financial

Centre for the Region

34

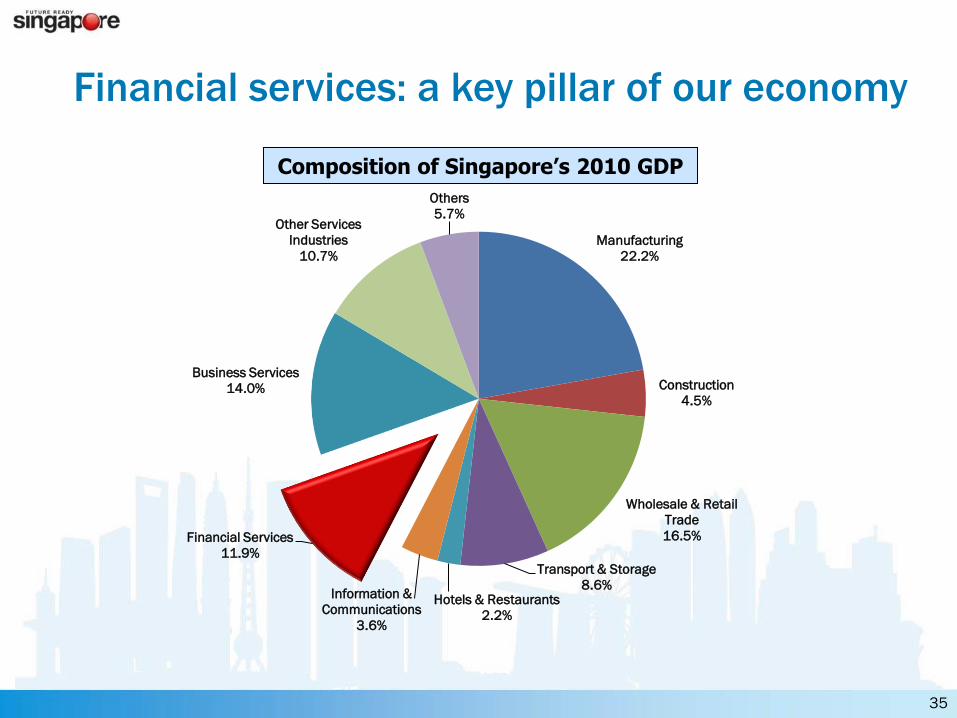

Financial services: a key pillar of our economy

35

Composition of Singapore’s 2010 GDP

Manufacturing

22.2%

Construction

4.5%

Wholesale & Retail

Trade

16.5%

Transport & Storage

8.6%Hotels & Restaurants

2.2%

Information &

Communications

3.6%

Financial Services

11.9%

Business Services

14.0%

Other Services

Industries

10.7%

Others

5.7%

International Financial Centre

Supporting Asia’s Growth Needso Financing for international corporates

o Financing for growing trade flows

o Risk Management for commodity trading in Asia

o Financing for the maritime sector

36

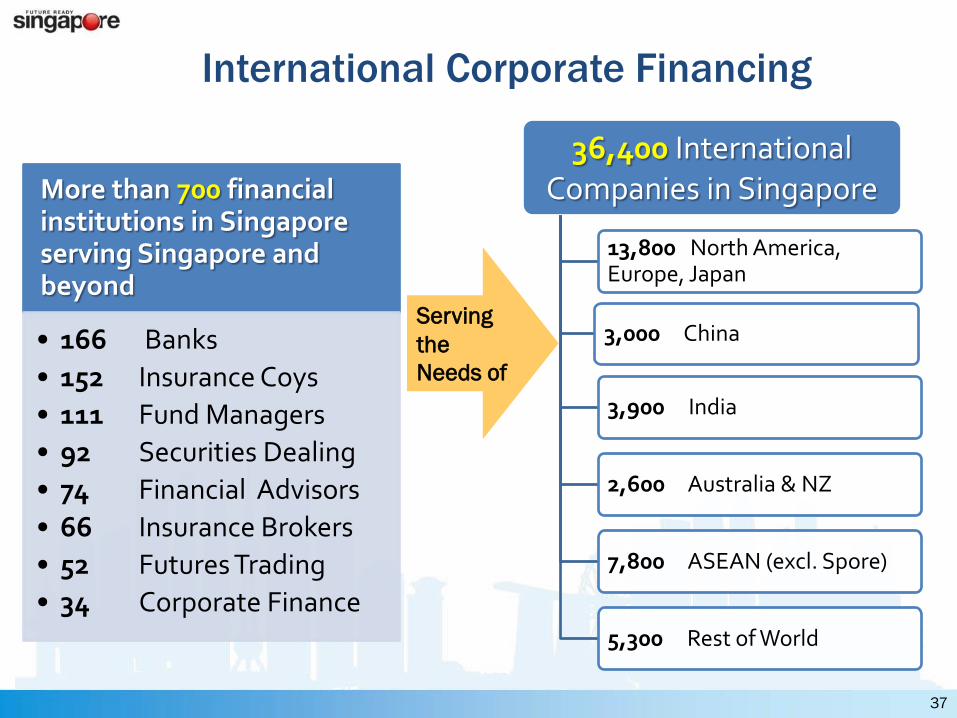

International Corporate Financing

37

Serving

the

Needs of

36,400 InternationalCompanies in Singapore

13,800 North America, Europe, Japan

3,000 China

3,900 India

2,600 Australia & NZ

7,800 ASEAN (excl. Spore)

5,300 Rest of World

More than 700 financial institutions in Singapore serving Singapore and beyond

• 166 Banks

• 152 Insurance Coys

• 111 Fund Managers

• 92 Securities Dealing

• 74 Financial Advisors

• 66 Insurance Brokers

• 52 Futures Trading

• 34 Corporate Finance

38

Source – MAS (assuming SGD/USD of 1.3)

Regional Loan Financing Centre

Total loans extended by Singapore-based banks have tripled over the last 20 years. 2/3 of that is dominated in foreign currencies.

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Tota

l lo

an

s (

US

D)

Millio

n

Regional Corporate Treasury & Cash Management Hub

Corporate Treasuries - Demand for Products to Hedge Financial (such as Currency, Interest Rate) Risks

Largest FX and OTC derivatives market

in Asia ex-Japanwith average daily turnover of

> US$300bn

Source: MAS

Leading FX teams in Singapore

39

40

Risk Management for commodities

Asian HQ for global banks’

commodity derivatives trading

Access to Trading and Clearing

Infrastructure

Largest Commodity Derivatives

Hub in the Asia-Pacific

Asian Trading Hub for Agri-Commodities

World’s Third Largest Energy

Trading Hub

Financing Trade Flows

Source: Global Insight, WTO, Oliver Wyman

US$ BN2008 ► 2020(CAGR)1

North America South and Central America Europe Africa Asia

3,702

► 10,763

(9%)

4,479

► 7,171

(4%)

616

► 829

(3%)

1378 ► 2,475

(5%)

998 ► 2.247

(7%)

134 ► 448

(11%)

864 ►1,306

(4%)

204 ► 1,159

(16%)

184 ► 608

(11%)

137 ► 1,574

(23%)

Leading Trade

Finance teams

Growing Trade Flows

41

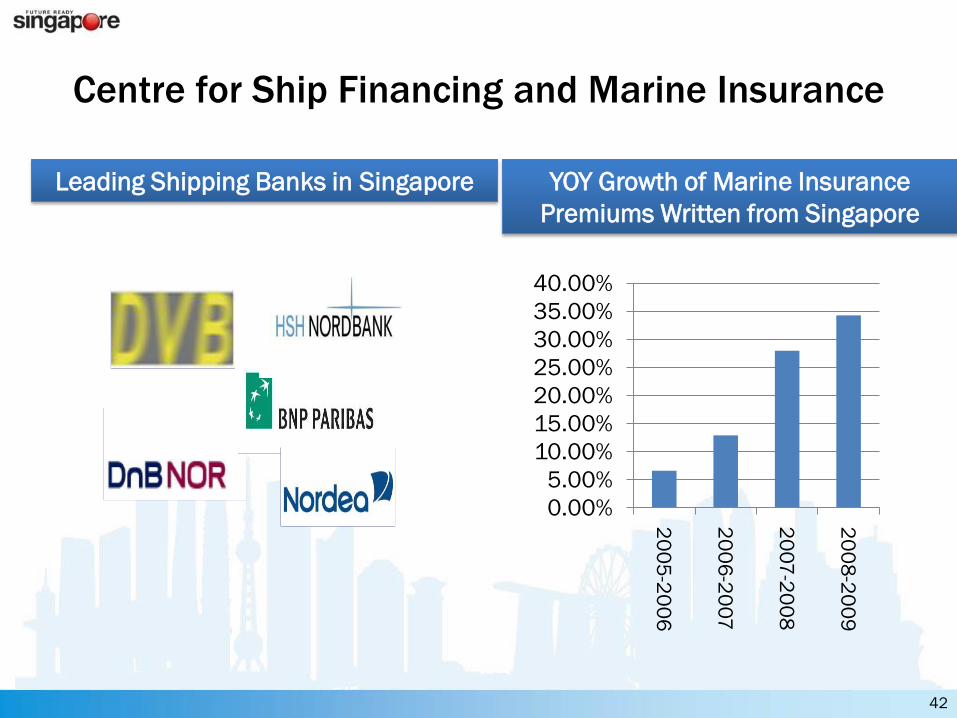

Centre for Ship Financing and Marine Insurance

Leading Shipping Banks in Singapore YOY Growth of Marine Insurance

Premiums Written from Singapore

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%2

00

5-2

00

6

20

06

-20

07

20

07

-20

08

20

08

-20

09

42

Singapore As a Global City

43

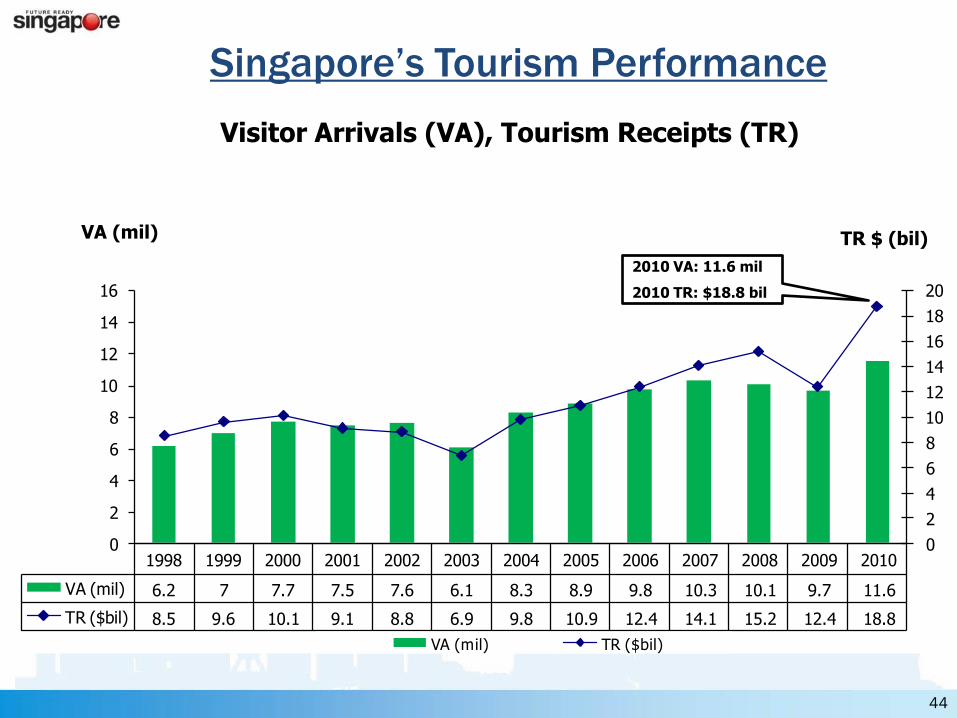

Visitor Arrivals (VA), Tourism Receipts (TR)

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

VA (mil) 6.2 7 7.7 7.5 7.6 6.1 8.3 8.9 9.8 10.3 10.1 9.7 11.6

TR ($bil) 8.5 9.6 10.1 9.1 8.8 6.9 9.8 10.9 12.4 14.1 15.2 12.4 18.8

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

16

VA (mil) TR ($bil)

VA (mil) TR $ (bil)

Singapore’s Tourism Performance

2010 VA: 11.6 mil

2010 TR: $18.8 bil

44

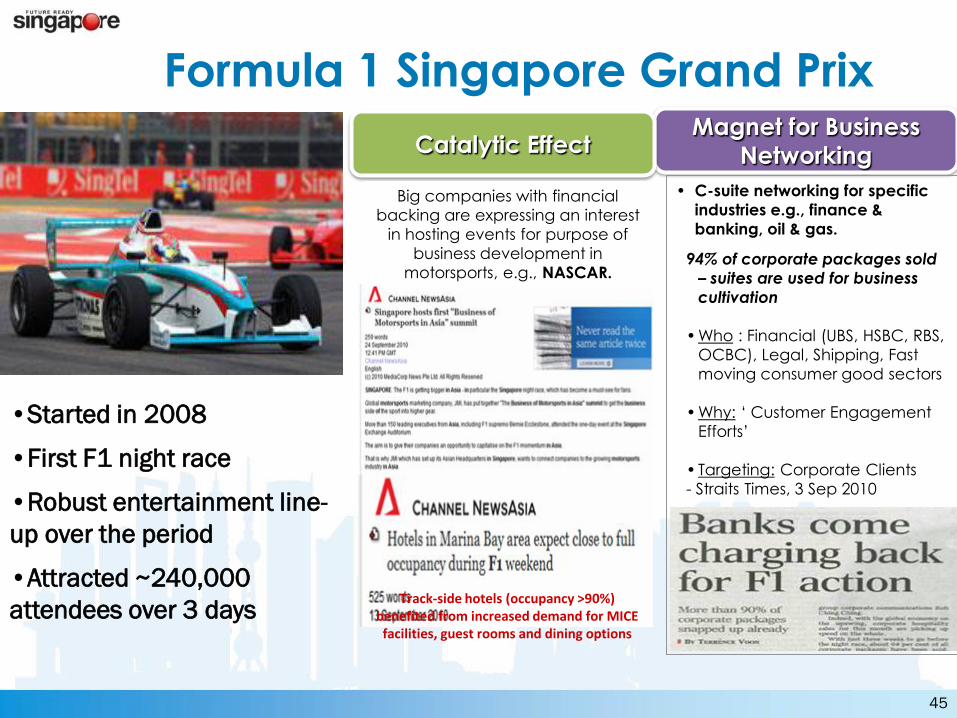

•Started in 2008

•First F1 night race

•Robust entertainment line-

up over the period

•Attracted ~240,000

attendees over 3 days

Formula 1 Singapore Grand PrixMagnet for Business

Networking

• C-suite networking for specific

industries e.g., finance &

banking, oil & gas.

94% of corporate packages sold

– suites are used for business

cultivation

• Who : Financial (UBS, HSBC, RBS,

OCBC), Legal, Shipping, Fast

moving consumer good sectors

• Why: ‘ Customer Engagement

Efforts’

• Targeting: Corporate Clients

- Straits Times, 3 Sep 2010

Catalytic Effect

Big companies with financial

backing are expressing an interest

in hosting events for purpose of

business development in

motorsports, e.g., NASCAR.

Track-side hotels (occupancy >90%) benefited from increased demand for MICE facilities, guest rooms and dining options

45

Opening of Integrated Resorts

• Celebrity Chef Restaurants (e.g. Guy Savoy, Wolfgang Puck, Osia)

• Universal Studios, Singapore

• Musical - Lion King Show • Circus Theatre show - Voyage de La Vie

• Opening in 2011 (Crystal Pavilion, LVMH, ArtScience Museum)

Total = over 120,000sqm of MICE facilities, 3,900 luxury rooms &

suites, over 74,000 sqm of retail

• Flagship and concept stores for global brands (e.g. Louis Vuitton, Chanel)

• Opening in 2011 (Maritime Experiential Museum & Aquarium, Marina Life Park)

• Flagship concept stores of global brands (e.g. Hersheys concept store, first Victoria Secrets store outside US)

46

Sharing Singapore’s Experience

in Urban Solutions

47

• Singapore started to share its town-planning and industry development expertise with other cities from the 1990s

• The early projects included BatamIndustrial Park in Indonesia and Wuxi-Singapore Industrial Park in China

Projects in Other Countries

48

Batam Industrial Park

Wuxi-Singapore Industrial Park

Vietnam Singapore Industrial Park

49

China-Singapore Suzhou Industrial Park

Sino-Singapore Tianjin Eco-City

Bangalore International Technology Park

Key Challenges for Singapore

• Face Global Competition

• Compact and dense urban setting

• Ensuring Economic Competitiveness

• Nurture an Enterprising culture with:

- Passion (Risk taking)

- Determination (Hard work)

- Vision (Global)

- Focus (Operational)

53

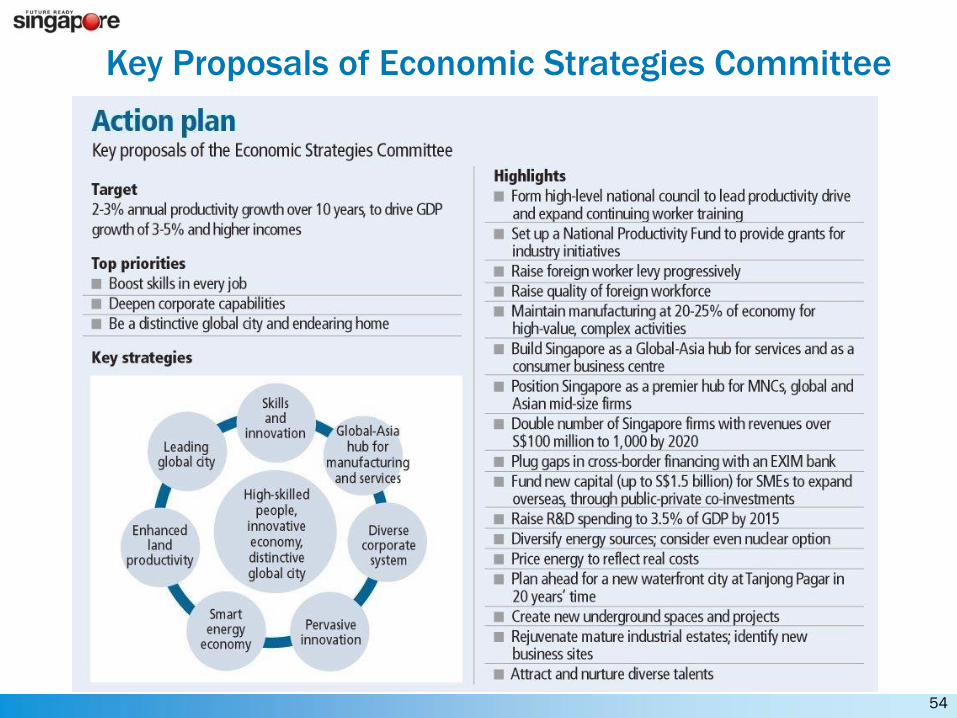

Key Proposals of Economic Strategies Committee

54

• Doubling the National Productivity Fund to S$2 bn (~US$ 1.54 bn)

• Enhanced Productivity and Innovation Credit -- 400% tax deduction for productivity and innovation expenditure , capped at $400,000 for each category

• Further Increases in Foreign Worker Levy, by between $60 and $200

Budget 2011 - Boosting Skills and Productivity

55