simplifying federal taxes: the advantages of … advantages of consumption-based taxation ... 20,000...

TRANSCRIPT

This year’s $1.35 trillion tax cut reduced incometax rates and modestly liberalized the tax rules forretirement saving plans. However, the new tax lawdid not slow the progression of the tax code towardincreasing levels of complexity. In fact, the law made441 changes to the tax code and created a compli-cated series of phase-in periods for tax changes.Meanwhile, the congressional Joint Committee onTaxation released a 1,300-page study cataloging theexcessive complexity of federal taxes but providingonly limited proposals for reform.

Minor simplification reforms will not beenough. The tax system is caught in a spiral ofcontinual change and nonstop growth in rules.Since the mid-1980s there have been 7,000 feder-al tax code changes and a 74 percent increase inthe number of pages of tax rules. Complyingwith federal tax requirements wastes 6 billionhours each year as families and businesses fillout tax forms, keep records, and learn tax rules.

The key factor that causes rising income taxcomplexity is that the tax base is inherently diffi-cult to measure. The Haig-Simons measure ofincome favored by many academic theorists iseconomically damaging and too impractical to

use in the real world. As a result, policymakershave fallen back on ad hoc and inconsistent rulesto define the income tax base. That intensifiescomplexity and creates instability as policymak-ers gyrate between different definitions of the taxbase. In addition, the lack of a consistentlydefined tax base increases the use of the tax codefor special-interest tax breaks, thus furtheradding to the system’s complexity.

The complexity and inefficiency of the indi-vidual and corporate income taxes have led togreat interest in replacing them with a consump-tion-based tax. The leading consumption-basedtax proposals, including the national retail salestax and the Hall-Rabushka flat tax, could dra-matically simplify federal taxation. Those tax sys-tems would eliminate many of the most complexaspects of federal taxation, including deprecia-tion accounting and capital gains taxation.

Imposing the largest federal tax on incomewas a historic mistake: no simple, efficient, andstable measure of income has been found in ninedecades of the income tax. It is time to recognizethis mistake and replace the income tax with aconsumption-based alternative.

Simplifying Federal TaxesThe Advantages of Consumption-Based Taxation

by Chris Edwards

_____________________________________________________________________________________________________

Chris Edwards is director of fiscal policy studies at the Cato Institute.

Executive Summary

No. 416 October 17, 2001

Introduction

At the beginning of the 20th century, fed-eral taxes accounted for about 3 percent ofthe nation’s gross domestic product, and theentire tax code and related regulations filledjust a few hundred pages. Today, federal taxesaccount for 21 percent of GDP, and federaltax rules span 45,662 pages.1

Each year Americans spend 6.1 billionhours—more than 3 million person-years—on tax compliance activities, such as fillingout tax forms, keeping records, and learningtax rules.2 The complexity of the tax systemhas spawned a huge public and private “taxindustry” to perform administrative, plan-ning, avoidance, and enforcement activities.Those activities represent a pure loss to theeconomy since they consume resources andhuman effort that could otherwise be used tocreate useful goods and services. In addition,tax complexity leads to inequitable treatmentof citizens, causes high error rates, promotesevasion, and impedes economic decision-making by creating uncertainty.

The chief source of federal tax complexityis the income tax on individuals and corpo-rations. Two-thirds of Americans think theincome tax system is “too complex.”3

Treasury Secretary Paul O’Neill called thesystem an “abomination.”4 In 1976 presi-dent-to-be Jimmy Carter called for “a com-plete overhaul of our income tax system. Ifeel it’s a disgrace to the human race.”5 SinceCarter’s attack, the number of pages of feder-al tax rules has doubled.6

In 1988 Princeton professor DavidBradford, a former deputy assistant secretaryin the Department of the Treasury, notedthat “recent experience confirms the tenden-cy of an income tax . . . to evolve toward evergreater complexity.”7 Another decade of expe-rience has underscored this reality. Therehave been 1,916 changes to the tax code inthe past five years and 7,000 changes since1986.8 This year’s tax cut law creates 441 sep-arate tax code changes.9

The good news is that this is a problem

about which policymakers can do some-thing. Congress has taken a few small stepsto raise the visibility of the tax complexityproblem, most recently with the release of a1,300-page report from the Joint Committeeon Taxation.1 0The study cataloged the exces-sive complexity of federal taxes and proposedmore than 100 specific reforms. However,most of the proposals were quite narrow andlimited in scope, as required by the commit-tee’s mandate.1 1

Limited simplifications will not beenough. Substantial reform can come onlyfrom uprooting the income tax system andreplacing it with a consumption-based sys-tem, such as the Hall-Rabushka flat tax, anational retail sales tax, or a consumed-income tax.1 2 Switching to a consumption-based tax holds the promise of spurringgreater economic growth and vastly simplify-ing the federal tax system.

This study examines the magnitude offederal tax complexity, the costs created bythat complexity, the problems inherent intaxing “income,” the simplification advan-tages of consumption-based taxes, and somelong-term economic trends affecting the taxsystem.

The Magnitude of FederalTax Complexity

The Growth of Federal Tax RulesA century ago the federal government

relied on excise taxes and customs duties for91 percent of its revenue. As the governmentgrew and sought new sources of revenue, itenacted the corporate income tax in 1909with a 1 percent rate and the individualincome tax in 1913 with rates ranging from 1to 7 percent.1 3 The income tax began withjust 16 pages of tax laws, and the entire fed-eral tax system still had only 500 pages oflaws and regulations in the late 1930s.1 4

World War II launched the income tax on atrajectory of continual growth, fueled byemployer withholding begun in 1943.

2

Switching to aconsumption-

based tax holdsthe promise of

spurring greatereconomic growthand vastly simpli-

fying the federaltax system.

Today, total federal tax rules span 45,662pages, having more than doubled in lengthsince the 1970s (Figure 1). This page countincludes the full tax code, tax regulations, andsummaries of various Internal Revenue Servicepronouncements such as letter rulings andtechnical advice memoranda.1 5 The tax codeitself runs at least 1.4 million words and hasincreased in length 51 percent since 1985.16

The growth in tax complexity can also bediscerned from other statistics, as summa-rized in Table 1. For example, the number ofdifferent tax forms produced by the IRSincreased 23 percent in the past decade from402 to 496.1 7Taxpayer phone calls to the IRSdoubled during the 1990s from 56 million to111 million, even though the number of tax-payers grew only 12 percent.18 Apparently,the growth in usage of home computer taxsoftware, and the 1.5 billion annual hits tothe IRS Web page, have not reduced taxpayerconfusion.1 9

The Tax IndustryThe complexity of the tax system has

spawned a huge “tax industry” engaged intax filing, administrative, planning, avoid-ance, enforcement, and other activities. The

most visible part of the tax industry is theIRS with a budget of $9 billion in fiscal 2001.The IRS employs 97,000 people and usesabout 74,000 volunteers each year duringtax-filing season.2 0 In addition, there areabout 24,000 tax workers in other federalagencies.21

The complexity of the income tax hasoverwhelmed federal tax workers. Year afteryear the IRS answers a large proportion oftaxpayer phone queries incorrectly. The mostrecent government investigation found thatIRS workers provided incorrect answers totaxpayer questions 47 percent of the time.22

Alongside the federal tax bureaucracy, ahuge private tax industry of accountants,lawyers, and other workers has developed. Ofthe 1.6 million accountants in the country,perhaps 30 percent, or 480,000, are in taxpractice.2 3 Of the 1,048,000 attorneys in thecountry, perhaps 10 percent, or 105,000, arein tax practice.24 Enrolled agents are anothergroup of tax specialists and number at least35,000.2 5 There are also uncounted thou-sands of computer specialists, administrativepersonnel, and others in the tax industry, aswell as tens of thousands of tax workers instate and local governments.2 6

3

Today, total fed-eral tax rulesspan 45,662pages, havingmore than dou-bled in lengthsince the 1970s.

14,00016,500

19,500

26,300

40,500

400 504

8,200

45,662

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1913 1939 1945 1954 1969 1974 1984 1995 2001

Figure 1Total Pages of Federal Tax Rules (tax code, tax regulations, various IRS rulings)

Source: CCH, Inc., Standard Federal Tax Reporter, 2001.

Total tax industry employment is proba-bly more than 1 million workers.2 7 Thatmeans that there are more workers in the taxindustry than there are in the entire motorvehicles and parts industry.2 8

The following statistics indicate the rapidgrowth of the tax industry:

•Individual Tax Preparation: This year 57percent of individual tax filers used a paidpreparer, up from 48 percent in 1990 andfrom fewer than 20 percent in 1960.29 Withabout 73 million individual taxpayersusing paid preparers, and an average H&RBlock fee of $112, basic tax preparationcosts individual taxpayers at least $8.2 bil-lion per year.3 0Many taxpayers have morecomplex tax situations and pay thousandsof dollars for tax help.

• H&R Block Revenues: H&R Block is thelargest tax preparation firm, with 90,000workers.3 1 H&R Block’s tax preparationrevenues are up 74 percent in the pastfive years.3 2 In addition to H&R Block,there are thousands of smaller practi-tioners. An IRS tabulation found that1.1 million different tax preparers hadsigned individual tax returns in 1997,

although some of those may have beenunpaid preparers.33

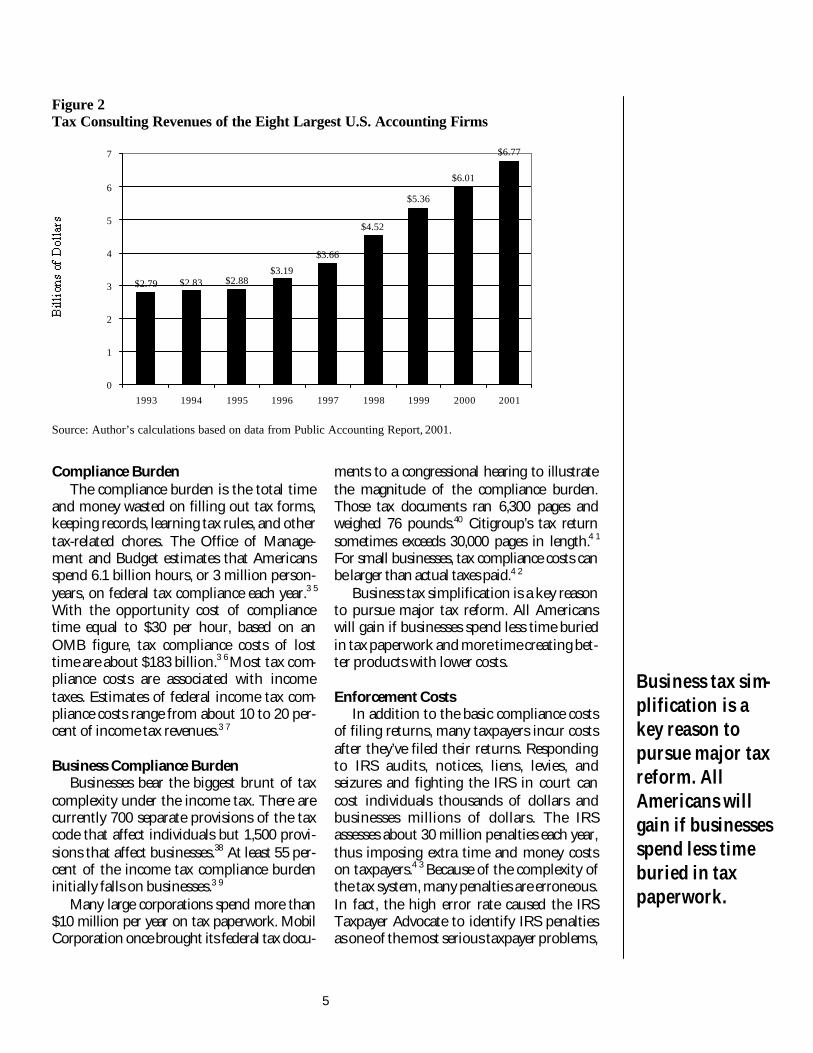

• Business Tax Preparation: Providing taxhelp to 25 million U.S. businesses is bigbusiness. Tax fees generate 29 percent ofrevenues for the top 100 accountingfirms, led by PricewaterhouseCoopersand Ernst & Young.3 4 Tax fees havesoared in recent years, more than dou-bling in the past seven years for the top100 firms, and more than doubling inthe past five years for the top 8 firms(Figure 2).

Costs of Tax Complexity

It will be of little avail to the people,that the laws are made by men oftheir own choice, if the laws be sovoluminous that they cannot beread, or so incoherent that they can-not be understood . . . or undergosuch incessant changes that no manwho knows what the law is today,can guess what it will be tomorrow.

James Madison, Federalist no. 62

4

H&R Block is thelargest tax prepa-ration firm, with

90,000 workers.H&R Block’s taxpreparation rev-enues are up 74

percent in thepast five years.

Table 1Escalating Income Tax Complexity

Item and Time Period Change

a) Total pages of federal tax rules, 1984–2001 Up 74% in 17 yearsb) Words in federal tax code, 1985–2000 Up 51% in 15 yearsc) Words in federal tax regulations, 1985–2000 Up 58% in 15 yearsd) Number of IRS tax forms, 1990–2000 Up 23% in 10 yearse) IRS phone queries from taxpayers, 1990–1999 Up 98% in 9 yearsf) Percentage of taxpayers using paid tax preparers, 1990–2000 Up 19% in 10 yearsg) H&R Block U.S. tax preparation revenues, 1996–2001 Up 74% in 5 yearsh) Top 8 accounting firms’ tax revenues, 1996–2001 Up 112% in 5 yearsi) Pages in Form 1040 instruction book, 1995–2000 Up 39% in 5 yearsj) Time to complete Form 1040 and Schedules. A, B, D, 1990–2000 Up 47% in 10 yearsk) Number of changed provisions in the tax code since 1986 7,000 in 15 years

Sources: Author’s calculations based on a) CCH, Inc. tax code, regulations, and IRS rulings; b) Tax Foundation;c) Tax Foundation; d) IRS; e) JCT; f) IRS; g) H&R Block; h) Public Accounting Report; i) National TaxpayersUnion; j) NTU; k) CCH, Inc.

Compliance BurdenThe compliance burden is the total time

and money wasted on filling out tax forms,keeping records, learning tax rules, and othertax-related chores. The Office of Manage-ment and Budget estimates that Americansspend 6.1 billion hours, or 3 million person-years, on federal tax compliance each year.3 5

With the opportunity cost of compliancetime equal to $30 per hour, based on anOMB figure, tax compliance costs of losttime are about $183 billion.3 6Most tax com-pliance costs are associated with incometaxes. Estimates of federal income tax com-pliance costs range from about 10 to 20 per-cent of income tax revenues.3 7

Business Compliance Burden Businesses bear the biggest brunt of tax

complexity under the income tax. There arecurrently 700 separate provisions of the taxcode that affect individuals but 1,500 provi-sions that affect businesses.38 At least 55 per-cent of the income tax compliance burdeninitially falls on businesses.3 9

Many large corporations spend more than$10 million per year on tax paperwork. MobilCorporation once brought its federal tax docu-

ments to a congressional hearing to illustratethe magnitude of the compliance burden.Those tax documents ran 6,300 pages andweighed 76 pounds.40 Citigroup’s tax returnsometimes exceeds 30,000 pages in length.4 1

For small businesses, tax compliance costs canbe larger than actual taxes paid.4 2

Business tax simplification is a key reasonto pursue major tax reform. All Americanswill gain if businesses spend less time buriedin tax paperwork and more time creating bet-ter products with lower costs.

Enforcement CostsIn addition to the basic compliance costs

of filing returns, many taxpayers incur costsafter they’ve filed their returns. Respondingto IRS audits, notices, liens, levies, andseizures and fighting the IRS in court cancost individuals thousands of dollars andbusinesses millions of dollars. The IRSassesses about 30 million penalties each year,thus imposing extra time and money costson taxpayers.4 3 Because of the complexity ofthe tax system, many penalties are erroneous.In fact, the high error rate caused the IRSTaxpayer Advocate to identify IRS penaltiesas one of the most serious taxpayer problems,

5

Business tax sim-plification is akey reason topursue major taxreform. AllAmericans willgain if businessesspend less timeburied in taxpaperwork.

$2.79 $2.83 $2.88

$3.66

$4.52

$5.36

$6.01

$6.77

$3.19

0

1

2

3

4

5

6

7

1993 1994 1995 1996 1997 1998 1999 2000 2001

Figure 2Tax Consulting Revenues of the Eight Largest U.S. Accounting Firms

Source: Author’s calculations based on data from Public Accounting Report, 2001.

and penalties are one of the most litigatedareas of tax law.4 4

ErrorsIn addition to added time and money

costs, tax complexity causes taxpayers, theIRS, and tax experts to make errors. IRSerrors have already been noted: the IRS getsthe answers to about half of taxpayer phoneinquiries wrong and often assesses erroneouspenalties.45 Errors can cost taxpayers money.For example, a new General AccountingOffice study found that more than half a mil-lion taxpayers together lose more than $300million per year because they take the stan-dard deduction when they should itemizetheir deductions.4 6

Other evidence of excessive complexitycomes from Money magazine’s annual test oftax experts who are asked to compute taxesfor a hypothetical family. Money’s results con-sistently show wide variations in experts’answers, as a result of the complexity of thetax laws. In 1998, 46 experts surveyed cameup with 46 different answers, with tax calcu-lations ranging from $34,240 to $68,912.4 7

Economic Planning DifficultyTax complexity impedes efficient deci-

sionmaking and results in families and busi-nesses missing opportunities and makingpoor economic judgments. This decision-making impediment of the tax system hasbeen called “transactional complexity.”48 Forexample, the growing number of saving vehi-cles under the income tax, including numer-ous individual retirement accounts (IRAs),confuses family financial planning. Thewrong saving choice may mean lowerreturns, less liquidity, and payment of penal-ties if money needs to be withdrawn. Otherexamples of transactional complexity includethe difficulty in figuring out when capitalgains should be realized and the complicatedtax implications of choosing a businessstructure for a new company.

A dramatic example of how income taxcomplexity interferes with economic planningis the recent phenomenon of taxpayers who

exercise incentive stock options (ISOs) beingunwittingly hit with large alternative mini-mum tax (AMT) bills.4 9Many ISO holders aremiddle-income families working for high-techfirms. When taxpayers exercise ISOs, the dif-ference between the option price and the mar-ket price may trigger the AMT, even if thestock is not sold. Many taxpayers have been hitwith large AMT bills without enough cashavailable to pay the IRS. While wealthy taxpay-ers might have tax advisers helping them,many middle-class families have never evenheard of the AMT and yet face large tax billsthey never planned for.

UncertaintyThe income tax system injects at least two

main types of uncertainty into economicplanning. The first is the continual change intax rules. This complicates long-term eco-nomic decisions, such as those regardingbusiness investment and retirement plan-ning. Taxpayers have faced remarkablechange in federal tax law in recent decades.Since 1954 more than 500 public laws havemade tax code changes.5 0 In the past fiveyears alone there have been 1,916 changes tothe tax code.5 1 This year’s $1.35 trillion taxcut law contains 85 major provisions and cre-ates 441 separate changes to the tax code.5 2

Each change in the law sets off changes intax regulations, requests for IRS guidance,changes to tax forms, and higher error rates.This year’s tax law adds new wrinkles inuncertainty with multiyear phase-in periodsfor numerous provisions. This creates thethreat that rules will be nullified before theybecome effective.

The second way tax complexity createsuncertainty is to confuse taxpayers and theIRS regarding the effects of current laws, letalone future changes. Discussing corporatetax paperwork costs, Prof. Joel Slemrod ofthe University of Michigan noted that “evenafter all this expense, neither the companynor the IRS is completely sure what the cor-rect tax liability really is. Audits, appeals, andlitigation can drag on for years.”5 3 The GAOfound that hundreds of tax disputes between

6

In the past fiveyears alone there

have been 1,916changes to the tax

code.

the IRS and large corporations remain unset-tled for 10 years or more.5 4 IRS agents haveestimated that “about 86 percent of corpo-rate tax disputes were due to different inter-pretations of the tax laws.”5 5

In 1992 the IRS estimated that after beingaudited large corporations owed $142 billionin taxes, but corporations themselves figuredthey owed just $118 billion.5 6Noting this gap,the GAO found that “the difference is sub-stantial and, in large part, attributable toambiguity and complexity in tax law.”5 7

Uncertainty about corporate tax liability hasmeasurable economic effects. One academicstudy found that tax law complexity decreasesthe accuracy of Wall Street estimates of com-pany tax rates, which are a key component ofbottom-line returns to shareholders.58

NoncomplianceTax complexity leads to noncompliance

with the tax system, whether caused by con-fusion or a desire to evade taxes. It is estimat-ed that the government loses about 17 per-cent of income tax revenues to noncompli-ance, or about $200 billion annually.5 9

Former IRS commissioner ShirleyPeterson thinks that confusion plays animportant role in noncompliance: “A goodpart of what we call non-compliance with thetax laws is caused by taxpayers’ lack of under-standing of what is required in the firstplace.”60 The JCT notes that for other taxpay-ers, “complexity can foster multiple interpre-tations of the law and aggressive planningopportunities. In addition, taxpayers mayconsciously choose to ‘play the audit lottery’by taking a questionable position on their taxreturns, in the belief that complexity willshield them from discovery.”61

Inconsistent and ambiguous income taxrules cause the government difficulty in find-ing tax evasion. As a consequence, it respondswith more audits, more information-report-ing requirements, more enforcement activi-ties, more court battles, and more extensiveregulation writing. Aggressive tax planningand the resulting responses by the IRS arelucrative for accountants and lawyers, but

the country would be better off if tax ruleswere simple and transparent so that businesscould spend its energies making good prod-ucts, not playing cat-and-mouse games withthe tax authorities.62

Inequity and UnfairnessTax code complexity creates unfairness

when it exacerbates “horizontal inequities,”which occur when similar families pay differ-ent tax amounts. As Congress has larded upthe income tax code with special preferences,inequities have increased. For example, taxincentives for education may reward individ-uals who pay to take classes but not individ-uals who learn by themselves at home. Suchinequities, and the tax complexity they cre-ate, have resulted in about 60 percent ofAmericans thinking that the income tax sys-tem is “unfair.”6 3 As Bradford has noted,echoing Madison, “A law that can be under-stood by only a tiny priesthood of lawyersand accountants is naturally subject to pop-ular suspicion.”6 4

Causes of Income Tax Complexity

The first decision to make when design-ing a tax system is what base, or economicquantity, to tax. In 1909 and 1913, respec-tively, the federal government imposed newtaxes on corporate and individual income.Initially, tax rates were low and very few peo-ple were affected, so any concerns about thesimplicity or efficiency of the tax base wouldnot have seemed important.6 5 But 90 yearslater, the twin income taxes have morphedinto giant revenue machines that togetherraise $1.3 trillion annually, or 60 percent oftotal federal receipts. Unfortunately, the gov-ernment picked an economically damagingand inherently complex tax base for the bulkof its revenue.

The income tax distorts the crucial eco-nomic tradeoff between consumption and sav-ing. Saving is a primary source of economicgrowth because it provides businesses with the

7

Inconsistent andambiguousincome tax rulescause the govern-ment difficulty infinding tax evasion.

investment funds they need to increase andmodernize the nation’s capital stock. It is wide-ly recognized that the income tax system isbiased against saving because the returns tosaving can face high tax rates, whereas currentconsumption does not. That bias has con-tributed to much of the interest in fundamen-tal tax reform in recent years. Nearly all recenttax reform proposals would adopt a consump-tion base to eliminate disincentives for savingand investment, and thereby boost capital for-mation and economic growth.

The other major burden of the income taxis excessive complexity. The following subsec-tions discuss why high and rising levels ofcomplexity are inherent to the income tax.

Haig-Simons IncomeThe Sixteenth Amendment to the U.S.

Constitution in 1913 allowed “taxes onincome from whatever source derived” butfailed to define how income should be mea-sured. Statutory definitions that followedwere just as vague, and there have been legalwrangling and congressional gyrations eversince about the proper base for the income tax.

Academic thought has been dominated bythe measure of income named after econo-mists Robert Haig and Henry Simons, whowrote in the 1920s and 1930s.6 6Haig-Simonsincome is simple to describe in theory: itequals consumption plus the rise in marketvalue of net wealth during a year. That meansthat it includes all forms of labor compensa-tion, such as wages and fringe benefits, and allsources of capital income, such as interest, div-idends, and capital gains. It includes allincome accrued during a year, whether or notit is received, including the paper value of netcapital gains. For example, if a worker hadwages of $30,000 that was spent on consump-tion and had unrealized stock market gains of$10,000, a Haig-Simons tax would have a baseof $40,000. Haig-Simons also includes itemsindividuals would not normally think of asincome, such as the implicit rent receivedfrom owning one’s home or the buildup ofwealth in life insurance policies.

This is a very expansive measure of

income, and our tax system has never comeclose to fully implementing it. While Haig-Simons income is simple in abstract theory,it is very impractical to tax in the real world.A basic impracticality stems from having todetermine the market value of all assets eachyear to measure gains and losses. In addition,Haig-Simons would require many imputa-tions to be made, such as taxing the phan-tom income from owning one’s home. Undersuch a system, taxpayers with little cash flowcould be hit with large tax bills they simplycould not pay.

Despite the impracticality of Haig-Simons, it has remained a touchstone formany public finance experts and still influ-ences current tax policy. Oddly, a Haig-Simons income tax does not have a strongeconomic argument in its favor. In fact, thetaxation of a broadly defined income baseleads to a bias against saving and investment.For example, the accrual taxation of capitalgains would clearly double tax investment: Arise in an asset’s projected future returnswould lead to an immediate taxable capitalgain; then, the return to the asset would betaxed again as it generated revenues in futureyears. Also, Haig-Simons fails to recognizethat saving is an expense incurred to earnincome, and leading theorists such as IrvingFisher have argued that it is very flawed.6 7

Without a strong economic justification,the attraction of a Haig-Simons income taxbase seems to stem partly from its theoreticalsimplicity and partly from the egalitarianimpulse to impose a heavy load of taxationon those with high incomes. Since Haig-Simons fully taxes capital income, many peo-ple have claimed that it is more equitablethan alternatives.6 8 That claim is of coursesubjective, and many other people argue thatconsumption-based taxation is superior toincome taxation on fairness grounds, but adiscussion of tax fairness is beyond the scopeof this paper.69

Falling Back on ad Hoc RulesThe impracticality of taxing Haig-Simons

income has forced policymakers to fall back

8

While Haig-Simons income issimple in abstract

theory, it is veryimpractical to taxin the real world.

on an array of ad hoc rules to implement thefederal income tax. Some income is exemptfrom tax, some income is taxed once, andother income is taxed multiple times. Incomemay be taxed when earned, when realized, orwhen received. There is no consistent stan-dard under present tax policy for what con-stitutes income or when it should be taxed.

Ad hoc rules have multiplied becausethere is no simple and efficient structure foran income tax. A key reason is the necessity ofdealing with inflation, which “wreaks havoc”with income taxes, as Bradford notes.7 0

Inflation distorts many key income taxitems, including capital gains, depreciation,and interest.

Dealing with inflation creates a Catch-22 ofefficiency and complexity problems for theincome tax. If inflation is not specifically dealtwith, the result will be overtaxation and distor-tion of tax rates across different investments.Alternately, fully adjusting the income tax forinflation would require excessive paperwork or“rule complexity.” As a result, governments usu-ally fall back on ad hoc and approximate fixesfor inflation. The problem with ad hoc fixes isthat they generate inconsistencies and thus cre-ate decisionmaking difficulties or “transaction-al complexities.”7 1

A classic example is capital gains taxation.To avoid taxing purely inflationary gains, spe-cial rules are needed. A full solution would beto allow indexing of the capital gain basis, butthat would involve excessive paperwork.Instead, the federal tax system has usuallyallowed an ad hoc adjustment for inflation inthe form of an exemption or a lower tax rate.Such makeshift adjustments provide only arough solution, and they create tension as tax-payers seek to recharacterize ordinary incomeas capital gains. Complexity increases as thegovernment drafts extensive rules to preventtaxpayers from unduly taking advantage ofthe special capital gains rules.

The realization tax treatment of capitalgains is another example of the Catch-22complexity problem of income taxation.72 AHaig-Simons income tax would tax capitalgains on an accrual basis, thus taxing all net

gains at the end of each year. As noted, thatwould be both difficult and unfair sincecash-poor taxpayers could not afford to paytaxes on purely paper gains. As a result, fed-eral taxation has fallen back on taxing capitalgains upon realization, or asset sale. But thatapproach creates transactional complexity astaxpayers seek to optimally time realizationsand offset capital gains with losses.Complexity has increased as the governmenthas created complicated rules to limit tax-payer flexibility. For example, special ruleslimit the extent that ordinary income may beoffset with capital losses, and “wash-salerules” restrict the use of timing techniques tomatch gains with losses.

Inherent Inconsistency for DeductionsDetermining which expenses may be

deducted against gross income also involvesinherent complexities. Under the income tax,businesses generally use accrual accountingto measure the tax base of net income orprofits. The basic idea is to match revenueswith expenses over time to accurately mea-sure net income within each period.7 3This isfar more difficult than it sounds, especiallybecause there is no agreed-upon definition ofnet income.

Consider business purchases of buildingsand capital equipment. Those assets generaterevenues in future years, so it is thought thatthey should not be simply deducted in theyear of purchase. Rather, they must be depre-ciated, or deducted against receipts, in futureperiods on the basis of the decline in theirvalue. If depreciation deductions don’t accu-rately track the decline in the asset’s value,the Haig-Simons income tax base will be mis-measured. Since every asset is different, andnew types of assets are being invented all thetime, it is difficult to maintain accurate andsimple rules for depreciation calculations.

As is the case with capital gains, inflationcreates depreciation distortions for whichthere are no simple solutions. The currentincome tax allows accelerated depreciation,which may roughly compensate for inflation,but this ad hoc fix involves complicated rules

9

There is no con-sistent standardunder present taxpolicy for whatconstitutesincome or whenit should betaxed.

and can lead to economic distortions.7 4

Inflation also causes problems for other taxcode provisions that attempt to match rev-enues and expenses through time, such asinventory accounting.

At a more fundamental level, the currentconcept of taxing income creates theintractable problem of determining whichexpenses should be deducted immediatelyand which should be capitalized. Purchasesthat are capitalized are deducted over futureyears using the special rules for depreciation,amortization, and inventory. In theory, anyasset that produces benefits in future yearsshould be capitalized, but the tax code con-tains no consistently followed principle ofcapitalization. A lack of consistency hasresulted in many battles between the IRS andtaxpayers.7 5 The Supreme Court has notedthe ambiguity: “If one really takes seriouslythe concept of a capital expenditure as any-thing that yields income, actual or imputed,beyond the period . . . in which the expendi-ture is made, the result will be to force thecapitalization of virtually every businessexpense.”76 For example, business advertisingcosts may be immediately deducted undercurrent rules. But most advertising producesbenefits in future years and so in theoryshould be amortized rather than immediate-ly deducted.

Congress has followed no consistent poli-cy on capitalization. For example, in oneattempt to properly measure Haig-Simonsincome, Congress burdened entrepreneursby requiring amortization over five years ofcosts associated with starting a new business.It decided that start-up costs create value infuture time periods and thus should not beimmediately deducted. On the other hand,Congress has decided that research anddevelopment expenses may be immediatelydeducted, even though R&D clearly gener-ates benefits over future years.

Inconsistency regarding deductions hasalso created complexity under the individualincome tax. For example, the personal inter-est deduction was eliminated in 1986 in aneffort to broaden the tax base. But because

mortgage interest remained deductible,home equity loans developed to essentiallyallow people who own homes to continue todeduct personal interest.

Such income tax inconsistencies createadministrative and enforcement problems.The government must create complicated“anti-abuse” rules to counter the natural ten-dency of taxpayers to reorganize their affairsto seek out tax preferences. And there is a con-tinual call for IRS guidance from taxpayersand tax accountants because, with no general-ly followed principles, it is not clear what thelaw requires in each specific situation.

Inconsistency Breeds InstabilityThe ad hoc and inconsistent rules of the

income tax have been a major source of insta-bility in the federal tax system. Policymakershave gyrated between broader and narrowertax bases, with saving and investment provi-sions as the main battleground. Proponentsof broadening the base use Haig-Simonsincome as the touchstone. Others are con-cerned about the economic damage causedby taxing broad-based income and insteadfavor removing excess taxes from personalsaving and business investment. Removingtaxes from saving and investment moves thesystem toward a consumption-based tax.Table 2 gives some of the gyrations taken byCongress as it has changed policy directionon saving and investment provisions inrecent decades.7 7

Congress has changed the treatment oflong-term capital gains 25 times since it firsttreated gains separately from ordinaryincome in 1922.7 8Another example of unsta-ble policy is the investment tax credit (ITC),which was adopted in 1962, repealed in thelate 1960s, reinstated and then increased inthe 1970s, and repealed in 1986.7 9Similarly,since accelerated depreciation was intro-duced in 1954, depreciation rules havechanged every decade or so.80

Major tax acts have embraced oppositetax base philosophies. The tax laws of 1969and 1976 generally moved toward a Haig-Simons income tax base but were followed by

10

The ad hoc andinconsistent rulesof the income tax

have been a majorsource of instabil-

ity in the federaltax system.

Table 2The Gyrating Income Tax Base: Changing Rules for Saving and Investment

Broad-Based Income Exceptions Are Exceptions Are Restrictions AreIs Taxed Created Restricted Liberalized

Restrictions areIncome tax is imposed, Harm from income liberalized asresulting in heavy taxation is recognized Exceptions are their disincen-tax burden on saving and exceptions are restricted in effort to tive effectsand investment. made. “broaden the base.” are recognized.

Personal Saving

Capital gains Capital gains rate Capital gains ratetreatment changed increased in 1986 reduced in 1997.25 times since 1922Rate reduced in1978 and 1981.

Creation of individual Restrictions im- Liberalization inand employer-based posed on eligibil- 1996, 1997,saving/pension plans. ity, contribution 2001. Creation

limits, early with- of SIMPLEdrawals, distri- plans withbutions, etc. fewer rules

IRAs liberalized IRAs restricted IRAs liberalizedin 1981. in 1986. in 1997, 2001.

Business Investment

Depreciation lib- Depreciation de- Calls to liberalizeeralized in 1962, ductions pared depreciation for1971, 1981. back in 1982, high-tech and other

1984, 1986. assets today.

Investment tax ITC eliminatedcredit (ITC) on in 1986.and off since 1962.

Business incentives Corporate AMT JCT, ABA, AICPA,in general. limits business and others call for

incentives. AMT repeal.

Small business Small business Small businessincentives, such incentives are expensing liberalizedexpensing capital restricted and in 1996.purchases. denied to larger firms.

Source: Author’s compilation.

11

12

While TRA86 cutmarginal tax

rates, the broad-ening of the tax

base toward Haig-Simons has beenwidely criticized

for its complexityand anti-saving

effects.

the 1978 tax law that moved back toward aconsumption base.8 1 The EconomicRecovery Tax Act of 1981 then moved the sys-tem much further toward a consumptionbase. It liberalized depreciation deductions,expanded IRAs, and lowered the capital gainstax rate. Congress changed course in 1982and 1984, scaling back the liberalized depre-ciation of the 1981 law and reducing the ITC.

The wide-ranging Tax Reform Act of 1986(TRA86) substantially expanded the tax basetoward the Haig-Simons ideal. IRA provisionswere cut back, the capital gains tax rate wasraised, depreciation deductions were furtherrestricted, the ITC was eliminated, and theindividual and corporate AMTs were beefedup. TRA86 also created some of the most com-plex parts of the income tax code, includingthe new rules for the AMT and inventoryaccounting. So while TRA86 cut marginal taxrates, the broadening of the tax base towardHaig-Simons has been widely criticized for itscomplexity and anti-saving effects.

After TRA86, Congress realized its over-reach and began slowly moving the tax sys-tem back toward a consumption base.Capital gains tax rates were lowered onceagain in 1997. Small business expensing forcapital purchases was modestly liberalized in1996. And rules for retirement saving planswere liberalized in 1996, 1997, and 2001.

Income Tax Damage and Band-Aid FixesA key cause of the gyration of the tax sys-

tem is that high tax rates imposed on anincome base cause substantial economicdamage, particularly to saving and invest-ment. In response to the damage, there arecontinuing demands for Congress to carveout exceptions. For small businesses,Congress carved out an exception to thecomplex and costly depreciation rules toallow immediate deduction, or “expensing,”of the first $24,000 of capital investment.8 2

Congress has recognized that full incometaxation of individuals’ personal savingwould be destructive. In response, it hascarved out dozens of preferential provisionsfor saving, including 401(k)s, numerous

IRAs, and other vehicles. With the incometax, Congress takes as its starting positionthat saving should be fully taxed, but numer-ous and complicated exceptions to the ruleshould then be carved out. This is a muchmore complex approach than starting withthe general rule that saving should not betaxed, as would be the case under a con-sumption-based tax system.83

The current approach causes great insta-bility, as shown in Table 2. Congress createstax preferences and then determines that thepreferences should not be used “too much”and restricts them. The negative effects ofrestrictions then lead to calls for liberalizingthe restrictions.

For personal saving vehicles, Congress hascreated a complicated patchwork of rules foreligibility, contribution limits, withdrawalrequirements, and “nondiscrimination”designed to broaden plan coverage. Employer-based plans are also subject to complex regu-lations under the Employee RetirementIncome Security Act of 1974. The JCT notesthat major areas of employer pension law havechanged nearly every year since the early1980s, and the changes often create such alarge backlog of regulations that employersare frequently left unsure of how to comply.84

The complexity of personal saving taxa-tion has led to both ineffectiveness andinequitable treatment. The complex rulesand limitations reduce the pro-saving bene-fits that saving vehicles might otherwisehave, thus defeating their purpose. In addi-tion, the results are inequitable since differ-ent individuals have access to different plans,and some purposes, such as retirement,receive favorable saving treatment while oth-ers do not.

Congress sometimes realizes that thecomplexity it created has gone too far. It thencreates newer rules to skirt the existing com-plex rules. For example, as the complexity ofemployer-based pension plans increased,firms, particularly smaller firms, droppedpension coverage. In response, Congress cre-ated SIMPLE retirement plans with less com-plicated rules for firms with 100 or fewer

13

Because the feder-al income tax fol-lows no consis-tent principles, itis ripe for loop-hole lobbyingand special taxbreaks forfavored groups.

employees. Simplified employee pensions(SEPs) were another congressional attemptto create a simpler retirement saving vehicle.

The 1996 tax law that created SIMPLEsincluded 32 other law changes under theheading “Pension Simplification Provisions.”The recently passed $1.35 trillion tax cutincludes 64 separate provisions changing therules for tax-favored saving plans.8 5Wouldn’tit be much better to exempt personal savingfrom taxation altogether? This would hugelysimplify financial planning and eliminate theneed for Congress to pick and choose formsof saving to favor. In fact, this would be thetreatment of saving under a consumption-based tax, as discussed further below.

The Income Tax Fosters SocialEngineering

In recent decades, the income tax systemhas become a popular tool for social engi-neering by the government. “Social engineer-ing” through the tax code may be defined asusing tax exemptions, deductions, credits,and other preferences to promote particularactivities that policymakers believe need spe-cial treatment. For example, there are eightdifferent education incentives under theincome tax, each with separate rules and ben-eficiaries.86

While individual policymakers often sup-port particular preferences, nearly everyoneagrees that the overall effect is a Swiss cheesetax code that is complex and sows taxpayerconfusion. Some of the political dynamicsthat lead to social engineering are unavoid-able in any tax system. After all, tax code pref-erences usually have easily identifiable bene-ficiaries, but the costs of complexity are morediffuse and less visible.

Nonetheless, because the federal incometax follows no consistent principles, it is ripefor loophole lobbying and special tax breaksfor favored groups. Inconsistent treatmentbegets further inconsistent treatment. And,as noted, the economic damage caused bytaxing income in the first place createsunending calls for special exceptions.

By contrast, a consumption base provides

a more consistent starting point for a tax sys-tem that could substantially reduce socialengineering. Consider the complexity of per-sonal saving provisions under the incometax. A consumption-based tax would elimi-nate all special rules for the taxation of per-sonal saving and thus preempt a major chan-nel for promoting favored activities. Forexample, five of the eight targeted provisionsfor education in this year’s tax law relate toeither saving or interest and would thereforebe automatically nullified under a consump-tion tax. Certainly, Congress could continuefavoring some activities under a consump-tion tax, but removing saving and investmentwould narrow the options for special taxpreferences.

A major tax reform could also reducesocial engineering if it reduced overall taxrates and levels. High taxes cause taxpayerpain, thus raising demands that Congressprovide Band-Aids. For example, the earnedincome tax credit (EITC) was created andexpanded to offset the heavy burden of pay-roll taxes that Congress imposes. The EITC isso complicated that it has a 25 percent filererror rate and requires a special $145 millionannual outlay for IRS compliance.8 7

Reducing overall tax levels would reduce thedemands to complicate the tax code withsuch special preferences.

The SimplificationAdvantages of

Consumption-Based TaxesNearly all of the major tax reform plans

introduced in recent years would replace theindividual and corporate income taxes with aconsumption-based tax. In addition to theeconomic growth benefits of such a reform,Bradford notes that a consumption-basedtax would have “vastly simpler implementa-tion” than the income tax.8 8

Dramatic simplification gains could beachieved under either a national retail salestax or a flat tax based on the design of RobertHall and Alvin Rabushka of the Hoover

14

A study by theAmerican

Institute ofCertified Public

Accountantsfound that the

flat tax would be“a massive simpli-

fication thatwould eliminate

much of the com-plexity that

plagues the cur-rent system.”

Institution.8 9 According to the TaxFoundation, replacement of the income taxwith a retail sales tax would reduce compli-ance costs by 95 percent, and the flat taxwould reduce compliance costs by 94 per-cent.90 Tax compliance expert Joel Slemrodmore conservatively estimates that the flattax would cut compliance costs by 50 per-cent.91 A study by the American Institute ofCertified Public Accountants found that theflat tax would be “a massive simplificationthat would eliminate much of the complexi-ty that plagues the current system.”9 2To sim-plify discussion, this section focuses primari-ly on the simplification advantages of the flattax over the income tax, but many of thepoints could be generalized to other con-sumption-based tax plans.

The Flat TaxA number of misconceptions surround the

Hall-Rabushka flat tax.9 3First, it is often mis-takenly assumed that it is the flat rate struc-ture of the flat tax that is the source of its sim-plification benefits. While a flat rate structuredoes create some simplification, the mainadvantage of a flat rate is that the economicdisincentive effects of the current tax systemwould be reduced.9 4 The second misconcep-tion is that the flat tax is just a simpler versionof the current income tax. In fact, the flat taxis a consumption-based tax, although it is col-lected like the income tax from both individu-als and businesses.95 Indeed, it is the con-sumption base of the flat tax that is the key toits simplification benefits.

To see why the flat tax is a consumption-based tax, note that only wages and pensionbenefits would be taxed at the individuallevel. At the business level, firms woulddeduct wages, pension payments, and pur-chases from other businesses, including capi-tal purchases. Now modify the flat tax to anequivalent structure where there is no indi-vidual-level tax and businesses are denieddeductions for wages and pensions. Theresulting tax would be a “subtractionmethod” value-added tax (VAT). VATs havethe same tax base as retail sales taxes. Hence,

the flat tax has essentially the same tax baseas a retail sales tax.9 6 Because of the similarbases of the flat tax and a retail sales tax, theywould share many of the simplification ben-efits that are discussed below.

Individual and Business Taxes SimplifiedThe basic difference between an income

tax and a consumption tax is the treatmentof saving and investment. For individuals,consumption-based taxes can treat savingunder rules similar either to those that gov-ern either regular IRAs or Roth IRAs. In thefirst case, saving is initially deducted, andthen later withdrawals are included in the taxbase. In the second case, no deduction isgiven for saving initially, but returns are nottaxed. The flat tax adopts the latter Roth IRAtreatment of saving.9 7Under the flat tax, div-idends, interest, and capital gains are nottaxed at the individual level and do not needto be reported to the IRS. This would greatlyease paperwork headaches for taxpayers,especially in comparison with complyingwith the current complicated rules for tax-favored saving vehicles. This structure wouldalso dispense with the need for businessesand the IRS to keep track of more than half abillion Form 1099s and other information-reporting documents each year.9 8

For businesses, the flat tax would vastlysimplify some of the most complex areas ofthe tax code, including accounting for capitalpurchases and inventories. This would occurbecause consumption-based taxes use cash-flow accounting in place of accrual account-ing, which is generally used under the currentincome tax.99 Accrual accounting requiresthat firms accurately match revenues andexpenses each year to measure net incomeand to capitalize expenses that create futurebenefits. Such timing of income and expenserecognition under the income tax is a keysource of complexity.

Because consumption taxes do not mea-sure broad-based income, they do not requirethe complexities of accrual accounting.Instead, under cash-flow accounting business-es would simply deduct materials, inventories,

15

The flat taxwould eliminatecapital gains taxa-tion for bothindividuals andbusinesses.

equipment, and structures immediately uponpurchase. The purchase price of a $1 pencilwould be deducted just the same as the pur-chase price of a $10 million machine. Bradfordnotes that “income accounting is more diffi-cult than cash-flow accounting. That difficul-ty is responsible for much of the complexity inthe current income tax system.”100

Complexities Eliminated under aConsumption-Based Tax

A 1995 survey asked 315 corporate taxdirectors to rank the most complex parts ofthe corporate income tax.101 Of the 10 mostcomplex parts, 4 dealt with “timing” issuesinherent to measuring income, such asdepreciation, and 4 dealt with internationaltax issues. The other two items were the AMTand “instability in the tax code.” Nearly all ofthose sources of complexity would be elimi-nated or greatly reduced under a consump-tion-based tax.102 Similarly, most complexfeatures of the individual income tax wouldbe eliminated under a consumption-basedtax such as the flat tax.

The first column of Table 3 gives complextax provisions that would be automaticallyeliminated under the flat tax and generallywould also be eliminated under other con-sumption-based tax proposals. The majoritems in this part are discussed separatelybelow. The rest of the table gives tax com-plexities that could remain under nearly anytax system. The second column is complexi-ties that could be eliminated by the specificdesign of a tax reform plan. The third col-umn is complexities that would remainunder the flat tax or other consumption-based tax designs.

Capital GainsComplaints about the difficulty of taxing

capital gains have been voiced since thebeginning of the income tax, and capitalgains “are generally credited with a high pro-portion of the [tax] law’s bulk and complexi-ty.”1 0 3 There are currently 17 different taxrates that may be applied to capital gains,and the current IRS Schedule D for reporting

capital gains is 54 lines long and scheduled togrow even longer next year.104

Capital gains taxation comes into play inindividual stock and bond ownership, mutualfund ownership, real estate taxation, and cor-porate and partnership taxation. Capital gainstaxpayers must deal with multiple tax rates,multiple holding periods, the timing of real-izations, strategies for netting gains and losses,different ways of calculating cost basis, limita-tions on deducting capital losses, loss carry-overs, “wash-sale rules” to prevent loss salesand repurchases, and many other issues.

Most of this complexity is unavoidableunder an income tax because capital gainscannot be widely taxed on an accrual basis assuggested by Haig-Simons income theory. Asa result, the government has fallen back ontaxing gains when realized. Unfortunately,“elaborate rules to define and limit capitalgains are inevitable in an income tax basedon realization.”105 Taxing gains on realiza-tion, combined with preferential capitalgains rates, stimulates large tax-planningefforts, such as recharacterizing ordinaryincome as capital gains.

While taxpayers invest large efforts to min-imize their tax bills, government busily churnsout rules and regulations to prevent “abuse”of the ambiguities in the capital gains appara-tus. For example, the rules that deny capitalgains treatment to businesses that try to char-acterize regular business receipts as gains arean area of continuing complexity. It is oftendifficult to draw distinct lines between assetssold as a part of regular business sales, whichare taxed as ordinary income, and assets soldby “investors” for “speculation,” which aretaxed as capital gains.1 0 6

There is no need for all this complexity.The flat tax would eliminate capital gains tax-ation for both individuals and businesses.107

Eliminating capital gains taxation wouldeliminate all the special tax rates and otherrules as well as extensive tax avoidance efforts.

Personal SavingAmericans interested in saving a portion

of their current income to support them-

Table 3Complexities Eliminated and Not Eliminated under a Consumption-Based Flat Tax

Complexities Eliminated Complexities That MustAutomatically Be Eliminated by Design Complexities Not Eliminated

Personal savings income: No taxation of Multiple tax rates. Transfer pricing issues forinterest, dividends, and capital gains at multinational corporationsindividual level. No need to track more than Family status adjustments, remain under flat tax.half a billion 1099s and other forms. such as child tax credit.

Defining taxable consumptionCapital gains: Special treatment eliminated at Earned income tax credit. vs. nontaxable savingsbusiness and individual levels. Gets rid of and investment.multiple tax rates and holding periods, timing Charitable contributionof realizations, matching gains with losses, tax preferences. Defining financial flows vs.calculating basis, etc. nonfinancial flows.

Health care taxInterest: Interest income and expense preferences. Defining financial servicescomplications, such as muni-bond preference, businesses vs. other“tracing rules,” “original issue discount,” Home ownership tax businesses.eliminated. preferences.

Defining taxable vs.Savings vehicles: Plethora of savings vehicles Education tax tax-exempt activities.eliminated including 401(k)s and numerous IRAs. preferences.Most complex business pension issues disappear.

Depreciation: Complex and distortionary accounting rules for capital purchases eliminated.

Inventory: Complex accounting rules for business inventory eliminated.

Inflation: Measurement problemsand distortions caused by inflation eliminated for depreciation, inventory,interest, capital gains, etc.

Other business complexities: Capitalizationissues, and most issues related to timing ofincome and deductions, eliminated.

International tax rules: Taxing businesses on a territorial basis would eliminate some ofthe most complex aspects of business taxation,such as the foreign tax credit and Subpart F.

Business structure: Uniform business taxationwould replace “C” and “S” corporations, LLCs,sole proprietorships, and partnerships. Merger and acquisition accounting greatly simplified.

Social engineering of capital income: Forexample, 8 of 20 income tax phaseouts that relate to capital income disappear. And 5 ofthe 8 education preferences that relate tointerest or savings disappear.

Source: Author’s compilation.

16

17

Consumptiontaxes wouldexempt personalsaving from taxa-tion.

selves in later years face an enormously com-plex array of tax rules. Different rules comeinto play for ordinary income, capital gains,401(k)s, Keoghs, SIMPLEs, SEPs, IRAs, tradi-tional pension plans, insurance companyannuities, tax-exempt bonds, and other sav-ing vehicles. An Amazon.com search findsthree books, one 258 pages long, to help fam-ilies figure out how just one vehicle, the RothIRA, works.

Each investment option has separate rulesregarding eligibility, income limits, maxi-mum contributions, required distributions,withdrawal limitations, penalties, rollovers,and other items.1 0 8Any of those rules can cre-ate confusion for individuals trying to planfor their future. For example, the AmericanBar Association recently noted that the “min-imum distribution requirements are amongthe most complex in the code,” and yetCongress expects millions of families to fig-ure them out.109

Employers face heavy burdens with theadministrative complexity of tax rules forpension plans. The JCT notes that “the feder-al laws and regulations governing employer-provided retirement benefits are recognizedas among the most complex sets of rulesapplicable to any area of the tax law.”1 1 0Theproliferation of new types of plans makes itdifficult for businesses to figure out whichoption they want for their employees.

The complexity of those saving plans isself-defeating in many ways. Individualsdon’t save as much as they might becausecomplex minimum distribution and otherrules limit the attractiveness of employer-provided plans. Those plans reduce familyliquidity compared with regular taxable sav-ing because of withdrawal restrictions. Highadministrative expenses for those plansreduce net returns to saving. And the tax andERISA rules for employer-based pensionplans have gotten so complex that manyfirms have dropped those plans altogether,particularly defined-benefit plans.

All this complexity is an artifact of theincome tax. Consumption taxes wouldexempt personal saving from taxation. Not

only would this be massively simpler, it wouldfree Congress from picking and choosingwhich forms of saving should be speciallyfavored. Retirement and education saving arethe current favorites among federal politi-cians, but families have other saving goals,such as saving for a new car or for possibleleaner times ahead. It would be much simpler,fairer, and more efficient for individuals them-selves, not the federal government, to choosethe form and purpose of their saving.

The flat tax exempts from personal taxa-tion the returns to saving, including divi-dends, interest, and capital gains. It worksessentially like an unlimited Roth IRA butwithout any of the Roth IRA rules. This wouldhugely simplify family financial planning.Families could receive all the benefits of thecurrent hodge-podge of accounts, but withnone of the complexity and none of the con-stant rule changes. Individuals could save inwhatever type of asset they saw fit, withdrawmoney any time they wanted for any purpose,and enjoy the full gross return to saving.

Depreciation and AmortizationBusiness investment in buildings and equip-

ment generates a stream of future revenues asproducts produced with the assets are sold inthe marketplace. The income tax is supposed tomeasure broad-based income in each period bymatching revenues against depreciation deduc-tions taken to recover the cost of assets. Inincome tax theory, depreciation deductionsshould come close to an asset’s actual decay orobsolescence over time.111

In practice, the depreciation system fallsfar short of measuring depreciation properly.Rough approximations are used in the taxcode to place assets in different classes thatdetermine how fast they are depreciated.1 1 2

The current asset classification system is veryout of date and is partly based on a 1959Treasury study.1 1 3 As a result, the treatmentof new technologies, such as computers, isoften wrong and results in those assets beingovertaxed. But even up-to-date depreciationschedules would be wrong because inflationmakes it extremely difficult to measure

18

A key problemwith the income

tax is inherentambiguity and

inconsistencyregarding the cap-

italization ofassets.

depreciation accurately. The depreciation system has many com-

plex features: assets must be placed in one ofeight “tax life” categories to determine theperiod over which deductions are taken; vari-ous mathematical formulas are used for cal-culating deductions; complicated rules deter-mine when assets are considered to be placedin service; if partly depreciated assets are sold,complex “depreciation recapture” rules comeinto play to deny capital gains treatment fora portion of the gain; and many assets areunique and thus raise difficult questions asto appropriate treatment.

Similarly complex issues arise aboutintangible assets, such as patents and trade-marks. When such assets are purchased, theymust be amortized to recover their cost overtime. Harvey Rosen, a leading public financeexpert, notes that the “intractable complexi-ties” related to intangible assets are“unavoidable if the base of the tax is income.”He discusses one real-life example from pro-fessional baseball:

If you buy a baseball team, part ofwhat you are buying is the contractsof the players. The tax authoritieshave ruled that the component ofthe acquisition cost that is attribut-able to player contracts is a deprecia-ble asset . . . on the other hand, othercomponents of the value of the fran-chise, such as television contracts,are not depreciable. Predictably, clubowners are locked into a perpetualbattle with the IRS over the value ofthe player-component of acquisitioncosts.114

This example highlights a key problemwith the income tax: there is inherent ambi-guity and inconsistency regarding the capi-talization of assets. As a result, there are fre-quent battles between the IRS and taxpayersover which items are capital purchases andwhich are regular expenses that may bededucted immediately. The JCT notes that,“despite guidance provided by the IRS and

decisions reached by courts, distinguishing acapital expenditure from a current expensecontinues to be uncertain and a source of sig-nificant disputes.”115 In fact, capitalization isone of the most litigated parts of the taxcode.116 In recent years, the IRS has exacer-bated the problem by aggressively forcingcompanies to capitalize all kinds of expensesthat the IRS unilaterally decides yield long-term benefits.117

The flat tax would eliminate the complex-ity of depreciation and amortization and thenonstop battles over capitalization. All busi-ness purchases would be treated the sameway and immediately deducted. Assets wouldnot need to be separated into various depre-ciation classes, so it wouldn’t matter ifCongress didn’t get around to updatingthem in 40 years, as is currently the case. Therules under the flat tax would be simple anddurable over the long term.

Congress has already recognized theexcessive complexity and inefficiency ofdepreciation accounting—but only for smallbusinesses. Small businesses may deduct thefirst $24,000 of capital purchases each year.The flat tax would give all businesses thishuge simplicity benefit that only very smallbusinesses enjoy today.

Inventory AccountingUnder the income tax, businesses with

inventories may not simply deduct the costs ofmaterials purchased for production or fin-ished goods held for sale. Rather, those inven-tory expenses must be capitalized and deduct-ed later when products are sold. The idea is tomatch revenues and expenses so as to accu-rately measure income in each period, thesame principle behind the depreciation rules.

Like the depreciation rules, the inventoryrules are complex, and they create economicdistortions because of the effects of inflation.And both the tax rules for inventory and thetax rules for depreciation differ from therules used for regular financial accounting.As a result, businesses must keep two sets ofbooks for these and other items.

The tax rules for inventory accounting

19

Former IRSnational taxpayeradvocate ValOveson called theAMT “absolutely,asininely stupid.”

have become more complex in recent years.In particular, the “uniform inventory capital-ization” rules enacted in TRA86 are “extraor-dinarily complex,” according to the ABA.1 1 8

These rules deny deductions for a range ofindirect costs, such as interest expenses, thatare related to inventories. The JCT has simi-larly called the rules “complex and burden-some” and proposed some reforms.119

Under the flat tax, all materials purchasedwould be immediately deducted. That wouldput an end to the complex inventory rulesunder tax law and end a major source of dis-putes between business taxpayers and the IRS.

Alternative Minimum TaxesThe corporate and individual AMTs are

complex income tax systems that operatealongside the ordinary income taxes. There isbroad agreement that these ill-conceived par-allel tax systems should be repealed. Forexample, AMT repeal has been recommend-ed by the JCT, the ABA, and the AICPA.1 2 0

Former IRS national taxpayer advocate ValOveson called the AMT “absolutely, asininelystupid.”121 Under current projections, 36 mil-lion taxpayers will be subject to the “asinine”individual AMT by 2010 unless Congressacts to repeal it.122

The AMTs are too extensive a topic tocover in this paper. However, of particular rel-evance is that the two AMTs were originallysupported in an attempt to better measure“income” under the income tax. For corpora-tions, that meant using the AMT to producemore consistent marginal tax rates acrossindustries. For individuals, that meant usingthe AMT to produce more consistent taxrates across families with similar incomes.

Consumption-based taxes easily achieveconsistent and neutral tax rates across indus-tries and across families with similar con-sumption levels. There would be no need forthe AMTs under the flat tax, and they wouldbe eliminated.

Taxing Multinational CorporationsRapid integration of the United States into

the world economy is raising questions about

the viability of the current “worldwide” systemof federal income taxation. Under this system,the foreign earnings of U.S. businesses are sub-ject to U.S. taxation. U.S companies operatemore than 24,000 foreign affiliates in Europe,Asia, and elsewhere.123

U.S. corporations set up foreign affiliatesto more easily penetrate foreign markets andto stay competitive by tapping into foreignbusiness and technological know-how. Thishas been a successful strategy as about one-third of the global sales of the largest 500U.S. corporations are from foreign affili-ates.124 Most U.S. foreign affiliates are inhigh-income countries, such as Germany andFrance, where they pay tax to foreign govern-ments at generally high rates.

In general, the U.S. income tax is assessedon foreign business income when it is repatri-ated to the United States, but a tax credit isprovided to roughly prevent double taxation.This is the general rule, but there is a largehodge-podge of special and often inconsistentrules for different industries and types ofinvestments. In fact, there are at least six over-lapping sets of “anti-deferral” rules that breakthe general rule of not taxing foreign profitsuntil repatriated, such as the Subpart Frules.125 This lack of consistently followedprinciples has led to complexity, instability,tax avoidance efforts, and loophole-closingBand-Aids applied by the government.

Many facets of the U.S. international taxsystem are complex: foreign income anddomestic income are measured differently;foreign assets and domestic assets have differ-ent depreciation rules; detailed rules arerequired to convert foreign currency earningsinto dollars; financial services face numerousspecial rules on foreign earnings; different lev-els of foreign affiliate ownership have differenttax treatment; some foreign income is taxedwhen repatriated, other income is taxed whenearned; different types of foreign income areplaced in nine different “baskets” with sepa-rate foreign tax credit limitations; special rulesallocate certain expenses between domesticand foreign-source income; and so on.

The overall result of these rules is to great-

ly complicate business planning. And theseworldwide tax rules raise little if any addedrevenue for the U.S. government because thegovernment provides a credit to roughly off-set foreign taxes paid. Glenn Hubbard, chair-man of the Council of Economic Advisers,and James Hines have in the past concludedthat “the present U.S. system of taxing multi-nationals’ income may be raising little U.S.tax revenue, while stimulating a host of tax-motivated financial transactions.”126

There have been repeated calls for simpli-fying the international tax rules. For exam-ple, the ABA has called for reform, noting,“These rules may never be truly simple, butactions can be taken to temper the extraordi-nary complexity of the current regime.”1 2 7Itis true that these rules may never be simpleunder a worldwide income tax system, butthey can be greatly simplified by replacingthe income tax with a consumption tax.

Consumption-based taxes, including theflat tax, would eliminate most internationaltax rules because they are “territorial” taxes,which do not tax the foreign operations ofU.S. businesses.128 Although all major con-sumption-based tax proposals are territorial,there are differences with regard to U.S.imports and exports. In particular, a nationalretail sales tax would tax imports and exemptexports from U.S. taxation. By contrast, theflat tax would tax firms on their export salesbut allow deductions for foreign inputs toproduction.129

Most economists think these differenceswould not be economically important, butthey would create different issues with regardto tax administration. In particular, underthe flat tax U.S. firms would continue to haveincentives to use “transfer pricing” to shifttheir tax base to low-tax countries, thusrequiring the IRS to continue monitoringsuch activity.130 These pressures also existunder the current income tax. On the otherhand, the low rate of the flat tax and othersof its features would increase the role of theUnited States as a tax haven. In a 1998 study,the U.S. International Trade Commissionconcluded that a consumption-based tax

would, on net, attract greater foreign invest-ment to the United States and encourageU.S. firms to increase capital investment hererather than abroad.131

Business StructureUnder the income tax, companies may take

a variety of legal forms, each with differentincome tax implications. These include soleproprietorship, partnership, LLC, S corpora-tion, and C corporation. This patchwork hascreated tax complexity and economic ineffi-ciency. In theory, reforms could be made with-in the income tax system to simplify this busi-ness framework. But the 90-year history of theincome tax has shown the tendency for thisweb of business structures to grow more com-plex over time. Recent decades have witnessedthe rapid growth of S corporations and LLCsin response to the tax disadvantages of regularC corporations.1 3 2

The flat tax would treat all business activ-ity equally and eliminate special forms ofbusiness organization.1 3 3Bradford notes that“uniform treatment of all businesses,whether corporate or in other form, auto-matically deals with a vast array of complexissues that are intractable under presentlaw.”134 It would also bring greater efficiencyas different investments would return thesame after-tax returns no matter which busi-ness structure the investment took.

A side effect of this simpler organizationof business would be that it would take mostcomplex tax planning issues out of businessrestructurings, such as mergers and acquisi-tions. According to the tax guide publisher,CCH, Inc., the income tax rules governingbusiness reorganizations are “immenselycomplicated” with an “alphabet soup” of atleast seven different methods of reorganiza-tion.135 Some of the different tax implica-tions include whether capital gains are trig-gered and the value of depreciation deduc-tions available after restructuring. These“notoriously complex” tax rules for businessrestructuring “would become almost entirelyobsolete” under the flat tax, according to theAICPA.1 3 6

20

Consumption-based taxes would

eliminate mostinternational tax

rules because theyare “territorial”taxes, which donot tax the for-

eign operations ofU.S. businesses.

21

Many of the areasin which a con-sumption taxwould need spe-cial rules arealready problemareas under theincome tax.

Financial Transactions“The present law tax treatment of finan-

cial instruments is governed by a patchworkof statutory rules located throughout theCode,” notes the JCT.137 This is no coinci-dence; it is inherent in the income taxbecause of the lack of clear and consistentprinciples defining the tax base.

The inconsistencies of capital gains taxa-tion have already been noted. The taxation ofinterest is also complex. For example, interestexpenses receive a range of different treat-ments under the income tax. Interest on per-sonal consumer debt and interest on debtused to purchase tax-exempt municipalbonds is not deductible. But mortgage inter-est is deductible, as is investment interest andnormal business interest. Under currentrules, at least 10 types of interest are subjectto special deduction limitations.1 3 8 Taxaccountants “have bemoaned the inordinatecomplexity” of interest expenses, which “havebecome far more complex” since TRA86.1 3 9

Such inconsistencies lead taxpayers toarbitrage different tax code provisions tolower their tax burden. The governmentresponds with complex rules to limit such“abuse,” and taxpayers invent new methodsto get around the rules.140 For example,because only some types of interest aredeductible, “interest-tracing” rules arerequired to draw lines between differenttypes of interest. These rules are “complexand subject to manipulation,” according tothe JCT.141 A well-known example of interestarbitrage is the increase in home equity loansin recent years to get around TRA86’s disal-lowance of personal interest deductions. Taxrules limit the deductibility of interest onhome equity loans.

Congress could try to tax financial flowson a more comprehensive and consistentHaig-Simons income basis. But as tax attor-ney Sheldon Pollack notes, some of the mostcomplex parts of the tax code stem fromattempts to tax on a Haig-Simons basis.1 4 2

One attempt is the original issue discount, orOID, rules for bond interest. OID rulesrequire interest income to be imputed and

taxed when accrued, not when actuallyreceived by taxpayers. Pollack notes thatthese rules add an “extraordinary andunprecedented level of complexity into thetax laws,” requiring sophisticated computersoftware to figure out how much tax is owed.The OID regulations are 441 pages long.143

A flat tax would eliminate most of theseintractable problems because it generally dis-regards financial flows at both the individualand business level. Under a flat tax, individu-als would not deal with financial flows at all,as they would be taxed only on wage and pen-sion income. Nonfinancial businesses wouldalso not deal with financial income orexpense items. Interest, dividends, and capi-tal gains income would not be included inbusiness taxable receipts, nor would interestexpenses be deductible.

However, financial businesses, such asbanks, would require special rules under aconsumption-based tax and pose a challengeto any tax system.1 4 4The tax base is difficult tomeasure for financial businesses because thevalue of financial services, such as accountadministration costs, are often hidden in mar-gins between borrowing and lending rates.One solution would be to exclude financialbusinesses from a consumption tax, as is thecase under most state retail sales taxes andVATS in foreign countries.145 A number ofother options have been discussed for taxingfinancial businesses under a consumption taxentailing varying levels of complexity.1 4 6

Complexities Not EliminatedWhile a consumption base is a much sim-

pler starting point for a tax system, someareas of complexity would remain. And, nodoubt, under a new tax system various loop-holes would arise that would need to beplugged with additional rules. However,many of the areas in which a consumptiontax would need special rules are already prob-lem areas under the income tax (see Table 3).

Under a consumption tax, as under anincome tax, there are problems of accuratelydefining taxable “consumption” versusdeductible “investment.” A good example is

22

The most effectiveway to reduce the

pressure for socialengineering is tolower overall lev-

els of taxation.

the purchase of a computer for home use. Ifit is mainly used for playing games it shouldbe taxable as consumption, but if it is usedfor a home business it should be deductibleas investment (or depreciable under theincome tax).147 Another example is expendi-tures for education, which may be viewed aseither consumption or investment.

Fringe benefit issues would continue topose challenges as they do under the incometax. Today, many fringe benefits are tax-freeand efforts are expended to engineer employ-ee compensation to fit into this tax-free win-dow. Under the flat tax, fringes would betaxed at the business level by denying adeduction. But problems may arise regardingthe valuation of fringe benefits and separat-ing them from normal business expenses.For example, a company tennis court mightbe considered a taxable fringe benefit anddenied a business deduction, or it might betreated as a deductible business expense.

Defining financial flows under a flat taxwould require special rules. Financial flows,which are generally not in the tax base, wouldneed to be separated from nonfinancialflows. For example, U.S. businesses selling toforeign firms would have an incentive toredefine regular sales receipts as financialincome in order to escape U.S. tax.148 Specialrules would be required to prevent this sortof tax avoidance and evasion.

Complexities Eliminated by DesignThe second and third columns of Table 3