sim/nyu the job of the cfo - nyu stern school of...

TRANSCRIPT

Giddy/SIM Swap Financing/1

Prof. Ian GiddyNew York University

Swap FinancingTechniques

SIM/NYUThe Job of the CFO

Copyright ©2001 Ian H. Giddy Swap Financing 2giddy.org

Interest Rate and Currency Swaps

l Mechanics of swaps

l Valuation of swapsl Credit risk of swaps

l Pricing swaps

l Hedging swaps

l The all-in cost of swap financing

l Currency swaps vs forwards

Giddy/SIM Swap Financing/2

Copyright ©2001 Ian H. Giddy Swap Financing 3giddy.org

Swaps: Mechanics and Valuation

IC&TelIC&Tel CIBCCIBC

Fixed ECU 7%

FloatingECU Libor

Periodic exchanges of interest payments are made during the life of the swap. Remember that the principal amount is not exchanged

Copyright ©2001 Ian H. Giddy Swap Financing 4giddy.org

Interest-Rate Swap Example

CIBC

AA

IC&Tel

BBB Fixed 5.00%Floating 6-MonthLIBOR + 25

Payments to CapitalMarkets

Payments to CapitalMarkets

Giddy/SIM Swap Financing/3

Copyright ©2001 Ian H. Giddy Swap Financing 6giddy.org

Interest-Rate Swap Example

Exchange of Interest Payments Every 6 Mo

Fixed 5.50%

Floating 6-MonthLIBOR Flat

Fixed 5.00%Floating 6-MonthLIBOR + 25

Cost of Funds After Swap:

- Pay fixed 5.50%- Receive LIBOR Flat- Pay LIBOR + 25- Net Cost: 5.75% Fixed

Cost of Funds After Swap:

- Pay 5.00% fixed - Receive 5.50% fixed - Pay 6-month LIBOR Flat- Net Cost: 6-month LIBOR - 50

Payments to CapitalMarkets

Payments to CapitalMarkets

AABBB

CIBCIC&Tel

Copyright ©2001 Ian H. Giddy Swap Financing 7giddy.org

Swap Quotation Screen

GovPX/GGB SwapPX US Medium Term Swaps vs 3M LIBOR 8/6/96 Page 261Term Cpn Mty TrPrice TrYld-SB SwapSpd-SB SwapRate-SB CBA-TED

2Y 6.250 07/98 100.214 /216 5.952 /948 19.50 21.00 6.143 /162 20.233Y 6.375 05/99 100.174 /176 6.103 /100 22.80 23.00 6.327 /333 22.924Y 6.202 /200 26.00 26.50 6.460 /468 25.66

5Y 6.625 07/01 100.114 /120 6.302 /299 27.00 27.80 6.569 /580 26.316Y 6.351 /348 30.00 31.00 6.648 /661 29.467Y 6.400 /397 33.00 34.00 6.726 /740 32.478Y 6.449 /446 33.50 34.50 6.781 /794 33.109Y 6.498 /494 34.50 35.50 6.839 /853 34.16

10Y 7.000 07/06 103.084 /094 6.547 /543 35.00 36.00 6.893 /907 34.7311Y 6.558 /554 38.00 40.00 6.923 /94712Y 6.569 /565 41.00 43.00 6.953 /97713Y 6.581 /577 44.00 45.00 6.983 /99714Y 6.592 /588 48.00 49.00 7.023 /03715Y 6.603 /599 51.00 52.00 7.053 /067

20Y 6.659 /654 53.00 55.00 7.113 /12725Y 6.715 /710 54.00 55.00 7.108 /12230Y 6.000 2/26 90.065 /085 6.771 /766 35.50 37.50 7.121 /146

Giddy/SIM Swap Financing/4

Copyright ©2001 Ian H. Giddy Swap Financing 8giddy.org

A Currency Swap

FMCFMC BANKBANK

GBP 100

USD 150

Company issues dollar debt, but wants sterling financingso exchanges its dollars for sterling equivalent

at today’s spot exchange rate

USD 150

Copyright ©2001 Ian H. Giddy Swap Financing 10giddy.org

Three Parts of a Currency Swap

FMCFMC BANKBANK

GBP 100

USD 150

FMCFMC BANKBANK

Fixed GBP 12%

Floating USDLibor s.a.

FMCFMC BANKBANK

GBP 100

USD 150

Giddy/SIM Swap Financing/5

Copyright ©2001 Ian H. Giddy Swap Financing 11giddy.org

l Valuation

l Off-market swaps

l Cancellation

l Counterparty exposure

l Hedging swap positions

Swaps: Applications of Valuation

BOND

FRN

ABBABB BVBBVB

Fixed ECU 7%

FloatingECU Libor

Copyright ©2001 Ian H. Giddy Swap Financing 12giddy.org

Valuation of an Interest Rate Swap

Valuation of the swap is based on discounting the cash flows over its life.

VALUE OF INTEREST RATE

SWAP

PRICE OFBOND WITH

N YEARSTO RUN

PRICE OFMONEY MARKET

INSTRUMENTWITH

M DAYS TO RUN

= -

A RECEIVE-FIXED, PAY-FLOATING SWAP:

Giddy/SIM Swap Financing/6

Copyright ©2001 Ian H. Giddy Swap Financing 13giddy.org

Labatt’sLabatt’s BankBank

Fixed USD 9%

Floating USDLibor s.a.

Swap Valuation

The value of a swap equals the "net worth" of the swap cash flows expressed as a balance sheet

Labatt’s swap:Receive floating, pay fixed

“ASSETS”

Receiving floating6-mo US$ LiborSemi-annual for 5 yearsPrincipal US$100mLike a 5-year US$ FRN

“LIABILITIES”

Paying fixed 9%Annual for 5 yearsPrincipal US$100mLike a 5-year bond

Copyright ©2001 Ian H. Giddy Swap Financing 14giddy.org

At Inception, Standard Swap is Worth Zero

Labatt’s swap:Receive floating, pay fixed

“ASSETS”

Receiving floating6-mo US$ LiborSemi-annual for 5 yearsPrincipal US$100mLike a 5-year US$ FRN

Value=$100m

”LIABILITIES”

Paying fixed 9%Annual for 5 yearsPrincipal US$100mLike a 5-year bond

Value=$100m

Giddy/SIM Swap Financing/7

Copyright ©2001 Ian H. Giddy Swap Financing 15giddy.org

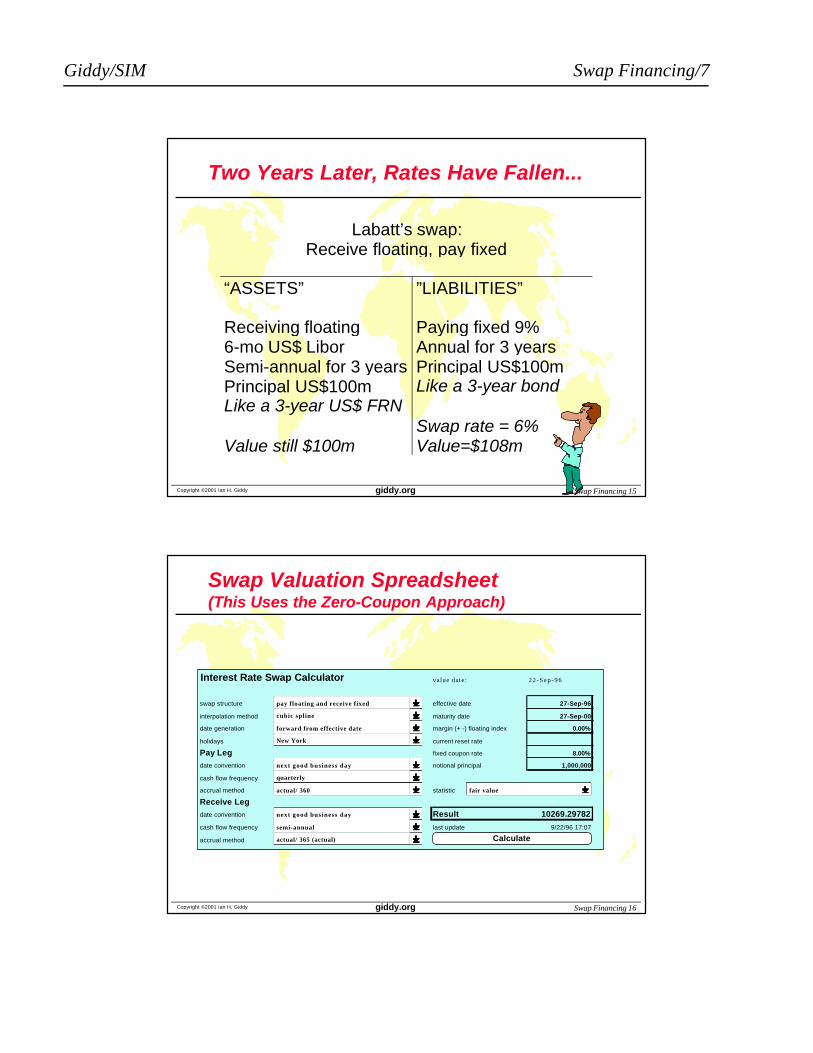

Two Years Later, Rates Have Fallen...

Labatt’s swap:Receive floating, pay fixed

“ASSETS”

Receiving floating6-mo US$ LiborSemi-annual for 3 yearsPrincipal US$100mLike a 3-year US$ FRN

Value still $100m

”LIABILITIES”

Paying fixed 9%Annual for 3 yearsPrincipal US$100mLike a 3-year bond

Swap rate = 6%Value=$108m

Copyright ©2001 Ian H. Giddy Swap Financing 16giddy.org

Interest Rate Swap Calculator value date: 2 2 - S e p - 9 6

swap structure 1 effective date 27-Sep-96

interpolation method 2 maturity date 27-Sep-00

date generation 1 margin (+ -) floating index 0.00%

holidays 6 current reset rate

Pay Leg fixed coupon rate 8.00%

date convention 2 notional principal 1,000,000

cash flow frequency 3

accrual method 2 statistic 1

Receive Legdate convention 2 Result 10269.29782

cash flow frequency 2 last update 9/22/96 17:07

accrual method 3

next good business day

forward from effective date

quarterly

actual/ 360

pay floating and receive fixed

cubic spline

actual/ 365 (actual)

next good business day

semi-annual

New York

fair value

Calculate

Swap Valuation Spreadsheet(This Uses the Zero-Coupon Approach)

Giddy/SIM Swap Financing/8

Copyright ©2001 Ian H. Giddy Swap Financing 17giddy.org

Termination of Swaps

l Basic principle: cancel or neutralize all future swap cash flows

l What are the alternative ways in which this can be done?uOffsetting swap with same counterparty

uOffsetting swap with new counterparty

uCancel swap

uReassign swap.

Copyright ©2001 Ian H. Giddy Swap Financing 18giddy.org

Default Risk in Swaps

l In-the-money swaps entail credit risk—the value of the swap is the amount owed

l At initiation, credit risk exposure is based on the potential value of the swap, which depends on potential changes in interest rates and currencies

l Credit risk can be mitigated by collateralization and by netting of bilateral exposure.

Giddy/SIM Swap Financing/9

Copyright ©2001 Ian H. Giddy Swap Financing 19giddy.org

How Swaps are Quoted

US$ INTEREST RATE SWAPS CURRENCY SWAPSYears Treasury Curve

BenchmarkSemi-Annual

Yields

Spread [b.p.]to AA

Counterparties

DEM/USDAnnual

JPY/USDAnnual

2345710

8.028.018.018.028.138.14

62-6670-7572-7678-8177-8178-81

7.00-7.107.00-7.107.00-7.107.00-7.107.02-7.127.02-7.12

5.35-5.455.35-5.455.35-5.455.35-5.455.40-5.505.45-5.53

CURRENCY SWAPSYears CHF/USD

AnnualGBP/USD

AnnualECU/USD

AnnualAUD/USD

Annual2345710

6.60-6.706.20-6.306.05-6.106.00-6.105.95-6.055.95-6.05

12.80-12.9012.35-12.4511.90-12.0011.75-11.8511.50-11.6011.26-11.36

9.20-9.309.15-9.259.10-9.209.05-9.159.05-9.159.05-9.15

15.65-15.8015.25-15.4015.1515.3014.78-15.13

NANA

Copyright ©2001 Ian H. Giddy Swap Financing 22giddy.org

Swap Spreads are Tied to TED Spreads

TreasurybondsTreasurybills

TEDspread

Swapspread

Interest rateswaps

Corporatebonds

FRAs andfutures

Libor:E$ market

+

+

=

=

LONG TERM

SHORT TERM

Giddy/SIM Swap Financing/10

Copyright ©2001 Ian H. Giddy Swap Financing 23giddy.org

FRAs and Friends

l FRA: A contract to lock in a rate for a future period

l Futures: A daily recontracted FRAl Swap: A strip of FRAs at a blended rate

Copyright ©2001 Ian H. Giddy Swap Financing 24giddy.org

Estimating the Cost of Funds in a Swap

Problem: Convert existing 4 year floating rate dollar sub-LIBOR funds into fixed rate sterling funds. Pay sterling fixed annually; receive dollar floating semi-annually.

What is the all-in sterling cost? Swap Quote Indication Sheet

Swap Quote: Standard four year sterling/dollar swap quote would be sterling 11.90-12.00 against 6 month $ LIBOR flat. If client wants a non-standard swap such as sterling fixed against 6-month $ LIBOR-25, bank might quote: “You pay sterling 11.73% annual, we pay 6-mo LIBOR less 25."

Years Treasury Yields Spread [s.a.] GBP/USD [ann]2345

8.028.018.018.02

62-6670-7572-7678-81

12.80-12.9012.35-12.4511.90-12.0011.75-11.85

Giddy/SIM Swap Financing/11

Copyright ©2001 Ian H. Giddy Swap Financing 25giddy.org

A Standard Currency Swap

FMCFMC BANKBANK

GBP 100

USD 150

FMCFMC BANKBANK

Fixed GBP 12%

Floating USDLibor s.a.

FMCFMC BANKBANK

GBP 100

USD 150

Copyright ©2001 Ian H. Giddy Swap Financing 26giddy.org

FMCFMC BANKBANK

Fixed GBP 12%

Floating USDLibor s.a.

Estimating the Cost of Funds in a Swap

Fixed GBP 11.73%

Floating USDLibor s.a.

-0.25%

Floating USDLibor -0.25%

Giddy/SIM Swap Financing/12

Copyright ©2001 Ian H. Giddy Swap Financing 27giddy.org

Basis Point Conversion:The quote of Sterling 11.73% annual fixed payments

against LIBOR - 25 required conversion from dollar basis points to sterling basis points.

How to do this:1. Find present value of 25 U.S. dollar basis points paid

semi-annually at 8.77% interest.

2. Find the sterling annuity equivalent of 82.84 at the sterling swap rate of 12.00% paid annually.

Annuity value of 82.84 @ 12% [annual] = 27.27bpGBP

Estimating the Cost of Funds in a Swap

PV bp bpUS tt[ ]

.( .

.$2512 5

1 4 385%)82 84

1

8=

+=

=∑

Copyright ©2001 Ian H. Giddy Swap Financing 28giddy.org

l Kalamazoo needs $60 million.l Receiving Euro, the European Currency unit.

Whose Zoo?

l K’zoo could borrow five-year money at semi-annual LIBOR + 3/4%, andDresdner agreed to enter into a currency swap with the company.u Diagram the swap with little boxes.u What would K’zoo's cost of capital be if it

did the swap? (US 5-yr swap rate = 10%)u Effect of a rise in ST & LT rate?u How would a 0.75% up front commitment

fee affect K’zoo's cost of capital?

DRESDNERSWAP

QUOTATIONS

Years

Euro Fixedvs USD Libor

sa23457

10

8.00 - 8.108.00 - 8.108.20 - 8.308.20 - 8.358.25 - 8.358.40 - 8.50

Giddy/SIM Swap Financing/13

Copyright ©2001 Ian H. Giddy Swap Financing 29giddy.org

Kalamazoo

K’ZOOK’ZOO DRESDNERDRESDNER

Fixed ECU 8.35%

Floating USDLibor s.a.

Fixed EURO 8.35+0.73%=9.08%

Floating USD Libor +0.75%

Floating USDLibor +0.75%

l 75bpUSD=73bpEuro; swapped cost is 9.08%

l ST rate: no effect. LT rate rise: value of swap will change by duration. K’zoo gains, Dresdner loses.

l Amortize the up-front fee of 0.75% over the period of the financing, and add it to swapped cost..

Euro revenues

Copyright ©2001 Ian H. Giddy Swap Financing 30giddy.org

BP Conversion: Excel Spreadsheet

Basis Point ConversionEnter the blue numbers

First currencyNUMBER OF BASIS POINTS (US$) 75US$ INTEREST RATE 10.00%NUMBER OF PAYMENT PERIODS PER YEAR 2NUMBER OF YEARS 5

PRESENT VALUE OF BASIS POINTS (US$) 290

Second currencyEuro INTEREST RATE 8.35%NUMBER OF PAYMENT PERIODS PER YEAR 1NUMBER OF YEARS 5

NUMBER OF BASIS POINTS (Euro) (ANNUITY EQUIV) 73.2

Giddy/SIM Swap Financing/14

Copyright ©2001 Ian H. Giddy Swap Financing 31giddy.org

INVESTORINVESTOR

Asset Swaps: The Same Idea

Fixed GBP 12.73%

l Investor buys cheap fixed-rate bond

l But wants a floating-rate note.

Copyright ©2001 Ian H. Giddy Swap Financing 32giddy.org

INVESTORINVESTOR BANKBANK

Fixed GBP 12%

Floating USDLibor s.a.

Asset Swaps: The Same Idea

Fixed GBP 12.73%

Floating USDLibor s.a.+0.75%

Fixed GBP 12.73%

Giddy/SIM Swap Financing/15

Copyright ©2001 Ian H. Giddy Swap Financing 33giddy.org

Currency Swapsvs Long-dated Forwards

SF

SFSF

£

£

LONG-DATED FORWARD

SPOTRATE

End-period exchange occurs atforward rate , which representsthe spot rate plus thecumulative interest tatedifferential.

FORWARDRATE

Copyright ©2001 Ian H. Giddy Swap Financing 34giddy.org

Currency Swapsvs Long-dated Forwards

SF SF

SFSFSF

£ £

££

LONG-DATED FORWARD CURRENCY SWAP

SPOTRATE

SPOTRATE

PERIODICINTERESTRATEDIFFERENTIAL

End-period exchange occurs atforward rate , which representsthe spot rate plus thecumulative interest tatedifferential.

End-period exchange occurs atspot rate , since thecumulative interest tatedifferential is paid duringinterim periods.

FORWARDRATE

SPOTRATE

Giddy/SIM Swap Financing/16

Copyright ©2001 Ian H. Giddy Swap Financing 35giddy.org

A Basis Swap

FujiBank

FujiBank CitiCiti

Fuji makes a loan at Prime + Spread, but gets funding in the Eurodollar interbank market

Prime + Spread

FloatingLibor

Copyright ©2001 Ian H. Giddy Swap Financing 36giddy.org

A Basis Swap

FujiBank

FujiBank CitiCiti

Prime

FloatingLibor

Fuji makes a loan at Prime + Spread, but gets funding in the Eurodollar interbank market

Fuji wants to lock in its spread, so does a basis swap with Citibank

Prime + Spread

FloatingLibor

Giddy/SIM Swap Financing/17

Copyright ©2001 Ian H. Giddy Swap Financing 37giddy.org

Basis Swap Quotations

GovPX/GGB GovPX Index Basis Swaps vs 3M LIBOR 8/6/96 Page 262 Prime vs LIBOR Fix LIBOR Fed Funds vs LIBOR

Term Pay Prime Rec Prime 1M 5 7/16 Term Pay FF Rec FF1Y P- 271 P- 267 3M 5 1/2 1Y FF+ 21 1/2 FF+ 23 1/22Y P- 268 P- 264 6M 5 11/16 2Y FF+ 23 FF+ 253Y P- 267 P- 263 Mkt LIBOR 3Y FF+ 23 1/2 FF+ 25 1/24Y P- 265 P- 261 1M 5 7/16 4Y FF+ 24 1/2 FF+ 26 1/25Y P- 263 P- 259 3M 5 1/2 5Y FF+ 25 FF+ 277Y P- 260 P- 255 6M 5 11/16 7Y FF+ 26 FF+ 2810Y P- 259 P- 254 10Y FF+ 26 FF+ 28 3M T-Bill vs LIBOR Prime 8.25 CP vs LIBOR

Term Pay T-Bill Rec T-Bill Term Pay CP Rec CP1Y B+ 37 B+ 40 Fed Funds 1Y CP+ 4 3/4 CP+ 6 3/42Y B+ 39 B+ 42 5 1/16-1/8 2Y CP+ 5 CP+ 63Y B+ 40 1/2 B+ 43 1/2 3Y CP+ 5 1/4 CP+ 6 1/24Y B+ 43 B+ 47 3M T-Bill Yld 4Y CP+ 5 1/2 CP+ 6 3/45Y B+ 44 B+ 48 5.171-166 5Y CP+ 6 CP+ 77Y B+ 45 B+ 49 7Y CP+ 6 1/2 CP+ 810Y B+ 46 B+ 50 30D CP 5.32 10Y CP+ 7 CP+ 9

Alert Line

Copyright ©2001 Ian H. Giddy Swap Financing 38giddy.org

A Basis Swap

FujiBank

FujiBank CitiCiti

Prime-263

Floating3-mo Libor

Fuji makes a 3-year loan at Prime + 1%, and swaps at P-2.63%

Fuji thus locks in a spread of 3.63%

Prime + 1%

FloatingLibor flat

Giddy/SIM Swap Financing/18

Copyright ©2001 Ian H. Giddy Swap Financing 39giddy.org

Commodity Swap Example: Qantas

QANTASQANTAS

US$ LIBOR +1/4%SEMIIANNUAL

PASSENGERREVENUES

FUELCOSTS

Copyright ©2001 Ian H. Giddy Swap Financing 40giddy.org

Example: Qantas

QANTASQANTAS PARIBASPARIBAS

US$ LIBOR +1/4%SEMIIANNUAL

PASSENGERREVENUES

FUELCOSTS

Giddy/SIM Swap Financing/19

Copyright ©2001 Ian H. Giddy Swap Financing 41giddy.org

Example: Qantas

QANTASQANTAS PARIBASPARIBAS

US$ LIBOR +1/4%SEMIIANNUAL

US$ FIXED 10%+/- $30 M X (1-%CH AW INDEX)

US$ LIBOR +1/4%SEMIIANNUAL

Copyright ©2001 Ian H. Giddy Swap Financing 42giddy.org

Summary

l Mechanics of swaps

l Valuation of swapsl Credit risk of swaps

l Pricing swaps

l Hedging swaps

l The all-in cost of swap financing

l Swap around the clock

Giddy/SIM Swap Financing/20

Copyright ©2001 Ian H. Giddy Swap Financing 44giddy.org

Ian H. Giddy

Stern School of Business

New York University

44 West 4th Street, New York, NY 10012, USA

Tel 212-998-0332

Fax 917-463-7629

http://giddy.org