sidoti & company -...

TRANSCRIPT

Sidoti

& Company Emerging Growth Conference March 24, 2009

2 ©2009 Veeco Instruments Inc 020909 Investor Slides

Veeco Business SnapshotVeeco Business Snapshot

LED & SolarProcess Equipment

Data StorageProcess Equipment Metrology

Core Technologies

MOCVD, MBE,CIGS Sources, CIGS Web Coaters

Ion Beam Etch & Deposition,

DLC, PVD, CVD,Saws & Lappers

Atomic Force Microscopes,

Stylus & Optical Profilers

2008 Revenue $166M $149M $128M

Veeco Market Position #1 or #2 #1 equipment supplier

for TFMH manufacturing

#1 or #2 -

large share in

all products

Multi-YearEnd Market Growth Rate*

20% LED

50% Solar5% 3-10%

*Sources: Strategies Unlimited, Canaccord, IDC, SDI, NSF, Veeco Estimates

3 ©2009 Veeco Instruments Inc 020909 Investor Slides

2008 Financial Results2008 Financial Results

Revenue up 10% to $443M

OPEX flat

EBITA increased 163% from $11M to $28M

Significantly improved balance sheet: generated cash and paid down debt

Met Street guidance every quarter

LED & Solar$166M

37% of Total43% Growth Rate

Data Storage $149M

34% of Total10% Growth Rate

Metrology$128M

29% of Total-15% Growth Rate

LED & Solar Becomes Largest Veeco Business in 2008

4 ©2009 Veeco Instruments Inc 020909 Investor Slides

2008: Refocused Company and Drove Improved Performance 2008: Refocused Company and Drove Improved Performance

Increased growth & profit in “green” equipment business (LED & Solar)–

Secured key new customers for MOCVD with K465 –

Realigned R&D spend: LED & Solar up 38%–

Grew “Solar”

revenues to >$40M in 2008 (CIGS and CPV)

Realigned Data Storage Business–

Consolidated overhead and locations; increased outsourcing–

Remained aligned with customers on key technology requirements

Refocused Metrology business with new leadership to execute operational turnaround

Strengthened organization and increased effectiveness across theCompany–

Better product development programs –

Improved manufacturing efficiency: supply chain management, outsourcing initiatives

–

Strengthened sales channel

5 ©2009 Veeco Instruments Inc 020909 Investor Slides

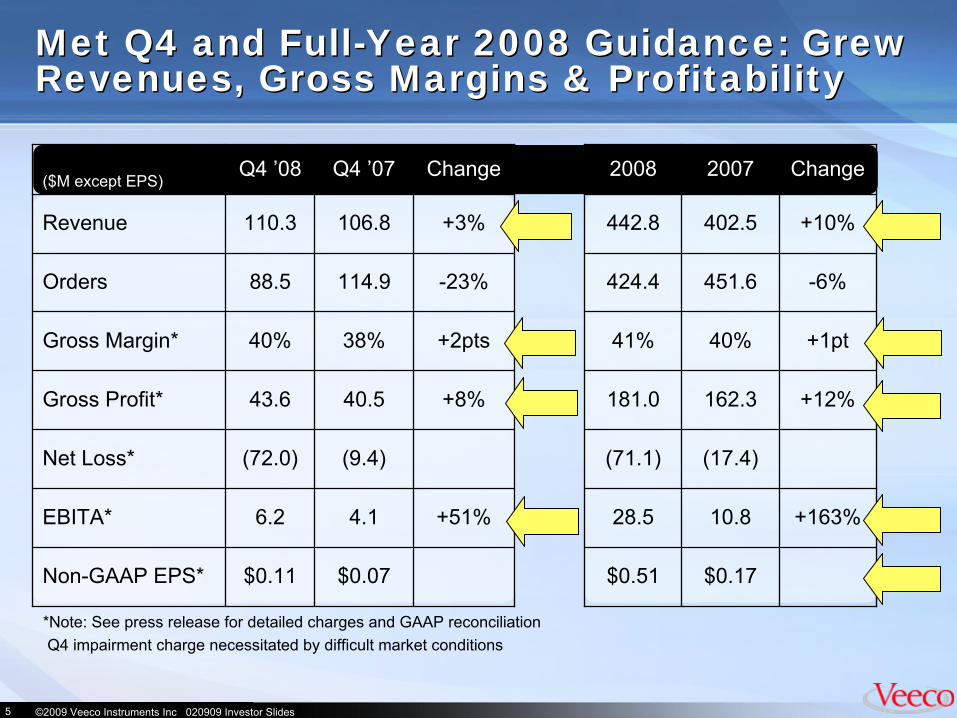

Met Q4 and Full-Year 2008 Guidance: Grew Revenues, Gross Margins & Profitability Met Q4 and Full-Year 2008 Guidance: Grew Revenues, Gross Margins & Profitability

*Note: See press release for detailed charges and GAAP reconciliationQ4 impairment charge necessitated by difficult market conditions

($M except EPS)Q4 ’08 Q4 ’07 Change 2008 2007 Change

Revenue 110.3 106.8 +3% 442.8 402.5 +10%

Orders 88.5 114.9 -23% 424.4 451.6 -6%

Gross Margin* 40% 38% +2pts 41% 40% +1pt

Gross Profit* 43.6 40.5 +8% 181.0 162.3 +12%

Net Loss* (72.0) (9.4) (71.1) (17.4)

EBITA* 6.2 4.1 +51% 28.5 10.8 +163%

Non-GAAP EPS* $0.11 $0.07 $0.51 $0.17

6 ©2009 Veeco Instruments Inc 020909 Investor Slides

Market Conditions WeakenMarket Conditions Weaken

End Market Conditions:–

LED & Solar: Q4 bookings better than expected…$44M included multi-system orders for LED & Solar…but outlook weak for new orders

–

Data Storage: customers have frozen CAPEX; Q4 bookings of $14M included no system orders…some “technology buy”

opportunities exist

–

Metrology: Relatively stable environment for industrial and research market products, Q4 bookings flat at $31M…

weak conditions continue in data storage and semiconductor

LED & Data Storage customers push-out $30M of revenue from Q109…nearly half of $147M backlog currently forecasted for 2H09 revenue

Q1 Guidance:–

Q109 Orders expected to be weaker than Q408–

Q109 Revenue Guidance: $60-70M–

non-GAAP EPS ($0.25)-($0.17)

Restructuring program implemented to significantly lower Company breakeven

7 ©2009 Veeco Instruments Inc 020909 Investor Slides

Significantly Improved Balance Sheet in 2008 Significantly Improved Balance Sheet in 2008

Retired $25M notes due 12/08

Repurchased $12.2M due 4/12 at very favorable pricing

Q2 acquisition of Mill Lane, initial purchase price $11M

Generated significant cash in 2008 - $19M free cash flow in Q4 alone

Cash balance at year-end $104M…net debt now $5M

Currently anticipate positive generation of cash in 2009

Balance of 12/31220

200

143

10596

5326

50

50

100

150

200

250

2005 2006 2007 2008

($M

)

Convertible Debt Net Debt

Restructuring Plan

9 ©2009 Veeco Instruments Inc 020909 Investor Slides

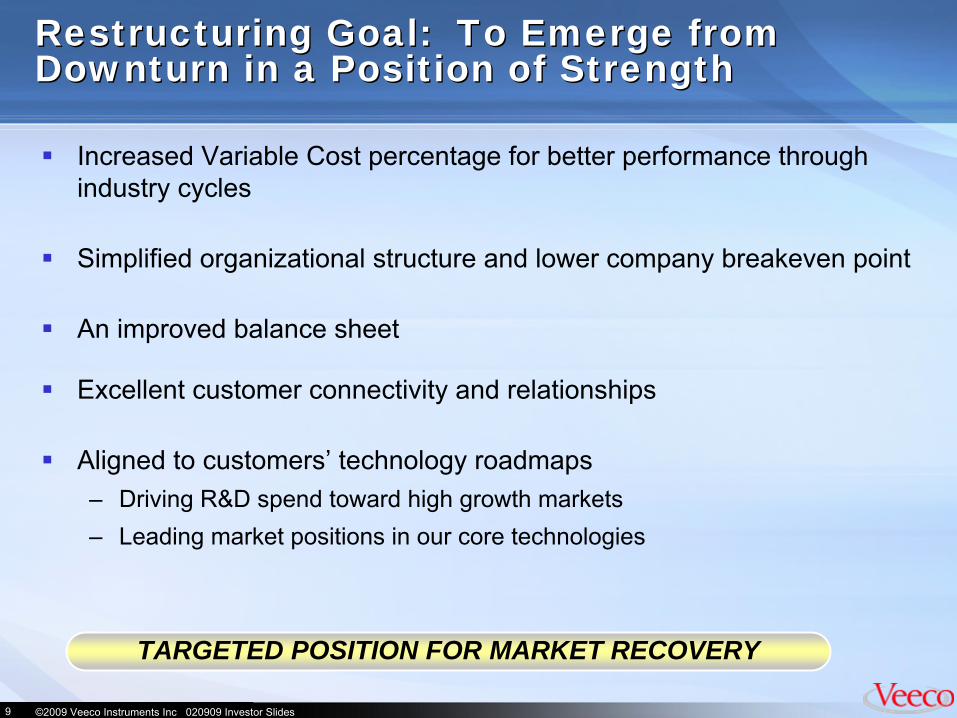

Restructuring Goal: To Emerge from Downturn in a Position of Strength Restructuring Goal: To Emerge from Downturn in a Position of Strength

Increased Variable Cost percentage for better performance through industry cycles

Simplified organizational structure and lower company breakeven point

An improved balance sheet

Excellent customer connectivity and relationships

Aligned to customers’ technology roadmaps–

Driving R&D spend toward high growth markets–

Leading market positions in our core technologies

TARGETED POSITION FOR MARKET RECOVERY

10 ©2009 Veeco Instruments Inc 020909 Investor Slides

Restructuring Program To Lower Quarterly Breakeven to $80M Goal to Return to EBITA Profitability by Q409

Restructuring Program To Lower Quarterly Breakeven to $80M Goal to Return to EBITA Profitability by Q409

26% reduction in force (340 employees) – 70% complete by end Q1’09–

1318 employees as of 9/30/08–

Remainder of impacted employees will exit Veeco by 12/31/09 aligned with manufacturing transitions

–

End of year headcount targeted <1,000

Centralized supply chain and operational organizations (began ’08)…qualified key APAC critical component vendors…driving material cost reductions

Reduce manufacturing sites from 8 to 4 by end 2009–

Product development/R&D groups remain for core technologies

Increase outsourcing: lower expenses & improve variable cost structure–

2008 progress begins to pay-off: by end of 2009 >80% of Veeco’s PE systems will be outsourced

MOVE TO AN ORGANIZATIONAL STRUCTURE THAT ENABLES NEAR-TERM RETURN TO PROFITABILITY AND 15% EBITA AFTER MARKET RECOVERY

11 ©2009 Veeco Instruments Inc 020909 Investor Slides

Decrease number of individual Veeco business units (cuts G&A)

2009 Compensation Changes:–

Executive pay cuts–

Decreased Board of Director compensation–

Employee wage freezes

Significantly cut discretionary spending: travel, IT,Telecom, operating supplies, MarCom, etc.

Restructuring results annualized savings of >$36M: –

Approximately $20M reduction in manufacturing labor and overhead

and service costs which are included in cost of goods sold

–

$16M reduction in operating spending

MOVE TO AN ORGANIZATIONAL STRUCTURE THAT ENABLES NEAR-TERM RETURN TO PROFITABILITY AND 15% EBITA AFTER MARKET RECOVERY

Restructuring Program ContinuedRestructuring Program Continued

12 ©2009 Veeco Instruments Inc 020909 Investor Slides

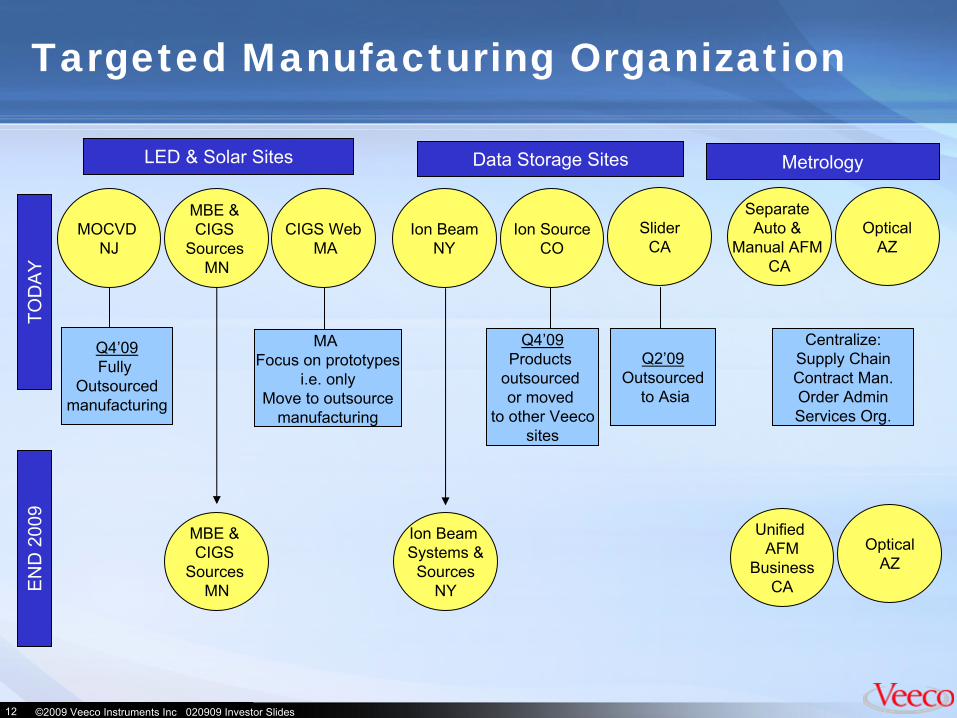

Targeted Manufacturing Organization

OpticalAZ

Separate Auto &

Manual AFM CA

SliderCA

Ion SourceCO

Ion BeamNY

CIGS WebMA

MBE & CIGS

Sources MN

MOCVD NJ

MBE & CIGS

Sources MN

MA Focus on prototypes

i.e. onlyMove to outsource

manufacturing

Q4’09Fully

Outsourcedmanufacturing

Q4’09Products

outsourced or moved

to other Veecosites

Q2’09Outsourced

to Asia

Centralize:Supply ChainContract Man.Order AdminServices Org.

Ion Beam Systems &

SourcesNY

OpticalAZ

Unified AFM

BusinessCA

LED & Solar Sites Data Storage Sites Metrology

TOD

AY

EN

D 2

009

13 ©2009 Veeco Instruments Inc 020909 Investor Slides

Restructuring Program Drives Lower Breakeven in 2009 Restructuring Program Drives Lower Breakeven in 2009

Q4 ’08 Q1 ’09 “Trough” Breakeven Quarter

“Modest Recovery”

Quarter

“End Market Recovery”

Model

Revenue $110M $60-70M $80M $90-100M $110-120M

GM 39.5% 33-36% 41-42% 43-44% 45-46%

Operating Spending $37M $33-34M $34-35M $35-36M $35-36M

EBITA%* 6% (10) –

(20)% 0-1% 6-7% 15-17%*

*Note: Beginning in Q1’09 EBITA calculation will exclude equity-based compensation. Q4 08 EBITA exclusive of equity based compensation is 7%.

14 ©2009 Veeco Instruments Inc 020909 Investor Slides

Aligning Veeco R&D to High Growth Market Opportunities Aligning Veeco R&D to High Growth Market Opportunities

20%20%16%

44% 44%

23%

7%

26%

0%

10%

20%

30%

40%

50%

Hard Disk Drives Semiconductor Chips Research & Industrial Market LED & Solar Devices

Actual R&D Spending % by Mkt '07 Forecasted R&D Spending % by Mkt '09

Approx. End Market 5% 5% 3-10% LED 20% Solar 50% Growth Rate

MAINTAIN COMMITMENT TO CUSTOMER ROADMAPSIN ALL MARKETS

More than doubling R&Din LED & Solar

Growth Opportunities

LED & Solar

17 ©2009 Veeco Instruments Inc 020909 Investor Slides

HB-LED Growth OpportunityHB-LED Growth Opportunity

Strategies Unlimited LED Growth Forecast

2,000

4,000

6,000

8,000

10,000

12,000

020122007 2008 2009 2010 2011

$B

other illumination signals automotive

signs & displays other mobile mobile phones

Veeco is #2 supplier of MOCVD for HB-LEDs

–

Significant in-roads in penetrating key customers in ‘08

Despite current overcapacity…remain optimistic about MOCVD TAM and end market applications:–

$250M 2007–

$500M 2011*

Customers are investigating transition to larger wafer size

*internal forecasts

>40%

Displays for outdoor apps, LCD-TV & Architectural growing >40%

20% CAGR

18 ©2009 Veeco Instruments Inc 020909 Investor Slides

LED Market Segmentation & Trends LED Market Segmentation & Trends

Standard LED(<0.1W)

High Current – HB LED

(0.1W to 1W)

High Power – UHB LED

(1W to 10W)Market GrowthCAGR (’07-’11)

0% -

5% > 10% > 40%

Main Applications Keypad lightingTraffic SignalsMobile Devices

Laptop BLUSigns/DisplaysOther Mobile

General LightingAutomotiveSign/Displays

Key Challenge for Customers

Low cost devicesHigh Volume

UniformityBrightnessLowest CoO

Brightness is kingUniformityLowest CoO

Customer Types Cost PlayersChina, CMLT, Tier

2 customers in Taiwan & China

Mass Production Tier 1, AUO,

Semco, LG, Epistar

Technology PlayersTier 1 – Lumileds,

Osram, SDK, TG, Nichia, Cree, Semco

Chip Size < 0.2mm2 0.2mm2

to 0.5mm2 0.5mm2

to 1.0mm2

Wafer Size Trend 2” 2”

→ 4” 2”

→ 4”

→ 6”

Source: Veeco/Strategies Unlimited

19 ©2009 Veeco Instruments Inc 020909 Investor Slides

Lowering LED Customer Cost/WaferLowering LED Customer Cost/Wafer

Three focus areas to increase yield and lower cost/wafer:

–

Improve binning through uniformity improvements

–

Increase productivity to reduce CoO

–

Reduce source consumption

Veeco MOCVD enables seamless transition to larger wafer sizes

Working closely with several strategic accounts to gain share

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.10

0.11

0.12

0.13

452 454 456 458 460 462 464 466 468

K465 GaNK465 GaN

K300 GaNK300 GaN

Bin 1 Bin 2 Bin 3 Bin 4 Bin 5

$0.01 $0.03 $0.07 $0.03 $0.01

20 ©2009 Veeco Instruments Inc 020909 Investor Slides

MOCVD for Concentrator (CPV) Solar Cells MOCVD for Concentrator (CPV) Solar Cells

Past market driven primarily by space applications

Potential expansion for terrestrial applications to 1GW by 2012

TurboDisc E475: Market share leader with highest productivity & lowest CoO for CPV

–

World-class process performance = high cell efficiency

–

Highest production throughput

–

Low maintenance enables industry’s highest uptime

TurboDisc E475

21 ©2009 Veeco Instruments Inc 020909 Investor Slides

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2008 2009 2010 2011 2012 2013 2014 2015

Source: NanoMarkets, LC

Emerging Opportunity in Thin Film CIGS Solar

Handful of companies producing up to 30MW of CIGS cells

Dozens more in various stages of pilot production

CIGS on flexible substrate provides new application opportunities compared to rigid materials

Equipment needs to be developed & performance improved – excellent entry point for Veeco solutions

CIGS/CIS thin-film Production Capacity (MW)

CIGS EMERGING AS LOW COST/HIGH EFFICIENCY ALTERNATIVE TO SILICON SOLAR WITH BROAD MARKET APPLICATIONS

22 ©2009 Veeco Instruments Inc 020909 Investor Slides

0.00

0.25

0.50

0.75

1.00

1.25

Silicon a-Si a-Si* CdTe CIGS

CIGS Projected to be Most Cost Competitive PV Technology CIGS Projected to be Most Cost Competitive PV Technology

Source: NREL, Presented at the 33rd IEEE Photovoltaic Specialists Conference San Diego, California May 11–16, 2008

Lower is Better

Anticipated Future Relative Cost

*Triple Junction

[Relative Cost analysis comparing factors such as efficiency, materials and manufacturing process]

23 ©2009 Veeco Instruments Inc 020909 Investor Slides

CIGS on Flexible Has Broadest Market Opportunity CIGS on Flexible Has Broadest Market Opportunity

Market CIGS C-Si a-Si Note

Solar FarmsLow efficiency ok

for large area installations

Building Integrated PV (BIPV)

Flexible substrate required, black

appearance

Rooftop Grid Connected

High efficiency required for small

surface area

Portable Devices

Flexible substrate required with high

efficiency

24 ©2009 Veeco Instruments Inc 020909 Investor Slides

Veeco’s Rapidly Expanding CIGS Product Portfolio Veeco’s Rapidly Expanding CIGS Product Portfolio

Veeco thermal deposition sources used by 14 CIGS manufacturers

FastFlex Platform for Flexible CIGS Solar Cells: Mo, TCO & now offer CIGS layer

Anticipate Q1 launch of FastLinePlatform for Glass CIGS Solar Cells

Quoting Veeco solutions to broad range of customers

FastFlex Web Coating System

PV-Series CIGS Sources

25 ©2009 Veeco Instruments Inc 020909 Investor Slides

Veeco Supplies Equipment for 3 out 4 Process Steps Veeco Supplies Equipment for 3 out 4 Process Steps

SEM Cross section Picture of a Typical CIGS film

TCOCdS

CIGS

Mo

Liquid Bath Deposited CdS Buffer Layer

Sputtering of ZnO+AZO Front Window Layer

Co-evaporation of Cu-In-Ga-Se Absorber Layer

Sputtering of the Mo Back Contact Layer

26 ©2009 Veeco Instruments Inc 020909 Investor Slides

Evaporation is the Best CIGS SolutionEvaporation is the Best CIGS Solution

Process of record for 20.0% efficiency cells65% of today’s CIGS manufacturing capacity use thermal evaporationLowest manufacturing costVeeco supplies sources to more than 50% of CIGS companies 3/5/09: –

Received Large Multi-Million Dollar Order

–

Korean Steel Manufacturer to Build CIGS Solar Cell Line

Data Storage

28 ©2009 Veeco Instruments Inc 020909 Investor Slides

Technology Trends & Areal Density Growth Technology Trends & Areal Density Growth

Customer capexdeclines in difficult economic climate

HDD makers must invest in new technology to lower $/GB cost

Veeco products aligned to technology requirements–

#1 provider of TFMH equipment

–

Leading edge products throughout TFMH process

0

200

400

600

800

1000

1200

1400

1600

1800

2006 2007 2008 2009 2010 2011 2012Year

WRITER PMR Damascene Pole HAMR/Assisted

READER TMR Low Energy Etch CPP-GMR

SLIDER Ultra-thin Carbon Overcoat (<20 Å)

MEDIA Conventional DTM

HDD Technology Trends and Areal Density Growth

DLC-X

CVD

IBE 420-EX

PVD-HR

Are

alD

ensi

ty [G

B/in

2 ]

Lab & Leading Edge Products

Volume Production Areal Density

29 ©2009 Veeco Instruments Inc 020909 Investor Slides

Key Products Aligned with Customers’ Technology Roadmaps for 2009 Key Products Aligned with Customers’ Technology Roadmaps for 2009

NEXUS PVD-HR

NEXUS DLC-X

Step coverage95 -105 %

~ 0.4 μm trenches

Step coverage95 -105 %

~ 0.4 μm trenches

NEXUS IBE

420-EX

Conformal films for small dimensions High productivity for overcoat films

Ultra-thin diamond-like coating for heads 3x uniformity improvement and low energy etching for smaller features

NEXUS CVD

Metrology

31 ©2009 Veeco Instruments Inc 020909 Investor Slides

Leadership in Scientific and Focus on Growth Markets within Industrial Metrology

Leadership in Scientific and Focus on Growth Markets within Industrial Metrology

Take share and expand market in AFM–

Turning the product development machine around

–

Increasing Nano-Functionality: Nano-

Analytical Thermal Analysis, Material properties mapping and Nano-Biological

–

Attacking operational costs

Growth in Optical / Stylus–

Focused application work on growth segments

–

Orienting product development towards significant industrial opportunities

–

Alignment with strong regional growth opportunities

Innova AFM

Wyko NT 9100

32 ©2009 Veeco Instruments Inc 020909 Investor Slides

New AFM Products Are Best in ClassNew AFM Products Are Best in Class

New Dimension Icon AFMThe world’s highest resolution large sample AFMMost productive AFM – Fastest time to resultsVery easy to use – intuitive user interface

Innovative New Nano-Analytical Components that Expand Functionality•VITA: Mapping thermal properties at the nanoscale•HarmonixTM: Mapping material properties at the nanoscale

33 ©2009 Veeco Instruments Inc 020909 Investor Slides

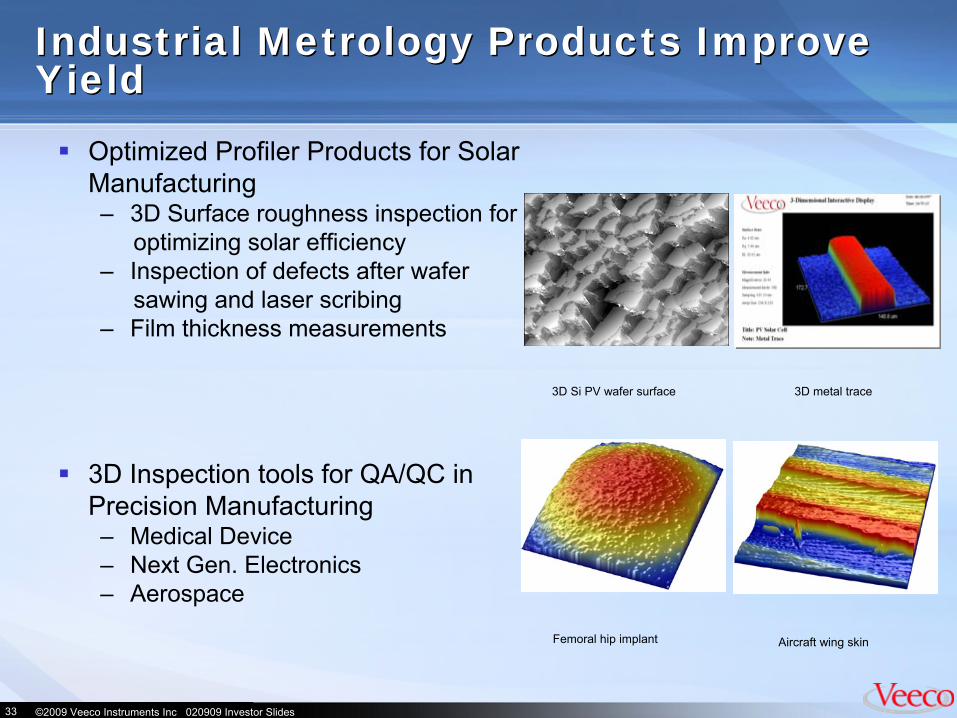

Industrial Metrology Products Improve Yield Industrial Metrology Products Improve Yield

Optimized Profiler Products for Solar Manufacturing–

3D Surface roughness inspection for optimizing solar efficiency

–

Inspection of defects after wafer sawing and laser scribing

–

Film thickness measurements

3D Inspection tools for QA/QC in Precision Manufacturing–

Medical Device –

Next Gen. Electronics–

Aerospace

Femoral hip implant Aircraft wing skin

3D Si PV wafer surface 3D metal trace

34 ©2009 Veeco Instruments Inc 020909 Investor Slides

SummarySummary

Q308 Actual“End Market Recovery”

Model

Revenue $116M $110-120M

GM 41% 45-46%

Operating Spending $39M $35-36M

EBITA%* 7.2% 15-17%*

Track record of solid execution in challenging 2008

Swift action to restructure Veeco:–

Simpler, more cost effective structure–

New quarterly breakeven $80M

Scalable operational model capable of delivering solid profitability

Aligned to multi-year technology growth opportunities

*Note: Beginning in Q1’09 EBITA calculation will exclude equity-based compensation. Q3 08 EBITA exclusive of equity based compensation is 8%.

35 ©2009 Veeco Instruments Inc 020909 Investor Slides

Safe Harbor StatementSafe Harbor Statement

To the extent that this presentation discusses expectations or otherwise make statements about the future, such statements are forward-looking and are subject to a number of risks and uncertainties that could cause actual results to differ materially from the statements made. These factors include the risk factors discussed in the Business Description and Management's Discussion and Analysis sections of Veeco's Annual Report on Form 10-K for the year ended December 31, 2007 and subsequent Quarterly Reports on Form 10-Q and current reports on Form 8-K. Veeco does not undertake any obligation to update any forward-looking statements to reflect future events or circumstances after the date of such statements.

In addition, this presentation includes non-GAAP financial measures. For GAAP reconciliation, please refer to the reconciliation section in this presentation as well as Veeco’s financial press releases and 10-K and 10-Q filings available on www.veeco.com.

36 ©2009 Veeco Instruments Inc 020909 Investor Slides

Back-Up and Reconciliation SlidesBack-Up and Reconciliation Slides

37 ©2009 Veeco Instruments Inc 020909 Investor Slides

Income StatementIncome Statement

(In thousands, except per share data)2008 2007 2008 2007

(Unaudited) (Unaudited)

Net sales $110,344 $106,822 $442,809 $402,475Cost of sales 70,189 71,145 266,215 244,964 Gross profit 40,155 35,677 176,594 157,511

Operating expenses:Selling, general and administrative expense 22,310 21,625 92,838 90,972 Research and development expense 15,180 14,833 60,353 61,174 Amortization expense 3,215 2,014 10,745 10,250 Restructuring expense 3,567 4,752 10,562 6,726 Asset impairment charge 73,037 1,068 73,322 1,068 Other income, net (77) (13) (668) (618)

Operating loss (77,077) (8,602) (70,558) (12,061)

Interest expense, net 899 757 3,812 3,013 Gain on extinguishment of debt (4,969) - (4,969) (738)

Loss before income taxes and noncontrolling interest (73,007) (9,359) (69,401) (14,336)

Income tax (benefit) provision (968) 161 1,892 3,651 Noncontrolling interest (30) (146) (230) (628) Net loss ($72,009) ($9,374) ($71,063) ($17,359)

Loss per common share:Net loss per common share ($2.29) ($0.30) ($2.27) ($0.56)Diluted net loss per common share ($2.29) ($0.30) ($2.27) ($0.56)

Weighted average shares outstanding 31,500 31,128 31,347 31,020 Diluted weighted average shares outstanding 31,500 31,128 31,347 31,020

Year endedDecember 31,December 31,

Three months ended

38 ©2009 Veeco Instruments Inc 020909 Investor Slides

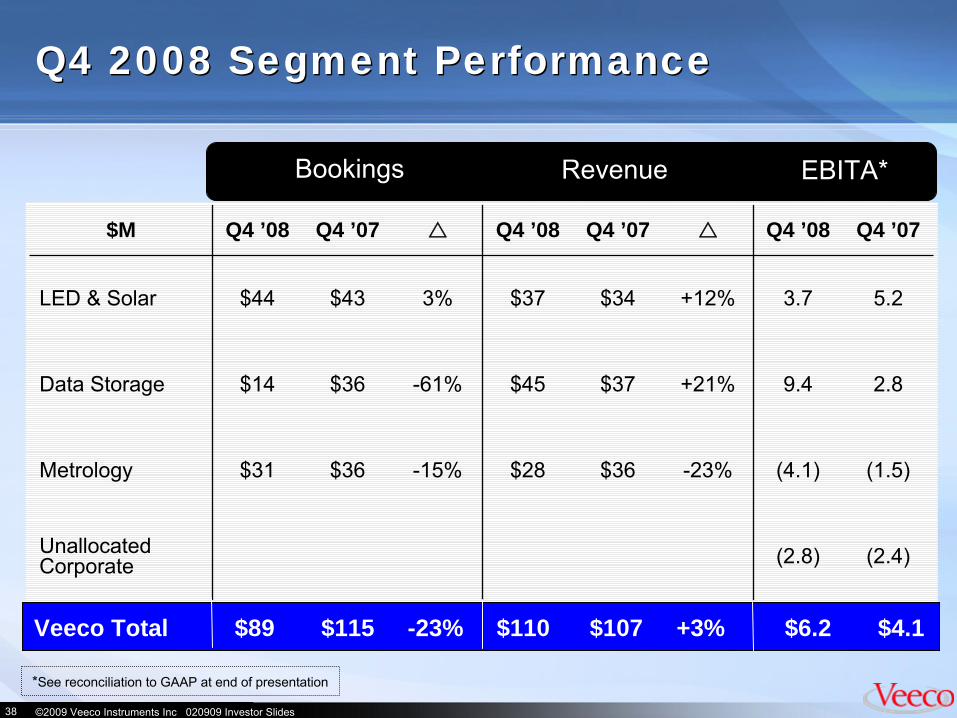

Q4 2008 Segment Performance Q4 2008 Segment Performance

*See reconciliation to GAAP at end of presentation

$M Q4 ’08 Q4 ’07 Q4 ’08 Q4 ’07 Q4 ’08 Q4 ’07

LED & Solar $44 $43 3% $37 $34 +12% 3.7 5.2

Data Storage $14 $36 -61% $45 $37 +21% 9.4 2.8

Metrology $31 $36 -15% $28 $36 -23% (4.1) (1.5)

Unallocated Corporate (2.8) (2.4)

Bookings Revenue EBITA*

Veeco Total $89 $115 -23% $110 $107 +3% $6.2 $4.1

39 ©2009 Veeco Instruments Inc 020909 Investor Slides

Segment InformationSegment Information

** Refer to footnotes on "Reconciliation of operating loss to earnings excluding certain items"

(In thousands) 2008 2007 2008 2007

LED & Solar Process EquipmentBookings 43,649$ 42,522$ 160,162$ 163,970$ Revenues 37,608$ 33,675$ 165,812$ 115,863$

Operating income 783$ 4,681$ 19,616$ 9,694$ Amortization expense 1,587 489 4,627 4,263 Restructuring expense 725 34 732 34 Purchase accounting adjustment 565 - 1,492 - EBITA 3,660$ 5,204$ 26,467$ 13,991$

Data Storage Process EquipmentBookings 13,968$ 35,826$ 138,653$ 141,663$ Revenues 45,026$ 37,329$ 149,123$ 136,169$

Operating loss (42,877)$ (6,374)$ (35,411)$ (6,332)$ Amortization expense 934 952 3,790 3,806 Restructuring expense 272 2,339 396 2,498 Asset impairment charge 51,102 1,068 51,102 1,068 Inventory write-off - 4,821 - 4,821 EBITA 9,431$ 2,806$ 19,877$ 5,861$

MetrologyBookings 30,884$ 36,547$ 125,622$ 145,939$ Revenues 27,710$ 35,818$ 127,874$ 150,443$

Operating loss (30,044)$ (2,479)$ (31,348)$ (997)$ Amortization expense 585 351 1,880 1,486 Restructuring expense 511 554 1,138 1,952 Asset impairment charge 21,935 - 21,935 - Inventory write-off 2,900 - 2,900 - EBITA (4,113)$ (1,574)$ (3,495)$ 2,441$

Unallocated CorporateOperating loss (4,939)$ (4,430)$ (23,415)$ (14,426)$ Amortization expense 109 222 448 695 Restructuring expense 2,059 1,825 8,296 2,242 Asset impairment charge - - 285 - EBITA (2,771)$ (2,383)$ (14,386)$ (11,489)$

TotalBookings 88,501$ 114,895$ 424,437$ 451,572$ Revenues 110,344$ 106,822$ 442,809$ 402,475$

Operating loss (77,077)$ (8,602)$ (70,558)$ (12,061)$ Amortization expense 3,215 2,014 10,745 10,250 Restructuring expense 3,567 4,752 10,562 6,726 Purchase accounting adjustment 565 - 1,492 - Asset impairment charge 73,037 1,068 73,322 1,068 Inventory write-off 2,900 4,821 2,900 4,821 EBITA 6,207$ 4,053$ 28,463$ 10,804$

December 31, December 31,Year endedThree months ended

40 ©2009 Veeco Instruments Inc 020909 Investor Slides

ReconciliationReconciliation

(1)

During 2008, the Company recorded a restructuring charge of $10.6 million, of which $3.6 million was incurred during the fourth quarter, $4.1 million was incurred during the third quarter and $2.9 million was incurred during the first quarter. These restructuring charges consisted of personnel severance costs and lease-related commitments.

(2)

During 2007, the Company recorded a restructuring charge of $6.7

million, of which $4.7 million was incurred during the fourth quarter, $0.5 million was incurred during the third quarter and $1.5 million was incurred during the second quarter. The fourth quarter restructuring charge consisted of $2.9 million of personnel severance costs, and $1.8 million of commitments associated with discontinued product lines. The third quarter and second quarter restructuring charges consisted of personnel severance costs.

(3)

During 2008, the Company recorded $1.5 million in cost of sales related to the acquisition of Mill Lane Engineering, of which $0.6 million was recorded during the fourth quarter. This was the

result of purchase accounting, which requires adjustments to capitalize inventory at fair value.

(4)

During 2008, the Company recorded a $73.3 million asset impairment charge, of which $73.0 million was recorded during the fourth

quarter and $0.3 million was recorded during the first quarter.

The fourth quarter charge consisted of $52.3 million related to goodwill and $20.7 million related to other long-lived assets. The first quarter charge consisted of $0.3 million related to fixed asset write-offs associated with the consolidation and relocation of our Corporate headquarters.

(5)

During the fourth quarter of 2007, the Company recorded a $1.1 million asset impairment charge related to fixed assets associated with discontinued product lines. (6)

During the fourth quarter of 2008, the Company recorded a $2.9 million inventory write-off in its Metrology segment associated with legacy semiconductor products. This was included in cost of sales in the GAAP income statement.

(7)

During the fourth quarter of 2007, the Company recorded a $4.8 million inventory write-off associated with discontinued product lines. This was included in cost of sales in the GAAP income statement.(8)

During the fourth quarter of 2008, the Company repurchased $12.2

million aggregate principal amount of its 4.125% convertible subordinated notes. As a result of these repurchases, the Company

recorded a net gain from the early extinguishment of debt in the

amount of $5.0 million.(9)

During the first quarter of 2007, the Company repurchased $56.0 million aggregate principal amount of its 4.125% convertible subordinated notes. As a result of these repurchases, the Company recorded a net gain from the early extinguishment of debt in the

amount of $0.7 million.Note: The above reconciliation is intended to present Veeco's operating results, excluding certain items and providing income taxes at

a 35% statutory rate. This reconciliation is not in accordance with, or an alternative method for, generally accepted accounting principles

in the United States, and may be different from similar measures presented by other companies. Management of the Company evaluates performance of its business units based on earnings before interest, income taxes and amortization excluding certain items ("EBITA"), which is the primary indicator used to plan and forecast future periods. The presentation of this financial measure facilitates meaningful comparison with prior periods, as management of the Company believes EBITA reports baseline performance and thus provides useful information.

(In thousands, except per share data) 2008 2007 2008 2007

Operating loss ($77,077) ($8,602) ($70,558) ($12,061)Adjustments:Amortization expense 3,215 2,014 10,745 10,250 Restructuring expense 3,567 (1) 4,752 (2) 10,562 (1) 6,726 (2)Purchase accounting adjustment 565 (3) - 1,492 (3) - Asset impairment charge 73,037 (4) 1,068 (5) 73,322 (4) 1,068 (5)Inventory write-off 2,900 (6) 4,821 (7) 2,900 (6) 4,821 (7)Earnings before interest, income taxes and amortization excluding certain items ("EBITA") 6,207 4,053 28,463 10,804Interest expense, net 899 757 3,812 3,013Gain on extinguishment of debt (4,969) (8) - (4,969) (8) (738) (9)Adjustment to exclude gain on extinguishment of debt 4,969 - 4,969 738 Earnings excluding certain items before income taxes and noncontrolling interest 5,308 3,296 24,651 7,791Income tax provision at 35% 1,858 1,154 8,628 2,727Noncontrolling interest, net of income tax provision at 35% (20) (95) (150) (408)Earnings excluding certain items $3,470 $2,237 $16,173 $5,472Earnings excluding certain items per diluted share $0.11 $0.07 $0.51 $0.17Diluted weighted average shares outstanding 31,564 31,399 31,516 31,346

Three months endedDecember 31,

Year endedDecember 31,

41 ©2009 Veeco Instruments Inc 020909 Investor Slides

Balance SheetBalance Sheet

(In thousands)

December 31, December 31,2008 2007

(Unaudited)

ASSETSCurrent assets: Cash and cash equivalents 103,799$ 117,083$ Accounts receivable, net 59,659 75,207 Inventories, net 94,930 98,594 Prepaid expenses and other current assets 6,425 8,901 Deferred income taxes 2,185 2,649 Total current assets 266,998 302,434

Property, plant and equipment, net 64,372 66,142 Goodwill 59,160 100,898 Other assets, net 39,011 59,860 Total assets 429,541$ 529,334$

LIABILITIES AND SHAREHOLDERS' EQUITYCurrent liabilities: Accounts payable 29,610$ 36,639$ Accrued expenses 66,964 60,201 Deferred profit 1,346 3,250 Income taxes payable 354 2,278 Current portion of long-term debt 196 25,550 Total current liabilities 98,470 127,918

Deferred income taxes 4,540 3,712 Long-term debt 108,669 121,035 Other non-current liabilities 2,391 1,978

Noncontrolling interest 784 1,014

Shareholders' equity 214,687 273,677 Total liabilities and shareholders' equity 429,541$ 529,334$

42 ©2009 Veeco Instruments Inc 020909 Investor Slides

Q1 2009 GuidanceQ1 2009 Guidance

LOW HIGH

Operating loss ($21,000) ($15,800)

Adjustments:

Amortization expense 1,800 1,800 Restructuring expense 6,000 (1) 5,000 (1)Equity-based compensation expense 1,700 1,700

Earnings before interest, income taxes and amortization excluding certain items ("EBITA") (11,500) (7,300)

Interest expense, net 1,500 1,500Adjustment for non-cash portion of interest expense (700) (2) (700) (2)

Earnings excluding certain items before income taxes (12,300) (8,100)

Income tax benefit at 35% (4,305) (2,835)

Earnings excluding certain items ($7,995) ($5,265)

Earnings excluding certain items per diluted share ($0.25) ($0.17)

Diluted weighted average shares outstanding 31,600 31,600

Guidance for the three months ended March 31, 2009

(1)

During the first quarter of 2009, the Company expects to record a restructuring charge between $5.0 and $6.0 million.(2)

Adjustment to exclude non-cash interest on convertible subordinated notes.(3)

NOTE -

The above reconciliation is intended to present Veeco's operating results, excluding certain items and providing income taxes at a 35% statutory rate. This reconciliation is not in accordance with, or an alternative method for, generally accepted accounting principles in the United States, and may be different from similar measures presented by other companies. Management of the Company evaluates performance of its business units based on earnings before interest, income taxes and amortization excluding certain

items ("EBITA"), which is the primary indicator used to plan and forecast future periods. The presentation of this financial measure facilitates meaningful comparison with prior periods, as management of the Company believes EBITA reports baseline performance and thus provides useful information.

(Unaudited)