shortsale data

DESCRIPTION

Short sale steps and informationTRANSCRIPT

- 1 -

Section 1 What This Lending Industry is Doing Today and What Your Future In Short Sales Holds Billions of dollars each year are loaned to individuals throughout the United States and abroad for various reasons. Because the demand for money is so great and the cost so low, lenders are willing to “Go The Extra Mile” or “Bend Underwriting Guidelines” to better meet the demand of consumers. In the Mortgage Industry this philosophy is held very close and is found commonly in corporate mission statements. One major lender wrote a press release stating the company’s monthly production is up more than 50% from the second quarter…

1) Changes include eliminating the requirement for a verification of mortgage/rent with customers with 620 FICOs Plus.

2) Increasing loan size limits to this target market. 3) Increasing maximum debt-to-income ratio on select

products. 4) Reducing business verification requirements on 620+

FICOs. 5) Increasing loan-to-value caps on non-owner occupied

loans. While relaxing underwriting guidelines may lead to increased business for lenders with proper marketing, it can also lead to increased delinquency. Eliminating the verification of rental history for example, may allow customers to be unjustly rewarded for paying rent past due while maintaining their personal credit with reasonably good success. Such customers may still be able to obtain a mortgage and continue to “play their game” but some get into serious trouble…foreclosure.

- 2 -

These changes were brought about for a number of reasons.

1) “Go The Extra Mile.” Increase benefit to the customer by relaxing underwriting guidelines.

2) Increase loan size limits that encourage the customer to take more. (Attract bigger loans)

3) Relaxed documentation assists in deeper penetration in broker/correspondent lending business.

4) Increase “Niche” lending, targeting non-owner occupied property owners that already know and understand the level of difficulty getting cash out on these types of properties.

5) Outrun Delinquency Rates by dramatically increasing loan volume.

The examples stated above are a sample of what hundreds of

lenders are doing throughout the United States to increase balance sheets. When you understand the process of how lenders obtain business and methods to get it, the role of the investor becomes clear. Investors benefit based on the failings from the following:

1) Customer mismanaging money 2) Lenders “relaxed guidelines” 3) Layoff’s and temporary curtailment of income 4) Divorce

Needless to say: THE INVESTOR IS HERE TO STAY AND

WILL THRIVE FOR MANY YEARS TO COME.

- 3 -

Section 2 How the Short Sale System Works With Lenders 1. The Inside Scoop Many questions are asked about, “How the short sale system works with lenders.” • Possessing a better understanding of this process will enable

the investor to avoid wasting time, money and efforts on a deal which may never close.

• With this knowledge The investor knows when to enter into negotiations with a lender and when to “Sit and Watch.”

Levels of delinquency and their significance Pre 30 Days Attempts to Contact – 3-5 by bank Collector skill level – typically no previous experience in

collecting • These accounts are past due from 5-10 days. For example, an

account that is due for a payment on June 1, 2004, is typically called for a payment beginning on June 6, 2004, and will continue to receive a call until the payment is made.

• While most calls are general in nature, serious reasons for default can be identified very early in the default and are typically managed by payment plans, and at times…Loss Mitigation will begin.

Reasons For Loss Mitigation Eminent Default: Irreversible loss of income (death of customer with no heirs, arrest/imprisonment, etc.)

- 4 -

Joint account with primary applicant deceased. Co-applicant would no longer qualify for the loan or afford the payments. Layoff: Customer’s negative perception of their financial status is alarming to THEM and request the bank take the property. Divorce: Neither party wants to pay on the mortgage, most of the time the wife is living in home and refuses to pay as per divorce decree. Mr. is to pay and Mr. refuses to pay as ex-wife is living in home. Non-Escrow Accounts: At times, the customer will fail to pay delinquent property taxes, which the bank is forced to pay. The bank will force an escrow and impound the account. Often the mortgage payments will double or triple the “On Time Payment.” This is a major cause of default!

30-Day Delinquency: Attempts to contact – 5-10 Collector skill level – usually 1 to 2 years of previous experience. Note that these individuals rarely have much experience in the

mortgage business. Most of them could not tell the difference between a note sale and a short sale or the difference between a Deed-in-Lieu-of-Foreclosure and a Quit Claim Deed. When communicating with them, do not get frustrated as they will tend to repeat professional sounding terms and/or phrases that they have heard their colleagues say or use. At times, their statements may not make sense because they are using “industry vocabulary” with which they have no frame of reference. In their mind(s), it sounds effective or threatening, whichever purpose he/she is trying to accomplish.

Characteristics – Goal oriented, persistent, argumentative, Usually highest level of customer complaints because of volume

of calls • These accounts are 31-59 days past due. Collection phone

calls are detailed and clearly explain the RFD (Reason for Default).

- 5 -

• Financial information is updated (un-audited) and verbally given to the collector. This information is used to check the customer’s ability to pay and remain current.

• Accounts with no ability to pay and no other assets to sell to cover the delinquency are encouraged to sell the house.

• If the customer refuses to sell, which is a common answer, the bank will typically allow the customer to make 1 payment per month and collect fee income (late charges) until such time that a more serious default is made.

• Find these 59-day accounts only through shotgun marketing (they contact you) Your goals: a) Wait to short sale once 90 days b) Deed transfer to you: you bring current

• Note sale possible at this stage – note sale provided that

sufficient equity present in property for you (30% or greater), and you have an agreed upon exit strategy with the customer

60-Day Delinquency Attempts to contact – 7-13 Collector skill level – 2 to 4 years Characteristics – persistent, aggressive, firm tone of voice,

argumentative, controlling micro account managers Note that these collectors are usually promoted from the pool of

collectors from the 30-Day Department within 6 months (or sooner if a vacancy is present). In other words, keep in mind that you are probably dealing with the same mentality as mentioned above.

These accounts are 60 to 89 days past due. Most accounts at this level of delinquency clearly indicate the customer’s real intentions about the account. By reviewing the account notes you can get a good handle on how the customer is going to react to you when contact is made. They have been described as:

- 6 -

• Mindless • Lack sense of advance planning • Lack motivation • Unorganized • Often seek out third party for validation about delinquency or

information • Expanded thoughts for validation & information

o Do I file for bankruptcy? If so what chapter? o Am I allowed to sell the house if I can’t pay it off? o Swap high impact “hard luck stories” to get a

reinstatement agreement o If I sell and there is not enough money to pay the balance,

am I still responsible for the remaining balance?

At 60 to 89 days past due, the mortgagor is considered at their peak of creativity to manipulate the bank into getting what they want. At times it can be challenging for the collector to distinguish fact from fantasy. Experience is usually the collector’s best tool for getting to the truth of the matter. An investor can do well to create a bond with a credit counselor at this level of delinquency. Suggested Action Plans To Locate 60 Day Accounts

• Make 1 call per day to a high profile mortgage company/bank and ask for the 30- or 60-day department.

• Identify yourself as an investor looking to assist the bank in resolving delinquent accounts.

• Offer to assist collector in contacting debtor (face-to-face interview).

• If the customer’s address is given, carry out the promise. If contact is made, ask questions about the nature of the delinquency and intent/ability to keep the house.

o Is there opportunity to buy the house? o Does the customer truly have no way to pay the mortgage? o Can you offer to help the customer and the bank? o Can you offer a creative make sense resolution that the

customer will understand and buy into?

- 7 -

o Is the customer scared to call the bank because of a “renegade collector?” If yes, how can you assist?

o Call the charge off/recovery department. They do have loans where the lien is still intact, and they have charged off the account as they were unable for whatever reason to foreclosure the property.

Don’t be afraid to think “out of the box.” Finding pre-foreclosures does not have to start at the 90-day level. Spend an hour a day cultivating new lead sources. It can only benefit you if it is done right and consistently. Loss Mitigation: Accounts over 90-days delinquent Attempts to contact – 5-10 Collector skill level – 2 to 20+ years Characteristics – persistent, aggressive, controlling, micro

account, analytical, concerned about property valuation and losses vs. collecting a payment

Note that loss mitigation is not for the “weak-at-heart.” Experience ranges but you can tell a “seasoned” veteran by their lack of concern for the customer’s situation, as their function is to reduce the loss to the lender when the account is “finalized” or the security is liquidated. In other words, successful loss mitigators will not be “on your side” if your angle is based on helping the customer. Your angle needs to be based on reducing losses to the lender (helping the customer is optional but secondary.)

Loss mitigation departments are the last lines of defense to “mitigate” potential losses. The Mitigator’s primary job is to determine if the customer desires and is able to save their home. Loss mitigators also enjoy expanded other authority:

• Have authority to reinstate without management’s expressed authorization.

• Have authority to refuse payments • Have authority to post payments their way, i.e., principal,

interest, late fees, foreclosure fees, etc. • Authority to order BPO’s as needed.

- 8 -

• Control over influencing any deals or proposals submitted to management (they write up the presentation if a presentation is made and they will usually discuss the proposal with senior management at the time it is submitted).

• Control if a deal is presented to management. • Authority to set up forbearance (attorney prepared

repayment plan)

- 9 -

New Processes In Loss Mitigation Summary – While each bank has their own set of policies and procedures for the short sale process, I have found some similarities that appear to be consistent throughout the industry. Recognizing these similarities will assist the investor in preparing a short sale package that should be globally accepted by banks and mortgage companies throughout the United States. Investors that understand this process will find it easier to communicate with loss mitigation departments, produce required documentation, reduce levels of frustration and understand the importance of each step. The Loss Mitigation Process I. Your introduction to the bank

• Identify the mitigator that you will be talking to. o If the mitigator is “matter of fact” you will want to present

yourself as a direct person. Limit small talk and stay on track.

o If the mitigator is a talker, pump them for information about the house.

o If the mitigator is “quiet,” ask open-ended questions to draw them out

II. Identify the property and discovery stages. Will the bank

consider a short sale? • Open discussions with the mitigator and release of the

signature authorization o Have prepared the customer’s signature authorization to

release information. Without this document, most banks will not discuss the account any further.

o Is the bank agreeable to a possible short sale? o Does the bank have a BPO value yet? If yes, ask for the

value. o Does the bank have a title search? If yes, what liens if

any are on the property? o Does the bank have contact with owners?

Remember that a bank will not typically enter into a short sale on a customer that is actively paying (Exceptions can be made)

- 10 -

o Use this time to ask questions about the property and find out what the bank knows. Every effort should be made to get the bank’s BPO value if possible. With this information, bids can then be provided to the bank with some certainty of acceptance.

III. Request the bank to order the BPO and title search

• Make the attempt to control the mitigator to order the BPO and title search before an offer is made This helps prevent over-paying for properties. Provides extra time to prepare a bid for the house. Provides time to persuade the mitigator to forward a copy

of the BPO to you • Mitigator refuses to order the BPO and demands the offer

before the BPO is ordered. Submit your short sale package • Purchase sales agreement • Customer’s financials

o 1 to 2 recent pay stubs o 1 to 2 years of most recent tax returns o Letter of hardship from the customer o 1 to 3 months of bank statements

IV. The short sale analysis – BPO received and short sale package

• Bank analyzes the BPO, customer’s financials and determines the best course of action for the bank o Most important, the bank determines if the BPO is valid

and true Are the comps of acceptable distance from the

subject property? Are the comps of comparable size? Does the square footage of the BPO match the

original appraisal? What is the visual interior condition like? How much is the deferred maintenance? Is the “crime” rating high/low?

• Mitigator compiles the information on a spreadsheet and submits his/her written report to management.

- 11 -

• Management reviews file. o If accepted, investor notified of approval and closing is set. o If accepted and the account is investor backed, the short

sale package is forwarded on to the investor for approval If the investor approves, the mitigator is free to set

the closing If the investor turns down, negotiations begin with

the investor. Key Notes and Points of Thought • Throughout the entire short sale process, you must continually

make requests to the bank for the value of the property • Throughout the entire short sale process, you must continually

make requests for a copy of the BPO • Throughout the entire short sale process, you must listen for

excitement, eagerness, aggressiveness to close from the mitigator. These are signs that you may have a highly motivated mitigator that may be willing to further discount a property to get the deal done.

• Key time to re-negotiate the short sale is 5 to 7 days before the end of the month. Remember that most goal-oriented banks and mortgage companies want to close out as many loans as possible by the end of the month.

• The beginning of the month, banks are more picky about what they will approve or take. At the end of the month, however, they are more aggressive and forgiving.

- 12 -

Individual Investor Backed Loans

• “Non-Pooled Loans” – one investor = one loan

• You’ll never talk to the investor directly

• You are building a case for the discount so the mitigator will in turn submit your package to one decision maker with a positive attitude

• Not all loans are solely owned by the bank that is servicing

them. • Large institutional investors will commonly buy $50 million plus

in mortgages per month and then service release them to other banks or mortgage companies that perform all servicing needs such as customer service functions, collections, billing, accounting, loss mitigations and at times REO

o Securitization: A mortgage, also known as a marketable security, is sold to an institutional investor for a premium price. The seller of the mortgage then guarantees interest payments on that mortgage sold to the investor regardless of the account performance.

o Securitizations typically offer deeper discounts than wholly owned mortgages.

o Some securitizations may require extra steps in the short sale process.

• All investors accept a percentage of fair market value (their

BPO) CitiMortgage 70% MLN 70-75% Litton 80-100% Fairbanks Capital 85% National City 70% …I could go on, yet none of these are completely hard and fast. It depends on the 3 controlling variables in the short sale process which are discussed later

- 13 -

Most of these investors will not allow more than $1,000 to $2,500 to go to subordinate financing The top 7 things influencing an investor (outside the short sale process) are:

• Borrowers intent with the property • Ability to pay • Amount of equity • Other liens – IRS, State, if delinquent property taxes are

converted to tax certificates or tax deeds • Environmental issues • Is the area good for third party bidders? • Economics – calculated by the REO ratio • How much do they regard the mitigator’s opinion The mitigator is the one who knows the account and reviewed the package – and thoroughly

Mitigator’s Note: F/C bids are sometimes taken into

consideration – meaning if the F/C would be at least 90 days from the closing of your proposal and net proceeds to the mortgage company or bank will exceed the maximum foreclosure bid, then your deal will be approved with little resistance.

• No matter how good your offer is, always expect a counter offer.

(There is an old saying in negotiating, “If you don’t ask for it, you won’t get it.) Don’t be discouraged, respond to the counter offer.

• Most mortgage companies or banks will bid around 85% (considered “industry standard”) of the fair market value at the F/C auction.

• There are some exceptions where the local foreclosure statues contain redemption provision. In these cases, the mortgage company or bank will sometimes bid an amount equal to “full payoff” of the note or judgment.

• Even though your offer may not exceed the intended F/C bid, it may still be accepted but will require a little more negotiating.

- 14 -

It is most common with non-conforming lenders to find investor backed loans. SOME REMAIN AS POOLED NOTES – ALWAYS ASK! Examples: Lender National City Mortgage Citi Financial (formerly Associates) Mortgage Lenders Network Litton Loan Servicing One Stop Mortgage Fairbanks Capital Household Finance Beneficial

- 15 -

The Process With Investor Backed Loans

• Rapport and friendly communication is a must

• You and mitigator team together to prove the case

1) Request the short sale package once authorization is presented

2) Confirm how long it will take to get an approval once a full package is received

3) Offer the mitigator field information to create trust 4) If less than 30 days before the lender foreclosure

REQUEST POSTPONEMENT This is difficult as it is usually not in the mortgage

company/bank’s best interest to postpone as this process usually costs money through attorney fees and F/C court costs. Also, the interest continues to accrue while the value remains the same, so the loss grows. It is better to have the complete short sale package ready. THIS IS VERY IMPORTANT. DO NOT BE FRUSTRATED IF YOU ARE ASKED TO FAX THE PACKAGE MORE THAN 4 TIMES. MANY TIMES, YOU WILL FAX IT TO THE FIRST PERSON THAT ASKS FOR IT AND THEY WILL NOT GET IT TO THE CORRECT PERSON. ALSO, LISTEN TO THE MITIGATOR. DO NOT SEND THEM MORE THAN WHAT THEY ASK FOR. VERBALLY CHECK WITH THEM FIRST TO SEE IF THEY WANT WHAT YOU ARE SENDING, AND THEY WILL BE GRATEFUL NOT TO GET A 45 PAGE SHORT SALE PACKAGE WHEN ALL THEY WANTED WAS THE 2-PAGE ESTIMATED HUD-1 NET SHEET.

5) Send mitigator the short sale package From Here The Process Is As Follows: A) The mitigator will require the following documents:

• Fully executed agreement of sale contingent upon the mortgage company’s approval and release of mortgage

- 16 -

• Estimated HUD-1 settlement statement disclosing all past due and current taxes, subordinate liens, water and sewer bills, state and federal tax liens, judgments, etc., showing the mortgage company’s net proceeds with no cash out to the seller (exceptions can be made to “no cash out to seller”). For example, a customer in Pennsylvania that is only 6 months into a F/C (takes 12-18 months to F/C) and has a large unpaid principal balance ($150K+) stands a good chance of getting $1-$5K as the mortgage company will accrue more losses through lost time waiting for the judicial F/C process to run it’s course, as well as, the fact that it is usually cheaper for the customer to continue to live in the security “rent-free” for the next 6 months so they can save money to pay first and last month’s rent in their new residence).

• Documentation showing proof of past due taxes, judgments, or senior/junior liens being paid

• Copy of the title search, name, address, and telephone number of the title company with contact name (not required by the mortgage company in most cases. Yet, you will want one prior to closing any deal as the clarity of the title will be in new owner’s best interest)

• Copy of any recent appraisal (it is important that the term appraisal is not abused. Mortgage companies and banks usually have their own independent broker’s price opinion (or BPO) done so that the value returned is: 1) Private/ confidential and 2) accurate – in other words, without consideration for the purchaser. In instances where the loan is guaranteed by FHA or VA, an appraisal is ordered. Again independently by the mortgage company or bank for the two reasons mentioned above. There is one exception to this “private value” rule. If the BUYER is financing via an FHA or VA loan, the appraisal they obtain for the purchase of approving their FHA or VA loan is commonly accepted by the mortgage company or bank. Back to the subject or “appraisal” term not being abused, some people are not aware of the differences between an appraisal (and there is more than one type of appraisal), Broker’s Price Opinion or a comparative market analysis on subject property, if available, and six comparables (or “comps”).

• Hardship and financial package from seller

- 17 -

B) The mitigator will put a package together and run an equity

analysis to find the bottom-line dollar amount the investor should accept

• The equity analysis is run just as if they are taking the property

to foreclosure sale. The decrease in value varies from state to state and by value of the property. (Example: Florida $100K interior value 5% cut, $100K exterior value 15% cut, $100K 10%). All foreclosure fees are standard with Fannie Mae per state guidelines.

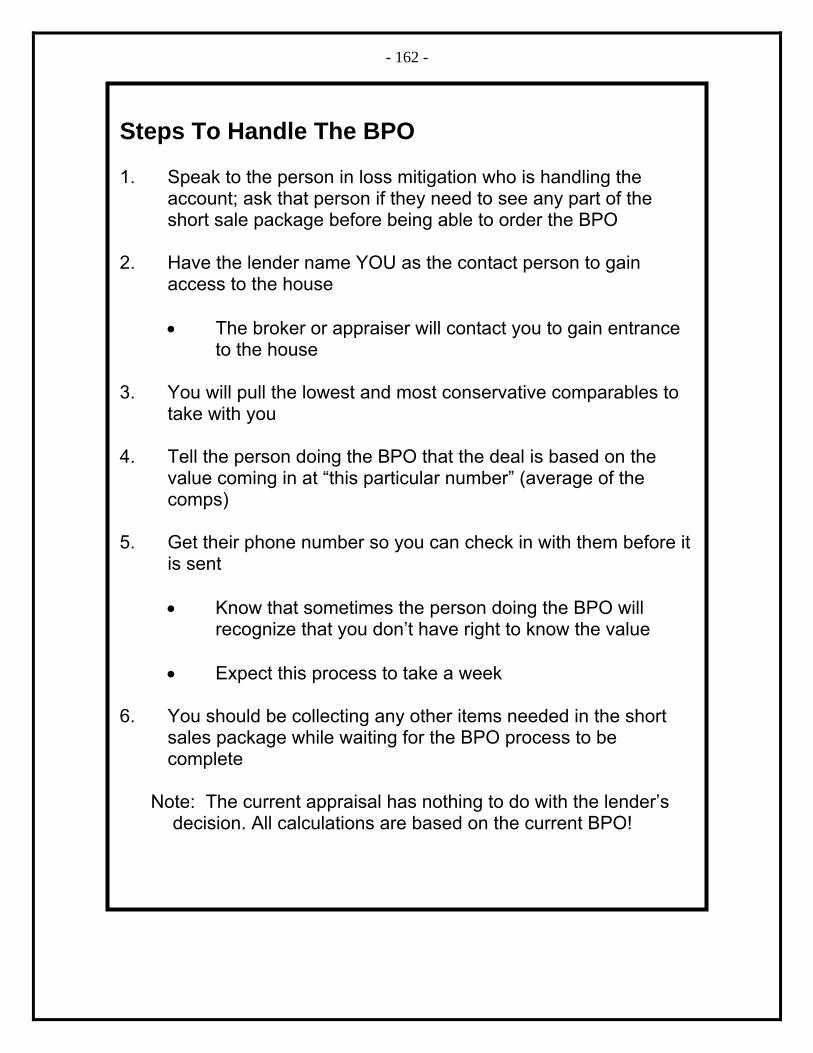

C) The mitigator will call the investor back to let him know that he

will present the package or counter offer D) Once the mitigator approves the deal, it is reviewed by the loss

mitigation manager, who will then approve or submit a counter offer back to the mitigator. If he approves the deal it goes to the Director of Loss Mitigation for his approval.

E) Once the Director approves, an approval letter is sent to the

investor and a verbal confirmation is completed for the closing. Most approvals are valid for 30 days only. If they rescind or expire, the whole process starts again.

What Makes A Mitigator The Maddest? • Waiting for the last week when a foreclosure sale date is set.

Only if the offer requires more than a day’s work – if the investor does all of the “due diligence” and has the financials. Contract, net sheet, authorization to release, and hopefully, the mortgage company/bank has recent opinion of value (they usually do by this time as they have to have it for determining their bid at sale). If the bank got “low-balled” on their opinion of value, and your value is higher than their value, then your deal will be appealing and they will run the “fire drill” to make the deal work but you have to be willing to close and have funds to them 24 hours prior to the F/C sale date.

- 18 -

• Pushing to close now • Falsified documents • Calling the manager because you think the mitigator isn’t

working your file quickly enough • Not closing the deal due to funding (don’t be surprised if the

mitigator asks for proof of funds) • Backdooring the mitigator by trying to get another mitigator to

get the deal closed • Constant phone calls (more than one a week) • Using an attorney as a go-between. I prefer dealing with

attorneys. Not to insult investors, but good attorneys usually have a better understanding of “compliance” and/or other issues and tend to be calm conversationalists).

• Trying to close a deal the last week of the month, thinking the mitigator needs your deal to make his month

• Not doing your due diligence (the mitigator is not going to do your work for you)

• Promising to do more deals at a better rate if they will just get this bad deal approved for you

• Don’t tell a mitigator what the house is worth or go on about how the property needs to be “bull-dozed” and how you are the Robin Hood of the community. If there are conditions that you think the mortgage company/bank is unaware of, make access to the interior of the security available so they can see for themselves. In most cases, the mortgage company/bank will use a drive-by BPO to determine the value for F/C purposes so they are not aware of the mold, cat urine/feces, water damage, etc.

Do they answer to anybody else?

• Yes, to the loss Mitigation Manager and the Director of Loss Mitigation

- 19 -

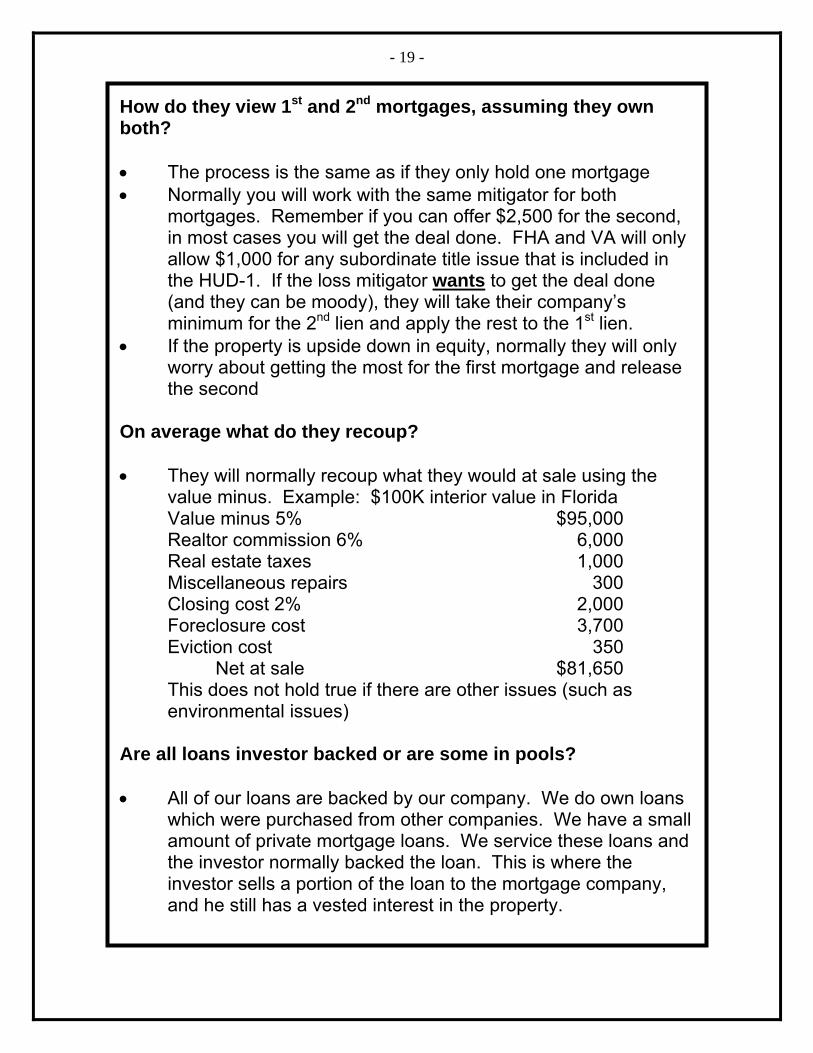

How do they view 1st and 2nd mortgages, assuming they own both? • The process is the same as if they only hold one mortgage • Normally you will work with the same mitigator for both

mortgages. Remember if you can offer $2,500 for the second, in most cases you will get the deal done. FHA and VA will only allow $1,000 for any subordinate title issue that is included in the HUD-1. If the loss mitigator wants to get the deal done (and they can be moody), they will take their company’s minimum for the 2nd lien and apply the rest to the 1st lien.

• If the property is upside down in equity, normally they will only worry about getting the most for the first mortgage and release the second

On average what do they recoup? • They will normally recoup what they would at sale using the

value minus. Example: $100K interior value in Florida Value minus 5% $95,000 Realtor commission 6% 6,000 Real estate taxes 1,000 Miscellaneous repairs 300 Closing cost 2% 2,000 Foreclosure cost 3,700 Eviction cost 350 Net at sale $81,650 This does not hold true if there are other issues (such as environmental issues)

Are all loans investor backed or are some in pools? • All of our loans are backed by our company. We do own loans

which were purchased from other companies. We have a small amount of private mortgage loans. We service these loans and the investor normally backed the loan. This is where the investor sells a portion of the loan to the mortgage company, and he still has a vested interest in the property.

- 20 -

• We have what we call securities loans. These are loans from other lenders that we service for them. By servicing these loans it adds to our borrowing power.

It is most common with non-conforming lenders to find investor backed loans. Some remain as pooled notes – always ask! Also important to understand in this process: Some lenders who write their own paper have buy back or

guarantee clauses in the event these notes go bad. A lender will mitigate these as servicers of the paper.

- 21 -

The Committee

• Pooled loans – several investors means a team of underwriters or committee makes the decision on what to accept on the short request

• There is less chance to negotiate a steep short because a very

motivated individual investor may be more likely to cut a deal

• The committee uses hard and fast ratios based on the information you submit to build a case

Common pooled mortgage lenders are

F.H.A. backed loans

FHA and VA loans only allow a certain amount of money to be given to a second mortgage if they take a short sale. Most second mortgage holders on this type first will ask for $2,500 to do the deal. Yet the HUD 1 will normally only be able to show $1,000 to the second so the remaining $1,500 will have to be sent by the investor in the same package.

- 22 -

Mitigator Note: If you find an FHA or VA deal, leap with joy. FHA calls short sale “pre-foreclosure sales” and VA calls them “sale in compromise” or VA comp sale for short. Anyway, FHA and VA guidelines are open to the public and the investor WILL NOT decline an offer that meets those guidelines as they will be reimbursed by the guarantor (the same holds true for loans insured by private mortgage insurance companies [Radian, PMI, MGIC, RMIC, GEMI, etc.], although their approval process is not open to the public). But, if you really are making a fair offer, and the mitigator is rejecting the deal, you can obtain the contact information for loss mitigation department at the private mortgage insurance company and see if you can get them to approve the deal. The original mitigator may not be happy with this at first, but if you smooth things over with him/her, everyone will be happy in the end because the mortgage insurance company approving the deal will reimburse the mortgage company/bank for any loss up to the maximum that their policy allows.

Lender Countrywide Home Loans

- 23 -

The Process With Pooled Note Lenders a) Request the short sale package. You may be required to

present a power of attorney before it will be sent. b) Find out how long it will take the short sale package to

make it to committee before acceptance c) The minimum time needed to submit a package for

approval is 7-21 days depending on whether the interior BPO has been obtained by the bank. Ask if there are any exceptions

d) Come out of the gate requesting a postponement e) Most of the time, they will not accept a month’s interest as

compensation to postpone Verbiage You: “Mr. Mitigator, is this a pooled or investor backed loan?” Mitigator: Pooled

Mitigator Note: My response is usually, “This is of no relevance to the issue other than the amount of time it will take to get the deal approved/denied. If 3rd party approval is needed, then it will take an additional 10-14 business days” (in reality, it usually can be done in 3 business days).

- 24 -

- 25 -

Section 3 The “Approach” And How We Present Ourselves

To Loss Mitigators

What Mitigators Know About People Who Call

To Request a Discount “I am the Buyer” vs. “I’m calling on behalf of my client.” How we represent ourselves represents a position we must choose, stick with and be able to support, defend with credibility and congruence in our story… Why not tell the truth? …All the while our deal must make economic sense to us while appearing to be in the lender’s best interest. • I prefer they know where I stand – As An Investor • I would rather develop huge rapport, be successful, close the

deal, have them remember me in case we meet on the next deal

It’s more about the negotiated numbers for the lender than how much we might make: stay away from dead end, against the wall conversations such as…

Mitigator: Why should I take a discount to watch you make a bunch of money?

You: First of all, who says I’m going to make money. I’m giving you all the real reasons why this is better than taking it back into REO. Besides, if it doesn’t match your numbers, I don’t expect you to do it.

- 26 -

Alternative Answer: Who left you in charge of fixing the world? We are both going to put together something that makes sense to your boss. Then, I’m pushing to make every dime I can make. Aren’t you bonused on this deal if we get it done? You have to be careful with this response because most calls are monitored randomly. The mitigator never knows when his call is being monitored and does not want to risk termination over 1 deal. You might try appealing to the mitigator to just take it to committee to try to get it approved. If rejected/countered, you can negotiate again. Most mitigators will then begin to think to themselves that they don’t have the weight of the world on their shoulders and will submit it for approval. Mitigator’s Note: Statistically speaking 90% of deals that are

closed in loss mitigation are done so by investors. We are the necessary component that turns the machinery. Less than 15% of sellers are able to get their own short sale completed or approved.

*Information obtained by interviewing 3 randomly chosen lenders.

- 27 -

What Mitigators Know About Investors A seasoned loss mitigator is not stupid and… • Knows many investors are a quick fix to delinquency issues • Expects quick funding • Expects an investor will not have to be guided through the short

sale process • Knows the investor has a hidden agenda. “What’s in it for

them?” • Expects experienced investors to have complete short sale

packages • Suspects a sum of cash is being paid to the customer off the

books • Suspects the property is already sold before the investor buys it • Expects the investor to itemize all problems with the property in

an attempt to get a better discounted price • Knows the investor will supply overstated repair estimates for

repairs • Expects the investor to use REO Comps to dispute the estimated

BPO value • Thinks the investor might be selling the house back to the

customer • Knows that the investor will be profiting from the deal or else he

would not be doing the deal – It’s unspoken because of monitored calls!

A new, inexperienced loss mitigator could have a different mindset… • May not be privy to team player rules of engagement, and makes

stupid comments such as: How much are you making? • May have personal agendas or personality issues which get in

the way of logical decisions based on factual information you give them

• Could be completely overwhelmed, untrained, and unorganized with regards to priorities and how to organize their communications

• Doesn’t always have the bank’s best interest at hand and won’t submit an offer if you tick them off

- 28 -

How we deal with inexperienced loss mitigators • Develop rapport and find out how long they have been in the

business • Carry them through the process with time frames. Can you get

me an answer by the 23rd of this month or my private loan commitments will expire?

• Establish clearly how to communicate, tell them you want to be able to do several deals with them

• Don’t back them into closed end situations • Inexperienced loss mitigators might not accept NEW information

into the equation even if it makes sense If the mitigator is being irrational, find out when their normal office hours are. Call back when that mitigator is not there and try to get one of the senior mitigators on the phone – do not ask for a manager – as the senior mitigators will try to help the inexperienced mitigator get the deal done without making you look like a jerk for going above them.

How we deal with experienced loss mitigators • Willing to assist mitigator in contacting the debtor; property

inspections • Let them know up front you are going to give them a complete

package • Above all, always make them feel comfortable you are able to

close • Give them proof of funds or established lines of credit if you are

telling them, “look, I can get this off your books if you just tell me what you need to get this short sale approved.”

• Expect the short sale they will accept is between $10,000 to $20,000 less than what they say they will accept.

o New information regarding negatives about the property, as well as a threat of prolonged foreclosure will give them something new to present to management and justify their acceptance

• Offer to secure the property and send them a key • Build an ultimate case supported the whole way through

- 29 -

• Tell them you’ll go place your own insurance on it the minute the short is accepted

What they hate the most • Pushy investors – mitigators are control freaks (sad but true) –

use month end deadlines to motivate them • “You won’t recoup your balance at the sale” • To catch you in a lie • Not to be edified • Constant calls with no purpose • “Toney, complaining” annoying investors • Indecisiveness. Be confident and sound it (use your scripts and

review verbiage in this manual)

There is no war between investors and mitigators – both want the same thing. The investor wants the deal to close. The mitigator wants the deal to close. The only difference is that the investor has to be able to close the deal at a price that the mitigator can get approved. Make it approvable, and you will avoid most complications. Listen to what the mitigator is telling you. He/she might be telling you exactly what you need to do to get the deal approved.

- 30 -

Eight Steps On Our First Call *Note – Negotiating script in Section 5 At the point we call the lender, it is important we have the deed recorded. True False Step One: Get the name, phone number and extension to the loss mitigator who is handling the account from the last letter of correspondence from the bank. • There may not be a letter from the bank with an appointed loss

mitigator unless the default is past 90 days. If not… • Get a number from the Collections Department and call to find

out who it will be assigned to Step Two: Fax the authorization Step Three: Test the Mitigator’s temperature ”I’m going to need a bit of a short sale to get this done. If my offer parallels your numbers, can you get it approved?” • This includes testing the Mitigator’s knowledge, experience,

general disposition, and what the mitigator seems to feel about how easily the property would sell as a REO.

• Find out how they feel about the debtor. If the debtor has been in several bankruptcies, the lender’s negative attitude towards the debtor may deter participation in short sale

Step Four: Establish rapport • How would you like to communicate to get this done? E-mail,

fax, phone? • Will I be working with you only? • State the facts and be direct

o “I saw this property and am interested in buying it.”

- 31 -

• If you know the reason the seller is delinquent, let the mitigator know

o This is an excellent way to get extra information. Gain information in a non-threatening, casual way.

• If the mitigator has not contacted the debtor, then offer assistance. This will increase instant credibility for the investor.

• Ask the mitigator what you can do to help them. Step Five: • Find out if it is investor-backed and what it will take to get it

approved Step Six: • Find out if they have a BPO This is your control opportunity –

don’t miss the chance to involve yourself in this stage. Get them to do another one. If they say they already have an exterior BPO, tell them there are pending issues they need to see inside. How old is the BPO?

Step 7:

• Discuss foreclosure time frames, their willingness to work

with you. Set up to communicate the short sale in a non-verbal manner.

Step 8: KNOW YOUR PRODUCT!!

- 32 -

Handling The BPO Once Received • Ask fact finding questions about what their findings are

regarding the BPO o What were the neighborhood ratings according to the

agent? o What was the overall condition rating? o What were the market considerations? Declining

values/appreciating values? o How far were the comps from the subject property? o Were the comps larger or smaller than the subject?

• These questions are not critical to the investor but are instead designed to draw the mitigator into open discussion about the BPO and in more detail.

• Gives the investor an opportunity to size up the mitigator. • Provide subtle tests to see if the mitigator is able to draw logical

conclusions about the property in question. o Ask open-ended questions directed to the mitigator about

their opinion on the validity of the BPO o Ask open-ended questions about assigned deferred

maintenance listed in the BPO o Ask if they agree with the agent’s assessment and why.

Mitigator’s Note: The idea is to keep the mitigator talking and drawing information about the BPO. Complement them on their analysis. After all, who would take offense of someone complementing you about your analytical abilities? Tear down their defenses. You’ll find they will open up and may be very surprised what they will tell you.

- 33 -

Ordering The Short Sale Package • Before the short sale package can be ordered the bank typically

wants to talk to the debtor to review the reason for default and reasons to consider a short sale. Personally, I would prefer avoiding contact with the customer. Have the customer – neatly – hand write the “reason for default” letter.

Remember, their goal is to save the account and make it performing …mitigation comes when the debtor says they want out! The top 6 things a lender sees in considering a short sale 1. Very poor history of delinquency helps your case – especially if

the debtor has been tough to reach 2. Divorce – bickering debtors 3. Debtor has lost job 4. Bank must first refuse to reinstate mortgage - instead pushing

foreclosure 5. Change in the property value once foreclosure has started (i.e.,

environmental issues, burned down property, no home owner’s insurance, fire damaged property).

6. Property listed too long on market and no offers. • Have the short sale package sent to your e-fax 7. Loan Fraud

- 34 -

Defaulted Loan Script 1 (1st Mortgage) Goal: To speak with the individual that is already handling this particular account #: _________________________.

● Using any correspondence from the customer, look on the bottom of the

page and locate the person’s extension. Call this individual directly and begin the script.

Script Questions: 1.) I need to speak with someone in loss mitigation or someone who handles short pays on first mortgages in foreclosure. The property is located in (Your state) and the account number is _______________________. 2.) Hi! My name is (Your name) and I need to ask some questions about this account. Authorization to Release Information? Fax # __________________________. Before you get transferred, get their direct line and extension: Phone: ___________________________________ Extension: __________ 3.) What is your name? _________________________________________ 4.) Fax authorization and call back. 5.) Hi! ___________________, this is (Your name) again from (Your company) in reference to account number __________________. Did you get my authorization? 6.) My boss is considering buying this property before it goes to sale, if he could do it quickly, do you think a short pay would be approved if the short-sale offer parallels the BPO? _______ 7.) We normally see a discount of 20% of BPO value on the first…. Do you think you could get that approved? 8.) Have you already ordered a BPO?________ 9.) Was it an interior or exterior?______________ 10.) Is this an investor-backed loan or will it need to be reviewed by a committee? ____________________________ HUD [ ] Hardship Letter [ ] Financial Stmt [ ] Purchase and Sale Agreement [ ] Pay Stubs [ ] W-2’s [ ] 2 Yr. Tax Returns [ ] 12.) If my boss could do forbearance on the account, what would be the least you could take to re-instate the account and begin making regular payments? ________________________ Okay great! I’ll pass this information to my boss and he’ll be in touch. What’s the best way to contact you –

- 35 -

Email?_____________________________ Fax?______________________________ Phone?_____________________________ Thank you for your help!

- 36 -

Defaulted Loan Script 2 (2nd Mortgage Lender)

Goal: To speak with the individual that is handling this particular account #: ___________.

● Using any correspondence from the customer, look on the bottom of the

page and locate the person’s extension. Call this individual directly and begin the script.

Script Questions:

1.) I need to speak with someone in loss mitigation or someone who handles short pays on second mortgages in foreclosure. The property is located in (Your state) and the account number is _______________________. 2.) Hi! My name is (Your name) and I need to ask some questions about this account. What’s your number, and I will fax you an Authorization to Release Information? Fax # ______________________. Before you get transferred, get their direct line and extension: Phone: ___________________________________ Extension: __________ 3.) What is your name? _________________________________________ 4.) Fax authorization and call back. 5.) Hi! ___________________, this is (Your name) again from (Your company) in reference to account number __________________. Did you get my authorization? 6.) My boss buys 1st and 2nd mortgages and is considering buying the 1st on this property to foreclose off any liens. He would much rather do a short pay or release of lien. Do you think you could get a short pay approved? __________ 7.) Will you need to see financials from the account holder before a decision on the short sale is made? _____________ HUD [ ] Hardship Letter [ ] Financial Stmt [ ] Purchase and Sale Agreement [ ] Pay Stubs [ ] W-2’s [ ] 2 Yr. Tax Returns [ ] 8.) Normal First Mortgage Lender guidelines will not allow more than $1,000 or $2,500 to be paid to subordinating liens. The first mortgage sees the value in taking a discount. Do you think you could get between $1,000 to $2,500 as a short pay approved? 9.) Are you participating in the foreclosure sale to protect your interest, or will you just write off the balance? _____ We are foreclosing _____Write off 10.) If my boss could do forbearance on the account, what would be the least you could take to reinstate the account and begin making regular payments? ______________________________ Okay great! I’ll pass this information to my boss and he’ll be in touch. Thank you for your help!

- 37 -

Section 4

Uncommon Objections To A Short Sale Package (Homecomings Financial, Ocwen, Fairbanks) • You are speaking to the wrong department • The account is not 90 days past due • The account is current. Why start the short sale process? • The account is past due but the bank has relatively good

contact with the debtor • Senior lien holder shows a junior mortgage and feels it would

be a waste of time to attempt to contact • The package can only be sent to the debtor (Use P.O.A. and

copy of deed) General Rule Of Thumb

• Tell the mitigator the seller has given you Power of Attorney (you’ll have to fax to the lender) and a deed in escrow. Tell the mitigator the seller will be checking in soon to fill out the package so you can overnight it back to them.

Mitigator’s Note: The mortgage company/bank views finalization of an account from 2 areas: 1) equity in the home, and 2) the ability of the customer to pay a deficiency balance. You can get a POA and a deed from the customer but it does not excuse the customer from the responsibility of a deficiency. If the customer is Chapter 7 BK, then you are OK. Otherwise, include the debtor’s financial package showing factual inability to deal with the debt along with the POA and deed.

- 38 -

• Watch and Wait investors depend on external forces to start the mitigation process

• Utilize and remind the bank of interest charges, foreclosure fees and costs, accrual of property taxes and foreclosure (lawyer’s) timelines especially in long foreclosure states

• Vacancy reports – If the customer jumps ship and vacates the house, the bank will have to spend money to secure it and maintain/insure the property – offer to secure the property

- 39 -

Give Me $300 And I’ll Order The BPO (Ocwen, Citifinancial)

• May take this posture if the mortgage is current and little collection activity present

• Conflicting information coming from investor versus what collection finds out

• Lack of experience, faulty bank process – Shortly after a foreclosure begins, the bank would normally order an exterior BPO, at a minimum, to get an idea on the value of the house.

Mitigator’s Note: It would not benefit the bank to foreclose on a house that is worth $10,000 for example, or to foreclose on a house where certain code violations would require the bank to demolish the house or which would severely inhibit the bank from selling the house. If the mortgage is 90 days past due or more and the bank is in senior position, chances are a valuation will be done.

Verbage: You: “I’ve never seen a BPO cost $300 before, and I’ve never seen

an account 90 days past due that at least didn’t have a drive by BPO completed. What did your exterior BPO come in at?”

“You are servicing this loan, right? Since when did you start

this policy? Is your investor aware that $300 could cause him a huge loss at REO?

- 40 -

Give Me An Offer And I’ll Order The BPO …he who speaks first loses.

• Bank wants to be compelled and drawn into ordering a BPO • Faulty mitigation process could be present • Inexperienced counselor handling file or they don’t want to

waste time! • For whatever reason exists for a bank to demand an offer

first, they will order the BPO and respond by the following: o Before giving bid, make sure you understand the current

value of the property o Make sure your bidding will provide you with an

acceptable profit margin o Low ball the offer. If the bank has no idea what the value

is they cannot reasonably turn down any offer. Don’t make the offer ridiculous but low enough where they are not sure what to do.

o Once the BPO is ordered, be prepared to increase the offer and start the REAL negotiations from this point forward

Note: As a general rule, expect the B.P.O. to be approximately 80% of actual value. Your first offer should not exceed 80% of this figure: $200,000 Current Market Value x .80 $160,000 Estimated B.P.O. x .80 $128,000 Maximum Offer (64%)

- 41 -

Ball Park Past The Impasse The Safe Offer

• A safe offer is any offer that is 20% below the bank’s BPO. • Bidding may come from the mitigator. • It’s a quick offer, don’t send over a complete letter building

the case unless the mitigator requests you do. Make it verbal to push things forward.

• Get yourself a good idea through comps or a realtor or appraiser’s verbal opinion, estimate repairs, then calculate no more than 65% of after repaired value minus cost to cure. Include your cost of money plus 3 month’s holding cost.

Time Frames That Kill The Short Sale

• Foreclosure sale date set and lack of time to put a short sale together

• Debtor files for bankruptcy. Bankruptcy is good for short sales. You just have to do a little more leg work. If the customer “surrenders” the home in the BK, the debt is discharged by the BK so the financial package is no longer needed. The home is still owned by the customer (even though it was surrendered in the BK but the title company will require that the BK Trustee or BK Judge grant permission to close the deal – which they will usually do as there is no equity in the home to pass to unsecured creditors in the BK). Also, the BK stops any collection and/or F/C actions by the mortgage company/bank furthering the F/C process and increasing the loss to the mortgage company/bank. I find that BK customers are the easiest short sales.

• Incomplete packages from investor

- 42 -

• Customer refuses to supply needed documents for short

sale consideration • Poorly submitted BPO’s where the value of the property is

highly suspect • Losing contact with the mitigator • Mitigation file becomes buried on a Mitigator’s desk under

other files • Mitigator has no time to review your file. Working on deals

that appear closer to closing • Tax sale set and lender not going to pay taxes, and investor

said he will and doesn’t, and property goes to tax sale and is lost.

- 43 -

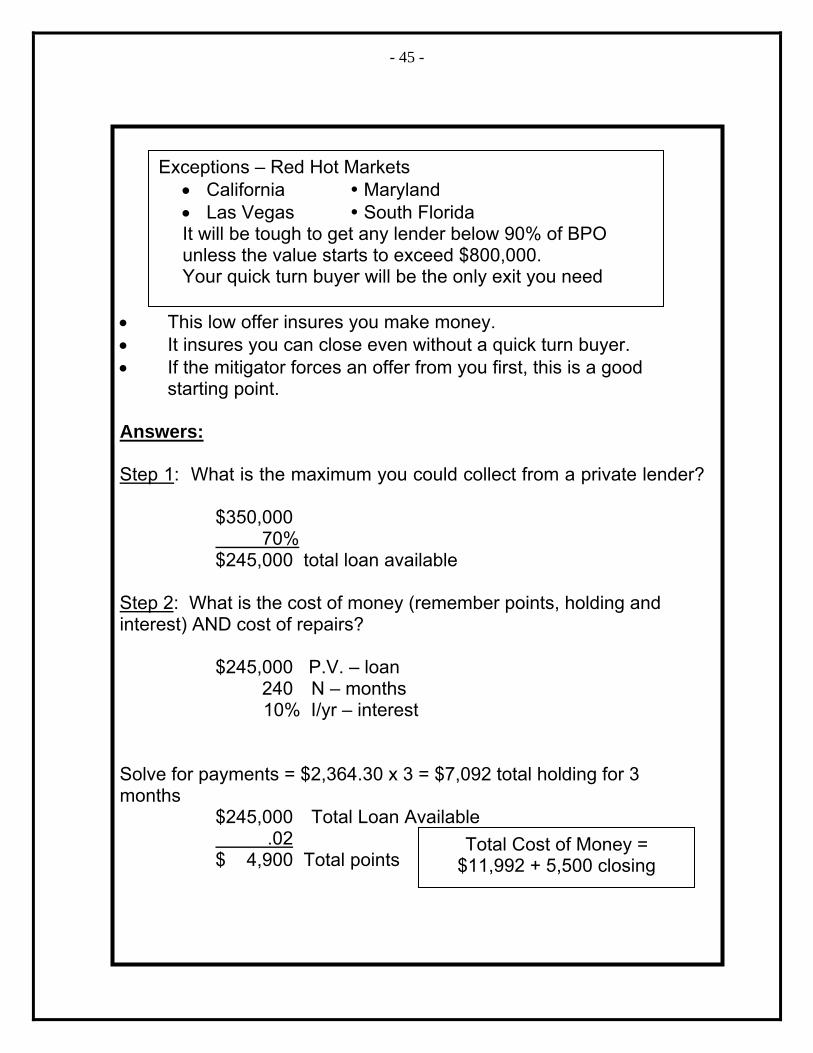

Section 5 How To Calculate The Short Sale Offer

Student Problem – Calculating An Offer You’ve got a property with an exterior BPO of $280,000 (The lender has already done the BPO on their own), and a value, after repairs of $350,000. Your private lender is willing to loan you up to 70% maximum loan to value including repairs, points and 3 months holding cost on an after repaired value (also called subject to repairs).

Repairs are $8,500 Loan balance is $301,394 Interest rate is 7.99% (approx. interest per month is

$2,000) Back taxes $3,942 Total taxes/year $4,300 Back insurance owed $1,650 Insurance per year $1,800 HOA $1,500 Attorney fees $2,000 Average days on market – 120 Last payment Jan. 13, 2004

He will charge 2 points and 10% interest, closing costs are $5,500. Amortization is 240 months. He is willing to finance 100% of the purchase up to 70% LTV

- 44 -

What would be your offer on the short sale? Solve by calculating the following: Step 1: What is the maximum you could collect from a private lender? Step 2: What is the cost of money (remember points, holding and interest) and cost of repairs? Step 3: How much money is left over to fund your short sale? Step 4: Once repairs and closing costs are taken into consideration, what is left over to pay the short sale? _______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________ Step 1: Start with the exit Our short sale offer is driven by what we can fund using private money at 65% excluding interest and points Maximum of 70% including closing costs and 3 months holding, repairs and closing Step 2: Build your case to support your offer using the REO ratio.

- 45 -

• This low offer insures you make money. • It insures you can close even without a quick turn buyer. • If the mitigator forces an offer from you first, this is a good

starting point. Answers: Step 1: What is the maximum you could collect from a private lender? $350,000 70% $245,000 total loan available Step 2: What is the cost of money (remember points, holding and interest) AND cost of repairs? $245,000 P.V. – loan 240 N – months 10% I/yr – interest Solve for payments = $2,364.30 x 3 = $7,092 total holding for 3 months $245,000 Total Loan Available .02 $ 4,900 Total points

Total Cost of Money = $11,992 + 5,500 closing

Exceptions – Red Hot Markets • California Maryland • Las Vegas South Florida It will be tough to get any lender below 90% of BPO unless the value starts to exceed $800,000. Your quick turn buyer will be the only exit you need

- 46 -

Step 3: How much money is left over to fund your short sale? $245,000 17,492 cost of money $227,500 - 8,500 repairs $219,000 Step 4: The Calculation

80% of the BPO or 65% of after repaired value minus repairs, minus cost of money WHICHEVER IS LESS! (Cost of money includes points, holdings and closing costs.)

Lender’s BPO 280K Actual After Repaired Value $280,000 $350,000 .80 .65 $224,000 $227,500 Repairs 8,500 $219,000 Cost of money - 11,992 $207,000 Closing Cost - 5,500 $201,500

• You can always come up in Price!

What is the highest you could offer and still secure private funds? ________________

Three main variables in the short sale process will control if you win. I. The right BPO II. Building the right case, the short sale package, justification with

the REO ratio III. Internal lender policies

The total you could borrow using private money is $233,000 – this drives your offer!

- 47 -

Step 5:

Make sure all other short sale variables are specifically crafted and calculated to support your offer of:

$201,500 Starting offer $219,000 Highest offer Your offer is driven by the money you can rent. …Now: What loan to value are you offering the lender in their mind? Offer $201,500 = 72% of BPO BPO $280,000 What are the chances a lender would accept this offer? Poor Fair Good

- 48 -

Three Controlling Variables In The Short Sale Process

Go Back and start reworking the variables which affect a Mitigator’s opinion of the value. I. The BPO Have an interior BPO done so you can provide the repairs estimate and comparables. This is the pivot point that affects everything. II. Building the right case, the package, justification with the

REO Ratio Building the right case – summarized on your offer letter

includes: 1. The debtor being insolvent and does not care 2. What the debtor could do including lengthening the foreclosure

time frame. • Chapter 13 • Chapter 7 • Lawsuit against the lender (this is a doubled-edged

sword, as it may cause the mitigator to refer the file to “in-house counsel”)

• Eviction process • The threat of additional deferred maintenance caused by

homeowner 3. Physical issues with the property:

• Functional obsolescence • No permits for addition • City citations • Survey issues • Appearance • Dated amenities • Largest house in the neighborhood • Inferior construction materials • Repairs

- 49 -

4. Other – Comps:

• Days on market • Low sold comps • Comp adjustments • Declining area • Reverse appreciation • Criminal activity in the area • Inaccessibility • Rural area • Tax liens (IRS and State) • Property tax sale done and property not redeemed yet

III. Internal Lender Policies

• These will not be known to you:

1. Is the debtor communicating something to the mitigator that affecting your Short Sale? 2. The PMI insurance company has the final say-so regarding discount. _______________________________________ 3. Does the mitigator have to reach a particular threshold of lack of communication before being able to negotiate with you?

- 50 - You can find some of your answers just by asking

the Mitigator: 1. What percentage of the B.P.O. do you normally accept as a Short Sale? ______________________________________ 2. The general opinion or attitude of the mitigator towards the chances of a third party bidding at the sale. 3. Are larger loans normally given more lead way regarding postponements? ___________________________________

- 51 -

- 52 -

Student Problem – Building The Short Sale Offer Letter

Bill Brokeleg is a struggling self-employed plumber recently injured on the job. He calls you indicating he is 38 days late on his 1st mortgage with Litton Loan Servicing. There is a second and small third. Both of these are 4 months in arrears. Taxes are one year overdue. Homeowners’ association dues for the year are unpaid. Subject property is in good condition. 3 years old. However, the septic system has failed, cannot be pumped. Homes are selling in about 4.5 months on average. Seller is willing to walk for no money, and can move any time. Some homes have taken as long as 13 months to sell. Basement floods at times. Some visible but minor mold. Ice maker supply has leaked for 2 years in the wall – cannot be seen unless refrigerator is pulled out from wall. Insurance per year is $475. Payment on first is due for January Summary: payments First mortgage – Litton loan Balance $165,000 1,450 x 3 Second mortgage – Fairbanks Capital 35,000 Third – Household Finance 4,500 H.O.A. 1,560 Taxes Due 2,875 Septic Cost to repair – seller got quote (new drain lines, labor) 4,100 No other cost estimates at this time Total costs excluding payments ____________ Current appraisal of $235,000 What’s the total LTV?_____________ exclude payments Other Factors:

• Lender had only one contact with homeowner. Debtor indicated he was going to let it go to sale

• Drive-by BPO complete • Seller signed deed package and all hold harmless agreements

- 53 -

• Second will eventually agree to accept $3,500, third accepts $500 but this is not known yet.

Key factors when short selling multiple mortgage deals: • Start with the LTV desired and work the points of least

resistance • Initiate contact to the first mortgage holder to test flexibility. (In

this case we had to wait.) Work on… o Other liens o Repairs o Taxes and H.O.A.

• Your REO ratio will be carefully calculated below what the first mortgage is willing to take hoping your final number does not exceed 70% of what your private lender is willing to loan inclusive of all costs.

Payments have nothing to do with the equation Our goal is to negotiate so all loans, liens and expenses do not exceed 65% LTV With regards to discounting only, name your 3 most productive actions: Step 1 Contact the first mortgage holder. Tell them you contacted the debtor who is considering bankruptcy and walking away. You: “I want to buy the house but will need a bit of a short pay to do so. How soon can I make an offer?” Lender: “Once it goes to loss mitigation, you can contact them. It will be about 60 days.” You: “Please indicate to the mitigator my contact information. Do you know who it will go to?”

- 54 -

Step 2 Call the second mortgage next. Ask flexibility questions. Start below 10% and work your way up. Will they need you to build a case? Your goal is $3,500 Next: Call third mortgage. Test flexibility.

• Tell them the house is going to sale! • Seller doesn’t care • You are going to buy the first and foreclose off junior liens

If you get lack of willingness, start to build a case. Your goal is $500 Step 3 Take your new numbers and calculate what the first mortgagee can accept as a short to achieve 65% Total LTV! $3,500 Second mortgage final acceptance 500 Third mortgage final acceptance 1,560 HOA payoff 2,875 Taxes due 4,100 (Septic (real costs) $12,535 Total known payoffs to this point Appraisal 235,000 .65 Desired LTV 152,750 Maximum loan - 12,535 Other real costs 140,215 Your baseline on first mortgage …Remember: Cost of Money: $152,750 x 2% pts =$3,055 $152,750 @ 240 months @ 10% interest = $1,474 x 3 months = $4,422 Estimated Closing = $2,000 Subtract Total Cost of Money = $9,477

- 55 -

$140,215 - 9,477 Total Closing Costs $130,738 Your offer starts here $130,738 $235,000 = 55% LTV Total What is the highest you could go up on the first mortgage offer and still not exceed a combined LTV of 70% $235,000 70% private investor funds $164,500 -22,012 other expenses Total ($12,535 + 9,477) $141,988 Highest offer With their balance at $165,000, you would need to get a minimum reduction of $24,237 on a discount of the first mortgage. What are your chances? Good Fair Poor Very, very ____________ because the __________________ has not been ordered yet. Your task: Build Your Short Sale Offer Letter Remember… Describe any issues with the seller Describe any issues with the property Tell the lender what you need What is your best controlling variable in this short sale? ____________________________________________ Don’t use the REO ratio at this time. This is just a preliminary offer to initiate the interior BPO

- 56 -

First Mortgage Negotiating Script – Short Time Frame States Date __________________

Sellers _________________________ Phone __________________

Cell Phone _________________ e-mail _______________________

Address ________________________________________________

Alternate Address ________________________________________

Sale Date ______________ Comps ____________ Value ________

Debtor’s Social _________________________

Balances ____________ 1st ____________ 2nd ____________

As Is Equity _______________________

You: 1) Hi, this is _____________ calling on Account # ___________.

The debtor is _____________. Do you have my authorization? Lender ______________________ Mitigator __________________ Address _____________________ Phone ____________ ext. ____ ______________________ Fax _____________________ e-mail ___________________ 2) I’m buying Mr. and Mrs. ___________ property but am going to

need a short sale. Can you fax or e-mail me the short sale package.

3) By the way, what’s the most efficient way to communicate to

get this done?

- 57 -

4) I just want to confirm the sale date. What date do you have? 5) What is the approximate principal balance on the account? 6) The seller has proposed a bankruptcy to stop the sale but I’ve

got him(her) talked out of it for now. If things line up on my offer will you do a bit of a postponement so I can get closed?

Mitigator: Possibly. How long a postponement? You: I’ll need until _________ (last business day of next month) to

finish title, get the package back to you and close. Alternate Answer: Mitigator: No You: Why not? Mitigator: It costs us money. You: I don’t expect you to postpone for free. How much would it

cost? You: I’ll put up the $_______ as a non-refundable deposit once we

come to terms on the short sale. Do you have a BPO back on this one?

Mitigator: Yes, exterior You: What is the fair market value you have? Mitigator: We can’t disclose our BPO You: There are some issues you should be aware of inside. Can

you get an interior ordered? Mitigator: Go ahead and send me an offer and I will.

- 58 -

You: I’ll put together a cost to cure and send the offer along with the BPO Can you have the person doing the BPO contact me to get in? The seller has given me access.

Mitigator: Send me an offer and I will. You: My offer will be between ________ and ________ depending

on my cost to cure analysis. Now will you go ahead and order the interior and give me a couple of weeks to get this completed?

Mitigator: Not until I get a written offer. This is your chance to send an offer reflecting the REO ratio. You: I’ll fax/e-mail it to you A.S.A.P. Do you still want me to try and keep the seller from filing a Chapter 13? Mitigator: I don’t care. Offer gets sent. Negtiations are started. Your offer declined. You call the mitigator back. Round Two: You: How far am I off from acceptance? Mitigator: Too far off for me to make anything happen You: That is because my offer reflects repairs you are unaware of; we aren’t comparing the same notes because you don’t have an interior. Assuming you had the BPO back, what percentage of the BPO are you normally able to accept? Mitigator: We take fair market value or 100% of the BPO You: How about the other hard costs – those aren’t calculated against the BPO?

- 59 -

Mitigator: No Mitigator: Then, I’ll order an interior You: Great, I’ll have the short sale package back to you A.S.A.P.

At this point you are dealing with a mitigator who is not willing to make a deal. Simply contact them during and directly after the Chapter 13 and Chapter 7 bankruptcies are in process.

Approximately 6 months later You: I’ve collected some empirical data on properties in this area and see lenders are recouping about 76% of fair market plus 3rd party bidding in this area is super weak. What would you do if you were in my shoes to get your boss to consider an offer that makes sense? Mitigator: Give me another offer. I’ll see what I can do.

- 60 -

Section 6 Geographical Areas And State Laws That Influence A Loss Mitigator’s Decisions Six Areas Affecting Your Ability To Short Sale • First identify your market • Don’t make assumptions on subjective, non-factual information • You can create exceptions based on…

o A superior marketing campaign to locate sellers o Your ability to build a case for the short sale o Sharp communication skills o Willingness to apply yourself, adapt, and build systems

Red Hot Markets • Most of California • Vegas • All of South Florida • Maryland • D.C. • Burrows in N.Y. • Miami • Parts of Georgia • Parts of Texas • New Jersey • Other pocket areas

- 61 -

Perceived Characteristics Seller’s Market - Multiple offers before you ever get to the deal. Sellers feel they can get top market because investors are bidding against each other Aggressive Investors – It appears other investors are door knocking and competition for a deal is tight. Investors pay more. Realtor Competition – Many sellers are able to list their homes during foreclosure knowing they will sell Strong Appreciation – Values incline faster than interest accrues on the debt, thus keeping the homeowner with the appearance of a safe equity position Mitigator Attitudes – Perception that all loss mitigators don’t think they should discount because if repossessed it will sell at full value.

- 62 -

How To Build Your Business in Hot Markets a. Increase shotgun marketing – they find you Your goal is to find sellers who are not on the defaulted list

• Systematically mail postcards into areas you want to buy. Get your stop foreclosure message out everywhere

• You are looking for extreme hardships, bitter divorces, custody battles, sellers who don’t care or don’t know about the market

b. Rifle marketing

• Stronger campaign to those on the default list. Win over your competition through superior communication and rapport

c. Target only vacants or relocation customers

• “Behind on your mortgage and want to relocate? We can help.”

d. Develop an iron clad marketing brand

• “Our business is built on integrity” e. Create an incredible benefits package

• Find the seller an apartment • Moving truck • Credit restoration • Buy them a car • Joint venture the deal (profit sharing)

f. Be better than your competition

• Get referrals from a mitigator

- 63 -

Mitigator’s Note: Send the mitigator a box of chocolates with

a thank you card telling him/her how nice and professional he/she was – it is great for the mitigator because we usually just get complaint calls…the chocolates can be shared with his/her co-workers so the gift is not extravagant enough to be considered a conflict of interest. Most importantly a decent (not gold-plated or silver - $5 total cost) ink pen with your name and phone number and area that you want properties. I have one from another investor – I like to use it because it is a nice pen with rubber cushions for my fingers and it has his name, number, and areas where he wants to buy. When I have a deal that fails, I call him because his name, number and geographics are literally at my fingertips – do not send more than 1 pen or they will get trashed. His co-workers will covet the pen and may even try to get your number to call you and work a deal just for the pen. Don’t send the same chocolates and card – make each “thank you” unique. • Referrals from a person conducting the brokers price

opinion – realtors – bankruptcy attorneys • Run TV spots or radio spots

g. Concentrate on high end homes only

• Add niche for waterfront or resort properties. Become known as the “high end home specialist”

• “Investment company wants 3 executive corporate homes in this area. Behind on payments, no problem”

h. Build a superior case for why the lender should discount

• Find houses with large second mortgages whereby the mitigator doesn’t understand the market

i. Search out fringe areas or rural areas in these markets j. Secure lines of credit or fast funding so you can close

quicker than your competition

- 64 -

Short Time Frame States – Perceived Characteristics

Not enough time to get the short sale package complete for an approval process which also takes too long. The attitude most lenders just want to take the house to sale. Not enough time to find the seller on a quick turn. Seller Issues – can’t get them to move quick enough or the seller gives up because they think the time frame has beat them It takes money in these areas to cure or fund quickly

- 65 -

How To Build Your Business in Short Time Frame States

a. Always, learn to communicate time frames with the lender. “Mr. Mitigator, I’m going to need a short sale on this one but we only

have 16 days left before the auction. Are you willing to work with me? You’ll find out why once I submit the package.”

“Do you have the BPO back on this one?” “Yes.” “I think you should get an interior done. There are some real issues.” (This process alone will give you two weeks.) b. Request a postponement with a contract – show proof of funds. “Mr. Mitigator, I’ll fax a copy of the purchase contract. The seller signed everything we need to close including the deed which is being held in escrow by the closing agent. All I need is 30 days to clear some final things before closing. I would have never gotten into this mess had I known it was going to sale in two weeks. If I go ahead and send you the contract, you can get it postponed, right?” … If No. “I’ve spent time securing the purchase money and I have proof of funds, surely your boss is wise enough to see this as a bird in hand. Besides, I need to send you some pictures and estimates. There are some REPAIR ISSUES you need to see. By the way, I’ll take it “as is,” where “is” means with no other contingencies. c. Go through bankruptcy conversation

- 66 -

“The seller was going to file a Chapter 13, then 7, but I talked her out of it. So we’ve got two choices: First, I’ll go to work to get you a complete short sale package, with a strong case for a short sale. Will you let me know what else we can get to your investor (or committee) to get the short sale approved? Secondly, I have calculated the approximate hard costs with both bankruptcies, assuming the seller tries to go that route. If I can keep this loan out of 9 months of bankruptcy, would this help my chances on the short sale assuming the deal makes sense with your net? d. Offer up another month’s interest to postpone.

Mitigator’s Note: Offer a non-refundable deposit of $2,500 (be willing to pay $5,000) but the $2,500 would be deducted from the short sale price. This way the bank can stop actions without risk/compensation.

“Of course, I don’t expect you to postpone the sale without me covering your hard costs for 30 days. What are the hard costs?” e. Bring the arrears current to prevent the sale f. Be sure you’ve automated the short sale process

• E-fax to collect packages or scanner to e-mail • Fax to seller • Have them pre-collect w-2s, pay stubs, bank statements

g. Build your business on private money and quick closings h. Fire out as much marketing as you can to have those in default

contact you. These will be people less than 90 days in arrears giving you more time.

i. Set your niche in $250,000 plus home in default. Lenders with

jumbo loans are 90% more likely to postpone. They foreclose on $100,000 houses all day.

- 67 -

Lengthy Redemption States • Minnesota – 6 mos • Michigan • Colorado • Maryland • Alabama Perceived Characteristics • Lack of flexibility from the Mitigator’s standpoint

o One the bank always bids the subject property back at the sale and therefore a mitigator won’t consider a discount

Seller Issues • They think they enjoy all the time in the world to redeem –

unmotivated • They want to camp in the house for free and are tough to move

out

- 68 -

How To Build Your Business In Lengthy Redemption Areas

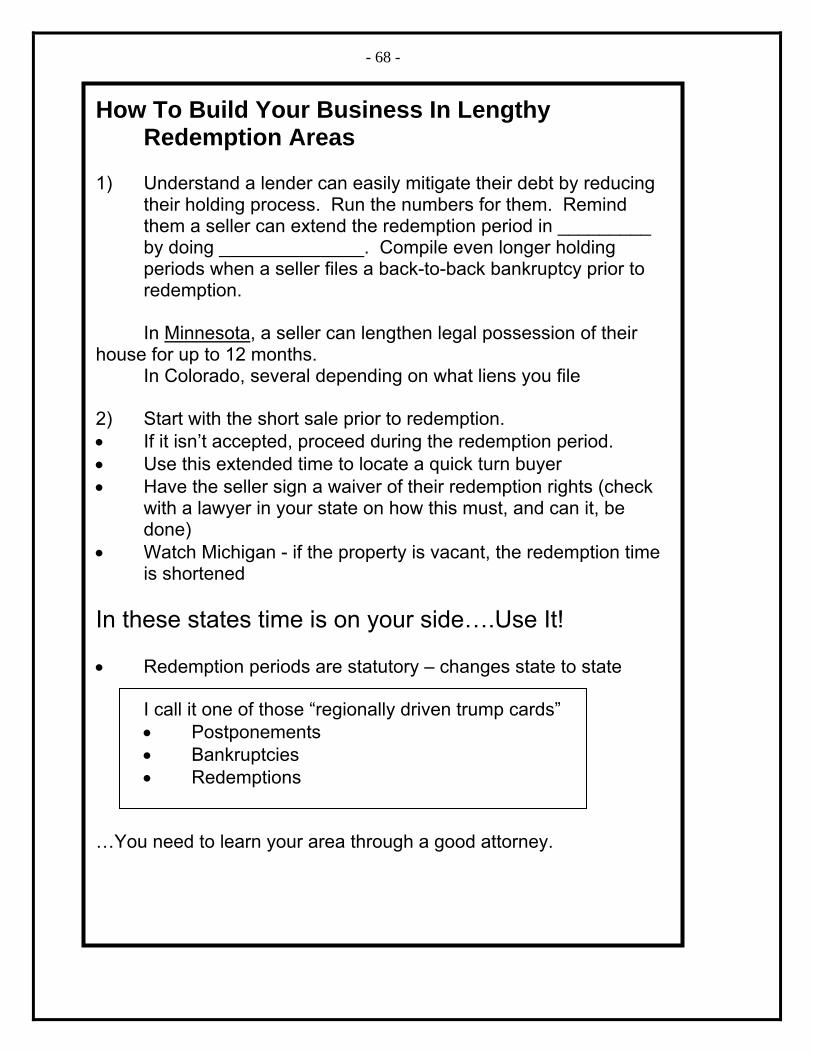

1) Understand a lender can easily mitigate their debt by reducing

their holding process. Run the numbers for them. Remind them a seller can extend the redemption period in _________ by doing ______________. Compile even longer holding periods when a seller files a back-to-back bankruptcy prior to redemption.

In Minnesota, a seller can lengthen legal possession of their house for up to 12 months. In Colorado, several depending on what liens you file 2) Start with the short sale prior to redemption. • If it isn’t accepted, proceed during the redemption period. • Use this extended time to locate a quick turn buyer • Have the seller sign a waiver of their redemption rights (check

with a lawyer in your state on how this must, and can it, be done)

• Watch Michigan - if the property is vacant, the redemption time is shortened

In these states time is on your side….Use It! • Redemption periods are statutory – changes state to state

I call it one of those “regionally driven trump cards” • Postponements • Bankruptcies • Redemptions

…You need to learn your area through a good attorney.

- 69 -

Make sure you clearly understand these issues: • Some lenders will approve short sales during the redemption

period • Legal title can be conveyed during the redemption period and

be a valid deed • A seller can file bankruptcy during the end of redemption period

increasing holding costs – your short sales will be greater as reflected on the REO ratio

• The redemption amount for the seller is the loan balance plus

costs, fees, etc. HOWEVER, the lender can underbid to preserve the right for a deficiency

(…according to the I.R.S., an insolvent seller has no gain)

• A court order can extend the redemption period • Your deed from the seller back to the bank prevents the

process of redemption • Are there any strategies a seller can use to extend redemption?

Yes! Adding liens prior to redemption expiration! …It has to do with lender redemption, as well as, owner redemption…watch for technical rules for filing notice of intent to redeem

A lender cannot accept payments and/or reinstatement during a

redemption period. Can they accept a non-refundable deposit?

- 70 -