short and medium-term oil market outlook - shfe.com.cn · short and medium-term oil market outlook...

TRANSCRIPT

© OECD/IEA 2016

Short and Medium-Term Oil Market Outlook

13th Shanghai Derivatives Market Forum - 25 May 2016

© OECD/IEA 2016

Oil world changed on Nov. 27th 2014

OPEC doesn’t cut production to support prices. “The market will find the price.”

Brent falls from $80/bbl to $70/bbl.

At Dec. 4th 2015 meeting OPEC removes production quotas & price falls from $43/bbl to $27/bbl.

20

40

60

80

100

120

May 14 Sep 14 Jan 15 May 15 Sep 15 Jan 16 May 16

$/bbl Brent crude oil

Copyright © 2016 Argus Media

© OECD/IEA 2016

Where are we now?

Demand growth is solid

China’s growth rate slows

India’s growth rate picks up

Global supply growth falling away

OPEC & non-OPEC growth down

Non-OPEC falls sharply led by US

Iran is stand-out country

Market getting close to balance

Prices reach 4-month high

Looking further ahead

© OECD/IEA 2016

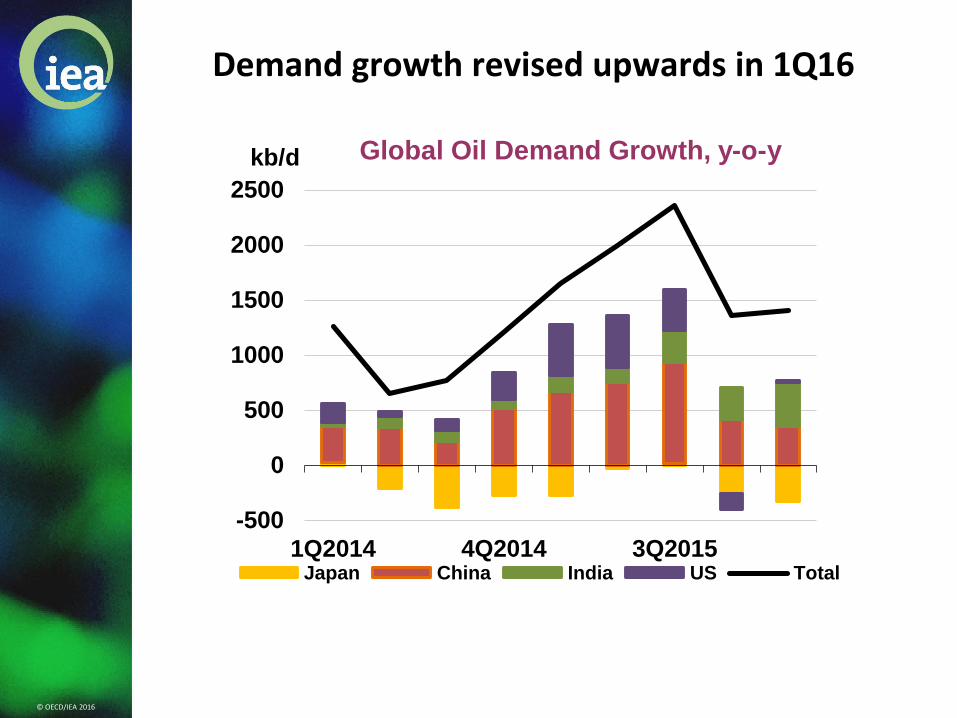

Demand growth revised upwards in 1Q16

-500

0

500

1000

1500

2000

2500

1Q2014 4Q2014 3Q2015

kb/d Global Oil Demand Growth, y-o-y

Japan China India US Total

© OECD/IEA 2016

Indian demand races ahead

0

100

200

300

400

1Q2015 3Q2015 1Q2016

kb/d Indian Demand Growth, y-o-y

LPG/naphtha FO/other

Gasoil/Jet/Kerosene Gasoline

Total

© OECD/IEA 2016

India takes the lead in oil demand growth

© OECD/IEA 2016

China – slowing growth but still strong

0%

3%

6%

9%

0

4

8

12

1Q2014 3Q2014 1Q2015 3Q2015 1Q2016

mb/d Chinese Oil Demand

LPG/naphtha Gasoline

Gasoil Others

Growth (RHS) %

© OECD/IEA 2016

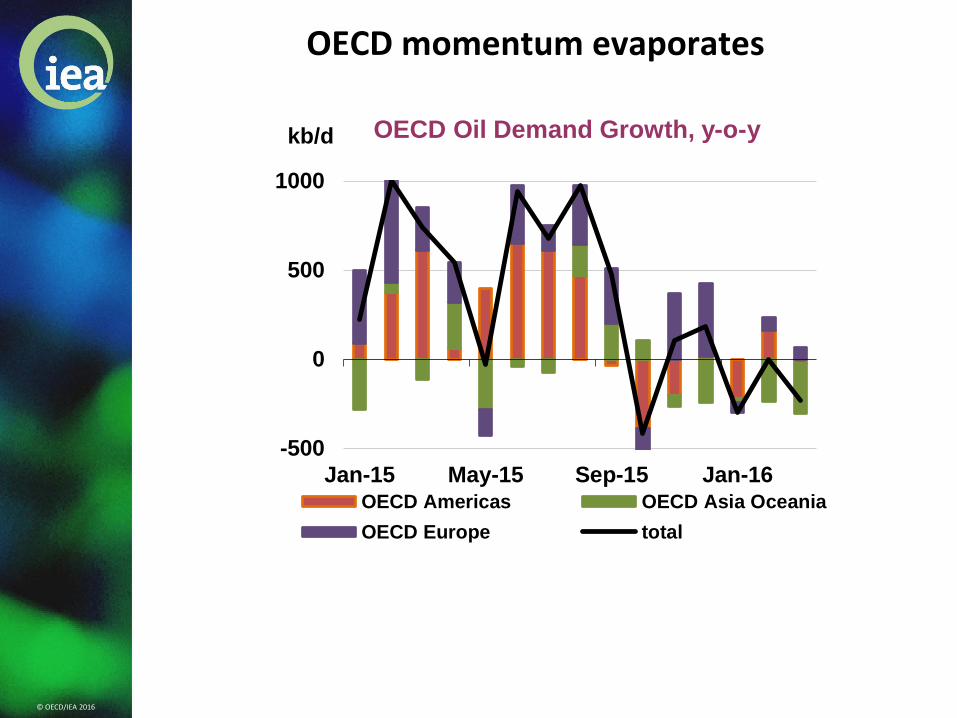

OECD momentum evaporates

-500

0

500

1000

Jan-15 May-15 Sep-15 Jan-16

kb/d OECD Oil Demand Growth, y-o-y

OECD Americas OECD Asia Oceania

OECD Europe total

© OECD/IEA 2016

Outages & low prices take toll on supply

-1.5-1.0-0.50.00.51.01.52.02.53.03.54.04.5

Jan 14 Jun 14 Nov 14 Apr 15 Sep 15 Feb 16

mb/d

Thousands

OPEC and Non-OPEC Oil Supply Year-on-Year Change

OPEC Crude Non-OPEC

OPEC NGLs Total Supply

© OECD/IEA 2016

Non-OPEC supply falling fast

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1Q12 1Q13 1Q14 1Q15 1Q16

mb/d

Other North America Total

Total Non-OPEC Supply, y-o-y Change

© OECD/IEA 2016

US supply growth vanishes

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

mb/d US Crude Supply - Yearly Change

© OECD/IEA 2016

OPEC pumps at robust rate

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Jan 14 Jul 14 Jan 15 Jul 15 Jan 16

mb/d OPEC Growth y-o-y

Other OPEC Iraq Saudi Arabia

Iran OPEC

© OECD/IEA 2016

Iran only major growth in OPEC

2.50

2.75

3.00

3.25

3.50

3.75

4.00

4.25

mb/d Iran Crude Supply

© OECD/IEA 2016

OECD stocks draw in February

2,500

2,600

2,700

2,800

2,900

3,000

3,100

Jan Mar May Jul Sep Nov Jan

mb OECD Total Oil Stocks

Range 2011-2015 Avg 2011-2015

2015 2016

© OECD/IEA 2016

Market heading towards balance

-2.5

-1.5

-0.5

0.5

1.5

2.5

3.5

84

86

88

90

92

94

96

98

1Q09 3Q10 1Q12 3Q13 1Q15 3Q16

mb/dmb/d Demand/Supply Balance until 4Q16*

Impl. stock ch.&misc (RHS) Demand Supply*

*OPEC crude production assumed to ramp up to average 33.0 mb/d in 2Q16, 33.2 mb/d in 3Q16 and 33.1 mb/d in 4Q16

© OECD/IEA 2016

Oil rallies to 4-month high near $45/bbl

20

40

60

80

100

120

May 14 Sep 14 Jan 15 May 15 Sep 15 Jan 16 May 16

$/bbl Benchmark Crude Prices

WTI Cushing N. Sea Dated Dubai

Copyright © 2016 Argus Media

© OECD/IEA 2016

Looking ahead to 2021

Demand growth solid at 1.2 mb/d through 2021

Production growth slashed as investment cuts bite

Crude trade shifts more and more eastwards

Huge uncertainties

OPEC production policy

Non-OPEC

World economy

Efficiency gains

© OECD/IEA 2016

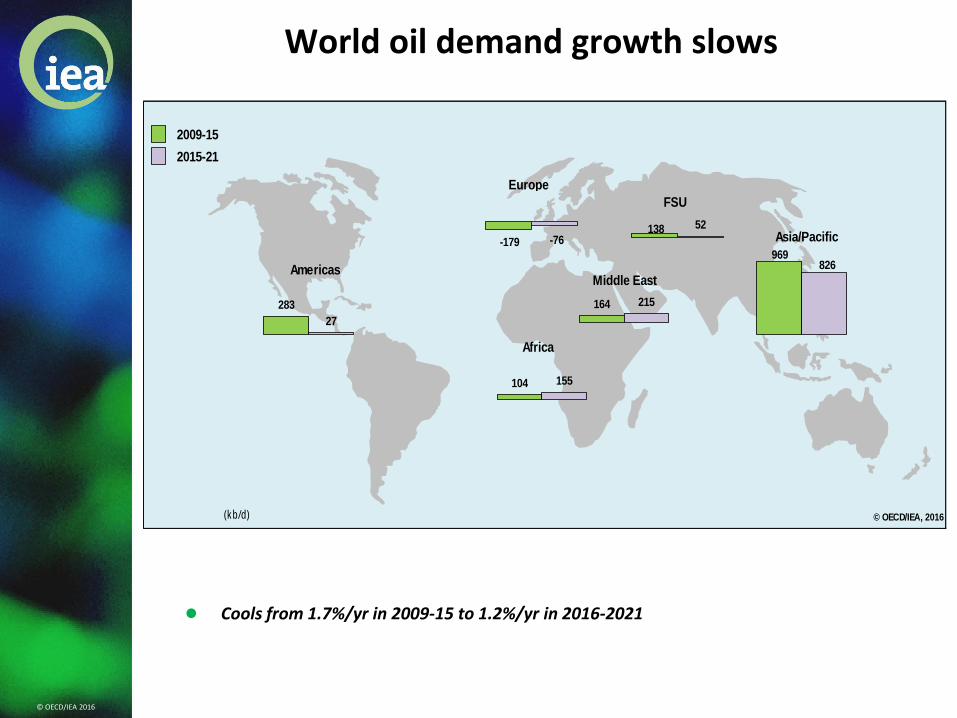

World oil demand growth slows

Cools from 1.7%/yr in 2009-15 to 1.2%/yr in 2016-2021

2009-15

2015-21

© OECD/IEA, 2016(kb/d)

-179 -76138 52

283

27

164 215

104 155

Americas

Africa

Middle East

Europe

FSU

969826

Asia/Pacific

© OECD/IEA 2016

Non-OECD drives global demand

Despite concerns about slowing Chinese demand, overall non-OECD momentum remains strong

0

10

20

30

40

50

60

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

mb/d

OECD vs NonOECD Total products

OECD NonOECD

0

2

4

6

8

10

12

14

16

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

mb/d

OECD vs NonOECD Motor Gasoline

© OECD/IEA 2016

Chinese demand growth slips a gear

Economy slows and shifts from industry to services

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

2

4

6

8

10

12

14

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

mb/d

LPG

Naphtha

Motor Gasoline

Jet & Kerosene

Gasoil/Diesel

Residual Fuel

Other Products

y-o-y Growth (RHS)

© OECD/IEA 2016

Indian oil use races ahead

Motorists take to the roads

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

kb/d

LPG

Naphtha

Motor Gasoline

Jet & Kerosene

Gasoil/Diesel

Other Products

© OECD/IEA 2016

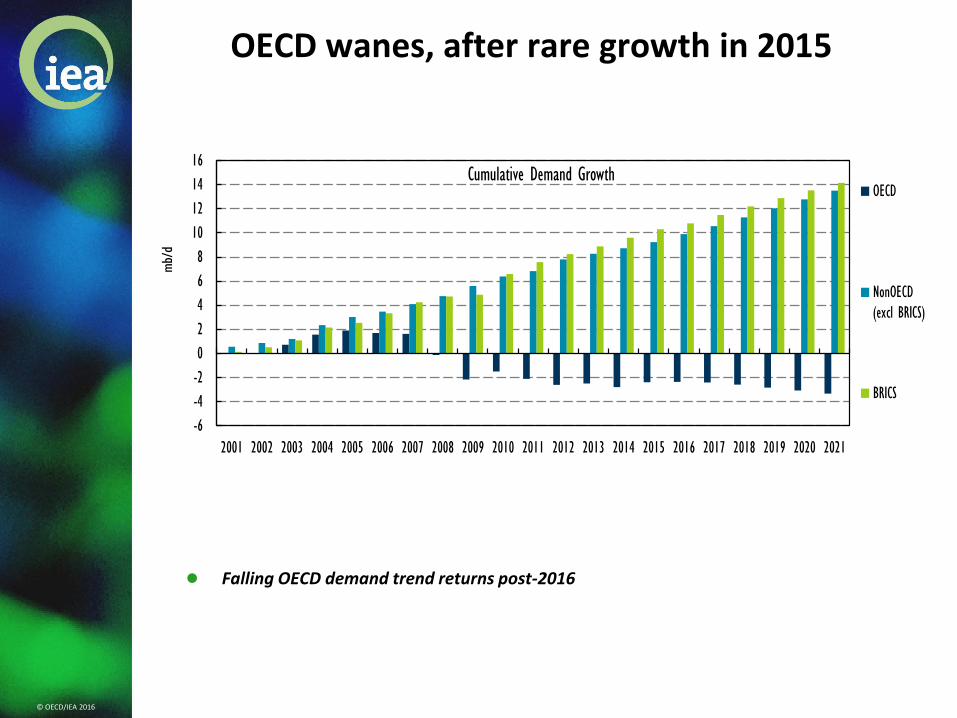

OECD wanes, after rare growth in 2015

Falling OECD demand trend returns post-2016

-6

-4

-2

0

2

4

6

8

10

12

14

16

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

mb/dCumulative Demand Growth

OECD

NonOECD

(excl BRICS)

BRICS

© OECD/IEA 2016

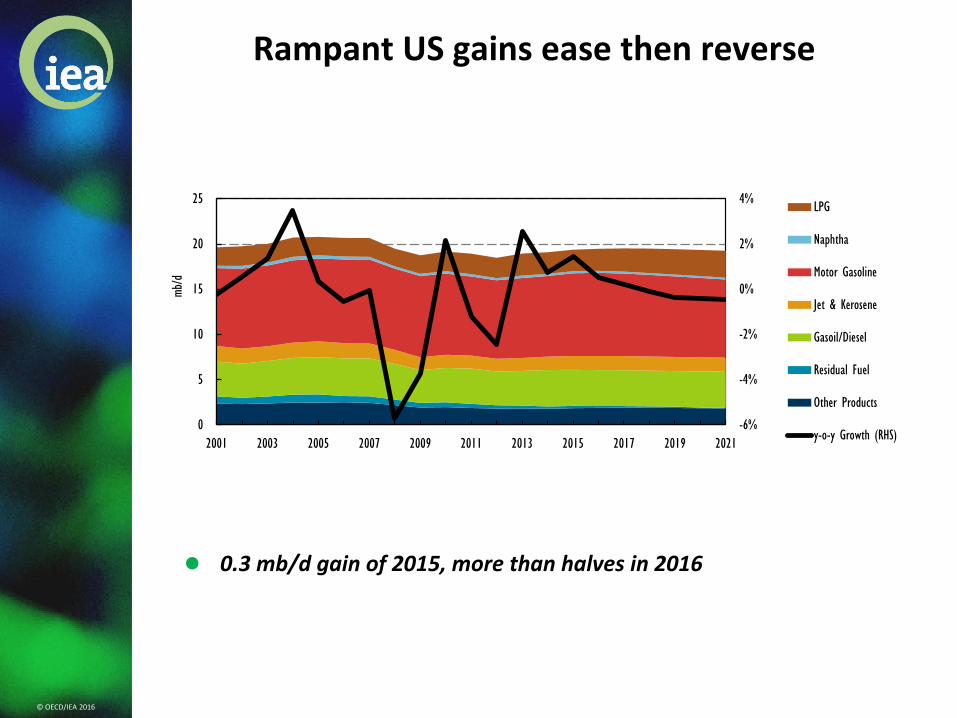

Rampant US gains ease then reverse

0.3 mb/d gain of 2015, more than halves in 2016

-6%

-4%

-2%

0%

2%

4%

0

5

10

15

20

25

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

mb/d

LPG

Naphtha

Motor Gasoline

Jet & Kerosene

Gasoil/Diesel

Residual Fuel

Other Products

y-o-y Growth (RHS)

© OECD/IEA 2016

Upstream oil capex cut for 2nd year

Drop of 17% in 2016 follows 24% reduction in 2015

0

100

200

300

400

500

600

2002 2004 2006 2008 2010 2012 2014 2016

USD

billion

0

100

200

300

400

500

600

2002 2004 2006 2008 2010 2012 2014 2016

USD

billion

America N America S Europe Australia

Middle East Russia Asia Africa

© OECD/IEA 2016

World supply growth plunges

2015-21 growth slows to 4.1 mb/d vs 11 mb/d in 2009-15

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2014 2015 2016 2017 2018 2019 2020 2021

mb/d

OPEC Non-OPEC

*2014 -15 shows actual output growth. 2016 assumes Iran ramp-up. OPEC capacity increases thereafter.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2014 2015 2016 2017 2018 2019 2020 2021

mb/d

OPEC Non-OPEC World

*2014 -15 shows actual output growth. 2016 assumes Iran ramp-up. OPEC capacity increases thereafter.

© OECD/IEA 2016

Non-OPEC supply growth collapses

-1500

-1000

-500

0

500

1000

1500

2000

2500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

kb/d

Other non-OPEC

China

Latin America

FSU

Other Asia

Europe

OECD Americas

Total

© OECD/IEA 2016

US LTO takes biggest hit for now

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2010 2012 2014 2016 2018 2020

mb/d

Bakken Eagle Ford W. Texas Niobrara Other LTO

Output to drop by 800 kb/d over 2016-17

© OECD/IEA 2016

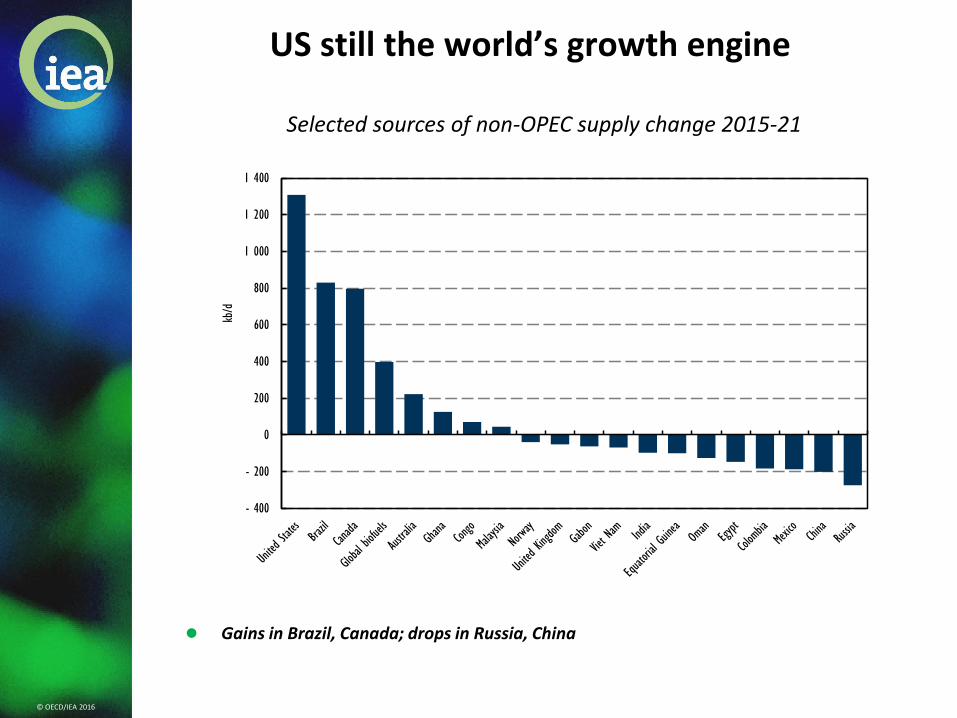

US still the world’s growth engine

Gains in Brazil, Canada; drops in Russia, China

Selected sources of non-OPEC supply change 2015-21

- 400

- 200

0

200

400

600

800

1 000

1 200

1 400

kb/d

© OECD/IEA 2016

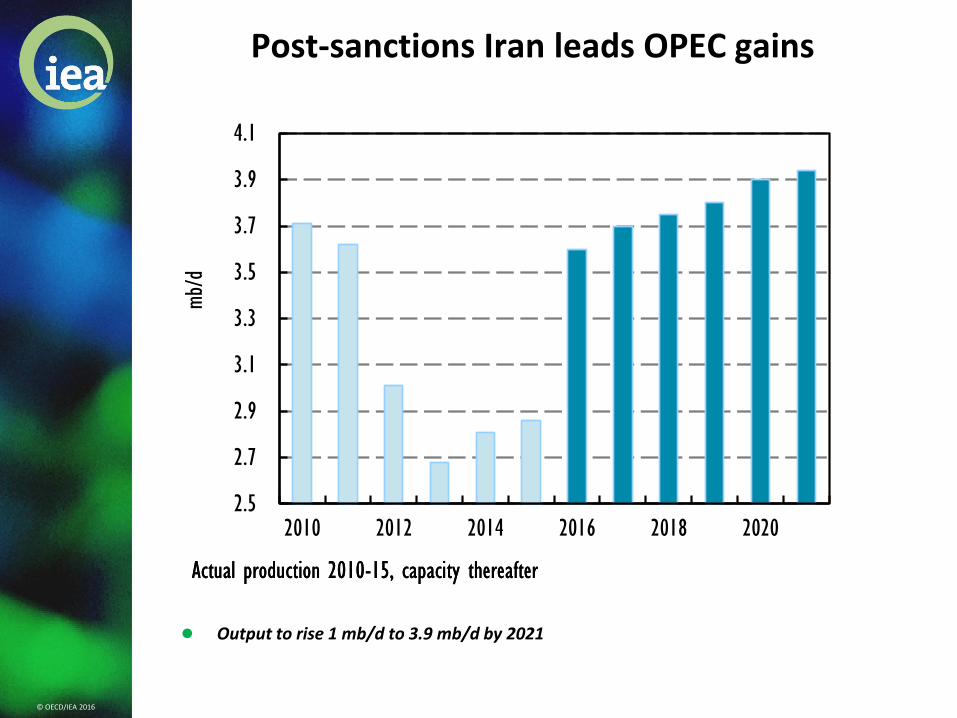

Post-sanctions Iran leads OPEC gains

Output to rise 1 mb/d to 3.9 mb/d by 2021

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

4.1

2010 2012 2014 2016 2018 2020

mb/d

Actual production 2010-15, capacity thereafterActual production 2010-15, capacity thereafter

© OECD/IEA 2016

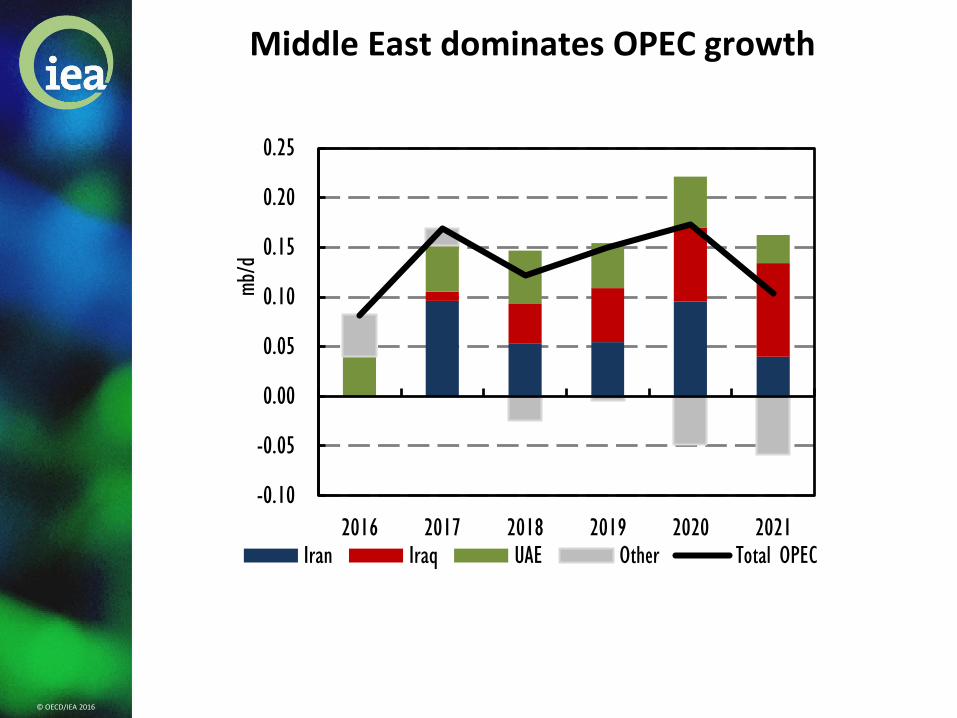

Middle East dominates OPEC growth

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

2016 2017 2018 2019 2020 2021

mb/d

Iran Iraq UAE Other Total OPEC

© OECD/IEA 2016

Surplus erodes in 2017

Tightening market drives price recovery - $80/bbl in 2020?

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

82

84

86

88

90

92

94

96

98

100

102

2004 2006 2008 2010 2012 2014 2016 2018 2020

mb/dmb/d Global balance

Implied Stock Change World Demand World Supply

© OECD/IEA 2016

Conclusions

Global oil supply growth is plunging, as low prices take their toll

Iran leads OPEC gains over the forecast period

Despite a near-term dip, U.S. production rises to an all-time high

While global oil demand growth is slowing, oil use crosses the symbolic 100 mb/d mark towards the end of the decade

The availability of resources that can be easily and quickly tapped set to limit the scope of price rallies – at least in the near-term

The historic investment cuts now being seen raise the odds of oil-security surprises in the not-too-distant-future

© OECD/IEA 2016

IEA Oil Market Analysis

The leading oil market report since 1983, with the latest data and outlook.

Market analysis underpins the IEA’s emergency response mandate

Five-year outlook for supply & demand trends.

Complements short-term OMR and long-term World Energy Outlook analysis.

www.oilmarketreport.org