sheldon township fire district - beaufort county · sheldon's investment in its capital assets...

TRANSCRIPT

SHELDON TOWNSHIP FIRE DISTRICT

ANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED JUNE 30, 2013

SHELDON TOWNSHIP FIRE DISTRICT ANNUAL FINANCIAL REPORT

JUNE 30, 2013

FINANCIAL SECTION

Independent Auditors' Report

Management's Discussion and Analysis

Basic Financial Statements

Government-Wide Financial Statements:

Statement of Net Position

Statement of Activities

Fund Financial Statements:

Balance Sheet- Governmental Funds

TABLE OF CONTENTS

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Position

Combined Statement of Revenues, Expenditures and Changes in Fund Balances- Governmental Fund Types

Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances of Governmental

Funds to the Statement of Activities

Notes to the Financial Statements

Required Supplementary Information

Statement of Revenues, Expenditures and Changes in Fund Balances- Budget and Actual- General Fund

Statement of Revenues, Expenditures and Changes in Fund Balances- Budget and Actual- Debt Service Fund

1

3

10

11

12

13

14

15

16

26

28

FINANCIAL SECTION

CRO\\'I.EY \\'ECIISI .ER & ASSOCIATES 1.1 .( .

cw RidLnd D Cw11 k~ . Cl-':\ . t Y·\ 1.1-.;t r. W~'<. l hll:r. CP.-\

n . R l ll' H-J.> l'l 'HLIC :\<.'COl ' I\T·\:\ IS

www.( '\\':\( 'P.\,;_o,:o\IJL

BF..\lll·OR l • \lOT JN ['Pt L\S_\ \1 1

INDEPENDENT AUDITORS' REPORT

To the Board of Commissioners Sheldon Township Fire District Sheldon, South Carolina

Report on the Financial Statements

.-\u t<.:J ~<:iln ht,lwuc ... r CP.\' ~ot:llt C.11oltm .-\·,,o.;·:al t{la (lf C'P.-\'

We have audited the accompanying financial statements of the governmental activities, and each major fund of Sheldon Township Fire District (Sheldon) as of and for the year ended June 30, 2013, and the related notes to the financial statements, which collectively comprise Sheldon's basic financial statements as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibility

Our responsibility is to express opm1ons on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An aud it also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, and each major fund, of Sheldon, as of June 30, 2013, and the respective changes in financial position for the year then ended in accordance with accounting principles generally accepted in the United States of America.

P. 0 l>UX l::; J 2<) 1' BOl"\TIARY'>T. snrF ::1 RF.AI TORT '\( ~99f' l

1-' U BUX:'.~6Q

~H HOC'\ fO\' \o:i\DK tTl InTI. \lOt "\'T Pl f..l.\'\\1. ~C:%'i'

Implementation of GASB 63 and GASB 65

As discussed in Note 1 to the financial statements, Sheldon} has adopted the provisions of the Governmental Accounting Standards Board (GASB) Statement No. 63, "Financial Reporting of Deferred Outflow of Resources, Deferred Inflows of Resources and Net Position" and GASB Statement No. 65, "Items Previously Reported as Assets and Liabilities".

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management's discussion and analysis and budgetary comparison information on pages 3-9 and 26-28 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management's responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

'i . (_j~ll;r-?·1./wUvJ ;h?teict-J Li-6

J

Beaufort, South Carolina December 18, 2013

2

Sheldon Township Fire District Management's Discussion and Analysis

As management of Sheldon Township Fire District (Sheldon), we offer readers of Sheldon's financial statements this narrative overview and analysis of the financial activities of Sheldon for the fiscal year ended June 30, 2013.

Financial Highlights

• The assets of Sheldon exceed its liabilities at the close of the most recent fiscal year by $898,154 (net position). Of this amount, $342,362 represents the investment in capital assets less depreciation and debt on those assets. $121,510 is restricted for net position held for debt service, impact fund, and one percent fund . The remaining balance of $434,282 represents the equity in unrestricted net position. Sheldon's total net position increased by $85,362.

• As of the close of the current fiscal year Sheldon's governmental funds reported a combined ending fund balance of $535,738, an increase of $58,018. Approximately 77% of this amount ($414,228) is available for spending at the government's discretion (unassigned fund balance).

Overview of the Financial Statements

This discussion and analysis is intended to serve as an introduction to Sheldon's basic financial statements. Sheldon's basic financial statements comprise three components: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves.

Government-wide financial statements. The government-wide financial statements are designed to provide readers with a broad overview of Sheldon 's finances, in a manner similar to a privatesector business.

The statement of net position presents information on all of Sheldon's assets, liabilities, and deferred inflows/outflows of resources, with the difference reported as net position. Over time, increases and decreases in the net position may serve as a useful indicator of whether the financial position of Sheldon is improving or deteriorating.

The statement of activities presents information showing how Sheldon's net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes are earned but unused vacation leave).

The government-wide financial statements distinguish functions of Sheldon that are supported by general revenues such as taxes and fees. The governmental activities of Sheldon include programs related to public safety for fire protection. Sheldon currently has no business type activities.

The government-wide financial statements can be found on pages 10 through 11 of this report.

3

Fund financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been grouped for specific activities. Sheldon like other public agencies uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the programs of Sheldon can be divided into governmental funds.

Governmental funds. Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating Sheldon's nearterm financing requirements.

Because the focus of governmental funds is narrower than that of the government-wide financial statements, it may be useful to compare the two for similar activities and programs. By doing so, readers may better understand the long-term impact of the government's near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to assist in this comparison of governmental programs and governmental activities.

Sheldon maintains four individual governmental programs. Information is presented by expenditure category in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures and changes in fund balances for the general fund. Data from these programs are combined into a single, aggregated presentation.

Sheldon adopts an annual budget for all funds except the special revenue funds - impact fee fund and the one percent fund. A schedule comparing actual to budgeted revenues and expenditures has been provided to demonstrate compliance with this budget.

The basic governmental fund financial statements can be found on pages 12 through 15 of this report.

Notes to the financial statements. The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found on pages 16 through 25 of this report.

4

Government-wide Financial Analysis

As noted earlier, net position may serve over time as a useful indicator of a public government's financial position. In the case of Sheldon, assets exceeded liabilities by $898,154. Comparative information has been presented for 2012. The following table reflects the condensed governmentwide statement of net position.

SHELDON TOWNSHIP FIRE DISTRICT NET POSITION

Governmental Activities 2013 2012

Current and Other Assets Capital Assets

Total Assets Long-term Liabilities Outstanding

Other Liabilities Total Liabilities

Net Position

Investment in Capital Assets, Net of Related Debt Restricted Unrestricted

Total Net Position

$

$

575,970 810,413

1,386,383 477,550

10,679 488,229

342,362 121 ,510 434,282 898,154

$

$

514,799 848,730

1,363,529 537,584 13,153

550,737

325,534 109,586 377,672 812,792

The largest portion of Sheldon's net position $434,282 (48 percent) reflects its unrestricted net position. Sheldon's investment in capital assets less the related debt on capital assets is $342,362 (38 percent) of net position. These capital assets are not available for future spending. Although Sheldon's investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate theses liabilities. At June 30, 2013, Sheldon had outstanding long-term liabilities of $477,550 for the purchase of fire trucks and annual leave. $121 ,510 (14 percent) was restricted for debt service funds, one percent funds, and impact fees.

unrestricted

restricted

/

Sheldon Net Position June 30, 2013 and 2012

I ;~·~~~:::~:.~: I' +-------~·--·---~---

$0 $100,000 $200,000

I . -·---""1

$300,000 $400,000 $500,000 L -- ----

5

• 2013

• 2012

Governmental activities. Sheldon's total net position increased by $85,362. Key elements of this increase are as shown in the following table.

SHELDON TOWNSHIP FIRE DISTRICT CHANGE IN NET ASSETS

Expenses Public Safety- Fire Protection

Personnel Services Materials and Services Depreciation Interest

Total Expenses Program Revenues

Operating Grants and Contributions Total Program Revenues

General Revenues Taxes Fees Miscellaneous

Total General Revenues

Increase (decrease) in net position Net position - beginning Net position - ending

$

$

Governmental Activities 2013 2012

916,146 154,625 67,403 17,234

1,155,408

29,245 29,245

1,180,432 23,303 7,790

1,211,525

85,362 812,792 898,154

$

$

865,371 144,551 72,051 32,543

1,114,516

1,205,370 20,423 22,381

1,248,174

133,658 679,134 812,792

Revenues were up due to a donation for an all terrain vehicle . Expenses increased due to promotions and cost of living raise. Depreciation expense is down due to assets that have reached full depreciation. Overall revenues and expenses were stable and led to an increase in net position of $85,362.

Expenses- Governmental Activities $1,000,000

$900,000

$800,000

$700,000

$600,000

$500,000

$400,000

$300,000

$200,000

$100,000

$0 i personnel

l services ______ , ___ _ materials

and services depreciation interest

-------------------·

6

• 2013

• 2012

I _ ___ j

f

I $1,400,000

Revenues by Source -Governmental Activities ----------·-------·-··

$1,200,000 ----·--·---------···--------

$1,000,000 ------------- ----

$800,000

$600,000

$400,000

$200,000

$0 . .., J£L --- 1

Financial Analysis of the Government's Funds

• 2013

• 2012

As noted earlier, Sheldon uses fund accounting to ensure and demonstrate compliance with financerelated legal requirements.

Governmental funds. The focus of Sheldon's governmental funds is to provide information on nearterm inflows, outflows, and balances of spendable resources . Such information is useful in assessing Sheldon's financing requirements. In particular, unassigned fund balance may serve as a useful measure of a government's net resources available for discretionary use as they represent the portion of fund balance which has not yet been limited to use for a particular purpose by either an external party, Sheldon itself, or a group or individual that has been delegated authority to assign resources for use for particular purposes by Sheldon ..

At the end of the current fiscal year, Sheldon's governmental funds reported combined ending fund balances of $535,738, an increase of $58,018. Approximately 77.3%of this amount ($414,228) constitutes unassigned fund balance, which is available for spending at the government's discretion. The remainder of the fund balance is restricted for a particular purpose ($121 ,51 0).

The general fund is the chief operating fund of Sheldon. At the end of the current fiscal year, the entire fund balance for the general fund ($414,228) was unassigned.

7

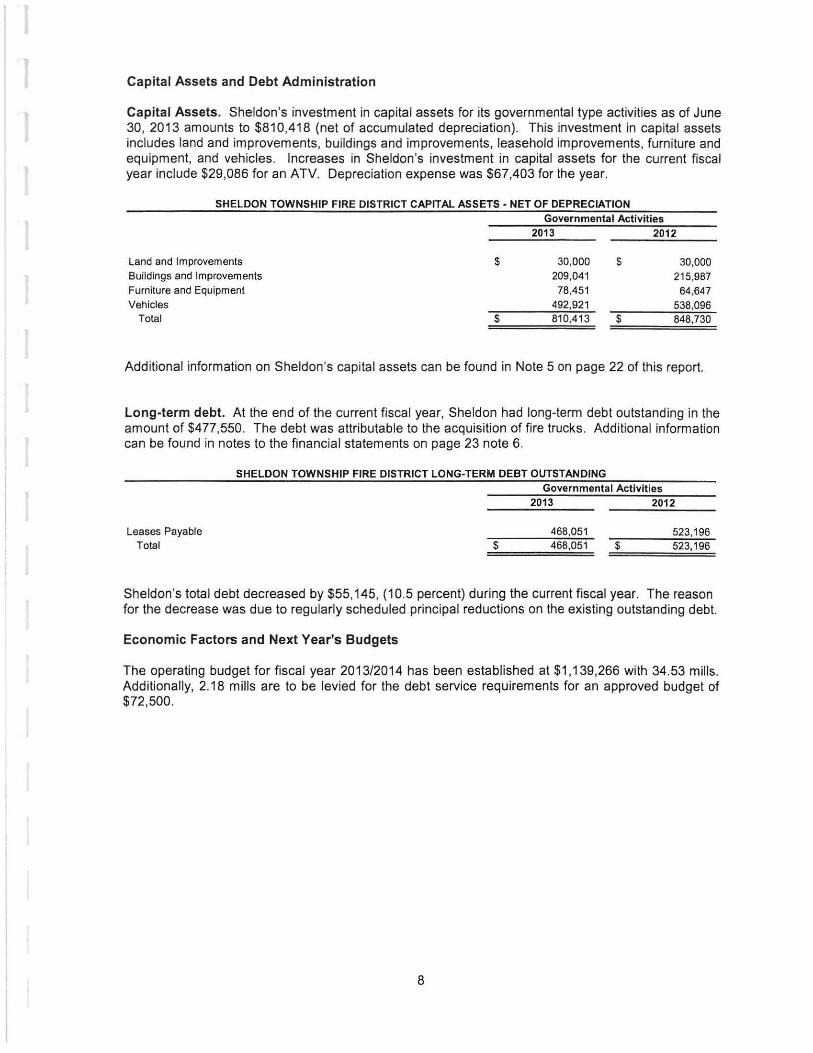

Capital Assets and Debt Administration

Capital Assets. Sheldon's investment in capital assets for its governmental type activities as of June 30, 2013 amounts to $810,418 (net of accumulated depreciation). This investment in capital assets includes land and improvements, buildings and improvements, leasehold improvements, furniture and equipment, and vehicles. Increases in Sheldon's investment in capital assets for the current fiscal year include $29,086 for an ATV. Depreciation expense was $67,403 for the year.

SHELDON TOWNSHIP FIRE DISTRICT CAPITAL ASSETS- NET OF DEPRECIATION

Land and Improvements Buildings and Improvements Furniture and Equipment Vehicles

Total

$

$

Governmental Activities 2013 2012

30,000 209,041

78,451 492,921 810,413

$

$

30,000 215,987

64,647 538,096 848,730

Additional information on Sheldon's capital assets can be found in Note 5 on page 22 of this report.

Long-term debt. At the end of the current fiscal year, Sheldon had long-term debt outstanding in the amount of $477,550. The debt was attributable to the acquisition of fire trucks. Additional information can be found in notes to the financial statements on page 23 note 6.

SHELDON TOWNSHIP FIRE DISTRICT LONG-TERM DEBT OUTSTANDING

Leases Payable Total $

Governmental Activities 2013 2012

468,051 523,196 468,051 $ 523,196

Sheldon's total debt decreased by $55,145, (1 0.5 percent) during the current fiscal year. The reason for the decrease was due to regularly scheduled principal reductions on the existing outstanding debt.

Economic Factors and Next Year's Budgets

The operating budget for fiscal year 2013/2014 has been established at $1,139,266 with 34.53 mills. Additionally, 2.18 mills are to be levied for the debt service requirements for an approved budget of $72,500.

8

Requests for information

This financial report is designed to provide a general overview of Sheldon Township Fire District finances for all those with an interest in the government's finances. Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to the Chief, Sheldon Township Fire District, Post Office Box 129, Sheldon, South Carolina, 29941 .

9

BASIC FINANCIAL STATEMENTS

ASSETS

Cash

Receivables

SHELDON TOWNSHIP FIRE DISTRICT STATEMENT OF NET POSITION

JUNE 30, 2013

Due from Beaufort County Treasurer

Capital Assets. not being depreciated

Capital Assets , being depreciated

Total Assets

LIABILITIES

Interest Payable

Noncurrent Liabilities:

Due within one year

Due in more than one year

Total Liabilities

NET POSITION

Unrestricted

Restricted for Debt Service

Restricted for Impact Fund

Restricted for One Percent Fund

Investment in Capital Assets, Net of Related Debt

Total Net Position

$

$

The notes to the financial statements are an integral part of this statement. 10

210,001

53,515

312,454

30,000

780,413

1,386,383

10,679

56,869

420,681

488,229

434,282

28,780

40,743

51 ,987

342,362 898,154

EXPENSES

Personnel Services

Materials and Supplies

Depreciation

Interest

Total Expenses

PROGRAM REVENUES

Operating Grants and Contributions

Total Program Revenues

GENERAL REVENUES

Taxes

Fees

Miscellaneous

Total General Revenues

Change in Net Position

Net Position, beginning of year

Net Position, end of year

SHELDON TOWNSHIP FIRE DISTRICT STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2013

$

$

The notes to the financial statements are an integral part of this statement. 11

916,146

154,625

67,403

17,234

1 '155,408

29,245

29,245

1 '180,432

23,303

7,790

1,211 ,525

85,362

812,792

898,154

......

"'

ASSETS

Cash $

Receivables

Due from Beaufort County Treasurer

Total Assets $

DEFERRED INFLOWS OF RESOURCES

Unavailable revenue - property taxes $

Total Deferred Inflows of Resources

FUND BALANCES

Unassigned

Restricted

Total Fund Balances

Total Liabilities, Deferred Inflows

of Resources, and Fund Balances $

SHELDON TOWNSHIP FIRE DISTRICT BALANCE SHEET

GOVERNMENTAL FUNDS JUNE 30, 2013

GOVERNMENTAL FUND TYPES

DEBT ONE

GENERAL SERVICE PERCENT

FUND FUND FUND

21 0,001 $ $

50,120 3,395 -191 ,853 27,871 51,987

451 ,974 $ 31,266 $ 51,987

37,746 $ 2,486 $ -37,746 2,486 -

414,228 -- 28.780 51,987

414,228 28 ,780 51 ,987

451 ,974 $ 31,266 $ 51,987

The notes to the financial statements are an integral part of this statement.

IMPACT

FEE

FUND TOTAL

$ $ 210,001

- 53,515

40,743 312,454

$ 40,743 $ 575,970

$ - $ 40,232

40,232

- 414,228

40,743 121,510

40,743 535,738

$ 40,743 $ 575,970

SHELDON TOWNSHIP FIRE DISTRICT RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET

TO THE STATEMENT OF NET POSITION JUNE 30, 2013

Total net position reported for governmental activities in the statement of net

position is different because:

Total fund balances for governmental funds $

Capital assets used in the District's activities are not financial resources

and therefore are not reported in the funds. Those assets consist of:

Land and improvements 30,000

Buildings and improvements, net of $94,476 accumulated depreciation 209,041

Vehicles, net of $435,411 accumulated depreciation 492,921

Furniture and equipment, net of $107,440 accumulated depreciation 78,451

Total Capital Assets

Some receivables will be collected after year-end, but are not

available soon enough to pay for the current period's expenditures, and

therefore are reported as deferred inflows in the funds .

Long-term liabilities applicable to District's activities are not

due and payable in the current period and accordingly are not reported as

fund liabilities. Interest on long-term debt is not accrued in governmental

funds , but rather is recognized as an expenditure when due. All liabilities

--both current and long-term- are reported in the statement of net position.

Balances at June 30, 2013 are:

Interest Payable (10,679)

Annual Leave (9,499)

Notes Payable (468,051)

Total Long-Term Liabilities

Total net position of governmental activities $

The notes to the financial statements are an integral part of this statement. 13

535,738

810,413

40,232

(488,229)

898,154

_. ~

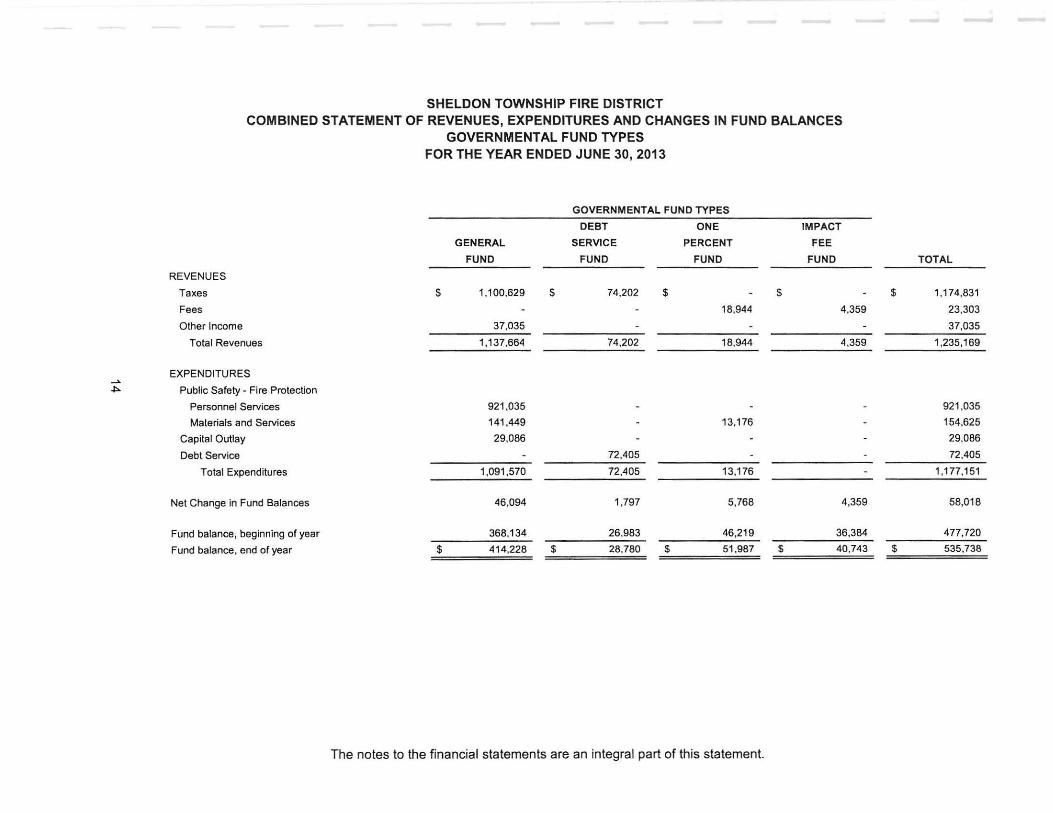

SHELDON TOWNSHIP FIRE DISTRICT COMBINED STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES

GOVERNMENTAL FUND TYPES FOR THE YEAR ENDED JUNE 30, 2013

GOVERNMENTAL FUND TYPES

DEBT ONE IMPACT

GENERAL SERVICE PERCENT FEE

FUND FUND FUND FUND

REVENUES

Taxes $ 1,100,629 $ 74,202 $ $

Fees 18,944 4,359

Other Income 37,035 -Total Revenues 1,137,664 74,202 18,944 4,359

EXPENDITURES

Public Safety- Fire Protection

Personnel Services 921,035 - -Materials and Services 141,449 - 13,176

Capital Outlay 29,086

Debt Service - 72,405

Total Expenditures 1,091 ,570 72,405 13,176 -

Net Change in Fund Balances 46,094 1,797 5 ,768 4,359

Fund balance, beginning of year 368,134 26,983 46,219 36,384

Fund balance, end of year $ 414,228 $ 28,780 $ 51,987 $ 40,743

The notes to the financial statements are an integral part of this statement.

TOTAL

$ 1,174,831

23,303

37,035

1 ,235,169

921 ,035

154,625

29,086

72,405

1,177,151

58,Q18

477,720

$ 535,738

SHELDON TOWNSHIP FIRE DISTRICT RECONCILIATION OF THE STATEMENT OF REVENUES,

EXPENDITURES AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2013

The change in net position reported for governmental activities in the

statement of activities is different because:

Net change in fund balances -- total governmental funds

Governmental funds report capital outlays as expenditures. However, in the

statement of activities the cost of those assets is allocated over their

estimated useful lives and reported as depreciation expense. This is the

amount by which capital outlays ($29,086) was less than depreciation

($67,403) in the current period.

Repayment of principal is an expenditure in the governmental funds but

reduces the liability in the statement of net position.

Revenues in the statement of activities that do not provide current financial

resources are not reported as revenues in the funds .

Some expenses reported in the statement of activities do not require the use of

current financial resources and, therefore, are not reported as expenditures in

governmental funds.

Annual leave

Interest Payable

Total change in net position of governmental activities

$

$

The notes to the financial statements are an integral part of this statement. 15

58,018

(38,317)

55,145

5,601

4,889

26

85,362

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Description of Government-Wide Financial Statements

The government-wide financial statements (i.e., the statement of net position and the statement of activities) report information on all of the nonfiduciary activities of the primary government. All fiduciary activities are reported only in the fund financial statements. Governmental activities, which normally are supported by taxes, intergovernmental revenues, and other nonexchange transactions, are reported separately from business-type activities, which rely to a significant extent on fees and charges to external customers for support. Likewise, primary government is reported separately from certain legally separate component units for which the primary government is financially accountable.

Reporting Entity

Sheldon Township Fire District (Sheldon) was established on August 24, 1977 for the purpose of providing fire protection for the residents of Sheldon Township in Beaufort County, South Carolina.

Sheldon is a special purpose tax district whose appointed board controls its operations and fiscal accountability. Sheldon is a separate reporting entity and is not a component unit of any other governmental entity. Beaufort County is a related party in that the Beaufort County Council has final approval of budget, assesses millage, collects taxes and prepares payroll for Sheldon.

The accompanying financial statements present the combined financial positions and combined results of operations of the various fund types controlled by Sheldon. Blended component units are, in substance, part of the primary government's operations, even though they are legally separate entities. Thus, blended component units are appropriately presented as funds of the primary government. Each discretely presented component unit is reported in a separate column in the government-wide financial statements to emphasize that it is legally separate from the government. Sheldon is not reporting any component units as described above.

Basis of Presentation -Government-Wide Financial Statements

While separate government-wide and fund financial statements are presented, they are interrelated. The governmental activities column incorporates data from governmental funds and internal service funds, while business-type activities incorporate data from the government's enterprise funds. Separate financial statements are provided for governmental funds, proprietary funds, and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Sheldon reports only governmental activities, as there are no business-type activities or component units.

The statement of activities demonstrates the degree to which the direct expenses of a given function or segment is offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function or segment. Program revenues include 1) charges to customers or applicants who purchase, use, or directly benefit from goods, services, or privileges provided by a given function or segment and 2} grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment. Taxes and other items not properly included among program revenues are reported instead as general revenues.

As a general rule, the effect of interfund activity has been eliminated from the government-wide financial statements.

16

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES -CONTINUED

Basis of Presentation- Fund Financial Statements

The fund financial statements provide information about Sheldon's funds . The emphasis of fund financial statements is on major governmental funds, each displayed in a separate column. All remaining governmental funds are aggregated and reported in a separate column. Major individual governmental funds are reported as separate columns in the fund financial statements.

Sheldon reports the following major governmental funds :

The general fund is Sheldon's primary operating fund . It accounts for all financial resources of the general government, except those required to be accounted for in another fund .

The debt service fund represents Sheldon's collection and payment of the general obligation bond. It accounts for all financial resources that are restricted for debt payment.

The impact fund represents Sheldon's collection of impact fees from developers within that area. It accounts for all financial resources that are restricted for capital assets.

The 1% fee fund contains funds collected from insurance companies and made available to Sheldon for certain specific purposes. Those purposes include retirement and insurance, training and education, and recruitment and retention .

During the course of operations, Sheldon has activity between funds for various purposes. Any residual balances outstanding at year end are reported as due from/to other funds and advances to/from other funds. While these balances are reported in fund financial statements, certain eliminations are made in the preparation of the government-wide financial statements. Balances between funds included in governmental activities (i.e., governmental funds) are eliminated so that only the net amount is included as internal balances in the governmental activities column.

Further, certain activity occurs during the year involving transfers of resources between funds . In fund financial statements these amounts are reported at gross amounts as transfers in/out. While reported in the fund financial statements, certain eliminations are made in the preparation of the government-wide financial statements. Transfers between the funds included in governmental activities are eliminated so that only the net amount is included as transfers in the governmental activities column.

Measurement Focus, Basis of Accounting, and Financial Statement Presentation

The accounting and financial reporting treatment is determined by the applicable measurement focus and basis of accounting. Measurement focus indicates the type of resources being measured such as current financial resources or economic resources. The basis of accounting indicates the timing of transactions or events for recognition in the financial statements.

The government-wide financial statements are presented using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met.

Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, Sheldon considers revenues to be available if they are collected within 60 days of the end of the current fiscal period.

17

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES -CONTINUED

Measurement Focus, Basis of Accounting, and Financial Statement Presentation - Continued

Expenditures generally are recorded when a liability is incurred, as under accrual accounting. However, debt service expenditures, as well as expenditures related to compensated absences and claims and judgments, are recorded only when payment is due. General capital asset acquisitions are reported as expenditures in governmental funds. Issuance of long-term debt and acquisitions under capital leases are reported as other financing sources.

Operating grants and contributions and client fees associated with the current fiscal period are all considered to be susceptible to accrual and so have been recognized as revenues of the current fiscal period. All other revenue items are considered to be measurable and available only when the cash is received by Sheldon.

Budgetary Information

Annual budgets are adopted on a basis consistent with generally accepted accounting principles for all governmental funds . An annual budget for the special revenue fund is not adopted as sufficient budgetary control is achieved through restrictions included in the various grant agreements. An annual operating budget for the capital projects fund is not adopted as its revenues and expenditures are adopted on a project basis . All annual appropriations lapse at fiscal year-end.

The appropriated budget is prepared by fund. Sheldon may make transfers of appropriations within a department. Supplemental appropriations require the approval of County Council. The legal level of budgetary control (i.e. , the level at which expenditures may not legally exceed appropriations) is the fund level. There were no supplemental budgetary appropriations approved during the year.

Appropriations in all budgeted funds lapse at the end of the fiscal year even if they have related encumbrances. Encumbrances are commitments related to unperformed (executor) contracts for good and services (i.e., purchase order, contracts, and commitments). Encumbrance accounting is utilized to the extent necessary to assure effective budgetary control and accountability and to facilitate effective cash planning and control. While all appropriations and encumbrances lapse at year end, valid outstanding encumbrances (those for which performance under executor contract is expected in the next year) are re-appropriated and become part of the subsequent year's budget pursuant to state regulations.

Assets, Liabilities, Deferred Outflows/Inflows of Resources, and Net Position/Fund Balances

Cash and Cash Equivalents

Sheldon's cash and cash equivalents are considered to be cash on hand, demand deposits, and short-term investments with original maturities of three months or less from the date of acquisition.

Sheldon is authorized by state statute to invest in the following:

Obligations of the United States and its agencies; General obligations of the State of South Carolina and its political units; Savings and loan associations to the extent that the same are insured by an agency of the Federal

Government; certificates of deposit where the certificates are collaterally secured by securities of the type described above and are held by a third party as escrow agent or custodian , at a market value not less than the amounts of the certificates of deposit plus interest; provided, however, such collateral shall not be required to the extent the same are insured by an agency of the federal government.

18

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES- CONTINUED

Assets, Liabilities, Deferred Outflows/Inflows of Resources, and Net Position/Fund Balances -Continued

Inventories and Prepaid Items - Continued

Inventories of the general fund consist of supplies held for consumption and are immaterial to the financial statements and accordingly are not recorded .

Certain payments to vendors reflect costs applicable to future accounting periods and are recorded as prepaid items in both government-wide and fund financial statements.

Capital Assets

Capital assets, which include buildings, equipment, and vehicles, are reported in the unrestricted net position on the statement of financial position. Capital assets are defined by Sheldon as property and equipment with an initial, individual cost of more than $5,000 and an estimated useful life in excess of two years. Such assets are recorded at historical cost or estimated historical cost if purchased or constructed.

The cost of normal maintenance and repairs that do not add to the value of the assets or materially extend assets lives are not capitalized .

Major outlays for capital assets and improvements are capitalized as projects are constructed. Property and equipment is depreciated using the straight-line method over the following estimated useful lives:

Assets Buildings Vehicles and Equipment

Deferred Outflows/Inflows of Resources

Years 50 years

5-10 years

In addition to assets, the statement of financial position will sometimes report a separate section for deferred outflows of resources. This separate financial statement element, deferred outflows of resources, represents a consumption of net position that applies to a future period(s) and so will not be recognized as an outflow of resources (expenses/expenditures) until then. Sheldon did not have any items that qualify for reporting in this category.

In addition to liabilities, the statement of financial position will sometimes report a separate section for deferred inflows of resources. This separate financial statement element, deferred inflows of resources, represents a consumption of net position that applies to a future period(s) and so will not be recognized as an inflow of resources (expenses/expenditures) until that time. Sheldon has only one type of item, which arises only under a modified accrual basis of accounting that qualifies for reporting in this category. Accordingly, the item, unavailable revenue , is reported only in the governmental funds balance sheet. The governmental funds report unavailable revenues from property taxes. These amounts are deferred and recognized as an inflow of resources in the period that the amounts become available.

19

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30,2013

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES -CONTINUED

Assets, Liabilities, Deferred Outflows/Inflows of Resources, and Net Position/Fund Balances -Continued

Net Position Flow Assumptions

Sometimes Sheldon will fund outlays for a particular purposes from both restricted (e.g., restricted bond or grant proceeds) and unrestricted resources. In order to calculate the amounts to report as restricted- net position and unrestricted- net position in the government-wide, a flow assumption must be made about the order in which the resources are considered to be applied. It is Sheldon's policy to consider restricted- net position to have been depleted before unrestricted- net position is applied.

Fund Balance Policies

Fund balance of governmental funds is reported in various categories based on the nature of any limitation requiring the use of resources for specific resources . Sheldon itself can establish limitations on the use of resources through either a commitment (committed fund balance) or an assignment (assigned fund balance).

The committed fund balance classification includes amounts that can be used only for the specific purposes determined by a formal action of Sheldon's highest level of decision-making authority. The Board of Commissioners is the highest level of decision-making authority for Sheldon that can, by vote prior to the end of the fiscal year, commit fund balance. Once adopted, the limitation imposed by the ordinance remains in place until a similar action is taken (the adoption of another policy) to remove or revise the limitation.

Amounts in the assigned fund balance classification are intended to be used by Sheldon for specific purposes but do not meet the criteria to be classified as committed. Sheldon may assign fund balance as deemed necessary. Unlike commitments, assignments generally only exist temporarily. In other words, an additional action does not normally have to be taken for the removal of an assignment. Conversely, as discussed above, an additional action is essential to either remove or revise a commitment.

Revenues and Expenses/Expenditures

Program Revenues

Amounts reported as program revenues include 1) charges to customers or applicants who purchase, use, or directly benefit from goods, services, or privileges provided by a given function or segment and 2) grants and contributions (including special assessments) that are restricted to meeting the operational or capital requirements of a particular function or segment. All taxes, including those dedicated for specific purposes, and other internally dedicated resources are reported as general revenues rather than as program revenues.

Property taxes

The County Ordinance provides for the taxation of all real and personal property located within Sheldon limits on the first day of January. Motor vehicle taxes are billed and collected by the County Treasurer on a monthly basis. Other personal and real property taxes are levied by the County after September of each year and become due and payable immediately upon receipt by the taxpayer. Real property taxes are delinquent after January 15th. Assessed property is subject to lien one year from the levy date if taxes remain unpaid. The property tax rate approved by ordinance for fiscal year 2013 is 33.07 mills.

20

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES- CONTINUED

Revenues and Expenses/Expenditures -Continued

Compensated Absences

Unused vacation leave liabilities are reported as incurred in the applicable governmental type activities columns in the government-wide financial statements. Sheldon employees can accumulate annual leave for a maximum of 144 hours for vacation leave and 72 hours for sick leave. Any amounts accrued in excess of the maximum limits are not carried forward. With sufficient notification of employment termination, unused vacation leave will be paid up to the maximum accrued hours of 144. Sheldon has no financial liability for its sick leave. Therefore, a liability of $9,499 has been recorded to reflect the accrued vacation leave liability for each eligible employee and includes 19.01 percent for related payroll costs for taxes and retirement. Compensated absences are paid from the general fund.

Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions. These estimates affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and revenues and expenditures/expenses during the reporting period. Actual results could differ from those estimates.

NOTE 2 DEPOSITS AND INVESTMENTS

South Carolina statutes provide for investment of governmental funds into certain authorized investment types including U.S. Treasury bills, other short-term U.S. and South Carolina government obligations, insured or collateralized time deposits, and certificates of deposit. The statutes do not prescribe regulations related to demand deposits but do allow the pooling of governmental funds for investment purposes.

Deposits of the governmental funds are maintained in demand deposits or savings accounts, or certificates of deposits. The bank balance at June 30, 2013 was $227,900 while the book balance was $210,001. The bank balance was insured by the FDIC.

Custodial credit risk is the risk that in the event of a bank failure, Sheldon's deposits may not be returned to it. Sheldon does not have a deposit policy for custodial credit risk.

NOTE 3 ACCOUNTS RECEIVABLE

Accounts receivable at June 30, 2013 were as follows:

Taxes Receivable Allowance for Doubtful Accounts

Total Accounts Receivable

Fund Statements

$ 54,955 (1 ,440)

$ 53,515

21

Government-wide Statements

$ 54,955 (1 ,440)

$ 53,515

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 3 ACCOUNTS RECEIVABLE- CONTINUED

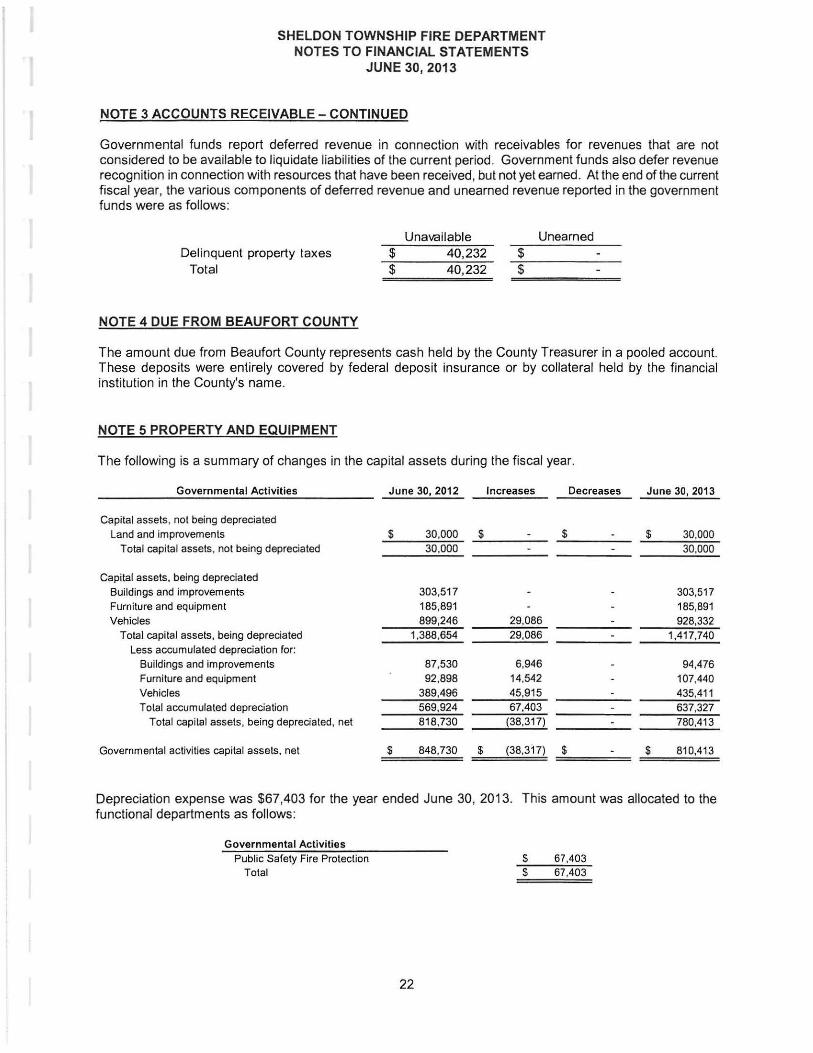

Governmental funds report deferred revenue in connection with receivables for revenues that are not considered to be available to liquidate liabilities of the current period. Government funds also defer revenue recognition in connection with resources that have been received, but not yet earned. At the end of the current fiscal year, the various components of deferred revenue and unearned revenue reported in the government funds were as follows:

Delinquent property taxes Total

NOTE 4 DUE FROM BEAUFORT COUNTY

Unavailable $ 40,232 $ 40,232

Unearned $ $

The amount due from Beaufort County represents cash held by the County Treasurer in a pooled account. These deposits were entirely covered by federal deposit insurance or by collateral held by the financial institution in the County's name.

NOTE 5 PROPERTY AND EQUIPMENT

The following is a summary of changes in the capital assets during the fiscal year.

Governmental Activities June 30, 2012 Increases Decreases June 30, 2013

Capital assets, not being depreciated Land and improvements $ 30,000 $ $ $ 30,000

Total capital assets, not being depreciated 30,000 30,000

Capital assets, being depreciated Buildings and improvements 303,517 303,517 Furniture and equipment 185,891 185,891 Vehicles 899,246 29,086 928,332

Total capital assets, being depreciated 1,388,654 29,086 1,417,740 Less accumulated depreciation For:

Buildings and improvements 87,530 6,946 94,476 Furniture and equipment 92,898 14,542 107,440 Vehicles 389,496 45,915 435,411 Total accumulated depreciation 569,924 67,403 637,327

Total capital assets, being depreciated, net 818,730 (38,317) 780,413

Governmental activities capital assets, net $ 848,730 $ (38,317) $ $ 810,413

Depreciation expense was $67,403 for the year ended June 30, 2013. This amount was allocated to the functional departments as follows :

Governmental Activities Public Safety Fire Protection

Total

22

$ 67,403 $ 67,403

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30,2013

NOTE 6 LONG TERM OBLIGATIONS

Changes in long term obligations were as follows :

Balance Balance June 30, 2012 Additions Retirements June 30, 2013

Leases payable $ 523,196 $ $ 55,145 $ Annual leave 14,388 4,889

Total $ 537,584 $ $ 60,034 $

Interest paid for the year ended June 30, 2013, was $17,260.

Leases payable at June 30, 2013 consisted of the following :

$534,237 Lease payable to BB&T due in ten annual installments of $61 ,934 in October and continuing through and including fiscal year 2021 . Payments include interest at 3.29%. Collateralized by fire trucks.

$56,000 Lease payable to BB& T due in six annual installments of $10,471 in May and continuing through and including fiscal year 2017. Payments include interest at 3.39%. Collateralized by a fire truck.

Total

Five-Year Debt Requirements

468,051 9,499

477,550

Balance

$

$

Due within One Year

$ 56,869

$ 56,869

429,488

38,563

468,051

Sheldon has entered into a lease purchase agreement to purchase a fire truck and equipment with a lease term of twelve years. The following is a schedule of future minimum lease payments under capital leases, together with the present value of net minimum lease payments at June 30, 2013.

Year Ended June 30, 2014 2015 2016 2017 2018

2019-2022 Total Minimum Lease Payments

Less Amount Representing Interest Net Present Value of Minimum Lease Payments

Amount $ 72,277

72,277 72,277 72,277 61 ,806

186,304 537,218 (69,167)

$ 468,051

The following is an analysis of property under capital leases included in property and equipment at June 30, 2013:

Fire trucks and equipment Accumulated depreciation

Net value of leased property

23

$ 877,839 (414 ,004)

$ 463,835

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 6 LONG TERM OBLIGATIONS- CONTINUED

Compensated Absences

Regular employees who are separated from Sheldon service will be paid for all accrued unused annual leave hours. Sheldon has no financial liability for its unused sick leave.

The accumulated unpaid annual leave earned, but not taken, by Sheldon employees as of June 30, 2013 totaled $9,499 computed at each employee's pay rate and includes an estimate of eighteen percent for benefits payable that are related to the annual leave pay. Unused annual leave liabilities are reported in the applicable governmental type activities columns in the government-wide financial statements. All annual leave is paid from the general fund.

Operating Leases

Sheldon has immaterial operating leases on office equipment that are short-term in length.

Debt Limitation

Sheldon's general obligation debt is limited by law to eight percent of the total assessed value of all taxable real and personal property of Sheldon. The latest assessed value for 2012 was $34,205,730.

The computation of legal debt limits is as follows :

Assessed value ($34,205,730 X 8%) General obligation debt at June 30, 2013 Excess of debt limit over general obligation debt

NOTE 7 PENSION PLAN OBLIGATIONS

$ 2,736,458

$ 2,736,458

All eligible employees are required to participate in a pension plan. All eligible employees must belong to the South Carolina Retirement System (SCRS). The plan is a cost-sharing multiple-employer administered by the Retirement Division of the SC Public Employee Benefit Authority (SC PEBA). Retirement costs are funded by withholding from the employee's salaries, and by a contribution from the employers of a percentage of the employee's salaries. A Comprehensive Annual Financial Report containing financial statements and required supplementary information for the South Carolina Retirement System and Police Officers Retirement System is issued and publicly available by writing the SC PEBA, Post Office Box 11960, Columbia, South Carolina 29211-1960.

Funding Policy

South Carolina Retirement System (SCRS) Sheldon is required to contribute 10.60 percent which includes 0.15 percent towards group life insurance. Sheldon's contributions for the years ending June 30,2013,2012, and 2011 were $4,437, $3,982, and $3,947, respectively, and were equal to the required contributions for each year.

Police Officers Retirement System (PORS) Sheldon is required to contribute 12.30 percent which includes 0.40 percent towards group life insurance and survivor and disability benefits. Sheldon's contributions for the years ending June 30, 2013, 2012, and 2011 were $73,267, $68,357, and $72,639, respectively, for SCPORS members and were equal to the required contributions for each year.

24

SHELDON TOWNSHIP FIRE DEPARTMENT NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2013

NOTE 8 RISK MANAGEMENT

Sheldon purchases insurance policies divided into coverage of workers' compensation, property and casualty, and employee health insurance from the insurance carrier. Management believes such coverage is sufficient to preclude any significant uninsured losses for the covered risks. The insurers promise to pay to or on behalf of the insured for covered economic losses sustained during the policy in accordance with insurance policy and benefit program limits. Sheldon has recorded insurance premium expenditures in the applicable functional expenditure categories of the general fund . These expenditures do not include estimated claim losses and estimable premium adjustments. There have not been any significant reductions in insurance coverage from the prior year.

NOTE 9 COMMITMENTS AND CONTINGENCIES

In the normal course of business, Sheldon can be subject to various claims for workers compensation and other accidents. It is the opinion of Sheldon that resolution of these matters will not have a materially adverse effect on the financial condition of Sheldon.

25

REQUIRED

SUPPLEMENTARY

INFORMATION

SHELDON TOWNSHIP FIRE DISTRICT STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES

BUDGET AND ACTUAL FOR THE YEAR ENDED JUNE 30,2013

GENERAL FUND

VARIANCE

ORIGINAL FINAL FAVORABLE

BUDGET BUDGET ACTUAL (UNFAVORABLE)

REVENUES

Taxes $ 1,099,070 $ 1,099,070 $ 1,100,629 $ 1,559 Other Income 37,035 37,035

Total Revenues 1,099,070 1,099,070 1,137,664 38,594

EXPENDITURES

Current

Public Safety- Fire Protection

Personnel Services

Personnel salaries 697,698 697,698 668,024 29,674 Overtime 16,000 16,000 11 ,427 4,573 Volunteer Per Diem 1,500 1,500 1,475 25 FICNMedicare 54,598 54,598 52,007 2,591 Retirement 87,038 87,038 82,376 4,662

Health insurance 62,877 62,877 60,557 2,320 Unemployment 2,789 2,789 2,392 397 Workman's Compensation 47,100 47,100 42,777 4,323

Total Personnel Services 969,600 969,600 921,035 48,565

Materials and Services

Audit 5,300 5,300 5,250 50 Physicals 9,000 9,000 7,221 1,779 Utilities 14,000 14,000 11 ,631 2,369

Grounds Maintenance 800 800 284 516 Custodial 1,200 1 ,200 1,268 (68)

Buildings repairs and maintenance 7,000 7,000 7,754 {754) Insurance 6,620 6,620 3,024 3,596

Equipment repairs and maintenance 6,500 6,500 8,337 {1,837)

Equipment and Vehicle Insurance 11 ,000 11,000 8,571 2,429

Membership and Subscriptions 850 850 594 256 Office Supplies 1,000 1,000 963 37 Postage 400 400 533 (133)

Printing 1,600 1,600 1,949 (349) Telephone 3,200 3,200 3,359 (159) Training 2,500 2,500 2,146 354 Uniform 5,000 5,000 4,641 359 Fuel 22,000 22,000 23,626 (1 ,626)

Vehicle repairs and maintenance 20,000 20,000 30,586 (10,586)

Fire Prevention 2,000 2,000 1,074 926 Equipment 14 ,627 (14 ,627} Miscellaneous 2,500 2,500 4,011 (1,511}

Total Materials and Services $ 122,470 $ 122,470 $ 141,449 $ (18,979}

See accompanying auditors' report. 26

SHELDON TOWNSHIP FIRE DISTRICT STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES

BUDGET AND ACTUAL

Capital Outlay

Capital Outlay

Total Capital Outlay

Total Expenditures

Net changes in fund balances

Fund balance, beginning of year

Fund balance, end of year

FOR THE YEAR ENDED JUNE 30,2013

GENERAL FUND

ORIGINAL FINAL

BUDGET BUDGET

$ 7,000 $ 7,000

7,000 7,000

1,099,070 1,099,070

368,134 368,134

$ 368,134 $ 368,134

See accompanying auditors' report. 27

ACTUAL

$ 29,086

29,086

1,091,570

46,094

368,134

$ 414,228

VARIANCE

FAVORABLE

(UNFAVORABLE)

$ (22,086)

(22,086)

7,500

46,094

$ 46,094

SHELDON TOWNSHIP FIRE DISTRICT STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES

REVENUES

Taxes

Total Revenues

EXPENDITURES

Debt Service

Total Expenditures

Net change in fund balance

Fund balance, beginning of year

Fund balance, end of year

BUDGET AND ACTUAL FOR THE YEAR ENDED JUNE 30,2013

DEBT SERVICE FUND

ORIGINAL FINAL

BUDGET BUDGET ACTUAL

$ 72,500 $ 72,500 $ 72,500 72,500

72,500 72,500

72,500 72,500

26,983 26,983

$ 26,983 $ 26,983 $

See accompanying auditors' report. 28

74,202

74,202

72,405

72,405

1,797

26,983

28,780

VARIANCE

FAVORABLE

(UNFAVORABLE)

$ 1,702

1,702

95

95

1,797

$ 1,797