shawn osell department of business and economics university of wisconsin – superior...

TRANSCRIPT

1

Shawn OsellDepartment of Business and Economics

University of Wisconsin – [email protected]

Interest on Reserves: A Fourth Tool of Monetary Policy

2

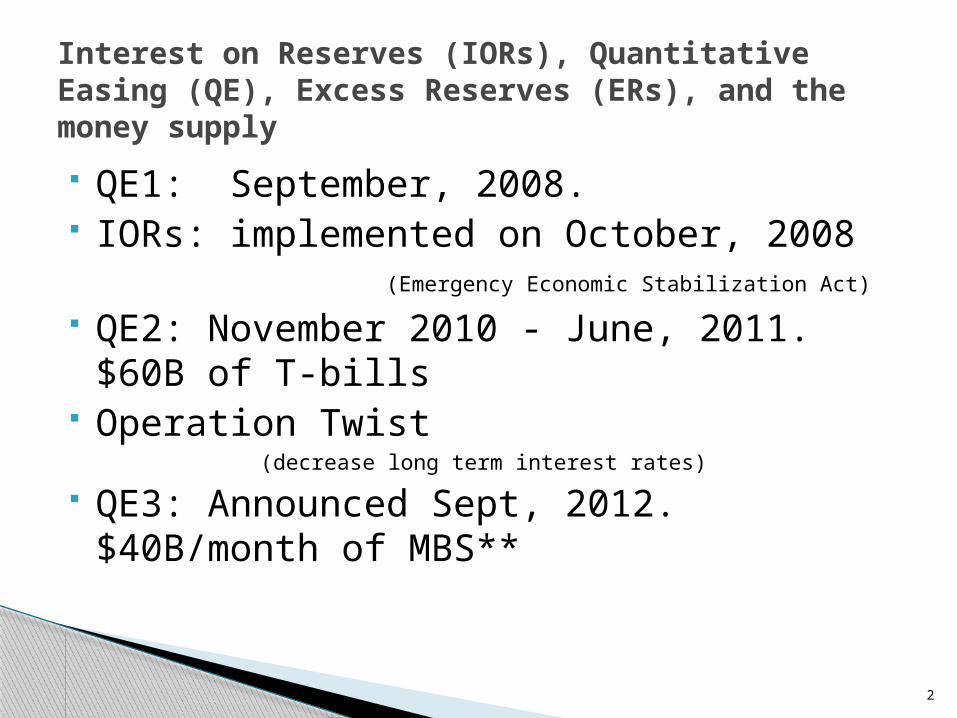

QE1: September, 2008. IORs: implemented on October, 2008

(Emergency Economic Stabilization Act)

QE2: November 2010 - June, 2011. $60B of T-bills

Operation Twist (decrease long term interest rates)

QE3: Announced Sept, 2012. $40B/month of MBS**

Interest on Reserves (IORs), Quantitative Easing (QE), Excess Reserves (ERs), and the money supply

3

M2; 1960 – 2012http://research.stlouisfed.org/

4

M2; 2006 – 2012

5

What is the money multiplier? (m) The maximum change in the money supply due to

an initial change in the excess reserves banks hold

What is the money multiplier equal to? m = 1 / required reserve ratio ≡ 1/r

i.e. 1/10% = 1/(1/10) = 10 M1 =initial ER x m

i.e. $90 X 10 = $900.

Where does money come from? -- What we learn about the money multiplier and money supply creation

6

Bank TR (Deposits) RR ER loans (or bonds)

M1 CumulativeΔM1

A $100 from O.M.O. $0 $100 $100 $0

B $100 $10 $90 $100 $0

C 90 9 81 190 90

D 81 8.10 72.9 271 171

E 72.9 7.29 65.61 343.9 243.9

F 65.61 ⁞ ⁞ ⁞ ⁞

Total: $1,000 $900

Money Creation via the Banking System -

A Lecture from a macroeconomics course

7

Can the multiplier be smaller than indicated?

The simple money multiplier assumes that:

1.* banks want to lend out all of their ER’s

2. borrowers’ want to borrow all of a bank’s ER’s

3. All loans are deposited back into the banking system.

Three Caveats regarding the money multiplier

8

Reserve Market and IOR Theory

9

0.5

11.

52

2.5

inte

rest

rate

jan2008 jan2009 jan2010 jan2011 jan20122008 - 2012

Interest rate on ERsEffective Federal Funds Rate

Effective Fed Funds Rate and Interest on Reserves

Interest on Required Reserves

Interest on Excess Reserves

Effective Federal Reserve Rate

Target Federal Funds Rate

Date Value 2008-10-22 1.40

2008-11-05 1.11

2008-11-19 1.00

2008-12-03 1.00

2008-12-17 0.89

2008-12-31 0.252009-01-14 0.25

To present 0.25

Date Value2008-10-15 0.752008-10-22 0.752008-10-29 0.652008-11-05 0.652008-11-12 1.002008-11-19 1.002008-11-26 1.002008-12-03 1.002008-12-10 1.002008-12-17 0.252008-12-24 0.25

0.25

Date Value2008-10-01 0.97

2008-11-01 0.39

2008-12-01 0.16

2009-01-01 0.15

.07 - .20

Date 12/16/2008

0 - .25

Federal Funds Rate and Interest on Reserves

10

05

10

15

20

Bill

ion

s o

f D

olla

rs

jan1960 jan1970 jan1980 jan1990 jan2000 jan2010January 1960 -April 2008

Excess Reserves

Excess Reserves (Bil.)1960-2008

11

05

00

1000

1500

Bill

ion

s o

f D

olla

rs

jan1960 jan1970 jan1980 jan1990 jan2000 jan20101960 - 2012

Excess Reserves

01

000

2000

3000

perc

en

t cha

nge

jan1960 jan1970 jan1980 jan1990 jan2000 jan20101960 - 2012

percent change Excess Reserves

Excess Reserves; 1960 - 2012

12

050

010

00

15

00

Bill

ion

s of

Dolla

rs

jan2008 jan2009 jan2010 jan2011 jan20122008 - 2012

Excess Reserves

Excess Reserves; 2008 - Present

13

Consequences of too much easy credit during the 2000s

Current economy Europe Future uncertainty i.e. presidential

election. Low interest rates are not profitable for

lenders – no incentive to lend. How much impact do/can IORs have? *** The opportunity cost of lending or buying liquid assets has

decreased.

Why are banks not lending their Excess Reserves?

14

0.2

.4.6

.81

Inte

rest ra

te o

n E

Rs

050

010

00

15

00

Excess R

eserv

es in B

illio

ns o

f $

jan2008 jan2009 jan2010 jan2011 jan2012month, year

Excess Reserves of Depository Institutions

Interest rate on ERs

Source: St. Louis FRB

ERs are in Billions of dollarsExcess Reserves amount and interest rate paid

Is there a relationship between Excess Reserves and interest on reserves? Causation vs. Correlation

15

0

.2

.4

.6

.8

1

ER

an

d R

R a

s p

erc

ent

of T

R

jan1960 jan1970 jan1980 jan1990 jan2000 jan20101960 - 2008

ER as percent ot TR RR as percent ot TR

ERs and RRs as a percent of TRs

0

.2

.4

.6

.8

1

ER

an

d R

R a

s p

erc

ent

of T

R

jan2008 jan2009 jan2010 jan2011 jan20122008 - 2012

ER as percent ot TR RR as percent ot TR

Excess reserves and Required Reserves as a Percentage of Total Reserves

16

Excess Reserve ratio = e = ER/D; where D = Checkable Deposits. Public can & does hold currency which slows the money creation

process.

Public preference for currency is measured by Currency ratio = c = C/D Currency has become a larger part of M1 than checkable deposits C > D.

Where is all the currency?: i.e. Overseas, Drug Trade.

m = 1 + c r + e + c

Include the Currency Ratio and Excess Reserve Ratio into the Money Multiplier

17

Now, how well can the Fed control the money supply, M1? MB X m = M1 (MBn + DL) X 1 + c = M1 r + e + c The Federal Reserve controls: MBn, r = req. reserve ratio

Financial Intermediaries control: e = ER ratio, and DLs = (note: Discount Loans are a right),

The public controls: c = Currency Ratio.

Money Creation with More Players

18

MB * m = M1 m = M1/MB0

1000

2000

3000

Billions o

f dollars

jan1960 jan1970 jan1980 jan1990 jan2000 jan2010years 1960 - 2012

M1 Money Stock

Monetary Base

M1 money supply and the monetary base

01

23

4

M1 m

m

jan1960 jan1970 jan1980 jan1990 jan2000 jan2010years 1960 - 2012

M1 money multiplier

0500

1000

1500

Billions o

f dollars

jan1960 jan1970 jan1980 jan1990 jan2000 jan2010years 1960 - 2008

M1 Money Stock

Monetary Base

M1 money supply and the monetary base

1000

1500

2000

2500

3000

Billions o

f dollars

jan2008 jan2009 jan2010 jan2011 jan2012years 2008 - 2012

M1 Money Stock

Monetary Base

M1 money supply and the monetary base

19

01

23

e/DD

and

c/D

D

jan1960 jan1970 jan1980 jan1990 jan2000 jan2010years 1960 - 2012

Excess Reserve ratio

Currency Ratio

Currency and ER ratios

01

23

e/DD

and

c/D

D

jan2008 jan2009 jan2010 jan2011 jan2012years 2008 - 2012

Excess Reserve ratio Currency Ratio

Currency and ER ratios

Variable Obs. Mean Std. Dev. Min Max

Jan. 1960 – Aug. 2008

ER (Bil.) 584 .8232414 .9451131 .12 19.015

ER ratio 584 .0030797 .0025858 .000558 .0511982

Sept. 2008 – May, 2012

ER (Bil.) 45 1,091.961 368.0216 59.482 1,618.129

ER ratio 45 2.034559 .470678 .1650902 19

Currency ratio and excess ratioa comparison before and after QE1

20

-500

0500

1000

1500

Bill

ions

of D

olla

rs

jan1960 jan1970 jan1980 jan1990 jan2000 jan2010Month, Year

Non-borrowed Reserves of Depository InstitutionsBorrowed Reserves of Depository Institutions

of Depository Institutions Borrowed and Non-Borrowed Reserves

-500

0500

1000

1500

Bill

ions

of D

olla

rs

jan2008 jan2009 jan2010 jan2011 jan20122008 - 2012

Non-borrowed Reserves of Depository InstitutionsBorrowed Reserves of Depository Institutions

of Depository Institutions Borrowed and Non-Borrowed Reserves

Supply of reserves:Borrowed and Non-Borrowed reserves

21

Banking and Excess reservesBank Loans and ER ratio after QE1

Regression on loans after QE1

01

23

ER

/Dep

osi

t rat

io

6600

6800

7000

7200

7400

Tot

al L

oans

in B

illio

ns o

f $

jul2008 jul2009 jul2010 jul2011 jul2012month, year

Total Loans and Leases of Commercial Banks

ER/Deposit ratio

Source: BoG and St. Louis FRB

Loans are in Billions of dollarsTotal Loans and Leases of Banks and ER ratio Coef. t

Constant 7625.366* 41.8*

ER ratio - 294.78* - 6.66*

C ratio - 83.57 - 1.09

Adj.-R = .49

22

IORs benefit Financial Intermediaries by lowering the opportunity cost of holding Excess Reserves and the Implicit tax on Required Reserves

Effective/additional Monetary Policy tool Disincentive for lending Loss of funds for US Treasury Can/will be used to moderate future

inflation

Concluding statements