seven mile generating station … mile generating station installation of the fourth generating unit...

TRANSCRIPT

SEVEN MILE GENERATING STATION INSTALLATION OF THE FOURTH GENERATING UNIT

EXECUTIVE SUMMARY

Background and Overview

The Seven Mile hydroelectric generation station is located on the Pend dlOreille River in southeastern British Columbia near Trail, 18 km downstream of Seattle City Light's Boundary Project and 9 km upstream of Cominco's Waneta Project. The Seven Mile Dam and Power plant came into service in 1979 and consist of a concrete gravity dam, a spillway, and a 4-bay powerhouse. Three generating units with a total nameplate capacity of 607.5 MW were initially installed. The installation of Unit 4 will complete the project and increase the capacity by approximately 210 MW and produce an average of 302 GWh of e!ectricity per year.

In January 2001 Minister has issued an exemption to the CPCN and directed BCH to proceed with the project for an in-service date of the spring 2004.

The Seven Mile Unit 4 project was approved by the BCH board at their January 22, 2001 meeting for an in-service date of March 1, 2004 and a CAR of $89.1 million. Expenditures to the end of May 2001 against the CAR are $10 million and the commitments are $46.8 million.

Since the approval by the BOD in January, to overhead rates charged to the project have changed and an opportunity to advance the in-service date has been explored.

The opportunity to advance the in-service date by teii months has been explored wiin GE Canada, the supplier of the generating units under the Strategic Partne~ship with BCH. Confirmed prices have been agreed with GE to accelerate work that will enable the project to enter service 10 months earlier, by 30 April 2003, at a cost to the project of $6.2 million. Other contract work in the project has been or can be scheduled to meet the accelerated in-service. Commitments have been made to preserve the early in- service date.

Analysis

Overhead Adjustment

The Power Supply SBU overhead rate has increased from 3 percent in fiscal 2001 to 6 percent in fiscal 2002. The increase is as a result of a change in overhead allocation methodologies adopted by BC Hydro and adjustment to eliminate an under-absorbed balance from the previous year. This results in a CAR request of $2.1 million.

Advanced In-Service Date

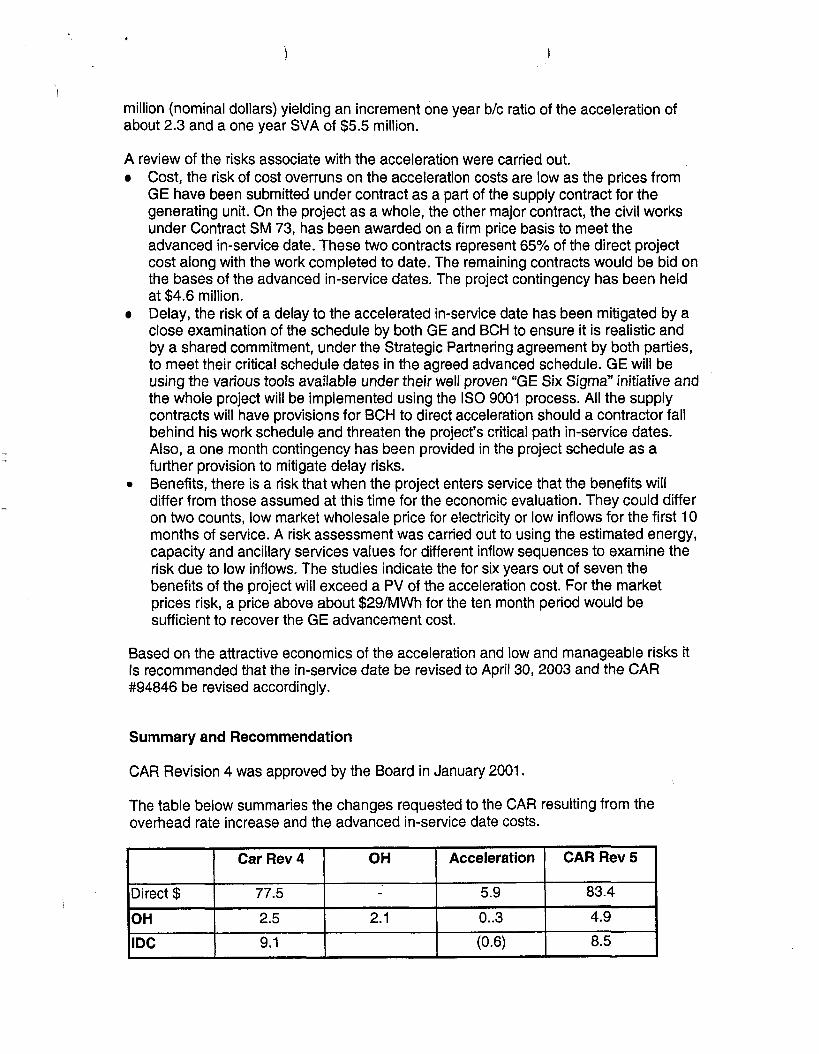

Based on the June 21, 2001 electricity price forecast, the expected incremental benefits of the generation due to the ten-month earlier in-service date are estimated at $1 4.6

million (nominal dollars) yielding an increment one year blc ratio of the acceleration of about 2.3 and a one year SVA of $5.5 million.

A review of the risks associate with the acceleration were carried out. 0 Cost, the risk of cost overruns on the acceleration costs are low as the prices from

GE have been submitted under contract as a part of the supply contract for the generating unit. On the project as a whole, the other major contract, the civil works under Contract SM 73, has been awarded on a firm price basis to meet the advanced in-service date. These two contracts represent 65% of the direct project cost along with the work completed to date. The remaining contracts would be bid on the bases of the advanced in-service dates. The project contingency has been held at $4.6 million. Delay, the risk of a delay to the accelerated in-service date has been mitigated by a close examination of the schedule by both GE and BCH to ensure it is realistic and by a shared commitment, under the Strategic Partnering agreement by both parties, to meet their critical schedule dates in the agreed advanced schedule. GE will be using the various tools available under their well proven "GE Six Sigma" initiative and the whole project will be impiemented using the IS0 9001 process. All the supply contracts will have provisions for BCH to direct acceleration should a contractor fall behind his work schedule and threaten the project's critical path in-service dates. Also, a one month contingency has been provided in the project schedule as a further provision to mitigate delay risks. Benefits, there is a risk that when the project enters service that the benefits will differ from those assumed at this time for the economic evaluation. They could differ on two counts, low market wholesale price for electricity or low inflows for the first 10 months of service. A risk assessment was carried out to using the estimated energy, capacity and ancillary services values for different inflow sequences to examine the risk due to low inflows. The studies indicate the for six years out of seven the benefits of the project will exceed a PV of the acceleration cost. For the market prices risk, a price above about $29/MWh for the ten month period would be sufficient to recover the GE advancement cost.

Based on the attractive economics of the acceleration and low and manageable risks it Is recommended that the in-service date be revised to April 30, 2003 and the CAR #94846 be revised accordingly.

Summary and Recommendation

CAR Revision 4 was approved by the Board in January 2001.

The table below summaries the changes requested to the CAR resulting from the overhead rate increase and the advanced in-service date costs.

CAR Rev 5

Direct $

OH

IDC

Acceleration I Car Rev 4 OH

77.5

2.5

9.1

2.1

5.9

0..3

(0.6)

83.4

4.9

8.5

It Is recommended that the CAR # 94846 be increased by $7.7 million to a total of $96.8 million.

I

Business Case approved by:

Total

In-Service

D. A. Harrison Senior VP, and CFO

Submitted by:

89.1

1 /Marl2004

A. Gillies Senior VP, Power Supply

Recommended by:

2.1

1 /Marl2004

M. Costello President and CEO

5.6

30lAprl2003

96.8

30lAprl2003

BC Hvdro Power and Authority Power Supplv - Resource Manaaemenf

Business Development

Calculation Information Sheet

Project Project No.

Requested By Completed By

Delivery Date Filepafh

Task

Seven Mile Unit 4

Peter Northcott Andrew GH Newell

June 15,2001 C:\Windows\TEMP\[SevenMileU4-Benefit-l SJunOl .xls]Summary - Vary Generation

Re-calculate benefit associated with accelerating construction of unit 4 using updated BC Price Forecast - 15JunOl.

Notes

PLY - - Discount Rate:

Inflation:

Annual = I 4.70% Monthly = 0.77% (blue numbers are calculaled)

Notes:

Notes:

Year

2000 2001 2002

1. Source: SNMU41-Accelerated.xls - assumed that CalCUlatiOns were in Nominal CAD.

Page 2 of 6

Annual Inflation (?o

1.700 1.900

CumulaUve

I=,": 100.0% 101.7% 103.6%

2003 1 2.000 2004 1 2.000

105.7% 107.8%

Notes: 1. &me: Corporate.

Capibl C a t (Nominal CAD):

Ancillary Service Revenue (Real 2000 CAD):

Revenue 157,794 15.061 21,418

7 n 139,362 47,969 57,157 52.164

12 191.931 Notes: 1. Source: VOE Report, DAR.

Genontion by TOD (GWhI:

1. Source: WKC.

Facton for Scaling Generatlon based on Precipitatlon: . . .

1. Source: WKC

LLH Inflow Variation 40%: 40 yr return period 50%: 12 yr return period 60°k 7 vr return narind

, . . - . - . . - . . - - , ..- , ... ..- , I." "." "."

Page 3 of 6

Jan 0.0 0.0 0 0

Feb 0.0 0.0 n n

130%: 5 yr return period 140%: 12 yr return period 150% 25 yr return period 164%: 60 yr return period

Selected

Mar 0.0 0.0 n n

Notes:

0.0 0.0 0.0 0.0 0.0

Apr 0.0 0.0 n I

0.0 0.0 0.0 0.0 0.0

May 0.0 0.1 n A

0.0 0.0 0.0 0.0 0.0

Jun 0.0 0.1 n 7

1.9 2.3 2.7 3.1 1 .O

Jul 0.0 0.0 n i

1.3 1.3 1.3 1.3 1 .O

Aug 0.0 0.0 n n

1.3 1.3 1.4 1.4 1 .O

Sep-Dec 0.0 0.0 n n

2.0 2.4 2.8 3.3 1.0

0.0 0.0 0.0 0.0 0.0

0.0 0.0 0.0 0.0 0.0

Price of BC Elecblclty (Nornlnrl CAD):

. . - .- - . 1. Source: 3lMayOl price forecast. AGHN.

Assurnptlanr:

1. Capital cost payments and revenues ocarr at the end of the month for NPV calculations.

Prlco Factor:

I lnflowVarlaHon I HLH I LLH ]

Page 4 of 6

IAE!El

BC HYDRO POWFR AND AUTHORlTY E MAN- -

P F-STIMATION OF NET BFNFFIT OF ACCEl FRATING CONSTRUCTION

C:\Wndows\TEMP\ISevenMileU4-Benefit-l5JunOl .xls]Surnmary - Vary Generation Date Printed: 25Jun-01

Notes: - -

1. NPV as of April I, 2001. 2. Totals have been rounded to the nearest hundred-thousand dollars. &rrL,r c6 f l 3. Capital cost calculations for the March 1,2004 in-service show expenditures beyond this in-service date. 7

F

C:\Windows\TEMP\[SevenMileU4-Benefit-15JunOl .xlspurnmary - Vary Generation Date Printed: 25Jun-01

Notes: 1. NPV as of April 1,2001. 2. Totals have been rounded to the nearest hundred-thousand dollars. 3. Capital cost calculations for the March I, 2004 in-service show expenditures beyond this in-service date. 4. Electricity prices have been approximated for the range of high inflow and low inflow conditions provided in the drop-down list.

The approximated prices reflect the assumption that higher prices occur in low hydro years and lower prices occur in high hydro years.

% lncreaselDecrease in Inflow from Mean with Estimated Return Period* = lM)%:2yrreturnperiod 1 - Changing expected inflow will increase or decrease generation and energy revenue of Unit 4 accordingly.

Seven Mile Unit 4 Initiative Assessment

CAR #94846

Resource Management November 2000

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Proiect

Executive Summary

The Seven Mile hydroelectric generation station is located on the Pend d'oreille River in southeastern British Columbia near Trail, 18 km downstream of Seattle City Light's Boundary Project and 9 krn upstream of Cominco's Waneta Project. The Seven Mile Dam and Power plant came into service in 1979 and consist of a concrete gravity dam, a spillway, and a 4-bay powerhouse. Three generating units with a total nameplate capacity of 607.5 MW were initially installed. The installation of Unit 4 will complete the project and increase the capacity by approximately 2 10 MW and produce an average of 302 GWh of electricity per year.

The 1994 Integrated Resource Plan (Electricity Plan) identified the installation of Unit 4 at the Seven Mile Generating Station as a prefened option to meet future domestic electrical need and recommended, through the Columbia Basin Development team, that the in-service date of 2000 be preserved. This included the application for an Energy Project Certificate (EPC). The 1995 Integrated Electricity Plan recommended continuing the licensing for the project for an in-service date of 2000.

The 1999 IEP Update concluded that no major resource acquisitions will be required by BC Hydro prior to 2006 to meet reliability planning criteria for domestic load. The IEP identifies the Seven Mile Unit 4 project will be needed to meet capacity reliability criteria in 201 1. The IEP also examined the option of advancing the Seven Mile Unit 4 project to its earliest in-service date of 36 months after receiving funding approval - March 2003. This examination identified that there may be an opportunity to advance Seven Mile Unit 4 construction ahead of domestic need to serve opportunities in electricity trade markets.

The SVA of Seven Mile 'u'nit 4, at its earliest in-service date cuiieiliiy March 2004, is $34 million over 50 years. Break-even is achieved approximately 19 years after in-service. The project provides the following additional benefits: - with an amage long-run cost of $29/MWh, the project provides a supply of electricity that

is less expensive, in the long-run, than a combined cycle gas turbine; 0 Enables retention of the Project Approval Certificate; - provides direct employment in the order of 250 person years and offset employment

through the GE Strategic Partnering Agreement of 360 person years of employment; and 0 provides green energy credits by reducing the use of gas fired electricity sources.

The Value Based Management score for this project is 60.

From a Provincial perspective, the SVA is $63 million.

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

TABLE OF CONTENTS

.................................................................................. .................................. . 1 Project Summary : 1

..................................................................................................................................... 1.1 Background 1

1.2 Opportunity ..................................................................................................................................... 2

............................................................................ . 2 Identification and Analysis of Alternatives 2

............................................................................................................................................ 2.1 Analysis 2 2.1.1 Key Assumptions ................................................................................................................................... 2

2.2 Summary of Results ....................................................................................................................... -3

3 . Risk ..................................... . . .............. .................................................................. 4

. 4 Recommendation .................................................................................................................... 7

............................................................................................................................ . 5 Project plan 7

6 . Deliverables ......................................................................................................................... 7

........................................................................................... 7 . Initiative assessment and scoring 8

............................................................................................................. 7.1 Summary of VBM Results 8

7.2 Strategic Alignment and Impact ................................................................................................... 9

.......................................................................................................................................... 7.3 Benefits 12 ................................................................................................................................. 7.3.1 Financial Benefits 12

................................................................................................................. 7.3.2 Additional BenefitsIImpacts 13

7.4 Projecthitiative Costs ................................................................................................................. 15

...................................................................................................... 7.5 Implementation Risk Factors 16

Appendices:

Appendix I: Detailed Assumptions Appendix 11: Results of Financial Analysis

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

I

1. PROJECT SUMMARY

The Seven Mile hydroelectric generating station is located on the Pend d'oreille River in southeastern British Columbia. The facility is situated 18 km downstream of Seattle City Light's Boundary Project and 9 krn upstream of Cominco's Waneta Project. The Seven Mile Dam and Power Plant came into service in 1979 and consists of a concrete gravity dam, a spillway and a 4- bay powerhouse. Three generating units with a total nameplate capacity of 607.5 MW were initially installed. The fourth bay remains empty. The power plant was designed as a four unit 8 10 MW facility, which would be in hydraulic balance with the ultimate six-unit development at the upstream Boundary plant. Unit 4 would increase the installed capacity by approximately 210 MW and enable the facility to produce average incremental energy of 302 GWh per year. No additional transmission facilities would be required between Seven Mile and Kelly Lake/Nicola to accommodate Unit 4.

The Seven Mile Unit 4 project was initiated as a result of the findings of the 1994 Integrated Resource Plan (IRP). The 1994 Integrated Resource Plan (Electricity Plan) identified the installation of Unit 4 at the Seven Mile Generating Station as a preferred option to meet future domestic electrical need and recommended, through the Columbia Basin Development team, that the in-service date of 2003104 be preserved. This included the application for an Energy Project Certificate (EPC).

Key events since the 1994 IRP include: Energy Project Certificate Appiication submitted, December 1994 The 1995 Integrated Electricity Plan recommended continuing the licensing for the project for an in-service date of 2000. BC Hydro's Board of Directors approved capital funding kr the project, February 1995. Completed the "Mitigation and Compensation Plan for the Installation and Operation of Unit 4 at the Seven Mile Generating Station", March 1996 Project Approval Certificate approved by the Province, 25 April 1996 Application for a Certificate of Public Convenience and Necessity (CPCN) made in, September 1995 Authorization under the Fisheries Act ganted December 1996 Application for a CPCN withdrawn December 1998 Water License issued allowing diversion of water for Unit 4, December 1998 The BCH Board endorses management's recommendation to "discuss with the Province options for advancing the project for a 2002 in-service date and that these discussions be expedited to preserve the 2002 in-service date", 13 September 1999. The 1999 IEP Update concluded that no major resource acquisitions will be required by BC Hydro prior to 2006 to meet reliability planning criteria for domestic load. The IEP identifies the Seven Mile Unit 4 project could be needed to meet capacity reliability

Page 1

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

1

criteria in 201 1. The IEP also examined the option of advancing the Seven Mile Unit 4 project to its earliest in-service date of October 2002.

There may be an opportunity to advance Seven Mile Unit 4 construction ahead of domestic need to serve opportunities in electricity trade markets.

2. IDENTIFICATION AND ANALYSIS OF ALTERNATIVES

Two alternatives have been considered to address electricity trade market opportunities:

1. Install Unit 4 Now: This alternative represents installing generating unit 4 with the earliest possible in-service date: March 2004 or 36 months after receiving approval.

2. Install Unit 4 Later: This alternative represents installing generating unit 4 for an in- service date of October 20 11.

, 2.1 .I Key Assumptions

The key assumptions used in the analysis include':

- 1 he anaiysis assumes a base case in-service date of March 2004.

c The analysis incorporates the September 2000 nominal electricity price forecast. o The analysis is conducted in nominal dollars using a nominal discount rate of 8.7% with

an amuai-lhflation rate of 2.0% applied to capital, OMA and water rentals. 0 The total direct capital cost, including inflation, used in the analysis of the project is

$76.8million. This excludes interest during construction (IDC), overhead, and monies previously spent.

+ The analysis excludes previous direct spending of $6,498 million for assessment and licensing. The loaded value of this spending is $8,391 million (loaded for overhead and IDC).

+ The generation forecast is based on the historical 45-year in-flow conditions for Seven Mile, adjusted to reflect current operating constraints.

+ The turbine will be purchased and installed by GE Canada under the terms of the Strategic Partnering Agreement.

Detailed assumptions are located in Appendix I.

Page 2

BC Hydro Power Supply Initiative Assessment and Scorina: Seven Mile Unit 4 Proiect

The two alternatives have in-service dates. Because of the significant impact on timing of costs and benefits, the results are presented for both alternatives to the end of the economic life; both alternatives assume a 50-year economic life2.

Table 2.1 indicates that proceeding with an in-service date of March 2003 is the most economic long-run of the alternatives presented.

Table 2.1 Summary of the Alternatives

10 Years of Benefit End of Life I 10 Years of Benefit End of Life

PV Project Benefits $47,286 $102,098 1 $20,050 $53,272

PV SVA3 (Nominal) $8,020 $33,676

PV Proiect Cost 63.812 68.423 1 45.078 47,679

($10,885) $5,593

.I I

NPV (Nominal) ($16,526) $33,675 1 ($25,029) $ 5,593

In addition to the financial benefits, other benefits include:

Benefit Cost Ratio 0.74 1.48

The implementation of the project will provide 250 person-years of employment. Under the Turbine Partnering Agreement with GE for the purchase of the generating unit the industrial offset agreement would provide a , further 360 person-years of employment through a $30 million industrial offset. The project supports the realization of the intent and objectives of the GE Partnering agreement. The forward electricity price curve is based on the long-run cost of combined cycle gas turbine (CCGT) located in the lower mainland. The analysis values electricity delivered to the lower mainland. Therefore, a project that has a long-run benefit-cost ratio greater than 1.0 is a more attractive long-run investment option than a CCGT located in the lower

0.44 1.07

Both alternatives presented discount results to 2000/01. 3 ~ h e analysis does not include dividend impacts.

-

Page 3 01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

mainland. Seven Mile Unit 4 has a long-run benefit cost ratio of 1.48, it is therefore considered an economic long-run source of electricity supply.

Further, the project includes costs that are likely to be incurred irrespective of the decision to proceed. These costs are;

0 Plant Reliability: There is an imminent requirement to replace the switch-gear at the existing units at Seven Mile. As part of the Unit 4 project, the switch-gear on Unit 3 will be replaced to be compatible with the new switch gear to be provided on unit 4. If Unit 4 is not installed, funding will be requested to replace the switch-gear on Units 1 and 2. The cost of replacing switch-gear on Units 1 and 2 or Units 3 and 4 is $4.6 million. Overhead Costs: The project includes an allowance for $2.4 million of overhead. These overhead costs are likely to be incurred whether the project proceeds or not. - Other costs: The project includes cost allowances for "other" work such as corporate administration, M&C, Power Facilities, public consultation etc. These costs, totaling $1.6 million would likely be incurred through other initiatives such as water use planning.

If the project does not proceed, the following costs will be incurred:

Strategic Partnering Agreement: If the project does not proceed, GE through the Strategic Partnering Agreement could seek damages due to failure to meet the expectations of the agreement, this could expose BCH to a penalty estimated at $3.3 million. These costs have been included in the delay option. Write-down: Approximately $8.3 million has been spent to date. If the project does not proceed, monies spent to date will be written-off. These costs have been included in the deiay option.

3. RISK --

The following risks have been given consideration as they relate to pursuing an in-service date of 2002103 :

Construction Cost: The construction cost estimate.is considered conservative for the following reasons:

1. Cost Estimate: The cost estimate consists of approximately $30 million (direct dollars) of work to be completed by GE Canada with $37 million (direct dollars) of work to be completed by others. The cost estimate was reviewed in November 2000 and the prices from GE Canada are under the Strategic Partnering Agreement are confirmed.

Political Issues: The project is attractive from a Provincial perspective, and the risk that rate payers could be adversely impacted is considered to be low.

Page 4 01/01/08

BC Hydro Power Supply Initiative Assessment and Scorina: Seven Mile Unit 4 Proiect

Option Values: Option evaluation has not been explicitly considered because the appropriate tools and skills are not readily available.

Foreign Exchange Exposure: Foreign currency exchange rates are not considered to be a project risk. Rather, foreign exchange exposure managed on a portfolio basis by the treasury group.

Transmission Risk: The cost of incremental transmission capital is included in the economic analysis.

Project Approvals: Project approvals are subject to cancellation if the work is not substantially started within five years of its date of issue. The Project Approval Certificate was issued on 25 April 1996. The Federal Department of Fisheries, Habitat Compensation Agreement requires that the civil works associated with the project commence within five years from the date of the agreement (Agreement date 22 March 1996). The Federal DFO Authorization requires that the construction of the civil works begin within five years of the date of the authorization (2 December 1996). If the project does not proceed prior to March 2001 then these approvals could lapse or require extension.

Sensitivity Analysis: The project is sensitive to changes in market prices and water conditions. - - - Accordingly, the following cases have been analyzed:

1. High market prices resulting in an increase in average prices of approximately 6%4. 2. Low market prices resulting in a reduction in average prices of approximately 6%. 3. High water conditions resulting in an increase in energy and a decrease in prices. 4. Low water conditions resulting in a reduction in energy and an increase in price.

4 High and low market prices are based on the high-low range of the long-run marginal cost of gas as provided by Confer in February 1999.

High and low water conditions represent a 1 &I 10 ten year event. The high and low water conditions have resulted in price impacts consistent with those described in the previous footnote.

Results are presented to the end of economic life.

Table 2.2 Summary of Sensitivity Analysis6

Nominal ($000)

Page 5 01/01/08

.C

SVA to economic life B/C Ratio to economic life

Annual HLH GWh Annual LLH GWh

Low Market

Price Case 'i

'" . - >

$26,030 1.37

200 102

Base Case In-Service.

2003104 ', ' . - ,d*

$33,675 1.48

200 102

High Water

' High . Market

. Price Case z

$41,322 1.59

200 102

Low Water

Conditions a* _ I- Case ,&$

$86,460 2.25

347 163

Conditions ,.pp -.< &, - A

, :,*,*~C&se -. - ;:

$17,592 1.25

13 1 70

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

7 ~ h e analysis does not include dividend impacts.

i

Assumptions for each sensitivity are located in Appendix I.

In addition, the following impacts have been considered:

C02 Offset: construction of Seven Mile Unit 4 avoids an estimated 170,000 tonneslyear of C02 which would be produced by other competitive sources of generation. The cost to offset the C02 is estimated $10 and $90 per tonne. At $10ltonne this results in an additional annual savings of $1.7 million.

(61% NIA

+6 % Nl A

Average Price Change Impact on Water Rentals

Also, a sensitivity analysis has been conducted using a discount rate of 12% nominal. This represents a rate risk adjusted for market price volatility. The results are provided in table 2.3.

NIA N/A

Table 2.3 Summary of the Alternatives Using a Discount Rate of 12% Nominal

(16) % +66%

+26 % (34)%

PV SVA7 (Nominal) ($3,893) $3,483 r-

Benefit Cost Ratio 0.64 '1.05 1 02 8 0.62

($17,732) ($13,316)

PV Project Benefits $37,974 $64,808 PV Project Cost 59,010 6 1,325 NPV (Nominal) ($2 1,036) $3,483

Page 6 01/01/08

$9,664 $22,539 34,819 35,855

$25,155 ($13,316)

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

I

4. RECOMMENDATION

The SVA of Seven ~ i l e Unit 4, at its earliest in-service date currently March 2004, is $34 million over 50 years. Break-even is achieved approximately 19 years after in-service. The project provides the following additional benefits:

a with an average long-run cost of $29/MWh, the project provides a supply of electricity that is less expensive, in the long-run, than a combined cycle gas turbine;

a Enables retention of the Project Approval Certificate; a provides direct employment in the order of 250 person years and offset employment

through the GE Strategic Partnering Agreement of 360 person years of employment; and a provides green energy credits by reducing the use of gas fired electricity sources.

The Value Based Management score for this project is 60.

From a Provincial perspective , the SVA is $66 million.

5. PROJECT PLAN

The project plan is documented in report number MEP392, titled: the "Columbia Basin Development, Seven Mile Unit 4 Implementation Phase Project Plan".

6. DELIVERABLES - The deliverables include:

Unit 4 installed and operational 36 months after funding approval. a Job creation which will be measured and recorded in accordance with the Industrial

Benefits Program agreement. .

Page 7 01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

7. INITIATIVE ASSESSMENT AND SCORING

7.1 SUMMARY OF VBM RESULTS

Figure 2.1 Summary of VBM Scores

STRATEGIC IMPACTS (0 - 25) Secure the Base

Efficiency & Productivity Effective Governance Public Support

Build a Strong & Capable Organization Enhance Customer Focus

Service Excellence Value Added Solutions

Grow the Business Market Development Strategic Businesses & Markets

Total Score for Strategic Irn~acts 11

ADDITIONAL BENEFITS (0 - 20) Environmental Impacts 7 LegaYRegulatory Adherence 0 Public Support 2 Employee or Union Issues 5 Aboriginal Relations 2 PublicEmployee Safety & Health 0 CornrnunitylEmployment Impacts

El 10

Total Score for Additional Benefits 20

I FINANCIAL BENEFITS (0 - 25)

PV of SVA to 10 Years $8.1 million PV of SVA to end of Life: $33.7 million

INITIATIVE COSTS (0 - 15)

PV of Costs to end of Life: $68.4 million 0

IMPLEMENTATION RISKS

Time to Implement Complexity Assumptions Past Performance Technology/Methodology Mitigation Strategy 48%

Total Score for Implementation Risks

I Total VBM Score for the Seven Mile Unit 4 Project I

Other Evaluation Measures

Corporate NPV (5 16,525) $33,676 Corporate BIC Ratio. 0.74 1.48 Unit Cost of Generation $29.18 Provincial NPV $62,771 Provincial B/C Ratio 1.92

Page 8 0 1/0 1/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

7.2 STRATEGIC ALIGNMENT AND IMPACT

Efficiency & Productivity Support competitive pricing

( Y W I Y: orovides new e n e r ~ v s u ~ ~ l v 1

Oprimize commercial availability I Y: ~rovides new caoacitv I Develop operating plans to maximize total margin I N I Develop investment plans for new plants I N I fn~esr/divest/maintain assets commercially I N I Garher customer, market and competitor intelligence I N I - I

Oprrmrze operating and resource data rncludrng the role of each plant I N I Effective Governance & Public Support

Enhance ~oodwd l and consent to operate I N I - 1

Balance multiple objectives I N I . - I

Manage issues (i. e. Sinkhole) I N L,nderstand constraints and impacts (ex . Dam Safety, WUPs) N I Develop and maintain Gov't and community relationshrps I Yes: supports Government initiative Seekstakeholder input I N

Service Excellence x. b

Delrver on promises 1 N Blrrld a siraiegic relaiionshi~ with Powerex N

Development of leadership Improved communication and information

Development of competencies Improved relationship Establishment of collaborative management

Alignment of the worL$orce Fostering diversiv Encoura~ement o f flexibilitv

N N N N N N N N

Value-Added

COLU&~IO strengIhen operafmg relat~onshp w ~ f h Powerex -

Manage . W C S and T&D relationshrps Define/develop relationshrps wrth M&CS and T&D

Create new product and service ideas N Enhance Power Supply 's capabilities N tinderstand customer needs and market requirements N Parrner with direct customers N L'nderstand core ca~abililies N

N N N

Market Development Creote new product and service ideas Enhance Power Supply's capabilities L'nderstand customer needs and market requirements

Partner with direct customers L'nderstand core caoabilities

Y: increase in fleet capacity t---"---l I I

New Strategic Businesses & Markets 9) ,

Develop targeted energy-related solutions I N Burld/mvest/drvest to caprtal~ze on new opportunrtres N Parmer with direct customers I N I

Page 9 0 110 1/08

- . . . ..

Ensurefit wrth Power Supply's strengths and strategrc drrectron

Scanjor oppor1imrfres en fry / ex11

. . N N

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

Slrategic Objectives ~ & p A EG " PS " Org A CS " GTB "

Strongly supports tho objective

Is mica1 to this objedivs as it

panaina le m S8UI KBU

Financial Efficiency and Productivity (E&P) Score: 6 Notes: Provides low cost supply of new energy and capacity.

Effective Governance (EG) Score: 5 Notes: Facilitates government initiative.

Build and Maintain Public Support (PS) Score: 0 Notes: No significant impacts on this objective.

Build a Strong and Capable Organization (ORG) Score: 0 Notes: No significant impacts on this objective.

Lead the Market - Enhance Customer Service (CS) Score: 0 Motes: No significant impacts on this objective.

Lead the Market - Grow the Business (GTB) Score: 0 - Notes: No significant impacts on this objective.

Is ckiIiC11 10 Ihls objeslive or n penainr

10 all of BCH

Page 10 01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

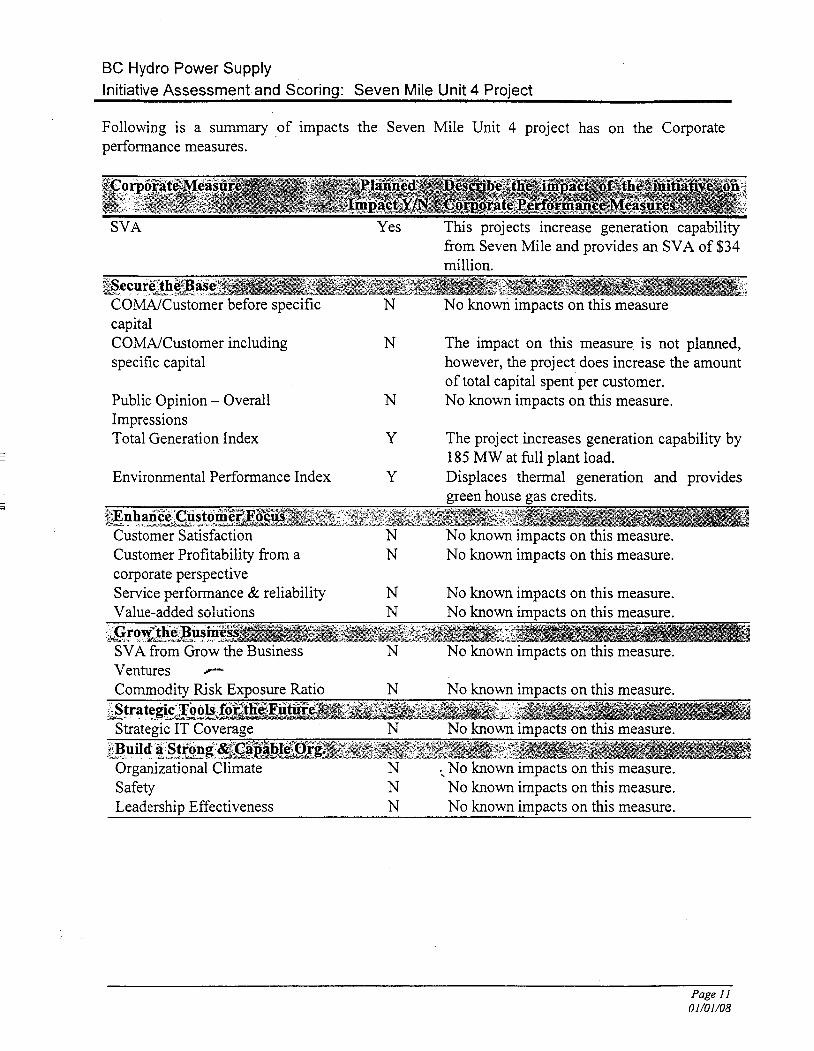

, Following is a summary of impacts the Seven Mile Unit 4 project has on the Corporate performance measures.

SVA Yes This projects increase generation capability from Seven Mile and provides an SVA of $34 million.

COMNCustomer before specific capital COMA/Customer including specific capital

Public Opinion - Overall Impressions Total Generation Index

Environmental Performance Index

N No known impacts on this measure

N The impact on this measure is not planned, however, the project does increase the amount of total capital spent per customer.

N No known impacts on this measure.

Y The project increases generation capability by 185 MW at full plant load.

Y Displaces thermal generation and provides green house eas credits.

Customer Satisfaction N No known impacts on this measure. Customer Profitability from a N No known impacts on this measure. corporate perspective Service performance & reliability N No known impacts on this measure. Value-added sohtions N No known impacts on this measure.

SVA from Grow the Business N No known impacts on this measure. Ventures -s

Commodity Risk Exposure Ratio N No known impacts on this measure.

Strategic IT Coverage N No known im~acts on this measure.

Organizational Climate Safety Leadership Effectiveness

N , No known impacts on this measure. N No known impacts on this measure. N No known impacts on this measure.

Page I I 01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

7.3 BENEFITS

7.3.1 Financial Benefits

PV of SVA: $34 million over the economic life of the project Score: 20 Notes: Refer to Appendix I1 for details on SVA calculations.

Summary of Scoring:

Summary of Financial Results In Service April 2004

Corporate SVA Score

The score assigned for SVA earned within 10 years.

SVA t Negative $1 Milfion 1 $2.5 1 $5 Million

Score assigned ~ O ~ V A earned over the life of the project:

Page I2 01/01/08

$25 Million

18 Million

16 Score

$50 Million

20

-

0

$1 Million

1

SVA

Score

$2.5 Million

1.5

Negative

0

4

$10 Million

3

$5 Million

2

Million 8

$25 Million

4

12

$50 Million

5

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

i

7.3.2 Additional Benefitsllmpacts

Score: 7 Notes: Mitigates the need to develop gas fired generation; provides green house credits.

Score: 0 Notes: No known legal/regulatory issues prevented or caused.

Score: 2 Notes: ThfTommunity of Trail may be interested in the construction of this project due to

potentially significant regional employment impacts.

Employee or

m rn v v

Nepabw general NepabYe general employee mteml n

P o ~ g e n c r a I PO+&#. general P- ponenl employe. mtsre.tl employee interenis employ.. mbrnt is

low. bu1mong.r ~enerally low to wy hqh. * l idnwd. . m t e r t held 4 a few d e r a t e , but high andlor a rnalorRyvM* OfOUP ammg swersl group rmong key group

Score: 5 Notes: Strongly held interests across KBUs and SBUs. Interested groups include Power

Supply Engineering, Resource Management, Power Facilities, Transmission & Distribution, Corporate Environment and PowerEx.

Page 13 01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Proiect

Score: 2 Notes: The Columbia Hydro Constructors have specific clauses for aboriginal training and

employment. Further, the local aboriginal group has been consulted on the project.

PublicErnployee Safety

T-7 r-7 r - 7 v W-T

PI.VIIII low Pr.9.m nigh P r t ~ e n 6 modcrate to probaUii of moderate probabilh of moderate h g h probability of high

impacl events imp& aenb, or l w probably of hmh

impad wech

Score: 0 Notes: No known impacts.

Premnb minor job Prwems m ~ l ~ job Revme moderat. to lar *l a man numer b u n a MA wmbn hgh job bu n a large

of m m m u d r 01 sornmwhs. w "Ymbwof minor job lo0. n r

hrg. ""mbef Of commYnh.s

w m m

Score: 10 Notes: Creaks 250 worker years of employment with an additional 360 person years of off-

set employment through the GE Partnering Agreement.

Page 14 01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

Score: 0 Notes: Present value of generation capital (including overheads) using a 2.0% net escalation

and an 8.7% discount rate is $59.6 million. Present value of transmission capital is estimated at $8.8 million. Present value of all project costs is $68.4 million.

Page 15 01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

Time to implement (What is the total elapsed time of the initiative, ffom commitment to full deployment?) Time to Implement

7 v 3' 7

Score: -5 Notes: Upon receiving funding approval, the project has a 36 month construction period.

Complexity (Describe any specific dependencies and linkages between this and a) other initiatives, b) other SBUs or KBUs, or c) external organizations.)

Complexity

Score: 0 Notes: Although this project uses external parties to supply and install the unit, one of the

major suppliers, GE, is a preferred supplier selected by the Board of Directors.

Past Performa~ce (Does BC Hydro have past experience implementing similar initiatives? I f so, would you characterize past results as being successfill or unsuccessfil? Explain.)

Past Performance /I T-* 7

f Y

Score: 0 Notes: BC Hydro has successful experience in installing generating equipment. .

Page 16 01/01/08

BC Hydro Power Supply Initiative Assessment and Scorina: Seven Mile Unit 4 Proiect

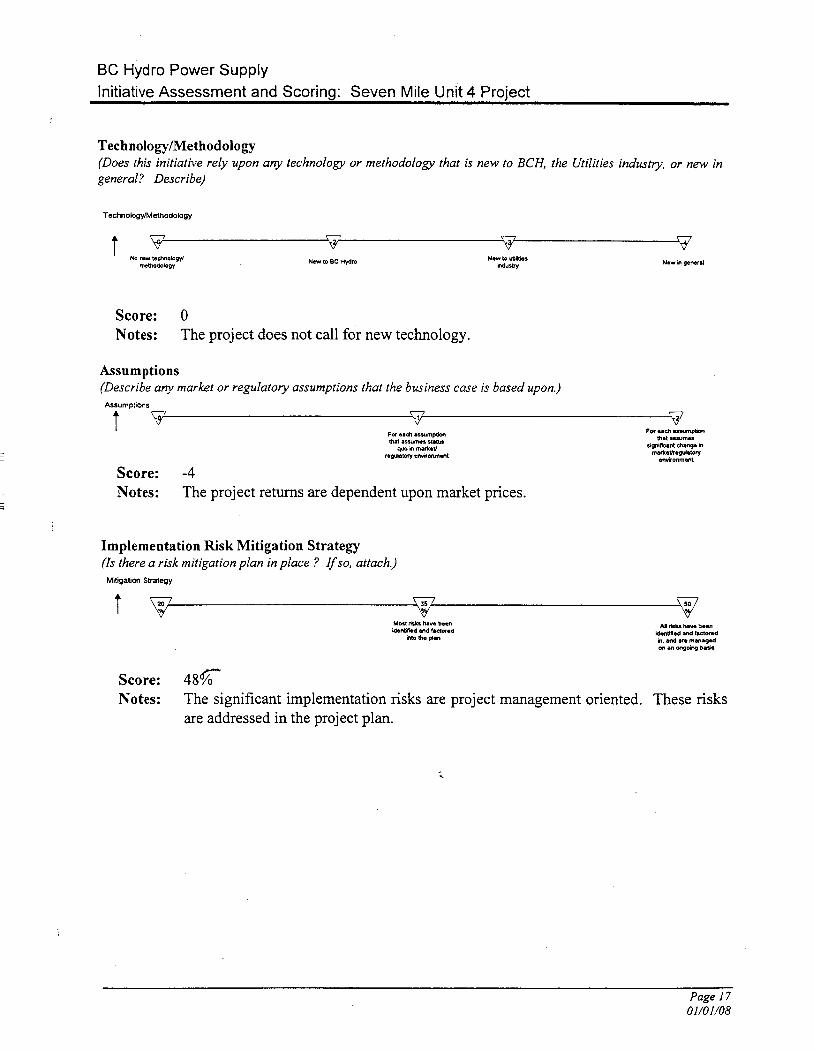

Technology/Methodology (Does this initiative rely upon any technology or methodology that is new to BCH, the Utilities industry, or new in general? Describe)

Score: 0 Notes: The project does not call for new technology

Assumptions (Describe any market or regulatory assumptions that the business case is based upon.)

Score: -4 Notes: The project returns are dependent upon market prices.

Implementation Risk Mitigation Strategy (Is there a risk mitigation plan in place ? If so, attach.)

Mitigation Strategy

Score: 48r Notes: The significant implementation risks are project management oriented. These risks

are addressed in the project plan.

Page 17 01/01/08

Seven Mile Unit 4 Initiative Assessment

APPEND!X I

Detailed Assumptions

Resource Management November 2000

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

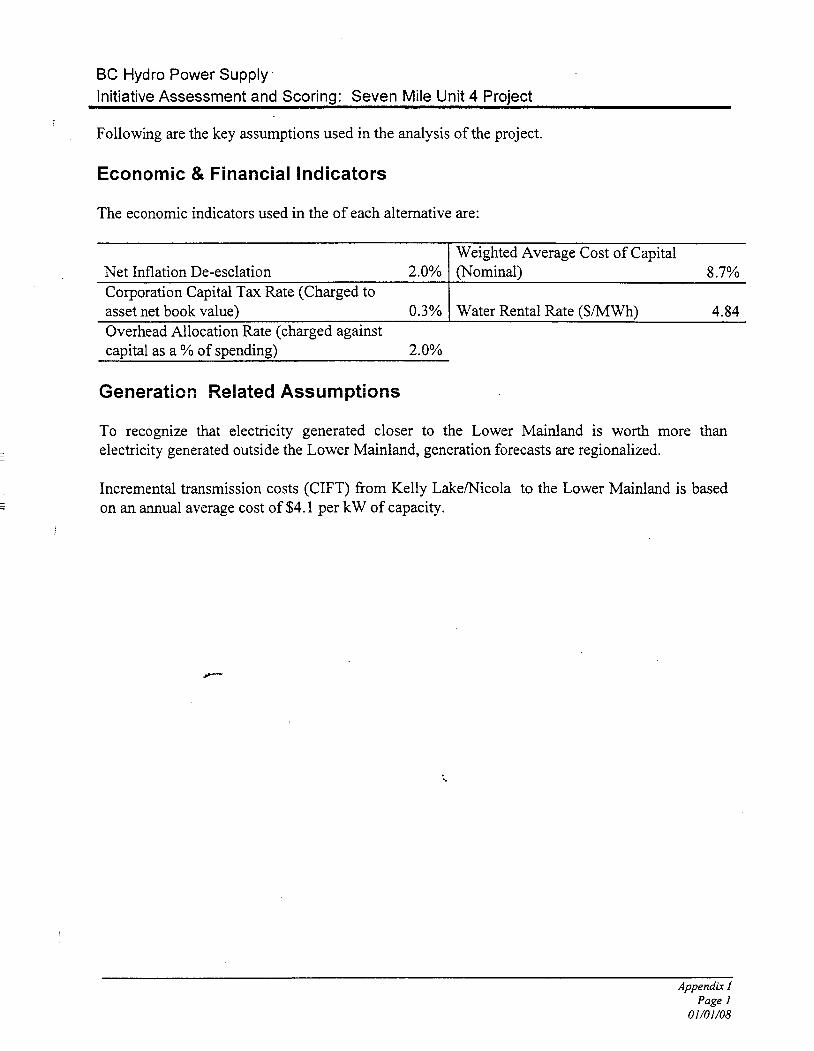

I Following are the key assumptions used in the analysis of the project.

Economic & Financial Indicators

The economic indicators used in the of each alternative are:

1 Weighted Average Cost of Capital

asset net book value) 0.3% 1 Water Rental Rate ($/MWh) 4.84 Overhead Allocation Rate (charged against capital as a % of spending) 2.0%

Net Inflation De-esclation 2.0% Corporation Capital Tax Rate (Charged to

Generaticn Related Assumptions

(Nominal) 8.7%

To recognize that electricity generated closer to the Lower Mainland is worth more than

- - - electricity generated outside the Lower Mainland, generation forecasts are regionalized.

Incremental transmission costs (CIFT) from Kelly LakeNicola to the Lower Mainland is based - - - on an annual average cost of $4.1 per kW of capacity.

Appendix I Page I

01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

Energy Impact Assumptions

The generation forecast is based on the historical 45 year in-flow conditions for Seven Mile, adjusted to reflect current operating constraints. The assumptions used to estimate energy impacts include:

1) Basin Description: - United States Basin: All but about 25 miles of the Pend Oreille River (US Spelling ... spelled Pend d'oreille in Canada; pronounced "Ponderay" in both Countries) are located in the US.

c Storage Reservoirs: There are 3 major storage reservoirs on the Pend Oreille and its tributaries (Flathead, Clark Fork, Bitterroot, Priest). Hungry Horse, owned by the US Bureau of Reclamation and directed by BPA, has over 3 MAF of active storage and provides multi-year storage operations. The Ken project, owned and controlled by the Montana Power Company, controls the level of Flathead Lake, has about 1 MAF of active storage and is operated over an annual cycle. The Albeni Falls project, owned by the Army Corps of Engineers and directed by BPA, controls the level of Lake Pend Oreille, has about 1 MAF of active storage and is operated over an annual cycle. - Storage Control: Operation of the Pend Oreille storage projects is coordinated with other Columbia basin operations through the Pacific Northwest Coordination Agreement (PNCA). BCH is not a member to this agreement, and has no input into basin storage operation. Unlike the Columbia Treaty Storage, the downstream agency (i.e. BCH) does not provide any compensation to the upstream parties for power-related streamflow improvements, and essentially takes the flow as provided by the US operation.

c Fish Operations: Over the last decade, fish related constraints have been imposed on aii reservoirs on the river. This has significantly reduced the effectiveness of the storage for power operations at both US and BCH project sites. Boundary-Dam: The Boundary project is located immediately upstream of 7 Mile. The project was expanded in 1985, and now has a discharge capacity of about 50 kcfs. Its forebay provides sufficient storage for its owner, Seattle City Light, to aggressively load factor the project. Generally this involves directing the available daily energy into 15 Heavy load Hours (HLH) up to the project discharge limit, with the residual water spread evenly over the remaining Light Load Hours (LLH). During the freshet period there is usually enough water coming down the rivkr to run Boundary at full load around the clock. As a result, no blocking is assumed in May, June and July. There is no minimum flow requirement for Boundary. 7 Mile: The current discharge limit for 7 Mile is about 39 kcfs. The addition of the 4" unit would increase this to about 52 kcfs, about the same as the Boundary limit. Since Boundary typically releases more water during HLH than 7 Mile (and Waneta downstream) can currently handle, the 7 Mile forebay is normally drawn down in advance of the high Boundary flows, to re-regulate the daily flows and reduce the spill at 7 Mile and Waneta.

Appendix I Page 2

01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

Waneta: This project is owned by Cominco, but its operation is directed by BCH. Under the terms of the 1972 Canal Plant Agreement, Cominco is provided with a constant annual entitlement to capacity and energy, and BCH retains the actual output from the project. The current discharge capability at Waneta (with 1 out of 4 units upgraded) is about 26.6 kcfs - approximately half that of Boundary. When the project is hl ly upgraded the discharge capacity is expected to be about 3 1.6 kcfs. An expansion project is also being considered (but is unlikely?) that could potentially bring Waneta into hydraulic balance with a 4-unit 7 Mile.

2) Strearnflow Modeling: * Monthly Flow Records: Power studies were completed using three different streamflow

records: the 1993 AOP flows (1940-1985), the 1996 BPA Rate Case flows (1928-1 978), and the Feb 1998 BPA 'Best Estimate' (1928-1978). The latter two records include all anticipated fish constraints, and therefore provide a range for the more realistic basin operations. The 1998 BPA flow estimate is presumed to be the more accurate, however, becaiise it was developed more recently. To the extent that dditiona!, uiianticipated constraints may be imposed upon upstream reservoirs, both increases or decreases in 7 Mile 4 generation estimates could be anticipated. As supported by the range of streamflow records studied, however, additional constraints tend to reduce total generation from the 7-Mile project while increasing the incremental output associated with the 4'h unit. Daily Flows: Daily flow estimates were synthesized from the monthly flow estimates, using an auto-correlation procedure originally developed by Kelvin Ketchum.

2) Power Studies: Modei Details: The simulation model is a fortran modei deveioped by Herbert Louie and Wun Kin Cheng. It simulates the operation of Boundary, 7 Mile and Waneta on a twice- daily time step. The definition of HLH is variable, and was set equal to 15 hours for all studies. Boundary Operation: The daily inflows into Boundary were regulated into a maximized 15 hourELH block and a residual, 9 hour LLH block. No distinction was made between days of the week (no weekend modeling is provided). 100% unit availability assumed for all plants (i.e. no forced or planned maintenance is directly modeled). 7 Mile Re-regulation: The model simulates the 7 Mile forebay which is used to re- regulate the flows to minimize spill at the lowest discharge BCH project (i.e. Waneta). In actual practice, BCH attempts to maximize generation value, which can differ from maximizing generation. When HLH / LLH differentials are high enough to justify the operation, BCH does incur avoidable at Waneta to generate additional HLH energy at 7 Mile. This additional value (of deliberate spill when economically driven) is captured outside the model studies. mote: Recent water licence amendments may preclude this operation during some portions of the year. Further interpretation of the amendment should be investigated.] Waneta Configuration: Since the model operates 7 Mile to minimize spill at Waneta, the assumed discharge capability at Waneta affects the estimation of the benefits from 7 Mile Unit 4. It was assumed that all 4 Waneta Upgrades were installed. No Waneta Expansion was modeled.

Appendix I Page 3

01/01/08

BC Hydro Power Supply Initiative Assessment and Scorinq: Seven Mile Unit 4 Proiect

Operating Constraints: All current forebay, tailwater and generation characteristics were reflected in model studies. Turbine efficiencies for 7 Mile were obtained from the 1981 - 1984 efficiency test studies for the existing units and from bid document for the 4th unit. 4th Unit Generation: Model studies were completed for both 3-unit and 4-unit installations at 7 Mile. HLH and LLH generation totals were obtained for each study, for all 50 water years provided in the 1928 - 1978 BPA Rate Case strearnflow record. Average generation estimates were computed for each month, for both HLH and LLH. Generation benefits from the unit addition were estimated by taking the differences between the 7 Mile generation estimates. Dispatchability Premiums: Supplementary power studies were completed with 1 hour, 2 hour, 3 hour (etc.) ... and 15 hour definitions for HLHs. By taking the differences between these studies, a daily HLH profile of the project's generation potential was developed. By multiplying this hourly generation profile by an assumed hourly price profile, monthly dispatchability premiums were defined for both the existing and the expanded project. These premiums estimate the aciciitionai vaiue that can be accessed by the additional 200 MW of capacity provided by the 4th unit, through shifting lower value HLH energy, into higher value HLHs.

- - -

Revenue Related Assumptions - - -

Revenues have been valued using the Value of Energy valuation methodology. The price forecast used to value electricty is as of September 2000.

Other Cost Assumptions

OMA: facility OMA is estimated at $279k per year. The incremental OMA is due to additional maintenance requirements associated with having another generating unit. - Municipal Taxes: taxes and grants have been estimated by the corporate group and are approximately $190k per year.

Water Rentals: water rentals are based on incremental energy produced at $4.84/MWh

Capacity Fees: capacity charges are basid on incremental capacity of 185MW at $3.453/MW.

Project Cash Flows

Direct 300 7,963 28,030 30,965 463 Loaded 310 8,334 29,705 33,227 503

Appendix I Page 4

01/01/08

BC Hydro Power Supply Initiative Assessment and Scorinq: Seven Mile Unit 4 Proiect

Appendix I Page 5

0 I/O//O8

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

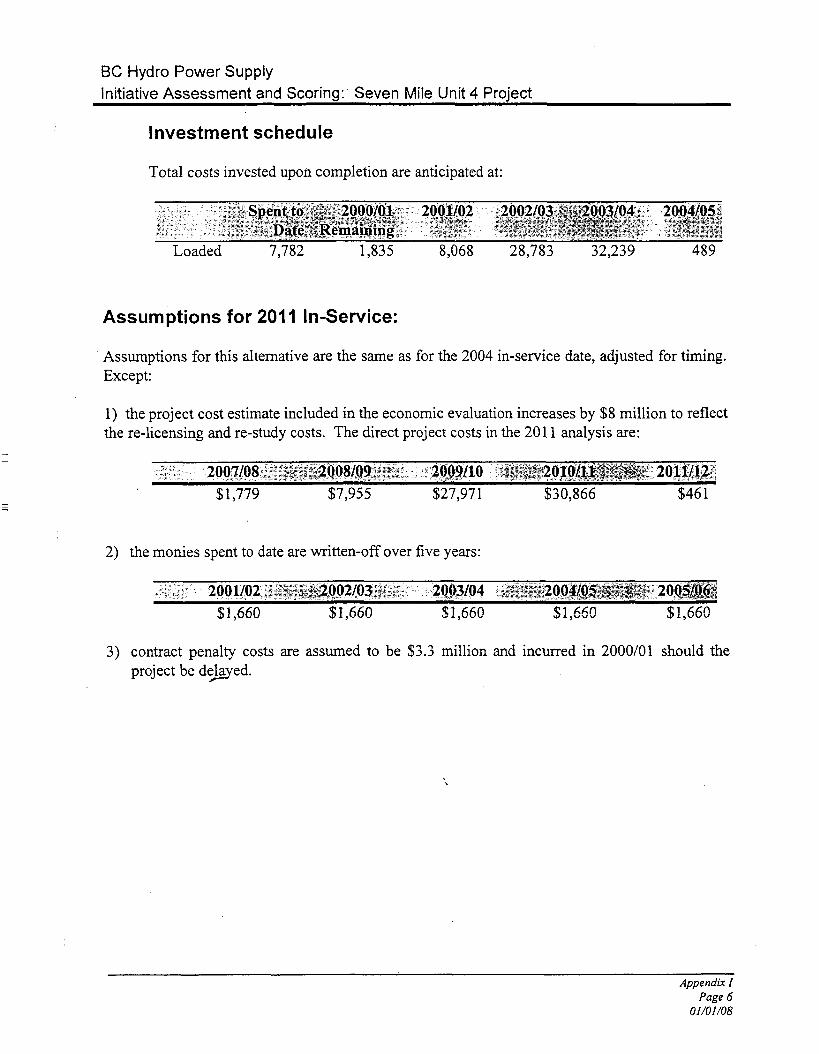

Investment schedule

Total costs invested upon completion are anticipated at:

Assumptions for 201 1 In-Service:

Assumptions for this alternative are the same as for the 2004 in-service date, adjusted for timing. Except:

1) the project cost estimate included in the economic evaluation increases by $8 million to reflect the re-licensing and re-study costs. The direct project costs in the 201 1 analysis are:

2) the monies spent to date are written-off over five years:

3) contract penalty costs are assumed to be $3.3 million and incurred in 2000/01 should the project be de@ed.

Appendix I Page 6

01/01/08

BC Hydro Power Supply Initiative Assessment and Scoring: Seven Mile Unit 4 Project

Assumptions for Sensitivity Analysis

VOE HLH Revenues VOE HLH Revenua VOE Dispatchability & Raeme Premiums Dispatchability & Reserve Premiums as a % of Revenues .J /

April May June July August September October November December January February

Total Annual Incremental

Heavy Lnad Light Load GW.h GW.h

Generatio EEi! VOE Levelized Base Case Price VOE Levelized Smsitiity Price

Price Change: 5.71%

VOE HLH Revenua VOE HLH Revenues VOE Dispatchability & Reserve Premiums Dispatchability & Reserve Premiums as a % of Revenus Generation:

Heavy Load Light Load CW.h GW.h

April IMay June July August September October November December January February March Total Annual Incr -EEl remental Generatio

VOE Levelized Base Case Rice IVOE Levelized Sensitivity Price

l ~ r i c e Change: -15.71%

VOE HLH Revenua VOE HLH Revenuer VOE Dispatchability & Reserve Premiums Dispatchability & Reserve Premiums as a %of Revenua -2

Heavy Load Light Lond GW.h GW.h

April May June July August September October November Decemba January February March Total Annual lncremenul Gneration

I VOE Levelired Base Case Price VOE Levelired Lnsitibity Rice -7 I Price Change: -5.71%

Heavy Load Light Load GW.h CW.h

April

June July August September OC* November December January February March Total Annual Incremental Gneration

VOE Levelired Base Case Rice IVOE Levelized Sensitivity Price E q lmCe change: 25.71%

Appendix 1 Page 7

01/01/08

Seven Mile Unit 4 Initiative Assessment

APPENDIX ll

Results of Financial Analysis

Resource Management November 2000

Seven Mile Financial Evaluation Key Assumptions

Enterthe Alternative Case # t o be Reviewed i n th is Spreadsheet:

In-Service March 2004 1

Case # In-Service March 2004 0 High Market Prlce Case 1 Low Market Price Case 2 High Hydro -Low Price Case 3 Low Hydro - High Price Case 4

Economic Assumptions

Annual rate of N a Inflation k De-escalation: Rwenue Annual rate of Net Inflation & De-escalation: Cost of Annual rate of Net Inflation & De-escalation: OMA Annual rate of Net Inflation & Deacalation. Capital

Consmction begins in Fiscal Yeaf Ending March In-Servicc Month ( April is I. March is I t ) in-Service Year: Fiscal Year Ending March: Economic Life of Asset First Year of Benefiu End of Useful Life: Fiscal Year ~nd ing March: Discount Rae: Real

Discount Rate: Nominal

USS Exchange Rate

Benefit Related Assumptions

VOE HLH Annualized RwmueBenetiu: REAL f VOE LLH Annualized Rcvenue Benetlu: REAL f VOE Annualized Dispatchability Premium: REAL S Dispatchability Premiums as a % of e l d c i t y rwenua

Change in Base Case Lcvelircd Price Per MWh

Generation impacts fo; the Forward Price C ~ W C : - Heavy Load Net H L H Light Load Net L L H

GW.h Regional GW.h Regional

April

May - June -

July

wfi Itember

xtober November December January February March Total Annual incmnentrl Gncrr t io

Peak Loss Adjustment Factor

Project Cost Assumptiool

Water Capacity Fee Water Rmtal Rate W h

Facility OMA Taxa & Granu Annual Proxy used in VOE for Corporation Capital Taxa Incrementai Annual OMA Expmdinrra Overhead charged IO capital Available Capacity ClFT Cosu m LM: Transmission Capital Rate on Capacity Revmue G~ant. Taxa in Lieu and Property Tax Rate Corporation Capital Tax Combined tax rate Capilal financed through debt (for CCT)

IM) 102 104 106 108

Generat~on Cap~tal Cash Flows Real 5 75,8581 01 3001 7,9071 27,6201 30.2661 4491 01 01 01 01 0

79,196 7.782 1,835 8.068 28,783 32,239 189

Conu~but~ons ~n atd (CIA) I 01 01 01 O l 01 01 01 01 01 01 0

~ V O E HLH Revenues Is6.611. VOE HLH Revenues VOE Dispatchability & Reserve Premiums Dispatchability & Reserve Premiums as a % of Revenues 12.459.

Generation: Heavy Load Light Load GW.h GW.h

April

May June July August September October November December January February March Total Annual Incremental Gnera t io 200 102

VOE Levelized Base Casc Price VOE ~evelizcd knsitivity Price -1

l ~ r i c e Chanp: 0 . W

Heavy Load Light Load GW.h GW.h

"Y August September October November December

January Fcbwry March Total Annual Incremental Generatio 200 102

VOE Levelized Base Case Pricc VOE Lwelized sensitivity price -1

r" Price Change: 5.71%

VOE HLH Revenues VOE HLH Revenues VOE Dispatchability & RerervePremiums Dispatchability & Reserve Premiums as a % o f Revenues 7 769.

I Generation: Heavy Load Light Load

GW.h GW.h

April

May Junc July August September October November December January February

-ch \I Annual Incremental Gacra t io 347 163

Price Change: -15.71%

Seven Mile Financial Evaluation

VOE HLH Revenues VOE HLH Revenues VOE Dispatchability & Reserve Premiums Dispatchability & Reserve Premiums as a % o f Rwenues 12.58%

Key Assumptions

In-Service March

Heavy Load Light Load GW.h GW.h

April

May Junc July August September October November December January Febmary March T o n 1 Annud Incrcmmtal Generation 102

VOE Lwelized Basc Case Price VOE Lwcl izd Sensitivity Pricc

Price Change: -5.71%

Low Hydro Sensitivity Caw: Y( - ~ V O E HLH Revenues I S,Y

I VOE HLH Rwenues VOE Dispatchability & Reserve Premiums Dispatchability & Reserve Premiums as a % of Revenues 18.00

I Generation: . H u v y Load t ight Load GW.h GW.h

April May Junc July August September October November December January February March Total Annual lncrcmcntal Generation 131 70

VOE Lwelized Basc Casc Pricc VOE Levelized Sensitivity Pncc

Price Change: 25.71%

Seven Mile Financial Evaluation Key Assumptions

Seven Mile Financial Evaluation

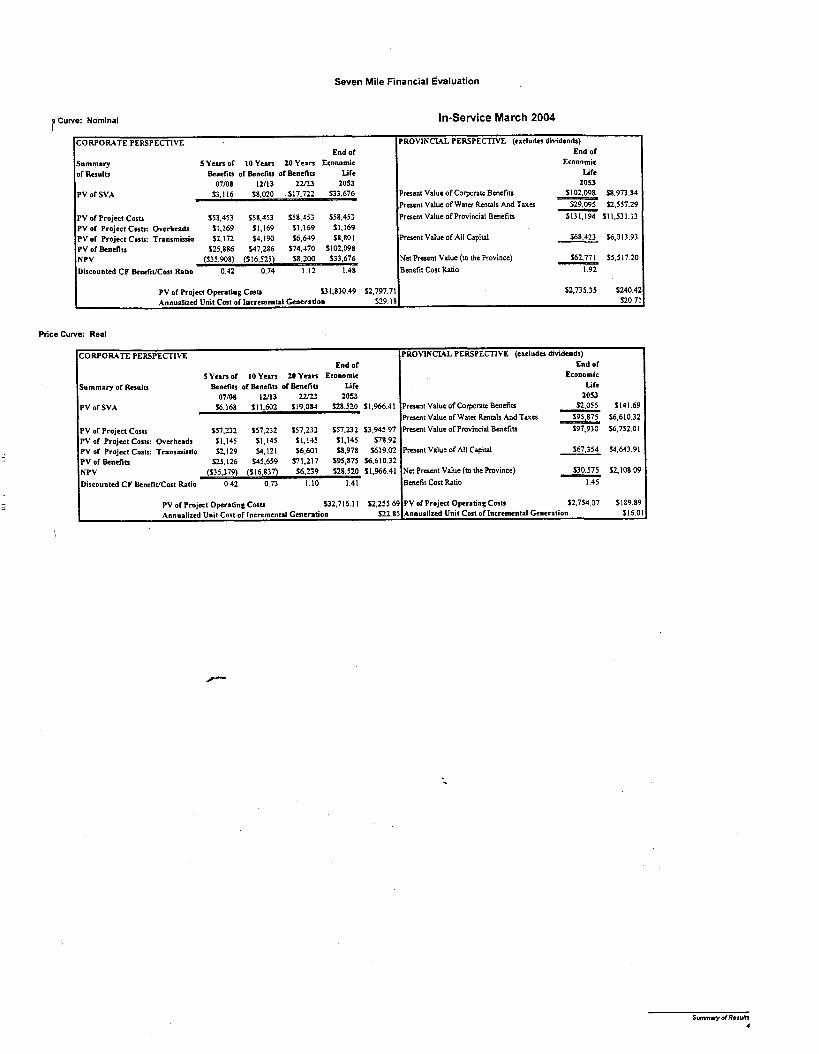

?Curve: Nominal InService March 2004

CORPORATE PERSPECTIVE End of

Summary 5 Yean of 10 Yean 20 Yean Economic of RUUIU Benefits of Benefits of Benefits Life

07/01 12/13 7.223 2053 PV of SVA 53,116 58.020 517.712 D3.676

PV of Proiect Costt 158.453 558.453 $58.453 558.453

I PV of Project Operating Costs S31.830.49 52,797.71 52,735.35 52404 Annualized Unit Cost of Incremental Generation 519.1 8 120 7

Price Curve: Real

PROVINCML PERSPECnVE (excludes dividends) End of

Economic Life

2 0 9 Present Value of Corporate Benefits - 5102.098 58.973.84

S29.095 12.557.29 Present Value of Wata Rentals And Taxes - Present Value of Provincial Benefits $131.194 511,531.13 . -~ -

PV o i Project Costs: Overheads 51.169 51.169 51.169 51.169 PV of Project Cosu: Transmissio 52. 172 %,I90 16.619 58.80 1 PV of Benefits $25.886 547,286 574.470 5102.098 NPV Discounted CF BcncfiUCost Ratio 0.42 0.74 1.12 1.48

Present Value of All Capital 568,423 16,013.93

Net Present Value (to the Province) - 162,771 55.5 17.20

Benefit Cost Ratio 1.92

I PV of SVA 56.168 51 1.602 119.081 S28.520 51.966.41 Present Value of Corporate Benefits I S2.055 5141.69 - 595.875 S6.610.32 Present Value of Wata Rentals And Taxes

PV of Project Cosu 557.232 157,232 557.31 557,232 53,945.97 Present Value of Provinsid Benefits 597.930 56.752.01

CORPORATE PERSPECTIVE End o i

S Yern of 10 Years 20 Y n n Economic Summary of Results Benefits ofklencfio of Benefits Life

07/08 12/13 22/23 2053

PROVINCIAL PERSPECTIVE (excluder dividends) End of

Economic Life

2053

I PV of Project Operating Costs 532, 716.1 1 52.255 69 PV of Project Operating C o w 52.754.07 S 189.89 Annualized Unit Cost of Incremental Generation S22.85 Annualized Unit Con of lncremenul Generation 516.01

PV of Project Costs: Overheads 51.145 51.145 5 l.l45 51.145 578.92 PV of Project Cow: Trnnsmissio 52,129 14,121 16.601 58,978 5619.02 PV of Benefits 525,126 545.659 571,217 595,875 56.610.32 NPV (S35.379) (516,837) 56.239 528,520 S1.%6.41

Discounted CP BenefiVCost b t i o 0.42 0 73 1.10 1.41

Present Value of All Capid 467.354 54,643.91

Net Present Value (to the Province) - 530,575 St. 108 09

Benefit Cost Ratio 1.45

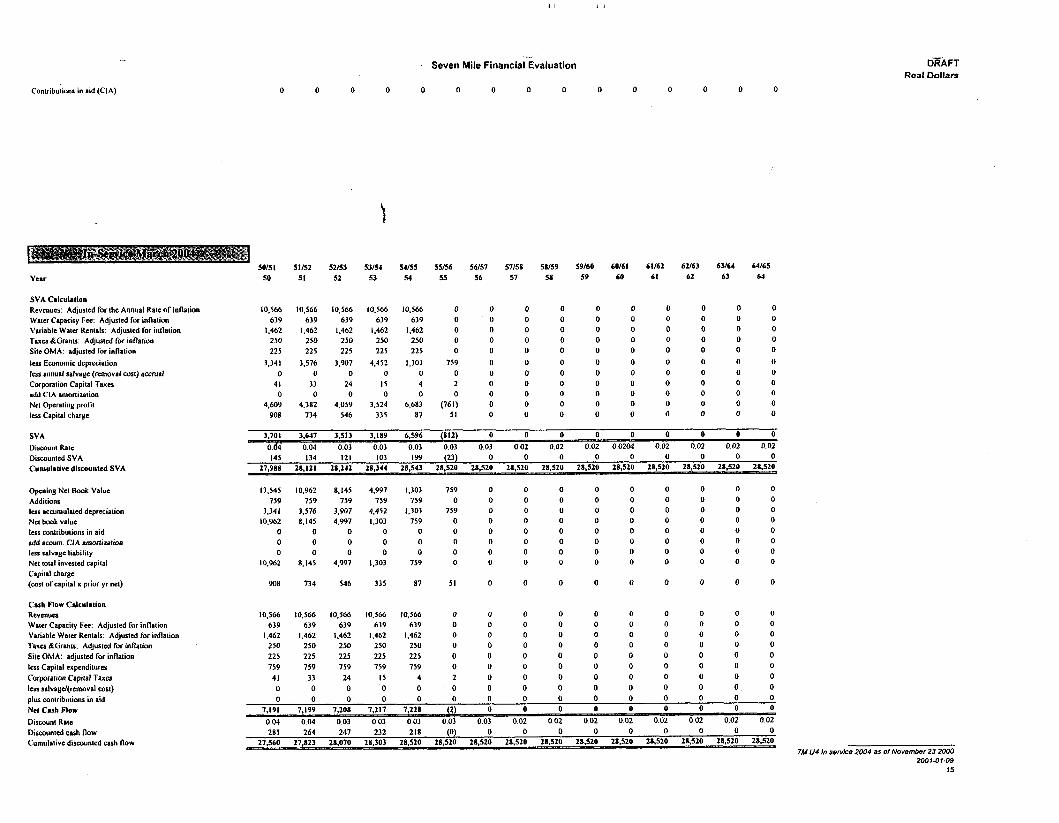

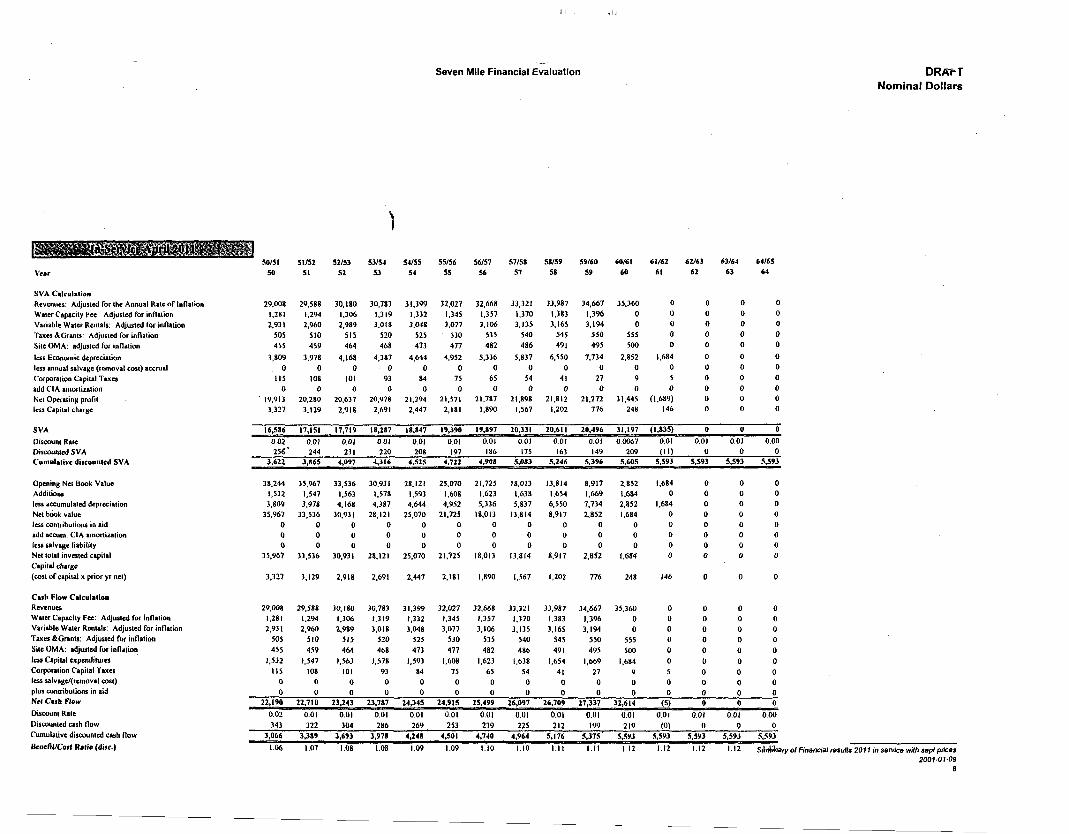

SVA Calculation Revenues: Adjusted for the Annual Rate o f Inflation Water Capacity Fee: Adjusted for inflation Variable Water Rentals: Adjusted for inflation Tares &Grants: Adjusted for inflation Site OMA: adjusted for inflation

less Ecanomic depreciation less annual salvage (removal cost) accrual Corporation Capital Taxes add CIA amonization Net Operating profit less Capital charge

SVA

Discount Rae Discounted SVA Cumula~ive discounlcd SVA

Opening Net B m k Value Additions less accumulated depreciation Nct bmk value less contributions in aid add accum. CIA amonization l a s salvage liability Net total inverted capital Capital charge (cost o f capital x prior y r ncl)

Cash Flow Calculation Revenues Water Capacity Fee Adjusted for inflation Variable Water Renals. Adjusled for inflation T u a &Grants. Adjusted for inflation Site OMA: adjusted for inflation I a s Capital expenditures Corporation Capital Taxes less salvage/(ren~oval cost) plus contributions in aid Net Cash Flow

Discount Rate Discminted cash flow Cumulative discounted c u h flow

BeneliI/CosI Ratio (disc.)

..-- Seven Mile Financial Evaluation

CORPORATE PERSPECTIVE

EII~ or 5 Years o r I 0 Vcars of 20 Years o f Econon~ic

& n t s Benclils & m i l s Wcsults to the end or Fiscal Year 07/08 12/13 22/23 2055 PV or SVA 53.1 16 58,020 117.722 $33.676

_P__-_s___

PV of Projecl Costs ' 558.453 158.453 158.453 $58.453 PV or Project Costs: Overheads $1,169 11.169 11.169 $1.169 PV of Projecl Costs: Tr rnm~iss ion 12.172 14,190 16.649 18.8OI

. - . NPV

D~SCOIIII~C~ C F BeneliUCost R b 42 074 112 148

'ROVINCIAL PERSPECTIVE (excludes dividends) End o f

Economic Life

2055 resent Value o f Corporate Bcnefiu 102,098 resent Value o f Water Rentals And Taxes 129.095 resent Value o f Pmvincial Benefits 1131,194

resent Value of A l l Capital 168.423

et Present Value (to the Province) 562,771 P

cnelit Cost Ralio 1 02

DRAFT minal Dollars

. -

Seven Mile Financial Evaluation -

DRAFT Nominal Dollars

SVA Calculation Revenuu: Adjusted Tor the Annual Rate o f Inflation Water Cnpeily Fee. Adjusted for inflalion Variable Water Rentals: Adjusted for inflalion Taxu &Grants Adjusted for inflation Site OMA: adjusted for inflation

less Economic depreciation less annual salvage (rcn~ovsl cost) accrual Corporalion Capital Taxu add CIA antonization Net Operaling profit less Capital charge

Discount Rate Discounted SVA Cuntulalivc discou~tted SVA

Openins Net Bmk Value Additions l u s accumulaad depreciation Net book value less contributions in aid add acwm. CIA amonizadon Iws salvage l iabi l i~y Net Iota1 invcstcd capital Capttsl charge (cost o f capital x prior yr net)

Cash f l ow Calculaliou Rcvenuu Water Capacity Fee Adjusled for inllation Variable Waler Rentals: Adjusled for inflalion T u u &Grants: Adjusted for inflalion Sile OMA: rdjuskd for inflalion less Capital wcpendituru Corporation Capilal Taxu less salvagd(ren~oval cost) plus contributions in aid NCI cash n o w

Discount Rale Discounted cash flow Cumulative discounted cash flow

BenefiUCost Ratio (disc.)

. - Seven Mile Financial Evaluation DEAFT

Nominal Dollars

SVA Calculation Revenues. Adjusted for the Annual Rate o f Inflation Water Capacity Fee: Adjusted for inflation Variable Water Rentals: Adjusted for inflation T u a &Grants: Adjusted for inflation Site OMA: adjusted for inflation

less Economic deprecialion less annual salvage (removal cost) accn~al Corporation Capital Taxer add CIA a~nonilr l ion Net Operating profit less Capital char~e

SVA

Discount Rate Discounted SVA Cu~uulat ivc Jisrountrd SVA

Opening Net Bmk Value Additions less accumulated depreciation N a book value l u s conuiburions i n aid add accum. CIA amonilolion I c u snlvagc liability Net total invested capital Capital charge (cost o f capital x prior yr net)

Cash Flow Calculation Revenues Waar Capacity Fee: Adjusted for inflation Variable Water Rentals: Adjusted for inflation Taxu &Grants: Adjusted for inflation Site OMA: adjusted for inflation less Capital expenditures Corporation Capital T u c r less salvagd(removal cost) plus contributions i n aid Nel Cash Flow

D i s m n t Rate Discounted cuh flow Cumulative discounted cash l low

BcneBUCosI Ralio (disc.)

-- Seven Mile Financial Evaluation DKAFT

Nominal Dollars

SVA Calculation Revenues: Adjusled for llte Annual Ralc of Inflation Water Capacity Fee: Adjusled for inflation Variable Water Rentals: Ad justd for inflalion Tax= &Grants Adjusted for inflation Site OMA: adjusted for inflalion Iws Econon~ic dcprcciaion I s s annual salvage (removal cost) accrual Corporation Capttal Taxa add CIA amortization Net Operating profit less Capital charge

SVA

Discount Rate Diswunled SVA Curnulalive discouuted SVA

Opening Net B w k Value Additions less accumulated depreciation Ncl book value less conlribulions in aid add rccum CIA amortimion less salvage liability Net total invested capital Capiul charge (cost o f captlal x prior yr net)

Cash Flow Calculation Revenues Water Capacity Fee: Adjusted for inflation Variable Water Rentals: Adjusted for inflation Taxes &Grants: Adjusted for inflation Site OhIA. adjusted for inflation less Capital expenditures Corporation Capital Taxes less salva~c/(rcnioval cost) plus cnntributions in aid Net Cash Flow

Diswunt Rate Discounled cmh flow Cu~nulative discounted cash flow

BeueWCosl Ratio (disc.)

.-- Seven Mile Financial Evaluation

- DRAFT

Real D o l l a r s

- -.

Contributions i n aid (CIA)

l ~ e s u l l s l a Ihe eud of F i r 4 Year 07/08 12/13 22/23 2055 I 2055

0 0 0 0 0 0 0 0 0 0 0 0

Ii.".;;".A. .. . - .. . ...- ~ . ... ~. - ~

56,168 51 1.602 519,084 528.520 - - - I Proenl Value of Corporate Benefits 95.875

$29.962 Present Value of Water Rentals And Taxes

CORPORATE PERSPECTIVE End or

S Years or I 0 Years or 20 Years o f Econon~ic kns f i t s knc f i t r Ucrtefils Lire

IPV of ~ r o j c c t ~ o r t s $57.232 557.232 557.232 $57.232 lpresent Value or Provincial Bellefits $125.837

PROVINCIAL PERSPECTIVE (excludes dividends) End or

Econonlic ire

I PVo f ProjeclCostr: Overheads $1,145 51.145 $1.145 $1.145 PV of Projecl Cools: Tranm~ission $2,129 $4,12 1 $6.601 58.978 I Present Value o f A l l Capital 567,354 PV or Benelils $25.126 $45.659 $71.217 595.875 NPV ) (~35.179) (516.837) 56.239 $28,520 Net Present Value (to the Province) $58.482 - - Uiscourled CF &~~efi t /Cort Ratio 0542 0.73 1.10 1.41 Benefit Cost Ratio 1.87

Year

SVA Cdculation Revenues: Adjusled for the Annual Rate o f Inflation Water Capacity Fee: Adjusted for inflalion Vnriable Water Rentals: Adjusted for inttation Taxes &Granu: Adjusted for inflation Site OMA' adjusted for inflation less Economic depreciation less annual salvage (removal cost) accrual corporation Capital Taxes add CIA amortization Net Operating profit less Capital charge

SVA Discount Rate D i s m t e d SVA Cumulative discounled SVA

Opening Net Book Value Additions less accumulated depreciation Net book value less contributions i n aid add accum CIA amortization less salvage liability Net total invested capital Capiul charge (cost o f capital x prior yr net)

Cash Flow Calculation Revenues Water Capacity Fee: Adjusted for inflation Variable Water Rentals. Adjusted for inflation Taxes &Grants: Adjusted for inflation Site OMA: adjusted for inflation less Capital expenditures Corporation Capital Taxes less salvagd(removal cost) plus wntributiona ill r i d Net Cash Now

Disuwnl Rate Disuwntcd cash flow Cumulative discounted cash flow

o o o o o o o o o (I o o o n n 7,042 7,UJ4 7,048

0.49 0.46 0.43 0 (306) (7.599) (24.768) (25.503) 6.122 6.051 5.561 5,023 4.250 3,926 3.681 3.450 3.235 3.033 0 (306) (7.865) (32.633) (58.136) (52.014) (45,963) (40.402) ( 3 5 . 3 7 9 ) ' ) (27.203) (23.522) (20.072) (16.837) (13.805) -

7M U4 In s e ~ c e 2004 as of November 23 2000

-"- Seven Mile Financial E v a l u a t i o n

Contributions i n aid (CIA)

- DRAFT

R e a l Dollars

0 0 0

SVA Calcul8lion Revenues: Adjusted for the Annual Rate of Inflation Water Capacity Fee: Adjusted for inflation Variable Water Rentals: Adjusted for inflation Tues &Grants: Adjusted for inflation Site OMA: adjusted for inflation

less Economic depreciation less annual salvage (removal wst) accrual Corporation Capital Taxes add CIA amortization Net Operating profit l a s Capital elwge

SV A

Discount Rate 1)ircounled SVA Cun~ulrt ive discounlrd SVA

Opening Net Book Value Additions less rown~ulated depreciation Net book value less wntributions i n aid add accum CIA amonization less salvye liability Net total invested capital Capital charge (cost o f capital x prior yr net)

Cash Flow Cdculal ion Revenues Water Capacity Fee. Adjusted for inflation Variable Water Rentals: Adjusted for innation Taxes k G r m u : Adjusted for inflation S ia OMA: adjusted for inflation less Capital expend~tures Corporatio~~ Capital Taxer less salva&d(re~~~avrl cost) plus con~ributiuns in aid N r t Cash Flow

Diswunl Rate Discounted cash flow Cumulative discounted cash flow

-- Seven Mile Financial E v a l u a t i o n

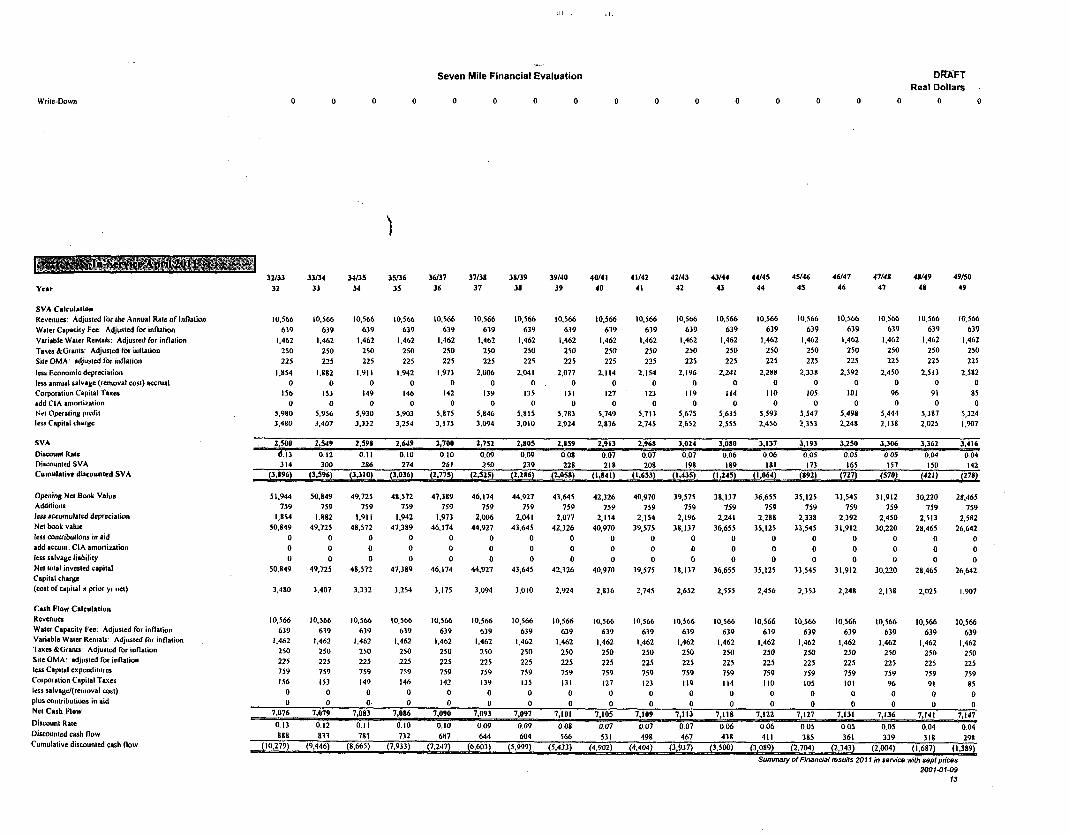

- DRAFT

R e a l D o l l a r s

Contributions in aid (CIA)

Year 32 33 34 35 36 37 38 39 40 4 I 42 43 44 45 46 47 48 49

SVA C8lcul8lion Revellua. Adjusted for the Annual Rate o f Inflation \\'ater Capacity Fee: Adjusled for inflation Variable Water Renlnls: Adjusted for inflation Taxu &Granu: Adjusted for inflation Site OMA: adjusted for inflation

less Econotnic depreciation less mnual salvage (ren~oval wst) accrual Corporalion Capital Taxes add CIA amoniulion Net Operating profit less Capital charge

SVA Discount Rate Discounled SVA Cun1ul8live discnunled SVA

Openins Nel Bmk Value Additions less accumulacd dep'reciation Net book value less contributions in aid add accunl CIA amortization less salvage liability Net total invested capital Capital charye (wst o f capital x prior yr net)

Cash Flow Calcul8lion Revenues Water Capacily Fee: Adjusted for inflation Variable Water Renlals: Adjusted for inflation Taxa &eranu: Adjusted for inflation Site OMA. adjuslcd for inflation less Capital cxpcndilures Corporation Capital Taxa l u r salvawcMrcn~oval cost) - . plus contributions in aid Net Cash Plow

Discount Rate Diswunled cash flow Cumulative discounted cash flow

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 7.101 7,104 7.108 7.112 7,116 7,120 7,124 7,129 7.133 7.138 7,143 7,148 7.154 7,159 7,165 7,171 7,177 7.184

0.13 0.12 0.11 0.10 0 0.05 0.05 0 04 0.04 891 836 784 735 689 646 606 568 533 500 469 440 412 387 363 340 319 299

18.352 19.188 19.972 20.707 21.396 22.042 22,648 23.216 23.749 24.249 24.718 ' 25,158 25.570 25.957 26.320 26.660 26.979 27,279 7M U4 In service 2004 as of November 23 2000

Contributions in aid (CIA)

-- Seven Mile Financial Evaluation DEAFT

Real Dollars

50151 51/52 52/53 53/54 54/55 55/56 56157 57/58 58/59 59160 60161 61162 62/63 63/64 64/15 Year 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64

SVA Calculation Revenues: Adjusted for the Annual Rate o f Inflation \Vater Capacity Fec: Adjusted for inflation Variable Water Rentals: Adjusted for inllation T a m &Granu: Adjusted for inflation Site OMA: adjusted for inflation

less Economic depreciation less annual salvage (removal cost) accmal Corporation Capital Taxer add CIA amortization Net Operating profit less Capital charge

SVA

Discount Rate Discounted SVA Cumulrtivc dircouutcd SVA

Opening Net Book Value Additions lus accumulated depreciation N a bmk value less contributions in aid add accum. CIA amortization l u r salvage liability Net total inverted capital Capital charge (cost o f capital x prior yr net)

Cash Flow Calculation Revenua Water Capacity Fee: Adjusted for inflation Variable Watu Rentals: Adjusted for inflation Taxa &Crane: Adjusted for inflation Site OMA: adjusted for inflation less Capital expenditures Corporation Capital Taxes less salvage/(removal cost) plus contributions in aid Net C u b Flow

Discount Rate Discounted cash flow Cumulative discounted cash flow

281 264 247 232 218 (0) 0 0 0 0 0 0 0 0 0

7M U4 In seme 2004 as of November 23 2000

8 9 10 1 1

3 , 1

18 1 March HLH 54.27 166.61 92.29 60.10 54.19 56.31 57.14 53.57 51.28 52.32 51.16 19 1 LLH 53.70 180.90 91.43 59.06 53.09 54.64 54.72 53.13 49.50 51.01 49.88

, January HLH 51.79 178.82 88.13' 59.16 52.38 54.15 53.47 52.14 48.87 50.45 49.33 LLH 48.30 181.17 82.161 51.44' 43.67' 45.82 47.33 50.07 42.86 46.15 45.13

Average

I L

13 14 15 16 + 7

20 1 Average I

7 4 I I

February HLH 53 82 171 01 91 57 59 56 53 97 56 30 55 89 53 45 49 95 51 80 50 65 LLH 53 82 181 04 91 61 59 53 53 97 5630 55 83 53 15 49 95 51 70 50 56

Average

5269 125 22 89 64 55 87 51 05 5370 5446 5245 48 33 5091 49 78

- A2 11 1OA 08 71 61 46 92 A2 51 43 79 A4 65 45 05 42 08 43 37 4240

-- A v e r a g e

L I

28 May HLH 4470 106 91 75 98 48 35 44 33 44 54 45 08 4570 41 64 42 69 41 75 29 LLH 28 71 68.76 48 93 33.49 31 51 33.20 32 82 3447 34 57 34 43' 33 67 30 Average I

32 33 34 35 36

June - HLH 4864 112 34 82 82 53 36 49 46 49 68 48 57 48 80 46 96 46 35 45 32

LLH -- 31 07 71 94 52 eo; 36 lo 32 80 33 02 34 35 33 go 33 46 33 99 33 24 Average

I -- I 37 38 39

I !

164.92 126.24 91.62, 59.63' 54.99 56.79 56.04 53.06 51.29 51.55 50.41 54 1 LLH 156.18 122.51: 89.10' 58.37. 53.16 54.89 54.01 49.08 47.87 49.11, 48.02

- July HLH 53 59 125 51 9042 5843 52 32 55 34 56 18 5274 49 01 50 65 49 52

LLH 45 82 108 59 7733 49 59 4477 45 39 46 48 45 14 41 58 41 57 40 65 -0 ] Average I

41 1 I - I 42 !

-- -- - - -- 171.62 12G5 92.68; 61.08: 55.20 57.09 56.25 53.13

LLH 144.52 125.76 90.62, 59.16' 53.40 55.50 55.36 52.28 49.29 51.02 49.89

43 44 45 46 .-,

A v e r a g e I

August HLH -- 5370 12579 9063; 5879 5311 5769 6306 5339 4932 5345 5227 LLH 48 30 112 27 81 53 50 91 45 61 46 26 46 78 47 05 41 97 43 07, 42 12

Average 8

Average 182326 311337 202121 131329 118547 123115 123949 118385 111789 115236, 112683

14684 92

63 64

62-- December HLH 170.74 132.47 99.00' 64.17: 56.76 59.10 58.24 53.59 54.29 55.36, 54.13

' LLH -- 144.44 111.70 80.66' 54.46' 47.95 48.24 50.75 43.44 44.89 46.10: 45.08

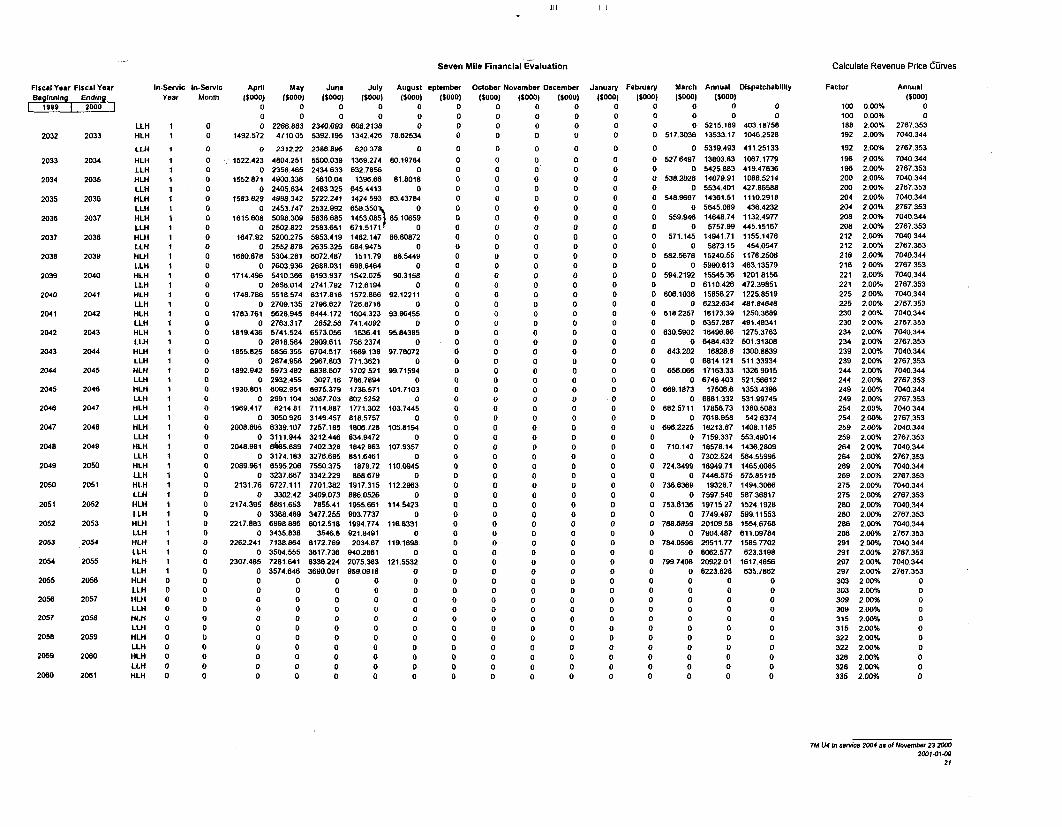

CALCULATION OF FORWARD PRICES: NOMlNAL

Fiscal Yea Fiscal Year Investment Cumlative Beginning Endlng Year I 0 I 2000 I 0

HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH LLH HLH

Inflation 100 100

LLH 142.82 19 2019 19 HLH 145.68

LLH HLH U H HLH LLH HLH LLH HLH LLH HLIi LLH HLH LLH HLH LLH HLH LLH 17069

28 '2026 26 HLH 174.10 LLH 174.10

29 2029 29 HLH 177.58 LLH 177.56

30 2030 30 HLH 181.14 LLH 161.14

31 2031 31 HLH 184.76 LLH 164.76

32 2032 32 HLH 168.45

Inflation Factor

2.00% 2 00% 2 00% 2 00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2 00% 2.00% 2.00% 2 00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2 00% 2 00% 2.00% 2.00% 2.00% 2.00% 2.00% 2 00%' ' 2 00% 2.00% 2.00% 2.00% 2.009 2 00% 2 00% 2.001 2.00% 2 00% 2.00% 2.00% 2 00% 2 00% 2.00% 2.00% 2.00% 2 00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00% 2 00% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00%

April UMWh

1 48.98 $39.67

$116.41 $ 96 07 $63.33 $67.47 $51.94 544.21 $47.46 $40.06 $49.92 $41.26 $50.63 $42 07 $48.76 $42.45 $44.93 $39.65 $47 33 $40.86 $46.27 $41.66 $49.24 $42.51 $50.22 $43.36 $51 23 $44.23 $52.25 $45.11 $53.30 $46.02 $54.38 $46 94 $55.45 $47.88 $56 56 $48.83 $57.69 $49.61 $58.64 $50.61 $60.02 $51.62 $61.22 $52.88 $62.45 $53.92 $63.69 $54.99 $64.97 $56.09 S68.27 $57.22 $67.59 $58.36 $68.95 $ 59.53 $70.32 $60.72 $71.73 $61.93 $73.17

May June UMWh UMWh

Seven

July SlMWh

150.05 543.37

$1'17.21 $102.76

104.44 173.19 954.58 W6.94 $49.42 $42 36 $51.66 $42 96 $52.47 $49.35 $49.25 $42.72 $45 77 $59.35 147.29 VJ9.04 $48.24 $40.13 $49.21 540.93 $50.19 $41.75 $51.19 $42.58 SS2.22 $43.44 153.26 w a i $54.33 $45.19 $55.41 $46.10 St6.62 $47.02 $57.65 147.96 $58.61 $48.92 $59.98 549.89 $61.16 $50.89 $62.40 551.81 $63.65 $52.95 184.93 $54.01 $66.22 $55.09 $67.55 $56.19 566.90 $57.31 570.28 $58.46 $71.68 159.63 273.12

I Mile Financial Evaluatl

August September SIMWh SIMWh

on

October SIMWh

1152.97 $146.99 1117.10 $115.30 $64.96 183.86 155.31 $54.93 $51.01 $50.03 152.68 $51.66 551.98 $50.83 $49.21 $46 19 $47.57 $45.06 $47.62 $46.22 $48.77 547.15 $49.75 $48.09 $50.75 $49.05 $51 76 $50.03 $52.80 $51.03 153.85 $52.05 $54.93 553.10 $58.03 554.16 157.15 $55.24 $58.29 556.35 $59.46 $57.47 $60.85 $58.62 561.88 $59 79 $63.10 $60.99 $64.36 $62.21 $65.64 $63.45 $66.96 164.72 566.30 $66.02 $69.66 $67.34 $71.06 $68.66 $72.46 $70.06 $73.93

November SlMWh

$157.36 $134 81 $1 16.67 $117.31 $64.99 $84.53 $58.02 $55.18 $50.62 $49 81 $52.36 $51.77 $51.59 $51.64 $48.72 $48.77 $46.62 $45.97 $48.22 $47.59 $49.18 $46.54 $50.17 $49.51 551.17 $50.50 $52.19 $51.51 $53 24 $52.54 $54.30 $53.59 $55.39 $54.67 $58.49 $55.76 $57.62 $56.87 $56.78 $58.01 $59.95 $59.17 $61.15 $60.36 $62.37 $61.56 $63.62 $62.79 $64.89 $64.05 566.19 $65.33 $67.52 $66.64 566.87 $67.97 570.24 $69.33 $71.65 $70.72 273.08 572.13 574.54

December SIMWh

1156 22 $134.59 $121.21 $ 104.06 $90.56 $75.15 $58.71 550.74 $51.93 $44.87 $54.08 544.95 $53.28 $47.28 $49.03 140.48 $49 67 $41 62 $50.65 $42.95 $51.66 $43.81 $52.70 $44.69 $53.75 $45.58 $54.63 $46.49 $55.92 547.42 $57.04 $48.37 $58.16 $49.34 $59.35 $50.32 $60.53 $5.1.33 $61.74 $52.35 $8.2.98 $5'3.40 $64.24 $54.47 $65.52 555.56 560.83 $56.67 $60.17 $57.81 $60.53 $56.96 $70.92 $60.14 $72.34 $61.35 $73.79 $62.57 $75.26 $63.62 $70.77 $65.10 $76.30

Calculate Revenue Price ~ k e s

UMWh SlMWh UMWh

$71.03 $70.44 $72.45 7M W h service 2004 as 01 November 23 2WO

- Calculate Revenue Price Curves

-

Fiscal Yea Fiscal Year Investment Year

0

33

34

35

36

37

38

39

40

41

42

43

44

45

48

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

Cumlative innation

100 100