set opportunity day04062010.pptptl.listedcompany.com/.../setopportunityday04062010.pdfmarch 2010...

TRANSCRIPT

1

POLYPLEX (THAILAND) PUBLIC COMPANY LIMITED

Friday, 4 June 2010

Presentation at the SET Opportunity Day

Website : www.polyplexthailand.com

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

2

About Polyplex group

PET film Industry

Performance Overview

Utilization of capacities

Financials

Table of contents

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Financials

Industry Comparison

Status of Projects under implementation

Business Outlook / Conclusion

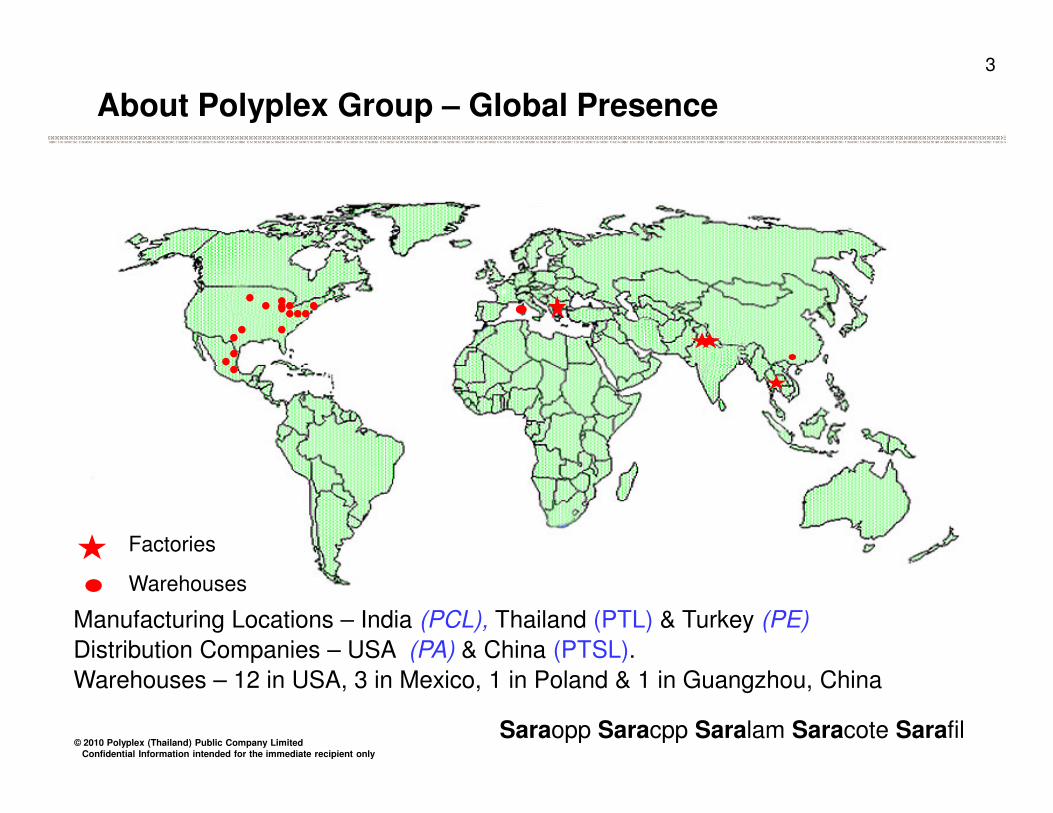

3

About Polyplex Group – Global Presence

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Manufacturing Locations – India (PCL), Thailand (PTL) & Turkey (PE)

Distribution Companies – USA (PA) & China (PTSL).

Warehouses – 12 in USA, 3 in Mexico, 1 in Poland & 1 in Guangzhou, China

Factories

Warehouses

4

• We’re a fully integrated, global manufacturer of plastic films

• Our vision is to continuously grow, create value and establish global leadership in the plastic film

business

About Polyplex Group

TurkeyTurkeyIndiaIndiaThailandThailand

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

business

• We’re moving towards establishing ourselves as a preferred packaging substrate provider as against

a PET film supplier

• We’re expanding to meet demand in new geographies and for new applications like Extrusion

lamination, Silicone Coated release films etc

• Judicious mix of On-shore, Off-shore and Near-shore strategy

• Our operational model of distributed manufacturing enables us to meet customer needs efficiently and

in a cost competitive manner

• We currently have three manufacturing locations - India, Thailand and Turkey and have distribution

set up in USA and in China

5

16.5% 53.5%

100%

30%

9.88%Polyplex (Thailand) Plc.

(PTL)General Public

Polyplex (Asia) Pte. Ltd.(PAPL)

Polyplex Corporation Ltd.(PCL)

About Polyplex Group - Structure

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

100%

100%

80.24%

9.88%

Polyplex (Americas) Inc. (PA)

Foreign Share holderPolyplex Europa Polyester Film Sanayi Ve Ticaret Anonim Sirketi

(PE)

Polyplex (Singapore) Pte. Ltd.(PSPL)

Polyplex (Trading) Shenzhen Co. Ltd. (PTSL)

100%

6

About Polyplex (Thailand) – Region wise sales break up

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Note: Above region wise break up is based on Sales Value at Polyplex (Thailand) Consolidated level

• Total sales value in 2009-10 has increased by 4% to THB 7,125 million over 2008-09.

• Share of North American market has decreased to 22% in 2009-10 as compared to 26% in the

previous year, even though the sale volume has increased by 5%, mainly on account of lower

selling price this financial year.

• Share of European markets have gone up from 34% to 38% mainly because of increased

volumes by Polyplex Europa, in the European markets.

7

About Polyplex Group –Global ranking in PET thin film

Polyplex group is the 3rd largest

producer of Thin PET films in the

world.

About 8% capacity share in PET

thin films

Significant presence & operations

in all large markets - Manufacturing

228200

151138

0

50

100

150

200

250

'000 M

T

Thin PET Films Capacity Ranking

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Polyplex Group FY Polyplex Group FY 20102010--11 11 end Capacity (PET) (MT end Capacity (PET) (MT p.ap.a))

in all large markets - Manufacturing

setup in India, Thailand & Turkey

and Marketing setup in USA and

China.

Investing in new PET line in

Thailand. The new line is expected

to commence commercial

production in FY 2012-13

Source: PCI Films ,Company Information

Location PET Film Captive PET resin Metallized PET film

India 51,000 77,600 11,800

Thailand 42,000 57,000 11,000

Turkey 58,000 57,600 11,000

POLYPLEX GROUP 151,000 192,200 33,800

� Due to attainment of high utilization levels (>100%), all attainable capacities within the group have been restated from FY 2009-10 onwards

� BOI approved capacities in Thailand remain unchanged.

Note:

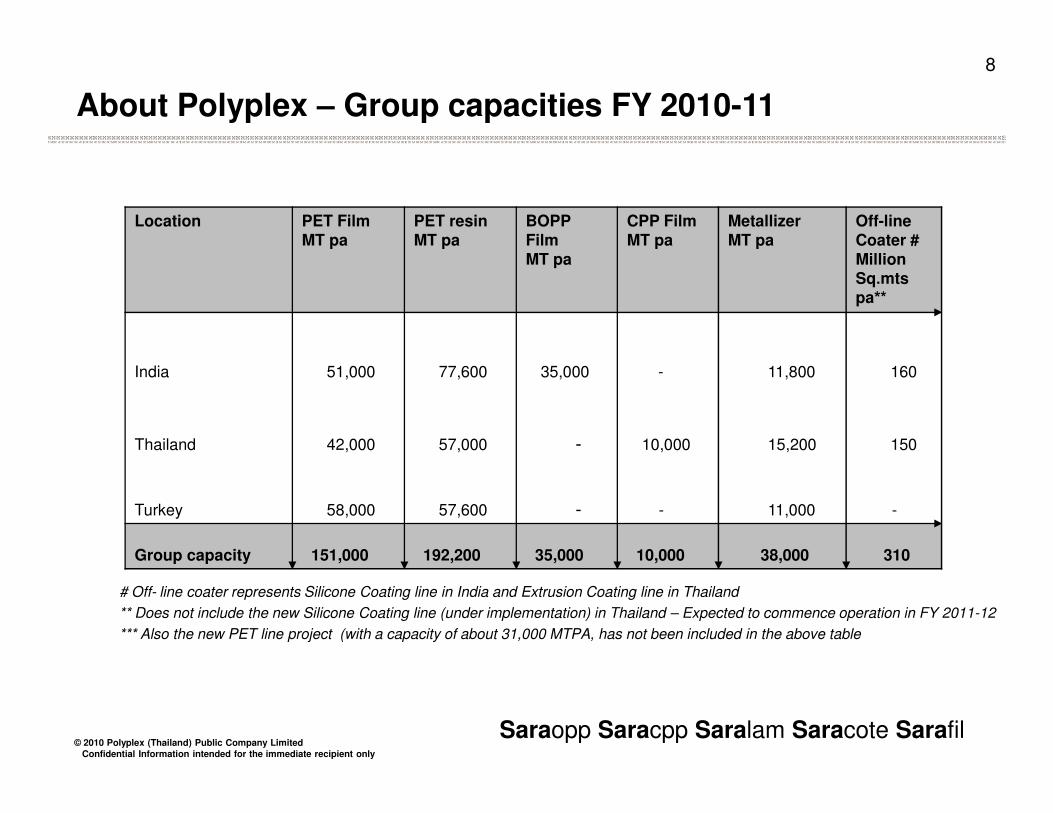

8

About Polyplex – Group capacities FY 2010-11

Location PET FilmMT pa

PET resin MT pa

BOPP FilmMT pa

CPP FilmMT pa

MetallizerMT pa

Off-line Coater # Million Sq.mtspa**

India 51,000 77,600 35,000 - 11,800 160

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

# Off- line coater represents Silicone Coating line in India and Extrusion Coating line in Thailand

** Does not include the new Silicone Coating line (under implementation) in Thailand – Expected to commence operation in FY 2011-12

*** Also the new PET line project (with a capacity of about 31,000 MTPA, has not been included in the above table

Thailand 42,000 57,000 - 10,000 15,200 150

Turkey 58,000 57,600 - - 11,000 -

Group capacity 151,000 192,200 35,000 10,000 38,000 310

9

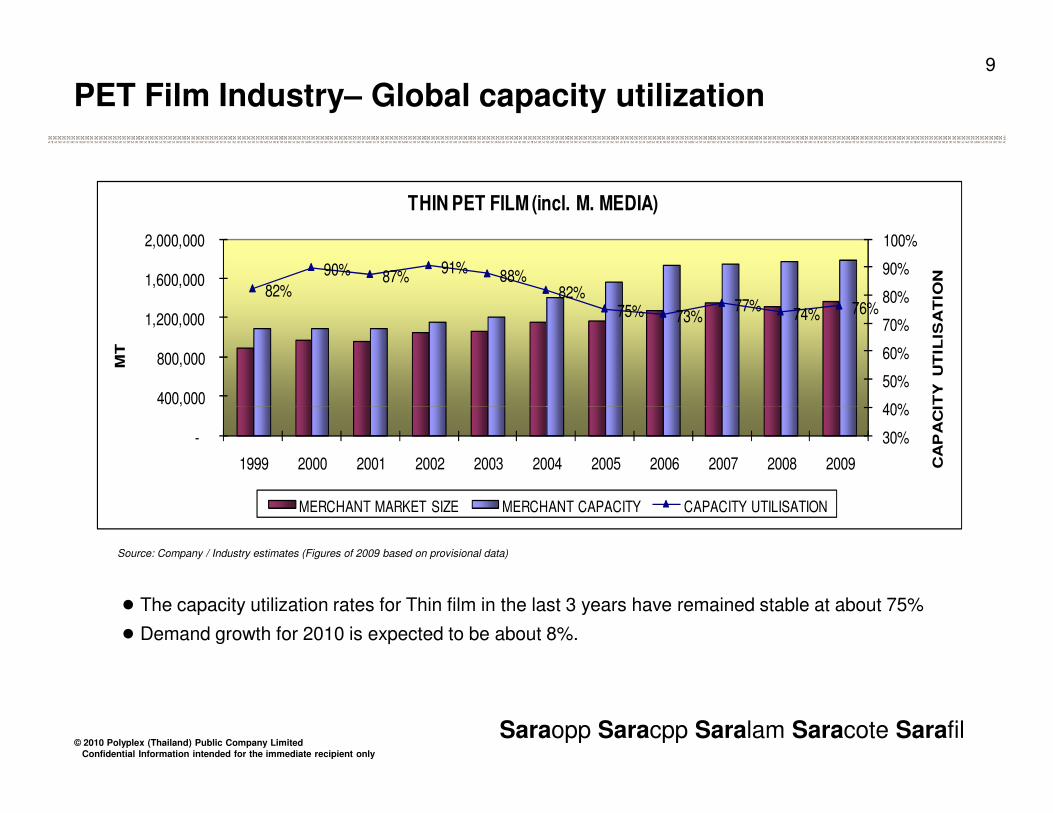

PET Film Industry– Global capacity utilization

82%

90% 87%91%

88%82%

75% 73%77%

74% 76%

40%

50%

60%

70%

80%

90%

100%

400,000

800,000

1,200,000

1,600,000

2,000,000

CA

PA

CIT

Y U

TIL

ISA

TIO

N

MT

THIN PET FILM (incl. M. MEDIA)

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

● The capacity utilization rates for Thin film in the last 3 years have remained stable at about 75%

● Demand growth for 2010 is expected to be about 8%.

Source: Company / Industry estimates (Figures of 2009 based on provisional data)

30%

40%

-

400,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 CA

PA

CIT

Y U

TIL

ISA

TIO

N

MERCHANT MARKET SIZE MERCHANT CAPACITY CAPACITY UTILISATION

10

• Packaging, Industrial and Electrical (PIE) segments – fastest growing segments with an average

growth of about 6% p.a. in the past few years. Growth in demand for 2010 is expected to be at about

8%.

• Mix of fiscal stimulus, exports, market growth and inventory adjustments are driving a recovery in the

flexible packaging segment from the lows of 2009.

• Leading film producers in developed economies like Japan, Korea etc are moving towards higher

PET Film Industry – Global trends and outlook

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

• Leading film producers in developed economies like Japan, Korea etc are moving towards higher

value added products, thereby creating a supply gap for near future in PET base film in packaging

segment.

• Addition to global capacity during the next 1-2 years is expected to be about 4%-5% per annum.

• Raw material prices are expected to remain unstable due to volatility in global crude oil prices and

fluctuations in demand

• Free Trade Agreements between various countries have thrown up opportunities as well as

challenges.

11

Performance Overview - Completion of Projects

Thailand*

Apr/ Nov

2003

Sep 2004

Feb 2005

July 2005

April 2008

PET Film – Line 1 & 2

Chip Plant –Batch /Continuous

Metallizer-1

Extrusion Coated Film Turkey*

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

May 2008 Metallizer -2

PET Film – Line 1

Metallizer - 1

Metallizer -2

Chip Plant

PET Film - Line 2

December

2005

March

2006

December

2006

May 2008

May 2008

March 2010 Cast Polypropylene Film

* Commencement of commercial production

Expected H1

FY 2011-12Silicone Coating line

12

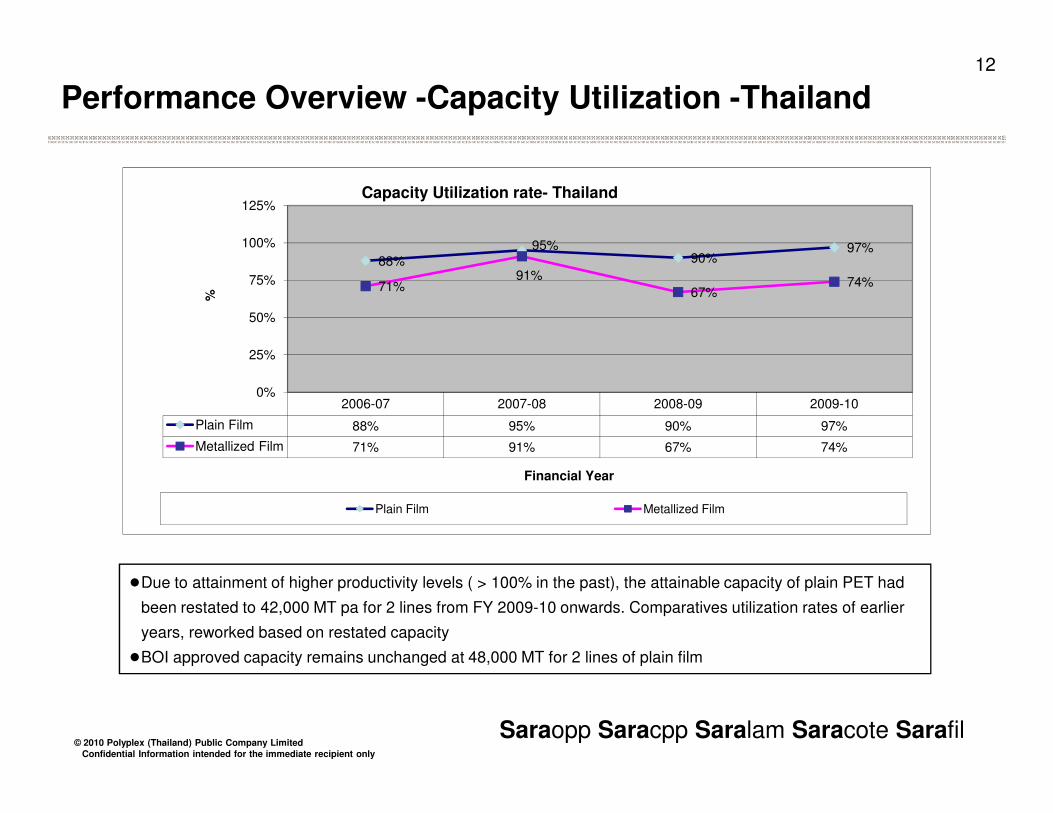

Performance Overview -Capacity Utilization -Thailand

2006-07 2007-08 2008-09 2009-10

88%95%

90%97%

71%91%

67%74%

0%

25%

50%

75%

100%

125%%

Capacity Utilization rate- Thailand

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

●Due to attainment of higher productivity levels ( > 100% in the past), the attainable capacity of plain PET had

been restated to 42,000 MT pa for 2 lines from FY 2009-10 onwards. Comparatives utilization rates of earlier

years, reworked based on restated capacity

●BOI approved capacity remains unchanged at 48,000 MT for 2 lines of plain film

2006-07 2007-08 2008-09 2009-10

Plain Film 88% 95% 90% 97%

Metallized Film 71% 91% 67% 74%

Financial Year

Plain Film Metallized Film

13

Performance Overview -Capacity Utilization – Turkey

2006-07 2007-08 2008-09 2009-10

Plain Film 81% 92% 74% 89%

81%

92%

74%

89%

50%

83%

57%

72%

0%

25%

50%

75%

100%%

Capacity Utilization rate- Turkey

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Plain Film 81% 92% 74% 89%

Metallized Film 50% 83% 57% 72%

Financial Year

Plain Film Metallized Film

●Due to attainment of higher productivity levels ( > 100% in the past), the attainable capacity had been restated

to 58,000 MT pa for 2 lines from FY 2009-10 onwards. Comparatives utilization rates of earlier years, reworked

based on restated capacity

●In FY 2009-10, Turkey has been able to ramp up utilization levels of the 2nd film line which started commercial

production in May 2008

14

20%

40%

60%

80%

100% Started operation in Thailand

with manufacture of only

commodity films

Within 2 years, set up a

capacity for manufacturing

value added metallized film

Share of value added

products will increase along

Performance Overview –Shift in sales mix

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

0%

Plain Film Value added film*

Plain Film 81% 75% 71% 63% 62%

Value added film* 19% 25% 29% 37% 38%

2005-06 2006-07 2007-08 2008-09 2009-10

products will increase along

with increase in utilization

rates of second Metallized

film line and Extrusion coated

film line

Helps business to de-risk

from cyclical industry

movements* Value added films include Chemically Coated films, Metallized Film and Thermal

Laminated film which have higher value addition as compared with normal plain film.

Note: Above data is for PTL (standalone) based on Sales quantity

15

Performance Overview –PTL PET film VA trends

0.83

1.05

1.18

1.63 1.65 1.70

1.53

1.23 1.24

1.39 1.36

0.85

1.10

1.35

1.60

$/K

g

VA trends -Plain & Met. Film

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

VA levels in 2009-10 have returned to normal levels, from the abnormal levels seen in Q2 & Q3

of 2008-09

Q1 2008-09 Q2 2008-09 Q3 2008-09 Q4 2008-09 Q1 2009-10 Q2 2009-10 Q3 2009-10 Q4 2009-10

Plain Film $ /Kg 0.83 1.05 1.18 0.79 0.65 0.67 0.78 0.74

Met.Film $ /Kg 1.63 1.65 1.70 1.53 1.23 1.24 1.39 1.36

0.83 0.79

0.65 0.67

0.78 0.74

0.60

0.85

16

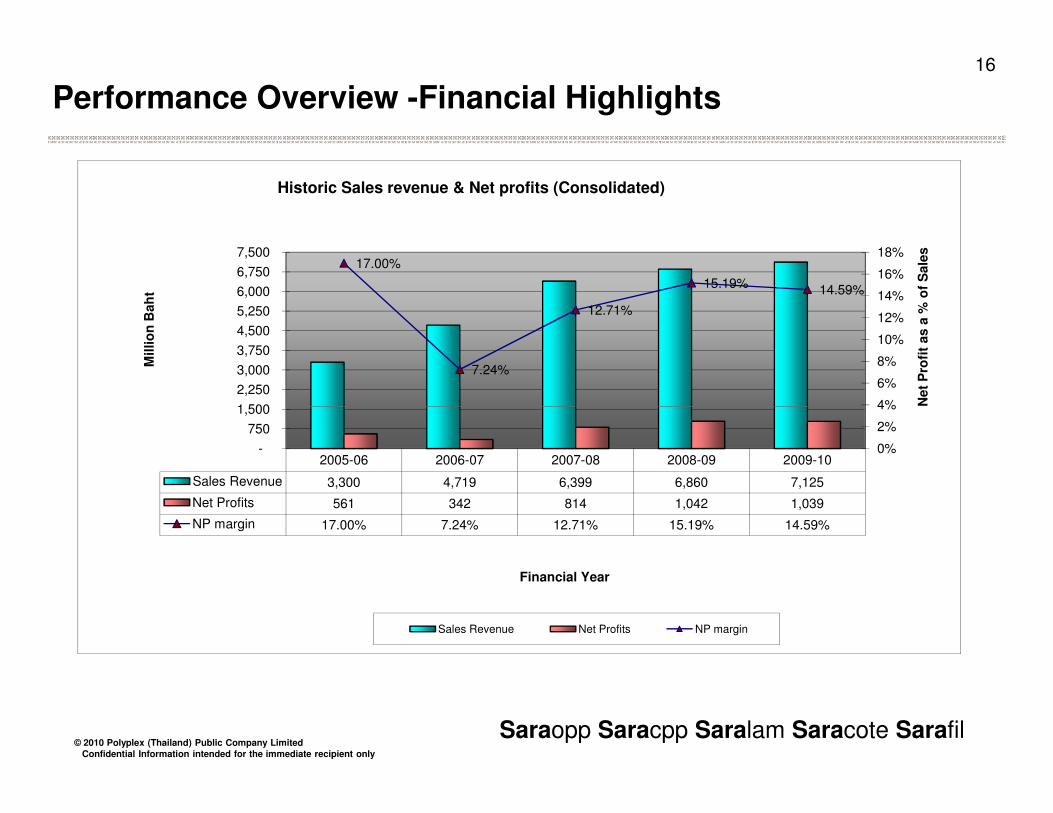

Performance Overview -Financial Highlights

17.00%

7.24%

12.71%

15.19% 14.59%

4%

6%

8%

10%

12%

14%

16%

18%

1,500

2,250

3,000

3,750

4,500

5,250

6,000

6,750

7,500

Net

Pro

fit

as a

% o

f S

ale

s

Millio

n B

ah

t

Historic Sales revenue & Net profits (Consolidated)

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

2005-06 2006-07 2007-08 2008-09 2009-10

Sales Revenue 3,300 4,719 6,399 6,860 7,125

Net Profits 561 342 814 1,042 1,039

NP margin 17.00% 7.24% 12.71% 15.19% 14.59%

0%

2%

4%

-

750

1,500

Financial Year

Sales Revenue Net Profits NP margin

17

• Increase in consolidated sales revenue in 2009-10 by about 3.86%, mainly due to

additional volumes coming from better capacity utilizations in Turkey as well as

in Thailand.

• Revenue growth would have been higher, but for the lower selling prices in 2009-

10 over 2008-09, especially in the first half of 2009-10

• Consolidated Net profits for 2009-10 have marginally decreased by 0.25% over

Performance Overview - Profitability (Consolidated)

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

• Consolidated Net profits for 2009-10 have marginally decreased by 0.25% over

previous year.

• Exchange gain of Bt 63 million as against an exchange gain of Bt 128 million last

year (lower by Bt 65 million) has also contributed in lower Net profits on a

consolidated basis

• Cost of sales 2009-10 as compared with 2008-09 has increased to 75.7% from

73.75%, mainly due to decrease in selling prices in 2009-10 as compared to 2008-

09.

18

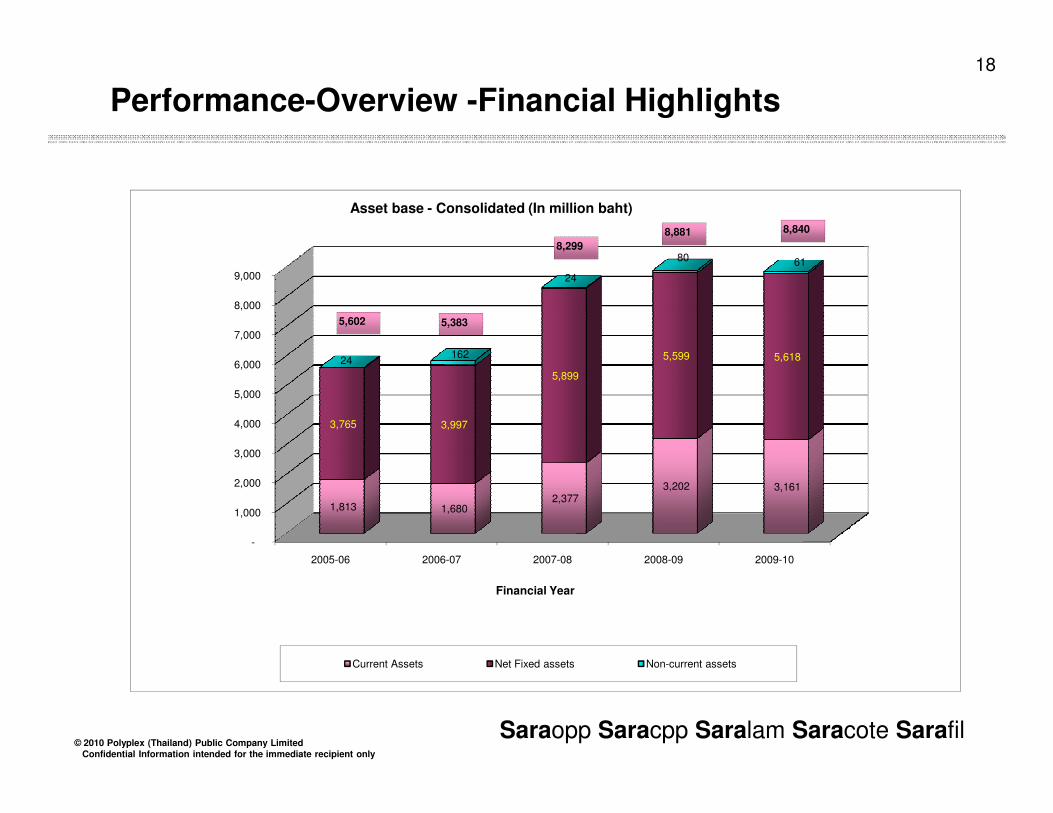

Performance-Overview -Financial Highlights

5,000

6,000

7,000

8,000

9,000

5,899

5,599 5,618 24 162

24

80 61

Asset base - Consolidated (In million baht)

8,881

8,299

5,3835,602

8,840

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

-

1,000

2,000

3,000

4,000

2005-06 2006-07 2007-08 2008-09 2009-10

1,813 1,680 2,377

3,202 3,161

3,765 3,997

Financial Year

Current Assets Net Fixed assets Non-current assets

19

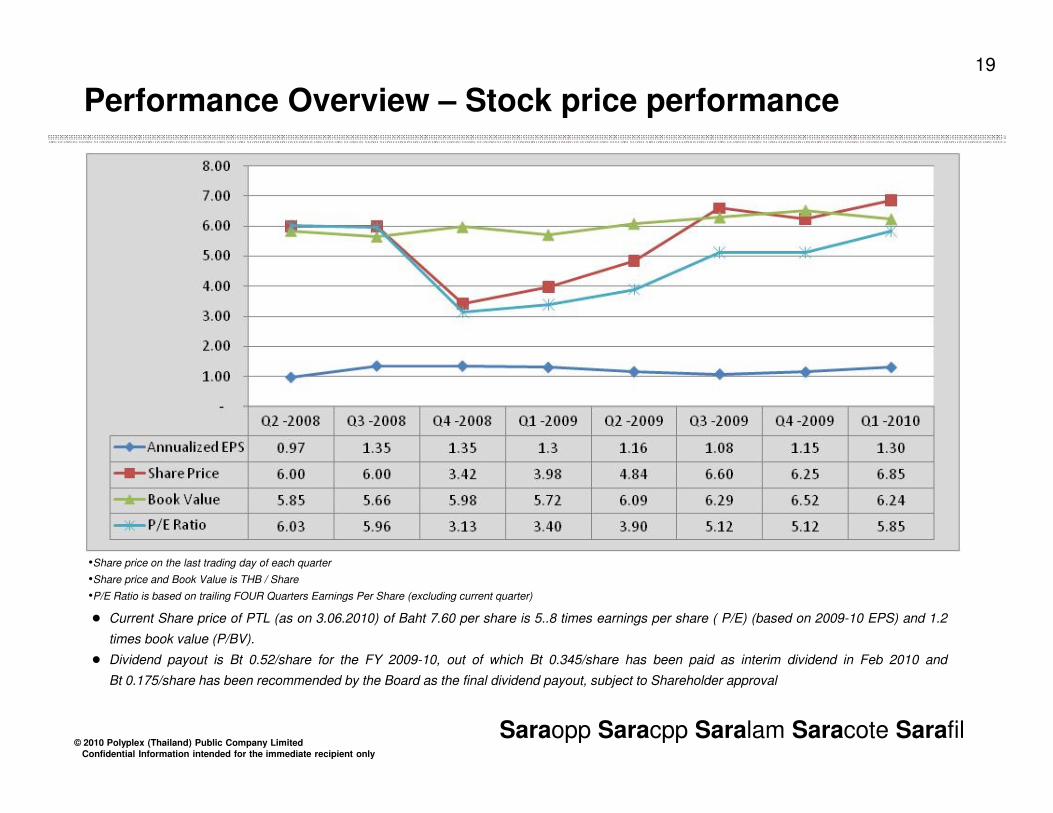

Performance Overview – Stock price performance

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

● Current Share price of PTL (as on 3.06.2010) of Baht 7.60 per share is 5..8 times earnings per share ( P/E) (based on 2009-10 EPS) and 1.2

times book value (P/BV).

● Dividend payout is Bt 0.52/share for the FY 2009-10, out of which Bt 0.345/share has been paid as interim dividend in Feb 2010 and

Bt 0.175/share has been recommended by the Board as the final dividend payout, subject to Shareholder approval

•Share price on the last trading day of each quarter

•Share price and Book Value is THB / Share

•P/E Ratio is based on trailing FOUR Quarters Earnings Per Share (excluding current quarter)

Performance

13.43% 6.29% -(3.88)%

7.42% 5.95% -(3.29)%

11.29% 19.15% -(10.74)%

18.29% 14.49% 5.44%

Net Profit Margin

ROA

ROE

EBITDA Margin

PTL*(FY 2009-10)

AJ*(FY 2009)**

TFI*(FY 2009)

Industry Comparison –Financial highlights

22

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Financial Position

1.45 0.55 0.45

0.52 2.32 2.05

12.46 4.11 0.02

2.64 1.17 0.97

Current Ratio

Debt to Equity

Interest Coverage Ratio

DSCR

Note : Interest Coverage Ratio = EBIT / InterestDSCR = EBITDA / (Interest + Current Portion of Long Term Loan)

*From SET filings (unconsolidated)**Includes income from scrap sale – 53.8 Million baht

21

Projects under Implementation Projects under Implementation –– Silicone Coating lineSilicone Coating line

• New investment approved by the board on May 26th 2009

• Investment size – USD 22 million, including working capital.

• Location –Thailand

• Target markets – Europe, US and Asia

• Applications – Used as a release liner for Label liners, graphic arts, medicalliners and Shingle Tapes

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

liners and Shingle Tapes

• Capacity – Dependant on the product mix being run on the line and can varysignificantly across different product types – 200 million sq.mts to 600 millionsq.mts

• Financial closure achieved.

• Ordering of main equipments completed

• Tender for civil work being floated.

• Expected to be operational in H1 of 2011-12.

22

Business Outlook / Conclusion

• Current global supply and demand situation, is likely to be in favor of PET filmsuppliers.

• The demand in flexible packaging segment in South-East Asia region isexpected to grow at10%-12% p.a.

• New PET line investment of Polyplex, which was earlier kept on hold, hasbeen revived, to capture the growth potential of the region as well as cater to thein-house requirement.

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

in-house requirement.

• Raw material and Currency fluctuation will impact the profitability of thecompany.

• Concentric diversification into CPP and other value added products like Thermallamination and Silicone coated films will help to de-risk the business from cyclicalnature of PET film industry.

23

Polyplex Polyplex (Thailand) Plc.(Thailand) Plc.

Polyplex Polyplex (Thailand) Plc.(Thailand) Plc.

Questions & Answers

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Questions & Answers

24

Polyplex Polyplex (Thailand) Plc.(Thailand) Plc.

Polyplex Polyplex (Thailand) Plc.(Thailand) Plc.

The views expressed here contain information derived from publicly available sources that have notbeen independently verified. No representation or warranty is made as to the accuracy,completeness or reliability of the information. Any forward looking information in this presentationhas been prepared on the basis of a number of assumptions which may prove to be incorrect. Thispresentation should not be relied upon as a recommendation or forecast by Polyplex (Thailand)Public Co., Ltd. Nothing in this release should be construed as either an offer to sell or a solicitation

© 2010 Polyplex (Thailand) Public Company Limited

Confidential Information intended for the immediate recipient only

Saraopp Saracpp Saralam Saracote Sarafil

Disclaimer

Public Co., Ltd. Nothing in this release should be construed as either an offer to sell or a solicitationto buy or sell shares in any jurisdiction.