session title - sap controlling conference 2017 · pdf fileusing sap templates for activity...

TRANSCRIPT

8/28/2015

1

© 2015 ERP Corp. All rights reserved.

Using SAP Templates For

Activity Allocation In CO

Martin Munzel

Espresso tutorials

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Introduction - Martin Munzel

• 2 years at Siemens

• 3 years at Capgemini

• 2 years at Tech Data

• 6 years at Sartorius

• Founded Espresso Tutorials in 2011 (Publishing / Consulting)

3

8/28/2015

2

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Topics

• Introduction – Why use templates?

• Using templates

• Formula planning

• Customizing

• Summary

4

Start of first section:

List the main points in your presentation and insert this slide at

the start of each new topic. Move the highlighted box down for

each new section. This divides your presentation into easy to

follow sections.

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Automatic Allocation Functions in SAP CO

• Activity Allocation

• Indirect Activity Allocation

• Templates

5

• Cost Allocation

• Periodic Reposting

• Distribution

• Assessment

• Templates can be used to automatically allocate activity

quantities during month end closing

• As senders, cost centers / activity types and business

processes can be used

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Activity Allocation in SAP CO

6

• Activities represent cost centers within an organization

performing services

• Activities can be performed by production cost centers, but

also by support cost centers

Pressing

Burning

Packaging

Maintenance

Electricity

Dust

removal

Production

Orders

8/28/2015

3

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining Activity Types and Activity Prices

Cost center

Maintenance

Cost element Plan costs

100100 430000 Wages 50,000

100100 476120 Depreciation 6,000

100100 476400 Training 4,000

Gesamt 60,000

Kostenstelle Activity type Plan qty

100100 MA00 Maintenance 6,000

Activity price = $ 60,000 / 6,000 h = $ 10 / h

You can define an activity price for every combination of cost

center and activity type

The price can be entered manually or determined by the system

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Using Activity Allocation in SAP

8

• Simplest scenario: Employees keep a time sheet and enter their

activities spent for a certain receiver manually (using

transaction KB21N or CAT2)

Cost center Any controlling object

Activity type Quantit

y

Unit

MA00 10 H

Price: $ 10

Allocation cost element

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

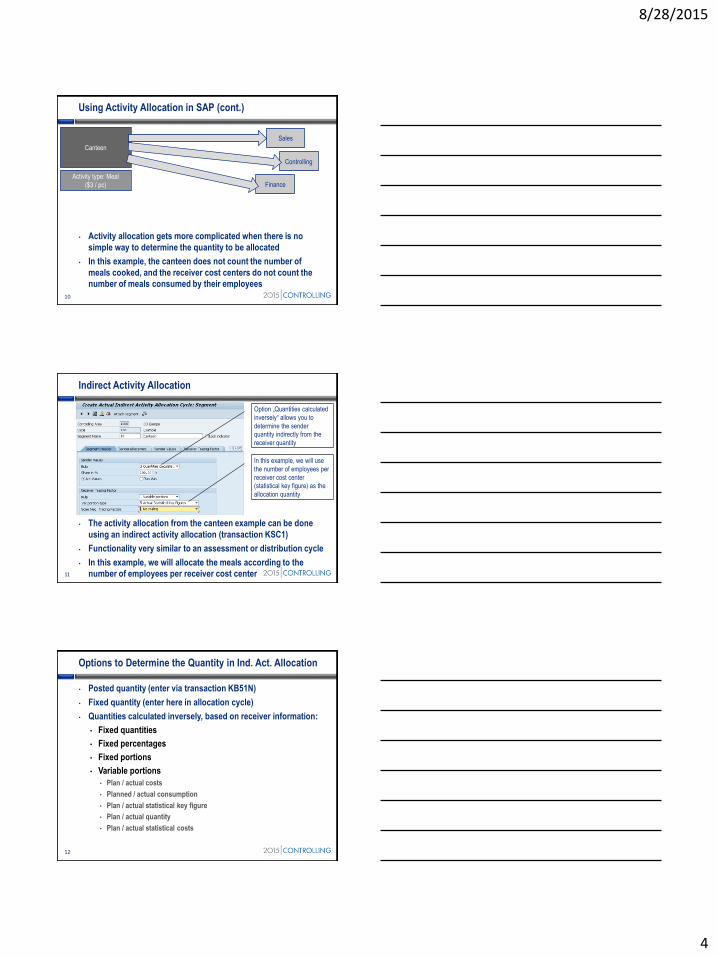

Using Activity Allocation in SAP (cont.)

9

• Common production scenario: Activities are confirmed (based

on time sheets) or backflushed (assuming that no variance

exists between planned and actual activity)

Cost center Production order

Step Work center Qty

1 Pressing 10 h

2 Burning 15 h

3 Packaging 1 h

8/28/2015

4

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Using Activity Allocation in SAP (cont.)

10

• Activity allocation gets more complicated when there is no

simple way to determine the quantity to be allocated

• In this example, the canteen does not count the number of

meals cooked, and the receiver cost centers do not count the

number of meals consumed by their employees

Canteen

Sales

Controlling

FinanceActivity type: Meal

($3 / pc)

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Indirect Activity Allocation

11

• The activity allocation from the canteen example can be done

using an indirect activity allocation (transaction KSC1)

• Functionality very similar to an assessment or distribution cycle

• In this example, we will allocate the meals according to the

number of employees per receiver cost center

Option „Quantities calculated

inversely“ allows you to

determine the sender

quantity indirectly from the

receiver quantity

In this example, we will use

the number of employees per

receiver cost center

(statistical key figure) as the

allocation quantity

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Options to Determine the Quantity in Ind. Act. Allocation

12

• Posted quantity (enter via transaction KB51N)

• Fixed quantity (enter here in allocation cycle)

• Quantities calculated inversely, based on receiver information:

• Fixed quantities

• Fixed percentages

• Fixed portions

• Variable portions

• Plan / actual costs

• Planned / actual consumption

• Plan / actual statistical key figure

• Plan / actual quantity

• Plan / actual statistical costs

8/28/2015

5

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

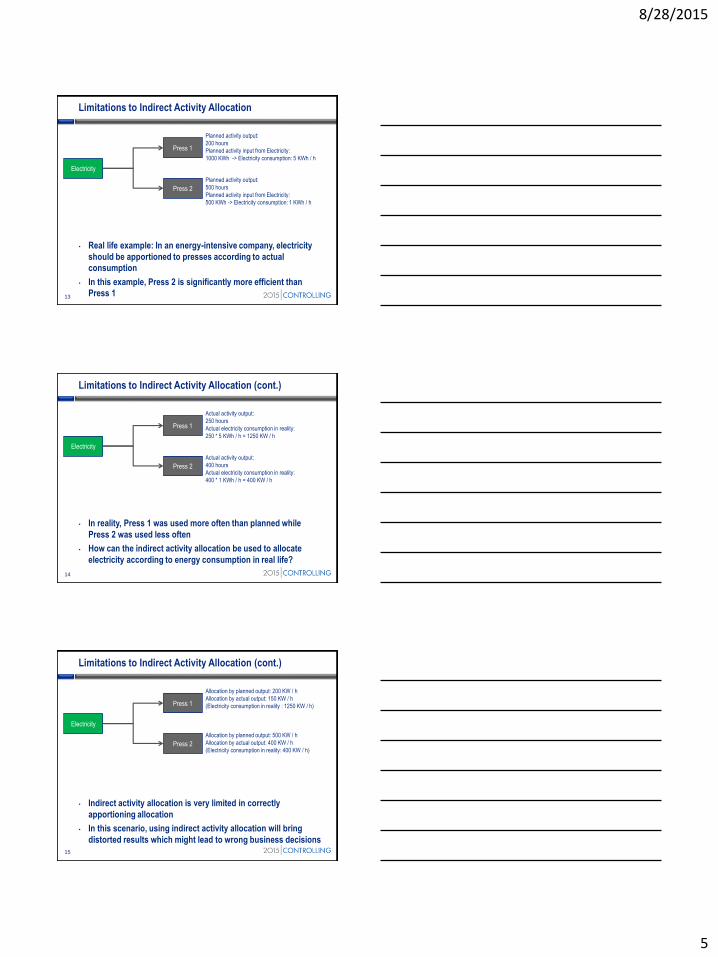

Limitations to Indirect Activity Allocation

13

• Real life example: In an energy-intensive company, electricity

should be apportioned to presses according to actual

consumption

• In this example, Press 2 is significantly more efficient than

Press 1

Press 1

Press 2

Electricity

Planned activity output:

200 hours

Planned activity input from Electricity:

1000 KWh -> Electricity consumption: 5 KWh / h

Planned activity output:

500 hours

Planned activity input from Electricity:

500 KWh -> Electricity consumption: 1 KWh / h

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Limitations to Indirect Activity Allocation (cont.)

14

• In reality, Press 1 was used more often than planned while

Press 2 was used less often

• How can the indirect activity allocation be used to allocate

electricity according to energy consumption in real life?

Press 1

Press 2

Electricity

Actual activity output:

250 hours

Actual electricity consumption in reality:

250 * 5 KWh / h = 1250 KW / h

Actual activity output:

400 hours

Actual electricity consumption in reality:

400 * 1 KWh / h = 400 KW / h

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Limitations to Indirect Activity Allocation (cont.)

15

• Indirect activity allocation is very limited in correctly

apportioning allocation

• In this scenario, using indirect activity allocation will bring

distorted results which might lead to wrong business decisions

Press 1

Press 2

Electricity

Allocation by planned output: 200 KW / h

Allocation by actual output: 150 KW / h

(Electricity consumption in reality : 1250 KW / h)

Allocation by planned output: 500 KW / h

Allocation by actual output: 400 KW / h

(Electricity consumption in reality: 400 KW / h)

8/28/2015

6

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

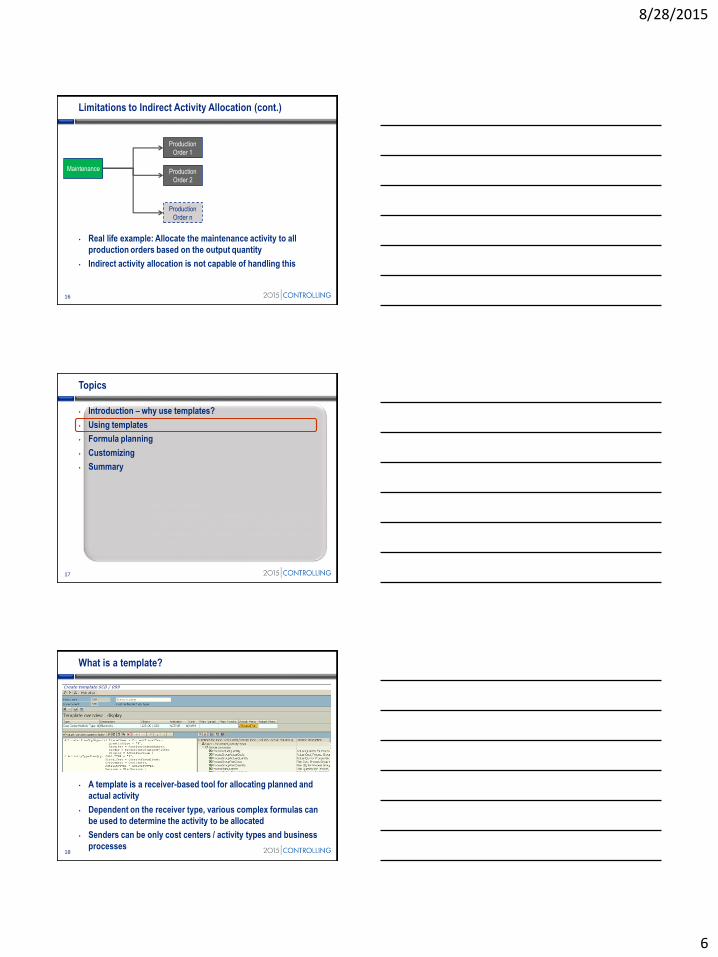

Limitations to Indirect Activity Allocation (cont.)

16

• Real life example: Allocate the maintenance activity to all

production orders based on the output quantity

• Indirect activity allocation is not capable of handling this

Production

Order 1

Production

Order 2

Maintenance

Production

Order n

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Topics

• Introduction – why use templates?

• Using templates

• Formula planning

• Customizing

• Summary

17

Start of first section:

List the main points in your presentation and insert this slide at

the start of each new topic. Move the highlighted box down for

each new section. This divides your presentation into easy to

follow sections.

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

What is a template?

18

• A template is a receiver-based tool for allocating planned and

actual activity

• Dependent on the receiver type, various complex formulas can

be used to determine the activity to be allocated

• Senders can be only cost centers / activity types and business

processes

8/28/2015

7

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

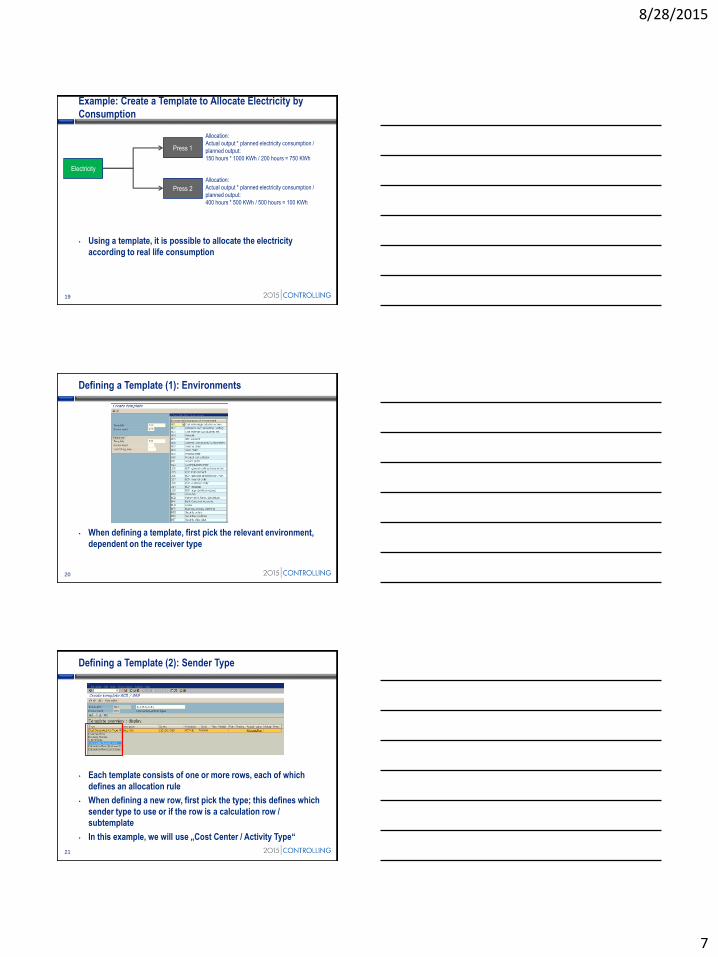

Example: Create a Template to Allocate Electricity by

Consumption

19

• Using a template, it is possible to allocate the electricity

according to real life consumption

Press 1

Press 2

Electricity

Allocation:

Actual output * planned electricity consumption /

planned output:

150 hours * 1000 KWh / 200 hours = 750 KWh

Allocation:

Actual output * planned electricity consumption /

planned output:

400 hours * 500 KWh / 500 hours = 100 KWh

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (1): Environments

20

• When defining a template, first pick the relevant environment,

dependent on the receiver type

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (2): Sender Type

21

• Each template consists of one or more rows, each of which

defines an allocation rule

• When defining a new row, first pick the type; this defines which

sender type to use or if the row is a calculation row /

subtemplate

• In this example, we will use „Cost Center / Activity Type“

8/28/2015

8

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (3): Description

22

• Description is optional; in this example, „Electricity“

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (4): Sender Object

23

• The sender object can be entered directly or be derived using

complex formulas

• In this example, the electricity cost center with corresponding

activity type is used

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (5): Activation

24

• You can activate / deactivate rows manually or determine

activation using complex formulas

• In this example, the row is always active

8/28/2015

9

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template(6): Unit of Measurement

25

• The unit of measurement is derived from the sender activity

type

• In this example, the unit is KWh

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (7): Actual allocation (variable)

26

• In the column „Actual: Variable quantity factor“, we enter a

formula to calculate the electricity received by the receiver

object

• To do this, we double-click on the data cell and then choose the

function „AllocatedPlanQtyObjects“; this will determine the

planned electricity consumption for the receiver from the

sending object

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (7): Actual allocation (variable)

27

• In the column „Actual: Variable quantity factor“, we enter a

formula to calculate the electricity received by the receiver

object.

• Any formula entered in the column „Actual: Variable quantity

factor“ will be multiplied with the actual activity output of the

receiver cost center, so we have already covered the first part of

the allocation:

• Actual output * planned electricity consumption / planned

output

8/28/2015

10

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

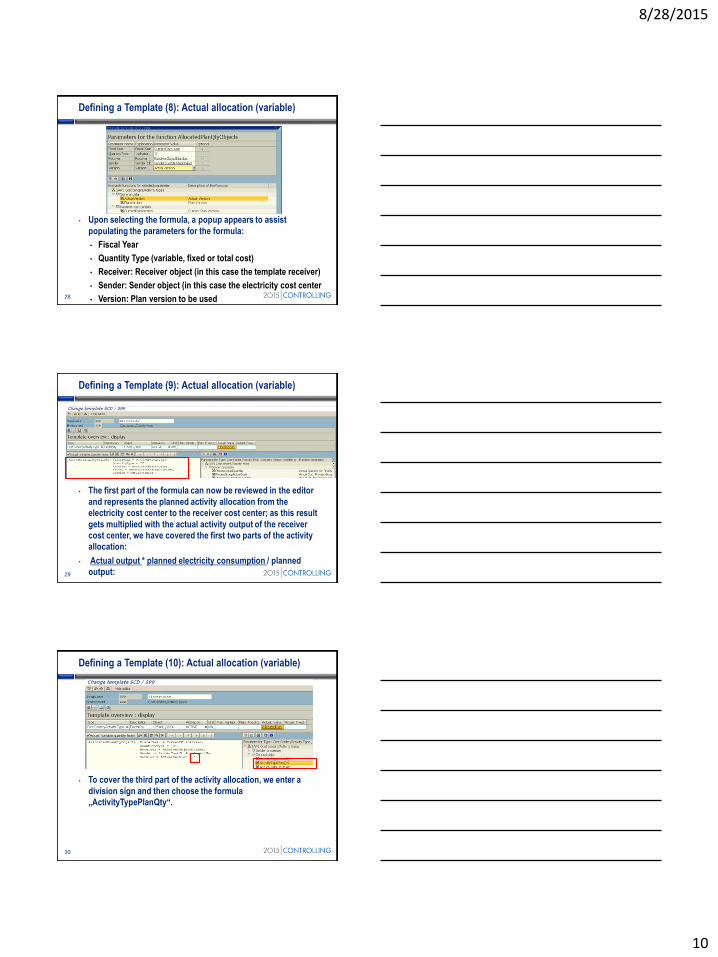

Defining a Template (8): Actual allocation (variable)

28

• Upon selecting the formula, a popup appears to assist

populating the parameters for the formula:

• Fiscal Year

• Quantity Type (variable, fixed or total cost)

• Receiver: Receiver object (in this case the template receiver)

• Sender: Sender object (in this case the electricity cost center

• Version: Plan version to be used

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (9): Actual allocation (variable)

29

• The first part of the formula can now be reviewed in the editor

and represents the planned activity allocation from the

electricity cost center to the receiver cost center; as this result

gets multiplied with the actual activity output of the receiver

cost center, we have covered the first two parts of the activity

allocation:

• Actual output * planned electricity consumption / planned

output:

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (10): Actual allocation (variable)

30

• To cover the third part of the activity allocation, we enter a

division sign and then choose the formula

„ActivityTypePlanQty“.

8/28/2015

11

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

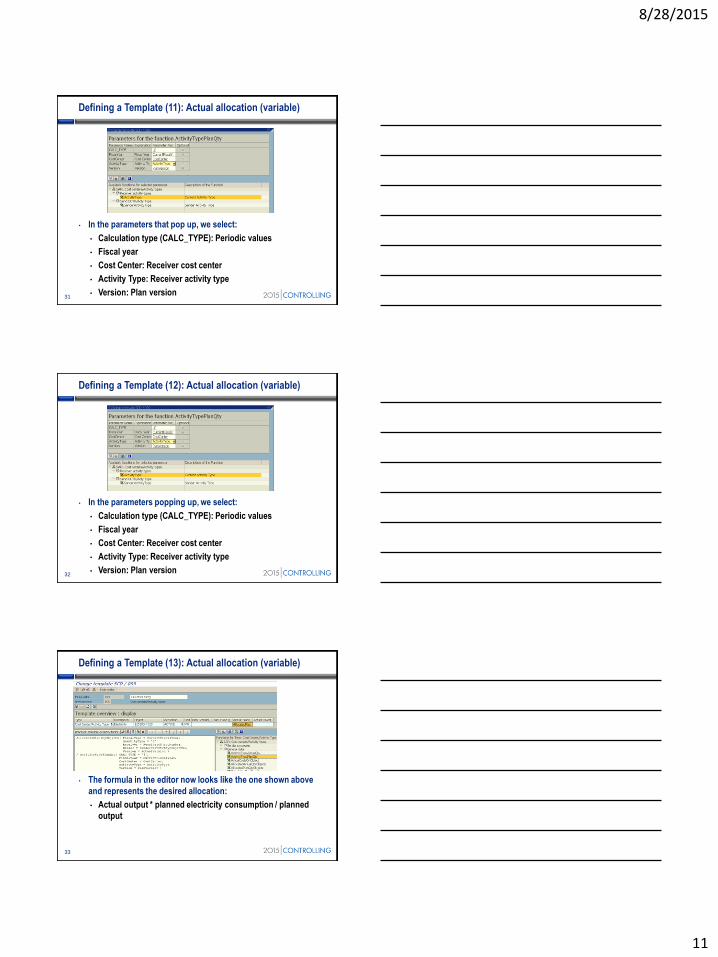

Defining a Template (11): Actual allocation (variable)

31

• In the parameters that pop up, we select:

• Calculation type (CALC_TYPE): Periodic values

• Fiscal year

• Cost Center: Receiver cost center

• Activity Type: Receiver activity type

• Version: Plan version

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (12): Actual allocation (variable)

32

• In the parameters popping up, we select:

• Calculation type (CALC_TYPE): Periodic values

• Fiscal year

• Cost Center: Receiver cost center

• Activity Type: Receiver activity type

• Version: Plan version

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Defining a Template (13): Actual allocation (variable)

33

• The formula in the editor now looks like the one shown above

and represents the desired allocation:

• Actual output * planned electricity consumption / planned

output

8/28/2015

12

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Assigning a Template to a Cost Center

34

• To use the template, we have to assign it to every receiver cost

center – in our example, the two press cost centers

• Remember that templates are receiver-oriented, so you need to

enter it for every cost center receiving activites through a

template

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Running a Template

35

• To run a template for cost centers, go to transaction KPAS,

enter the receiver cost center(s) and then execute.

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Template Result

36

• As a result, the template will allocate the figures accordingly.

8/28/2015

13

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Video: Creating and Running a Template

37

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Fixed Quantities

38

• Instead of using variable quantities (multiplied with the actual

receiver output), you can use a fixed quantity which does not

get multiplied

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Planning Template

39

• Templates can also be used for activity output planning.

Choose the corresponding columns for variable and fixed

quantities.

8/28/2015

14

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

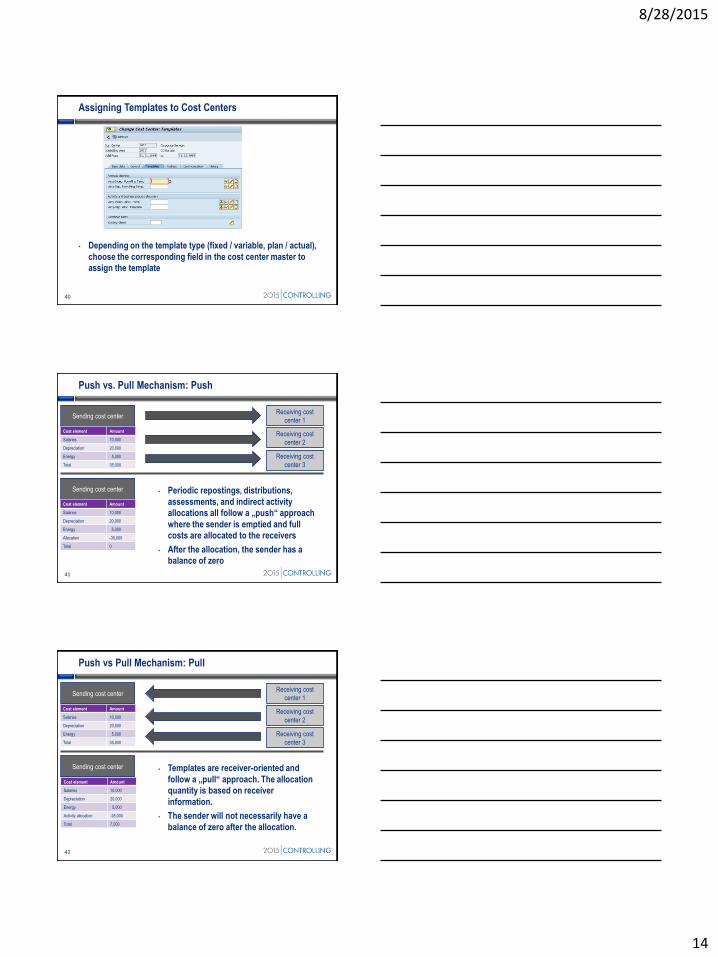

Assigning Templates to Cost Centers

40

• Depending on the template type (fixed / variable, plan / actual),

choose the corresponding field in the cost center master to

assign the template

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Push vs. Pull Mechanism: Push

41

• Periodic repostings, distributions,

assessments, and indirect activity

allocations all follow a „push“ approach

where the sender is emptied and full

costs are allocated to the receivers

• After the allocation, the sender has a

balance of zero

Sending cost centerReceiving cost

center 1

Cost element Amount

Salaries 10,000

Depreciation 20,000

Energy 5,000

Total 35,000

Receiving cost

center 3

Receiving cost

center 2

Sending cost center

Cost element Amount

Salaries 10,000

Depreciation 20,000

Energy 5,000

Allocation -35,000

Total 0

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Push vs Pull Mechanism: Pull

42

• Templates are receiver-oriented and

follow a „pull“ approach. The allocation

quantity is based on receiver

information.

• The sender will not necessarily have a

balance of zero after the allocation.

Sending cost centerReceiving cost

center 1

Receiving cost

center 3

Receiving cost

center 2

Sending cost center

Cost element Amount

Salaries 10,000

Depreciation 20,000

Energy 5,000

Total 35,000

Cost element Amount

Salaries 10,000

Depreciation 20,000

Energy 5,000

Activity allocation -28,000

Total 7,000

8/28/2015

15

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Scenario From Activity Based Costing

43

Cost center 100

Quote verification

Salaries $ 1,000

Depreciation $ 500

Buildings $ 500

-------------------------------------

Plan output 100 h

Plan price $ 20/h

-----------------------------------------

Business process 100

Sales order management

Plan output from cost center 100 $ 2,000

Plan output from cost center 200 $ 3,000

Plan output (sales orders) 200 EA

Plan price $ 25 / EA

------------------------------------------------

Profitability segment

with char. customer 1

60 sales orders

Cost center 100

Back Office

Salaries $ 2,000

Depreciation $ 700

Buildings $ 300

----------------------------------------

Plan output 200 h

Plan price $ 15/h

----------------------------------------

Profitability segment

with char. customer 2

15 sales orders

Profitability segment

with char. customer 3

75 sales orders

Consumption 15 EA

Allocation BP100 $ 1.500

-----------------------------------------

Balance $ 500

Allocation BP100 $ 2.250

-----------------------------------------

Balance $ 750

------------------------------------------------

Output from cost center 100 $ 1,500

Output from cost center 200 $ 2,250

Output to customer 1 $ 1,500

Output to customer 2 $ 375

Output to customer 3 $ 1,875

Allocation from BP 100 $ 1,600

Allocation from BP 100 $ 375

Allocation from BP 100 $ 1,875

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Topics

• Introduction – why use templates?

• Using templates

• Formula planning

• Customizing

• Summary

44

Start of first section:

List the main points in your presentation and insert this slide at

the start of each new topic. Move the highlighted box down for

each new section. This divides your presentation into easy to

follow sections.

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Formula Planning: Overview

45

• Formula planning can be used to plan primary costs

independently from activities

• Environment to be used: CPI

8/28/2015

16

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

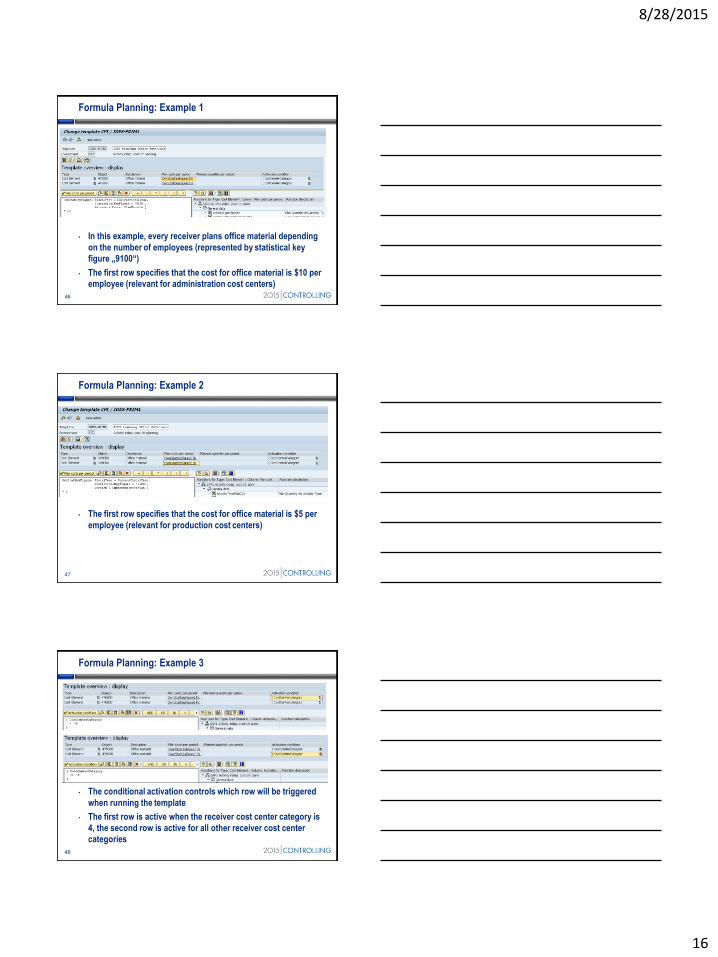

Formula Planning: Example 1

46

• In this example, every receiver plans office material depending

on the number of employees (represented by statistical key

figure „9100“)

• The first row specifies that the cost for office material is $10 per

employee (relevant for administration cost centers)

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Formula Planning: Example 2

47

• The first row specifies that the cost for office material is $5 per

employee (relevant for production cost centers)

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Formula Planning: Example 3

48

• The conditional activation controls which row will be triggered

when running the template

• The first row is active when the receiver cost center category is

4, the second row is active for all other receiver cost center

categories

8/28/2015

17

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Topics

• Introduction – why use templates?

• Using templates

• Formula planning

• Customizing

• Summary

49

Start of first section:

List the main points in your presentation and insert this slide at

the start of each new topic. Move the highlighted box down for

each new section. This divides your presentation into easy to

follow sections.

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Customizing for Templates

50

• Run transaction CTU6 for an overview of all template functions

available

• Templates are classified by environment

• For each environment, there is a function hierarchy containing

all the functions relevant for the environment

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Function Details

51

• Double-click on a function to analyze the details

• Functions are either a field reference (returning a table value) or

a function reference (using an ABAP function)

• It is possible to create your own functions

8/28/2015

18

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Topics

• Introduction – why use templates?

• Using templates

• Formula planning

• Customizing

• Summary

52

Start of first section:

List the main points in your presentation and insert this slide at

the start of each new topic. Move the highlighted box down for

each new section. This divides your presentation into easy to

follow sections.

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Resources

• Rogerio Faleiros, Configuring Controlling in SAP ERP (SAP

PRESS, 2012).

• ISBN: 978-1-59229-401-5

• https://www.sap-press.com/configuring-controlling-in-sap-

erp_2920/

• SAP Help:

• http://help.sap.com/erp2005_ehp_07/helpdata/en/ba/ed29535

87d2c3ee10000000a423f68/content.htm?frameset=/en/ed/0cd

553088f4308e10000000a174cb4/frameset.htm¤t_toc=/e

n/2e/11d553088f4308e10000000a174cb4/plain.htm&node_id=3

84&show_children=false

53

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Five Key Ideas

• Templates are complex at first glance, but are very powerful

• Templates can do things that the other allocation methods

cannot

• Templates follow a pull approach rather than push

• Formula planning is not very widely known, but can be very

useful

• With some ABAP knowledge, you can create your own template

functions

54

8/28/2015

19

R 150

G 140

B 140

R 213

G 209

B 209

R 0

G 176

B 240

R 292

G 0

B 0

R 255

G 192

B 0

R 234

G 40

B 57

R 123

G 167

B 157

R 146

G 208

B 80

R 60

G 61

B 62

R 7

G 43

B 128

Questions

• Now:

• Ask questions now for immediate answers

• Later:

55

Q&A

Disclaimer

SAP®, R/3, mySAP, mySAP.com, xApps, xApp, SAP NetWeaver®, Duet®, PartnerEdge, and other SAP® products and

services mentioned herein as well as their respective logos are trademarks or registered trademarks of SAP AG in

Germany and in several other countries all over the world. All other product and service names mentioned are the

trademarks of their respective companies. ERP Corp is neither owned nor controlled by SAP.