session 4 - kirchhoff acc gbs

TRANSCRIPT

Sponsored by

I di Ai t Pl i India : Airport Planning with a Regulatory Focus

Agenda Outline

• 1. Indian Aviation – The Growth Story• 2. Indian Airports – Key Challenges and Regulatory Overview• 3. Indian Airports – Financing Development• 4. Indian Airports – Airport Planning with a Regulatory Focus• 5. Conclusions

LeighFisher has offices in Chicago, Cincinnati, Dallas, London, New Delhi, Ottawa, the San Francisco area, and the Washington, D.C. area. For over 60 years, we have assisted our clients in achieving their vision and goals. We have extensive practical experience in all disciplines necessary for the planning and management of airports, including airfield and airspace analyses, airport management and operation, commercial and concession planning, forecasting and economics, facilities planning and design, federal funding and policy development, financial analysis and planning, financial feasibility and reporting, ground transportation planning, air quality analysis, noise and other environmental analyses, privatization, parking planning and analysis, rental car facility development and business planning, security planning and implementation, and simulation and operational analyses.

San Francisco Area Office:555 Airport Boulevard, Suite 300Burlingame, California 94010, USATelephone: (650) 579-7722Fa : (650) 343 5220Fax: (650) 343-5220E-mail: [email protected] Washington D.C. Area Office:

11730 Plaza America Drive, Suite 310Reston, Virginia 20190, USATelephone: (703) 961-9000Fax: (703) 961-9318

New Delhi:242 Okhla Industrial Estate, Phase IIINew Delhi 110 020 , INDIATelephone: 9.1.11.2684.6500

London Office:16 Connaught London W2 2ES, UKTelephone: +44.20.7087.8700Fax: +44.20.7706.7147

www.leighfisher.com

1 Indian Aviation Growth Story1. Indian Aviation – Growth Story

4

Indian Aviation – Growth Phase

160

Indian Airports Passenger Growth FY 2004 – 2011 (in mppa) Slow growth till early/mid 90sM i th i th

60

80

100

120

140 Massive growth since the advent of the LCC and liberalization of Indian skies and bilateral agreements

0

20

40

60

FY'04 FY'05 FY'06 FY'07 FY'08 FY'09 FY'10 FY'11

Dom Intl

– Grew from approx. 48mppa in FY ‘04 to approx. 143mppa in FY ‘11

– Grew from approx. 600k ATMs in FY ‘04 annually to approx.1,400k ATMs

Indian Airports ATM Growth FY 2004 – 2011 (in ‘000s of ATMs)

1 000

1,200

1,400

1,600

y pp ,in FY ‘08

– Number of scheduled airlines has increased from 4 to 14 since 2002

– Drop in FY ‘09 due to financial crisis

200

400

600

800

1,000 p

-FY'04 FY'05 FY'06 FY'07 FY'08 FY'09 FY'10 FY'11

Dom Intl

Indian Aviation – Trends

The fluctuation in oil prices and the global economic crisis have hit the market hard

– India along with China is particularly sensitive to fuel prices given state control of oil prices

Significant fall in domestic traffic in 2008 as financial crisis took its toll, however domestic traffic has recovered strongly since then

– Airlines have cut back on capacity in a big way– Kingfisher has pulled out of the LCC market– Network carriers are proceeding cautiously

Underlying growth driver the economy is expected to lead to aUnderlying growth driver, the economy, is expected to lead to a return to growth in the medium term once current market correction has passed through system

Long-term outlook remains positive Air India’s long term future needs to be resolved if Indian aviation Air India’s long-term future needs to be resolved if Indian aviation

can really progress

Indian Civil Aviation – Key Drivers

Recent policy developments have had an unprecedented effect on Indian aviation

Policy aspect Effect on Indian Aviation and Traffic

Drivers

Establishment of new airlines incl. LCCs leading to lower fares. Aviation an alternative to rail

Increased competition stimulated demand/improved products

International capacity increase - Indian carriers benefit too Domestic Deregulation and International Liberalisation (incl. Open Skies agreements)

Increased investment in Indian airports significantly improving capacity and providing ‘world-class’ infrastructure

Private Sector Investment in Indian Airports

world class infrastructure

Huge non-aeronautical revenue potential unleashed

More regulatory certainty will help

Air Traffic Improvements and AERA

More regulatory certainty will help

ATM-CNS project slated to improve airspace capacity

More air traffic controllers required urgently

India – Major Airports

Airports historically owned / managed by Airports Authority of I di (AAI) LEGENDIndia (AAI)

Privatisation timeline:– Cochin – part privatised (PPP) in 1999– Bangalore and Hyderabad – part privatised

> 20 mppa

> 10 mppa

> 5 mppa

> 2 mppa

LEGEND

Bangalore and Hyderabad part privatised (PPP) in 2002

– New Delhi and Mumbai – part privatised (PPP) in 2006

– Navi Mumbai and NOIDA– likely to be bid in

DEL

CCUAMDNavi Mumbai and NOIDA likely to be bid in 2009 – 2010 as PPP projects

– Nagpur – being developed as freight/MRO hub

– Landside of non-metro airports likely to be

HYD

BOM

Landside of non metro airports likely to be developed via PPP in next few years – (e.g., Amritsar, Ahmedabad, Udaipur)

Chennai & Kolkata (now being developed by AAI)

MAABLR

COK

GOI

developed by AAI)TVM

Traffic – Mainly at Top-6 Airportsp

• A majority of the air traffic in India is concentrated at the top 6 airportsat the top-6 airports

- Mumbai and New Delhi cater to approximately 30 mppa and about 45% of the total air traffic in India

- Chennai and Bangalore cater to over 10mppa

- Kolkata and Hyderabad are other major airports with over 5mppa

- Some smaller airports have between 1 and 5mppa incl. some with more intl. traffic than domestic (COK and TVM)

• Only four airports in India have over 100,000 annual ATMs

- Mumbai and New Delhi have over 200,000 annual ATMs

- Chennai and Bangalore have over 100,000 annual ATMs

2. Indian Airports – Key Challenges and Regulatory Overview

Regulation – Key Issues

The Airport Economic Regulatory Authority (AERA) is now expected to provide clarity on many of these issues and frame regulatorymany of these issues and frame regulatory policy for airports with over 1.5mppa. Key areas of focus include:

– Nature and quantum of tariffs and degree of cross subsidization between aeronautical andcross-subsidization between aeronautical and non-aeronautical revenues

– Addressing issues related to competition– Addressing level-of-service and quality of

infrastructureinfrastructure– Assessing the cost of delivering capacity– Ground handling policy at major airports– Issue of development fees at major airports

(private and AAI-owned)– Also, the issue of revenue share and its credited

back to the Government and whether it is a cost / tax (or equivalent thereof to the Government / taxpayer) needs to be debatedtaxpayer) needs to be debated.

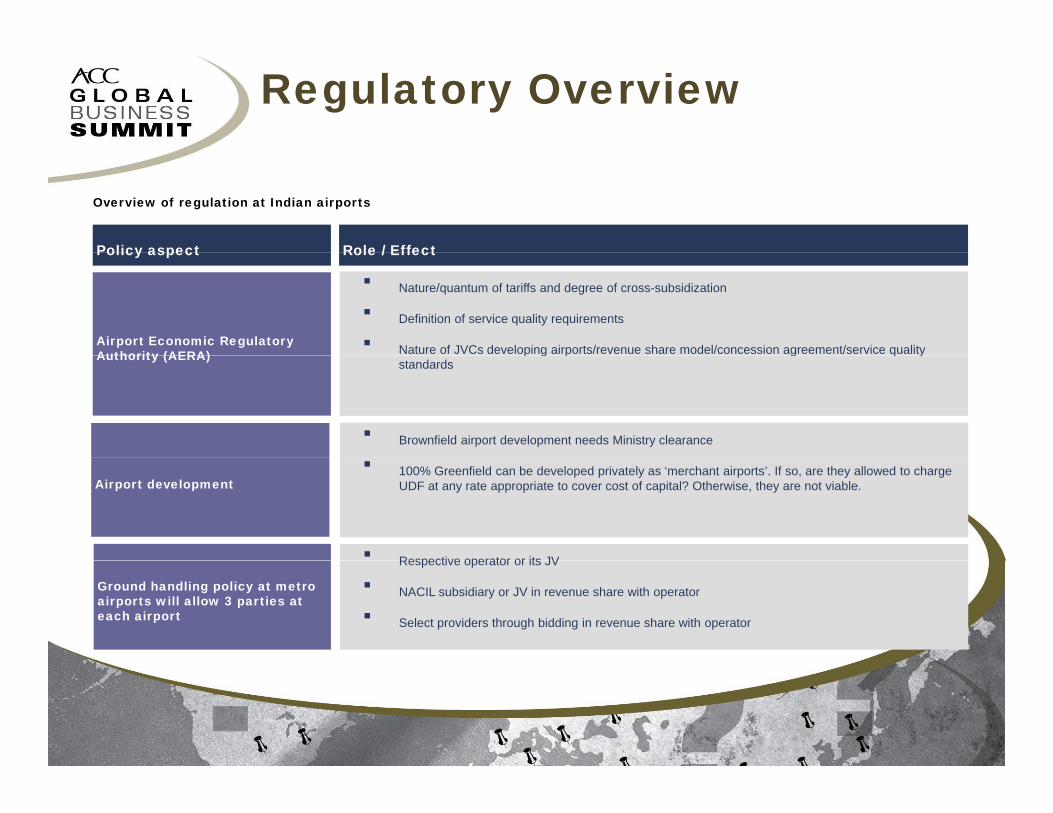

Regulatory Overview

Overview of regulation at Indian airports

Policy aspect Role / Effect

Nature/quantum of tariffs and degree of cross-subsidization

Definition of service quality requirements

Nature of JVCs developing airports/revenue share model/concession agreement/service quality Airport Economic Regulatory Authority (AERA)

Policy aspect Role / Effect

p g p g q ystandards

Authority (AERA)

Brownfield airport development needs Ministry clearance

Airport development 100% Greenfield can be developed privately as ‘merchant airports’. If so, are they allowed to charge

UDF at any rate appropriate to cover cost of capital? Otherwise, they are not viable.

Respective operator or its JV

Ground handling policy at metro airports will allow 3 parties at each airport

Respective operator or its JV

NACIL subsidiary or JV in revenue share with operator

Select providers through bidding in revenue share with operator

Regulatory Overview

Issue Effect

Overview of regulation at Indian airports (contd.)

Concession agreements are based on revenue share. In the case of New Delhi and Mumbai, the revenue share percentages are so high that the airports have to recover their cost on between 50-60% of income.

Regulatory solutions need to take project viability into account.Concession agreements and revenue share

No relation between charge and demand. Difficult to justify from a capacity / demand perspective.

Weight – related charges for landing is a poor indicator of cost

Runway use and costs are not related to weight and are related to fixed cost and opportunity cost.

Airlines want single-till; airports prefer dual-till.

Cross-subsidizing of aeronautical revenues with non-aeronautical revenues

Extent of cross-subsidization is not defined except at BOM/DEL.

What is the relevant approach? Does the same approach make sense at all airports?

3 Indian Airports Financing Development3. Indian Airports – Financing Development

Financing of Airport Projects

Two types of PPP models in India– Long-term concession model (BOM, DEL, g ( , ,

HYD, BLR etc.)– Limited concession model (city-side

development ) of non-metro airports under consideration earlier. Various models being looked at currently

Financing depends on type of concession model

Debt financingDebt financing– Recourse and non-recourse borrowing,

external commercial borrowings (ECBs) and Debt instruments such as airport bonds, preference shares etc. , p

Equity financing– Sponsors, financial investors and private

equity

Financing of Airport Projects

WACCWhat is an appropriate cost of capital and– What is an appropriate cost of capital and how is this set?

– How can this take upfront project risk into account?

Upfront deposits Upfront deposits– Sub-contracting development with upfront

payments

Securitisation– Securitisation of receivables – aero / non-

aero revenues

Special charges– User Development Fee (UDF) or Airport– User Development Fee (UDF) or Airport

Development Fee (ADF), earnings from commercial development and other charges from aeronautical facilities

4 Indian Airports Planning with a Regulatory Focus4. Indian Airports – Planning with a Regulatory Focus

Balancing Capacity with LoS

PPP process started due to needed major investment in capacity

This needs to be seen in the context of providing capacity and infrastructure and its cost to users and level-of-service (LoS) objectives

If you want ‘world-class’ infrastructure, you have to be prepared to pay ‘world-class’ prices

The airline industry viewpoint

“Quite frankly, I do not care who owns the airport. It is the cost and the service levels that matter.”

Giovanni Bisignani, Director General, IATA, April 2005

Capacity and Level-of-Service

Capacity is often a function of LoS

- A facility can operate at varying degrees of congestion and delay depending on level of service intended

Different operators and airports have different LoS standards

- Within airlines there is significant service differentiation (network vs. LCC)

- For instance, Air India vs. Air India Express, or Jet vs. JetKonnect

IATA - Levels of Service (LoS) Definitions

Flows Delays Comfort

A - Excellent Free None Excellent

Level of Service

(LoS)

State

B - High Stable Very few High

C - Good Stable Acceptable

D - Adequate Unstable Passable Adequate

E - Inadequate Unstable Unacceptable Inadequate

F - Unacceptable UnacceptableSystem breakdown

Good

F - Unacceptable UnacceptableSystem breakdown

Translating LoS to CapacityTranslating LoS to capacity varies from airport to airport. Key factors

include:

Processing speed

- Check-in processes, Immigration / customs and security queue queuing times which then decide numbers for each

- Hold room capacities

- Bag delivery

Functionality standards

- Minimum connect times (MCTs)

- Walking distances

- Type of operation (LCC vs. FSC) and turnaround times

- Average aircraft load

Availability

- Key operating systems such as monitors, escalators, etc.

Capacity and Expansion Modular expansion

Plan for modular expansion in tranches

Always relate landside and airside systems together and have similar inputs (i.e. same forecasts schedules peak-data)forecasts, schedules, peak-data)

Remember to involve stakeholders

Flexibility and constraints

Airports are changing systems and are affected by market forces and other factors (e.g. fuel i fi i l h lth f i li t ti li ti l l liti t )prices, financial health of airlines, route rationalizations, local politics etc.)

Time required to add the capacity to the system

Nothing is done overnight. It takes time to envision, plan, develop, test and commission

Dealing with existing operations and constraints (esp. in Brownfield g g p ( pscenarios)

Always need to understand local constraints and operational issues in terms of prioritizing

Capacity and Expansion• Capacity is always relative and depends on

the user profile and the operator and depends very much on LoSp y

• LCC facilities generally have lower LoS and therefore can generate higher throughputs but even this number can vary depending on

tioperations

– e.g. number of annual pax per stand, which can vary depending on usage, peaking, and contact vs. remote

C it i l i d b l ‘ k ’ • Capacity is also increased by less ‘peaky’ schedules and spreading demand

• This increases utilisation rates significantly

• Traditionally international gateways have created efficiencies by mixing natural international and domestic peaks and schedules especially so at Indian airports

Capacity and Level-of-Service

Capacity and LoS Key factors / issues

Capacity

Capacity is relative and depends on user (Network vs. LCC)

LCCs have lower LoS so differentiated product is key. Less peaky schedules/optimization are hallmarks of LCC operations

Passengers however need to realize difference in product and therefore charges – not easy in India

When and how much to invest is critical and its important to know that it takes time to go through an expansion program

Business plan needs to drive CapEx and not the other way

Flexible demand-driven expansion is key.

Always relate airside and landside systems

Timing and extent of investment

Higher definition of service quality requirements (SQRs) and level-of-service (LoS) means increased specification of facilities, more area and by definition a higher level of investment

Level-of-Service

Capacity and Level-of-Service

Capacity and LoS Key factors / issues

Operational constraints

Operational constraints are key.

Local political and other sensibilities need to kept in mind

Government needs to be more proactive in helping with situations. No use in State Support Agreement otherwise

5 Conclusions5. Conclusions

Conclusions

Issue Way Forward

Clarity in setting of charges and till system; Clarity and flexibility of concession agreements

Regulation – Clarity on Concession agreements

Provision of capacity and flexibility with benefits and costs clear to operators and stakeholders including airlines and public.

Government obligations need to be clear (esp. for non-metro)

Debt – viable mix of domestic and ECB required; Risk allocation and capital structuring need to be clear

Debt instruments such as revenue, recourse bonds to be explored

Equity – need for greater flexibility to allow dilution/early exit for PE; Clarity in allowable rate of return and upsides/downsides

Security – innovative mechanisms such as up-front deposits to be encouraged to leverage debt; Robust documentation to prevent misuse

Sub-contracts based on long-term fixed receivables can be securitized

Financing – Flexibility is the key

Conclusions

Capacity – depends on user (LCC vs FSC) and product differentiation is required based on LoS

Issue Way Forward

Capacity depends on user (LCC vs. FSC) and product differentiation is required based on LoS.

Capacity - master plans need to be reviewed and updated depending on state of industry and forecasts – so flexibility is key.

LoS – varying LoS depending on user group and it affects costs and therefore what passengers pay. This needs to be made very clear and explicit to airlines and passengers.

Investment – needs to be driven by modular expansion.

Investment – business plan needs to drive CapEx so project viability is key.

Investment – stakeholder involvement is critical and charges and regulatory process needs to be explained clearly early based on business plan and stakeholders need to sign-off on expansion and

Airport Planning – Plan for Capacity/LoS and balance with

charges.

Investment – airlines need to pay fair charges.

Investment - airports need to keep upside if they do well.

investment requirements and return on investment for investors – Clarity, differentiated service and what you pay for the product are key

Final thoughts…

• Airports by definition need huge capital investments and the quantum of investment in a runway or terminal cannot be scaled down once built (as againstinvestment in a runway or terminal cannot be scaled down once built (as against an airline for instance that can sell aircraft or divest assets).

• Larger infrastructure projects such as airports have longer gestation periods and upfront risk by a private operator needs to be taken into account.

• A major difference in the quality and level of infrastructure and the addition of a capacity will by extension normally lead to a significant increase in charges.

• Economic regulation of airport projects ultimately need to ensure project viability and investor confidence Having unusually high revenue-share percentages mayand investor confidence. Having unusually high revenue share percentages may not ultimately benefit either investor or consumer.

• The goal of regulation is to prevent abuse of power and monopoly pricing as it cannot reflect the power and efficiency of market pricing. So regulating areas

here competition can or does e ist is not good policwhere competition can or does exist is not good policy.• One size does not fit all.

28