september/october issue

DESCRIPTION

ÂTRANSCRIPT

SEP TEMBER/OCTOBER 2013

BRING RETAIL TO THE PEOPLE

IS LAND REFORM THE END OF PROPERTY RIGHTS?

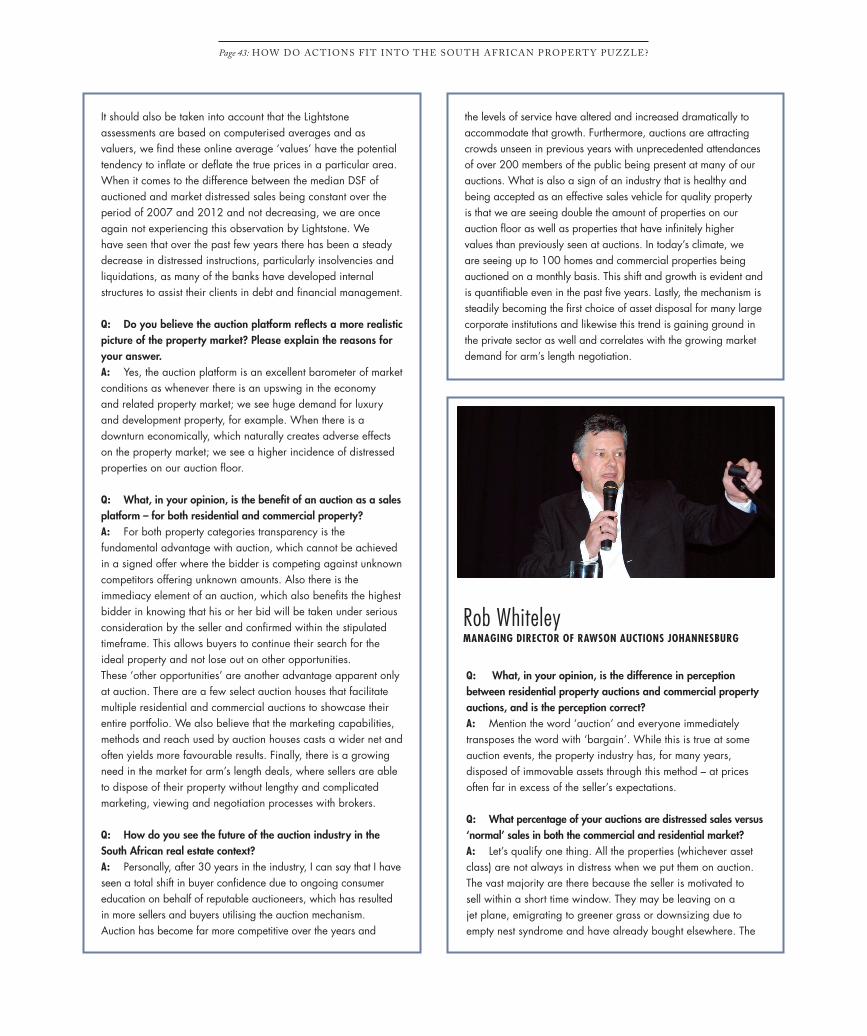

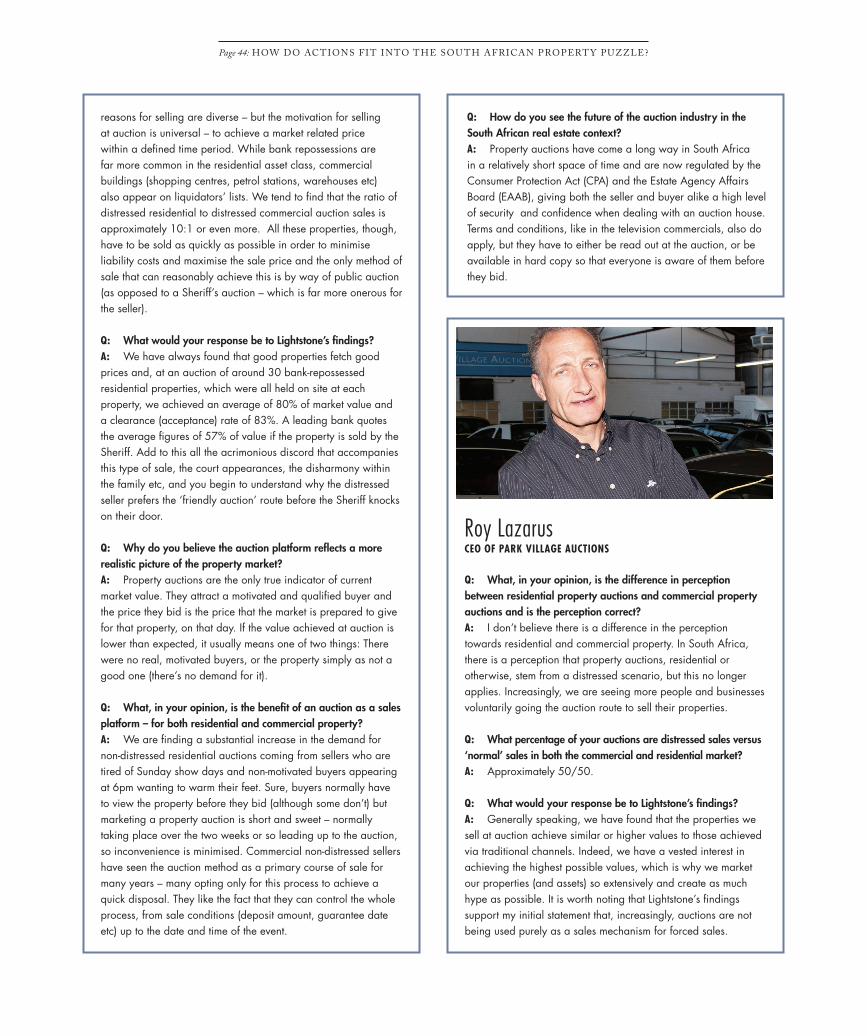

PROPERTY PLATFORM: EXPERT OPINION ON PROPERTY VALUATION IN SA

MORTGAGES: WHERE THEY HAVE COME FROM AND WHERE THEY ARE GOING TO

21930_Savills Single Page FA.indd 1 2013/08/22 1:13 PM

This issue marks the publication of Property Professional’s inaugural Property Platform, hosted in Sandton in August, and sponsored by Knowledge Factory. The aim of the Property Platform is to bring together a selection of South Africa’s leading property businesspeople to discuss, debate and share insights around a particular topic on a ‘by invitation only’ basis. This Property Platform tackled property valuation methods. When it comes to the valuation of property, banks, homeowners, developers, estate agents and the municipality all seem to get to different figures. While everyone took the fifth when it came to discussing municipalities and their property evaluations, it is interesting to see the difference in perspectives on valuation methods that developers and the banks have. Read what some industry leaders have to say in the discussion on page 10. In other industry news, while the training debacle rages on - which we provide some updated coverage on in this issue on page 16 - the good news is that the Estate Agency Affairs Board has extended the deadline for affected estate agents to be certificated against the required real estate qualifications until 30 June 2015. Be that as it may, extension or no extension, there are still agents out there who deem the whole educational process to be unconstitutional and who are therefore considering their legal options. The training issue has a long way to go before it can be considered resolved, and we will keep you posted every step of the way. In this issue we also touch on land reform and what the future holds, green building trends and the economic challenges that are still facing the industry. There is an interesting feature on mortgages on page 28, and we look at retail development trends on page 36. The Q&A with auctioneers on page 40 provides some interesting insight into that section of the property industry in relation to the perception of the auction as a property sales mechanism and in response to Lightstone’s findings that distressed sales that transact in the market are on average 13.2% higher than those sold at auction. New agents and top performing agents are also featured, along with our regular facts, figures and tech reviews. Thank you for all your positive feedback on the magazine, it is always great to hear when we are getting things right! We look forward to receiving more of your feedback and suggestions.

PUBLISHED BY THE PROPERTY ADVERTISING JOINT VENTURE 6 Beach Road, Old Castle Brewery Woodstock 7925 021 447 7130 CEO - PA MEDIA Shaun Minnie 083 629 6081 [email protected] EDITOR Michelle Funke 011 462 8959 [email protected] ADVERTISING SALES Sarah Steadman 082 334 4367 [email protected] ADVERTISING PRODUCTION & SUBSCRIPTIONS Nikki Barnard [email protected] ACCOUNTS & FINANCE Nicolette Lubbe 011 476 6293 PRINTING Paarl Media Disclaimer: The publisher of this magazine gives no warranties, guarantees or assurances and makes no representation regarding any goods or services advertised within this edition. © Copyright Property Advertising Joint Venture. All rights reserved. No portion of this publication may be reproduced in any form without prior written consent from the publisher. The publishers are not responsible for any unsolicited material.

EDITOR’S NOTE

MICHELLE FUNKE [email protected]

EDITOR’S NOTE

CONTENTS

CONTENTS04 INDUSTRY NEWS 10 PROPERTY PLATFORM 16 THE TRAINING DEBACLE 20 LAND REFORM 24 CAPE TOWN ACCELERATES TOWARDS ENERGY SMART-STATUS 28 THE DEVIL IS IN THE DETAILS 30 F INANCE & F IGURES : HOW DO HOME LOANS MEASURE UP?

32 INTO THE EYE OF THE ECONOMIC STORM 36 BRING RETAIL TO THE PEOPLE

40 HOW DO AUCTIONS F IT INTO THE SOUTH AFRICAN PROPERTY PUZZLE? 44 MARKET SHARE : PROPERTY F INANCE IN SOUTH AFRICA 46 PROPERTY PROFESS IONAL NEW AGENTS ON THE BLOCK 52 PROPERTY PROFESS IONAL TOP PERFORMING AGENTS 58 TECH TOOLKIT 60 DEVELOPMENT UPDATE 64 WORD ON THE STREET

ON OUR COVER FROM LEFT TO RIGHT: Mike Walters, Zain Sayed, Kumeshini Naidoo, Mohammed Areff, Ewald Kellerman. COVER IMAGE: Kelly Jane Photography

Go to www.payprop.com for the full story on how we helped Lynne automate and

integrate her rental transactions within our audited trust environment, or call us on

087 820 7368 to discuss how we can help you run a better and safer rental portfolio.

TRUSTED PAYMENTS

“PayProp has added to my life quality, not just my business quality.

And if my life is better, I can do business better.”

~ Lynne Henkenjohann, My Property Broker ~

Page 6: INDUSTRY NEWS

INDUSTRY NEWS

Entrepreneurial, owner-managed South African businesses and property owners are increasingly looking for more value added services and flexible financing arrangements from their lenders than prior to the economic crisis in 2008. This is according to Gary Palmer, CEO of Paragon Lending Solutions, who says that prior to the financial meltdown, clients primarily sought finance from their lender.

“As market conditions deteriorated, the clients’ needs changed and they are now not only asking for access to finance if they require it, but also with assistance for buying and selling of property, how changes in regulations affect their investments, how market conditions can affect their business practices and how lenders can assist them with a variety of other financial matters.” Recent credit data from the Reserve Bank has indicated that growth in unsecured lending has slowed, while mortgage lending has only grown at less than 2% a year because banks have tightened rules around long-term lending. However, Palmer says that South Africa’s economy still offers good opportunities for entrepreneurs and owner-managed businesses if they employ the right strategy and utilise diverse value-added services.

“Smaller businesses and property owners unfortunately do not have access to financial advice and support in the same manner as larger corporations do. These larger businesses are in the position to employ experienced staff who have established relationships with commercial banks, have additional financial advice from auditors and access to legal experts who have a thorough knowledge of that enterprise.”As a result, Palmer says that private non-bank lenders, who are also not governed by the same regulations as the major banks, are in the ideal position to assist clients who require financial assistance via their value-added services. “Private lenders are usually entrepreneurs themselves and therefore understand and can identify with entrepreneurial challenges and how to respond to them.”

South African property owners and businesses seek more from their financiers

Palmer says that no matter what the businesses situation, they should always consult a professional lender to assist with cash flow forecasts. “A financial oversight can potentially bring devastating financial losses if adequate planning, risk management scenarios and financial resources are not in place.”

He adds that a financier can also assist with the sale and purchase of a property to ensure that all legal and compliance affairs are in order. “Property rights and the associated legalities are also complicated issues and individuals often misunderstand what is required of them or neglect to consider what the legal parameters are when looking to finance a property deal. This is particularly important when it comes to urban development and town planning matters,” says Palmer. Furthermore, he says that a financier would also facilitate if a client is considering buying a distressed apartment block. “The financier would only be able to lend to the client if the National Home Builders Registration Council (NHBRC) is involved and deems the building as compliant,” he says.

“However, one of the most common mistakes property owners make is that of under or over insuring because they neglected to have an appropriate property valuation conducted at the offset, due to bad or incorrect advice.”Palmer adds, “Non-bank lenders can also assist with deceased estates to prevent any loss of capital and to protect the financial interests of the heirs. The Master’s office supervises the administration of deceased estates to ensure an orderly winding up of the financial affairs of the deceased in terms of the Intestate Succession Act, 81 of 1987.” Finally, he says that there may be certain transactions which are more suitable for commercial banks. “The lender may also be in the position to assist with Commercial Bond Origination by applying for a commercial loan on their behalf. The client submits a variety of financial information to the lender who will determine their eligibility and what interest rate he or she will pay,” he concludes.

Tower Property Fund was officially the first new fund in South Africa to list on the main board of the JSE under the Diversified REITs sector when it listed on 19 July 2013. Tower successfully raised R300-million for the listing. REITs (Real Estate Investment Trusts) have been introduced in South Africa to bring the listed property sector in line with international

standards and are tax advantaged investment vehicles that invest in and derive their income from income-producing property and distribute rental income to the holders of shares or units.“By investing in REITs investors are given exposure to a diversified portfolio of properties, which may be high quality office, industrial and retail properties, in one investment,”

First South African property fund to list under the new REIT structure

ARE THERE PROVISIONS

• The Landlord must furnish the tenant with a written receipt for all payments received from the Tenant. The receipt must show the date, address of the rented premises and what the payment was for (ie arrears, monthly rental, etc).

• If the agreement provides for the payment of a deposit, the Landlord must invest it in an interest-bearing account with a fi nancial institution. At the end of the lease period, the Landlord must pay the interest (and deposit) to the Tenant (or the balance thereof, if repairs for damages were required). The interest rate must at least be equal to the rate offered by the relevant fi nancial institution on a savings account.

• If, during the lease, the Tenant requests written proof of the interest that had accrued on the deposit, the Landlord must oblige. (If the Landlord is an estate agent, the deposit and interest thereon is dealt with as provided for in the Estate Agency Affairs Act.)

• The deposit (plus interest) must be returned to the Tenant within 7 days of the expiry of the lease. If the money was used to pay for repairs of damage caused by the Tenant, the balance must be returned to the Tenant within 14 days after the repairs were effected. In the latter case, the relevant receipts which indicate the costs incurred, must be available to the Tenant for inspection.

• The Tenant and Landlord (or their agents) must jointly, before the Tenant moves into the premises and also before he moves out, inspect the dwelling to ascertain the existence or not of any defects/ damage .

• If the Landlord (or his agent) fails to inspect the dwelling in the presence of the Tenant as required, he is deemed to acknowledge that the dwelling is in a good and proper state of repair. The Landlord will in that case not have a claim for damages that were ascertained after the Tenant moved out.

www.stbb.co.za

more than just

Our ability to add value is an art form that has taken years of experience to perfect. At STBB we build long lasting relationships and give you hands-on-advice to protect your rights of ownership.

PROTECT YOUR OWNERSHIP WITH THE PAPERWORK.

THAT AUTOMATICALLY APPLY TO A LEASE AGREEMENT?In an effort to protect the rights of Tenants, the Rental Housing Act lists certain provisions that are deemed to be included in each and every rental agreement for residential accommodation. This means that the provisions apply to the agreement, irrespective whether the Landlord and Tenant actually included these in their written or oral agreement; and they cannot contract ‘out of’ these provisions either. The deemed provisions are found in section 5(3) of the Act. In the below bullet points we highlight the most important of these:

Cape Town 021 406 9100 | Claremont 021 673 4700 | Fish Hoek 021 784 1580 | Somerset Mall 021 850 6400 Table View 021 521 4000 | Tygervalley 021 943 3800 | Johannesburg 011 853 8300 | Bedfordview 011 453 0577 | Centurion 082 851 1816

COMMERCIAL LAW | CONVEYANCING | EMPLOYMENT LAW | ESTATES | FAMILY LAW | LITIGATION | PERSONAL INJURIES & 3RD PARTY CLAIMS

Escalation of Green Star South Africa ratings in month of June

June proved a bumper month for green building certifications with a total of six new buildings receiving a Green Star South Africa rating from the Green Building Council South Africa. This upsurge further substantiates that the green building movement is rapidly gaining ground in South Africa as developers and progressive businesses increasingly embrace sustainable building practices. These new ratings take the total number of Green Star rated buildings in South Africa to 36, and include some impressive and significant developments such as the Department of Environmental Affairs’ head office, which has scored a 6-Star Green Star SA rating – the highest rating possible and a first for a national government-owned building in South Africa.

Hyundai’s new head office, situated in Bedfordview, is another exciting development to receive a Green Star rating as it signifies buy-in and commitment to sustainable practices from this large motor corporation – the first green building rating in South Africa achieved within this sector. The Hyundai building, which achieved a 4-Star Green Star SA Design rating comprises two floors of A grade office space and one basement level, and will accommodate 200 full-time employees.Another notable rating is that of the 9 000m2 Chevron Project CORE building, situated in Century City in Cape Town, which achieved a 5-Star Green Star SA Design rating – an exciting indication of the shift in mindset towards green business practices from one of the leading refiners and marketers of petroleum products in South Africa - Chevron South Africa. The impressive Portside building, which achieved a 5-Star Green Star SA Design rating, is a joint initiative between Old Mutual and FNB, and is set to become an impressive landmark tower in the foreshore

area of Cape Town’s CBD - featuring 32 floors, over 52 000m² of office space and 1 200m² of retail and banking space.The Lakeside Office Park in Centurion, which is a redevelopment of the Meerlus building, not only scored a 4-Star Green Star SA Design rating, but also recently won the (SAPOA) Innovative Excellence Award for Green and Industrial Property Development. Located opposite the Centurion Gautrain Station and with easy access to the national roads network, the building offers over 5 000m2 of lettable space for tenants seeking proximity to major transport nodes and other amenities. The building is the first of three to be developed in the Lakeside Office Park.

Finally for June there was the 5-Star Green Star SA ‘As Built’ rating achieved by the Nedbank Menlyn Maine – Falcon Building in the Menlyn Maine Precinct. The Menlyn Maine Precinct is envisaged as a live, work, play neighbourhood where the buildings and urban planning design strongly subscribe to environmentally sustainable principles. All buildings within the precinct will be required to achieve, at a minimum, a 4-Star Green Star rating, and it is the first project in Africa to be registered with the Clinton Climate Initiative, a stringent rating mechanism evaluating the carbon neutrality of a project. “The GBCSA is very encouraged to see this spike in the number of buildings achieving Green Star SA ratings,” says Brian Wilkinson, CEO of the Green Building Council South Africa. “We are confident that the green building movement in South Africa will continue this upward trajectory and that we will increasingly see green building practices becoming the norm. The industry is embracing this absolutely necessary shift towards sustainable practices and it is exciting to be part of this change.”

says Marc Edwards, CEO of Tower Property Fund. Tower was well received by investors and its shares rose from the initial offering of R8.70 to R10 per share on the first day of trade. The fund has benefitted from its REIT status as a number of smaller developers have placed their properties into the fund in exchange for shares to take advantage of the Capital Gains Tax Rollover relief they obtain.“Tower aims to provide investors with strong investment returns, comprising a growing income stream and capital value. This will be achieved firstly by adding value through active property asset management, and secondly through the cost-effective ‘greening’ of properties in the portfolio, which will result in reduced occupation costs for tenants and increased investment performance,” says Edwards.

“Our investment strategy is to target acquisitions of medium-sized (R30-million to R200-million) properties, diversified across the retail, office and industrial sectors, and geographically across the major metropolitan areas. Competition for medium-sized properties is less intense, and well-located, good quality, medium-sized properties provide a diversified earnings base, better yields and, frequently, the opportunity to improve performance. However, larger properties will not be excluded where

suitable opportunities arise.”“Properties acquired, and to be acquired, by Tower were and will be selected for their potential to generate and sustain strong rental income streams,” explains Edwards. “Diversification is a key component of the company’s investment strategy, and is achieved through a geographic spread of properties across major urban centres, a mix of property types, a staggered lease expiry profile and the fund’s active ‘greening’ strategy.”

According to Edwards, Towers’ initial ‘greening’ focus will be on improving energy efficiency, which will result in significant savings in electricity costs, thus making buildings more competitive and helping to ‘future-proof’ them against future rises in tariffs. Basic cost-effective energy and water savings measures that can be implemented at low or no cost will be applied immediately, while additional measures will be implemented over time as opportunities arise. “We will be benchmarked against the Green Building Council of South Africa’s Energy and Water Benchmarking tool and improvement in performance will be monitored and reported on. These measures will increase the competitiveness and values of buildings in Tower’s portfolio over time.”

Page 8: INDUSTRY NEWS

New South African REITs and real estate as an asset class – not all it’s cracked up to be?

Much has been said about the benefits of the new Real Estate Investment Trust (REIT) structure which has become available to the South African property sector. Aimed at aligning the South African listed property sector with our international counterparts, REITs may create a more attractive investment structure, significantly enhancing international interest, whilst at the same time bringing about much needed tax and regulatory changes that local property structures could certainly benefit from in the long term. However, Grant Alexander, director of Private Client Holdings, warns that REITs might not offer investors as much as hoped and advises that real estate as an asset class holds several pitfalls which South African investors must be aware of.“The arguments in favour of listed property include diversification with strong, predictable returns when equities are weak; good yields compared to cash; benefits afforded in a low interest rate environment and being a good inflation hedge.”

“However, there are many arguments against listed property,” says Alexander. “Volatility is higher with listed property than a defensive or balanced portfolio; property yields are currently lower than bond yields making property more expensive but there is more risk associated with property; the rand is a threat to our bond market and given the close correlation, the property market is also under threat from a weaker rand; lower economic growth causes increased vacancies and rising operating costs will eat into profits.”Alexander states that rising bond yields is the

main threat to the sector – higher yields mean lower prices. “Listed property has benefitted from strong retail performance – and many of the factors which have led to this strong performance, such as unsecured lending and salary increases ahead of inflation, are unsustainable. If the retailers slow down, the property sector will slow down as vacancies rise and retailers will start resisting annual rental escalations more.

According to Alexander, the introduction of REITs to South Africa will make real estate more attractive to foreign investors, but it does not significantly change the South African property investment structure compared to the previous regime. “It is thought that one of the main benefits provided by the REIT structure is the tax change. South African investors will receive gross distributions from a South African REIT entity – without the 15% dividends withholdings tax being levied. However, investors will have to pay tax on the distributions at their applicable marginal income tax rate, so paying tax is unavoidable,” says Alexander.

“Real estate is a complicated asset class as one must consider many factors such as occupancy levels, yields and retail demand. However, all of this being said, REITs are a good diversifier and should be held as part of a balanced portfolio, but if you intend to buy as your sole focus, caveat emptor - ‘let the buyer beware’,” concludes Alexander.

Property buyers beware! Rates clearance certificates are a cold comfort

In a ruling with significant implications for property owners and banks, the Supreme Court of Appeal (SCA) recently held that all amounts due for unpaid debts are secured by the property, even when a rates clearance certificate has been issued confirming that municipal charges for the preceding two years have been paid. Lior Nickig, associate attorney at pan-African corporate law firm Bowman Gilfillan, explained that for new property owners this means they are at risk regarding unpaid municipal debts that are more than two years old, and the property concerned can be sold in execution and the proceeds used to pay the outstanding debt.

“The Supreme Court of Appeal recently held, in City of Tshwane Metropolitan Municipality vs Thomas Mathabathe and Nedbank Limited, in relation to a section 118(1) clearance certificate issued in terms of the Municipal Systems Act 32 of 2000, that all amounts due for unpaid municipal debts are secured by the property. “The SCA held that all amounts owing to the municipal authorities that have not prescribed are secured by a lien on the property and this lien is not lost when the property is transferred,” explained Nickig. The SCA confirmed that if municipal charges for the two-year period preceding an application for a clearance certificate are paid, the municipality is obliged to issue

a clearance certificate. However, the court also held that if there are additional charges due over and above those that arose during the two-year period, the municipality is not entitled to withhold the clearance certificate. The remedy available to the municipality in respect of these charges is that it exercises a lien in respect of the property for an unlimited duration. It was confirmed that if these charges are not paid, and an appropriate court order is obtained, the property may be sold in execution and the proceeds applied to the unpaid debts. Nickig explained that, in practice, this means that the new property owner is at risk in relation to charges owed to the municipality for unpaid debts older than two years. “Conceivably, this means that the municipality could sue the previous owner for outstanding charges and if the previous owner is unable to satisfy any judgment obtained in this regard, seek to sell the property in order to satisfy the judgment.”

“A purchaser of a property will be well advised to ensure that once a rates clearance certificate is issued, there are no additional amounts owing to the municipality. In circumstances where there are outstanding charges owed to the municipality, a purchaser should obtain sufficient collateral from the seller in order to limit its exposure.”

Page 9: INDUSTRY NEWS

National Debt Mediation Association (NDMA) welcomes survey showing consumers benefit from alternative dispute resolution services

The National Debt Mediation Association (NDMA) has welcomed a survey by the National Credit Regulator (NCR) that shows that alternative dispute resolution (ADR) services offered to consumers are largely seen as effective in resolving a range of disputes between service providers and consumers. “Alternative dispute resolution, which includes mediation, offers consumers a way to resolve their disputes in a quicker, simpler and cheaper manner instead of following a court process that is adversarial and expensive,” says NDMA CEO Magauta Mphahlele. Within a short period of time, the NDMA has been able to establish its footprint across most provinces and has handled more than 6 000 disputes and complaints with more than 70% success rate for cases with a resolved outcome. The high success rate of alternative dispute resolution is confirmed by the research report which reports that 85% of respondents were satisfied with ADR services provided by various entities and would recommend them. However, the report indicates a low usage of free services offered by the NDMA, NCR, provincial offices and ombudsman. It is important to note that the low usage might also be due to private companies having very big marketing budgets and therefore consumers being more aware of their existence. This is supported by the finding of the report that a majority of consumers heard about the services through newspapers, radio and television. “Over the past few years, the NDMA has been advocating for mediation as it is able to help consumers through the often legally complex and technical aspects of credit and payment disputes and offers huge benefits to consumers, especially low income consumers who most times cannot afford the services of a lawyer,” says Mphahlele. The NDMA, which is currently in the process of transitioning into an independent consumer services NGO, is considering applying a mixed model where those who can afford the dispute resolution services are

charged a nominal fee, but those who cannot afford it are assisted for free through donor funding or partnership referrals. This is because the report indicates that consumers sometimes prefer to pay for these services as this gives them the confidence that their ADR agent will be on their side and will be committed to ensuring the case is resolved in their favour. This should, however, not discount the important role played by the various ombudsman schemes as they service an underserved and often low income and vulnerable market. Consumers need to understand that ADR often happens through mediation where the purpose is to find win-win solutions and therefore there is always a balance of rights and responsibilities. The report proposes that ADR agencies need to be regulated. While the NDMA agrees with this proposal to some extent, it is important to note that most service providers, including ADR service providers, are regulated by the Consumer Protection Act, which covers advertising, service standards, contracting and fair pricing. It is therefore important to consider what is already covered in existing legislation before additional regulations are imposed. Concerns raised by the NDMA regarding some ADR agents are misleading advertising, overcharging and lack of transparency. The NDMA and the various ombudsmen report publicly on the cases received and resolved and this ensures accountability and transparency. THE SERVICES OFFERED BY THE NDMA INCLUDE:

• Anationalhelplinethatprovidesinformationonanycreditrelated matter, including the explanation of the options available to consumers to resolve their debt problems.• Budgetingandpaymentplanassistancewhereconsumersare experiencing difficulties with repaying their debt.• Assistancewithcreditdisputes,exceptdebtcounsellingcomplaints which are referred to the NCR.• Directoremployerhostedconsumereducationworkshops.• ReferralassistancewheretheNDMAdoesnothavejurisdiction.

NUMBERS T O KN OW

Numbers to know is a feature that catalogues the most notable, quirky

and surprising statistics in South Africa. See this issue’s selection…

“A small black-owned Johannesburg agency with a staff complement that can be counted on the fingers of two hands, has been awarded the Eskom advertising account, a piece of business on which Eskom spends around R175-million a year (including production costs).

It looks like a stunning vote of confidence in the relatively low-key agency.”Finweek - Eskom’s daring choice

R175-MILLION

Page 10: INDUSTRY NEWS

Get rewarded for your loyalty!

Join today and you too could beearning points with BetterRewards.All you have to do is submit your OTP’sand registered deals to BetterBond, anddepending on which tier you qualify for,you could earn a maximum 2000 pointsper OTP submitted and 7500 points per

R1M registered bond! It is like cash inyour pocket.And when you see the range of goodies on our online catalogue that you can redeem your points against,you won’t look back! What are you waiting for?

SAVE, EARN, REDEEM with BetterRewards, today!Register online at www.betterrewards.co.za.

prop prof September October ads_Layout 1 2013/08/20 2:07 PM Page 1

Everyone seems to get to different figures when valuating property. Property Professional wanted to find out how and why, and what the future holds. Ewald Kellerman, head of sales at FNB Home Loans, Zain Sayed, regional manager of FNB Commercial Property Finance for Gauteng South West and East, Timothy Akinnusi, head of sales and client value management at Nedbank Home Loans as well as Mike Walters, divisional and asset manager at Renprop sat around the table discussing how we can, or perhaps should, effectively value property in South Africa.

THE MEASUREMENT METHODS While everyone took the fifth when it came to discussing municipalities and their property evaluations, it is clear that the residential and commercial property sectors use completely different evaluation methods. Walters says that from a commercial perspective, the valuation exercise is a lot easier. “There are essentially two ways in which commercial property can be valued: Firstly based on the income that the property

Page 12: PROPERT Y PLATFORM

Evaluating property in South Africa

There is more often than not a discrepancy between property valuations from various institutions and developers. So just how should property be effectively valued in South Africa? The inaugural Property Professional Property Platform asks some industry leaders what their thoughts are on the matter.

PROPERTY PLATFORM

Timothy Akinnusi, head of sales and client value management at Nedbank Home Loans Photographs: Kelly Jane Photograph

Page 13: PROPERT Y PLATFORM

produces or the known cap rates for the area, which are published by Rode. The calculation is a simple percentage of net income that the property can produce while there is a lease in place. Factors that influence the cap rate are location, the age and condition of the building, the terms of the lease and the type of tenant. The second way in which commercial property is valuated comes into play with vacant buildings, where generally a rate per square metre is used which will fluctuate depending on age, design and whether or not the property is already built. This rate is negotiated and agreed at the time of sale.” Kellerman says that on the residential side there are number of different challenges compared to the commercial side as residential property is not driven by the same commercial factors. “A typical residential buyer will place value on a property based on its features that meet their requirements,” he says. “A modern kitchen, for example, would win over one buyer, while the fact that the property is close to a certain school may win over another. Specific investment value that is placed on a certain property by a person with unique requirements can mean that the property will sell for more than what open market would pay for it. This is where a lot of anomalies come in to residential property values.” Kellerman goes on to say that with residential property valuations, there is a lot of irrationality as it’s usually a personal decision. “In the residential market, a comparable sales approach is typically used to determine the value of a property, and is based on property sales in the area, adjusted for time, difference in characteristics and other market conditions in the area. This method has its own anomalies as it can drive irrationality and help the market get ahead of itself easily. The gap between value and income stream from buy-to-let properties in the residential sector is quite big generally, as is the gap between replacement value and market value. The residential market is strongly driven by sentiment – what buyers are willing to pay for properties.”

TOP VALUE INFLUENCERS When it comes to commercial property, the cliché of location, location, location holds true, says Sayed, followed closely by the term of lease and the type of tenant and then the condition of the building. Akinnusi points out that residential property values are based on the same criteria, except where the term of the lease is important from a commercial perspective, amenities close to the property, accessibility and town planning take precedence in the residential sphere. “Accessibility and amenities are what really give residential property its real intrinsic value – it’s not just the bricks and mortar with which the house is built, but rather what the surrounding suburb can offer such as schools, shopping centres and the like.” Kellerman takes a step back, and looks at specific market drivers like debt levels, which have a huge influence on the market. “When financial institutions had a greater appetite for lending, it was a massive driver for residential sales in the boom years.” He also points to external economic factors, particularly around inflation and interest rates, and lastly, from an economics perspective, is supply and demand. Walters says the state of the economy and GDP play a massive role in the value of property, as does the political climate, the unemployment rate, individual levels of disposable income and the government’s ability to deliver, or not, on existing and new infrastructural projects. THE VALUATION CHALLENGES While commercial property valuations don’t seem to have the complex issues surrounding them like the residential side of things, Sayed says that one of the biggest challenges in commercial property finance is trying to explain the difference between market value and replacement

Ewald Kellerman, head of sales at FNB Home Loans Mike Walters, divisional and asset manager at Renprop Zain Sayed, regional manager of FNB Commercial Property Finance for Gauteng South West and East,

Page 14: PROPERT Y PLATFORM

value. “Market value is based on the willing buyer and willing seller principle, whereas replacement value is linked to costs of rebuilding the building. There are anomalies here, like a building in Sandton, for example, might have higher market value than replacement value, whereas a building in the Johannesburg CBD will have a market value that is a lot lower than the replacement value.” According to Walters, there are fundamental challenges with the way in which banks value new residential property projects which does not sit well with developers. “Most of the time the valuers that the banks appoint are not as close to the market as the developers are, so they are often unaware of the needs/demand in a particular sector,” he says. While historical data plays a role, he says it is not the only basis on which a new project should be valued. In addition the method used and the use of external valuers can be seen as an easy way out for the banks, especially when the valuer does not find value. From a banking perspective, Kellerman says that when it comes to valuations, the purpose is to use the valuation as a prudency check during the loan approval process. “The bank looks at it from a security perspective and so has to take the resalability of the property into account.” Walters says that even so, the way in which the banks value properties is a huge challenge – both for the institutions themselves and for the purchaser. He says that valuations are generally conducted by external or independent parties who only look at historical sales figures and price growth. “Due to the fact that they look at historical figures, it is extremely difficult from a development point of view – no matter whether you are looking at an urban city environment or a country town environment – as the statistics can skew the figures to such an extent that developers are disadvantaged by the method that is used. The historical figure evaluation method lacks a broad approach that we would like to see. Valuers and banks are not at the coal face of the property market, and should therefore rather look at the developer and their track record to see the potential for the development over the historical area data.” While Kellerman agrees that on the residential side there is a historical bias, he says that financial institutions work on scientific information – the nature of which is not forward looking. “While it is a good idea to look at the credibility of the developer, many banks have burnt their fingers with many developers, so we need to protect the assets and money we invest. We are not in a position to take an uncalculated risk – if growth in an area’s property market cannot be proven, it is difficult to commit finance and show that we have lent money prudently. There are a couple of factors involved, and while I think a developer’s credentials can be relevant, there has to be caution around the risks. There have been many developments or inexperienced investors over the past few years that have received financial backing in situations where the potential for growth has not been realised.” Sayed adds that while commercial property does not seem to have a valuation problem as there is generally a consensus between all parties on the value most of the time, when it comes to residential property, post

Powered by

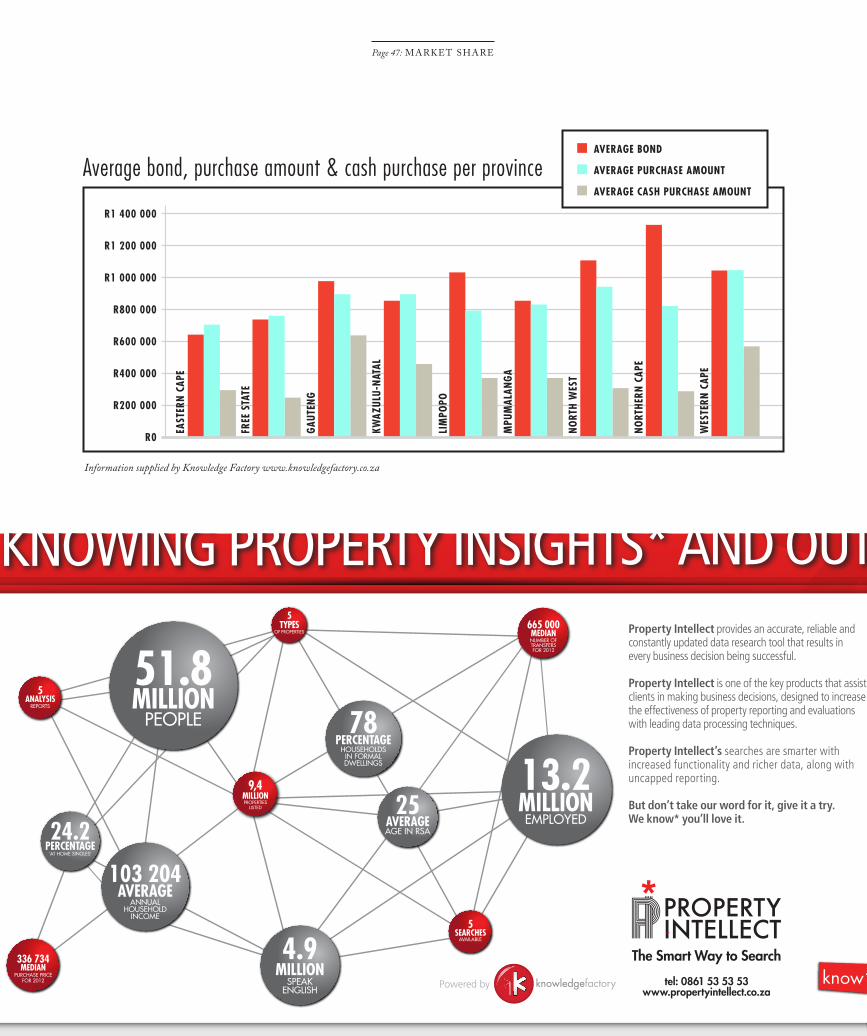

tel: 0861 53 53 53www.propertyintellect.co.za

The Smart Way to Search

KNOWING PROPERTYINSIGHTS* AND OUT

Property Intellect provides an accurate, reliable andconstantly updated data research tool that results in every business decision being successful.

Property Intellect is one of the key products that assist clients in making business decisions, designed to increase the effectiveness of property reporting and evaluations with leading data processing techniques.

Property Intellect’s searches are smarter with increased functionality and richer data, along with uncapped reporting.

But don’t take our word for it, give it a try. We know* you’ll love it.

9,4MILLIONPROPERTIES

LISTED

5TYPES

OF PROPERTIES

665 000PURCHASE PRICE

FOR 2012

5SEARCHES

AVAILABLE

336 743MEDIANNUMBER OFTRANSFERS

REPORTS

5ANALYSIS

51.8PEOPLE

MILLION

25AGE IN RSAAVERAGE

103 204ANNUAL

HOUSEHOLDINCOME

AVERAGE4.9SPEAK

ENGLISH

MILLION

13.2EMPLOYED

MILLION

24.2‘AT HOME SINGLES’

PERCENTAGE

78HOUSEHOLDS

IN FORMALDWELLINGS

PERCENTAGE

BY MICHELLE FUNKE

2009 almost all financial institutions took a big loss and have therefore limited their lending capacities towards residential developments. “But Mike has a point; there is perhaps room for developers to be backed financially based on their track record. However, one should bear in mind that unlike commercial property, leases are shorter in the residential sector and there is still a long-term loan on the property that needs to be serviced. It becomes more challenging in the residential sector as financial institutions have to look at other important factors that can influence the property value such as the market demand, growth of area and other factors.” On the commercial property front, while getting to a value that everyone can agree on is not really an issue, government’s delivery on infrastructure is. So much so that there seems to be a move for development further up Africa as there is a willingness from the governments to co-operate with developers through offering a smoother process in terms of land rights, access to services such as power, zoning and the like. “South Africa is losing potential investment as there seem to be better returns developments up Africa. While there are challenges in every market, South Africa’s service delivery seems to be getting worse,” says Walters. TIME TO CHANGE THE WAY PROPERTY IS VALUED? Kellerman says that the comparable sales approach or the scientific approach has been a viable one for banks in the past. “A home loan is a highly geared asset as we can lend up to 100% on residential properties, and when we have to call in an asset, which is a very

unfortunate part of our business, our losses are just as leveraged so we end up losing a lot. Generally in the market, the losses are between 20% and 30% when a loan goes into default, which are massive loss rates considering the low margins of home loan finance. This makes it a very risky business in a very competitive environment and because of that, the valuation methodology needs to be sharpened. We are quite far away from replacing the traditional valuation methods; however there is a space for more innovative methods or improvement on the current methods, particularly around the process of conducting valuation and not so much the methodology.” There is a general agreement around the table that going forward, the commercial property valuation model is successful and will stay much the same. According to Sayed, the only factor that might influence commercial property value in the next couple of years is the interest rate. “We are at the bottom of the cycle, and if the rates increase, it could slow down the values of commercial property, but other than that, this market is expected to stay on its current path.” When it comes to valuating residential property, Akinnusi feels there is data lacking. “Valuation is a very critical part of the process. Over reliance on finance is only going to stop when people start saving up for a deposit and when sustainable jobs are created. And that will only happen when the economy begins to strengthen. In the meantime, those who are leveraged to the hilt will fall hard with any interest rate hikes.” For Kellerman, the biggest gap between banks and developers is lack of information. “From a banking perspective there are many risk factors as we sit with the asset for 20 years after a developer has handed over the key. However, there is a lot of room for improvement to bridge the gap between industry players. Perhaps banks are overly conservative to a degree, but smaller companies are a lot more agile and are better able to respond to changing market conditions. The fundamentals of property valuation will stay the same, but there is a huge gap in the valuation process and technological information relating to it and hopefully necessity will breed co-operation between the various entities.” It is evident that while the current valuation methods used by financial institutions serve the purpose for determining finance feasibility to a degree, they fall short of foresight and lack a certain understanding or comprehension of market potential. If this knowledge gap or lack of information and communication between banks and developers is bridged, it could unlock a whole lot more potential for development in South Africa.

Page 16: PROPERT Y PLATFORM

The Property Platform is sponsored by Knowledge Factory, a leading data, property and marketing insights company. Knowledge Factory consolidates, interrogates and interprets relevant data sets to provide clients in the financial, hospitality, FMCG, property and media industries with reliable market data that highlights needs and opportunities and supports informed strategic business decisions. Knowledge Factory is a proud subsidiary of Kagiso Media Limited, South Africa’s largest BBBEE media group.

IA2013B5PP 8/20/13 3:01 PM Page 1

C M Y CM MY CY CMY K

Page 18: THE TRAINING DEBACLE

There must have been a collective sigh of relief among thousands of estate agents across the country when it was announced by the Estate Agency Affairs Board (EAAB) that the deadline for NQF4 and NQF5 compliance had been extended to 30 June 2015. While it could be argued that agents have had more than enough time to get their acts together and complete the necessary qualifications, there is a large number of agents who completed the course in plenty of time, only to discover at a later stage that the training provider they had utilised had lost its accredited status. Stuck between a rock and a hard place, these agents struggled to get answers and results from the Services Sector Education and Training Authority (SSETA) and the EAAB and, judging by numerous emails received by the Property Professional magazine, some are gearing up to go to court in an effort to get the situation resolved. Although the EAAB has thrown agents a temporary lifeline, SSETA still has a lot to answer for. Why, for example, are agents who completed the qualification two years before the respective training providers they utilised lost their accreditation still waiting to be certified? Perhaps, more importantly, will the extended deadline provide enough time for SSETA to get its house in order once and for all? The confusion, lack of communication and the threat of losing their licences to sell property have led to some people questioning the entire

The educational policies introduced by the powers that be have ruffled more than a few feathers. It now appears that the entire process could be placed under a legal microscope in order to ascertain whether or not the policies are legal

THE TRAINING DEBACLE:

WILL AGENTS HAVE TO RESORT TO LITIGATION?

education process. Alon Rathbone, from the Property Scene, says he suggested to the EAAB that agents who had written the EAAB exam should be accredited with a minimum qualification that matched the NQF4 qualification. He believes that the new qualifications should have been phased in rather than disrupting the industry in the way it has. “Before this whole fiasco started, we had approximately 87 000 registered agents; today the figure has dropped to approximately 16 700. The EAAB has estimated that by the end of this unacceptable process, we will be lucky to have 8 000 agents. This is insufficient to service the industry and could place the country and its coffers in jeopardy.” Ongoing education is a fact of life and occurs in many professions across the world. Rathbone argues that while keeping up to date with the latest changes in legislation and the like is understandable, being told that agents will lose the right to sell property if they fail to complete courses that take months to complete isn’t acceptable at all. He isn’t talking about agents who are entering the profession; he is referring to those, like himself, who wrote the old Estate Agency Affairs Board exam and who were found competent to sell property in South Africa. “It is our democratic and constitutional right to earn an honest living in the industry, as the EAAB themselves qualified us prior to their new requirements, and have issued a certificate for this existing qualification,

entitling me and others to display CEA (Certified Estate Agent) behind our names in recognition of this qualification issued by them. By proposing to revoke this qualification, which is precisely what they are proposing, they are jeopardising my constitutional and democratic right to earn an honest living.” He may well have a point. Both the legal and medical professions have undergone enormous changes over the years. Doctors, for example, now have to complete one year of compulsory community service before they are allowed to practise. The legislation, however, only applies to new graduates and has no bearing whatsoever to those who qualified in years gone by. The legal profession has also been faced with ongoing changes to the law, however, while it may have become compulsory for older practitioners to attend certain courses, no one has threatened to remove their initial qualification. Why should this be any different in the real estate industry? While further education within the real estate sector was undoubtedly a necessity, there are those who question the compulsory standards imposed on those who are already qualified and the way in which the entire process was rolled out. Stories of agents and principals paying for courses and not receiving the correct learning materials are prolific. Accredited training providers who had been endorsed by the EAAB, then had their accreditation withdrawn, leaving learners high and dry with little or no recourse, also abound. In short, it appears that the

Page 19: THE TRAINING DEBACLE

BY LEA JACOBS

legislation that was supposed to improve the industry has created a major headache for those caught up in the mess. Rathbone is determined to take the matter further and has sought legal advice as a first step to having the qualifications found unconstitutional. “We have based our claim on the fact that we have already been found competent to sell property by the EAAB and believe that once a person has qualified, they are always qualified.” When asked his opinion about the EAAB’s decision to delay the implementation of the required educational standards again and if he believed that the decision was going to help the industry in any way, Rathbone responded: “They are making a mockery of the whole thing because they know that what they are trying to do is potentially unconstitutional and illegal. The extension is just delaying the inevitable, by kicking the can down the road…again. Unless the law is changed during this extension time, giving them the authority to withdraw their initial qualifications, which is again unconstitutional, they will be exactly where they are at the moment, with empty threats and promises.” He has also approached the office of the Public Protector, which, at the time of going to press, had lodged Rathbone’s dispute with the EAAB and SSETA.

“We are also in the process of gathering information from all affected parties and are proposing to institute a class action, if need be, against the EAAB. We intend holding them accountable for loss of earnings and damages should we not find a resolution prior to the D-Day proposed. By not issuing us with Fidelity Fund Certificates timeously - they themselves will make us illegal operators.” Rathbone doesn’t believe that the EAAB understands the ramifications of their actions, which, in his opinion, will lead to the demise of the industry. “When we asked the EAAB to forward our objections and queries to the relevant departments or authorities, which included the minister responsible for our industry, we were told that it is not in their mandate to do so. We then asked for the ombudsman’s contact details, but to date have not received a response. In our opinion, the Constitutional Court may be the last resort as, in our opinion, we have an industry in crisis and it is our aim to find a resolution.”

Page 20: THE TRAINING DEBACLE

�E�n�t�r�e�p�e�n�e�u�r� �B�a�c�k� �p�a�g�e� �U�p�d�a�t�e�d� �F�e�b� �2�0�1�3

�2�1� �F�e�b�r�u�a�r�y� �2�0�1�3� �1�0�:�5�6�:�2�1� �P�M

LAND REFORM: IS THIS THE END OF PROPERTY?

Page 22: LAND REFORM

‘Let them eat cake’ has to be one of the most memorable statements made before the French Revolution, which saw the ruling royalty lose their heads. Whether Marie Antoinette actually said that is not known, but it is what she is remembered for. What do you suppose the slogan in South Africa will be? Perhaps it will be ‘let them eat promises’ after land reform becomes a reality and food production and property rights become a thing of the past. Land reform has become a hot topic and it’s little wonder why; the voices against re-opening land reform and its ugly twin sisters, the Expropriation Bill and Property Valuation Bill, are foretelling lots of doom and gloom should they come to pass, but how true is this? Land reform was formed in 1994 and entailed a three-pronged process of land reform, embracing restitution, redistribution and tenure reform. Basically the aim of land reform in 1994 was to transfer 30% of commercial farmland to black people either by restitution or redistribution. They wanted to have this finalised by 1994, then the date became 2014 and now it looks like it might only be realised by 2025. Before we look at re-opening land reform, the question must be asked, did it work the first time around? One of the problems that quickly surfaced was false claims; some had no historical foundation, while others were claimed by more than one person. False claims are worrying but even more so are claims that have been inflated by the officials involved. Another problem arose in the way the land was redistributed; rather than being divided up into the community (in the case where the land was given back to a community), it was given over to the community as a whole, who then had to decide which members were to be allowed to use the land. This naturally led to massive conflict. The restitution process for the farmers who sold their land didn’t work, dogged as it was by inefficiency; there were often delays in payment, sometimes for years. But the feather in the cap of land reform was the failure of the land reform projects. By government’s own admission, between 50% and 90% of all land reform projects have failed. Formerly successful farms have failed to produce any marketable surplus. The government has endorsed a restitution project that has cost billions of your money; only to leave hundreds of farms defunct of purpose, threatening the one thing on which we are all reliant – food production. Agri Eastern Cape president and fourth generation farmer, Ernest Pringle, has gone so far as to say, “ To date nearly all successful land claims have resulted in highly productive farms being given over to communities, and becoming unproductive, with total destruction of their infrastructures. It should be clear to even the most fanatical demagogue that turning productive commercial farms into communal farms is a certain way of terminating food production on those properties. Since this is clearly a by-product of the restitution process, it should be fairly obvious that restitution is a threat to food security as well as agricultural exports, and should be terminated as an option.” Strong words but the facts behind them can’t be ignored – threatening food production will do little to put faith in the agricultural industry and will start a mass exodus in this sector, and place South Africa on the road to starvation.

Even though the Restitution Bill will seek only to put land back in the hands of those who will use it productively, the potential productiveness of one person in charge of a new farm is not an easy thing to measure. It’s even harder to measure in advance on paper before a court. There is a range of factors that measure whether a farm will be productive or not and few people have faith that the courts will be able to accurately decide this. Instead, Dr Anthea Jeffery, the head of research at the South African Institute of Race Relations, says, “Lost agricultural production also means lost jobs on farms that used to be thriving concerns but have since collapsed. Already, some 331 000 agricultural jobs have been lost (in the period from 2001 to 2012), and some of these job losses have resulted from failed land reform initiatives. The loss of these jobs has already worsened rural poverty, while more land transfers are likely to put an end to more farm jobs – with few compensatory benefits to others – and add to destitution.” South Africa needs commercial farming to feed the millions of people who reside in urban areas. At present some 90% of food produced in South Africa comes from the country’s 37 000 commercial farmers. How many of these farmers will find themselves on the claim list if land reform is re-opened? The actual timeframe for land reform will severely compromise the security of the agriculture industry; the actual process will take two decades to complete, meaning tenure insecurity for farmers for at least the next 20 years. In terms of the actual effect on the property industry there are a number of red flags raised by the two bills, which will go hand in hand with the re-opening of land reform claims, namely, the Expropriation Bill and the Property Valuation Bill. The Expropriation Bill of 2013 has been lauded as better than its 2008 predecessor as it allows the courts rather than the state to decide the compensation payable for expropriated property, but says Dr Jeffery, “Although this seems like a major advance, in practice the gain is likely to be negated by other aspects of the Bill, in particular, it allows hundreds of organs of state to take ownership and possession of property simply by giving notice to the owner before any compensation has been paid.” In addition, the Bill also fails to recognise that, where expropriation includes a person’s home, there are eviction laws that come into play and require the express authority of the courts. The Valuation Bill in the meanwhile defines property as including ‘immovable property’, ‘rights in such property’, and ‘any movable property which is contemplated to be acquired with the relevant immovable property.’ The provision for immovable property in the Bill will allow the state to expropriate not just farmland but also farm equipment, vehicles, irrigation systems and livestock. But a far more dire aspect of this Bill is that it doesn’t just extend to farmland, even though it is being introduced by Rural Development and Land Minister Gugile Nkwinti, its provisions extend to land on which mines, factories or other buildings stand. The Expropriation Bill gives the power of expropriation to all the national and provincial departments, municipalities and organs of state. If you want to contest the compensation that has been decided by the courts for your property and land, the Valuation Bill allows the

Page 23: LAND REFORM

BY COLLEEN MAY

government to proceed directly to expropriation, regardless of whether or not there is any dispute over the compensation by the parties involved. You, as the owner, may lodge an objection with the office of the valuer-general within 30 days, and the valuer who was responsible must then ‘promptly’ (there isn’t a time limit given so promptly, could mean anything,) decide on the objection and give a written reason for his decision. If you are still not happy with the outcome, you then have to apply for a review of this decision by a ‘valuation review committee’, who are able to close its meeting to the public when deliberating on a decision. The lack of transparency in this process is frightening. Who will be ensuring that this process is fair and accurate and not touched by corruption? Once a decision has been made, that decision is final and binding and is only subject to a review by a court of law. So only after you have been through two review processes totalling who-knows-how-many days can you actually take your case to the courts, an option that in reality only the very wealthy could afford, as going through the courts is a lengthy and costly procedure for someone who has just lost their property and possibly their only source of income to the state. The Expropriation Bill will attempt to make it quicker and cheaper for the State to expropriate land for less than market value and with no mind for further losses suffered by the owner, including loss of future income.

Dr Jeffery sums up both bills perfectly, “In combination with the Expropriation Bill and the green paper, the Valuation Bill threatens the property rights of all South Africans. It clearly forms part of the ‘second phase’ of the ruling party’s national democratic revolution. Part of its aim is doubtless to make it easier to achieve ‘state ownership of all the land in the country’, as the Congress of South African Trade Unions (COSATU) has urged in order to ‘empower the democratic state to break the power of white capital’. Cosatu will in fact be getting even more than it anticipated because so much property other than farmland will also be vulnerable to cheaper and quicker expropriation by state.” The government seems to be playing fast and loose with the property rights enshrined in the constitution and it remains to be seen whether the Pandora’s box of bills will pass or not. One thing that can’t be denied is that there are surely better ways to go about addressing the wrongs of the past than destabilising food production and pushing bills through parliament that will destabilise the property industry in South Africa, an industry that contributes greatly to the economy, to job creation and wealth creation for all.

Page 24: LAND REFORM

The Rawson Property Group offers

FRanchise OPPORTuniTies in:

Rawson Properties (residential sales & administration)

Rawson Rentals (rentals & administration)

Rawson Commercial (commercial & industrial sales and letting)

Rawson Auctions (auctions of immovable property)

Own a Rawson franchise today.

Franchise opportunities: Head Office 0860 RAWSON/729766 [email protected]

career opportunities: Head Office0860 RAWSON/[email protected]

Contact us TODAY!

Visit our newly launched website at www.rawson.co.za

Become part of one of the biggest and fastest-

growing brands in the country and grow your own

business according to a highly profitable, tried-and-

tested business model, developed through decades

of personal experience. Receive expert support,

advice, training and assistance from a business

partner dedicated to your success.

The Rawson Property Group is

committed to the philosophy of

franchising through partnership.

More than meets the eye...and this is just the tip of the iceberg.

Otherwise known as the city with a conscience, Cape Town is known as the growth engine of the Western Cape. And on a national scale, it has been a top investment destination for some time. From a global perspective, the city has become a fierce competitor in attracting foreign direct investment into the country. As the city’s status of being a high return investment destination gains momentum, industry players are realigning business strategies across different sectors of the property market. Renewed focus with a global perspective on the joint benefits of long-term economic growth coupled with environmental sustainability is evident. Accelerated growth in the commercial and industrial property sectors, as well as commerce and tourism, is linked to the practice of sustainable business principles as well as the environment. A number of support

Page 26: GREEN CAPE TOWN

CAPE TOWN ACCELERATES TOWARDS ENERGY-SMART STATUS

BY ANNA-MARIE SMITH

Page 27: GREEN CAPE TOWN

structures have enabled private enterprise to gain a foothold in local markets that would bear long-term dividends. These are provided by various business forums, the City of Cape Town, the Green Building Council South Africa and the Graduate School of Business at the University of Cape Town. While fulfilling its role as facilitator in the process of strategic development and economic growth, the city has partnered with business to encourage and incentivise environmentally sound business practice. Also spreading their wings to southern shores are some South African REITs companies, now regulated to compete in global investment markets. Central to the acceleration process are the actions of the Accelerate Cape Town/KPMG Sustainability Forum. In collaboration with local business and city authorities, it aids the process of corporate implementation of green building initiatives. Chris Wheelan, CEO of Accelerate Cape Town, says South Africa currently has 35 Certified Green Star Buildings, and projections are that this number will increase to 150 by 2014, 300 by 2015 and 500 by 2016. He says examples of green building initiatives are seen nationally within different sectors of the property market. Speedy transformation in the government property sector is seeing 4-Star ratings at offices fast becoming the norm. This is setting the tone for achievements such as the Department of Environmental Affairs Head Office in Tshwane’s accreditation of the state’s first 6-Star Green Star rating, says Wheelan. Wheelan says large corporate institutions that are developing new properties, as well as those committed to upholding leases for rentals in older existing buildings, are benefiting from transformation within the property sector. He says when looking at global cities, new development and refurbishments of buildings reflect long-term vision based on tried and tested research models. Available in South Africa, he says, are locally developed models by the Green Building Council South Africa. He says these offer a wealth of research and certification training programmes to local industry, while studies such as the Davis Langdon Environmental Study of 2011 provide efficient design useful for broad applications. Another factor driving greener operating principles that go beyond green building certification is the need for commitment to corporate reputation as well as staff wellbeing. A recent example is the design and construction behind Allan Gray’s head office in Cape Town. Michael Smith says: “During the planning process Allan Gray realised that the biggest lesson of green building lies in the realisation that real substance is what gains respect from clients and employees.” He says investing is about so much more than just capital growth, but rather the finer balance between optimum productivity, occupant health and corporate reputation. Smith says the nine-month design and planning process took place in collaboration with the company’s landlord, the V&A Waterfront. During this time extensive research and feasibility studies around sustainability principles of the architectural design, construction and occupancy of No. 1 Silo were prioritised. He says: “Operating within the guidelines

of the Green Building Council South Africa went hand-in-hand with a commitment to only implement tried and tested measures with clear track records.” In addition, only those that could be applied across a broad spectrum of business principles would be implemented. Another large scale Cape Town project where impressive energy savings have been implemented is the Black River Office Park. This office development in Observatory features the biggest roof-mounted solar photovoltaic system in southern Africa. This installation, to take place over three stages, will soon be ready to take advantage of local carbon tax benefits when implemented. Estimations are that the system will save 1 725 tons of carbon dioxide per annum by not relying on electricity produced from coal. Black River Park developer and stakeholder Joubert Rabie says it makes sense to run an operation that is green and sustainable, not only because of the impact it has on the environment, but also from a good business practice point of view. He says installation costs for this system, which will operate for a minimum of 25 years, will be recouped within the first seven years. The design allows power usage throughout the park to be monitored and micro managed. From a business principle perspective, this was one of many factors taken into consideration before the Green Building Council South Africa moved its offices to Black River Park. Brian Wilkinson, chief executive of the Green Building Council South Africa, says the opportunity for tenants to be able use green energy and potentially go off grid means Black River Park meets some of the sustainable criteria for green building accreditation. Also adding to the long list of green developments in the city is Hotel Verde, which will shortly be launched in the Cape Town International Airport Industria precinct. Named as South Africa’s first green hotel, it is the brainchild of a family of foreign owners who have invested heavily in a commitment to the environmental and economic benefits of sustainable development. Their wish is for Hotel Verde to serve the hospitality, business and tourist industry with an educational model that will illustrate sustainable building as it applies to hotel accommodation. André Harms of Ecolution Consulting says his client is aiming to achieve Gold or Platinum accreditation within the stringent LEED green building certification programme. Guests at Hotel Verde will participate in a number of energy saving programmes, such as Friday night dinners served by candlelight from a wood fired pizza oven. Hotel guests will also be incentivised to reduce, recycle and reuse to minimise consumption at all levels. Of particular interest during the building site tour was a surprise view from the hotel rooms onto a green open space adjacent to the premises. Harms said this municipal retention pond, originally created to absorb water in the area, is now rented from the city by Hotel Verde in an effort to uplift the neighbouring surroundings.

There was a time, not too long ago, when agents had two major problems to contend with – finding a buyer who was seriously interested in buying a home and finding a buyer who was in a financial position to raise a bond. Thankfully, it appears that buyers are well and truly back on the scene and that the banks have once again opened the purse strings and are again writing out cheques. Overall, the property market seems to have picked up in all sectors and agents around the country are reporting an increase in sales and enquiries across the board. The demand for 100% bonds is still high with both Ooba and Bond Gallery indicating that close to 50% of bond applications received are for the full amount. Unfortunately, Elmar Pittendrigh, managing director of Bond Gallery, also notes that the decline ratio on 100% loans is still higher than in the case where a deposit is available. There has been a steady influx of first-time buyers and Kay Geldenhuys from Ooba says that 52% of bond applications received by their company comprised first-time buyers. Sadly, however, the much hyped Finance Linked Individual Subsidy Programme (FLISP), announced by President Zuma in his 2012 State of the Nation Address, hasn’t borne fruit. Daphney Klopper from the Rawson Property Group says that although the FLISP scheme looked exceptionally promising because it offered subsidies of up to R87 000 towards the purchase of a home by a first-time buyer, clients who approached the group, banks or mortgage originators for a bond making use of the scheme have not as yet seen any concrete response to their applications. Klopper says, “The banks appeared to be equally keen to implement the scheme, but when approached for this type of subsidy were almost always told that the Department of Housing was still establishing the

procedures that had to be adhered to and was not yet in a position to grant these subsidies.” She said that this was confirmed by the Western Cape Minister of Housing, Bonginkosi Madikizela, in an interview on Radio 567 Cape Talk. But, says Klopper, he apparently later told Mike van Alphen, national manager of Rawson Finance, that the department thought it essential to “educate” first-time buyers before embarking on the FLISP scheme. More recently, it was learned via the government’s website information service that the full sum set aside for these subsidies had been entirely allocated as part of the state’s R17,9-billion poverty relief programme. “Exactly to whom the grants had been made was not spelt out, but the net result was that the franchise’s potential homebuyers had clearly been left out in the cold,” says Klopper. While the lack of a subsidy may be extremely frustrating to those who desperately need a roof over their heads, it has become pretty clear that first-time buyers will benefit from ‘homeownership’ education. Interestingly, FNB’s Affordable Housing Division has taken its compulsory homeownership education programme for first-time home buyers out of the classroom and onto the web – with great success. First-time homeowners applying for a Smart Bond are expected to complete the course before registration of their bond. Of all the bond applicants, 75% are now choosing to use the e-learning system. Since its introduction of e-learning in February 2013, FNB has seen an 87% decrease in turnaround time for completion of the course from 9.8 days to an average of 1.3 days. There are currently 4 000 first-time homeowners who have either completed or are currently completing the course through e-learning. “Our homeowners programme has always been an important aspect of the bond registration process for our customers. Good quality financial education on owning a home is vital in order to ensure that homeowners

THE DEVIL IS IN THE DETAILS

Page 30: THE DEVIL IS IN THE DETAILS

High debt and the lack of a deposit continue to plague South African property buyers

understand the financial impact of their decisions and make the most of their biggest asset,” says Marius Marais, CEO FNB Housing Finance. First-time buyers aside, Nedbank reports that recent estate agent surveys indicate that smaller-sized properties are still driving activity in the residential market. “Our outlook remains positive, with the growing source of demand from the emerging middle class seeking to upgrade to better homes mostly in middle class areas,” says Timothy Akinnusi, head of sales and customer management at Nedbank Home Loans. He says that unfortunately consumers’ disposable incomes remain under pressure due to high levels of debt, mainly due to the surge in unsecured lending, which carries much higher interest rates, given the greater risk of default. Consumers are also finding it increasingly difficult to uphold credit repayments resulting in compromised credit bureau profiles. This subsequently prevents them from accessing further credit based on default payment behaviour. Nedbank’s statistics are backed up by what is going on in the marketplace. BetterBond reports that it secured bonds for 6 400 buyers during the second quarter of this year. In the same three months, the company’s statistics show that the average approved bond amount for the total market was R770 200. The average approved bond amount for first-time buyers was R619 000. Self-employed individuals are still finding it more difficult to secure bond finance. Pittendrich notes that it is definitely more challenging in terms of supporting documents required and the amount of motivation in getting the self-employed deals finalised successfully. “This is simply as a result of the responsibility on the bank to ensure that they abide by the National Credit Act (NCA) and reckless lending guidelines.” He says that the banks are required to ensure that a client is able to service his bond instalments by conducting checks on affordability and sustainability of income. In the case of a salaried person, they cannot do more than

confirm employment, income etc. with the applicant’s employer. In the case of a self-employed individual, however, the bank requires certain accounting criteria to be met regarding the financial health of the business. These include the latest set of audited financials (also previous years) and management accounts. “Personally, I do not foresee any change in this trend as it does not only rest on the bank’s appetite for lending in the self-employed space, but more so on the requirements in terms of reckless lending,” he says. The amount of debt that the average South African consumer carries continues to have a negative effect on those attempting to secure a home loan. Rudi Botha, CEO of BetterBond, says that the average household debt to income ratio is currently sitting at around 75%. “This means that although a potential borrower may have a substantial monthly income, a great deal of it is most likely being used to repay existing debt, such as vehicle and furniture repayments, credit and store card instalments, and quite likely the repayments on a personal loan. When all that is taken into account, plus the monthly regular expenses such as food, transport, utilities, insurance and school fees, there is often not enough left to afford the repayments on a home loan. As noted, the NCA requires that the banks check on this before granting any new credit, in order to avoid situations in which the consumer is over-borrowed. Of course, a large household debt load also makes it difficult for consumers to save money towards a deposit, and with the majority of buyers (65%) being required to pay a deposit in order to be granted a home loan, that is also a challenge – especially to first-time buyers who do not have any equity in an existing property to put towards a deposit,” says Botha.

BY LEA JACOBS

Page 31: THE DEVIL IS IN THE DETAILS

Page 32: FINANCE AND FIGURES

HOW DO HOME LOANS MEASURE UP?

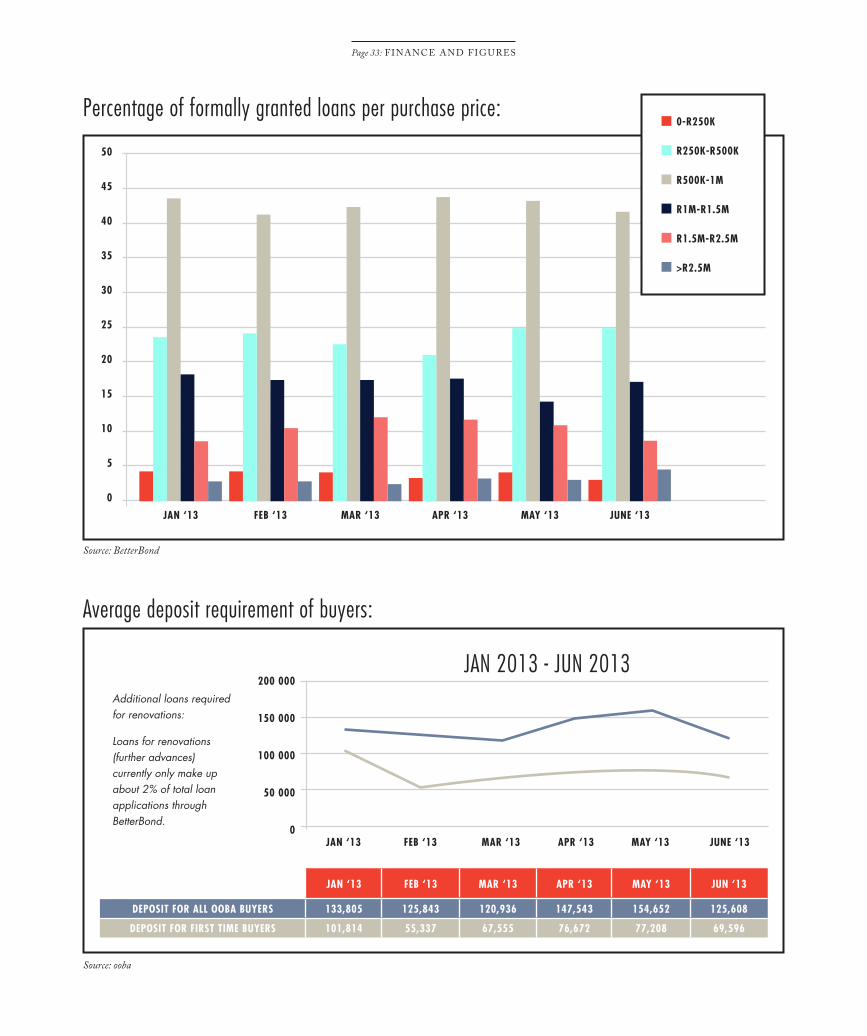

Property Professional gathered information from some of the country’s leading mortgage originators to provide some insight into what the average purchase price is per age group as well as what percentage of loans are granted per purchase price and what the average deposit amount is required for buyers. In addition, we asked what percentage of bonds have been granted with further advances for renovations. We compare statistics from January 2013 to end-June 2013:

Average purchase price per age group:

Source: BetterBond

1 400 000

1 200 000

1 000 000

800 000

600 000

400 000

200 000

0

JAN ‘13 FEB ‘13 MAR ‘13 APR ‘13 MAY ‘13 JUNE ‘13

20-30YRS

31-40YRS

41-50YRS

51-60YRS

>60YRS

Page 33: FINANCE AND FIGURES