sept. 21-23, 2011 • ft. lauderdale

TRANSCRIPT

Sept. 21-23, 2011 • Ft. Lauderdale

2010 - 2011 Accounting Shows Committee

Christine Moreno - Chair Lynn H. Clements - Vice Chair

Alan D. Campbell Lenice A. DeLuca Wayne T. DeWitt

Richard M. Dotson Gary A. Fracassi

Lucinda L. Gallagher Paulette M. Holder

Sharon S. Lassar James M. Luffman William L. Maloney

Mario R. Nowogrodzki Cecil Patterson, Jr. Robert M. Rankin

Diane J. Reich Poornima Srinivasan

Denise M. Stubbs Caridad Vasallo

Frank Ward Donna C. Zeitler

26th Annual Accounting Show September 21-23, 2011

Ft. Lauderdale

1:40-2:30pm Export Financing Strategies for Bottom .......................1 Line Results Susanne Keough Managing Director and Head of Global Trade Solutions SunTrust Bank and Keri A. Gawrych Executive Vice President-Division Sr. Credit Officer SunTrust Bank and Mary E. Hernandez Regional Manager / U.S. Small Business Administration 3:05-3:55pm Alternative Financing ......................................................18 Lunelle Siegel, EDFP Lending Manager / Corporate Funding 3:55-4:45pm Hot Topics in Bankruptcy: Debt .................................. Forgiveness and Credit Repair Edward J. Peterson, III Partner / Stichter, Riedel, Blain & Prosser, P.A.

Export Financing Strategies for Bottom Line Results

Susanne Keough Keri A. Gawrych

Mary E. Hernandez

Susanne Keough, MBA Managing Director & Head of Global Trade Solutions

SunTrust Bank

Susanne Keough manages SunTrust Bank’s trade finance and trade banking business as the head of the Global Trade Solutions Department. In this capacity she is responsible for SunTrust’s trade finance sales, compliance and portfolio management areas. Ms. Keough joined SunTrust Bank in 2002 as Vice President with trade finance and trade banking business development responsibilities for the Georgia and Tennessee markets. Prior to joining SunTrust, Ms. Keough was employed by AmTrade International Bank of Georgia in Atlanta and was the senior lender in the bank’s trade finance group, which specialized in Ex-Im Bank-supported medium-term buyer finance. From 1994 to 1998 Ms. Keough was the Export Finance Manager for the State of Georgia (Georgia Department of Industry, Trade & Tourism). In this capacity she was responsible for the development and implementation of Georgia’s export finance programs designed to assist the business and banking communities and increase exports from the state. Ms. Keough worked closely with Ex-Im Bank and SBA staff in marketing export assistance programs to Georgia exporters. Ms. Keough’s international banking career also includes employment with Citibank, in credit administration supporting the World Corporate Group, and in the international division of a predecessor to Bank of America in Atlanta. Ms. Keough is a graduate of the University of South Carolina with a BA in International Studies and a Minor in European History, and an MBA from Georgia State University with a concentration in Finance.

Keri A. Gawrych Executive Vice President,

Division Senior Credit Officer SunTrust Banks, Inc.

Keri Gawrych is Executive Vice President, Division Senior Credit Officer for SunTrust Banks, Inc. In this role, Ms. Gawrych is responsible for overseeing the credit approval process and asset quality for the South Florida Division of SunTrust Bank. She is based in Fort Lauderdale, Florida.

Ms. Gawrych assumed her current role in 2010. She began her career with SunTrust over 20 years ago where she held various relationship management and credit positions throughout the state of Florida. She then served as the Regional Senior Credit Officer for the Tampa Division of SunTrust for 8 years prior to her current position.

Ms. Gawrych is extremely active in community and civic affairs. She currently serves on the Board of Directors of the University of South Florida Foundation Board of Trustees, and is the current Chair for their Audit Committee. She was also a past Board member for Goodwill Industries. Ms. Gawrych is a lifetime and founding member of the University of South Florida Women in Leadership & Philanthropy, the Founder & Chairman of Dream Givers U.S.A., Inc., and a graduate of Leadership Tampa and Leadership Daytona.

Ms. Gawrych earned a Bachelor of Science degree in Finance from the University of South Florida, and is a Graduate of the Graduate School of Banking at LSU.

Mary E. Hernandez Regional Manager

U. S. Small Business Administration Mary Hernandez is the Regional Manager for the U.S. Small Business Administration's (SBA) International Trade Programs in South Florida and Puerto Rico. Based out of the U.S. Export Assistance Center in Miami, Florida, Mary works closely with other Federal agencies such as the U.S. Commercial Service and the Export-Import Bank of the United States to offer seamless service to the U.S. exporter. Together, they provide a wide range of programs including tools to expand into other foreign markets and to mitigate credit risk. Mary is especially focused on identifying and training lenders to participate in SBA's export finance programs- ultimately providing the working capital needed by small business exporters. During her career with SBA, Mary has also worked with its Office of Congressional and Legislative Affairs in Washington, DC, as well as its National Outreach Office based in Los Angeles, California. Mary is married with a seven year old daughter.

Export Financing Strategies For Bottom Line Results

FICPASeptember 2011

2

Agenda

I. National Export Initiative

II. Government Programs to Assist Exporters

III. Export Working Capital Financing

IV. Preparing Loan Package for Lender

V. Q&A

3

Government Support

Mary Hernandez5835 Blue Lagoon Drive, Suite 203Miami, FL 33126Phone:305-526-7425 Ext. 21E-mail: [email protected]: www.sba.gov/international

National Export InitiativeGovernment Programs to Assist Exporters

Small businesses are a critical component of the U.S. economy, but there is large room for growth via exports

However, there is much room for small businesses to grow by exporting

• Only ~250,000 U.S. Small Businesses export, however, they account for ~30% of all merchandise exports

• Additionally, of U.S. companies that export:

o 58% export to only one country, and

o 83% export to only one of four markets

Small Businesses are important job creators in the U.S. economy

• There are ~28 million small businesses in the United States

• Small businesses account for nearly 1/2 of the total U.S. private-sector payroll

• Small businesses have created ~65% of net new jobs over the past 15 years*

Small Business Jobs Act of 2010 provides additional support for SBA’s Trade Promotion and Finance Programs

DescriptionSBJA Support

Export Express Pilot Becomes Permanent; The law made the Export Express pilot loan program into a permanent program with a 90% guarantee for loans up to $350,000 and 75% for loans greater than $350,000, up to the maximum loan limit of $500,000Permanent higher loan limits for the Export Working Capital Program (EWCP) and International Trade Loan (ITL): The Act significantly increased the maximum loan sizes for EWCP and International Trade Loans to $5 million with full (90)% guaranty

Export Finance Programs

State Trade and Export Promotion (STEP) Grants Pilot: The law authorized $30 million per year for the next three years in competitive grants for states to assist small business owners to expand their exporting

Small Business Development Center (SBDC) Counselor Training: TPCC Certificate Training offered to SBDC counselors; Pilot launched at SBDC annual conference in San Antonio in 2010 with subsequent training scheduled for San Diego in 2011

Management & Technical

Assistance

Established an Independent office of International Trade: Increased Staff and Strengthened Export Counseling ResourcesStronger Inter-Agency Collaboration

Stronger Office of International

Trade

The President’s National Export Initiative has four clear goals

Support over 2 million high-quality, above-average-paying jobs tied to increased exports during this period

Support U.S. business and competitiveness along with promoting stability and market development abroad

Double U.S. exports of goods and services over the next five years

Increase the number of companies that export, AND exports to more than one market by 50 percent, respectively, over the next five years

National Export Initiative (NEI) Goals

To achieve this goal for small businesses, SBA and our federal partners have organized around four key objectives

• Identify more small businesses to begin or expand exporting1

• Prepare those businesses to export successfully2

• Connect them to export opportunities3

• Support them once they have export opportunities4

Small Business Working Group key objectives

U.S. Export Assistance Center

• U.S. Commercial Service• Marketing Intelligence• Trade Counseling• Business Matchmaking• Trade Advocacy• www.trade.gov/cs

• Export-Import Bank of the United States• Export Working Capital• Credit Insurance• Foreign Buyer Program• www.exim.gov

Partner Agencies

The SBA Office of International Trade is in your backyard

Office of International Trade Footprint

Legend

SBA’s bone-structure is leveraged for total small business support, including export promotion

In addition to the 14,000 SBDC, SCORE, and WBC counselors, SBA maintains a network of regional trade finance specialists at U.S. Export Assistance Centers

SBA District Offices (68)U.S. Export Assistance Centers (19)

10

Export Working Capital Programs

Susanne Keough, SunTrust BankGlobal Trade SolutionsPhone: 404-813-1030Email: [email protected]

Topics:International Payment RisksSBAEx-Im Bank Insured Foreign Receivables

11

International Methods of Payment

12

Commercial RisksBuyer’s ability to pay (bankruptcy, insolvency, protracted default)Seller’s ability to deliver

Political RisksGovernment or political interventionProblems with currency exchange Problems with the movement of merchandiseActs of God

Other Factors in determining the payment methodSize and type of salePrior experience with the buyerCompetition

Payment Risks and Factors

13

Selecting Payment Terms

Can the exporter afford the loss if it is not paid?Will extending credit and the possibility of waiting several months for payment still make the sale profitable?Can the sale be made only by extending credit?How long have the buyers been operating, and what is their credit history?Has the exporter sold successfully to the buyer before?Are there reasonable alternatives for collecting if the buyer does not pay? (Does the buyer’s country have the legal and business infrastructure for settling disputes fairly and swiftly?)If shipment is made but not accepted, can alternative buyers be found?

Questions to Ask:

14

Analyze Client Needs - Gather information on export business including products, sales terms, export countries, buyers, suppliers etc.Determine the best financing program (solution) for the ExporterFinancial Analysis of Borrower (Underwriting)Obtain / facilitate any guarantees and/or insurance working with Ex-Im, SBA, Insurance ProviderSunTrust is an Ex-Im Delegated Lender up to $7.5MM and also an SBA Preferred LenderFund and manage the loan processClient relationship management

Lender’s Role in Export Financing Programs

15

Criteria and ProgramRequirements

Ex-ImDelegated Authority Lender

SBA Working CapitalPreferred Lender

SBA Export ExpressPreferred Lender

IFRF

Max/Min loan amount None / $1MM $5MM / $500M $500M / $25M None / $1MM

# of years operating historyTangible net worthLocation of borrowerPersonal guaranties

1 yearPositive tangible net worthDomiciled in United States>20% owner guaranty required

1 year N/ADomiciled in United States>20% ownership guaranty required. Guarantor personal liquidity rule assessment required (liquid assets > total facility amount)

1 yearN/ADomiciled in United States>20% ownership guaranty required. Guarantor personal liquidity rule assessment required(liquid assets > total facility amount)

1 yearN/ADomiciled in United StatesN/A

Country of export Subject to Guarantor Country Limitation Schedule.Subject to SunTrust internal BSA/AML guidelines.

Subject to Guarantor Country Limitation Schedule.Subject to SunTrust internal BSA/AML guidelines.

Subject to Guarantor Country Limitation Schedule.Subject to SunTrust internal BSA/AML guidelines.

Approved by insurer

Eligible Product Criteria Exports being financed must be shipped/titled from the U.S. Inventory may include raw materials, work-in-process and finished goods

Exports being financed must be shipped/titled from U.S .Inventory may include raw materials, work-in-process and finished goods

Exports being financed must be shipped/titled from U.S .Inventory may include raw materials, work-in-process and finished goods

Subject to insurance policy requirements

Collateral Financing against inventory and A/R

Purchase Order Financing, inventory and A/R financing

General lien against all business assets

Relies on normal credit criteria but ‘domesticates’ the foreign A/R risk. Only post shipment financing

Military sales Sales are restricted to foreign military

Must adhere to SunTrust Internal Policy

Must adhere to SunTrust Internal Policy

Must adhere to SunTrust Internal Policy

Indirect Exports Exports to domestic buyers who subsequently export is allowed

Exports to domestic buyers who subsequently export is allowed

Exports to domestic buyers who subsequently export is allowed

Refer to policy guidelines

US content requirement 51% US content requirement N/A N/A N/A

Export Working Capital Financing

16

Export Credit Insurance

Allows the seller to sell on open account terms Mitigates the foreign buyer payment riskMitigates commercial and political risks Policies usually cover terms up to one yearDoes not cover product disputesExport credit insurance makes foreign receivables eligible for financing; policy can be assigned to LenderExport Credit Insurance is available from:• Export-Import Bank of the United States • Private insurers (Euler, Atradius, etc)

Insurance brokers can assist in “shopping” for the best policy (e.g. rates, coverages, deductibles) and administering the policy

17

Consult a bank with international trade finance experience in your local market

Determine financing strategy based on:Volume of exporting and transaction sizeRisk tolerance of exporterExport market risks, diversification/concentrationCash flow cycles and Payment termsUS vs Non-US content of goodsIndustry norms for sales termsCurrency issues

International Finance Strategy

18

SBA Export Lender of the Year 2010 & 2011

National Recognition as Small Business Export LenderTwo Years in a Row!!!

19

Preparing Financial Package for Lender

Michael Walker, SunTrust BankCommercial Banking Manager515 E. Las Olas BlvdFt. Lauderdale, FL 33602Phone: (954)765-7482Email: [email protected]

Topics:Underwriting role of bankFinancial information needed for underwritingBackground Information helpfulKey Elements of Financial ReviewEx-Im Bank ratiosInsured Foreign Receivables

2020 | ©Copyright 2007 SunTrust Banks, Inc.

Loan Underwriting Done by Bank

Commercial banks that are Delegated Authority Lenders withthe Export Import Bank handle the underwriting without pre-approval from Ex-Im BankCommercial banks that are Preferred Lenders with SBA’sExport Programs handle the underwriting without pre-approval from SBACommercial Bankers active with export financing help the exporter assess the right program for their needsExporters do not need to deal directly with SBA or ExIm Bank to obtain financing from these programs

2121 | ©Copyright 2007 SunTrust Banks, Inc.

Financial Information Required by Bank

3 Years financial statements and tax returns on company (size of deal may require CPA reviewed or audited statements)Interim statementsA/R aging showing Foreign A/R by country and debtorInventory reportPFS and tax returns on principals with more than 20% ownershipMore detailed and complete information results in higher approval rates and quicker turnaround times

2222 | ©Copyright 2007 SunTrust Banks, Inc.

Helpful Background Information

Company history (type of business, export experience, etc.)Business Plan if availableOwnership/Management backgroundProduction Information (U.S. content value)Export Credit Insurance policy (if applicable)Export Transaction information

Countries Exporting toProduction/delivery cyclesPayment terms/methodsNumber & types of buyersLoss historyBuyer profiles (end user, distributor, etc)

23

Key Elements of Financial Review

Management expertiseHistorical Cash FlowDebt Service CoverageLeverageLiquidityQuality of collateral

23 | ©Copyright 2007 SunTrust Banks, Inc.

24

ExIm : Industry Comparison of Financial Ratios

Ex-Im Bank Working Capital Loans OnlyTo approve a loan under a bank’s delegated authority, as well as to determine the Ex-Im Bank fees, the lender must calculate certain ratios to determine if the exporter meets or exceeds at least four out of seven ratios (lower quartile) on an annual basis which are calculated based on their FYE financials. These ratios are compared to the prospect’s industry analysis from the RMA Annual Statement Studies, sorted either by Sales or by Assets. These ratios include:Current Ratio Net Sales/Total Assets Debt to Worth Ratio (Net Profit + Depreciation + Depletion + Amortization Expense)/Current Portion of Long Term Debt EBIT/Interest Cost of Sales/Inventory Sales/Accounts Receivable

24 | ©Copyright 2007 SunTrust Banks, Inc.

Alternative Financing

Lunelle Siegel, EDFP

Lunelle M. Siegel, EDFP Lending Manager Corporate Funding

Lunelle Siegel is Lending Manger at Corporate Funding. For over 25 years Lunelle has financed small and medium sized companies, not only at major regional commercial banks including First Union and Barnett but also at national finance companies including GE Capital and Textron Financial. She has worked in the areas of conventional lending, SBA lending, import/export finance, factoring, asset based lending, and real estate construction lending on commercial, investment and residential projects. To address the needs of business during the capital freeze, she formed Corporate Funding in November. She assists companies seeking capital obtain it through her extensive database of sources. Her sources include lines of credit secured by receivables, inventory, purchase order, real estate, and equipment. She also assists banks assessing refinance options for their problem loans, and refinancing ones that are viable. Lunelle is accredited as an Economic Development Finance Professional through the National Development Council. She earned her B.S. in Finance from Florida State University. Lunelle is a tenacious advocate for small business and is a frequent speaker, panelist and moderator at business assistance events, professional development meetings and conferences. Lunelle currently serves on the International Board of the Turnaround Management Association (TMA), and is on the editorial board of the “Journal of Corporate Renewal”. She is immediate past Vice President of Membership, Internationally. She is Immediate Past President of the Florida Chapter of the TMA. Lunelle currently serves on the Loan Committee of Gulf Coast Business Finance, the St. Petersburg based SBA 504 Certified Development Company.

1

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

CREDIT MARKET UPDATESummer 2011

“SIZE MATTERS”

September 22, 2011– Ft. Lauderdale –26th Annual Accounting Show

2

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

2 YEARS AGO

3

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Source: Federal Reserve Board “The January 2009 Senior Loan Officer Opinion Survey on Bank Lending Practices”

WHERE WE WERE

4

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

2009 - TMA MEMBERS PREDICT THAW

Source: Turnaround Management Association May 2009 Trendwatch Poll –www.turnaround.org

5

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

SINCE THEN?• TARP - $50B• Unemployment - $2B Florida debt

6

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

7

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

8

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

SINCE THEN

FAILED BANK

9

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

10

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

11

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

EFFECT ON BUSINESS LENDING?

12

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Tier 1 Capital < 8%

2 Types of BanksCan Do and Can’t Dos

Tier 1 Capital > 8%•Probably under a public order•Internal Focus•Capital locked into criticized

assets Order Provisions for- Flushing of ‘classified assets’- Prohibition on restructuring of

‘classified assets’

-Deemed well-capitalized-Seeking to employ assets for ROE

CriticizedAssets

13

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Typical “Order” Provisions• Charge off Classified Assets

Time Charge off %90 days 15%180 days 25%360 days 45%720 days 75%

•Prohibition on Extension or Renewal of Credit toClassified Borrower

14

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

TYPICAL ORDER PROVISIONS

• Concentration of Credit Reduction Plan– Heavily Concentrated in CRE

• ADC Capped at 100 percent of total risk-based capital

• Total commercial real estate loans, capped at 300 percent or more of the institution's total risk-based capital

15

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

PROBLEM LOANS?

“YOUR LOCAL COMMUNITY BANKER”

16

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Bank Name City Core

CapitalCortez Community Bank Brooksville 9.60

LandMark Bank of Florida Sarasota 0.26

Old Harbor Bank Clearwater 0.63

First Peoples Bank Port Saint Lucie 1.31

Sunrise Bank Cocoa Beach 1.33

First Commercial Bank of Tampa Bay Tampa 1.55

Southshore Community Bank Apollo Beach 2.04

First Guaranty Bank and Trust Company of Jacksonville Jacksonville 2.37

The Royal Palm Bank of Florida Naples 2.48

The First National Bank of Florida Milton 2.69

First City Bank of Florida Fort Walton Beach 2.88

OptimumBank Plantation 3.54

Bank of Naples Naples 3.90

17

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

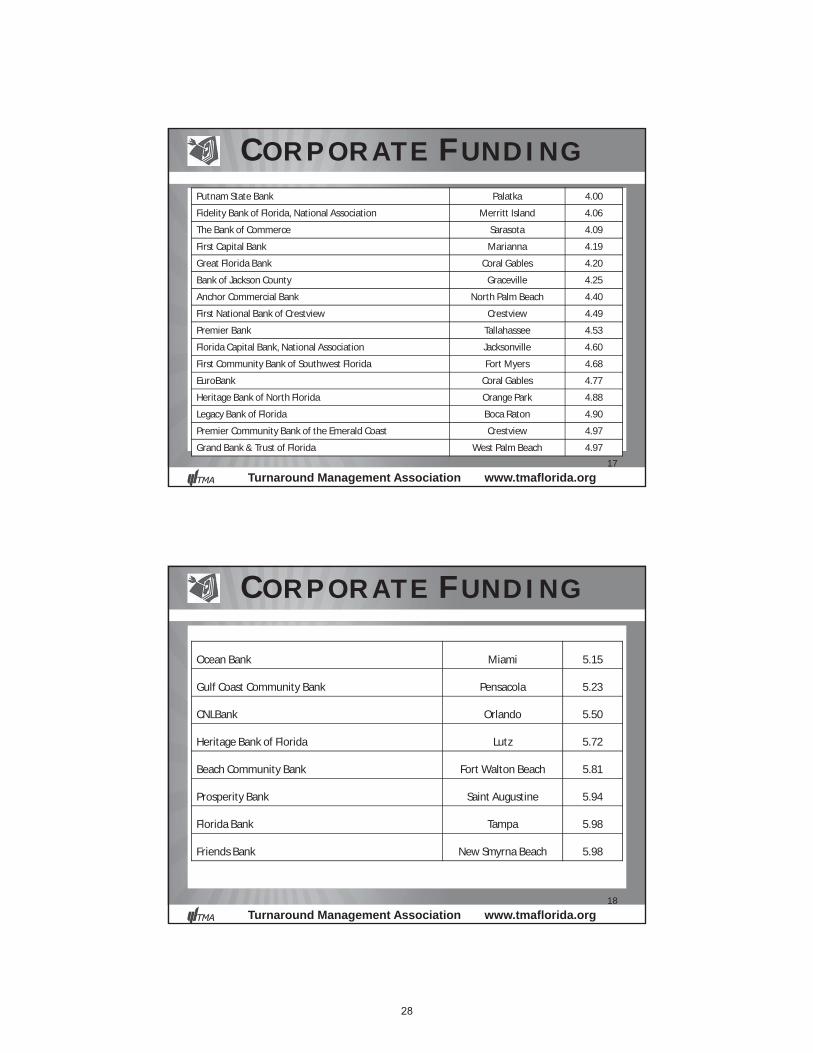

Putnam State Bank Palatka 4.00

Fidelity Bank of Florida, National Association Merritt Island 4.06

The Bank of Commerce Sarasota 4.09

First Capital Bank Marianna 4.19

Great Florida Bank Coral Gables 4.20

Bank of Jackson County Graceville 4.25

Anchor Commercial Bank North Palm Beach 4.40

First National Bank of Crestview Crestview 4.49

Premier Bank Tallahassee 4.53

Florida Capital Bank, National Association Jacksonville 4.60

First Community Bank of Southwest Florida Fort Myers 4.68

EuroBank Coral Gables 4.77

Heritage Bank of North Florida Orange Park 4.88

Legacy Bank of Florida Boca Raton 4.90

Premier Community Bank of the Emerald Coast Crestview 4.97

Grand Bank & Trust of Florida West Palm Beach 4.97

18

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Ocean Bank Miami 5.15

Gulf Coast Community Bank Pensacola 5.23

CNLBank Orlando 5.50

Heritage Bank of Florida Lutz 5.72

Beach Community Bank Fort Walton Beach 5.81

Prosperity Bank Saint Augustine 5.94

Florida Bank Tampa 5.98

Friends Bank New Smyrna Beach 5.98

19

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Freedom Bank of America Saint Petersburg 6.14

Citizens Bank and Trust Frostproof 6.18

Community Bank of Broward Dania Beach 6.19

Central Florida State Bank Belleview 6.21

Marine Bank & Trust Company Vero Beach 6.22

Pinnacle Bank Orange City 6.29

FLAGLER BANK West Palm Beach 6.30

GulfSouth Private Bank Destin 6.31

Bank of Coral Gables Coral Gables 6.39

FineMark National Bank & Trust Fort Myers 6.44

Calusa National Bank Punta Gorda 6.47

Sabadell United Bank, National Association Miami 6.50

International Finance Bank Miami 6.51

ProBank Tallahassee 6.61

Security Bank, National Association North Lauderdale 6.76

Highlands Independent Bank Sebring 6.86

Independent Banker's Bank of Florida Lake Mary 6.95

Citizens First Bank The Villages 6.95

Paradise Bank Boca Raton 6.99

20

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Florida Citizens Bank Gainesville 7.04

U. S. Century Bank Doral 7.05

BRANNEN BANK Inverness 7.24

First Bank Clewiston 7.25

Orange Bank of Florida Orlando 7.32

The Palm Bank Tampa 7.34

USAmeriBank Largo 7.38

Biscayne Bank Miami 7.51

First National Bank of the Gulf Coast Naples 7.54

FIRST STATE BANK OF THE FLORIDA KEYS Key West 7.65

Cornerstone Community Bank Saint Petersburg 7.67

East Coast Community Bank Ormond Beach 7.71

CenterState Bank of Florida, National Association Winter Haven 7.75

Alarion Bank Ocala 7.75

Community Bank of Florida, Inc. Homestead 7.90

The Jacksonville Bank Jacksonville 7.96

Charlotte State Bank Port Charlotte 7.97

21

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org 21

Source: Atlanta Federal Reserve Bank

22

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

COMMERCIAL LOAN DEMAND

Source: Federal Reserve Board “The April 2011 Senior Loan Officer Opinion Survey on Bank Lending Practices”

23

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

REAL ESTATE LOAN DEMAND

Source: Federal Reserve Board “The April 2011 Senior Loan Officer Opinion Survey on Bank Lending Practices”

24

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Pepperdine Private Capital Markets Project Summer –Survey Report V – Summer 2001

25

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

WHAT’S THE WEATHERLIKE FORBUSINESSCREDIT?

26

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

FREEZE THAWING“Credit Conditions….finally starting

to return towards ‘normal’”

Source: Greenwich Associates April 2011 Report “Credit Conditions (Finally) Normalizing for U.S. Small Businesses”

27

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

CREDIT AVAILABILITY THEN & NOW

Source: TMA Trend-Watch Credit Survey - prelim June 2011

Tighter

Looser

About the Same

28

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

BANKS – RELAXING CREDIT

Source: Federal Reserve Board “The April 2011 Senior Loan Officer Opinion Survey on Bank Lending Practices”

29

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Easy Money Tight Credit

30

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

WHERE’S THE MONEY?

Source: TMA Trend-Watch Credit Survey - prelim June 2011

Large Institutions

Small Institutions

Private Equity

Hedge Funds

Other

31

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

REDUCED PRICING

Source: Federal Reserve Board “The April 2011 Senior Loan Officer Opinion Survey on Bank Lending Practices”

32

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

BIG DEAL TRENDS

•Pricing Competition•Easing loan covenants•Larger Holds (less syndications)•Syndications with few or no covenants

33

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

BIG BUSINESSES

34

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

WHO?

Source: TMA Trend-Watch Credit Survey - prelim June 2011

35

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

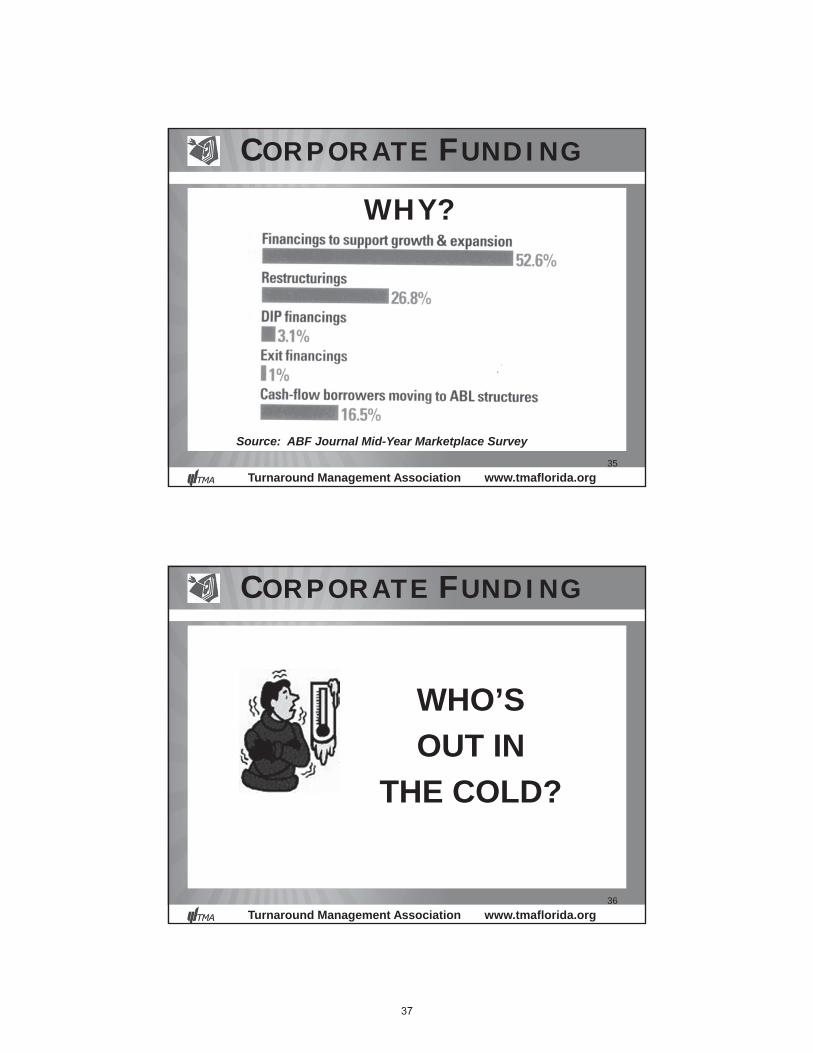

WHY?

Source: ABF Journal Mid-Year Marketplace Survey

36

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

WHO’SOUT IN

THE COLD?

37

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

“”WHO’s ASKING?”Small Businesses Middle Market Businesses

Source: Greenwich Associates April 2011 Report “Credit Conditions (Finally) Normalizing for U.S. Small Businesses”

38

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

SMALL BUSINESSES

Pepperdine Private Capital Markets Project Summer –Survey Report V – Summer 2011

39

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

SIZE MATTERS

40

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

STILL FROZEN INDUSTRIES

•Real Estate, esp. Home Builders•Housing Industry as a whole•Bankruptcy Financing: DIP and Exits

41

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

42

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

$ Volume of Single-Asset Real Estate Transactions

Source: REIS, Inc.

43

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

HOW LOW WILL IT GO?

Source: Scotsman Guide Loan Post

44

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Source: Scotsman Guide Loan Post

RE UNDERWRITING TIGHTENING

45

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Source: Federal Reserve Board “The April 2011 Senior Loan Officer Opinion Survey on Bank Lending Practices”

MEDIA ALERT –BANKS RELAX on REAL ESTATE LENDING

46

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

47

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

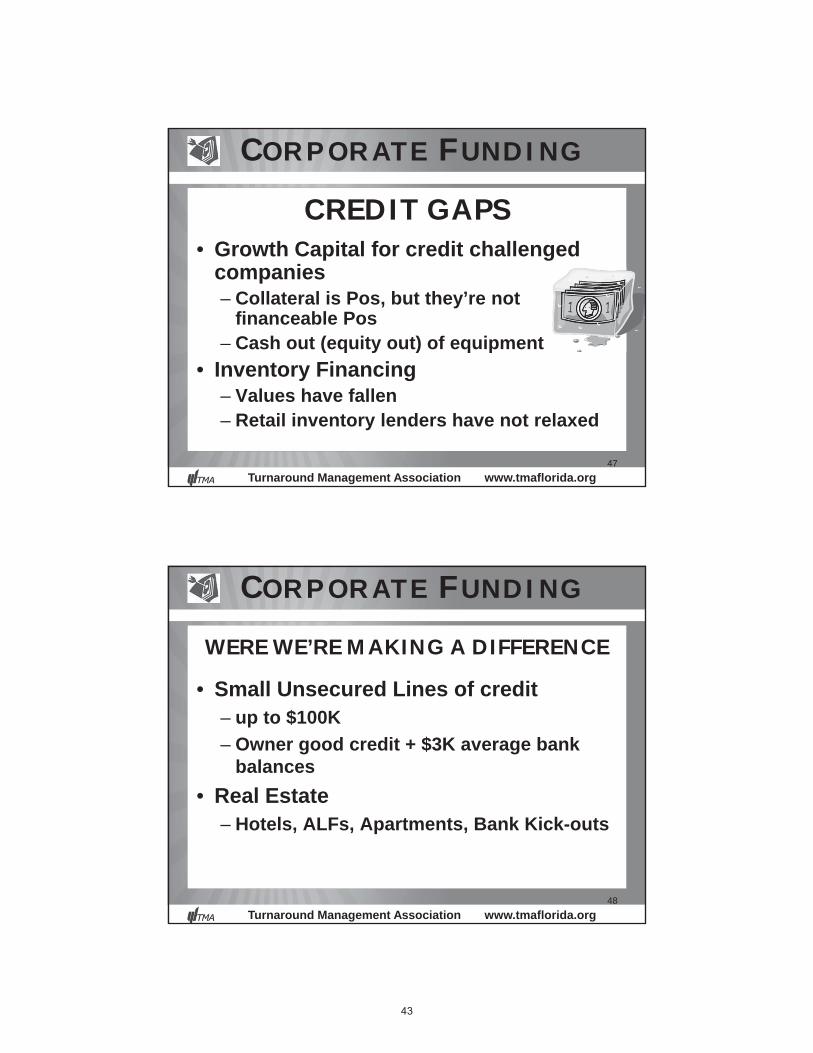

CREDIT GAPS• Growth Capital for credit challenged

companies– Collateral is Pos, but they’re not

financeable Pos– Cash out (equity out) of equipment

• Inventory Financing– Values have fallen– Retail inventory lenders have not relaxed

48

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

• Small Unsecured Lines of credit – up to $100K– Owner good credit + $3K average bank

balances• Real Estate

– Hotels, ALFs, Apartments, Bank Kick-outs

WERE WE’RE MAKING A DIFFERENCE

49

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

BRIGHT SPOT!

SBA 504 Loan Expanded for Debt Refi!

•90% Loan/value•SBA or USDA Debt not included•2 Years operating history•Current for last 12 months•No creditor short pays•2 year old debt•10 year Equipment•20 year Real Estate

50

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

WERE WE’RE MAKING A DIFFERENCE

• Fast Growth Companies with A/R & Inventory– $500K up to $10MM

• Turnarounds with A/R & Inventory– Construction subs and materials suppliers

• Story Credits

51

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

THE FUTURE?

52

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

FUTURE LOAN DEMAND

Source: Greenwich Associates April 2011 Report “Credit Conditions (Finally) Normalizing for U.S. Small Businesses”

53

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

NON-BANK REVOLVERS

Source: ABF Journal Mid-Year Marketplace Survey

54

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

CONCERNSLenders

1. Competition - 85%

2. Fiscal & Regulatory Policies – 53%

3. Rising Commodity Prices - 30%

Source: ABF Journal Mid-Year Marketplace Survey

55

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

#1 CONCERN

1. Government Regulations & Taxes- 31%

2. Economic Uncertainty - 18%

3. Access to Capital - 14%

Pepperdine Private Capital Markets Project Summer –Survey Report V – Summer 2001

Borrowers

56

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

MY CONCERNS1. Loss of Banks as capital providers to Small

Businesses

Source: www.census.gov/smallbus.html

57

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

CAUSED BY:• Persistent Regulation with unintended

consequences

• Loan Accounting Standards – FASB 5 & 114

58

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

MY CONCERNS

• PENDULUM at BIG BANKS

• Instability of Real Estate Value– Regulatory flushing of bank criticized

assets prevent a bottom

59

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

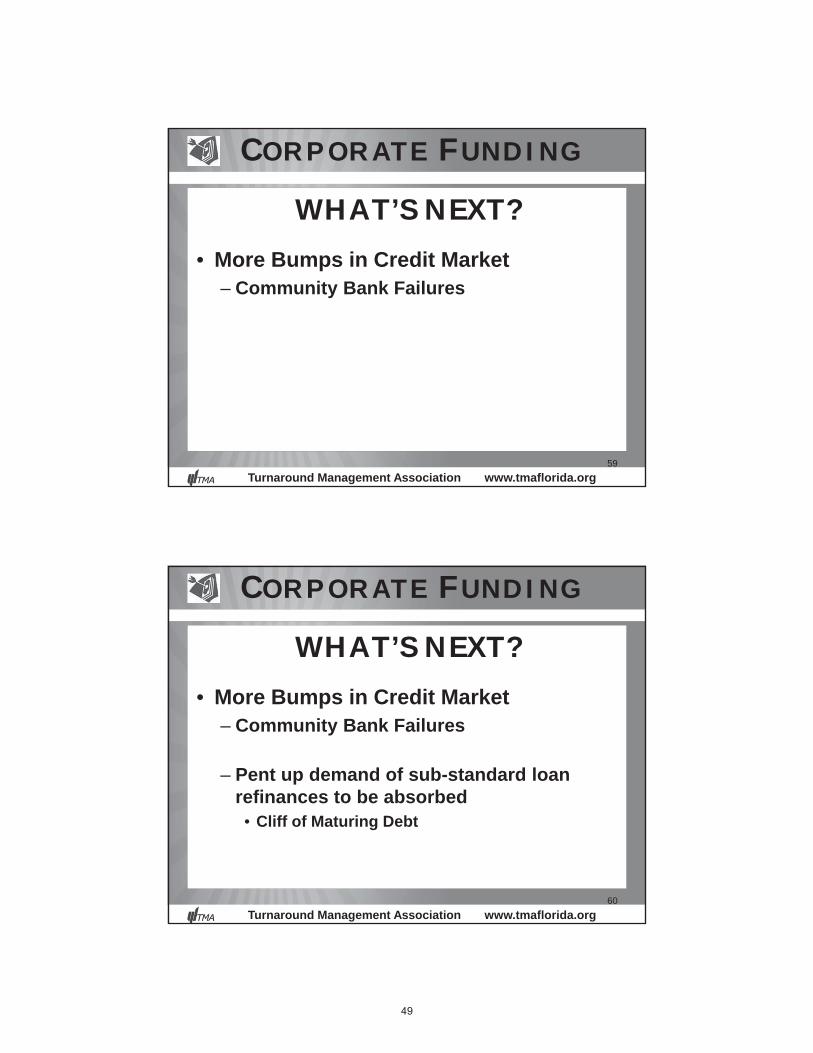

WHAT’S NEXT?

• More Bumps in Credit Market– Community Bank Failures

60

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

WHAT’S NEXT?

• More Bumps in Credit Market– Community Bank Failures

– Pent up demand of sub-standard loan refinances to be absorbed

• Cliff of Maturing Debt

61

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

“The Cliff”

Source: Standard & Poor’s LCD

62

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

WHAT’S NEXT?• More Bumps in Credit Market

– Community Bank Failures

– Pent up demand of sub-standard loan refinances to be absorbed

• Cliff of Maturing Debt• “Extend and Pretend (Amend) will soon end as

Community Banks fail

63

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

EXTEND & PRETEND

64

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

PROBLEM LOAN?

“YOUR BIG BANK “SPECIAL” BANKER or FDIC AUCTION INVESTOR

65

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

66

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

67

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

“SPECIAL ASSET” CLIENT TIPS

•Be Proactive don’t IGNORE the problem!•Communicate, communicate, communicate•Document review:

•Defects•X Guaranty•X Default•Depository Agreements offset

•Hire a Pro•Develop Sustainable Plan•Communicate Plan with 13 week cash flow forecast

“When it Really Matters”

68

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

REQUESTED VIEWING

69

CORPORATE FUNDING

Turnaround Management Association www.tmaflorida.org

Q & A

Lunelle Siegel, EDFPFunding Manager

Corporate [email protected]

888-831-9477

International Board Directorsof Turnaround Management AssociationImmediate Past Present, Florida Chapter

Hot Topics in Bankruptcy, Debt Forgiveness and Credit Repair

Edward J. Peterson, III

Edward J. Peterson, III Partner

Stichter, Riedel, Blain & Prosser, P.A. Edward J. Peterson, III specializes in the representation of debtors and creditors in out-of-court workouts, bankruptcy cases and proceedings, and state court proceedings. He is co-lead counsel with Russell Blain in the Chapter 11 case of Taylor, Bean & Whitaker Mortgage Corp. that was recently filed in Jacksonville, Florida with approximately $1 billion in assets and liabilities. He has successfully represented numerous debtors in possession in the Middle District of Florida, was active as counsel for the Creditors’ Committee in the massive Anchor Glass Chapter 11 case, and serves as conflicts counsel in the Bill Heard Chevrolet cases pending in the Northern District of Alabama. He also appears in state courts in connection with civil litigation arising out of loans secured by real estate. He serves as a Director of the Tampa Bay Bankruptcy Bar Association, has published several articles on bankruptcy issues, and has spoken on multiple occasions on insolvency issues in Florida and Alabama. Mr. Peterson joined Stichter Riedel in 2005 after four years with the firm of Bradley Arant Rose & White, LLP, in Birmingham, Alabama. While at Bradley Arant, he appeared on behalf of creditors in a number of large bankruptcy cases, including Kmart, Service Merchandise, Encompass Services Corporation, Just for Feet, CEI Roofing, and The Resort at Summerlin. Mr. Peterson assisted in the debtor representation of J.A. Jones and 57 of its subsidiaries in Chapter 11 cases filed in Charlotte, North Carolina, involving over $3 billion in creditor claims. Additionally, he had extensive involvement representing the debtors in the Pride Restaurants, LLC Chapter 11 case involving a chain of fast food restaurants, and a Chapter 9 case involving the representation of a theme park owned by various municipalities.

The Bankruptcy Process and Other Hot Topics in Bankruptcy

Edward J. Peterson, III

Stichter, Riedel, Blain & Prosser, P.A. 110 E. Madison Street

Suite 200 Tampa, Florida 33602

(813) 229-0144 – phone (813) 229-1811 – fax [email protected]

Introduction

The purpose of this paper is to provide information to accountants whose clients may be

experiencing financial troubles. This paper will explore the different options that may be

available for those in financial trouble. This paper will primarily focus on the legal intricacies

and business issues involved in a Chapter 11 reorganization case. Although there were a number

of ways of organizing these materials, the most logical one seemed to be on a chronological

basis. Thus, the decision-making process is discussed first. The decision to file Chapter 11 can

often be an agonizing one to make, and an intelligent decision can only be made if there is a

complete understanding of the general framework of Chapter 11 as well as the specific benefits

and disadvantages of a filing. Next follows a discussion of what is necessary to prepare for the

filing, surviving during Chapter 11, and the confirmation process.

I. Overview of Chapter 11 and Other Chapters of the Bankruptcy Code

A. Chapter 11 and Its Purpose

Congress enacted Chapter 11 to allow, and indeed encourage, the rehabilitation

rather than the piece-meal liquidation of financially distressed entities. In a Chapter 11, the

corporate debtor remains in possession of its assets and in control of its affairs. The Chapter 11

debtor can continue to operate in the ordinary course of business without further court approval.

Because Chapter 11 does give the debtor broad powers and protections, management should

understand its provisions even if a filing is not desirable for other reasons. This threat of a

Chapter 11 filing is sometimes enough to bring creditors to an agreement which would not

otherwise be reached. The goal of Chapter 11 is to reorganize the debtor through a plan of

reorganization which will restructure its debt.

B. Benefits of Chapter 11

There are numerous benefits of a Chapter 11 case, including the following:

i. Continuation of Business Operations. The operation and management of the

debtor’s business, ordinarily as a debtor-in-possession, continues during the Chapter 11 case,

subject only to any restrictions imposed by the bankruptcy court or applicable law. The court

may order the appointment of a trustee for cause if the court finds the existence of fraud,

dishonesty, incompetence, or gross mismanagement or if it finds that such appointment would be

in the best interest of the estate.

ii. The Automatic Stay. The filing of the bankruptcy case operates as an

automatic stay of virtually every type of creditor action taken against the debtor. The purpose of

this automatic stay is to give the debtor a breathing spell in order to reorganize. Although there

are certain exceptions to the automatic stay, those exceptions will not seriously impact most

Chapter 11 debtors. In the case of individual debtors, divorce and domestic support proceedings

are generally not stayed. Criminal proceedings against individuals or corporations are generally

not stayed, and certain enforcement actions by governmental entities are not stayed.

Nevertheless, the “garden variety” creditor enforcement actions are stayed.

iii. Ability to Assume Beneficial Contracts and to Reject Burdensome

Contracts. Under the Bankruptcy Code, the debtor-in-possession has the ability to assume

executory contracts and unexpired leases which are beneficial to it and to reject those which it

regards as burdensome. Absent a bankruptcy filing, if the debtor is in default under a valuable

contract, there is a risk that the contract will be terminated under non-bankruptcy law.

iv. Continued Use of Property Under Section 363 of the Bankruptcy Code. A

debtor-in-possession may continue to use, lease, and sell its unencumbered property in the

ordinary course of its business without bankruptcy court approval. If the property is encumbered

by a lien or security interest, the debtor is authorized to continue to use it without prior court

order unless the property constitutes “cash collateral”. In the case of cash collateral, the

bankruptcy court may condition the use, sale, or lease of such collateral upon the debtor’s

furnishing adequate protection to the secured creditor. Adequate protection is a very elastic

concept and courts have determined that a secured creditor may be adequately protected even

though a debtor-in-possession does not comply with loan terms and covenants and even though it

makes no payments to the secured creditor during the bankruptcy.

v. Borrowing of Funds. Pursuant to Section 364 of the Bankruptcy Code, a

bankruptcy court may authorize the debtor-in-possession to borrow funds and may grant to the

lender a variety of rights, including granting to its loan a priority in repayment over all

prepetition unsecured creditors, as well as priority in repayment over post-bankruptcy

administrative expenses, and a lien on assets.

vi. Avoiding Powers and Related Theories. A debtor-in-possession has the

same rights as a trustee in a Chapter 7 bankruptcy case to recover preferential transfers to

creditors, to avoid unperfected or statutory liens, and to recover transfers or avoid obligations

which are constructively or actually fraudulent as to creditors.

vii. The Establishment of a Bar Date for Filing of Claims and Centralized

Forum for Litigation of Claims. The bankruptcy court must establish a bar date for the filing of

proofs of claim. This will force all disputed and unliquidated claims to be filed with the

bankruptcy court where the claims will be subject to objections by the debtor. The normal forum

for the litigation of any disputed claims against the debtor is the bankruptcy court, and such

litigation is regarded as a core matter. Further, actions pending in other courts may be removed

to the bankruptcy court for determination there (assuming, of course, that the bankruptcy court

has jurisdiction).

viii. Income Tax Advantages Under Section 108 of the Internal Revenue Code.

The discharge (or forgiveness) of debts in a Chapter 11 case does not result in taxable income to

the debtor-in-possession. Although the debtor may have to reduce various tax attributes such as

net operating loss, carry forwards, or basis in assets, this benefit can be very substantial from a

cash standpoint.

ix. Plan of Reorganization. The key benefit to a debtor comes with the

confirmation of the reorganization plan. The plan can and frequently does, result in the

following:

1. A reduction in the amount of claims against the debtor, providing both

balance sheet and future cash flow relief;

2. An extension of payments to secured creditors, taxing authorities, and

unsecured creditors, providing further cash flow relief;

3. A discharge of claims which are unknown, speculative or conjectural

(provided that appropriate notice was given);

4. The requirement that payments to the IRS be applied to the trust fund

portion of taxes, providing relief to other parties responsible for

payment of trust fund amounts; and

5. Relief from certain documentary stamp and similar taxes.

x. Ability to Sell Assets Free and Clear of Liens and Encumbrances. The

liquidation of assets is possible through a Chapter 11 case. Section 363 of the Bankruptcy Code

provides a framework for debtors to sell assets free and clear of liens, claims, and encumbrances.

The bankruptcy court may order that all such liens, claims, and encumbrances be transferred to

the proceeds of the sale, may enjoin actions against the purchaser by creditors of the debtor, and

may retain jurisdiction to enforce the injunction and resolve disputes over the assets.

C. Drawbacks of Chapter 11

i. Restrictions on Management’s Decision Making Process. As discussed

above, no prior court approval is needed for ordinary course type transactions. The same rule

does not apply to decisions out of the ordinary course of business. The debtor can use, sell, or

lease property out of the ordinary course only with court approval.

ii. Required Disclosures. A debtor in a Chapter 11 case is subjected to a level

of scrutiny that is unfamiliar to most business owners. Information must be provided in the

schedules of assets and liabilities and in the statement of financial affairs that are filed with the

court shortly after the Chapter 11 petition. If the debtor operates a business, as is the norm in

Chapter 11 cases, then the debtor must file periodic operating reports.

iii. Costs of Administering the Case. Chapter 11 cases can be expensive.

iv. Prohibition Against Payment of Pre-Petition Claims. A debtor-in-

possession is prohibited from paying pre-petition unsecured claims during the pendency of the

Chapter 11 case. The types of pre-petition debt that may be excepted from this rule are wages or

benefits to employees to the extent that such wages are paid in arrears and payments to sole

source suppliers whose continued furnishing of goods is essential to the debtor’s reorganization.

v. Impact on Customers. The filing of a Chapter 11 petition will introduce a

level of uncertainty to customers for at least some types of debtors. The businesses that will be

most affected are those that depend upon longer term relationships with customers. For example,

since homes take months to construct, a home builder involved in a Chapter 11 case can expect

his competitors to urge potential customers to select a builder not involved in bankruptcy. Other

entities engaged in the construction business may find a loss of business from a Chapter 11 case.

On the other hand, retail businesses which can ensure a good supply of inventory and which do

not provide warranty contracts or service contracts to customers are likely to be less impacted by

the Chapter 11 case.

vi. Delay. Chapter 11 cases, like any other court proceedings, are subject to

delays attributable to the court’s calendar and the like.

vii. Cashflow. The accumulation of cash prior to the Chapter 11 case may well

be the difference between success and failure. On the negative side, the debtor can expect the

following demands on its cash reserves after the Chapter 11 filing:

1. Credit terms may be generally unavailable from trade creditors and

these creditors may require C.O.D.

2. Ultimately the cost of administering the case will have to be paid as

administrative expenses.

3. Account debtors of a Chapter 11 debtor may delay payments of

amounts due to the debtor in order to determine whether the Chapter

11 case will be successful.

4. Customers concerned about the reliability of the debtor as a continued

source of supply may curtail purchases, thus reducing revenues.

D. Alternatives

i. Out Court Workout. An out of court workout is normally an attractive

alternative for a debtor. It is a more viable option for those debtors that can ascertain what cash,

future revenues, or other property will be available for distribution to creditors after reserves

sufficient for future operating expenses and working capital are established. For a debtor in the

midst of a significant operational restructuring or industry-wide slump, there may be no clear

answer to the question of what can be paid to creditors. The first rule is any going concern value

must be preserved at all costs. If this can only be done over months or years, Chapter 11 may be

the only real alternative. Ordinarily, the fewer the creditors from whom concessions are needed,

the greater the chances of a successful out of court workout. For example, a single-asset real

estate entity with one large secured creditor and few trade creditors will almost invariably file a

Chapter 11 case only after negotiations with the secured creditor have reached an impasse. In

contrast, a debtor with numerous creditors from whom substantial concessions are needed will

find it almost impossible to achieve the unanimity that is required in an out of court workout.

One feature that is frequently included within loan documents arising from out of

court workouts with secured creditors is a provision which purports to give the secured creditor

additional rights in the event of a bankruptcy case (such as consensual relief from the automatic

stay) or factual admissions designed to result in relief from the stay, dismissal of the case, or

similar action. Generally, cases hold that such provisions will not have a preclusive effect but

many of the cases recognize that the presence of such agreements is a factor that courts will

consider in determining whether to grant relief from the stay, dismiss the case, or take other

action against the debtor. The major danger to the debtor in one of these restructurings is that it

will give the secured creditor too much control over its assets. It is particularly frustrating for an

attorney to meet for the first time with a client who has already granted liens on all of its assets to

creditors, transferred all of its spare cash to creditors, obtained and delivered parent or related

party guaranties, or entered into contracts agreeing not to file Chapter 11 and not to oppose relief

from the stay, all in exchange for a short extension of a maturity date. One cardinal rule for a

debtor in such negotiations is to make sure that the concessions obtained from the creditor are

equal to the concessions granted to that secured creditor in the form of collateral, cash,

guaranties, or covenants.

ii. Liquidation Under Chapter 7. Chapter 7 is rarely a viable alternative for a

corporation. There are almost always superior alternatives for a corporate debtor than a Chapter

7 case. These alternatives include liquidation in Chapter 11, non-judicial liquidation outside of

bankruptcy, and state-law liquidation.

iii. Chapter 13 Debt Adjustments (for individuals only). Chapter 13 is available

only for individuals who have a regular source of income and non-contingent, liquidated,

unsecured debts of less than $360,475.00 and similar secured debt of less than $1,081,400.00. A

Chapter 13 petition can be an individual petition or a joint petition by husband and wife. If,

however, the husband and wife operate a business as a partnership, the partnership is not eligible

for Chapter 13. For eligible individuals, Chapter 13 offers many of the same benefits of Chapter

11. However, some of the disadvantages of Chapter 11 will also apply in Chapter 13 cases.

iv. Assignment for the Benefit of Creditors. Florida has a very well established

statutory scheme for assignments for the benefit of creditors. Generally, under an assignment for

the benefit of creditors, a debtor voluntarily transfers its assets to an assignee. The assignee

holds the assets in trust, liquidates the assets, provides notices to creditors of the debtor and then

distributes the proceeds in accordance with the distribution priority set forth in the statutes.

Upon assignment to the assignee, the assignee takes legal title to the debtor’s assets subject to the

liens, claims, and encumbrances upon those assets. An assignment for the benefit of creditors

provides a useful and less costly alternative to Chapter 11. However, state windup provisions

generally conflict with federal bankruptcy law and therefore the risk of an involuntarily

bankruptcy petition must always be considered by the practitioner. Additional problems exist in

a case where a corporation or business entity has contacts or assets outside of the state where the

applicable windup provision applies. Jurisdictional concerns may hamper or otherwise impede a

state court liquidation.

E. Factors that Dictate a Chapter 11 Filing.

Whether Chapter 11 is the best approach depends upon: (a) whether the Chapter 11

filing will itself damage the underlying business enterprise and (b) whether there is a viable

alternative that is quicker, less expensive, and less risky than a Chapter 11 filing. In order to

assess whether a Chapter 11 filing is appropriate, the debtor should consider the following

factors as soon as it begins thinking about a Chapter 11:

i. What is the size and composition of the creditor body? Specifically, are

there problem claims that are unlikely to be resolved outside of a Chapter 11 case?

ii. What are the adverse consequences of attempting, but failing to achieve an

out of court workout? For example, will the debtor lose assets to unstayed creditor enforcement

actions?

iii. Will a Chapter 11 filing give the debtors rights or defenses not otherwise

available, such as avoidance actions, which it needs an order to survive?

iv. Is there anything to reorganize?

If the debtor’s financial problems are historical in nature and if the debtor appears

to have the ability to operate profitably, there is every reason to believe that it can successfully

reorganize. However, a Chapter 11 cannot ultimately save a business that has no prospect of

being profitable and that has no ability to generate cash for distribution to unsecured creditors

from the sale of assets that are not subject to encumbrances. The major circumstances in which

Chapter 11 should be avoided is in the case of business that with simply no realistic hope of

survival. If “the dog won’t hunt,” a Chapter 11 case is wasteful. A Chapter 7 petition may or

may not be advisable. It may be wise to delay the filing of a Chapter 11 case in circumstances

where the debtor is expected to build up its cash reserves, where it is exploring a workout, and

where it is attempting to reduce claims through state court proceedings. Timing is critical. The

debtor will have the luxury of calculating the ideal filing time only if it recognizes the possibility

of filing early and consults with its counsel and accountants well in advance of an emergency

filing date. If the debtor waits too long to file, the prospects for a successful Chapter 11 may be

significantly reduced.

F. Special Chapter 11 Situations.

i. The Real Estate Debtor. The Chapter 11 case filed by a debtor whose only

significant asset is one parcel of real estate can generally expect its bankruptcy filing to

be subject to various contested matters. First, the secured creditor may seek to dismiss

the bankruptcy as being filed in bad faith. Second, the secured creditor could seek to

prohibit the debtor’s use of cash collateral (i.e., rents from or other income generated by

the property). Third, the secured creditor could seek relief from the automatic stay to

institute or complete its foreclosure proceeding. Finally, a secured creditor could oppose

confirmation of any plan reorganization proposed by the debtor and might ultimately be

permitted to propose its own plan.

a. Dismissal for Bad Faith. The Eleventh Circuit Court of Appeals was

very active in developing the law with respect to bad faith filings in a series of cases

during the 1980s:

i. In re Phoenix Piccadilly, Ltd., 849 F.2d 1393, 1394 (11th

Cir.1988)(“[T]here is no particular test for determining whether a debtor

has filed a petition in bad faith. Instead, the courts may consider any

factors which evidence an intent to abuse the judicial process and the

purposes of the reorganization provisions or, in particular, factors which

evidence that the petition was filed to delay or frustrate the legitimate

efforts of secured creditors to enforce their rights.”)

ii. In re Natural Land Corporation, 825 F.2d 296 (11th Cir.1987).

iii. In re Albany Partners, 749 F. 2d 670 (11th Cir. 1984).

iv. In several of these cases, the Eleventh Circuit cited with approval

the Fifth Circuit’s decision in In re Little Creek Development Co., 779 F.

2d 1068 (5th Cir. 1986). Little Creek is famous for its list of “factors,”

some of which apply automatically to any single purpose entity (“SPE”)

owning real estate. Before listing those factors, it should be emphasized

that the Fifth Circuit framed its non-exhaustive list of factors by declaring:

"Determining whether the debtor's filing for relief is in good faith depends

largely upon the bankruptcy court's on-the-spot evaluation of the debtor's

financial condition, motives, and the local financial realities. . . . [T]hey

are based on a conglomerate of factors rather than on any single datum."

Id. at 1072.

v. The Little Creek factors are:

1. The debtor has one asset, such as a tract of undeveloped or

developed real property.

2. The secured creditors’ liens encumber this tract.

3. There are generally no employees except for the principals,

little or no cash flow, and no available sources of income to

sustain a plan of reorganization or to make adequate

protection payments pursuant to 11 U.S.C. §§ 361, 362(d)(1),

363(e), or 364(d)(1).

4. Typically, there are only a few, if any, unsecured creditors

whose claims are relatively small.

5. The property has usually been posted for foreclosure because

of arrearages on the debt and the debtor has been

unsuccessful in defending actions against the foreclosure in

state court. Alternatively, the debtor and one creditor may

have proceeded to a stand-still in state court litigation, and

the debtor has lost or has been required to post a bond which

it cannot afford.

6. Bankruptcy offers the only possibility of forestalling loss of

the property.

7. There are sometimes allegations of wrongdoing by the debtor

or its principals.

8. The "new debtor syndrome," in which a one-asset entity has

been created or revitalized on the eve of foreclosure to isolate

the insolvent property and its creditors, exemplifies, although

it does not uniquely categorize, bad faith cases.

vi. The results of litigation over the “bad faith” issue varied widely.

In discussing the 11th Circuit precedent in a 1989 decision, Judge

Alexander L. Paskay noted that the Little Creek factors were “merely a

guide” and did not constitute a bright-line test, writing:

An analysis of the decisions of the Eleventh Circuit and the other bankruptcy courts in the Middle District of Florida reveals that there is nothing inherently improper in a single asset debtor filing a chapter 11 Petition for Reorganization, even shortly before or after a foreclosure proceeding has been commenced. Rather the key considerations to the courts’ decisions in this area are (1) the debtor’s intent or motive for filing the petition; (2) the extent to which the debtor is a going concern; and, (3) the ability of the debtor to reorganize.

In re Tiffany Square Associates, Ltd., 104 B.R. 438, 441 (Bankr. M.D..

Fla. 1989).

In the Bankruptcy Reform Act of 1994, Congress enacted provisions

applicable to only one class of debtors – “single asset real estate”

(“SARE”) debtors. See Section 101(51B)) of the Bankruptcy Code. See

In re Lake Ridge Associates, 169 B.R. 576 (E.D. Va. 1994).

(b) Single-Asset Real Estate Issues (“SARE”).

Pursuant to Section 101(51B), in order to be subject to the SARE

Provisions, each of the following elements must be present:

i. The debtor owns real property constituting a single property or

project;

ii. The real property must generate substantially all of the gross

income of the debtor; and

iii. The debtor must not be involved in any substantial business other

than the operation of its real property and the activities incidental thereto.

See In re View West Condominium Assoc., Inc. Case No. 08-11561-BKC-RAM (Bankr. S.D. Fla. July 29, 2008)(citing Ad Hoc Group of Timber Noteholders v. Pacific Lumber Co. (In re Scotia Pacific Co., LLC), 508 F.3d 214, 220 (5th Cir. 2007) and In re Kara Homes, Inc., 363 B.R. 399 (Bankr. D.N.J. 2007)).

iv. If the debtor is determined to be a SARE debtor, then §362(d)(3)

provides that relief from stay must be granted unless either (i) within

ninety days after the bankruptcy case is filed (or a later date if the

bankruptcy court determines cause for an extension exists) the debtor has

filed a plan of reorganization meeting the "effective reorganization" test or

(ii) the debtor has commenced monthly payments to all creditors whose

claims are secured by the property (except judgment lienholders) in

amounts equal to "interest at a current fair market rate."

v. In determining whether a debtor is a SARE debtor, the court

must determine that all three elements in the statutory definition are

satisfied. See In re View West Condominium Assoc., Inc., Case No. 08-

11561-BKC-RAM (Bankr. S.D. Fla., July 29, 2008) (citing In re Scotia

Pacific Co., LLC, 508 F.3d 214, 220 (5th Cir. 2007)).

vi. In addition to §101(51(B)), Congress also added a paragraph (3)

to section 362(d) of the Bankruptcy Code concerning the circumstances

under which relief from the automatic stay will be granted in cases of

SARE debtors. See 11 U.S.C. §§101(51B) (former), 362(d)(3) (former);

H.R. Rep. 103-835, 103 Cong. 2d Sess. (1994). According to the

legislative history, the purpose of these amendments was to “ensure that

the automatic stay provision is not abused, while giving the debtor an

opportunity to create a workable plan of reorganization.” See S. Rep. No.

168, 103d Cong., 1st Sess. (1993).

vii. Cases decided after the 1994 Act continue to hold that debtors

that have other business activities are not SARE debtors:

a. Golf course cases include:

i. In re Club Golf Partners, Case No. 07-40096-BTR-11,

2007 WL 1176010 (Bankr. E.D. Tex. April 20, 2007) (noting

that “the Debtor owns real estate but also operates a variety of

revenue-producing activities on it. It employs third-party

employees, without whom little or nothing of a revenue-

producing nature would happen on the land; and it enjoys

revenues from a variety of commercial activities on the property,

including selling memberships, charging fees or prices for access

to the public golf course; use of a golf cart; use of the driving

range; use of the tennis courts; merchandise in its pro shop; food

and beverages (beer, wine, and nonalcoholic) in the restaurant in

its clubhouse; and use of the clubhouse for special events.

Because its business activities are variegated and multiple and

are dependent on the entrepreneurial efforts and ongoing hard

work of its principals and its other employees, and because it

does not simply lease its property to tenants as the owner of true

single asset real estate such as an apartment house does, the

Debtor’s golf course does not fall within the scope of the

definition of “single asset real estate” in Code § 101(51B), and

the Debtor is therefore not subject to Code § 362(d)(3)”). 2007

WL 1176010 at 6.

ii. In re Larry Goodwin Golf, Inc., 219 B.R. 391 (Bankr.

M.D. N.C. 1997) (golf course, golf cart rentals, pool, concessions

and undeveloped property for sale constitute “substantial

business” and not holding property solely for income).

iii. In re CGE Shattuck LLC, 1999 WL 33457789 (Bankr.

D. N.H. 1999) (not single asset case where real property does not

generate substantially all of the debtor’s gross income and

percentage of revenues are derived from pro shop, golf rentals

and golf-related services).

iv. In re Prairie Hills Golf & Ski Club, 255 B.R. 228

(Bankr. D. Neb. 2000) (Debtor is not a single asset real estate

where it builds and sells residences, constructs roads to

residences, golf and ski areas, removes snow from golf and ski

area, sells liquor in the clubhouse and leases golf and ski area to

third party).

b. Hotel cases include:

i. Centofante v. CBJ Dev. Inc., (In re CBJ Dev. Inc.), 202

B.R. 467 (9th Cir. B.A.P. 1996) (hotel is not single asset real

estate because bar, gift shop and restaurant constitute significant

other business).

ii. In re Whispering Pines Estate, Inc., 341 B.R. 134

(Bankr. D. N.H. 2006) (finding in addition to bar, restaurant, gift

shop, and tour revenues, debtor’s operation of a hotel is

sufficiently active in nature to constitute a business other than

mere operation of property).

iii. In re Scotia Development, LLC, 375 B.R. 764, 774-79

(Bankr. S.D. Tex. 2007), aff’d, 508 F.3d 214 (5th Cir. 2007)

(debtor’s ownership of rights to harvest and sell timber was

sufficient to exclude debtor from SARE treatment).

iv. In re Philmont Dev. Co., 181 B.R. 220-3 (Bankr. E.D.

Pa. 1995) (ownership and management of non-debtor affiliates

was sufficient to exclude debtor/general partner from SARE

treatment); In re Kkemko, Inc., 181 B.R. 47 (Bankr. S.D. Ohio

1995).

c. Cases finding SARE status include:

i. In re Kara Homes, Inc., 363 B.R. 399 (Bankr. D.N.J.

2007), where the affiliated debtors identified themselves as

“single asset real estate” entities in submitting their initial

bankruptcy petitions and statements of financial affairs. Id. at

401. After examining the debtors’ operations, the Kara Homes

court determined that the activities of acquiring land, in addition

to planning and marketing communities, were incidental to the

debtor’s efforts to sell homes, and accordingly the affiliated

companies were single asset real estate entities. Id. at 406.

ii. In re Webb MTN, LLC, 2008 WL 656271 *4, *6

(Bankr. E.D. Tenn. March 6, 2008) (finding the debtor to be a

SARE debtor where “no development has actually commenced

upon the Webb Mountain Property, therefore it is not producing

any income and is passive in nature”).

d. Hot SARE Issues:

• If multiple SPEs, each owning a single project, that have a common

parent file chapter 11 petitions, is each a SARE debtor? What if there

is:

o Common management and control;

o Vertically integrated operations;

o Tax returns filed on a consolidated basis;

o Unified marketing;

o Single auditor and tax advisor; and

o Cross-guarantors among various Debtors?

• Is there an “intent” element in the SARE determination? Does it matter whether the case is viewed as an abusive chapter 11 petition filed primarily to frustrate the exercise of foreclosure remedies where there is no reasonable probability of a feasible plan? See In re 83-84 116th Owners Corp., 214 B.R. 530, 535 (Bankr. E.D. N.Y. 1997)?

• What about In re General Growth Properties, 409 B.R. 43 (Bankr.

S.D. N.Y. 2009)? The debtors included the parent company and several hundred special purpose entities that owned shopping centers in 44 states across the country. Is each entity a SARE debtor? Did Congress intend that multi-billion dollar enterprises such as that in the General Growth Properties be subject to the expedited time table set forth by the SARE Provisions?

In General Growth, certain of the lenders filed motions to dismiss the

bankruptcy cases as bad faith filings, citing to the traditional indicia of bad faith,

including whether the debtor has only one asset. Id. at 56. The movants argued that the

“single purpose entity” or bankruptcy remote structure of the project level debtors

required that each debtor’s financial distress be analyzed exclusively from its perspective

and that the court should only consider the financial circumstances of the individual

debtors. However, the bankruptcy court disagreed, instructing that a court is not required

to examine the issue of good faith as if each debtor were wholly independent. Id.

Considering the group as a whole, the court found that there was neither objective bad

faith nor subjective bad faith with respect to the filings. Interestingly, it does not appear

from a review of the docket of the General Growth Properties cases that a SARE finding

was ever made by the court.

Kara Homes, supra, involved multiple debtors, each responsible for

acquiring developable land, arranging for construction of units, and then marketing and

selling the units; each was determined to be a SARE debtor. “Marketing, sales and

construction [were] handled from a construction trailer and model located on each

property.” Id. at 403. The common area, amenities and roadways were still in

construction and development stages. Id. In Philmont Dev., the SARE determination

was made as to the limited partnership debtors whose only assets were the semi-detached

houses each individually purchased from the general partner. 181 B.R. at 221. The court

found that the semi-detached homes owned by the limited partnership debtors were

comparable to the type of real property at issue in a typical single asset real estate case.

Unreported decisions that have come to the attention of the author go both

ways. Judge Kathleen Thompson recently addressed this very issue in a similar case and

held that even if one or more debtors, when considered in isolation, would fall within the

ambit of §101(51B), the consolidated, inter-related business operations of the collective

group of debtors were sufficient to avoid a SARE designation, because to rule that the

SARE Provisions applied would inappropriately elevate form over substance. See,

Meruelo Maddux Properties, Inc., et. al., Case No. SV 09-13356-KT (Bankr. Central

District of Cal. June 17, 2009). A copy of Memorandum Decision is available from the

author.

Judge Rodney May adopted Judge Thompson’s analysis and found that the

debtors in In re Fiddler’s Creek, Case No. 8:10-bk-3846-KRM) (Bankr. M.D. Fla.,

February 23, 2010), some of which owned only raw land, should not be subject to the

SARE Provisions because they were part of a larger enterprise and there was no

indication of the abuse which was the premise for the addition of Section 362(d)(3) of the

Bankruptcy Code. Judge May based his decision, in part, upon the purpose of the SARE

provisions to curtail abusive filings by debtors whose cases involved an absence of

economic activity, lack of significant employees, or no going concern value.

Judge Catherine Peek McEwen ruled the other way in the case of In re

Odyssey Properties III, LLC, et al., Lead Case No. 8:10-bk-18713-CPM (Bankr.

M.D.Fla., August 2, 2010).

(c) Not All is Lost for SAREs – Weapons in SARE Cases and Other Cases

i. Loan documents in Chapter 11 – lenders may find themselves with

non-standardized loan documents.

a. "The covenants to be included in the loan documents of a

cramdown need not precisely track the covenants in the parties'

existing loan agreement." In re P.J. Keating Co., 168 B.R. 464, 473

(Bankr. D. Mass.1994) quoting In re Western Real Estate Fund, Inc.,

75 B.R. 580 (Bankr. W.D. Okla.1987).

b. In re Stratford Assoc. Ltd. P'ship., 145 B.R. 689, 703 (Bankr.

D. Kan.1992) (finding that if a debtor could not modify loan

documentation it would make the whole reorganization process

unworkable).

c. In re American Trailer and Storage, Inc., 419 B.R. 412,

442 (Bankr. W.D.Mo. 2009) (the court refused to insert covenants and

confirmed a plan over an objection by a secured creditor, stating that

“[t]he Court finds that slavish adherence to the financial ratio

covenants included in the parties original loan documents or inclusion

of a sales restriction covenant, would unnecessarily impair Debtor's

ability to reorganize and potentially be a drain on this Court's

resource”); In re TCI 2 Holdings, LLC, 428 B.R. 117,

167 (Bankr.D.N.J. 2010) (“the loan documents need not track

precisely the covenants in the parties' existing loan agreement. …

[n]or must the post-confirmation loan documents be consistent with

what the market would require for a new loan”).

ii. Loan Maturity in Chapter 11.

a. There is no provision in Chapter 11 that establishes a

maximum time during which payments to creditors may extend, unlike

Chapter 13. See § 1322(b)(5),(c)(2),(d)(2). Rather, Chapter 11

explicitly permits the extension of maturity dates. § 1123(b)(5)(H).

b. Cases likewise indicate no hard and fast rule regarding

maturities:

i. Koopmans v. Farm Credit Services of Mid-America,

ACA, 102 F.3rd 874 (7th Cir. 1996)(two year extension of

maturity, putting new maturity date nine years out).

iii. Interest Rate Reduction.

a. In order for a plan to be "fair and equitable" with respect to a

class of claims, the plan must provide that a secured creditor must

“receive or retain on account of such claim property of a value, as of

the effective date of the plan, equal to the allowed amount of such

claim.” The statutory provisions related to interest rates in Chapter 11

and Chapter 13 cases contain identical language. Compare

1129(b)(ii)(B), 1225(a)(5)(B), and 1325(a)(5)(B).

b. Prior to Till v. SCS Credit Corp., 541 U.S. 465, 124 S.Ct.

1951, 158 L.Ed.2d 787 (2004), courts had used a number of different

methodologies to determine the proper interest rate in bankruptcy

cases: the formula, coerced loan, presumptive contract rate and cost of

funds approaches. In Till, a Chapter 13 case, the Supreme Court (by

plurality decision) settled on the formula approach in Chapter 13 cases

while stating that “[w]e think it likely that Congress intended

bankruptcy judges and trustees to follow essentially the same approach

when choosing an appropriate interest rate under any of these

provisions. Moreover, we think Congress would favor an approach

that is familiar in the financial community and that minimizes the need

for expensive evidentiary proceedings.” Till v. SCS Credit Corp., 541

U.S. 465, 474-475, 124 S.Ct. 1951, 1959 (U.S. 2004). In footnote 14,

the Court also noted that there is "no free market of willing cramdown

lenders" in Chapter 13, unlike in Chapter 11, and concludes that "when

picking a cramdown rate in a Chapter 11 case, it might make sense to

ask what rate an efficient market would produce." Id. at 477 n. 14, 124

S.Ct. 1951. An “efficient market” is defined as a “[m]arket where all

pertinent information is available to all participants at the same time,

and where prices respond immediately to available information. Stock

markets are considered the best examples of efficient markets.”

http://www.businessdictionary.com/definition/efficient-market.html

Before applying Till in the Chapter 11 context, some decisions have

sought to undertake a “nuanced” determination as to whether or not an