self-storage investment trends to watch marcus & millichap research services, national...

TRANSCRIPT

Self-Storage Investment Trends to Watch

April 16, 2015

Economic Outlook UnderpinsSelf-Storage Sector

Hiring Makes Steady Gains –Supports Broader Economic Performance

-2.7

-1.8

-0.9

0.0

0.9

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

*

Qua

rter

ly J

ob G

row

th (M

illio

ns)

* Forecast** Through MarchSources: Marcus & Millichap Research Services, BLS

+8.2 Million +11.5 Million**

-8.7 Million

2015 Forecast: 3.1 Million - 3.5 Million

U.S. Employment Gains Broad-BasedY-O-Y Sector Change Through March 2015

Sources: Marcus & Millichap Research Services, BLS

U.S. Employment Sectors Absolute Change % Change

Prof. & Business Services 662,000 3.5%Trade, Transport & Utilities 607,000 2.3%Education and Health Services 541,000 2.5%Leisure & Hospitality 490,000 3.4%Construction 282,000 4.7%Manufacturing 188,000 1.5%Financial Activities 150,000 1.9%Other Services 73,000 1.3%Government 72,000 0.3%Information 59,000 2.2%Natural Resources & Mining 4,000 0.5%

Net Change 3,128,000 2.3%

Sources: Marcus & Millichap Research Services, BLS

National Employment Rank by MetroY-O-Y Absolute Change Through February 2015

Top 10Metros

Absolute Change

PercentChange

Dallas-Ft. Worth 132,200 4.1%

Atlanta 113,200 4.6%

New York 106,500 2.6%

Houston 97,700 3.4%

Los Angeles 94,500 2.3%

Chicago 67,400 1.5%

Phoenix 62,700 3.4%

Seattle 58,400 3.2%

Inland Empire 57,600 4.6%

Denver 55,600 4.2%

U.S. Total 3,227,000 2.3%

Bottom 10Metros

Absolute Change

PercentChange

Milwaukee 8,900 1.1%

Cleveland 10,800 1.0%

St. Louis 13,900 1.1%

Jacksonville 14,000 2.3%

Cincinnati 18,900 1.8%

Palm Beach 21,400 3.9%

Oakland 25,500 2.4%

Columbus 25,900 2.6%

Las Vegas 26,800 3.1%

Austin 27,500 3.0%

U.S. Total 3,227,000 2.3%

Sources: Marcus & Millichap Research Services, BLS

0

40

80

120

160

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

*

80

90

100

110

120

Consumer Confidence Small Business Optimism

* Consumer confidence through March; small business optimism through FebruaryIndex: December 2002 = 100Sources: Marcus & Millichap Research Services, The Conference Board, NFIB

Con

sum

er C

onfid

ence

Inde

x Confidence Rising –

Will Support Economic Momentum

Small B

usiness Optim

ism Index

Year

-Ove

r-Ye

ar C

hang

e

$190

$230

$270

$310

$350

01 03 05 07 09 11 13 15*

Ret

ail S

ales

($ B

il.)

+19%

* Through MarchCore retail sales excludes auto and gasoline salesSources: Marcus & Millichap Research Services, U.S. Census Bureau

$869/person

$980/person

Rec

essi

on

20-YearAverage: 4.2%

U.S. Core Retail Sales Building Steady Momentum - Growth Lifting Economy

-8%

-4%

0%

4%

8%

07 08 09 10 11 12 13 14 15*

Economic Outlook UnderpinsSelf-Storage Sector

Emerging Housing and MigrationPatterns Influence Self-Storage

0.0

0.5

1.0

1.5

2.0

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

201420

15*

Single-Family Construction Multifamily Construction Household Growth

* ForecastSources: Marcus & Millichap Research Services, U.S. Census Bureau

Hom

e C

ompl

etio

ns (M

il.)

and

Hou

seho

ld G

row

th (M

il.)

Plunge in Home Construction Supports Housing Recovery

1999-2007 Oversupply: 3.5M 2008-2015* Undersupply: 2.8M

250

350

450

550

650

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

*

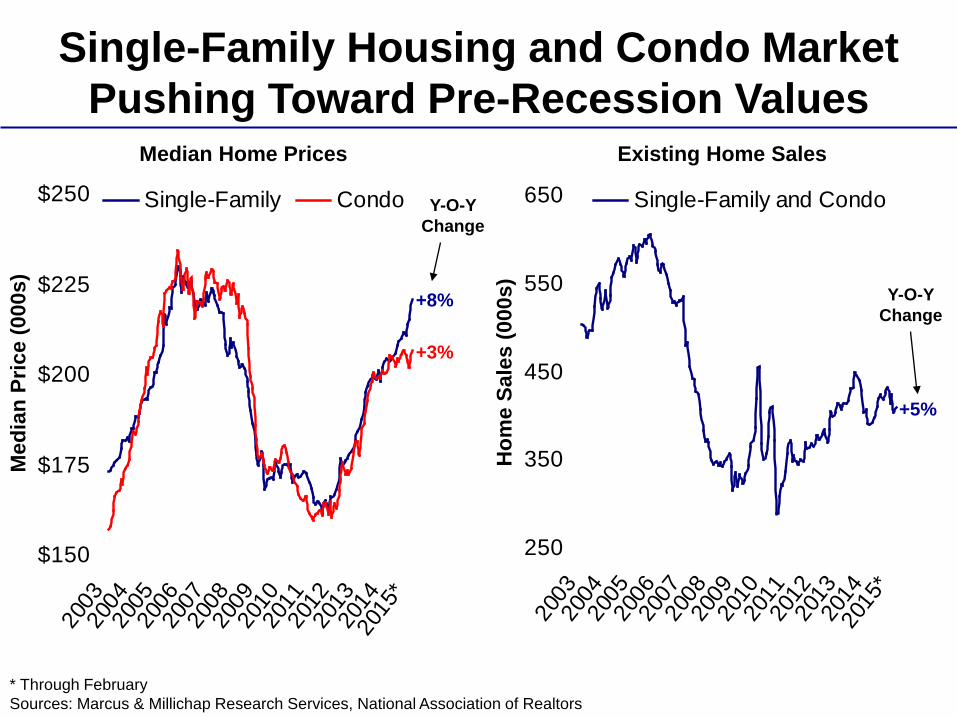

Single-Family and Condo

$150

$175

$200

$225

$250

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

*

Single-Family Condo

* Through FebruarySources: Marcus & Millichap Research Services, National Association of Realtors

+8%

+3%

Med

ian

Pric

e (0

00s)

+5%

Hom

e Sa

les

(000

s)

Median Home Prices Existing Home Sales

Y-O-Y Change

Y-O-Y Change

Single-Family Housing and Condo Market Pushing Toward Pre-Recession Values

Bottom 5DeparturesDestinationsTop 5

Sources: Marcus & Millichap Research Services, United Van Lines Migration Study

2014 Residential Migration Trends

National Metro RankingAbsolute Population Growth 10-Year Forecast*

Top 10 Markets

Population Growth

Percent Change

Dallas-Ft. Worth 1,467,000 20.9%

Phoenix 1,163,000 25.6%

Houston 1,111,700 17.0%

Atlanta 1,046,900 18.6%

Los Angeles 842,200 8.3%

Orlando 691,200 29.3%

Washington, D.C. 643,900 10.7%

Inland Empire 591,600 13.2%

Las Vegas 555,800 26.5%

Austin 509,800 25.9%

U.S. Total 27,700,000 8.6%

Bottom 10 Markets

Population Growth

Percent Change

Cleveland -57,000 -2.8%

Detroit -40,200 -0.9%

Milwaukee 33,300 2.1%

Cincinnati 133,500 6.1%

Columbus 161,700 8.4%

Philadelphia 169,200 2.8%

Kansas City 179,100 8.5%

San Francisco 185,400 9.9%

Indianapolis 202,000 10.8%

San Jose 212,100 10.8%

U.S. Total 27,700,000 8.6%

* 1Q 2015-1Q 2025Sources: Marcus & Millichap Research Services, U.S. Census Bureau

Emerging Housing and MigrationPatterns Influence Self-Storage

Capital Markets

0%

1%

2%

3%

4%

2010

2011

2012

2013

2014

2015

*

Core Inflation 10-Year Treasury10-Year Avg. Core Inflation 10-Year Avg. 10-Year Treasury

Rat

e

* Core inflation through February 2015; 10-year Treasury through April 6, 2015Sources: Marcus & Millichap Research Services, Federal Reserve, BLS

Inflation Generating Little Pressure10-Year Treasury Range-Bound

3.39%

1.91%

Core Inflation: 1.91%

10-Year Treasury: 3.39%

10-Year Average

* As of April 8, 2015Sources: Marcus & Millichap Research Services, Trading Economics

10-Year Treasury Rates by Country

Country 10-Year Treasury Rate*Germany 0.2%Japan 0.4%France 0.5%Canada 1.4%United Kingdom 1.6%United States 1.9%Australia 2.4%China 3.7%Russia 11.7%Brazil 12.8%

Includes sales of properties $2.5 million and greaterSources: Marcus & Millichap Research Services, Real Capital Analytics

1% 1%5% 7% 9%

15% 13% 12% 11%

16% 22% 23%27%

11%9% 11%

13%

15%8%

8% 7%8%

7%12%

13% 13%

18%14%

31% 27% 28%18% 16%

1%2%1%

5% 5%

20%

17%

0%

25%

50%

75%

100%

2010 2011 2012 2013 2014

Gov't Agency

National Bank

International Bank

Regional/Local Bank

CMBS

Insurance

Financial

Private/Other

Perc

ent o

f Tot

al D

olla

r Vol

ume

Commercial Real Estate Lender Composition by Percent of Total Dollar Volume

Capital Markets

Self-Storage Performance

0%

5%

10%

15%

20%

Self-Storage Apartment Retail Office Industrial

2006-2012 2013 2014 2015*

U.S. Commercial Property Vacancy Trends

Aver

age

Vaca

ncy

Rat

e

* ForecastSource: Marcus & Millichap Research Services, MPF Research, CoStar Group, Inc., Reis Services, LLC

17.9%

11.5%

8.0%

4.8%

8.1%6.0%

17.1%

14.5%

10.5%

6.5%

$1.0

$1.2

$1.4

$1.6

$1.8

2011 2012 2013 2014 2015*4%

8%

12%

16%

20%Asking Rent - Climate ControlledAsking Rent - Not Climate ControlledVacancy

National Self-Storage Vacancy and Rent Trends

* ForecastRent for 10X10 unitSources: Marcus & Millichap Research Services, Reis Services, LLC

Average Vacancy Rate

Aski

ng R

ent p

er S

quar

e Fo

ot

National Self-Storage Rank by Metro2014 Vacancy Rate

Top 10Markets

2014Vacancy

Y-O-YBps Chg.

San Francisco 7.3% -140

San Jose 7.3% -40

Oakland 8.9% -290

Denver 9.8% -50

San Diego 9.8% -310

Los Angeles 10.0% -240

Portland 10.2% -260

Miami 10.3% -30

Dallas-Ft. Worth 10.5% -150

Kansas City 10.6% -330

U.S. Average 12.0% -150

Bottom 10Markets

2014Vacancy

Y-O-YBps Chg.

Phoenix 17.1% -100

Las Vegas 16.4% -170

Inland Empire 15.6% -320

Columbus 13.8% 20

Orlando 13.6% -320

Minneapolis 13.1% -10

Atlanta 12.9% -270

Sacramento 12.9% -350

Detroit 12.8% -240

Tampa 12.8% -220

U.S. Average 12.0% -150

Sources: Marcus & Millichap Research Services, Reis Services, LLC

Self-Storage Performance

Self-Storage Investment

CRE Investor Sentiment Index Has Been a Strong Indicator of CRE Capital Flows

Includes all apartment, office, retail, and industrial sales $1 million and greaterSources: Marcus & Millichap Research Services, CoStar Group, Inc., Real Capital Analytics, M&M/NREI Investor Survey

$0

$150

$300

$450

$600

04 05 06 07 08 09 10 11 12 13 1440

80

120

160

200

CRE Sales Volume CRE Investor Sentiment

Tota

l Sal

es V

olum

e (B

il.)

Investor Sentiment Index

Self-Storage Price and Cap Rate Trends

* Preliminary estimate through 1QIncludes sales $1 million and greaterSources: Marcus & Millichap Research Services, CoStar Group, Inc.

$40

$50

$60

$70

$80

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15*6%

7%

8%

9%

10%

Average Price Average Cap Rate

Average C

ap Rate

Ave

rage

Pric

e Sq

uare

Foo

t

Self-Storage Cap Rate Trends by Class and Market Type*

Sources: Marcus & Millichap Research Services, BLS

Primary Secondary Tertiary Average

Class A 4.5% - 5.5% 5.5% - 6.25% 6.5% - 7.5% 6.1%

Class B 5.5% - 7.0% 6.5% - 7.5% 7.5% - 8.5% 6.8%

Class C 6.5% - 8.0% 7.0% - 9.0% 8.0% - 10.0% 7.8%

Average 6.0% 6.9% 7.8% 6.6%

* Trailing 12-month through 1Q 2015Sources: Marcus & Millichap Research Services, CoStar Group, Inc.

0.0%

2.5%

5.0%

7.5%

10.0%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

*

Self-Storage Cap Rate 10-Year Treasury Rate

Self-Storage Cap Rate vs. 10-Year Treasury

* Through March 6Includes sales $1 million and greaterSources: Marcus & Millichap Research Services, CoStar Group, Inc., Federal Reserve

Aver

age

Rat

e

10-Yr. Treasury Long-Term Average

Cap Rate Long-Term Average

270 bps

580 bps 470 bps

520 bps

0%

3%

6%

9%

12%

Self-Storage Apartment Retail Office Industrial

2000-2012 2013 2014

U.S. Commercial Property Cap Rate Trends

Aver

age

Cap

Rat

e

Source: Marcus & Millichap Research Services, CoStar Group, Inc., Real Capital Analytics

-30 bps +10 bps -10 bps +30 bps +30 bpsChange From Prior Cyclical Low

Self-Storage Investment

Self-Storage Investment Trends to Watch

April 16, 2015