self-insurance plus healthcare funding model

TRANSCRIPT

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 1

Introduction If you could hear me speak this proposal, it is my hope that you would perceive me as, in the

words of Quintilian, “a good man speaking well”. I only want the best for my country.

I don’t have all the answers. I only know that the National Debt is growing at an alarming rate.

Medicare and Medicaid are expensive components of the Federal budget and preventable health

problems, such as problems stemming from obesity, are significant contributors to the high cost

of Medicare, Medicaid and private insurance plans.

How expensive would auto insurance be if tens of millions of Americans drove recklessly and

caused tens of millions more accidents, injuries, and lawsuits every year? How expensive would

homeowner’s insurance be if tens of millions of Americans were careless and let their homes

burn down every year? How much more would it cost to stay in business if business owners

neglected workplace safety and allowed their workmen’s compensation premiums to skyrocket?

Did you know that your homeowner’s insurance generally protects you from losses that are

sudden and accidental but not from losses that are gradual? So if a tornado happens to pass over

your house, you are covered; but if termites slowly but surely damage your home, you are not

covered because you had ample opportunity to take preventive measures.

Health insurance on the other hand is more complicated because it applies to human beings

rather than to cars, properties, and businesses. How much more expensive is it because tens of

millions of Americans neglect their health and gradually develop problems such as diabetes,

heart disease, cancer, a long list of other preventable ailments, and the malpractice lawsuits that

sometimes accompany them? Preventable ailments are to the human body as termites are to a

home.

Imagine how much more affordable health insurance would be if it were like homeowner’s

insurance and it protected you from unpredictable and unpreventable events but it did not protect

you from problems you could have prevented?

One reason that health insurers have not developed plans that exclude preventable ailments is

because it is difficult to prove in court what is preventable and what isn’t. We know obesity leads

to heart disease but can a doctor prove in court that obesity was definitely the cause of

someone’s heart attack? Even if it were possible to prove it, the patient still had to be treated and

the bills still had to be paid by someone, somehow; directly or indirectly. Whether a particular

insurance contract paid for it or not is a moot point; the event happened and healthcare providers

had to be paid for their services.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 2

Somehow, we Americans need to be convinced that the Golden Rule applies to our health; I’ll

practice good health habits if you practice good health habits and together we will reduce our

health insurance premiums and have more money to spend on better things.

The Self-Insurance Plus model is an alternative way to pay for healthcare that has the potential to

motivate people to practice wellness and comparison shop for healthcare services; thus reducing

the frequency and severity of preventable health problems.

My only motivation for writing this proposal is to do my altruistic duty as an American citizen

and try to help my Government solve a critical problem in a way that is hopefully acceptable to

conservatives, liberals, and everyone in between. Lee Iacocca was right when he said “Where the

hell is our outrage? (Iacocca, 2007)” I’m not sure if the cost of healthcare will ever be affordable

if many people have poor health habits that increase the frequency and severity of health

problems; so something has to be done to motivate people to stay in shape.

The Federal Government routinely alters the tax code in order to create incentives for people to

behave one way or another; such as the mortgage interest deduction, credits for hybrid cars,

credits for renewable energy, etc. We need incentives to practice wellness too.

An enabling feature of the Self-Insurance Plus model is that it is uniquely American and

consistent with the rugged-individual American heritage. We the People have the option of

giving it a try before the unsustainable cost of healthcare pushes the U.S. to adopt a controlled

single-payer system as other developed nations have done.

This is a draft proposal that rewards people for staying healthy and avoiding preventable health

problems during their lifetimes. It isn’t perfect but neither are any of the other alternative

models.

About the author I have worked for an insurance company since 1984, am an information technologist, have

completed several Chartered Property Casualty Underwriter insurance courses, and have learned

much about the insurance business over the years. I have a healthcare savings account (HSA),

am familiar with how it works and how it motivates me to think about my health.

I have absolutely no conflict of interest or ulterior motives driving me to write this proposal. It

consists entirely of my own ideas. Neither my employer nor any other party has anything to do

with it.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 3

Abstract SELF-INSURANCE: “insurance of oneself or of one's own interests by the setting aside of

money at regular intervals to provide a fund to cover possible losses (Merriam Webster).”

There is no magic bullet way to pay for healthcare because it is expensive and millions of

persons cannot afford it on their own if something catastrophic happens to them. This proposal is

an attempt to make a difference. Households will be required to save money for healthcare rather

than pay insurance premiums. They will see healthcare financing from a holistic lifetime

investment point of view instead of seeing it as just another bill to pay.

Some experts are projecting that interest on the National Debt will exceed revenues between

2030 and 2040. That means the Federal Government will cease to function unless it changes the

way it does business pretty soon. That foreboding fiscal forecast is what stirred me to write this

proposal. I am also disappointed with the forces in American culture that are causing destructive

health habits in many individuals while expecting everyone to pay for the consequences of those

habits. I have not yet thought of a way to compel persons to practice wellness that will withstand

legal challenges; therefore, a friendlier alternative is to give them a significant financial motive

to do so.

If this proposal were enacted into law, it would take years, or even a generation or two, before

the majority of Americans changed their habits and viewed wellness as an investment; but once

they did, the benefits would be significant. The sooner we get started, the better. If combined

with nutrition and lifestyle education programs, the benefits would be enormous.

The Patient Protection and Affordable Care Act does many good things and it gets most

Americans into the insurance pool but it does not change the way healthcare is financed the way

this proposal does. It does not give everyone a financial incentive to practice wellness.

If you make the arguments that everyone needs healthcare, everyone should receive the

healthcare they need, and everyone should pay for it; then you can make the claims that everyone

is in the pool together and any healthcare financing model you use simply moves money among

parties but does not change the end result which is that patients get treated by providers. So why

not choose the model that motivates wellness and drives down the cost for everyone without

nationalizing healthcare?

Policymakers are assuming the USA will educate, innovate, and build its way back to fiscal

stability (Goolsbey, 2011). Informed pundits say the only way to eliminate deficits and reduce

debt will be to enact a general purpose value added tax (VAT) unless policymakers can find a

better way to pay for entitlements such as Medicare, Medicaid, and Social Security. This

proposal could solve the Medicare and Medicaid problem if it is enacted correctly. It can be

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 4

a step on the path toward fiscal responsibility. Maybe the USA can have a small VAT that is

only used to pay for supplemental healthcare rather than a large VAT that will be used to pay for

everything?

This proposal describes a healthcare financing model that integrates the components listed below

in a way not previously proposed by anyone else to the best of my knowledge:

1. Managed healthcare savings accounts (MHSAs)

2. A national healthcare reserve (NHR) partially funded by a healthcare-only value added

tax (HVAT) and optionally with other taxes depending on political choices.

3. Savings contributed by each person

4. Private-sector healthcare insurance

5. Cost containment programs

This proposal does the following:

1. Permits everyone living in the USA to receive good quality healthcare provided that each

individual or family contributes into the system as much as it can reasonably be expected to

pay up to an annual maximum.

We won’t hear too many more tragic stories of persons who need healthcare but

cannot afford it.

2. Does not require private sector employers or public sector employers to purchase health

insurance for their employees or retirees except under specific circumstances.

No more businessmen complaining with outrage about their rising premiums.

No more governors blaming state deficits on Medicaid and employee/retiree

health insurance.

No more worrying that Medicare and Medicaid will swell the National Debt.

Makes it easier for businesses to hire more workers.

3. Gives everyone a financial incentive to practice wellness and stay healthy.

4. Will probably decrease the percentage of GDP spent on healthcare, or it will reduce

healthcare cost inflation, because it is a more efficient system and it gives everyone an

incentive to stay healthy.

5. Probably will reduce waste, fraud, and abuse significantly.

6. Probably will reduce government bureaucracy by having fewer employees involved with

healthcare-related social programs.

7. Shifts the focus to individual responsibility.

Let’s debate this in the national discourse I see little value in complaining about runaway Government debt while not offering alternatives

and so I voluntarily gave a substantial amount of my time to write one.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 5

I can continue to cite many more examples and spend many more hours expounding on the

merits of this model and the details to make it work; but that is a job that government

policymakers and NGOs get paid to do; rather than me doing it in my spare time. I hope I have

supported my position enough to motivate professional analysts in the Government to estimate

the reduction of GDP the U.S. would spend on healthcare if everyone were enrolled in the Self-

Insurance Plus system. Additionally, analysts should evaluate how much more value the U.S.

would receive for the money it spends on healthcare if millions of low-income persons receive

better care than they receive now from Medicaid and other programs. It is a big win for our

nation even if the cost remains about the same but the value jumps significantly.

If professional analysts study the spreadsheets I have provided and the assumptions I have made,

they will see that this model is feasible. In a nutshell: Everyone saves money for their healthcare

throughout their lives. Everyone pays for their healthcare throughout their lives. If they saved

more than they paid during their lives, their heirs will inherit the surplus or some portion of it. If

they spent more than they saved during their lives, they will have been subsidized by an

equitable tax. It really is that simple. It is simple and effective.

This is a draft of a concept. It is a starting point; food for thought and debate. Let the People

debate it and see where it leads

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 6

Contents Introduction ..................................................................................................................................... 1

About the author ............................................................................................................................. 2

Abstract ........................................................................................................................................... 3

Let’s debate this in the national discourse ...................................................................................... 4

Figure 1 - Conceptual Flow Diagram of this healthcare financing model ............................... 10

Points Made by Figure 1 ........................................................................................................... 12

Figure 2 - Illustrations That Show How this Proposal Creates the Incentive to Practice Wellness

....................................................................................................................................................... 13

Scenario 1 in the above chart .................................................................................................... 14

Scenario 2 in the above chart .................................................................................................... 14

General Concept of How the Money Will Flow ....................................................................... 14

Benefits ......................................................................................................................................... 15

Fairness...................................................................................................................................... 15

Benefits to Businesses and by Extension to the Economy ........................................................ 15

Benefits to the People ................................................................................................................ 16

Benefits to Government and by Extension to the People .......................................................... 16

General Parameters I Have Thought of So Far ............................................................................. 16

Requirements ............................................................................................................................. 16

Exceptions and Limitations ....................................................................................................... 18

Hypothetical illustrations of this proposed system in action..................................................... 19

What the examples illustrate ..................................................................................................... 20

My Replies to the Negative Rhetoric I Anticipate ........................................................................ 20

Fraud Prevention ........................................................................................................................... 21

The Underground Economy .......................................................................................................... 21

Impact on lower-income persons .................................................................................................. 22

How many basis points will the HVAT be when it is first enacted? ............................................ 22

Other Ways and Means to Add Funds to the NHR ....................................................................... 23

Smoothes the Trend Line of Healthcare Cost Inflation ................................................................ 23

Opt out or opt in ............................................................................................................................ 24

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 7

Why not let the Federal Government (Medicare) Be the TPA? ................................................... 24

Phase In ......................................................................................................................................... 24

Aphorisms for This Model ............................................................................................................ 24

Philosophic Justification of MHSAs and HVAT .......................................................................... 25

Personal responsibility .............................................................................................................. 25

We all bear responsibility for our own health and the health of others directly and indirectly 25

Business expenses are indirect flat taxes................................................................................... 25

Governments pay for healthcare with taxes .............................................................................. 25

Payroll taxes already pay for Medicare ..................................................................................... 25

Health Insurance Companies Cannot Tell People How to Behave ........................................... 26

Perks and Paternalism ............................................................................................................... 26

Supporting Materials ..................................................................................................................... 26

Medicare is Unsustainable ........................................................................................................ 26

Opinions of others who support a VAT to pay some of the cost of healthcare. ....................... 26

Dr. Victor Fuchs .................................................................................................................... 26

Money That Rightfully Belongs in MHSAs to Pay Real Medical Bills, Not in the Excessive

Profits of Private Health Insurers .............................................................................................. 27

Evidence That the Affordable Care Act is Reducing Premiums for Younger Persons and

Employers.................................................................................................................................. 27

Conclusion .................................................................................................................................... 27

Examples ....................................................................................................................................... 29

Example 1 – Trivializing arterial plaque ................................................................................... 29

Example 2 –Health insurance fraud is expensive ...................................................................... 30

Medicare Fraud ...................................................................................................................... 30

Private Insurance Fraud ......................................................................................................... 30

Example 3 –Personal choice ..................................................................................................... 31

Example 4—Self-Insurance Plus simplifies disaster relief ....................................................... 32

Example 5—Self-Insurance Plus simplifies relief after a hypothetical terror attack on a large

city. ............................................................................................................................................ 33

Example 6—Self-Insurance Plus gives more control to the people .......................................... 34

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 8

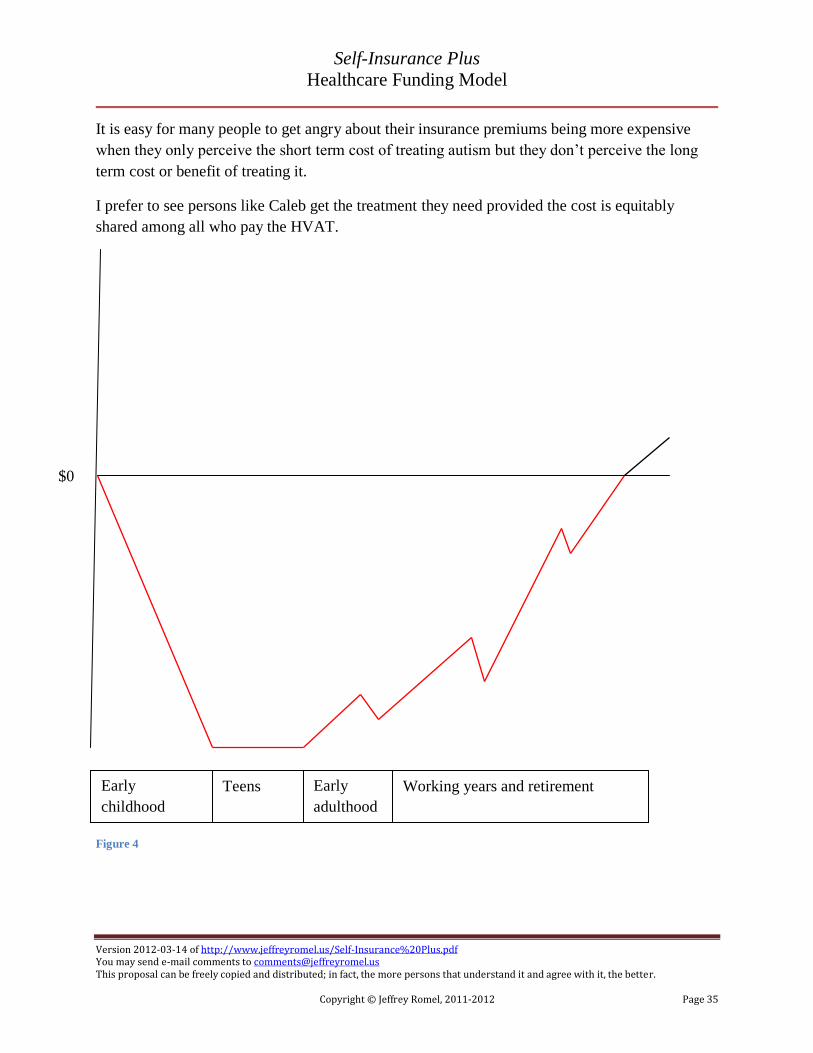

Example 7—Near-end-of-life decisions.................................................................................... 36

Example 8—Comparison shopping versus free healthcare....................................................... 36

Example 9—Motivating people to be concerned with wellness ............................................... 37

Example 10—Diverted funds .................................................................................................... 38

Example 11—Self-Insurance Plus would relieve state and municipal governments from

soaring healthcare costs ............................................................................................................. 38

Example 12—Take the politics out of health insurance ........................................................... 38

Example 13—Transparency ...................................................................................................... 38

Example 14—What will the financial planners say? ................................................................ 38

Comparison to a hypothetical insurance product .......................................................................... 39

Other observations ........................................................................................................................ 39

Glossary ........................................................................................................................................ 41

Bibliography ................................................................................................................................. 42

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 9

+ = + B

A modest and

equitable

healthcare-only

value added tax

and perhaps

other taxes such

as vice taxes,

junk food taxes,

and processed

food taxes.

A

Amount of

money each

person or

household can

reasonably be

expected to pay

for healthcare

plus the

investment

income they

earn in their

managed

healthcare

savings

accounts.

C

All other forms

of insurance that

pay for

healthcare; e.g.,

workmen’s

compensation,

liability

coverage,

veterans’

benefits, and

private

healthcare

policies for

exposures not

covered by A

and B.

+

Charitable

contributions

D

All the money

our society is

able to pay for

healthcare.

Any way you

slice it and dice

it, that’s all the

money there is

for healthcare

and there is no

more.

If more money

is needed,

policymakers

will probably

have to increase

B and possibly

A and/or find

ways to contain

healthcare costs.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 10

Figure 1 - Conceptual Flow Diagram of this healthcare financing model

Income

Everyone is required to contribute about

5% of his pre-tax income to his MHSA.

Purchases

Most products will be subject to an HVAT of 1% -

2% (experts will decide the percentage). Essential

items such as food staples, clothing, etc. will be

exempt; similarly to how those items are exempt

from sales tax today. Excess HVAT paid can be a

deduction on tax returns.

Healthcare Value Added Tax (HVAT)

A value added tax (VAT) that is strictly used to pay

for healthcare when MHSAs and other insurance

coverage are insufficient.

MHSA Contributions

Withheld from paychecks and other

income sources up to an annual maximum.

Other Taxes

Policymakers might choose to contribute funds from

vice taxes, junk food taxes, and so on.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 11

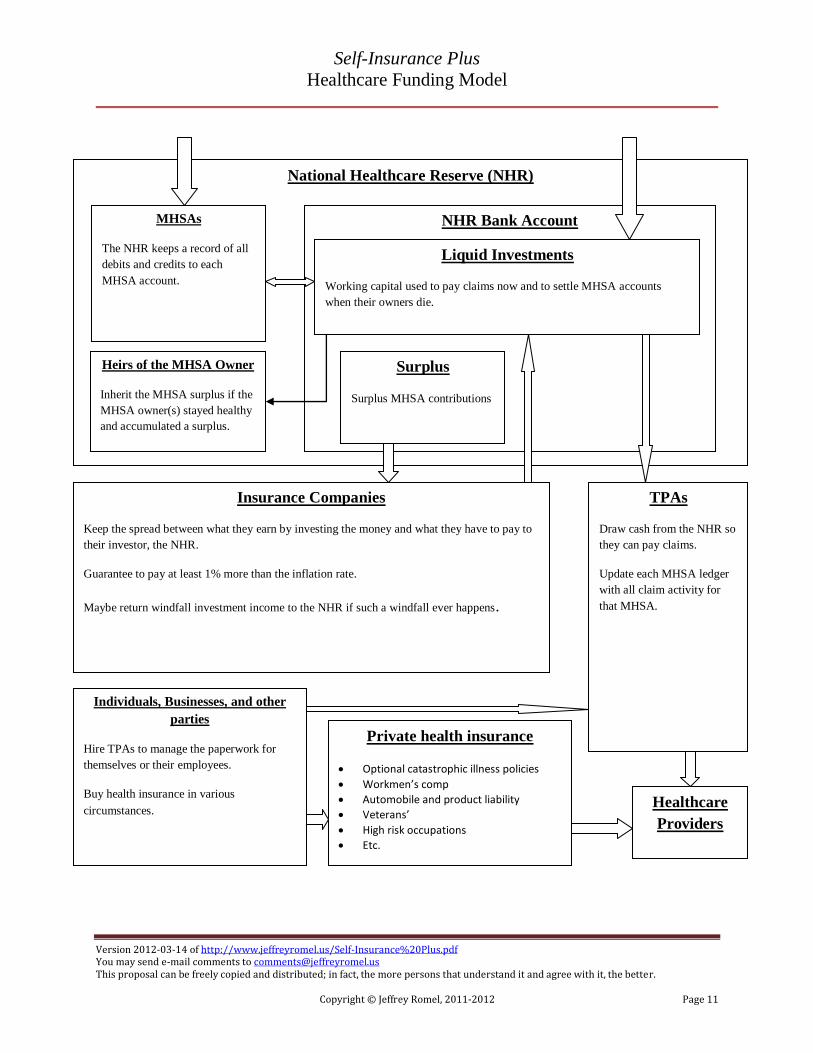

National Healthcare Reserve (NHR)

MHSAs

The NHR keeps a record of all

debits and credits to each

MHSA account.

NHR Bank Account

TPAs

Draw cash from the NHR so

they can pay claims.

Update each MHSA ledger

with all claim activity for

that MHSA.

Private health insurance

Optional catastrophic illness policies

Workmen’s comp

Automobile and product liability

Veterans’

High risk occupations

Etc.

Healthcare

Providers

Liquid Investments

Working capital used to pay claims now and to settle MHSA accounts

when their owners die.

Surplus

Surplus MHSA contributions

Insurance Companies

Keep the spread between what they earn by investing the money and what they have to pay to

their investor, the NHR.

Guarantee to pay at least 1% more than the inflation rate.

Maybe return windfall investment income to the NHR if such a windfall ever happens.

Heirs of the MHSA Owner

Inherit the MHSA surplus if the

MHSA owner(s) stayed healthy

and accumulated a surplus.

Individuals, Businesses, and other

parties

Hire TPAs to manage the paperwork for

themselves or their employees.

Buy health insurance in various

circumstances.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 12

Points Made by Figure 1

1. The contribution is a percentage of each person’s income up to annual maximum.

a. Healthcare insurance companies do not decide how much premium to charge except

in the case of private policies they sell independently from this proposed system.

b. If the health insurance companies in business today are overcharging their customers,

this model will prevent that from continuing because healthcare cost inflation will no

longer be an excuse they can use to raise rates.

c. If healthcare prices continue to rise faster than the general rate of inflation, Congress

will have to vote to change the MHSA rate or the HVAT rate; at least there will be

some accountability.

2. Public and private employers are not responsible for the healthcare of others nor do they have

to pay the premiums for it; individuals and families are responsible for their health and they

will pay for their own healthcare up to a reasonable limit.

3. The NHR Administration will be the only customer of the insurance companies that manage

the investments. The NHR Administration will deposit funds with those insurance companies

that offer the most competitive bids to manage the investments and guarantee the interest

rate.

4. Businesses, governments, and individuals will have business relationships with the TPAs that

win them as customers in a competitive TPA market.

5. Healthcare providers will bill the TPA or insurance company of each patient similarly to how

they do it today. It will be less complex than it is today.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 13

Figure 2 - Illustrations That Show How this Proposal Creates the Incentive to Practice Wellness

Cumulative MHSA contributions and investment

returns during an individual’s or couple’s lifetime

Cumulative healthcare claims paid out of the

MHSA during the individual’s or couple’s

lifetime.

Surplus in the MHSA that the individual or

surviving spouse can leave to his heirs, estate,

charity, etc.

Cumulative MHSA contributions and investment

returns during an individual’s or couple’s lifetime

Cumulative healthcare claims paid out of the

MHSA during the individual’s or couple’s

lifetime.

Deficit in the MHSA when this individual passes

away or when the surviving spouse passes away.

Younger age adult

Older age adult

Younger age adult

Older age adult

Scenario 1

Scenario 2

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 14

Scenario 1 in the above chart

This couple avoided costly healthcare claims during their lives. Not only do they have money in

their MHSA to give to their heirs but they also paid the HVAT throughout their lives and never

directly benefitted from it except for preventive care.

If their MHSA surplus is substantial, this couple might decide to hedge against a catastrophic

illness by purchasing a catastrophic healthcare insurance policy in the private market. The

private healthcare industry therefore still has an important role to play in the healthcare insurance

business but it will be voluntary among parties, not compulsory.

Scenario 2 in the above chart

This couple or individual spent more on healthcare claims during their lifetime than they

contributed to their MHSA, but the chart does not tell the whole story. If this couple had a

substantial surplus in their MHSA when they reached their older years, before the onset of a

catastrophic illness, they could have protected their MHSA by buying a catastrophic healthcare

policy in the private market. If they did that, their chart would look more like Scenario 1.

This couple also paid the HVAT during their lives. It is possible that the total amount they

contributed to their MHSA plus the amount of tax they paid was greater than the total of their

healthcare claims; if that were the case, it means they paid all of their healthcare bills during their

lives and did not benefit from other people’s money.

General Concept of How the Money Will Flow

1. Every individual or family will contribute about 5% of its income to its MHSA up to an

annual maximum.

a. About 4% will be a self-insurance premium. Policymakers will decide how much of it

the MHSA owner’s beneficiaries can inherit if there is an unspent surplus when the

owner dies.

b. About 1% will be used to pay excess healthcare claims if the individuals or families

have them during their lifetimes. Whatever portion they didn’t use, because they

stayed healthy, they can give to their heirs.

c. Policymakers will decide the percentages in items (a) and (b) above. The smaller the

value of (a), the higher that (b) can be. The smaller the value of (a), the higher the

HVAT rate will be.

2. The insurance companies will invest pools of MHSA money and try to get the best ROI they

can without taking too much risk, just as they do today with annuities and similar products.

3. The insurance companies will pay a guaranteed interest rate on the MHSA money. I don’t

know what that guaranteed interest rate will be but it should be at least 1% greater than the

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 15

inflation rate, on average, at all times. I have used that assumption in the example worksheet

referenced later in this document.

a. You might wonder why the MHSA should not be permitted to earn a higher rate of

return, such as the historic rates of return of the S&P 500. I am guessing that if many

billions of dollars are collectively accumulating in MHSA accounts, there will be too

much money chasing too few shares of quality equities and that would put the MHSA

balances at risk of losing money in market crashes. I am guessing that the money will

have to be professionally managed and regulated just as annuities and life insurance

contracts are regulated today.

b. If you consider how high inflation has been at different times over the last century or

so; it is not a bad deal if you can earn 1% or more above the inflation rate.

4. If all of the money collected to pay for healthcare, from all sources, is not sufficient to cover

the cost of healthcare nationwide, the HVAT will make up the shortfall. In other words; if

workmen’s compensation, veterans’ benefits, medical liability, contributions from every

person’s income, and everything else I have not thought of, do not raise enough money to

pay the national healthcare bill, then the HVAT will kick in. Hopefully that means the

HVAT rate will remain low.

Benefits

Fairness

o It is fair and reasonable to pay for preventive care with public money from the NHR

because everyone needs preventive care and everyone will receive it fairly equally; we all

should get roughly the same physical exams, vaccinations, and screenings during our

lives and so it nets out equitably. Psychologically, most people will perceive that it is

free and therefore they will use it.

o Illegal aliens will pay the HVAT every time they buy something and that money can be

used to give them healthcare in emergency situations.

o Those who spend unreported income will pay the HVAT every time they buy something.

o It does not force the wealthy to pay an unfair share of the cost.

o There is no rule that says the healthcare insurance companies that exist today cannot be

both TPAs and investment companies. They can still do everything they do today except

decide how much premium to charge.

Benefits to Businesses and by Extension to the Economy

o Businesses will have much better certainty about their costs so they can hire more

workers without worrying about health insurance price increases. Unemployment

could go down.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 16

o One of the motives for sending work offshore is to avoid the high cost of employee

benefits. Maybe fewer workers will be laid off if the cost of healthcare is shifted to

MHSAs and HVAT.

o Businesses large and small will no longer pay health insurance premiums. They have the

option to voluntarily negotiate the best TPA contract they can find on behalf of their

workers.

o The HVAT will be across the board for all businesses; the playing field will be level.

o Some businesses, such as restaurants, will go out of business if they are forced to pay for

employee health insurance. This proposal takes that pressure off of them.

Benefits to the People

o Everyone will have an incentive to utilize preventive care because it will be paid for by

the NHR. Therefore, hopefully, the Nation as a whole will be healthier and the overall

portion of GNP spent on healthcare will decrease.

o This proposed system gives every individual a significant financial incentive to stay as

healthy as possible throughout his or her life so that he or she will have a significant

surplus in his or her MHSA that will be inherited by his or her loved ones.

o Provides benefits during periods of unemployment; for example, if a person saves

money in his MHSA for many years and then loses his job, he will have a surplus in his

MHSA to pay for healthcare. It is unfair to expect persons to pay for health insurance

throughout their lives and then have nothing to show for it if they become unemployed.

Benefits to Government and by Extension to the People

o States will be relieved of the high cost of Medicaid or at least most of it. There might

still be programs to help those who fall through the eligibility cracks for various reasons.

o The cost of government will go down significantly because governments at all levels

will no longer have to pay health insurance premiums for employees or retirees. They

have the option to voluntarily negotiate the best TPA contract they can find on behalf of

their workers.

o Relieves the pressure to make politically difficult choices such as budget cuts and tax

increases.

General Parameters I Have Thought of So Far

Requirements

This proposal shifts the cost of healthcare from businesses, governments, Medicaid,

Medicare, and other programs; to the model explained above.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 17

o The amount of money that many persons will contribute to their MHSA plus what

they pay in HVAT will be less than what they and their employers pay now for

insurance premiums. I am hoping that employers will give their employees pay

increases when and if this system is implemented to offset any initial shock it might

cause. It will then become the norm and hopefully everyone will be comfortable with

it.

Create a National Healthcare Reserve (NHR) and fund it with a Healthcare-only Value

Added Tax (HVAT), contributions paid into the MHSAs, and other taxes that policymakers

choose to contribute.

Require everyone or every household to have a managed healthcare savings account (MHSA)

and contribute to it as much as they can afford up to a reasonable limit; for example, $3,000

per year for each person living in the household, up to a maximum of 5% of household

income; adjusted for inflation every year.

Allow the health insurance companies we have today to be the day-to-day administrators of

the system. The insurance industry refers to such companies as Third Party Administrators

(TPAs).

The policymakers (federal and state) must ensure that there is vigorous competition among

TPAs so that TPA fees are as reasonable as possible.

The TPAs will earn money and a profit by charging fees for transactions and services. TPAs

will be responsible for doing what they do best:

o Managed care.

o Negotiating PPO prices and contracts with providers.

o Administering wellness programs.

o Paying claims accurately.

o Uncovering fraud (they should be given an incentive to so).

Each individual must be a customer of a TPA either directly or indirectly so that they receive

the cost containment benefits of managed care and PPO arrangements. An employer can pay

the TPA on behalf of its employees; associations can negotiate on behalf of their members;

some individuals will pay on their own, etc.

o The TPAs that negotiate the most reasonable PPO contracts and provide the best

customer service are the TPAs that will win the most customers in the free market.

o Policymakers will decide the best way to enroll senior citizens into TPAs and how to

pay the fees. Many employers might offer to do it on behalf of their retirees.

Health insurance companies will remain in the underwriting business and sell policies to

customers in specific circumstances such as those mentioned under the Exceptions heading

below.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 18

Everyone (with a few exceptions mentioned below) must participate in the same system

using the same rules. There will not be special benefit classes for government workers,

elected officials, union workers, executives and everybody else.

If the premiums and HVAT paid by the owner during his lifetime exceeded his medical

expenses, his heirs will inherit the surplus in his MHSA account and that will be the

incentive for the MHSA owner to stay healthy; he can live a healthier, wealthier,

happier life and give a substantial gift to his heirs.

Exceptions and Limitations

This proposed system does not replace liability-related indemnity systems such as

workmen’s compensation and the medical liability coverage from other types of insurance.

Persons in paid occupations that put them at high risk of injury; such as, NFL players, other

professional athletes, racecar drivers, acrobats, and stuntmen, should have private insurance

or other means to pay for the injuries they sustain at their jobs. All sorts of variations might

be invented; such as requiring people to buy insurance to protect them while they are

engaging in risky activities such as sky diving, SCUBA diving, skiing, etc. Analogous to

buying insurance when renting a car.

Government workers that serve in harm’s way should probably be insured separately from

this system but that topic is open for debate. A progressive tax is a more equitable way to

pay for the healthcare of soldiers and wounded veterans in my opinion.

Policymakers will have to decide how much benefit a person can receive from the NHR if

that person has under-contributed to his MHSA (relative to his age). This is one of those

difficult moral hazard problems to solve; if a person could have and should have earned or

reported more income but didn’t, that person might have to buy a healthcare personal

umbrella policy to cover losses in excess of what the NHR will pay. There is a good chance

that such umbrella policies will be very affordable since they will only cover losses after a

person has exceeded some (to be determined) lifetime deductible; for example, the lifetime

deductible might range from $50,000 to $100,000 in 2011 dollars depending on the person’s

age and the degree of under-funding in his MHSA.

o Legal immigrants, who come to the USA later in life and have contributed very little

to their MHSAs or to the NHR, are a class of persons that fall into this category. The

more time such persons live and work in the USA, the higher their lifetime umbrella

policy deductibles will be, the less those policies will cost, until they are no longer

required.

o Policymakers will decide how to handle illegal aliens. They should probably be

enrolled in a non-profit or modest-profit insurance pool as others before me have

proposed. The HVAT paid by this class of persons could be used to offset some of the

cost of the insurance pool.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 19

Paternal and maternal responsibility should not be circumvented; for example, biological

fathers have to help pay for the healthcare of the children they fathered by having their

children linked to their MHSA accounts. This rule applies whether the parents were married

or not. If you are the father or the mother, you are responsible for the child unless the child is

legally adopted by someone else.

Wealthy persons who live off of investment income will have to contribute to their MHSAs.

Just because you are wealthy today does not mean you will be wealthy tomorrow (you could

lose it all for some reason, such as a failed business venture). You have to fund your MHSA

like everyone else just in case you need it in the future.

There should be a limit on how much HVAT a person has to pay per year. Very wealthy

persons can easily spend enough money to pay much more than their fair share of the NHR

tab. They should keep their receipts and be able to take a deduction on their income tax

returns for the excess HVAT they paid. Policymakers will have to decide what amount

constitutes “excess”. I would say somewhere around $10,000 per person on their tax returns;

for example, if a billionaire has a family of four and pays $200,000.00 a year for HVAT, he

should be able to deduct $160,000.00 of HVAT from his income on his tax return

($200,000.00 – ($10,000 x 4)). It might even be permissible for very wealthy persons to opt

out of the system and not pay the HVAT at all if they put enough money into escrow

accounts to guarantee they will pay for their own healthcare throughout their lifetimes.

Policymakers cannot not raid the NHR and use it to pay general government expenses. If

they do that, they will break this model; for example, policymakers cannot allow wealthy

persons to deduct excess HVAT on their tax returns if HVAT revenue is being used for non-

healthcare expenses. They will also cause the public to distrust them more than they do

already because they will perceive the HVAT as a back door tax increase. If policymakers

want to use a VAT for general expenditures, Congress will have to muster the votes to pass

one that is separate and distinct from the HVAT.

There should be limits and/or extra scrutiny of medical services that are discretionary more

than they are necessary; for example, psychiatry is necessary and proper for those who really

need it but it can also be abused by those who don’t really need it. The same is true for

physical therapy. The TPAs have a lot of experience in these areas and will help administer

it. The goal is not to use public money for unnecessary healthcare; we can’t have millions of

people chatting with their psychiatrists every week or getting massages from physical

therapists because they know the NHR will pay for it.

Hypothetical illustrations of this proposed system in action

Please take time to carefully look over the illustrations prepared with Microsoft Excel

worksheets. Change the numbers and model your own examples if you like. Be sure to study the

assumptions and the formulas at the top of each column so you can follow my thinking.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 20

Hypothetical MHSA HVAT Examples - PDF1

Hypothetical MHSA HVAT Examples - Excel Workbook2

What the examples illustrate

They illustrate:

1. If individuals and families make an effort to stay healthy and avoid preventable health

problems, they have a very good chance of funding their own health care during their

lives and still have money left in their MHSAs to pass on to their heirs.

2. It will be mostly those individuals who have low incomes and health problems that will

need help from the NHR.

3. If the NHR is used to pay for preventive care, individuals and families have a good

chance of saving and accumulating significant amounts of money in their MHSAs by the

time they reach their senior years and they can use that money to pay for healthcare

during their senior years when many health issues arise.

4.

My Replies to the Negative Rhetoric I Anticipate 1. One of the first things the opponents of this proposal are going to do is scare the pubic by

branding it as a tax increase, socialism, government meddling, etc. Those are false claims.

This proposal is good for everyone and it lets private insurance companies run most of it and

profit from it.

2. Critics might say that the assumptions I made in my hypothetical illustrations are optimistic.

Even if that were true; if everyone pays as much as they can reasonably afford to pay during

their lifetimes and the rest of the money comes from a common pool (the NHR) that is

funded by an equitable tax, and some claims are paid from private insurance; isn’t that the

best we can do for ourselves as a nation anyway? If that is not good enough than what is? Do

the critics have a better plan? Just keep in mind that there is a National Debt crisis, an

obesity crisis, and other health problems. All of them need to be mitigated.

Maybe the health insurers will resist even though they will still be profitable.

o If we’re lucky, maybe some health insurers will be satisfied by being the TPA for

tens of millions of new customers from Medicare and Medicaid and they will

actually support this plan. They would not have to insure any of them; just do the

paperwork and make a profit without assuming any risk.

1 http://www.jeffreyromel.us/Hypothetical%20HSA%20HVAT%20Examples.pdf

2 http://www.jeffreyromel.us/Hypothetical%20HSA%20HVAT%20Examples.xls

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 21

Now that new health care laws have put restrictions on cherry picking, perhaps the health

insurance companies will prefer this new system.

There will still be a market for private health insurance for many individuals as written

above.

3. Persons who are currently covered by health insurance policies with low deductibles and low

copayments might resist this new system until they realize that their health insurance plans

are going to be weakened eventually anyway and that this new system will reduce other

taxes and prices that they pay if governments and businesses pass on their cost

reductions to the public.

Fraud Prevention We have all probably read news about Medicare fraud; such as stories about healthcare service

providers that submit phony claims to Medicare, etc. This new proposed system will make fraud

more difficult to commit. Healthcare providers have to submit claims to a TPA. The TPA has to

withdraw money from a real MHSA that belongs to a real person and they have to send an

Explanation of Benefits (EOB) to the owner of the MHSA. If the owner of the MHSA actually

reads his EOB and notices that money has been withdrawn from his MHSA for a service he

never received, he is going to report that to the TPA and get the discrepancy resolved. The TPA

and/or the MHSA owner will then report the suspected fraud to law enforcement.

The only way fraudulent claims can be successful is if the healthcare provider and the healthcare

recipient are in collusion and the healthcare recipient is willing to run up a deeper and deeper

negative balance in his MHSA. The healthcare provider would then presumably have to kick

back some of the claim money to the healthcare recipient thereby introducing a money

laundering crime into the mix. The more parties that are involved in a fraud, the more likely it is

that the fraud will be uncovered.

The Underground Economy An HVAT is a great way to collect revenue from those who under-report their incomes and

under-contribute to their MHSAs; for example, if a drug dealer launders most of his ill-gotten

income, at least he will pay the HVAT when he buys his expensive car(s), his luxurious home(s),

his fancy meals at five star restaurants, and everything else money can buy.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 22

Impact on lower-income persons A value added tax that is only used for healthcare and which pays for everyone’s preventive care

does not put an unfair burden on lower-income persons. Lower-income persons will probably

get out of it more than they put into it.

A general purpose value added tax arguably puts an unfair burden on low-income persons. This

proposed system does not endorse a general purpose VAT.

MHSAs are not unfair to the poor. If low-income persons can afford other discretionary items,

they can afford a modest 5% pre-tax MHSA contribution; for example, a person who earns

$10.00 per hour, earns about $80.00 per day. 5% of $80.00 is only $4.00. A person can spend

$4.00 pretty fast nowadays on all kinds of discretionary items.

This proposal will at least give low-income persons a chance to save money for their heirs; a

low-income person and his spouse can accumulate a respectable surplus in their MHSA account

if they get their preventive care from the NHR, take care of themselves throughout their lives, do

not get costly diseases during their lives, and their children stay healthy while they are

dependents. Such a couple would be able to leave a significant amount of money to their kids

and maybe help break the cycle of poverty just that much more.

How many basis points will the HVAT be when it is first enacted?

I am not an expert on everything and so my calculations are reasonable guesses. I know that

Denmark has a 25% VAT that is used to pay for all manner of things in that country. If a 25%

VAT pays for a lot more than just healthcare, what would Denmark’s HVAT rate be if they had

one? I know that the percent of GDP spent on healthcare in the USA in 2008 was about 16.2%. I

can therefore guess that if the USA had a 25% VAT, the healthcare component of it would be

about 4.05%; however: (1) the USA also has an income tax, (2) this proposal requires that

MHSAs pay a large part of the healthcare cost, and (3) private healthcare insurance will still be

used in many circumstances if the parameters I described above play out. I can therefore guess

that the HVAT will be around 2% (a.k.a. 200 basis points), maybe even 1% if the 16.2% figure

above includes workmen’s compensation, veterans’ benefits, etc., because the HVAT is only

going to pay for claims that are not covered by any other source.

In Denmark, VAT is generally applied at one rate . . . The current standard rate of VAT in Denmark is 25%. That makes Denmark one of the countries with the highest value added tax, alongside Norway and Sweden. A number of services have reduced VAT, for instance public transportation of private persons, health care services, publishing newspapers, rent of premises (the lessor can, though, voluntarily register as VAT payer, except for residential premises), and travel agency operations. (Value added tax, 2011)

In 2008, U.S. health care spending was about $7,681 per resident and accounted for 16.2% of the nation’s Gross

Domestic Product (GDP); this is among the highest of all industrialized countries. Total health care expenditures grew

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 23

at an annual rate of 4.4 percent in 2008, a slower rate than recent years, yet still outpacing inflation and the growth in

national income. Absent reform, there is general agreement that health costs are likely to continue to rise in the

foreseeable future. Many analysts have cited controlling health care costs as a key tenet for broader economic stability

and growth, and President Obama has made cost control a focus of health reform efforts under way. (Kaiser Family

Foundation, 2010)

Other Ways and Means to Add Funds to the NHR Policymakers can choose to keep the HVAT rate lower by funding the NHR from multiple

sources; such as with vice taxes, a modest junk food sales tax, gambling taxes, confiscated assets

from illegal activities, and so on.

Smoothes the Trend Line of Healthcare Cost Inflation The excerpt cited below states that premiums for small businesses in New Hampshire had to be

increased from 20 – 43 percent in 2011 because of rising healthcare costs and coverage for new

items such as preventive care, autism and hearing aids.

Workers at a circuit-board factory here just saw their health insurance premiums rise 20 percent. At Buddy Zaremba’s print shop nearby, the increase was 37 percent. And for engineers at the Woodland Design Group, they rose 43 percent . . . “The rate of increase is phenomenal,” said Jean Pierre La Tourette, owner of Flora Ventures, a florist with 11 employees in Newmarket, N.H., near Portsmouth. When he was recently notified that the monthly premium for single employees at his firm was going up by $229, or 40 percent, to $789, Mr. La Tourette said, he felt “a combination of anger and frustration.”

— (Pear, As Health Costs Soar, G.O.P. and Insurers Differ on Cause, 2011)

If the USA had an HVAT rate of 100 basis points, Congress would have to increase it to 120 –

143 basis points in a single year. Would Congress have the willpower to do that? Maybe they

would if the CBO and GAO demonstrated it was really necessary in order to include preventive

care for everyone as the new healthcare law requires. Would Congress enact such large

increases again and again year after year? I doubt it. It would come to a political head.

One benefit of this proposal is that it takes the healthcare price inflation anxiety off of businesses

and governments and puts everybody’s attention on the HVAT rate and the MHSA contribution

rate because those are the two numbers each person is going to be affected by the most.

It seems to me that small businesses like those mentioned above and large businesses too would

rather deal with a 20 – 43 basis point increase in the HVAT rate rather than a 20 – 43 basis point

increase in their health insurance premiums. The premiums force them to increase their prices

and could affect their competiveness. The HVAT would have a much smaller impact and it

would be passed on to the next link in the supply chain. All businesses would be affected equally

by the HVAT. There would not be variations of 20 – 43 basis points from one business to the

next as there was in the case cited above.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 24

Additionally, if there were an HVAT, the rate would increase at the national average or maybe at

the state average rather than on a case by case basis.

Opt out or opt in It is theoretically possible that individuals could opt out of the system. If they want to opt in

later they will have to make catch-up contributions to their MHSAs and to the NHR and that

could be expensive.

Why not let the Federal Government (Medicare) Be the TPA? I considered endorsing the idea that everyone be enrolled in Medicare because Medicare is

efficient and pays out 98% of its premiums to claimants. The problem with Medicare is that it is

run by Government employees and our Government is already deep in the red. It is better to let

private TPAs do most of the work while the Government functions as auditor and law enforcer.

Let most of the employees work in the private sector and pay taxes rather than work in the public

sector and be paid by taxes. That is the way most other departments of the Government operate.

We don’t nationalize defense companies even though they benefit everyone so why should we

nationalize TPAs?

Phase In Policymakers will have to decide the best way to phase in this system and phase out the old

systems. It is unfair to make those who have paid Medicare premiums all their lives to also pay

HVAT taxes. Policymakers should devise a formula to let taxpayers deduct the HVAT they have

paid to the extent that they have already paid Medicare payroll taxes; or perhaps older persons

will be exempt from paying HVAT taxes on many items, or some combination of both, etc.

The Medicare administration has records of how much payroll tax each person has paid and

when they paid it. It also has records of claims paid on behalf of each person and when they

were paid. That means the Medicare administration can calculate the MHSA balance that each

person would have today based on when each deposit and withdrawal occurred as if this new

system had been in effect all along. That means the Government could seed the MHSA account

of each person with a fair and equitable starting amount (positive or negative), enroll everyone in

a TPA based on some formula, and phase out Medicare as we know it.

Aphorisms for This Model

Keep your health well and your MHSA will swell.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 25

To have a happier heir; for your health you should care.

An ounce of prevention is worth a pound£

in your MHSA.

Philosophic Justification of MHSAs and HVAT

Personal responsibility

Much of the healthcare utilized in our society today is used to treat preventable illnesses caused

by improper diet, inadequate exercise and harmful personal habits.

We all bear responsibility for our own health and the health of others directly and

indirectly

Think about why persons get sick and then stop to think about how we are all at least partially

responsible for it. There is tons of research and writing on this topic.

We have pollution, pesticides, violence, unhealthful foods, legal drugs like nicotine3, and

harmful illegal drugs in our society; and to the extent we do not or cannot control them, we all

bear responsibility for them to the extent we each create a demand for them.

We all buy products from developing countries because they are less expensive in the short run

but who is going to pay for the treatment of diseases caused by the massive amounts of pollution

released into the environment in those countries; some of which finds its way into the food we

eat, the water we drink, and the air we breathe?

Business expenses are indirect flat taxes

If businesses pay for employee health insurance, they pass that cost along to their customers in

the form of higher prices. If businesses receive tax credits to offset some of the cost of

insurance, then the burden is shifted to other taxpayers.

Governments pay for healthcare with taxes

If governments pay for employee healthcare and Medicaid, they shift that cost to the people in

the form of taxes; some of which are flat taxes similar to an HVAT; such as vice taxes, and fees.

Payroll taxes already pay for Medicare

Why not simply replace Medicare with this proposed system?

3 Nicotine makes us want to smoke or chew tobacco and it is the smoking or chewing that is harmful more so than the nicotine

itself.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 26

Health Insurance Companies Cannot Tell People How to Behave

Other kinds of insurance have long had loss control incentives associated with them; for

example, if you make your workplace safer, your workmen’s compensation premiums will be

reduced. If you drive recklessly, your auto insurance premiums will rise or your insurance will

be cancelled. Health insurers have thus far been unable or unwilling to offer significant

incentives to persons who stay in good health. HSAs are a good way to motivate wellness

without regulating personal behavior.

Perks and Paternalism

Employer-sponsored health insurance was a voluntary benefit designed to indemnify workers for

their healthcare-related losses so that they would not become financially ruined and thus become

unproductive or steal from their employers (Wood, Lilly III, Malecki, Graves, & Rosenbloom,

1989, pp. 381, 398), (Rodda, Trieschmann, Weining, & Hedges, 1988, p. 372). Since then it has

become a perk that workers have come to expect and some employers use to attract workers.

Employers should not be responsible for my health in my opinion; I am an adult and it should be

up to me to manage my health and avoid preventable health problems. I would rather be paid a

higher wage and then fund my MHSA myself. Self-Insurance Plus would protect both me and

my employer.

Business owners have enough responsibilities already and they should not have to spend

precious time concerning themselves with healthcare financing arrangements for their

employees.

Supporting Materials

Medicare is Unsustainable

Medicare will run out of money by 2024 according to the official Federal Government

projections given during testimony on May 13, 2011 (Levey, 2011). If everyone accumulated

money in their MHSAs during their younger years as described above in this proposal, most of

them would have MHSA nest eggs in their senior years and the USA would not be facing the

catastrophic Medicare shortfall that it now has to deal with.

Opinions of others who support a VAT to pay some of the cost of healthcare.

Dr. Victor Fuchs, emeritus professor of economics and health research and policy at Stanford

University, said the following (as cited in Kolata, 2012):

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 27

The big thing for me is a dedicated value-added tax. It would provide universal coverage,

a basic health care system for everyone. But the tax could be used only to pay for basic

medical care, and basic medical care could be paid for only with the tax.

We want to subsidize the poor and the sick. The value-added tax is a function of income

— the poor and the sick would pay much less. People are free to buy more health

insurance, but they would do it with after-tax dollars.

Money That Rightfully Belongs in MHSAs to Pay Real Medical Bills, Not in the

Excessive Profits of Private Health Insurers “The nation’s major health insurers are barreling into a third year of record profits, enriched

in recent months by a lingering recessionary mind-set among Americans who are postponing

or forgoing medical care. . . . Yet the companies continue to press for higher premiums, even

though their reserve coffers are flush with profits and shareholders have been rewarded with

new dividends. Many defend proposed double-digit increases in the rates they charge, citing

a need for protection against any sudden uptick in demand once people have more money to

spend on their health, as well as the rising price of care.”

— (Abelson, 2011)

Evidence That the Affordable Care Act is Reducing Premiums for Younger Persons and

Employers

“U.S. Rep. Joe Courtney, D-2nd District, said the price decrease ‘is a direct result of the

new medical-loss ratio requirement in the Affordable Care Act.’

‘This announcement combined with the health care reform law's small employer tax

credit will further turn the tide of rising health care costs for Connecticut's job creators,’

Courtney said in a written statement.”

— (Sturdevant, 2011)

Even if some excess is premium is being forced out of the private health insurance companies’

pricing models, it still is not helping healthier younger persons save money to pay for their

healthcare when they are older. It is also complicated and difficult to audit the private health

insurance companies.

Conclusion

Healthcare is going to be paid for by our society one way or another. The variables are: who pays

for it, who benefits from it, and who profits from it. The financing model that motivates

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 28

people to practice wellness and shop for the best value in a competitive market is a

powerful, free-market way to contain healthcare costs.

If healthcare costs continue to rise far faster than the general rate of inflation, Congress will have

to enact some combination of MHSA contribution rate increases, HVAT rate increases, and

healthcare price limits. The democratic system of checks and balances will hopefully do what it

is designed to do and reach the equilibrium that most everyone can live with.

No matter what happens with healthcare cost inflation, the burden of it will be distributed fairly

to each individual; it won’t be obscured in the budgets of businesses and governments.

Businesses and governments cannot vote but most Americans can.

MHSAs, HVAT, vice taxes, and junk food taxes are fair ways to pay for all kinds of illnesses

and injuries brought on by our own habits and the modern industrialized market economy we

live in and prosper from.

The frequency and severity of many ailments would be reduced if each person were continuously

reminded that his MHSA surplus will go up and the HVAT will go down if he does his part to

take care of himself and the planet he lives on.

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 29

Examples

Example 1 – Trivializing arterial plaque

Following is an excellent case in point; a restaurant owner and his patrons are making a mockery

of wellness and personal accountability for health. I say this: it is a free country; do what you

want; but pay for your self-induced “triple bypass” with money you have saved in your MHSA

before you spend other people’s money to pay for it.

Man Has Heart Attack While Eating "Triple Bypass Burger"

Figure 3 - Heart Attack Grill Facebook Page

LAS VEGAS -- A man is recovering after suffering an apparent heart attack while eating a "Triple Bypass

Burger" at the Heart Attack Grill in Las Vegas. The unidentified man suddenly began complaining of chest

pains, started sweating and stuttering his words, says restaurant owner Jon Basso. The restaurant plays up

its "Taste Worth Dying For" slogan by dressing waitress [sic] and cooks like medical personnel. So, at first

fellow diners and staff thought the man was joking. But, it quickly became clear he was in serious trouble.

Basso called an ambulance and paramedics were quickly on hand to treat the man.

The customer is recovering in a nearby Las Vegas hospital.

The 6,000 calorie Triple Bypass Burger features 3 half-pound hamburger patties with buns dipped in lard,

half of an onion cooked in lard, a whole tomato, 15 pieces of bacon, cheese, and special sauce. Diners can

also enjoy a side of fries cooked in pure lard and butterfat shakes.

(KTLA News, 2012)

Self-Insurance Plus

Healthcare Funding Model

Version 2012-03-14 of http://www.jeffreyromel.us/Self-Insurance%20Plus.pdf You may send e-mail comments to [email protected] This proposal can be freely copied and distributed; in fact, the more persons that understand it and agree with it, the better. Copyright © Jeffrey Romel, 2011-2012 Page 30

Example 2 –Health insurance fraud is expensive

Medicare Fraud

“. . . Since 2009, Medicare fraud strike forces — teams that are run by the Department of