segmentation of bank commercial markets

TRANSCRIPT

SEGMENTATION OF BANK COMMERCIAL MARKETS by Emmanuel J. Chéron Laval University, Quebec City, Canada Ronald McTavish Concordia University, Montreal, Canada Jean Perrien University of Quebec at Montreal, Montreal, Canada

With the increasing competition and technological improvements in bank marketing, the need to make better and faster market planning decisions is greater than ever. Industrial markets represent attractive actual and potential customers for a bank. In contrast to retail markets, in the industrial markets, financial services are not acquired for themselves, or to meet a narrow personal need, but only for the contribution they can make to the economic, political or social objective of the purchaser.

The industrial market can be subdivided into the commercial market of small and medium-sized firms on the one hand and the corporate market on the other. Commercial markets represent the "middle" market and differ from the retail market and the corporate market. Corporate markets consist of very large corporations and government accounts offering high volume sales and requiring professional account management.

In the corporate market, individual contact with customers allows banks to adapt the offer to satisfy special financial services (Watson, 1986). However, in the commercial market, bankers can no longer maintain personal relations with all customers due to more heterogeneous and complex markets and a wider variety of financial products available. In that context, market segmentation can help account managers to better understand the market they face. The purpose of this article is twofold: (1) a review of market segmentation as a key element of bank marketing planning, and (2) the presentation of a two-step segmentation procedure involving: (a) secondary data such as geographical economic statistics, and (b) primary data such as the perception by the bank clients of the importance and the performance of financial services offered by the bank to the commercial market.

The Role of Segmentation within Marketing Planning Marketing is often thought of as customer orientation. Therefore bank marketing is centred on knowledge of the market and how financial products and services are perceived by small and medium-sized firms. Perceptions by actual and potential commercial customers are also influenced by competitive products within the political, legal and working relations environment.

Marketing planning covers the larger perspective of establishing performance objectives, deciding about branch expansion, information system development, fixing interest rates, sales personnel development, promotion, marketing budgeting and timing of market activities.

In the banking industry, the marketing orientation is not yet completely accepted at the top management level. One of the main reasons for this is the confusion between marketing and selling. The marketing concept is broader than selling in that it covers all the activities to which a bank's name might be attached. An additional reason for the lack of acceptance of marketing is that its contribution to the bank's profitability is not easy to quantify. However, structured market planning and market analysis can be evaluated in terms of concrete activities and results of account managers.

The marketing management process relies heavily on designing the bank's offering in terms of the target market's needs. Therefore, market analysis and knowledge is a key element to organising the bank's resources in such a way that clients are satisfied at a profit for the bank (McTavish and Perrien, 1988).

Commercial Market Segmentation The process of segmentation can be defined as separating the commercial market into groups of clients or potential clients in such a way that members of each resulting group have more in common with one another than with the members of other segments. Segmentation results from the fact that the commercial market is not homogeneous and that the identification of differing needs in the business market is required to adapt the marketing effort to serve the varying client needs at a profit.

Segmentation can be applied to both present and potential clients and several variables can be used such as client characteristics and/or buying situations. One constraint is that segments must reflect differences in

IJBM 7,6 1989

25

needs clearly connected with some adaptation of the marketing strategy. Further details of this constraint will be presented below.

Purpose of Commercial Market Segementation Three reasons can be identified that justify the segmentation of the commercial banking market:

(1) A better understanding of the market and its tendencies. The analysis of the market by subgroups according to financial services needed allows client characteristics to be related to different type of services required. For example, the line of credit requirements can be related to the size of the client and its area of activity (large wholesalers will need more credit margin than small retailers).

(2) Identification of unfulfilled needs. The analysis of the behaviour of certain segments can reveal new service opportunities for the bank. For example, the need for operating loans may be perceived as important by manufacturers and the corresponding service offered by the bank may be perceived as not well performed.

(3) Improvement of marketing activities through a better adaptation of the services offered in response to the need of clients. The simplication of banking transactions with a multi-purpose account is an example of adaptation to the needs of small businesses.

Commercial Market Segmentation Variables Many variables can be used to segment the bank commercial market. Two broad classes of variables can be identified. The first class corresponds to observable descriptive variables based on readily accessible existing data. The second category is based on non-observable variables requiring an additional data collection effort. The two classes of variables are respectively related to the two-stage market segmentation proposed by Wind and Cardozo (1974).

In the case of the bank commercial market, the first class of variables consists of the characteristics of the buying organisation and the financial services that are

needed. This is the traditional first stage of a segmentation approach based on the product/market combination. The following examples are available with respect to this category of variables (Chéron and Kleinschmidt, 1985):

• Characteristics of the buying organisation: size, industry type, geographical location, organisation structure, purchasing volume.

• Financial services needed: line of credit limit, type and number of treasury management services, number of financial institutions utilised (single source, multi-source), purchasing situation (new, modified, rebuy).

The first stage will be illustrated with the use of existing statistical data on the commercial market. Municipal data from urban communities are especially useful for assessing the relative position of the bank in a specific area with respect to different segments of the commercial market. In the previously mentioned second stage, subgroups of clients can be further examined for differences with respect to characterisitics of the buying unit.

Examples of variables in this category are:

• Structure of the buying unit, role, influence, participation and involvement of buying centre members.

• Degree of centralisation of financial decision making in the buying organisation.

• Individual characteristics of participants, attitudes, perceived risk, preferences, perception of determinants of the buying decision (product diversity, cost of financial charges, quality of financial services).

Since the second stage requires the collection of primary data, additional costs are involved and they should be examined in relation to the additional benefits resulting from a better adjustment to the clients' needs.

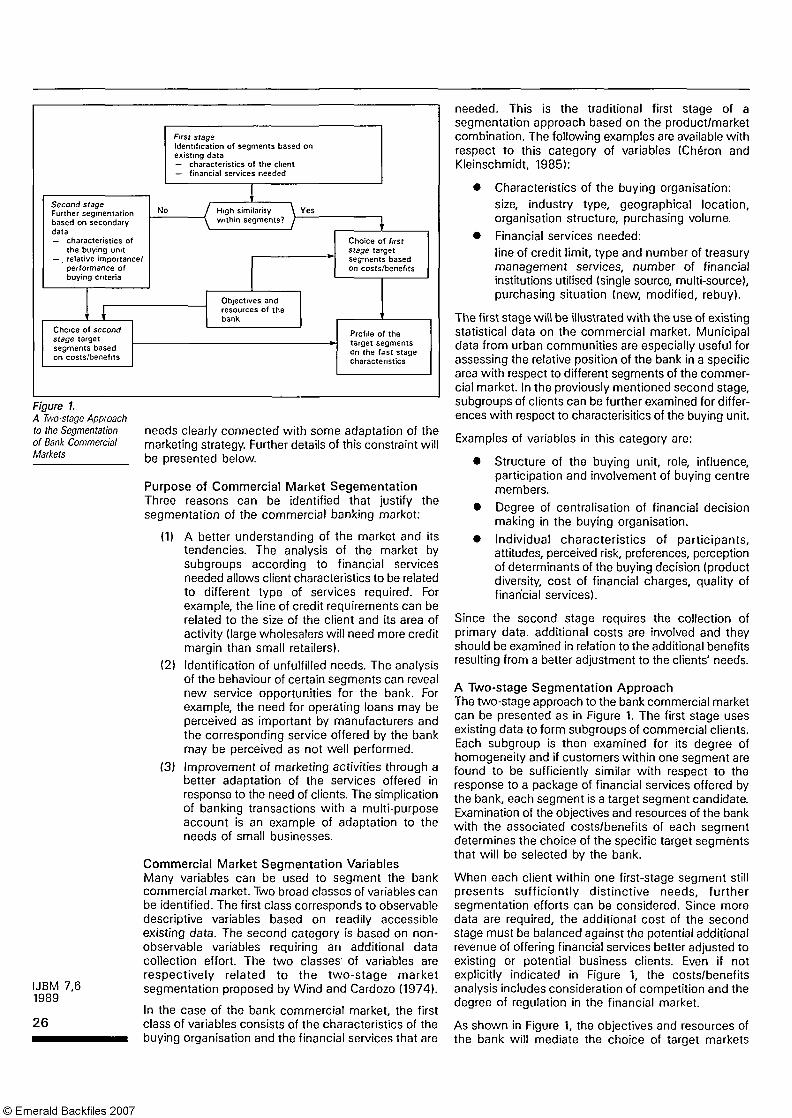

A Two-stage Segmentation Approach The two-stage approach to the bank commercial market can be presented as in Figure 1. The first stage uses existing data to form subgroups of commercial clients. Each subgroup is then examined for its degree of homogeneity and if customers within one segment are found to be sufficiently similar with respect to the response to a package of financial services offered by the bank, each segment is a target segment candidate. Examination of the objectives and resources of the bank with the associated costs/benefits of each segment determines the choice of the specific target segments that will be selected by the bank.

When each client within one first-stage segment still presents sufficiently distinctive needs, further segmentation efforts can be considered. Since more data are required, the additional cost of the second stage must be balanced against the potential additional revenue of offering financial services better adjusted to existing or potential business clients. Even if not explicitly indicated in Figure 1, the costs/benefits analysis includes consideration of competition and the degree of regulation in the financial market.

As shown in Figure 1, the objectives and resources of the bank will mediate the choice of target markets

IJBM 7,6 1989

26

whether at the first or the second segmentation stage. For example, in Canada, banks of category "A" are larger and will tackle a number of business market segments simultaneously. In contrast, " B " banks are more specialised and will tend to concentrate on fewer market segments (McTavish and Perrien, 1988).

In addition to the bank objectives and source, the choice of second-stage target segments must be connected with the segment's profiles on the first-stage characteristics. The requirement for the practical implementation of the second-stage segmentation is that second-stage segments also present distinct first-stage characteristics (Chéron and Kleinschmidt, 1985). For example, two segments of business clients may be associated with high and low sensitivity to automatic funds transfer. This second stage segmentation is not very useful unless the two segments also differ with respect to first-stage characteristics, such as size, industry type, geographical location, etc.

Requirements for Practical Implementation of a Commercial Market Segmentation The segmentation approach that has been presented is based on many variables and does not explicitly indicate where the process should stop before serving each business client individually. Four principal constraints can be associated with the practical implementation of segmentation.

(1) Economic attractiveness of a segment. The ultimate criteria for the choice of a target segment of actual or potential customers is its economic attractiveness in terms of size, growth rate, profitability and need for financial transactions. The size of the segment must also be related to the actual and potential competition among banks within the target segment.

(2) Segments should demonstrate distinctive needs for financial services. Each business client within a segment should be sufficiently similar with respect to the relative sensitivity to various financial services. Each segment must be homogeneous enough as regards their buying behaviour of financial services.

(3) Segments must be determinable for practical implementation. As discussed above, less observable variables of the second stage segmentation must be connected with descriptive characteristics of business clients for practical implementation of differentiated marketing strategy to different marketing segments.

(4) Compatibility of segments with the bank priorities. As indicated in Figure 1, the objectives and resources of the bank play a role in the choice of target segments. Each financial institution has its own characteristics and develops its own internal set of standards to guide the choice of target market. A bank will develop criteria that favour the choice of segments requiring financial services corresponding to the strengths of the bank.

Implementation of the Two-stage Segmentation Approach The authors' purpose is now to illustrate the first stage segmentation of the bank commercial market with

existing area statistics. A second stage segmentation will be presented with additional data on business clients' perceptions of the importance and the performance of various financial services.

First Stage Segmentation with Area Coding The procedure uses existing geographical data from Statistics Canada for the smallest area available. Statistical data on businesses provided by urban communities are used for the commercial market. These data classify the number of businesses, for each area, by type of activity, type of product or service and municipal assessment for tax purposes.

The use of business classification data, along with inputs from the bank's internal information on commercial customers, allows one to carry out the first step of segmentation. This first step leads to the examination of the commercial market coverage of the bank in each geographical area. Comparing the characteristics of the bank's clients with those of the market for each area is a. useful guide for the choice of target markets. The existence of a weak market coverage of the financial products and services of the bank for one area and for one type of business activity suggests directions for further investigation. A potential market segment opportunity may be available for the bank if the four requirements for implementation of segmentation are satisfied.

Segmentation with area coding is based on the analysis of commercial markets within areas of interest using external secondary data from census districts and the bank's internal data based on postal codes. The geographical matching between groups of census districts and postal codes is at the centre of the procedure.

Eight activities are involved in performing the commercial market segmentation with area coding for one branch of a bank:

(1) Definition of geographical areas to be analysed. This step requires the choice of criteria to form homogeneous areas of interest for the branch marketing strategy. The most common criteria are: • business districts • industrial areas • areas with potential for development • areas located close to the branch. Geographical maps from municipalities are necessary to delineate each areas of interest and to list the postal codes associated with each area (each postal code being associated with only one area). Postal codes will be necessary to connect the branch's actual clients and the municipal data to each defined area.

(2) Connection between municipal data and defined areas. Since the postal code is a larger geographical unit of analysis than the census district used by Statistics Canada, the latter can be used to ensure that the right commercial client is attached to the right defined area.

(3) File update of the commercial clients of the branch. This activity is required to make sure that postal codes are present and to account for multiple entries (clients with multiple accounts

IJBM 7,6 1989

27

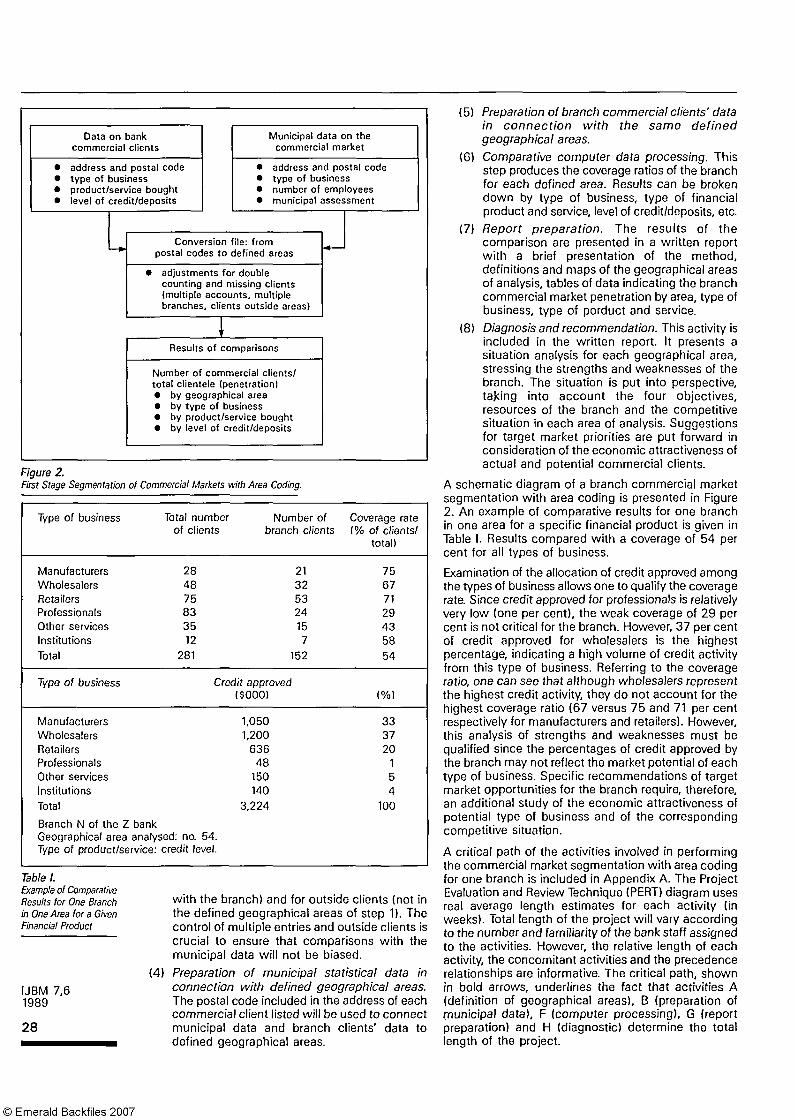

Type of business

Manufacturers Wholesalers Retailers Professionals Other services Institutions Total

Type of business

Manufacturers Wholesalers Retailers Professionals Other services Institutions Total

Branch N of the Z bank

Total number of clients

28 48 75 83 35 12

281

Number of branch clients

21 32 53 24 15 7

152

Credit approved

Geographical area analysed: no. 54. Type of product/service: credit level.

($000)

1,050 1,200

636 48

150 140

3,224

Coverage rate (% of clients/

total)

75 67 71 29 43 58 54

(%)

33 37 20

1 5 4

100

Table I. Example of Comparative Results for One Branch in One Area for a Given Financial Product

with the branch) and for outside clients (not in the defined geographical areas of step 1). The control of multiple entries and outside clients is crucial to ensure that comparisons with the municipal data will not be biased.

(4) Preparation of municipal statistical data in connection with defined geographical areas. The postal code included in the address of each commercial client listed will be used to connect municipal data and branch clients' data to defined geographical areas.

(5) Preparation of branch commercial clients' data in connection with the same defined geographical areas.

(6) Comparative computer data processing. This step produces the coverage ratios of the branch for each defined area. Results can be broken down by type of business, type of financial product and service, level of credit/deposits, etc.

(7) Report preparation. The results of the comparison are presented in a written report with a brief presentation of the method, definitions and maps of the geographical areas of analysis, tables of data indicating the branch commercial market penetration by area, type of business, type of porduct and service.

(8) Diagnosis and recommendation. This activity is included in the written report. It presents a situation analysis for each geographical area, stressing the strengths and weaknesses of the branch. The situation is put into perspective, taking into account the four objectives, resources of the branch and the competitive situation in each area of analysis. Suggestions for target market priorities are put forward in consideration of the economic attractiveness of actual and potential commercial clients.

A schematic diagram of a branch commercial market segmentation with area coding is presented in Figure 2. An example of comparative results for one branch in one area for a specific financial product is given in Table I. Results compared with a coverage of 54 per cent for all types of business.

Examination of the allocation of credit approved among the types of business allows one to qualify the coverage rate. Since credit approved for professionals is relatively very low (one per cent), the weak coverage of 29 per cent is not critical for the branch. However, 37 per cent of credit approved for wholesalers is the highest percentage, indicating a high volume of credit activity from this type of business. Referring to the coverage ratio, one can see that although wholesalers represent the highest credit activity, they do not account for the highest coverage ratio (67 versus 75 and 71 per cent respectively for manufacturers and retailers). However, this analysis of strengths and weaknesses must be qualified since the percentages of credit approved by the branch may not reflect the market potential of each type of business. Specific recommendations of target market opportunities for the branch require, therefore, an additional study of the economic attractiveness of potential type of business and of the corresponding competitive situation.

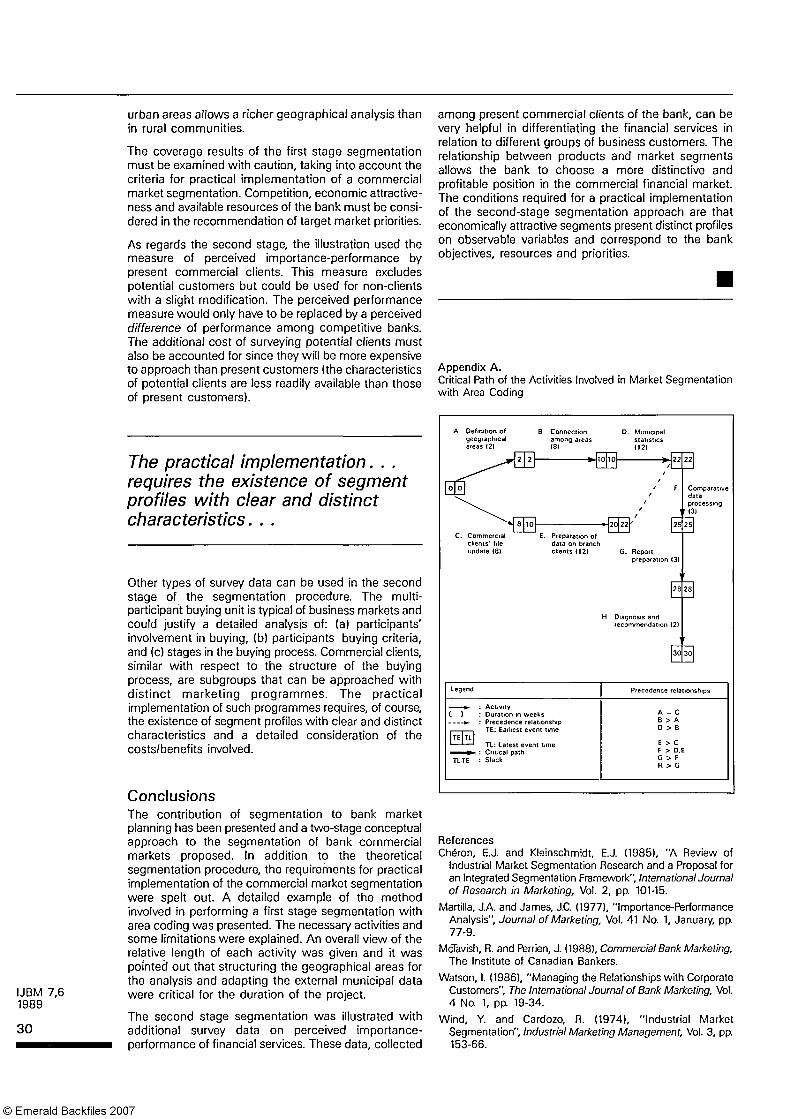

A critical path of the activities involved in performing the commercial market segmentation with area coding for one branch is included in Appendix A. The Project Evaluation and Review Technique (PERT) diagram uses real average length estimates for each activity (in weeks). Total length of the project will vary according to the number and familiarity of the bank staff assigned to the activities. However, the relative length of each activity, the concomitant activities and the precedence relationships are informative. The critical path, shown in bold arrows, underlines the fact that activities A (definition of geographical areas), B (preparation of municipal data), F (computer processing), G (report preparation) and H (diagnostic) determine the total length of the project.

IJBM 7,6 1989

28

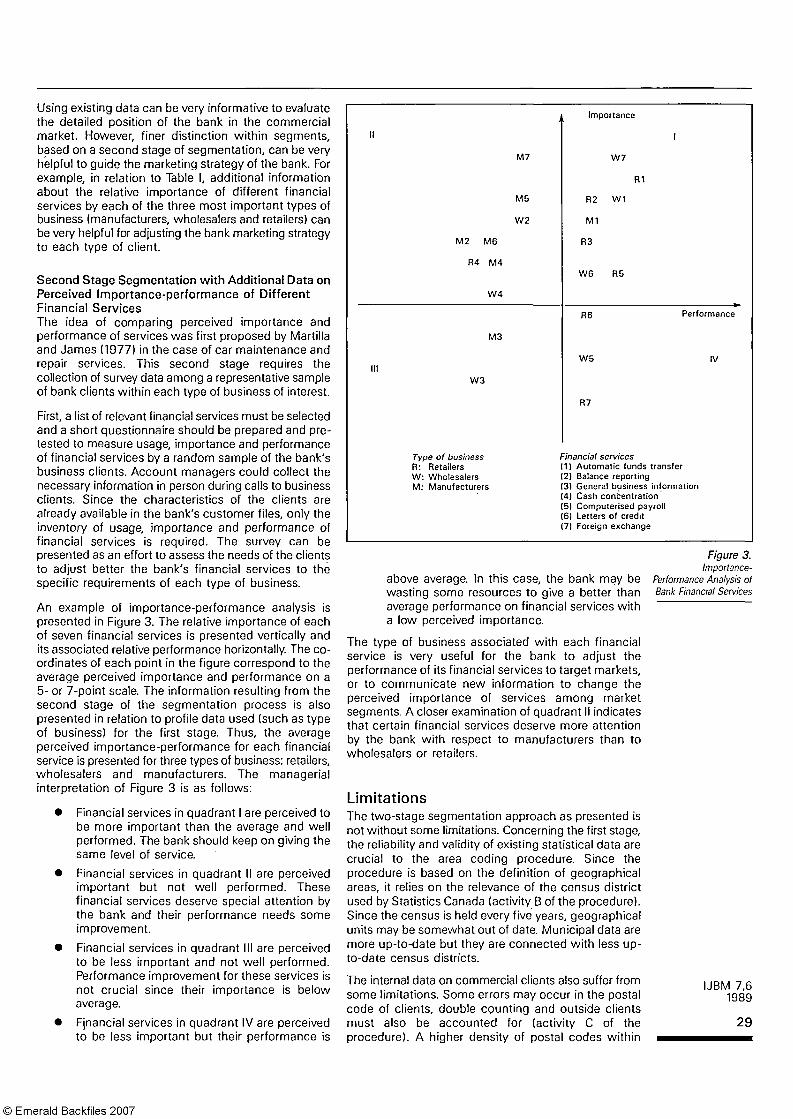

Using existing data can be very informative to evaluate the detailed position of the bank in the commercial market. However, finer distinction within segments, based on a second stage of segmentation, can be very helpful to guide the marketing strategy of the bank. For example, in relation to Table I, additional information about the relative importance of different financial services by each of the three most important types of business (manufacturers, wholesalers and retailers) can be very helpful for adjusting the bank marketing strategy to each type of client.

Second Stage Segmentation with Additional Data on Perceived Importance-performance of Different Financial Services The idea of comparing perceived importance and performance of services was first proposed by Martilla and James (1977) in the case of car maintenance and repair services. This second stage requires the collection of survey data among a representative sample of bank clients within each type of business of interest.

First, a list of relevant financial services must be selected and a short questionnaire should be prepared and pretested to measure usage, importance and performance of financial services by a random sample of the bank's business clients. Account managers could collect the necessary information in person during calls to business clients. Since the characteristics of the clients are already available in the bank's customer files, only the inventory of usage, importance and performance of financial services is required. The survey can be presented as an effort to assess the needs of the clients to adjust better the bank's financial services to the specific requirements of each type of business.

An example of importance-performance analysis is presented in Figure 3. The relative importance of each of seven financial services is presented vertically and its associated relative performance horizontally. The co-ordinates of each point in the figure correspond to the average perceived importance and performance on a 5- or 7-point scale. The information resulting from the second stage of the segmentation process is also presented in relation to profile data used (such as type of business) for the first stage. Thus, the average perceived importance-performance for each financial service is presented for three types of business: retailers, wholesalers and manufacturers. The managerial interpretation of Figure 3 is as follows:

• Financial services in quadrant I are perceived to be more important than the average and well performed. The bank should keep on giving the same level of service.

• Financial services in quadrant II are perceived important but not well performed. These financial services deserve special attention by the bank and their performance needs some improvement.

• Financial services in quadrant III are perceived to be less important and not well performed. Performance improvement for these services is not crucial since their importance is below average.

• Financial services in quadrant IV are perceived to be less important but their performance is

above average. In this case, the bank may be wasting some resources to give a better than average performance on financial services with a low perceived importance.

The type of business associated with each financial service is very useful for the bank to adjust the performance of its financial services to target markets, or to communicate new information to change the perceived importance of services among market segments. A closer examination of quadrant II indicates that certain financial services deserve more attention by the bank with respect to manufacturers than to wholesalers or retailers.

Limitations The two-stage segmentation approach as presented is not without some limitations. Concerning the first stage, the reliability and validity of existing statistical data are crucial to the area coding procedure. Since the procedure is based on the definition of geographical areas, it relies on the relevance of the census district used by Statistics Canada (activity B of the procedure). Since the census is held every five years, geographical units may be somewhat out of date. Municipal data are more up-to-date but they are connected with less up-to-date census districts.

The internal data on commercial clients also suffer from some limitations. Some errors may occur in the postal code of clients, double counting and outside clients must also be accounted for (activity C of the procedure). A higher density of postal codes within

IJBM 7,6 1989

29

urban areas allows a richer geographical analysis than in rural communities.

The coverage results of the first stage segmentation must be examined with caution, taking into account the criteria for practical implementation of a commercial market segmentation. Competition, economic attractiveness and available resources of the bank must be considered in the recommendation of target market priorities.

As regards the second stage, the illustration used the measure of perceived importance-performance by present commercial clients. This measure excludes potential customers but could be used for non-clients with a slight modification. The perceived performance measure would only have to be replaced by a perceived difference of performance among competitive banks. The additional cost of surveying potential clients must also be accounted for since they will be more expensive to approach than present customers (the characteristics of potential clients are less readily available than those of present customers).

The practical implementation. . . requires the existence of segment profiles with clear and distinct characteristics. . .

Other types of survey data can be used in the second stage of the segmentation procedure. The multi-participant buying unit is typical of business markets and could justify a detailed analysis of: (a) participants' involvement in buying, (b) participants buying criteria, and (c) stages in the buying process. Commercial clients, similar with respect to the structure of the buying process, are subgroups that can be approached with distinct marketing programmes. The practical implementation of such programmes requires, of course, the existence of segment profiles with clear and distinct characteristics and a detailed consideration of the costs/benefits involved.

Conclusions The contribution of segmentation to bank market planning has been presented and a two-stage conceptual approach to the segmentation of bank commercial markets proposed. In addition to the theoretical segmentation procedure, the requirements for practical implementation of the commercial market segmentation were spelt out. A detailed example of the method involved in performing a first stage segmentation with area coding was presented. The necessary activities and some limitations were explained. An overall view of the relative length of each activity was given and it was pointed out that structuring the geographical areas for the analysis and adapting the external municipal data were critical for the duration of the project.

The second stage segmentation was illustrated with additional survey data on perceived importance-performance of financial services. These data, collected

among present commercial clients of the bank, can be very helpful in differentiating the financial services in relation to different groups of business customers. The relationship between products and market segments allows the bank to choose a more distinctive and profitable position in the commercial financial market. The conditions required for a practical implementation of the second-stage segmentation approach are that economically attractive segments present distinct profiles on observable variables and correspond to the bank objectives, resources and priorities.

References Chéron, E.J. and Kleinschmidt, E.J. (1985), "A Review of

Industrial Market Segmentation Research and a Proposal for an Integrated Segmentation Framework", International Journal of Research in Marketing, Vol. 2, pp. 101-15.

Manilla, J.A. and James, J.C. (1977), "Importance-Performance Analysis", Journal of Marketing, Vol. 41 No. 1, January, pp. 77-9.

McTavish, R. and Perrien, J. (1988), Commercial Bank Marketing, The Institute of Canadian Bankers.

Watson, I. (1986), "Managing the Relationships with Corporate Customers", The International Journal of Bank Marketing, Vol. 4 No. 1, pp. 19-34.

Wind, Y. and Cardozo, R. (1974), "Industrial Market Segmentation", Industrial Marketing Management, Vol. 3, pp. 153-66.