securities and exchange board of india framework for consolidation … · page 1 of 32 securities...

TRANSCRIPT

Page 1 of 32

SECURITIES AND EXCHANGE BOARD OF INDIA Framework for consolidation and re-issuance of debt securities issued under the SEBI (Issue and Listing of Debt Securities) Regulations, 2008. 1. Objective:

1.1. This Board Memorandum proposes the framework for consolidation and re-

issuance of debt securities issued under the SEBI (Issue and Listing of Debt

Securities) Regulations, 2008.

2. Background: 2.1. An amendment was made to the SEBI (Issue and Listing of Debt Securities)

Regulations, 2008 (ILDS) in the year 2015, wherein regulation 20A was inserted,

to provide for an enabling clause for consolidation and re-issuance of debt

securities, in case of private placement.Only one issuer since then had

undertaken the process of consolidation and re-issuance.

2.2. The amount of private placement of corporate bonds has increased from Rs

1.18 lakh crores in the FY 2007-08 to Rs 6.4 lakh crores in the FY 2016-17.

Thus, private placements in corporate bonds have increased by approximately

442% since FY 2007-08 till FY 2016-17. Concurrently, the public issues in the

primary market have increased from nil figures in the FY 2007-08 to Rs 29,328

crores in the FY 2016-17 (As on February 28, 2017). Thus, the total primary

issuance in the corporate bond market has increased by approximately 467%

since FY 2007-08.

2.3. As per section 42 of the Companies Act, 2013 read with the Companies

(Prospectus and Allotment of Securities) Rules, 2014, if a debt issue is made to

more than 200 investors (excluding QIBs), the issuer has to follow the public

Page 2 of 32

issue route. To meet their funding requirements, some of the issuers take

recourse in issuing several issues of bonds through private placement in a single

month/quarter/year. The private placement mode of issuance of corporate bond

is substantially robust and favored for raising funds.

2.4. The trading of corporate bonds in the secondary marketing has increased from

Rs 1.48 lakh crores in the FY 2008-09 to Rs 14.7lakh crores in the FY 2016-17.

However, the average volume of trades per day continues to be very limited at

around Rs 4000 crores.

Thus, while the primary market for corporate bonds/debt securities has grown

since the year 2007, the liquidity in secondary market has not been high and

commensurate with the growth in the primary market.

2.5. There are several reasons for lack of liquidity in secondary market for corporate

bonds such as some investors’ preferto buy and hold the security instead of

trading it in the secondary market, prohibition on some investors for trading the

debt securities unless the rating of such debt securities falls two notches below

their initial credit rating. Further, the absence of a well-developed corporate bond

repo market, credit default swaps, interest rate futures, non-participation of the

institutional investors on the dedicated debt segment of the exchanges etc. can

also be some of the reasons for lack of liquidity in the secondary market.

2.6. Fragmentation of corporate bond issues in the primary market may also lead to

illiquidity in secondary market. The table below shows that each of the top

issuers of corporate bonds have more than 200 International Securities

Identification Numbers (ISINs), which has resulted in large number of

outstanding issuances at any point of time.

Serial No. Issuer Name No of ISINs

issued

Custody

Value (Rs

Page 3 of 32

Crores)

1. Issuer 1 447 6674.15

2. Issuer 2 331 15232.9

3. Issuer 3 305 19205.5

4. Issuer 4 281 68520.3

5. Issuer 5 251 27862.2

6. Issuer 6 222 13024.3

7. Issuer 7 222 34509.7

8. Issuer 8 216 19135.6

9. Issuer 9 212 96940.1

10. Issuer 10 203 14882.2

Source: NSDL Data as on November 30, 2016

The investor normally would trade in those corporate bonds of a particular

issuer, which have been freshly issued, thus rendering the old outstanding

issues of the same issuer illiquid. This in turn may affect the secondary market

liquidity in corporate bonds.Thus, one of the suggestions to increase liquidity in

the secondary market for corporate bonds, is the capping of such fragmented

issues vide consolidation and re-issuance. This may aid in generation of liquidity

through minimization in number of ISINs without curtailing the issuers’ ability to

raise funds.

3. The experience of consolidation and re-issuance in Government Securities market:

3.1. The Gandhi Committee Report ("Report of the Working Group on Enhancing

Liquidity in the Government Securities and Interest Rate Derivatives Markets")

had recommended consolidation of G-Sec as the objective of the working group

was to enhance secondary market liquidity in G-sec. The report had

recommended that the process should begin with the issuance of securities at

Page 4 of 32

various maturity points in conjunction with further steps like buyback and

switches.

3.2. Thus, in the Government Securities (G-Sec) market, the gradual extinguishing of

illiquid, infrequently traded and reissue of liquid bonds has helped in improving

liquidity. In the G-Sec market, a policy of passive consolidation through

reissuance was started in 1999 in order to improve fungibility among the

securities and to facilitate consolidation of debt.

3.3. In the case of G-secs, it is pertinent to note that the process of carrying out

consolidation and re-issuance is simpler as compared to the corporate bonds.

This is primarily due to the following:

a. Government is a single issuer in case of G-secs;

b. Fungible nature of G-secs;

c. No requirement for credit rating and

d. The borrowing calendar for the government is fixed at the beginning of the

financial year and the borrowings are made to finance the government

expenditure as well as to cover shortfalls (deficits) in its annual budget.

4. Consultation process followed:

4.1. The working group, on “Development of Corporate Bond market in India”, under

the chairmanship of Shri. H R Khan in its report, inter-alia, recommended that

the issuers coming out with frequent debt issues with the same tenor during a

quarter may club them under the same umbrella ISIN which in turn would

increase the float in the market, thus enhancing its liquidity. The committee also

recommended that these issuers may come out with a feasible maturity structure

wherein they can stagger the redemption amount across the year by amortizing

the repayments.

Page 5 of 32

4.2. The Corporate Bond and Securitization Advisory Committee (CoBoSAC) of

SEBI, in its meeting held on November 16, 2016 constituted a sub-committee

with respect to the mechanism for carrying out consolidation and re-issuance.

4.3. Taking into recommendations of the sub-committee of CoBoSAC, SEBI placed a

consultation paper (Annexure A) on the SEBI website on February 02, 2017 for

inviting public comments on the same.

4.4. On the consultation paper, a large number of comments were received that no

restrictions maybe be imposed on the number of ISINs especially on theNon

Banking Finance Companies and Housing Finance Companies as this would

curtail the flexibility of these issuers to raise funds.

5. Meeting held with the Non Banking Finance Companies, Housing Finance Companies and market participants: 5.1. In view of the comments received on the consultation paper, a meeting of SEBI

was called with Non Banking Finance Companies, Housing Finance Companies

and market participants such as exchanges, credit rating agencies etc. to

heartheir concerns and views on the proposals made in the paper.

5.2. Taking into consideration the consultation paper, the comments received on the

said paper and the feedback gathered from the aforesaid meeting, the following

proposals are recommended for the consideration of the Board.

6. Proposals to the Board with respect to the consultation paper:

6.1. Passive Consolidation : 6.1.1. Restriction on maximum number of ISINs in a year:

The consultation paper proposed the following:

Page 6 of 32

a) The issuers can have only one ISIN per quarter, i.e. total of 4

ISINs in a financial year or

b) The issuers can have only one ISIN in a period of two months,

i.e. total of 6 ISINs in a financial year.

In case the issuer raises funds by way of private placement of debt securities

in a particular quarter/ two month period, then for the whole of that

quarter/two month period, the issuer can have only one ISIN. Further, if the

issuer makes another issuance of debt security in the same quarter/two

month period, whose maturity is in the same quarter/same half year, as that

of the maturity of the existing debt instrument, then the issuer must

consolidate both the issuers under the same existing ISIN by adjusting the

difference in the issue price. The debt may be issued either at a discount or at

a premium. (An illustration for the same is there in the consultation paper

attached at Annexure A.)

6.1.1.1. Public comments:

Commentators have suggested that:

a) Restricting the number of ISINs to 4 or 6 a year and bundling of liabilities to a

single maturity date which would otherwise spread across the quarter, would

not only limit issuers’ ability to tap the market but would also result in liquidity

and asset-liability mismatches. Also, tapping the market for refinancing of

bunched up liabilities may potentially increase the cost of funds.

b) ISIN for plain vanilla annual coupon bearing bonds to be capped at 12 ISIN

per financial year whereas limits on ISIN issuance may exclude any

bonds/debentures (NCDs) which are used for raising regulatory capital (e.g.

Tier I, Tier II bonds), structured debt instruments like Zero Coupon bonds,

Page 7 of 32

NCDs with coupon compounding payable on maturity structure, NCDs with

only Put / NCDs with only Call, NCDs with Put/Call, NCD floaters, partly paid

NCDs structures, Sub-debt NCDs, Nifty linked NCDs, Dual rated NCDs,

Perpetual NCDs etc.

c) For Non-Banking Finance companies (NBFCs) and Housing Finance

Companies (HFCs), the maturity profile of debt issued is also governed by

Asset Liability Mismatch (ALM) requirements where debt is issued for various

maturities to match the loan assets of similar maturities. It would be difficult to

manage the ALM guidelines of their respective regulators i.e Reserve Bank of

India (RBI) and National Housing Bank (NHB), if consolidation and re-

issuance is implemented.

d) In respect of private placement of NCDs, the issue takes place depending on

market movement on a day-to-day basis. Therefore, if the company is

permitted to have only one ISIN which is maturing per quarter, it would impact

the issuer to a greater extent in the sense that they might have to fix

discounts and premium very frequently depending on the market situation, the

investor predominantly, mutual funds, may not be willing for adjusting to the

discounts/premium, as the case may be. Also, in case of extreme volatility,

the adjustment on discount/premium would be high making the issue

unattractive ab-initio for both issuer/investors.

e) Many corporates and NBFC’s issuance of debt securities on private issuance

basis gets underwritten with a clear understanding that issuer shall not come

out with a new issue immediately and such mechanisms are very effective to

support liquidity of earlier issues until stock of those get sold out. Subsequent

to this only, the issuer can plan its second issuance (especially the larger

corporates uses these routes). Thus, flexibility should be given to issuer and

investor in structuring the debt issue as per mutual agreement which would

support issuer’s business growth. Many investors especially banks like to hold

Page 8 of 32

the debt securities until maturity and hence secondary market transactions

are also affected by this.

f) Non-Banking Financial Companies (NBFCs) registered with Reserve Bank of

India (RBI) should be exempted from the proposal for restriction on maximum

number of ISINs in a year. The proposal may limit the potential investors and

investor base of NBFCs.

6.1.1.2. Recommendation & rationale :

a) It is proposed that maximum of 12 ISINsmaturing per financial year be

allowed.This may seem reasonable considering the fact that the corporate

bond market is in the growing stages and any stricter restriction of 4/6 ISINs

in a year may dent its growth. However, going forward, once the proposal is

implemented, the proposal for restriction on ISINs may be reviewed after

gauging its impact on the market.

b) There may not be any ISIN restriction on debt instruments which are used for

raising regulatory capital such as Tier I, Tier II bonds, bonds for affordable

housing etc. This is in view of the fact that many issuers such as

NBFCs/HFCs have to raisesuch capital for meeting regulatory requirements

or for priority sectors like affordable housing.

c) It may be noted that capital gains tax bonds can also be issued under section

54EC of the Income Tax Act 1961 on private placement basis and the series

is open for the full year for collection of funds on tap basis. The funds can

only be utilised after completion of allotment process, thus, this issuance

requires one ISIN each month, thereby consuming 12 ISIN in a year for this

product only. Hence, it is proposed that these bonds may also be excluded

from ISIN restriction.

Page 9 of 32

d) It is also proposed that for structured debt instruments of a particular category

(say bonds with call option or bonds with both call and put option) there may

be restriction of 5 ISINs per financial year.If these instruments are clubbed

with the plain vanilla NCDs for the purpose of ISIN restriction, then the

investor demand for them may be hampered. Hence, a separate bucket of 5

ISINs as stated above, may be provided for structured NCDs/ bonds.

e) It is also proposed that within the bucket of 12 ISINs as proposed in

paragraph 6.1.1.2 (a) above, the issuer can issue both secured and

unsecured NCDs/bonds and no separate category of ISINs may be provided

to them. Hence, for a financial year, the issuer can have only 12+5 (plain

vanilla NCDs and structured NCDs) i.e.a total of 17 ISINs maturing in a

financial year excluding the bonds issued in compliance with regulatory

requirements of sectoral regulators, other statutes such as the Income Tax

Act etc. as proposed in paragraph 6.1.1.2(b) and (c) above.

6.1.2. Staggered repayments of the redemption amount:

In order to resolve the issue of bunching of liabilities, the consultation paper

proposed that the issuer can as a one-time exercise make a choice of

having bullet maturity payment or in order to avoid bunching of liabilities, the

issuer can make equated quarterly payment or equated monthly payment of

the maturity proceeds within that financial year. This will enable the issuers

to stagger the redemption amount across the year by amortizing the

repayments. However, this should clearly be disclosed in the information

memorandum

6.1.2.1. Public comments:

a) Commentators have stated that there are genuine constraints on opting

for staggered repayments at maturity as majority of the investors prefer

Page 10 of 32

bullet maturity. Many large investors do not appreciate bunched

redemption of their investments as this may lead to increased

reinvestment risk on their investment portfolios.

b) Staggered repayments of the redemption amount may be offered but the

problem of bunching of liabilities would still remain as the restriction of

ISIN would lead to bunching of liabilities across 4 - 6 tenors which for large

issuers would create liquidity problem on maturity.

c) Such staggered redemptions will affect the pricing and will add to

complexity of the product. Further, some investors such as mutual funds,

provident funds (PFs) etc. may not like to have staggered redemption as

they may require the funds as bullet redemption as per their ALM position.

6.1.2.2. Recommendation & rationale :

a) It is proposed that in order to avoid bunching of liabilities, the issuers

may be given a choice of having bullet maturity payment or, the issues

can make equated quarterly payment or equated monthly payment of

the maturity proceeds, as may seem feasible to them. Moreover, this is

just an option and it is up to the issuer to finance its liabilities.

b) The argument regarding bunching of liabilities does not stand to

reason as it is felt that issuance of Commercial Papers could be

explored to fund any gaps.

6.2. Active consolidation 6.2.1. Proposed mechanics of Switching or Conversion and reduction on

number of ISIN’s issued:

Page 11 of 32

Switching or Conversion, would offer investors the opportunity to convert

their holdings of smaller debt securities into larger debt securities of same

issuer. A bond switching or conversion is a repurchase in advance of

maturity, where other debt securities would be supplied as payment. The

less-liquid debt securities would usually be paired with liquid benchmarks

that are of similar maturity and coupon rate. The switching rate/ratio may be

carried out by the issuer by exercising call option as given in information

memorandum either by Tender Offer Method or reverse auction

conversion/switching ratio. It is proposed that the issuers having large

number of outstanding issues and multiple ISINs, should resort to Switching

or Conversion to reduce the number of outstanding ISINs in a phased

manner. Such switching or conversion may be done through the Electronic

Book Platform (EBP) mechanism of exchanges.

6.2.1.1. Public comments:

a) Commentators have stated that investors have subscribed to existing

debentures based on their ALM requirements, scheme requirements,

regulatory constraints and tax implications. Reissuance of different

structures with different repayment schedules, maturity dates etc. may not

be feasible to investors in all instances. Further, compulsory reissuance of

ISIN may be unfavorable to the Issuers as they may be compelled to

reissue at unfavorable price, which may lead to severe financial losses.

Further, investors such as mutual funds and insurance companies would

have invested in a particular bond with a defined objective and may be

unwilling to surrender the bonds for a switch. They may even have to go

back to their ultimate investors for approvals. The Fixed Maturity Plan

(FMP) schemes of mutual funds that are dominant investors in corporate

bonds have predefined maturities and hence, fund managers of such

schemes are unlikely to take the repricing risk inherent in any

switching/conversion.

Page 12 of 32

b) Comments have also been received that many corporates are not allowed

as per articles and board resolution to carry out any buyback or

consolidation of debt securities. The FIPB may also restrict foreign owned

NBFCs from carrying out such buyback and consolidation as such activity

may not be construed to be part of the permissible activities. This will also

create legal problems where the original debt did not have any put / call

option or the Issuer has agreed not to buyback / repurchase issued NCDs

as a part of commercial negotiation as per Information Memorandum. The

consolidation would also lead to long tedious task of coordinating with

exchange, trustee, and investors and can lead to disputes where price

adjustment is not acceptable to either of the parties.

c) It has been stated that an existing ISIN may not be extinguished unless

each and every investor in that bond agrees to the conversion/switch

which is very unlikely. The commentators have suggested that old

outstanding securities may be allowed to mature in their current form and

the active consolidation may not be mandatory as the process would

require approval from respective investors which are regulated by various

authorities.

d) Comments have been received that switching/conversion would be difficult

in an era where bond rates are continuously moving downwards over the

years. New bonds issued at a discount may not suite all the investors.

Further, the issuers would face extreme difficulty since the outstanding

NCDs would have varying coupons and structures and involve a vast list

of investors.

e) Comments have also been received that reissuance of ISINs should not

be considered as fresh issuance of securities and should not attract stamp

duty. In case the Stamp authorities give a relaxation on reissuances of

Page 13 of 32

security, there should be a clear definition, of what constitutes a ‘reissued

security’ and ‘fresh issuance of security’ to prevent tax related ambiguities.

Moreover, this needs to be clarified upfront before formal notification of the

guidelines to avoid litigation and disputes with stamp authorities and also

whether it covers both unsecured as well as secured debenture issuance.

6.2.1.2. Recommendation & rationale : a) Considering the operational and regulatory difficulties that would be faced

by the issuers and investors in carrying out active consolidation, it is

suggested that active consolidation may be made recommendatory at

present which may be reviewed at a later stage. The old securities may be

allowed to naturally mature at their respective redemption dates and

wherever issuers are able to find opportunities to consolidate the earlier

ISIN, they could go ahead with the same. Such a move would also give

market some time to settle down and adjust to new guidelines and would

help in containing the volatility in rates.

7. Miscellaneous suggestions:

7.1. Comments have been received in the consultation paper on the aspect of

Alteration of Articles of Association (AOA) with respect to inclusion of clause on

consolidation and re-issuance. The commentators have suggested that the

Companies Act 2013 is silent on the provisions regarding consolidation andre-

issuance of debt securities and hence the onus is placed on the enabling

provision in Articles of Association (AOA) of the respective issuer. Currently, the

AOA of many issuers does not provide for consolidation and re-issuance of debt

securities. Any change to the AOA will require shareholders resolution, either

through an Annual General Meeting/Extraordinary General Meeting (AGM/EGM)

or Postal Ballot.

Page 14 of 32

7.2. In this regard, a suggestion has been received to save the issuer from the time

and cost in amending the articles of association with respect to providing for

enabling provision as per regulation 20A of the SEBI ILDS regulations. It has

been suggested that regulation 20A of ILDS regulations may be amended to

provide that unless any provision contrary to consolidation and re-issuance,

whether express or implied, is contained in the articles, or in the conditions of

issue, or in any contract entered into by the company, the company can carry

out such consolidation and re-issuance.

7.3. Recommendation and rationale:

a) As per the suggestion received, it is proposed that an amendment may be made

to regulation 20A of the SEBI ILDS regulations to provide that unless any

provision contrary to consolidation and re-issuance, whether express or implied,

is contained in the articles, or in the conditions of issue, or in any contract

entered into by the company, the company can carry out such consolidation and

re-issuance. This is in view of the fact that carrying out amendment of AoA may

be a long drawn process for the investors and hence to provide operational

flexibility, amendment may be made to the SEBI ILDS regulations.

b) It is also proposed that a time period of six months may be granted to the issuers

and market participants for making necessary structural changes, to implement

the provisions pertaining to consolidation and re-issuance.

8. Regulatory Impact: 8.1. The specification of framework for consolidation and re-issuance of debt

securities, would help in capping the fragmented issues of debt securities and

could be one of the possible solutions that would aid in generation of secondary

market liquidity in corporate bonds through minimal number of ISINs.

Page 15 of 32

8.2. A liquid corporate bond market would help in better price discovery and help in

the emergence of benchmark securities in the market.

9. Proposal: 9.1. The Board is requested to consider and approve the recommendations

mentioned above to make suitable amendments to the ILDS regulations and/or

issue necessary circulars.

9.2. The Board is also requested to authorize the Chairman to take consequential

and incidental steps to give effect to the decision of the Board.

Place:Mumbai Date: April 06, 2017

Ananta BaruaExecutive Director

Page 16 of 32

Annexure A CONSULTATION PAPER

Consolidation and re-issuance of debt securities issued under the SEBI (Issue and Listing of Debt Securities) Regulations, 2008

A. Market Structure of corporate bonds: The development of the primary market in corporate bond has been important part of

the reform process as it was essential for discovery of price through an efficient market

mechanism and providing for both listing and issuance of debt securities on private

placement and public issuance basis.

Table 1:Primary market data for private placement of corporate bonds:

Financial Year

No. of Public Issues

Amount Raised through Public Issue (Rs. Crore)

No. of Pvt. Placement

Amount Raised through Private Placement (Rs. Crore)

Total Amount Raised through Public Issue and Pvt. Placement (Rs. Crore)

2007-08 0 0 744 118,485 118,485

2008-09 1 1,500 1041 173,281 174,781

2009-10 3 2,500 1278 212,635 215,135

2010-11 10 9,451 1404 218,785 228,236

2011-12 20 35,611 1953 261,283 296,894

2012-13 20 16,982 2489 361,462 378,444

2013-14 35 42,383 1924 276,054 318,437

2014-15 25 9,713 2611 4,04,136 4,13,849

2015-16 20 33,811 2975 4,58,073 4,91,884

Page 17 of 32

2016-17# 14 29213 2662 478,974 5,08,187

# As on January 2017; private

placement data is up to

December 2016

Table 1 shows that the amount of private placement of corporate bonds has increased

from Rs 1.18 trillion in the FY 2007-08 to Rs 4.78 trillion in the FY 2016-17. Thus, it can

be seen that the private placement issues have increased by 176.41 % since FY 2007-

08 till date.

Further, the public issues in the primary market have increased from nil figures in the

FY 2007-08 to Rs 29,213 crores. The total primary issuance in the corporate bond

market has increased by 328.9% since FY 2007-08.

As per section 42 of the Companies Act, 2013 read with the Companies (Prospectus

and Allotment of Securities) Rules, 2014, if a bond issue is made to more than 200

investors (excluding QIBs), the issuer has to follow the public issue route. To meet their

funding requirements, some of the issuers take recourse in issuing several issues of

bonds in a single month/quarter/year. This evidences that the private placement mode

of issuance of corporate bond is substantially robust and favored for raising funds.

While the primary market for corporate bonds/debt securities has grown since the year

2007, the liquidity in secondary market has not been high and commensurate with the

growth in the primary market.

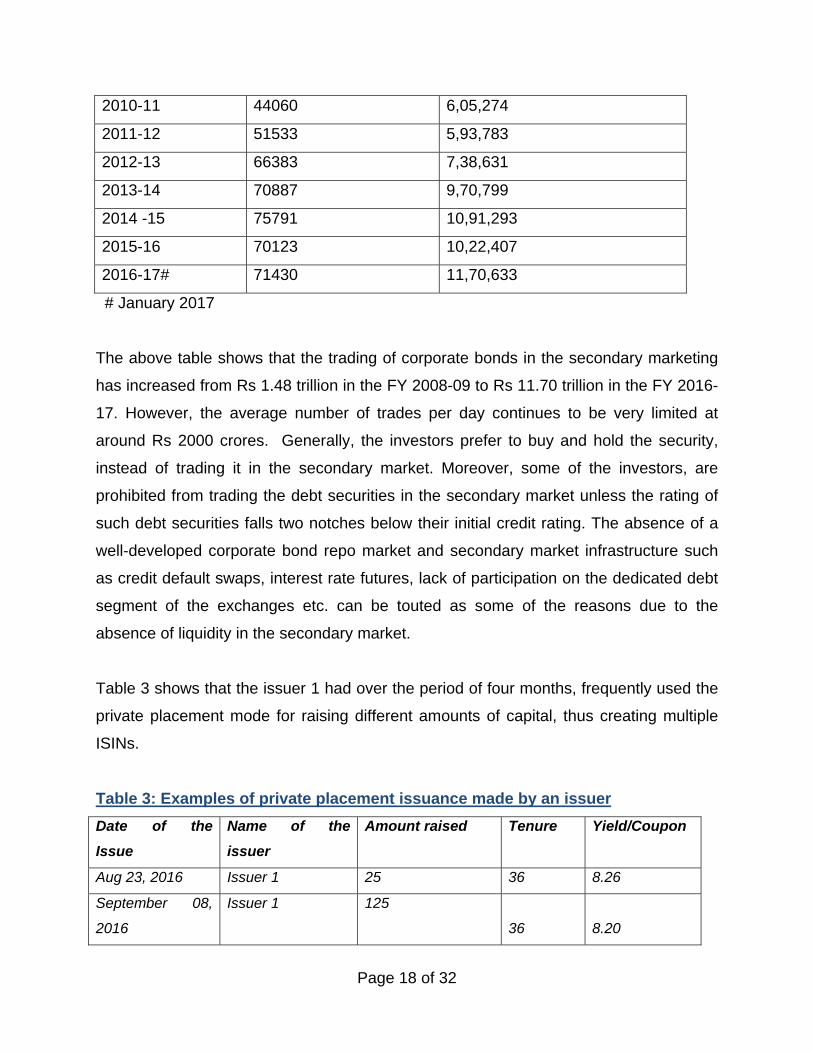

Table 2: Details of Trades in Secondary Market in Listed Corporate Bonds:

Secondary Market Trades in Corporate Bonds

Month/Year Total no. of trades Total Amount (Rs Crores)

2008-09 22730 1,48,166

2009-10 38230 4,01,198

Page 18 of 32

2010-11 44060 6,05,274

2011-12 51533 5,93,783

2012-13 66383 7,38,631

2013-14 70887 9,70,799

2014 -15 75791 10,91,293

2015-16 70123 10,22,407

2016-17# 71430 11,70,633

# January 2017

The above table shows that the trading of corporate bonds in the secondary marketing

has increased from Rs 1.48 trillion in the FY 2008-09 to Rs 11.70 trillion in the FY 2016-

17. However, the average number of trades per day continues to be very limited at

around Rs 2000 crores. Generally, the investors prefer to buy and hold the security,

instead of trading it in the secondary market. Moreover, some of the investors, are

prohibited from trading the debt securities in the secondary market unless the rating of

such debt securities falls two notches below their initial credit rating. The absence of a

well-developed corporate bond repo market and secondary market infrastructure such

as credit default swaps, interest rate futures, lack of participation on the dedicated debt

segment of the exchanges etc. can be touted as some of the reasons due to the

absence of liquidity in the secondary market.

Table 3 shows that the issuer 1 had over the period of four months, frequently used the

private placement mode for raising different amounts of capital, thus creating multiple

ISINs.

Table 3: Examples of private placement issuance made by an issuer Date of the Issue

Name of the issuer

Amount raised Tenure Yield/Coupon

Aug 23, 2016 Issuer 1 25 36 8.26

September 08,

2016

Issuer 1 125 36 8.20

Page 19 of 32

September 08,

2016

Issuer 1 25 39 8.20

September 08,

2016

Issuer 1 25 18 8.00

September 08,

2016

Issuer 1 25 39 8.18

November 22,

2016

Issuer 1

100 36 7.77

November 22,

2016

Issuer 1

200 24 7.76

November 22,

2016

Issuer 1

150 18 7.66

Total 675

Table 4 below shows that each of the top issuers of corporate bonds have more than

200 ISINs, which has resulted in large number of outstanding issuances at any point of

time.

Table 4: Top Issuers of corporate bonds with their total ISINs: Serial No. Issuer Name No of ISINs issued Custody Value (Rs Crores)

1. Issuer 1 447 6674.15

2. Issuer 2 331 15232.9

3. Issuer 3 305 19205.5

4. Issuer 4 281 68520.3

5. Issuer 5 251 27862.2

6. Issuer 6 222 13024.3

7. Issuer 7 222 34509.7

8. Issuer 8 216 19135.6

9. Issuer 9 212 96940.1

10. Issuer 10 203 14882.2

Source: NSDL Data as on November 30, 2016

Page 20 of 32

The trader would trade in those corporate bonds of a particular issuer, which have been

freshly issued, thus rendering the old outstanding issues of that same issuer illiquid.

This in turn affects the secondary market liquidity in corporate bonds.

Thus, one of the suggestions is the capping of such fragmented issues vide

consolidation and re-issuance. It is envisaged that such consolidation and re-issuance

could be one of the possible solutions that would aid in generation of liquidity through

minimal number of ISINs. It is also felt that such fragmented issues can be avoided, if

the maximum number of investors (which are two hundred at present) to whom private

placement are made are increased to a higher number under the Companies Act, 2013.

B. Government Securities Market In the Government Securities (G-Sec) market, the gradual extinguishing of illiquid,

infrequently traded and reissue of liquid bonds has helped in improving liquidity. In the

G-Sec market, a policy of passive consolidation through reissuance was started in 1999

in order to improve fungibility among the securities and to facilitate consolidation of

debt.

In the case of G-secs, it is pertinent to note that the process of carrying out

consolidation and re-issuance is simpler as compared to the corporate bonds. Some of

the reasons for the same being as under:

e. Government being one single issuer in case of G-secs; f. Fungible nature of G-secs; g. No requirement for credit rating and h. The borrowing calendar for the government is fixed at the beginning of the

financial year and the borrowings are made to finance the government

expenditure as well as to cover shortfalls (deficits) in its annual budget.

The Gandhi Committee Report ("Report of the Working Group on Enhancing Liquidity in

the Government Securities and Interest Rate Derivatives Markets") had recommended

consolidation of G-Sec. Considering the objective of the working group i.e. to enhance

Page 21 of 32

secondary market liquidity, the group felt that there was a need to undertake

consolidation of the G-Sec outstanding for which a framework needs to be prepared for

the next 3-4 years. The process should begin with the issuance of securities at various

maturity points in conjunction with further steps like buyback and switches. The

framework should outline the various objectives proposed to be achieved through the

exercise, various constraints that need to be taken into account in the process and the

buyback program should be long drawn.

The process should lead to the consolidation of the GoI’s market borrowings to a fewer

securities and fresh borrowings through a limited number of securities thereby

increasing the outstanding amount of each security, which would have a direct bearing

on the secondary market trade volumes. The consolidation in the G-sec market has

greatly improved market liquidity and helped the emergence of benchmark securities in

the market

C. Background for consolidation and re-issuance of debt securities:

Section 121 of the erstwhile Companies Act 1956 had provisions of consolidation and

re-issuance. However, the recently notified Companies Act 2013 is silent regarding the

company's power to reissue their bonds. In this regard, the Ministry of Corporate Affairs

(MCA) has clarified that since Companies Act 2013 is silent on the issue, it may be

assumed that such reissuance is possible if there is enabling provision in this behalf in

the articles of the company. In view of the clarification provided by MCA, SEBI provided

an enabling framework for consolidation and re-issuance. However it may be noted that

only one issuer has since come for taking advantage of this provision.

As stated above, an amendment was made to the SEBI (Issue and Listing of Debt

Securities) Regulations, 2008 (ILDS) in the year 2015, wherein regulation 20A was

inserted, to provide for consolidation and re-issuance of debt securities. The regulation

reads as under:

Page 22 of 32

An issuer may carry out consolidation and re-issuance of its debt securities, subject to

the fulfillment of the following conditions:

a) there is such an enabling provision in its articles under which it has been

incorporated;

b) the issue is through private placement;

c) the issuer has obtained fresh credit rating for each re-issuance from at least one

credit rating agency registered with the Board and is disclosed;

d) such ratings shall be revalidated on a periodic basis and the change, if any, shall

be disclosed;

e) Appropriate disclosures are made with regard to consolidation and re-issuance in

the Term Sheet.

The working group, on Development of Corporate Bond market in India, under the

chairmanship of Shri. H R Khan in its report has made the following observations in

respect of consolidation and re-issuance:

a. One of the reasons for the lack of trading volume is non-availability of sufficient

floating stock for each International Securities Identification Number (ISIN) as

corporates have preferred fresh issuance rather than going for reissuance of

bonds. Each new issuance from the same issuer receives a separate ISIN;

hence older bonds in the same maturity become illiquid.

b. To augment market liquidity, it is necessary that corporates are encouraged to

re-issue existing bonds under the same ISIN code.

c. A major argument against common ISINs is the bunching of liabilities on the

same date which can lead to asset-liability mismatch; however, this can be

resolved by spreading out the redemption amount across the year through

amortizing the payments.

Page 23 of 32

d. SEBI has enabled consolidation and re-issuance with a view to reducing

fragmentation in corporate bond market. Though SEBI has recently allowed

reissuances by the corporates, there has not been any reissue of bonds by any

corporate due to problems related to bunching of liabilities and stamp duty.

e. Corporates may be permitted to issue bonds under the same ISIN with a

flexibility in terms of timing for raising the funds as well as structuring of the

redemption requirements.

In view of the aforesaid observations, the H R khan working group, inter-alia,

recommended that the issuers coming out with frequent debt issues with the same tenor

during a quarter may club them under the same umbrella ISIN which in turn would

increase the float in the market, thus enhancing its liquidity. These issuers may come

out with a feasible maturity structure wherein they can stagger the redemption amount

across the year by amortizing the repayments.

The Corporate Bond and Securitization Advisory Committee (CoBoSAC) of SEBI, in its

meeting held on November 16, 2016, inter-alia, deliberate on the ways to increase

secondary market liquidity in the corporate bonds. It was discussed that a sub-

committee may be formed by SEBI to explore the mechanism for implementation of the

consolidation and re-issuance in the corporate bonds.

The sub-committee was constituted and while preparing this consultation paper, inputs have been taken from the market participants

D. Structural issues faced in the consolidation for corporate bonds: While carrying out deliberations on laying down an implementable and feasible

operational framework for consolidation and re-issuance for corporate bonds, the

following legal/structural issues have been noted by SEBI:

i. Stamp Duty:

Page 24 of 32

It is understood that re-issuance is not legally recognized and is considered a fresh

issue of securities. As a fallout of this, re-issuing securities attracts stamp duty thereby

making the process cost ineffective. However, as no fresh securities are actually being

issued, there should not be any incidence of stamp duty on the re-issued securities. In

this regard, the H R Khan committee had already made the recommendation that the re-

issuances may not be treated as fresh issuance for the purpose of stamp duty. The

matter is under deliberation.

ii. Bunching of liabilities:

In case of consolidation and reissuance of debentures, the maturities of debentures

issued under consolidation will fall on same day which shall create liquidity problem and

bunching of liabilities for borrowers. The same shall also have impact on their liquidity

and rating.

iii. Issuances are triggered as per the demands of the investors:

The issue amount is not predetermined rather the issuers bring out the corporate bond

issuances in the market in accordance with the investor appetite. This is elaborated by

the fact that the mutual funds would demand only for those papers whose maturities are

in alignment with the tenure of their debt funds or those suiting their requirements.

Consolidation and reissue would reduce the demand/appetite of the investors and also

increase the coupon rate because of lower demand.

iv. Re-issuance at a discount or premium

The coupon rate on bonds is a dynamic factor and mostly market driven, hence the

interest rate frozen at the time of issue of ISIN may change and in such case

subsequent issue of bonds

Page 25 of 32

have to be made at discount or premium depending on market conditions. This kind of

arrangement may not be acceptable by to certain categories of investors like mutual

fund, provident fund etc. This will also lead to accounting and taxation issues.

E. Objective of the consultation paper

In spite of the technical issues mentioned above, in carrying out consolidation and re-

issuance, it is felt that such a measure would help in building secondary market liquidity

in corporate bonds.

This consultation paper has been prepared with the objective of seeking public

comments/views on the proposals mentioned in this paper. Apart from the proposals

mentioned here, other suggestions/ inputs, to develop the secondary market for

corporate bonds, are also invited from the public at large.

i. Passive Consolidation :

a. Restriction on the maximum number of ISINs for private placement of debt

securities;

b. Staggered repayments of the redemption amount on the debt securities;

and

ii. Active consolidation:

a. Switching or conversion of less liquid debt securities into larger, more

liquid benchmark bond issues. This can be carried out via following two

methods:

i. Tender offer method

ii. Reverse Auction Conversion/Switching Ratio

F. Proposals:

1. Passive Consolidation :

Page 26 of 32

1.1. Restriction on maximum number of ISINs in a year: Option A: One ISIN per quarter:

It is proposed that the issuers can have only ISIN per quarter, i.e total of 4 ISINs in a

financial year. In case the issuer raises funds by way of private placement of debt

securities in a particular quarter, then for the whole of that quarter, the issuer can have

only one ISIN. Further, if the issuer makes another issuance of debt security in the

same quarter, whose maturity is in the same quarter as that of the maturity of the

existing debt instrument, then the issuer must consolidate both the issuers under the

same existing ISIN by adjusting the difference in the issue price. The debt may be

issued either at a discount or at a premium.

If the issuer makes another issuance of debt security in the same quarter, whose

maturity does not fall in the same quarter as that of the maturity of the existing debt

instrument, then the issuer has the flexibility to obtain a new ISINs for that particular

issuance. However, the total number of ISINs in a financial year shall not exceed 4 i.e. 1

ISIN per quarter.

Or Option B:One ISIN in a period of two months:

It is proposed that the issuers can have only ISIN in a period of two months, i.e total of 6

ISINs in a financial year. In case the issuer raises funds by way of private placement of

debt securities in a two month period, then for the whole of that two months, the issuer

can have only one ISIN. Further, if the issuer makes another issuance of debt security

in the same period of two months, whose maturity is in the same half year as that of the

maturity of the existing debt instrument, then the issuer must consolidate both the

issues under the same existing ISIN by adjusting the difference in the issue price. The

debt may be issued either at a discount or at a premium.

If the issuer makes another issuance of debt security in the same period of two months,

whose maturity does not fall in the same half year as that of the maturity of the existing

Page 27 of 32

debt instrument, then the issuer has the flexibility to obtain a new ISINs for that

particular issuance. However, the total number of ISINs in a year shall not exceed 6.

1.2. Staggered repayments of the redemption amount

It has been pointed out that if the restriction as above are implemented, it may lead to a

situation of liquidity mismatch and bunching of liabilities for the issuer. In order to

resolve this issue, it is proposed that the issuer can as a onetime exercise make a

choice of having bullet maturity payment or in order to avoid bunching of liabilities, the

issuer can make equated quarterly payment or equated monthly payment of the

maturity proceeds within that financial year. This will enable the issuers to stagger the

redemption amount across the year by amortizing the repayments. However this should

clearly be disclosed in the information memorandum

1.3. Illustration to show as to how the number of ISINs will be capped for option A under proposal 1.1 above:

Assuming first option i.e. wherein only one ISIN is allowed per quarter, then say an

issuer issues 14 debt securities in the financial year 2017-18 (of maturity profile 1 to 5

years) as under :

Serial number Date of issue Date of maturity

Total number of months and quarter in which maturity is due

1 01/04/2017 01/04/2019 24 months (April-June 2019)

2 23/04/2017 23/04/2020 36 months (April-June 2020)

3 05/05/2017 05/04/2021 47 months (April-June 2021)

4 15/06/2017 15/06/2019 24 months (April-June 2019)

5 25/06/2017 25/06/2020 36 months (April-June 2020)

6 15/07/2017 15/09/2022 62 months (July-September 2022)

7 26/07/2017 26/04/2021 45 months (April-June 2021)

8 10/08/2017 10/08/2022 60 months (July-September 2022)

9 20/08/2017 20/08/2022 60 months (July-September 2022)

Page 28 of 32

Serial number Date of issue Date of maturity

Total number of months and quarter in which maturity is due

10 18/10/2017 18/12/2020 38 months (October-December 2020)

11 15/11/2017 15/11/2022 60 months (October-December 2022)

12 20/12/2017 20/12/2022 60 months (October-December 2022)

13 10/01/2018 10/01/2020 24 months (January-March 2020)

14 25/01/2018 25/01/2021 36 months (January-March 2021)

The allotment of ISINs for the aforesaid schedule of issuance shall be as under:

Maturity date of issuance

ISIN for year ISIN for quarter Nos of ISINs

2018-19 April-June 1

July-September 1

October- December 1

January- March 1

01/04/2019 and

15/06/2019

2019-20 April-June 1

July-September 1

October- December 1

10/01/2020 January- March 1

23/04/2020,

25/ 06/2020

2020-21 April-June 1

July-September 1

18/12/2020 October- December 1

25/01/2021 January- March 1

05/04/2021,

26/04/2021

2021-22 April-June 1

July-September 1

October- December 1

January- March 1

2022-23 April-June 1

Page 29 of 32

10/08/2022,

20/08/2022

15/09/2022,

July-September 1

15/11/2022,

20/12/2022

October- December 1

January- March 1

From the aforesaid table, following can be deduced:

For the Financial year 2018-19, as there are no securities due for maturity, the issuer

can take 1 ISIN each in every quarter.

For the financial year 2019-20, it can be seen that for the quarter ended June 2020,

there are two securities due for redemption. Hence, in such a case the issuer, for the

security issue on 01/04/2019, the issuer would take a new ISIN. However, for the

subsequent security issued on 15/06/2019, the issuer cannot take a new ISIN and will

necessarily have to consolidate it with the ISIN of the security issued on 01/04/2019 as

both these securities are due for redemption in the same quarter. Further, for the

quarter ended January-March 2020, the issuer can again take a new ISIN.

Similarly for the financial year 2022-23, it can be seen that for the quarter ended

September 2023, there are three securities due for redemption. Hence, in such a

scenario, for the security issued on 10/08/2022, the issuer would take a new ISIN. For

the subsequent security issued on 20/08/2022 and 15/09/2022 the issuer cannot take a

new ISIN and will necessarily have to consolidate it with the ISIN of the security issued

on10/08/2022 as both these securities are due for redemption in the same quarter.

In both the above scenarios, the issuer has to flexibility to make staggered re-payments

on maturity of the instruments, instead of bullet repayment.

2. Active Consolidation: Switches-Conversion

Switching or Conversion, would offer investors the opportunity to convert their holdings

of smaller debt securities into larger debt securities of same issuer.A switching or

Page 30 of 32

conversion can be viewed as a repurchase of the debt securities in advance of maturity

where payment for these repurchases would be in terms of newly issued more-liquid

benchmark securities. Thus, a bond switching or conversion is a repurchase in advance

of maturity, where other debt securities would be supplied as payment. The less-liquid

debt securities would usually be paired with liquid benchmarks that are of similar

maturity and coupon rate.

Here, it may be pointed out that switching or conversion rate or ratio mostly depend on

the secondary market prices at the time of the announcement of a conversion.

However, due to lack of liquidity here the pricing may be a concern. Hence the following

is proposed for carrying out the switching or conversion.

2.1. Proposed mechanics of Switching or Conversion

2.1.1. Conversion/Switching Rate/Ratio

The switching rate/ratio may be carried out by the issuer by exercising call option as

given in information memorandum in the following manner:

2.1.1.1. Tender offer method

A tender offer is a fixed price offer, i.e. the issuer will fix a particular price for the

maximum number of debt securities it is willing to purchase and sends a letter of

offer to all the holders of debt securities. The issuer will also fix an outer time limit for

accepting the offer. The issuer may determine the rate which may be at a premium

or discount. However, more likely, the issuer may fix the rate at a discount in order to

encourage holders to switch their debt securities.

2.1.1.2. Reverse Auction Conversion/Switching Ratio

Page 31 of 32

Reverse Auction Conversion/Switching is where the market participants would

submit various competitive rates of conversion as well as the amount they wish to

convert to the issuer/arranger and is essentially an auction. The mechanics that

underlie the reverse auction conversion is same as standard conventional auction

where bidders are bidding to purchase debt securities and are offering debt

securities as payment for their purchase in lieu of cash. Thus offers are simply price

or yield ratios. This can further be done by multiple-price auction i.e. French Auction

or single-price auction method based on discretion of the issuer.

Further, the issuer, at the beginning of the financial year, shall specify the pre-

notified amount for which he is willing to carry out the switch operations. Such

switching or conversion may be done through the Electronic Book Platform (EBP)

mechanism.

2.1.2. Reduction on number of ISIN’s issued

It is proposed that the issuers having large number of outstanding issues and multiple

ISINs, should resort to Switching or Conversion to reduce the number of outstanding

ISINs in a phased manner.

Assuming an issuer has 250 outstanding ISINs as on March 31, 2017 with maturities

over say next 5 years. Issuer should switch all existing ISINs in such a manner so as to

restrict the number of ISINs to maximum 12 ISINs in a financial year. This would be in

addition to limit proposed above i.e. maximum number of ISINs for fresh issuances. For

example, say some of the ISINs in the said 250 ISINs may be due for maturity in the FY

2018, FY 2019, FY 2020, FY 2021, FY 2022. Then these ISINs should be switched in

such a manner to reduce the number of ISINs to 60 i.e. 12 ISINs outstanding in each of

FY 2018, FY 2019, FY 2020, FY 2021, FY 2022.

G. Public Comments:

Page 32 of 32

In the light of the above, public comments are invited on the consultation paper.

Comments may be forwarded by email to [email protected] or may be sent by post to

the following address latest by February 28, 2017 to:

Richa Agarwal Deputy General Manager Investment Management Department, Division of Funds I Securities and Exchange Board of India SEBI Bhavan C4-A, G Block Bandra Kurla Complex Mumbai - 400 051 Comments should be given in the following format:

Issued on February 02, 2017

Name of entity/ person/ intermediary: _______________________

S. No. Pertains to Point No. Proposed/

suggested

changes

Rationale