sector review deep dig on mining capex & capital allocation

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

3 March 2017 Global

Equity Research Diversified Metals & Mining

Global Mining 2020 Capex The Ideas Engine series showcases Credit Suisse’s unique

insights and investment ideas.

Research Analysts

Europe

Liam Fitzpatrick

44 20 7883 8350

James Gurry

44 20 7883 7083

Michael Shillaker

34 91 791 58 78

Conor Rowley

44 20 7883 9156

Australia

Paul McTaggart

61 2 8205 4698

Christian Prendiville

612 8205 4012

Canada

Ralph M. Profiti, CFA

416 352 4563

Yan Truong, CFA

416 352 4584

Latin America

Ivano Westin

55 11 3701 6318

Renan Criscio

55 11 3701 6210

Specialist Sales: James Brady 44 20 7888 4267 [email protected]

Please contact your Sales person to access the supplemental analysis behind this report

SECTOR REVIEW KEY CONCLUSIONS

Deep dig on mining capex & capital allocation Figure 1: Diversified miners' capex progression 2016-20E ($m)

Companies used: BHP Billiton, Rio Tinto, Anglo American, Glencore, Vale and Teck Resources Source: Company data, Credit Suisse estimates

In this Ideas Engine, we take a global approach to future capital

allocation and capex: Through our in-depth analysis of the asset bases and

investment profiles of the six largest diversified miners, we assess longer-term

capex requirements and find material differences between the companies, with

important implications for future cash flows and shareholder returns.

■ Capex on the rise: A rebounding capex cycle is a sign of a healthier industry and only becomes a problem after several years of elevated returns (well above what is currently priced in), when more marginal projects are pursued. However, with growth capex having hit trough levels in 2016, volumes will begin to decline post 2020 without fresh investment.

■ 2020+ normalised capex: An area lacking in competitor analysis is longer-

term reliable capex estimates. Using our capex projection model, based on a detailed analysis of annual depletion rates and future project costs, we estimate that industry capex could rise by 50-60% compared with 2016. Under our 2020+ capex estimates and assuming spot iron ore and coal prices moderate (iron ore to $55-60/tonne), sector FCF yields would fall from over 15% to 8-10%. However, we think material increases in capex are unlikely until 2019/20.

■ Not all companies are equal: Companies where we see the lowest level of potential capex increases on a three- to five-year view look to be the best positioned. Vale is in the strongest position with declining capex, followed by Rio and Teck with limited increases expected by 2020. We see the greatest risk of capex increases at BHP and Anglo American. Glencore's capex could also rise significantly, but latent capacity is an advantage.

■ Stock calls: Our preferred names are Rio, Glencore and Teck, all Outperform-rated. We have raised our 2017/18 iron ore price forecasts from $55/53 per tonne to $78/$58 per tonne and sit materially ahead of consensus. Linked to our view of contained capex for the next two years, we make significant upgrades to our two-year cash return assumptions.

22,144

33,380

2,338

8,898

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2016 Capex increase to maintainstable production

Capex to grow at 2% pa 2020E

3 March 2017

Global Mining 2020 Capex 2

Focus charts

Figure 2: Diversified miners' capex outlook

Figure 3: 2020+ capex outlook (% change vs 2017

guidance)

Source: Company data, Credit Suisse estimates, CY basis, Companies used: BHP, RIO, AAL, GLEN, Vale and Teck

Source: Credit Suisse estimates

Figure 4: Illustrative FCF Bridge 2017E spot to

2020E normalized Figure 5: CS capex estimates vs consensus

Source: Credit Suisse estimates, CY basis Note: Above charts based on BHP,RIO, AAL, GLEN. Spot prices assumed for 2020 except for iron ore ($60), thermal coal ($70), coking coal ($140)

Source: Company data, Credit Suisse estimates, I/B/E/S Consensus,

Figure 6: Copper industry expansionary capital ($/t

annual production) Figure 7: Large cap growth capex 2005-16

Source: Wood Mackenzie, Credit Suisse research Source: Company data, CY basis

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2016 2017E 2020E

2020E normalized capex to offset

production decline

2020E normalized capex to grow production by

2%pa

Potential ~52% capex

2016/17 guided capex increase

of 5%

-20%

0%

20%

40%

60%

80%

100%

AAL BHP GLEN Teck VALE RIO

2020+ capex to keep volumes stable 2020 capex to grow at 2% pa

Capex Increase Risk

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Spot 2017EFCF

Change incapex 2020 vs

2017

Highervolumes

Iron ore $60/tand lower coal

prices

2020ENormalised

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

20

15

20

16

20

17

E

20

18

E

20

19

E

20

20

E

Total Capex CS estimates IBES Consensus Capex

2020E normalized capex to grow production by 2%pa

0

500

1,000

1,500

2,000

2,500

2000 2002 2004 2006 2008 2010 2012 2014 2016

-

10,000

20,000

30,000

40,000

50,000

60,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

BLT RIO GLEN AAL VALE TECK

3 March 2017

Global Mining 2020 Capex 3

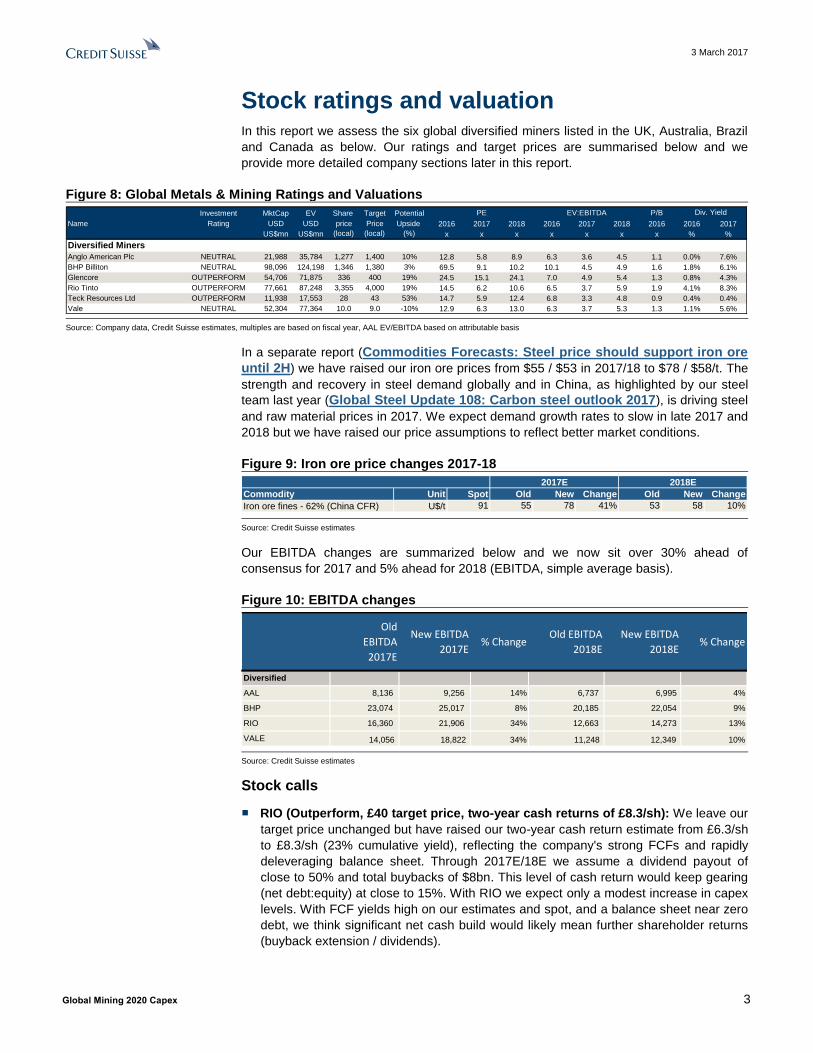

Stock ratings and valuation In this report we assess the six global diversified miners listed in the UK, Australia, Brazil

and Canada as below. Our ratings and target prices are summarised below and we

provide more detailed company sections later in this report.

Figure 8: Global Metals & Mining Ratings and Valuations

Source: Company data, Credit Suisse estimates, multiples are based on fiscal year, AAL EV/EBITDA based on attributable basis

In a separate report (Commodities Forecasts: Steel price should support iron ore

until 2H) we have raised our iron ore prices from $55 / $53 in 2017/18 to $78 / $58/t. The

strength and recovery in steel demand globally and in China, as highlighted by our steel

team last year (Global Steel Update 108: Carbon steel outlook 2017), is driving steel

and raw material prices in 2017. We expect demand growth rates to slow in late 2017 and

2018 but we have raised our price assumptions to reflect better market conditions.

Figure 9: Iron ore price changes 2017-18

Source: Credit Suisse estimates

Our EBITDA changes are summarized below and we now sit over 30% ahead of

consensus for 2017 and 5% ahead for 2018 (EBITDA, simple average basis).

Figure 10: EBITDA changes

Source: Credit Suisse estimates

Stock calls

■ RIO (Outperform, £40 target price, two-year cash returns of £8.3/sh): We leave our

target price unchanged but have raised our two-year cash return estimate from £6.3/sh

to £8.3/sh (23% cumulative yield), reflecting the company's strong FCFs and rapidly

deleveraging balance sheet. Through 2017E/18E we assume a dividend payout of

close to 50% and total buybacks of $8bn. This level of cash return would keep gearing

(net debt:equity) at close to 15%. With RIO we expect only a modest increase in capex

levels. With FCF yields high on our estimates and spot, and a balance sheet near zero

debt, we think significant net cash build would likely mean further shareholder returns

(buyback extension / dividends).

Investment MktCap EV Share Target Potential PE EV:EBITDA P/B

Name Rating USD USD price Price Upside 2016 2017 2018 2016 2017 2018 2016 2016 2017

US$mn US$mn (local) (local) (%) x x x x x x x % %

Diversified Miners

Anglo American Plc NEUTRAL 21,988 35,784 1,277 1,400 10% 12.8 5.8 8.9 6.3 3.6 4.5 1.1 0.0% 7.6%

BHP Billiton NEUTRAL 98,096 124,198 1,346 1,380 3% 69.5 9.1 10.2 10.1 4.5 4.9 1.6 1.8% 6.1%

Glencore OUTPERFORM 54,706 71,875 336 400 19% 24.5 15.1 24.1 7.0 4.9 5.4 1.3 0.8% 4.3%

Rio Tinto OUTPERFORM 77,661 87,248 3,355 4,000 19% 14.5 6.2 10.6 6.5 3.7 5.9 1.9 4.1% 8.3%

Teck Resources Ltd OUTPERFORM 11,938 17,553 28 43 53% 14.7 5.9 12.4 6.8 3.3 4.8 0.9 0.4% 0.4%

Vale NEUTRAL 52,304 77,364 10.0 9.0 -10% 12.9 6.3 13.0 6.3 3.7 5.3 1.3 1.1% 5.6%

Div. Yield

2017E 2018E Long-

Commodity Unit Spot Old New Change Old New Change

Iron ore fines - 62% (China CFR) U$/t 91 55 78 41% 53 58 10%

Old

EBITDA

2017E

New EBITDA

2017E% Change

Old EBITDA

2018E

New EBITDA

2018E% Change

Diversified

AAL 8,136 9,256 14% 6,737 6,995 4%

BHP 23,074 25,017 8% 20,185 22,054 9%

RIO 16,360 21,906 34% 12,663 14,273 13%

VALE 14,056 18,822 34% 11,248 12,349 10%

3 March 2017

Global Mining 2020 Capex 4

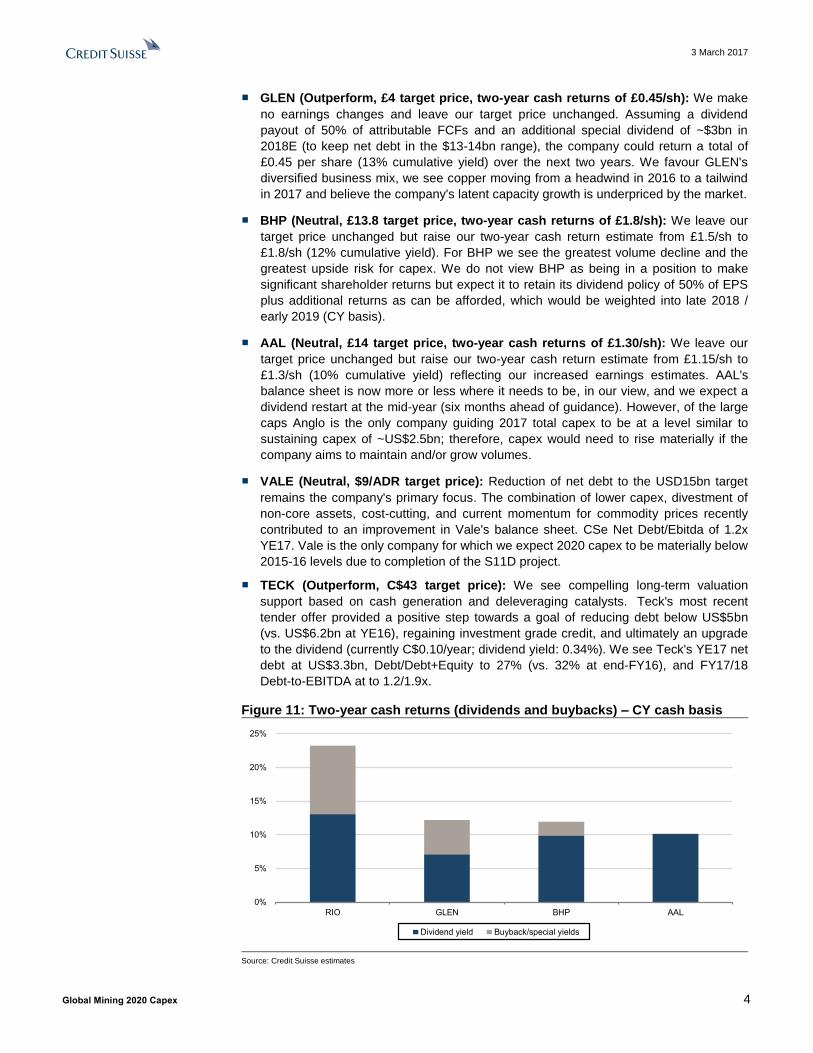

■ GLEN (Outperform, £4 target price, two-year cash returns of £0.45/sh): We make

no earnings changes and leave our target price unchanged. Assuming a dividend

payout of 50% of attributable FCFs and an additional special dividend of ~$3bn in

2018E (to keep net debt in the $13-14bn range), the company could return a total of

£0.45 per share (13% cumulative yield) over the next two years. We favour GLEN's

diversified business mix, we see copper moving from a headwind in 2016 to a tailwind

in 2017 and believe the company's latent capacity growth is underpriced by the market.

■ BHP (Neutral, £13.8 target price, two-year cash returns of £1.8/sh): We leave our

target price unchanged but raise our two-year cash return estimate from £1.5/sh to

£1.8/sh (12% cumulative yield). For BHP we see the greatest volume decline and the

greatest upside risk for capex. We do not view BHP as being in a position to make

significant shareholder returns but expect it to retain its dividend policy of 50% of EPS

plus additional returns as can be afforded, which would be weighted into late 2018 /

early 2019 (CY basis).

■ AAL (Neutral, £14 target price, two-year cash returns of £1.30/sh): We leave our

target price unchanged but raise our two-year cash return estimate from £1.15/sh to

£1.3/sh (10% cumulative yield) reflecting our increased earnings estimates. AAL's

balance sheet is now more or less where it needs to be, in our view, and we expect a

dividend restart at the mid-year (six months ahead of guidance). However, of the large

caps Anglo is the only company guiding 2017 total capex to be at a level similar to

sustaining capex of ~US$2.5bn; therefore, capex would need to rise materially if the

company aims to maintain and/or grow volumes.

■ VALE (Neutral, $9/ADR target price): Reduction of net debt to the USD15bn target

remains the company's primary focus. The combination of lower capex, divestment of

non-core assets, cost-cutting, and current momentum for commodity prices recently

contributed to an improvement in Vale's balance sheet. CSe Net Debt/Ebitda of 1.2x

YE17. Vale is the only company for which we expect 2020 capex to be materially below

2015-16 levels due to completion of the S11D project.

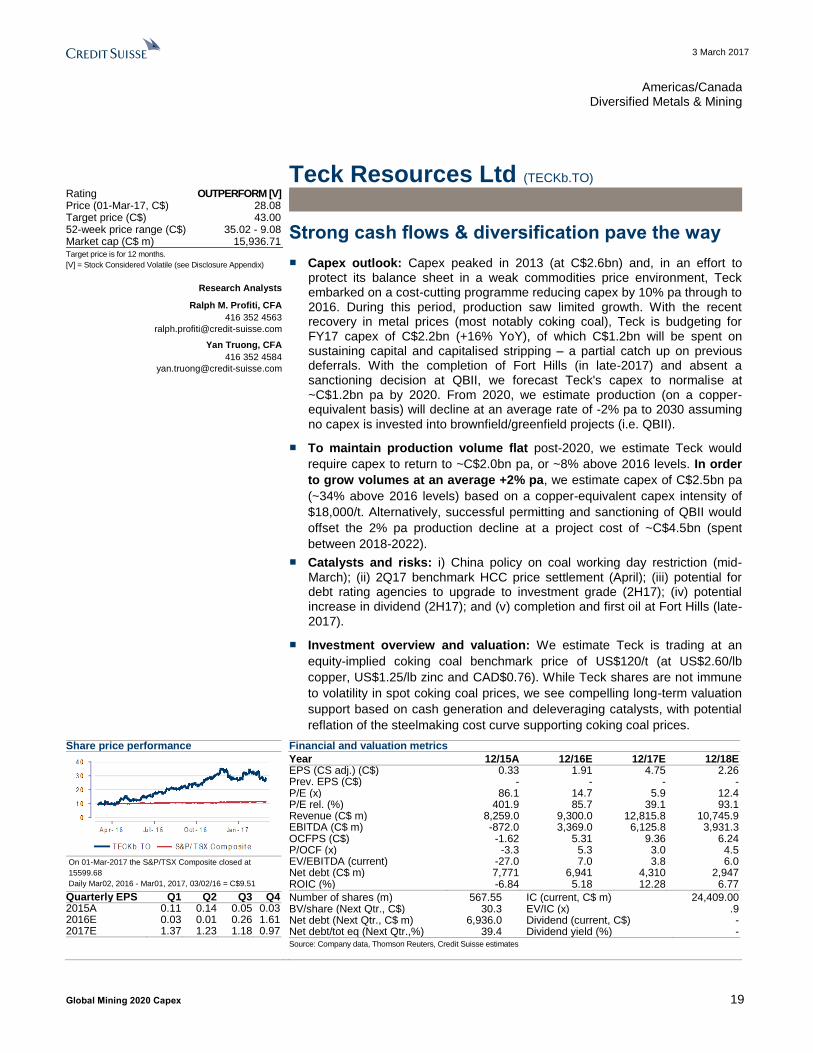

■ TECK (Outperform, C$43 target price): We see compelling long-term valuation

support based on cash generation and deleveraging catalysts. Teck's most recent

tender offer provided a positive step towards a goal of reducing debt below US$5bn

(vs. US$6.2bn at YE16), regaining investment grade credit, and ultimately an upgrade

to the dividend (currently C$0.10/year; dividend yield: 0.34%). We see Teck's YE17 net

debt at US$3.3bn, Debt/Debt+Equity to 27% (vs. 32% at end-FY16), and FY17/18

Debt-to-EBITDA at to 1.2/1.9x.

Figure 11: Two-year cash returns (dividends and buybacks) – CY cash basis

Source: Credit Suisse estimates

0%

5%

10%

15%

20%

25%

RIO GLEN BHP AAL

Dividend yield Buyback/special yields

3 March 2017

Global Mining 2020 Capex 5

Our commodity price assumptions are summarised below:

Figure 12: Commodity price forecast

Source: Credit Suisse estimates, Thomson Reuters

Base case and spot multiples are summarized below for the six companies.

Figure 13: Valuation summary base and spot

Source: Credit Suisse estimates, CY basis, PE based on Underlying EPS, AAL EV/EBITDA adjusted for minorities.

Commodity Unit 2015 2016E 2017E 2018E Spot

Spot

vs. 2016

Spot

vs. 2017

Spot

vs. 2018

Iron ore 62% CFR $/t 56 57 78 58 91 59% 18% 57%

Thermal coal $/t 58 61 74 70 83 36% 13% 19%

Coking coal Contract $/t 102 114 200 130 162 42% -19% 25%

Ferrochrome $/lb 1.07 0.96 1.53 1.20 1.65 73% 8% 38%

Copper U$/lb 2.50 2.22 2.45 2.05 2.72 23% 11% 33%

Nickel U$/lb 5.38 4.37 5.25 6.00 4.98 14% -5% -17%

Zinc U$/lb 0.88 0.95 1.15 1.05 1.29 36% 13% 23%

Aluminium U$/lb 0.75 0.73 0.79 0.74 0.88 21% 12% 20%

Platinum U$/oz 1,053 990 938 940 1,015 3% 8% 8%

Palladium U$/oz 690 618 730 740 775 25% 6% 5%

Gold U$/oz 1,160 1,251 1,338 1,375 1,245 0% -7% -9%

Oil (Brent) US$/t 52.7 44.5 56.3 65.0 56.7 28% 1% -13%

USD:AUD 0.75 0.74 0.73 0.72 0.77 4% 6% 7%

USD:ZAR 12.77 14.73 13.75 14.25 12.82 -13% -7% -10%

USD:Peso 655 678 675 720 641 -5% -5% -11%

USD:KZT 223 342 323 315 312 -9% -3% -1%

USD:SEK 8.44 8.55 9.00 9.20 8.98 5% 0% -2%

Base Case

2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018

Diversifieds

BHP 8.1 11.2 4.2 5.4 0.5 0.5 0.1 0.1 13.6% 9.1% 6.2% 4.5%

RIO 6.2 10.6 3.7 5.9 0.2 0.5 0.0 0.1 16.1% 8.0% 8.3% 5.5%

Glen 15.1 24.1 4.9 5.4 0.8 0.8 0.2 0.2 10.3% 8.6% 4.3% 4.3%

AAL 5.8 8.8 3.6 4.5 0.6 0.6 0.3 0.2 16.0% 11.0% 7.6% 5.7%

Teck 5.9 12.4 3.3 4.8 0.7 0.7 0.3 0.2 12.7% 11.5% 0.4% 0.4%

Vale 6.7 13.9 3.9 5.5 1.0 1.0 0.3 0.2 17.5% 12.6% 5.3% 3.6%

Spot Case

2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018

Diversifieds

BHP 7.2 6.3 3.8 3.5 0.4 0.1 0.1 0.0 15.0% 15.2% 7.0% 7.0%

RIO 5.1 4.8 3.1 3.0 0.0 -0.1 0.0 0.0 19.4% 18.5% 9.6% 10.3%

Glen 13.6 13.4 4.6 4.3 0.8 0.5 0.2 0.1 11.1% 11.2% 4.7% 6.0%

AAL 5.6 5.3 3.4 3.0 0.5 0.3 0.2 0.1 16.9% 18.8% 8.2% 9.4%

Teck 5.5 7.2 3.2 3.3 0.7 0.3 0.3 0.1 13.6% 18.4% 0.4% 0.4%

Vale 4.5 3.7 3.2 2.4 0.8 0.2 0.3 0.1 19.8% 27.6% 3.3% 6.7%

FCF Yield Div YieldP/E EV/EBITDA ND/EBITDA ND/Mrk Cap

Div YieldP/E EV/EBITDA ND/EBITDA ND/Mrk Cap FCF Yield

3 March 2017

Global Mining 2020 Capex 6

Executive summary After three years of heavy cuts, the global mining capex cycle is turning. The sector

reached unprecedented levels of capex from 2011 to 2013 but then needed to cut

investment sharply in reaction to weaker demand growth, falling prices and the resultant

pressure on balance sheets and cash flows. From strategies led by volume and market

share gains only 4-5 years ago, the large cap CEO mantra is now one of value over

volume and a prudent approach to growth is likely to remain.

However, mining is a capex-intensive industry with finite reserves and, with balance

sheets repaired and the outlook for commodities brighter than 12 months ago, the industry

now looks to be in a position to begin investing again to offset natural mine depletion and

for longer-term growth. A frustration for investors is that sell-side estimates typically only

factor in known projects and may show unrealistic capex and FCF profiles on a 2-3 year

horizon. Our report addresses this issue by analysing where capex could trend to from

2020. We expect only modest increases in 2017/18 capex with businesses generally well

capitalised following the significant investment during the boom years and steady annual

volume growth from projects committed to 5-6 years ago. From 2020, we estimate capex

for the six companies assessed could increase by 50-60% compared with 2016 levels

assuming the companies aim to maintain average annual volume growth at 2% pa. If the

companies only invest sufficiently to offset reserve decline/mine depletion, capex could

remain at levels similar to 2017 guidance.

Figure 14: Large cap total capex U$m – could increase 60% by 2020E (vs 2016)

Source: Company data, Credit Suisse estimates, Glencore pro forma before 2013 and XTA capex before 2006

Balance sheet improvements should lead shareholder cash returns and then capex higher

Capex cuts and efforts to improve cash flows were at their maximum in late 2015/early

2016. 2016 was a year of balance sheet recovery and 2017 and 2018 should see further

material net debt reductions and higher shareholder returns. By end 2017, we expect net

debt for the six diversified miners to have more than halved from the 2012 peak of $120bn

to below $60bn. Net debt:EBITDA should on average fall below 1x. All of the corporates

are signaling more conservative balance sheet policies than in the past, but by the end of

2017 balance sheets should be under-geared, allowing for increased shareholder returns

through ordinary dividends, specials and buybacks.

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017E

2018E

2020E

2020E

BLT RIO GLEN AAL Vale Teck

2020E normalized capex to offset

production decline

2020E normalized

capex to grow production by

2% pa

3 March 2017

Global Mining 2020 Capex 7

Figure 15: Net Debt: EBITDA 2016 and 2017E Figure 16: Large cap aggregate Net Debt

Source: Company data, Credit Suisse estimates, CY basis Note: 2017 are CS estimates Source: Company data, Credit Suisse estimates, CY basis, Includes BLT, RIO, GLEN, AAL, VALE and Teck

Below we illustrate total shareholder cash returns (through dividends and buybacks)

expected over the next two years. We break this down between our normal dividend

assumptions and specials/buybacks. The below chart excludes VALE and TECK where

we expect the focus through 2017 and 2018 to still be on debt reduction.

Figure 17: Shareholder cash returns (dividends and buybacks)

Source: Credit Suisse estimates

Volumes likely to decline post 2019/20 without increased investment

For the diversified miners, volume growth averaged ~5% pa over 2010-15 but slowed

sharply thereafter. Legacy growth projects should keep volumes expanded out to 2019,

but from 2019/20, we expect volume growth to grind to a halt without fresh investment in

replacement projects and potential new growth opportunities. An exception to this is VALE

where iron ore growth volumes are expected to continue over the next 3-4 years.

-

0.50

1.00

1.50

2.00

2.50

VALE GLEN TECK AAL BLT RIO

2016 2017

-

0.50

1.00

1.50

2.00

2.50

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2011 2012 2013 2014 2015 2016 2017

Net Debt ND/EBITDA

0%

5%

10%

15%

20%

25%

RIO GLEN BHP AAL

Dividend yield Buyback/special yields

3 March 2017

Global Mining 2020 Capex 8

Figure 18: Large cap indexed volume growth 2010-20E

Source: Company data, Credit Suisse estimates, CY basis Note: CS estimates from 2017-20

Total industry capex from 2020 could rise by 50-60% vs 2016

We estimate capex trends for each of the companies based on expected production levels

in 2020, anticipated production declines thereafter (due to lower grades, mine depletion

etc) and estimated project costs. Under a scenario where each of the companies invests

sufficiently to offset reserve decline (typically of 3-4% pa) and grow group production

volumes by 2% (slightly below long-term commodity demand growth trends), we estimate

capex for the industry could climb by 50-60% from 2020 onwards. However, as we discuss

in the company sections that follow, there are large differences between the companies.

VALE is the only major where we expect lower capex in 2020 vs 2016. Excluding VALE

we expect capex for the other companies to be up over 60% vs 2016 levels.

Figure 19: Capex progression 2016-20E ($m)

Source: Company data, Credit Suisse estimates, Companies used: BHP, RIO, AAL, GLEN, VALE and Teck

The companies have inherent flexibility around capex and we don’t expect more material

increases until 2019/20. If prices were to decline and companies only invest sufficiently to

keep group volumes stable, capex could remain at levels similar to 2017 guidance.

22,144

33,380

2,338

8,898

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2016 Capex increase to maintainstable production

Capex to grow at 2% pa 2020E

3 March 2017

Global Mining 2020 Capex 9

Capex increases only become a problem at the end of a cycle

The sector is enjoying high margins and FCFs well above the market average and

historical norms, and a return to the free-spending 2007-12 years seems to be a growing

concern with investors. Commodity prices, which lead capex direction by ~1 year, have

recovered strongly over the past year and spot EBITDA margins are now higher than the

peak years. Based on current guidance, the companies are already guiding in aggregate

to 2017 capex 5-10% above 2016 levels. At the company level, there are different trends,

with Vale guiding to lower capex YoY in 2017, Anglo to flat and the other companies to

increases of more than 10% (details in the company sections).

While capex will most likely increase over the coming years, a rebounding capex cycle is a

sign of a healthier industry and excessive capex becomes a problem only towards the end

of a cycle when supply outpaces demand and marginal projects are pursued. We think the

industry would need to generate several years of elevated returns before a lack of capex

discipline becomes a concern.

Figure 20: Large cap EBITDA margins 2005-17E vs

prices Figure 21: Average ROCE 2005-17E vs capex (U$m)

Source: Company data, Credit Suisse estimates, Thomson Reuters, Large cap includes BLT,RIO and AAL, CY basis, Weights for Commodity index: Iron ore 35%, Cu 25%, Coal 15%, Ali 5%, Ni 3%, Zn 5%, Pt 5%, Brent 7%

Source: Company data, Credit Suisse estimates, Large cap includes BLT, RIO and AAL, CY basis, Total capex for BLT, RIO, GLEN, AAL, Vale and Teck

Capex intensity in US$ terms should remain structurally lower than the peak 2010-13 period, but…

The major mining resource currencies are now 25-40% weaker against the US$ compared

with average levels in the 2010-12 period. Key input costs such as oil and steel are also

materially lower and the overall supply chain is looser. Company management teams have

estimated that current project costs are down 15-40% compared with the peak 2012

period (bigger increases for iron ore / bulk projects versus copper/base metals)

… capex intensity structurally higher for copper than for iron ore and…

Capex for growth is likely to be directed more towards later-cycle copper than to earlier-

cycle iron ore where we expect production to continue to ramp up to installed capacity

over the next three years. Our analysis later in this report shows that copper capex

intensity (measured by capex:sales and capex to unit of production) is almost double that

of iron ore, meaning targeted growth in copper will increase capex requirements over the

long term.

0

50

100

150

200

250

300

350

400

30%

32%

34%

36%

38%

40%

42%

44%

46%

48%

2005 2007 2009 2011 2013 2015 2017E

EBITDA % Underlying Commodity index, Rhs

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

0%

5%

10%

15%

20%

25%

30%

2005 2007 2009 2011 2013 2015 2017E

Average ROCE Total Capex, Rhs

3 March 2017

Global Mining 2020 Capex 10

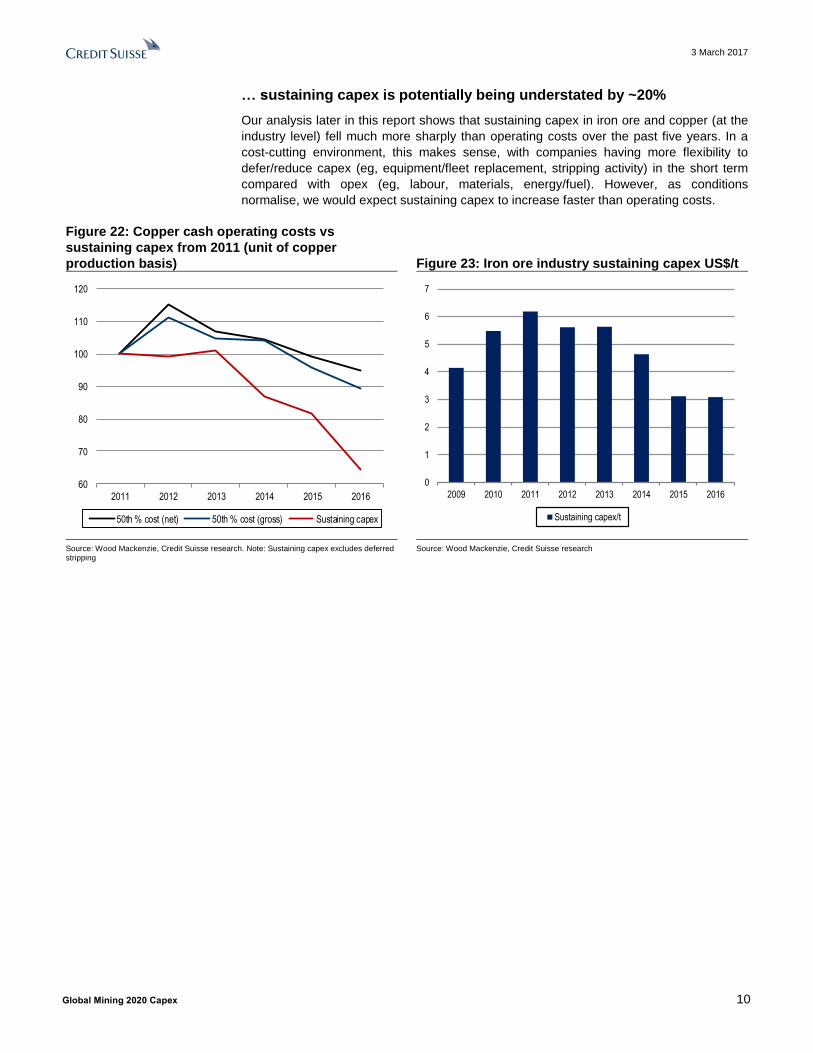

… sustaining capex is potentially being understated by ~20%

Our analysis later in this report shows that sustaining capex in iron ore and copper (at the

industry level) fell much more sharply than operating costs over the past five years. In a

cost-cutting environment, this makes sense, with companies having more flexibility to

defer/reduce capex (eg, equipment/fleet replacement, stripping activity) in the short term

compared with opex (eg, labour, materials, energy/fuel). However, as conditions

normalise, we would expect sustaining capex to increase faster than operating costs.

Figure 22: Copper cash operating costs vs

sustaining capex from 2011 (unit of copper

production basis) Figure 23: Iron ore industry sustaining capex US$/t

Source: Wood Mackenzie, Credit Suisse research. Note: Sustaining capex excludes deferred stripping

Source: Wood Mackenzie, Credit Suisse research

60

70

80

90

100

110

120

2011 2012 2013 2014 2015 2016

50th % cost (net) 50th % cost (gross) Sustaining capex

0

1

2

3

4

5

6

7

2009 2010 2011 2012 2013 2014 2015 2016

Sustaining capex/t

3 March 2017

Global Mining 2020 Capex 11

Europe/United Kingdom Diversified Metals & Mining

Anglo American Plc (AAL.L) Rating NEUTRAL [V] Price (01 Mar 17, p) 1310.00 Target price (p) 1400.00 Market Cap (£ m) 18,369.4 Enterprise value (£ m) 27,411.7 Target price is for 12 months.

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Liam Fitzpatrick

44 20 7883 8350

Michael Shillaker

34 91 791 58 78

James Gurry

44 20 7883 7083

Conor Rowley

44 20 7883 9156

Sustaining capex is not sustainable

■ Capex outlook: Anglo is the only of the large caps guiding 2017 total capex

to be at a similar level to sustaining capex of ~US$2.5bn. From 2019, group

volumes will likely begin to decline and from 2020, we estimate group

volumes will decline at a rate of close to 3% pa assuming no capex is sunk

beyond sustaining capex (of ~US$2.5bn). This will mean capex will need to

rise materially if the company aims to maintain and/or grow volumes. To keep

group volumes flat post 2020, we estimate the company would need to spend

~US$3.5bn pa (US$2.5bn sustaining). To grow volumes at 2% pa from 2020,

and assuming that incremental volume growth is primarily in copper rather

than iron ore, would mean that group capex could climb to US$4.5bn.

■ Investment overview: At the recent FY16 results, management gave the

latest iteration of the Anglo strategy which now envisages retaining most of

the iron ore and coal businesses. The balance sheet is now more or less

where it needs to be and we expect a dividend restart at the mid-year (six

months ahead of guidance). However, as we outlined in our recent note

(Anglo American Plc - Breaking up is hard to do) we see strategic merit in

divesting a large part (if not all) of the SA businesses, including reduced EM

exposure (higher multiple, lower perceived political risk), simpler corporate

structure and greater concentration towards later cycle commodities. The

tough question for management now is whether Anglo in its current form is

sufficiently differentiated compared to its larger (and simpler) global peers.

■ Catalysts and risks: Progress on divestments (Samancor, domestic coal in

SA); Coking coal, iron ore, platinum and copper prices; Regulatory

developments in South Africa.

■ Valuation and earnings changes: We increase EBITDA estimates by

14%/4% in 2017/18 on our higher base case iron ore prices. We leave our TP

unchanged at £14 but increase our dividend assumptions for 2017/18 (50%

payout ratio assumed).

Share price performance

The price relative chart measures performance against the

FTSE ALL SHARE INDEX which closed at 4014.7 on

01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.-

Eu.95/US$1

Performance 1M 3M 12M Absolute (%) -6.0 5.6 143.7 Relative (%) -10.0 -3.9 124.7

Financial and valuation metrics

Year 12/16A 12/17E 12/18E 12/19E Revenue (US$ m) 21,378.0 24,614.1 22,255.4 23,290.6 EBITDA (US$ m) 6,075.0 9,256.1 6,994.7 7,459.3 Pre-tax profit adjusted (US$ m) 4,724.00 6,664.34 4,343.80 4,729.69 CS EPS (adj.) (US$) 1.23 2.68 1.76 1.89 Prev. EPS (US$) - 2.31 1.66 - ROIC (%) 9.8 15.0 9.9 10.5 P/E (adj.) (x) 13.1 6.0 9.2 8.5 P/E rel. (%) 73.4 40.7 67.3 68.2 EV/EBITDA (x) 6.0 3.7 4.7 4.3

Dividend (12/17E, US$) 1.20 Net debt/equity (12/17E,%) 19.6 Dividend yield (12/17E,%) 7.4 Net debt (12/17E, US$ m) 5,419.3 BV/share (12/17E, US$) 16.9 IC (12/17E, US$ m) 33,109.4 Free float (%) 100.0 EV/IC (12/17E, (x) 1.0 Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 12

Anglo American Plc (AAL.L)

Price (01 Mar 2017): 1310.00p; Rating: NEUTRAL [V]; Target Price: 1400.00p; Analyst: Liam Fitzpatrick

Income statement (US$ m) 12/16A 12/17E 12/18E 12/19E

Revenue 21,378 24,614 22,255 23,291 EBITDA 6,075 9,256 6,995 7,459 Depr. & amort. (2,309) (2,628) (2,753) (2,831) EBIT 3,766 6,628 4,242 4,629 Net interest exp. (229) (407) (259) (262) Associates 278 443 361 363 PBT 4,724 6,664 4,344 4,730 Income taxes (698) (1,661) (1,025) (1,177) Profit after tax 4,026 5,003 3,319 3,552 Minorities (332) (832) (466) (520) Preferred dividends - - - - Associates & other (2,100) (685) (566) (569) Net profit 1,594 3,487 2,287 2,463 Other NPAT adjustments 0 0 0 0 Reported net income 1,594 3,487 2,287 2,463

Cash flow (US$ m) 12/16A 12/17E 12/18E 12/19E

EBIT 3,766 6,628 4,242 4,629 Net interest (229) (407) (259) (262) Cash taxes paid - - - - Change in working capital 1,863 (400) 0 (118) Other cash and non-cash items (1) 1,133 1,601 1,527 Cash flow from operations 5,399 6,954 5,584 5,776 CAPEX (2,418) (2,499) (2,553) (2,839) Free cashflow to the firm 4,112 3,875 2,477 2,366 Acquisitions 0 0 0 0 Divestments - - - - Other investment/(outflows) 1,893 282 137 70 Cash flow from investments (525) (2,216) (2,415) (2,769) Net share issue/(repurchase) - - - - Dividends paid 0 (807) (1,287) (1,206) Issuance (retirement) of debt (4,519) (5,320) (3,000) 0 Cashflow from financing (5,780) (6,990) (4,979) (1,847) Changes in net cash/debt 4,423 3,068 1,190 1,160 Net debt at start 12,910 8,487 5,419 4,230 Change in net debt (4,423) (3,068) (1,190) (1,160) Net debt at end 8,487 5,419 4,230 3,069

Balance sheet (US$ m) 12/16A 12/17E 12/18E 12/19E

Assets Total current assets 12,449 10,197 8,386 9,776 Total assets 50,149 47,794 45,748 47,178 Liabilities Total current liabilities 6,525 6,125 6,125 6,236 Total liabilities 25,824 20,104 17,104 17,215 Total equity and liabilities 50,149 47,794 45,748 47,178

Per share 12/16A 12/17E 12/18E 12/19E

No. of shares (wtd avg.) (mn) 1,300 1,300 1,300 1,300 CS EPS (adj.) (US$) 1.23 2.68 1.76 1.89 Dividend (US$) 0.00 1.20 0.89 0.96 Free cash flow per share (US$) 3.16 2.98 1.91 1.82

Key ratios and valuation 12/16A 12/17E 12/18E 12/19E

Growth/Margin (%) Sales growth (%) 4.5 15.1 (9.6) 4.7 EBIT growth (%) 69.4 76.0 (36.0) 9.1 Net income growth (%) 128.3 118.7 (34.4) 7.7 EPS growth (%) 128.1 118.7 (34.4) 7.7 EBITDA margin (%) 28.4 37.6 31.4 32.0 EBIT margin (%) 17.6 26.9 19.1 19.9 Pretax profit margin (%) 22.1 27.1 19.5 20.3 Net income margin (%) 7.5 14.2 10.3 10.6

Valuation 12/16A 12/17E 12/18E 12/19E

EV/Sales (x) 1.7 1.4 1.5 1.4 EV/EBITDA (x) 6.0 3.7 4.7 4.3 EV/EBIT (x) 9.7 5.1 7.8 6.9 Dividend yield (%) 0.00 7.43 5.51 5.94 P/E (x) 13.1 6.0 9.2 8.5

Credit ratios (%) 12/16A 12/17E 12/18E 12/19E

Net debt/equity (%) 34.9 19.6 14.8 10.2 Net debt to EBITDA (x) 1.4 0.6 0.6 0.4 Interest coverage ratio (x) 16.4 16.3 16.4 17.7

Company Background

Anglo American plc is a global mining company. Its portfolio of mining assets and natural resources includes platinum group metals and diamonds, with interests in copper, iron ore, metallurgical coal, nickel and thermal coal.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (p) 1800.00

Our Blue Sky valuation of £18.0 assumes a full break-up / take-out valuation for the group.

Our Grey Sky Scenario (p) 800.00

Our Grey Sky valuation of £8 assumes ~$45/t iron ore and ~200c copper, but we do not assume a return to the extreme balance sheet stress as seen in late 2015/early 2016.

Share price performance

The price relative chart measures performance against the FTSE ALL SHARE

INDEX which closed at 4014.7 on 01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.- Eu.95/US$1

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates

3 March 2017

Global Mining 2020 Capex 13

Asia Pacific/Australia Diversified Metals & Mining

BHP Billiton (BLT.L) Rating NEUTRAL [V] Price (01 Mar 17, p) 1353.50 Target price (p) 1380.00 Market Cap (£ m) 78,458.7 Enterprise value (£ m) 90,015.4 Primary RIC BHP.AX Price (01 Mar 17, A$) 24.88 Target price (A$) 26.50 Target price is for 12 months.

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Paul McTaggart

61 2 8205 4698

James Gurry

44 20 7883 7083

Liam Fitzpatrick

44 20 7883 8350

Conor Rowley

44 20 7883 9156

Rising capex requirements on a 2-3 year

horizon

■ Event: We increase BHP EBITDA by 8%, 9% and 3% over the 3 years FY17-

FY19 on our higher base case iron ore prices. However, in this analysis, we

also note the rising capex profile we expect at BHP as it considers the next

round of project approvals including the next Phase at Escondida, Olympic

Dam growth to 450kt/yr, iron ore replacement mines near 2020 and the

Jansen potash project as shaft development approaches completion. This is

even before considering the oil business where volumes are declining and

investment increasing, with extremely high levels of exploration spend at

~US$800m/yr. We do not see BHP in a position to make significant

shareholder returns but expect it to stick to its dividend policy of 50% of EPS

plus additional returns as can be afforded.

■ Investment overview: Oil is the differentiator and we would be more

negative on BHP except for our view on oil prices is for upside risk. The shale

operations were FCF positive for the first time in the Dec-2016 half year.

■ Catalysts and risks: Oil and iron ore prices are key risks and potential

catalysts and we see divergent expectations - positive for the former and

negative for the latter - on a 12-month view. We expect the Spence copper

project US$2.2bn to be approved in coming months. Thereafter, we highlight

a series of project approval considerations for BHP over the coming 2-3

years.

■ Valuation: BHP trades on c.9x FY17E PE and 4.4x EBITDA. This is not

demanding but lacks the clear value and shareholder return case we see in

its major rivals.

Share price performance

The price relative chart measures performance against the

FTSE ALL SHARE INDEX which closed at 4014.7 on

01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.-

Eu.95/US$1

Performance 1M 3M 12M Absolute (%) -6.4 3.2 72.9 Relative (%) -10.4 -6.3 54.0

Financial and valuation metrics

Year 6/16A 6/17E 6/18E 6/19E Revenue (US$ m) 30,912.0 43,611.2 40,416.6 36,619.0 EBITDA (US$ m) 12,340.0 25,017.2 22,054.4 17,918.3 Pre-tax profit adjusted (US$ m) 2,445.00 16,300.31 13,752.29 10,421.24 CS EPS (adj.) (US$) 0.24 1.81 1.63 1.29 Prev. EPS (US$) - 1.58 1.39 1.19 ROIC (%) 2.4 13.6 12.4 9.5 P/E (adj.) (x) 69.9 9.2 10.2 12.9 P/E rel. (%) 391.0 62.2 75.2 103.8 EV/EBITDA (x) 9.9 4.4 4.8 5.9

Dividend (06/17E, US$) 1.01 Net debt/equity (06/17E,%) 21.6 Dividend yield (06/17E,%) 6.1 Net debt (06/17E, US$ m) 14,392.9 BV/share (06/17E, US$) 11.4 IC (06/17E, US$ m) 81,036.9 Free float (%) 99.5 EV/IC (06/17E, (x) 1.4 Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 14

BHP Billiton (BLT.L)

Price (01 Mar 2017): 1353.50p; Rating: NEUTRAL [V]; Target Price: 1380.00p; Analyst: Paul McTaggart

Income statement (US$ m) 6/16A 6/17E 6/18E 6/19E

Revenue 30,912 43,611 40,417 36,619 EBITDA 12,340 25,017 22,054 17,918 Depr. & amort. (8,871) (7,803) (7,596) (6,861) EBIT 3,469 17,214 14,458 11,057 Net interest exp. (1,024) (913) (706) (636) Associates 0 0 0 0 PBT 2,445 16,300 13,752 10,421 Income taxes 1,052 (5,927) (4,401) (3,335) Profit after tax 1,444 10,423 9,352 7,086 Minorities (178) (706) (634) (298) Preferred dividends - - - - Associates & other 0 0 0 0 Net profit 1,266 9,717 8,718 6,788 Other NPAT adjustments (7,651) (40) 0 0 Reported net income (6,385) 9,677 8,718 6,788

Cash flow (US$ m) 6/16A 6/17E 6/18E 6/19E

EBIT 3,469 17,214 14,458 11,057 Net interest (702) (457) 0 0 Cash taxes paid (2,286) (3,682) (3,000) (2,273) Change in working capital - - - - Other cash and non-cash items 10,144 5,412 5,543 5,464 Cash flow from operations 10,625 18,487 17,001 14,248 CAPEX (7,022) (4,600) (5,400) (6,547) Free cashflow to the firm 9,835 17,491 15,023 11,202 Acquisitions (237) (243) (150) (150) Divestments 273 681 0 0 Other investment/(outflows) (259) (707) (900) (784) Cash flow from investments (7,245) (4,869) (6,450) (7,481) Net share issue/(repurchase) 0 0 0 (3,000) Dividends paid (4,217) (3,227) (5,556) (4,002) Issuance (retirement) of debt 4,451 (1,000) 0 1,000 Cashflow from financing 284 (4,303) (5,556) (6,002) Changes in net cash/debt (1,685) 11,709 4,996 (234) Net debt at start 24,417 26,102 14,393 9,397 Change in net debt 1,685 (11,709) (4,996) 234 Net debt at end 26,102 14,393 9,397 9,632

Balance sheet (US$ m) 6/16A 6/17E 6/18E 6/19E

Assets Total current assets 17,714 27,165 32,161 32,926 Total assets 118,953 123,754 126,766 127,402 Liabilities Total current liabilities 12,340 11,999 11,999 11,999 Total liabilities 58,882 57,110 57,110 58,110 Total equity and liabilities 118,953 123,754 126,766 127,402

Per share 6/16A 6/17E 6/18E 6/19E

No. of shares (wtd avg.) (mn) 5,322 5,362 5,362 5,278 CS EPS (adj.) (US$) 0.24 1.81 1.63 1.29 Dividend (US$) 0.30 1.01 0.82 0.65 Free cash flow per share (US$) 1.85 3.26 2.80 2.12

Key ratios and valuation 6/16A 6/17E 6/18E 6/19E

Growth/Margin (%) Sales growth (%) (30.7) 41.1 (7.3) (9.4) EBIT growth (%) (70.8) 396.2 (16.0) (23.5) Net income growth (%) (80.1) 667.5 (10.3) (22.1) EPS growth (%) (80.1) 661.8 (10.3) (20.9) EBITDA margin (%) 39.9 57.4 54.6 48.9 EBIT margin (%) 11.2 39.5 35.8 30.2 Pretax profit margin (%) 7.9 37.4 34.0 28.5 Net income margin (%) 4.1 22.3 21.6 18.5

Valuation 6/16A 6/17E 6/18E 6/19E

EV/Sales (x) 4.0 2.5 2.6 2.9 EV/EBITDA (x) 9.9 4.4 4.8 5.9 EV/EBIT (x) 35.3 6.4 7.3 9.6 Dividend yield (%) 1.80 6.07 4.92 3.89 P/E (x) 69.9 9.2 10.2 12.9

Credit ratios (%) 6/16A 6/17E 6/18E 6/19E

Net debt/equity (%) 43.5 21.6 13.5 13.9 Net debt to EBITDA (x) 2.1 0.6 0.4 0.5 Interest coverage ratio (x) 3.4 18.8 20.5 17.4

Company Background

BHP Billiton Limited is a diversified natural resources company. It operates nine units: petroleum, aluminium, base metals (incl. uranium), diamonds and specialty products, stainless steel materials, iron ore, manganese, metallurgical & energy coal.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (p) 2000.00

China reverses its declining steel demand trend and stimulates the economy significantly, resulting in much tighter iron ore markets and prices in the $85/t range, while oil and copper markets also tighten on higher China demand resulting in a valuation of GBp2000/shr.

Our Grey Sky Scenario (p) 400.00

China steel demand declines significantly as the economy slows and urbanisation rate declines. While still generating positive bottom of the cycle earnings, we think iron ore could trade as low as $35/tonne, petroleum and copper prices also fall to $30/bbl and $1.75/lb resulting in a valuation of GBp400/shr.

Share price performance

The price relative chart measures performance against the FTSE ALL SHARE

INDEX which closed at 4014.7 on 01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.- Eu.95/US$1

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates

3 March 2017

Global Mining 2020 Capex 15

Europe/United Kingdom Diversified Metals & Mining

Glencore (GLEN.L) Rating OUTPERFORM [V] Price (01 Mar 17, p) 337.75 Target price (p) 400.00 Market Cap (£ m) 44,797.5 Enterprise value (£ m) 55,743.2 Target price is for 12 months.

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Liam Fitzpatrick

44 20 7883 8350

Michael Shillaker

34 91 791 58 78

James Gurry

44 20 7883 7083

Conor Rowley

44 20 7883 9156

Benefiting from latent capacity

■ Capex outlook: At the recent results, the company guided capex would

remain ~US$4bn over the next 3-5 years of which sustaining would account

for ~US$3bn. In our view the company should be able to maintain this level

(US$4-4.5bn) through 2017-19 without the need to approve any major

projects benefiting from latent capacity growth potential in copper and zinc.

This should underpin growth of ~3% pa 2016-20 after which point, assuming

all suspended volumes return, we estimate group production volumes will

decline at a rate of 3% pa or higher, assuming no capex is sunk beyond

sustaining capex. To keep group volumes flat post 2020, we estimate

Glencore (GLEN) would need to spend $4.5-5.0bn pa. To grow volumes at

2% pa from 2020, and assuming that incremental volume growth is primarily

in copper, this would mean that group capex could climb to ~US$6bn.

■ Investment overview: As we recently outlined (Glencore - Diversification

and copper exposure to the fore), we favour GLEN's diversified business mix,

we see copper moving from a headwind in 2016 to a tailwind in 2017, and the

company's latent capacity growth is under-priced by the market, in our view.

The company delivered a strong cost and cash flow performance in 2016 and

gave consistent guidance for 2017. We expect the balance sheet to move to

an 'under-geared' position (sub 1x net debt : EBITDA by mid-2017 or H217)

and this should open the door for higher dividend payments. Based on our

medium-long term price assumptions, we believe the business can sustain a

dividend payout of over US$2.5bn pa (>4.5% dividend yield) based on a 40%

payout of industrial cash flows.

■ Catalysts and risks: Base metal and thermal coal prices, potential M&A.

■ Valuation: Glencore has no iron ore exposure and therefore we have left our

estimates unchanged. Our £4/sh TP is based on a target EV/EBITDA multiple

of 6x 2017E and 6.5x 2018E (higher due to lower price assumptions). Our

Blue Sky valuation is £5 based on a rerating to 2013/14 multiples of ~7x

industrial EV/EBITDA.

Share price performance

The price relative chart measures performance against the

FTSE 100 IDX which closed at 7382.9 on 01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.-

Eu.95/US$1

Performance 1M 3M 12M Absolute (%) 2.9 20.9 148.1 Relative (%) -1.1 11.2 128.0

Financial and valuation metrics

Year 12/16A 12/17E 12/18E 12/19E Revenue (US$ m) 177,351.0 209,082.9 221,137.3 233,014.0 EBITDA (US$ m) 10,268.0 13,955.5 12,374.6 13,918.3 Pre-tax profit adjusted (US$ m) 2,397.00 6,398.62 4,256.93 5,429.00 CS EPS (adj.) (US$) 0.17 0.27 0.17 0.22 Prev. EPS (US$) - - - - ROIC (%) 5.4 9.3 7.0 9.5 P/E (adj.) (x) 24.7 15.2 24.3 18.6 P/E rel. (%) 137.9 102.9 178.5 149.4 EV/EBITDA (x) 7.0 4.9 5.4 4.5

Dividend (12/17E, US$) 0.18 Net debt/equity (12/17E,%) 30.5 Dividend yield (12/17E,%) 4.3 Net debt (12/17E, US$ m) 13,876.0 BV/share (12/17E, US$) 3.2 IC (12/17E, US$ m) 59,352.2 Free float (%) 65.0 EV/IC (12/17E, (x) 1.2 Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 16

Glencore (GLEN.L)

Price (01 Mar 2017): 337.75p; Rating: OUTPERFORM [V]; Target Price: 400.00p; Analyst: Liam Fitzpatrick

Income statement (US$ m) 12/16A 12/17E 12/18E 12/19E

Revenue 177,351 209,083 221,137 233,014 EBITDA 10,268 13,955 12,375 13,918 Depr. & amort. (6,338) (6,225) (6,683) (7,039) EBIT 3,930 7,730 5,691 6,880 Net interest exp. (1,533) (1,332) (1,434) (1,451) Associates 0 0 0 0 PBT 2,397 6,399 4,257 5,429 Income taxes (362) (1,813) (1,328) (1,602) Profit after tax 2,035 4,586 2,929 3,827 Minorities 422 (293) (183) (239) Preferred dividends - - - - Associates & other (264) (405) (315) (419) Net profit 2,193 3,888 2,431 3,170 Other NPAT adjustments 0 0 0 0 Reported net income 2,193 3,888 2,431 3,170

Cash flow (US$ m) 12/16A 12/17E 12/18E 12/19E

EBIT 3,930 7,730 5,691 6,880 Net interest (1,533) (1,332) (1,434) (1,451) Cash taxes paid - - - - Change in working capital (1,201) (344) 19 (1,878) Other cash and non-cash items 3,622 2,451 3,664 3,436 Cash flow from operations 4,818 8,506 7,940 6,987 CAPEX (3,048) (3,617) (3,528) (3,536) Free cashflow to the firm 8,430 5,308 4,907 4,137 Acquisitions 0 (534) 0 0 Divestments 5,839 0 0 0 Other investment/(outflows) 821 952 495 685 Cash flow from investments 3,612 (3,198) (3,033) (2,851) Net share issue/(repurchase) 3 0 0 0 Dividends paid 0 (1,501) (2,684) (2,654) Issuance (retirement) of debt (7,839) 0 0 0 Cashflow from financing (8,629) (1,501) (2,684) (2,654) Changes in net cash/debt 10,619 3,755 2,011 4,564 Net debt at start 28,250 17,631 13,876 11,865 Change in net debt (10,619) (3,755) (2,011) (4,564) Net debt at end 17,631 13,876 11,865 7,301

Balance sheet (US$ m) 12/16A 12/17E 12/18E 12/19E

Assets Total current assets 43,412 47,185 49,159 57,511 Total assets 124,600 126,298 125,117 129,966 Liabilities Total current liabilities 36,206 36,206 36,206 41,416 Total liabilities 80,819 80,822 80,816 86,121 Total equity and liabilities 124,600 126,298 125,117 129,966

Per share 12/16A 12/17E 12/18E 12/19E

No. of shares (wtd avg.) (mn) 14,224 14,218 14,218 14,218 CS EPS (adj.) (US$) 0.17 0.27 0.17 0.22 Dividend (US$) 0.04 0.18 0.18 0.19 Free cash flow per share (US$) 0.59 0.37 0.35 0.29

Key ratios and valuation 12/16A 12/17E 12/18E 12/19E

Growth/Margin (%) Sales growth (%) 2.7 17.9 5.8 5.4 EBIT growth (%) 80.9 96.7 (26.4) 20.9 Net income growth (%) 63.4 77.3 (37.5) 30.4 EPS growth (%) 67.0 62.5 (37.5) 30.4 EBITDA margin (%) 5.8 6.7 5.6 6.0 EBIT margin (%) 2.2 3.7 2.6 3.0 Pretax profit margin (%) 1.4 3.1 1.9 2.3 Net income margin (%) 1.2 1.9 1.1 1.4

Valuation 12/16A 12/17E 12/18E 12/19E

EV/Sales (x) 0.4 0.3 0.3 0.3 EV/EBITDA (x) 7.0 4.9 5.4 4.5 EV/EBIT (x) 18.4 8.9 11.8 9.1 Dividend yield (%) 0.84 4.28 4.26 4.51 P/E (x) 24.7 15.2 24.3 18.6

Credit ratios (%) 12/16A 12/17E 12/18E 12/19E

Net debt/equity (%) 40.3 30.5 26.8 16.7 Net debt to EBITDA (x) 1.7 1.0 1.0 0.5 Interest coverage ratio (x) 2.6 5.8 4.0 4.7

Company Background

Glencore is a leading commodities producer and marketer. It produces, sources, processes, refines, transports, stores, finances and supplies commodities that industries around the world need.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (p) 500.00

Our Blue Sky valuation of £5.0 assumes >300c copper and thermal coal remaining above $70/t.

Our Grey Sky Scenario (p) 220.00

Our Grey Sky valuation of £2 assumes ~200c copper and thermal coal falling back below $60/t, but we do not assume a return to the extreme balance sheet stress as seen in late 2015/early 2016.

Share price performance

The price relative chart measures performance against the FTSE 100 IDX

which closed at 7382.9 on 01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.- Eu.95/US$1

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates

3 March 2017

Global Mining 2020 Capex 17

Asia Pacific/Australia Diversified Metals & Mining

Rio Tinto (RIO.L) Rating OUTPERFORM Price (01 Mar 17, p) 3406.00 Target price (p) 4000.00 Market Cap (£ m) 63,406.4 Enterprise value (£ m) 66,133.9 Primary RIC RIO.AX Rating OUTPERFORM Price (01 Mar 17, A$) 61.37 Target price (A$) 72.00 Target price is for 12 months.

Research Analysts

James Gurry

44 20 7883 7083

Paul McTaggart

61 2 8205 4698

Liam Fitzpatrick

44 20 7883 8350

Conor Rowley

44 20 7883 9156

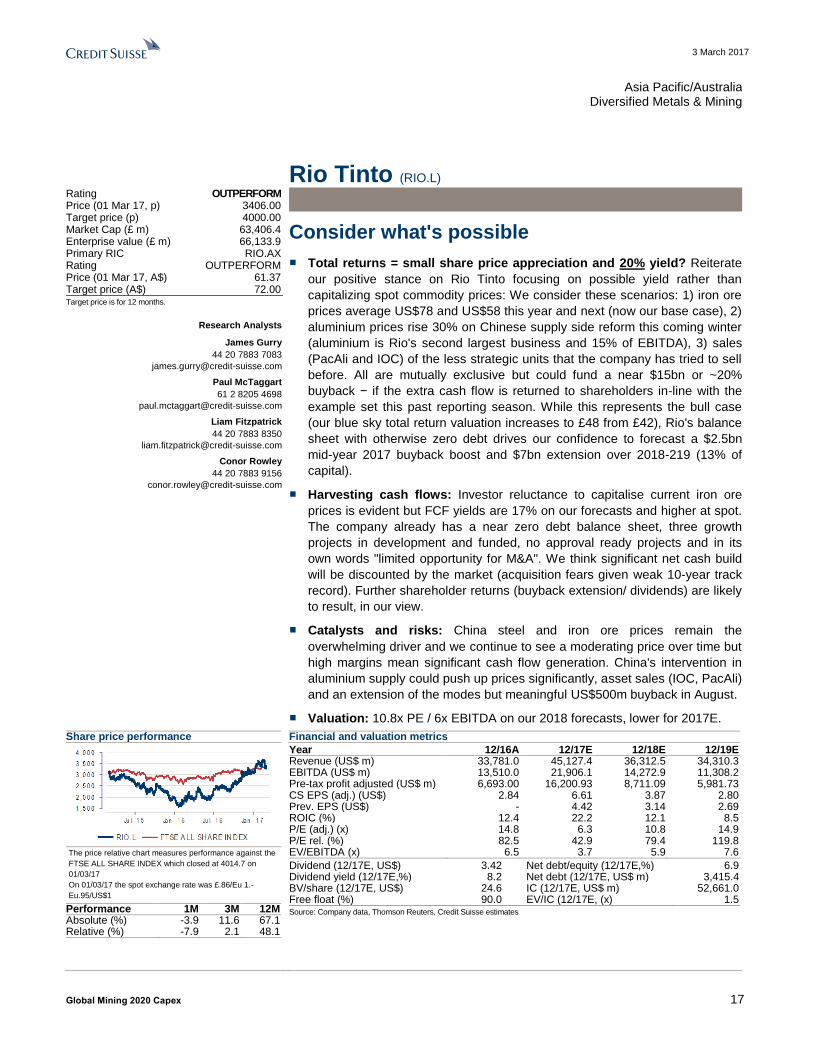

Consider what's possible

■ Total returns = small share price appreciation and 20% yield? Reiterate

our positive stance on Rio Tinto focusing on possible yield rather than

capitalizing spot commodity prices: We consider these scenarios: 1) iron ore

prices average US$78 and US$58 this year and next (now our base case), 2)

aluminium prices rise 30% on Chinese supply side reform this coming winter

(aluminium is Rio's second largest business and 15% of EBITDA), 3) sales

(PacAli and IOC) of the less strategic units that the company has tried to sell

before. All are mutually exclusive but could fund a near $15bn or ~20%

buyback − if the extra cash flow is returned to shareholders in-line with the

example set this past reporting season. While this represents the bull case

(our blue sky total return valuation increases to £48 from £42), Rio's balance

sheet with otherwise zero debt drives our confidence to forecast a $2.5bn

mid-year 2017 buyback boost and $7bn extension over 2018-219 (13% of

capital).

■ Harvesting cash flows: Investor reluctance to capitalise current iron ore

prices is evident but FCF yields are 17% on our forecasts and higher at spot.

The company already has a near zero debt balance sheet, three growth

projects in development and funded, no approval ready projects and in its

own words "limited opportunity for M&A". We think significant net cash build

will be discounted by the market (acquisition fears given weak 10-year track

record). Further shareholder returns (buyback extension/ dividends) are likely

to result, in our view.

■ Catalysts and risks: China steel and iron ore prices remain the

overwhelming driver and we continue to see a moderating price over time but

high margins mean significant cash flow generation. China's intervention in

aluminium supply could push up prices significantly, asset sales (IOC, PacAli)

and an extension of the modes but meaningful US$500m buyback in August.

■ Valuation: 10.8x PE / 6x EBITDA on our 2018 forecasts, lower for 2017E.

Share price performance

The price relative chart measures performance against the

FTSE ALL SHARE INDEX which closed at 4014.7 on

01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.-

Eu.95/US$1

Performance 1M 3M 12M Absolute (%) -3.9 11.6 67.1 Relative (%) -7.9 2.1 48.1

Financial and valuation metrics

Year 12/16A 12/17E 12/18E 12/19E Revenue (US$ m) 33,781.0 45,127.4 36,312.5 34,310.3 EBITDA (US$ m) 13,510.0 21,906.1 14,272.9 11,308.2 Pre-tax profit adjusted (US$ m) 6,693.00 16,200.93 8,711.09 5,981.73 CS EPS (adj.) (US$) 2.84 6.61 3.87 2.80 Prev. EPS (US$) - 4.42 3.14 2.69 ROIC (%) 12.4 22.2 12.1 8.5 P/E (adj.) (x) 14.8 6.3 10.8 14.9 P/E rel. (%) 82.5 42.9 79.4 119.8 EV/EBITDA (x) 6.5 3.7 5.9 7.6

Dividend (12/17E, US$) 3.42 Net debt/equity (12/17E,%) 6.9 Dividend yield (12/17E,%) 8.2 Net debt (12/17E, US$ m) 3,415.4 BV/share (12/17E, US$) 24.6 IC (12/17E, US$ m) 52,661.0 Free float (%) 90.0 EV/IC (12/17E, (x) 1.5 Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 18

Rio Tinto (RIO.L)

Price (01 Mar 2017): 3406.00p; Rating: OUTPERFORM; Target Price: 4000.00p; Analyst: James Gurry

Income statement (US$ m) 12/16A 12/17E 12/18E 12/19E

Revenue 33,781 45,127 36,312 34,310 EBITDA 13,510 21,906 14,273 11,308 Depr. & amort. (4,794) (5,223) (5,109) (4,845) EBIT 8,716 16,683 9,164 6,463 Net interest exp. (1,022) (482) (453) (482) Associates - - - - PBT 6,693 16,201 8,711 5,982 Income taxes (1,412) (4,860) (2,613) (1,795) Profit after tax 5,281 11,341 6,098 4,187 Minorities -0 (307) (58) (44) Preferred dividends - - - - Associates & other (181) 656 513 411 Net profit 5,100 11,689 6,553 4,554 Other NPAT adjustments (483) 0 0 0 Reported net income 4,617 11,689 6,553 4,554

Cash flow (US$ m) 12/16A 12/17E 12/18E 12/19E

EBIT 8,716 16,683 9,164 6,463 Net interest (1,294) (482) (453) (482) Cash taxes paid - - - - Change in working capital (341) 318 1 3 Other cash and non-cash items 1,384 1,018 3,009 3,462 Cash flow from operations 8,465 17,538 11,722 9,446 CAPEX (3,012) (5,000) (5,500) (5,500) Free cashflow to the firm 6,465 15,538 9,722 7,366 Acquisitions 0 0 0 0 Divestments 1,115 2,266 100 100 Other investment/(outflows) (207) 0 0 0 Cash flow from investments (2,104) (2,734) (5,400) (5,400) Net share issue/(repurchase) 101 (3,000) (5,000) (2,000) Dividends paid (2,725) (5,620) (4,632) (3,167) Issuance (retirement) of debt - - - - Cashflow from financing (7,491) (8,620) (9,632) (5,167) Changes in net cash/debt 4,671 6,172 (3,311) (1,121) Net debt at start 14,258 9,587 3,415 6,726 Change in net debt (4,671) (6,172) 3,311 1,121 Net debt at end 9,587 3,415 6,726 7,847

Balance sheet (US$ m) 12/16A 12/17E 12/18E 12/19E

Assets Total current assets 15,086 19,944 16,659 15,588 Total assets 89,263 91,748 88,755 88,239 Liabilities Total current liabilities 9,362 8,367 8,394 8,447 Total liabilities 43,533 42,538 42,565 42,618 Total equity and liabilities 89,263 91,783 88,790 88,274

Per share 12/16A 12/17E 12/18E 12/19E

No. of shares (wtd avg.) (mn) 1,797 1,768 1,692 1,624 CS EPS (adj.) (US$) 2.84 6.61 3.87 2.80 Dividend (US$) 1.70 3.42 2.27 1.65 Free cash flow per share (US$) 3.60 8.79 5.75 4.54

Key ratios and valuation 12/16A 12/17E 12/18E 12/19E

Growth/Margin (%) Sales growth (%) (3.0) 33.6 (19.5) (5.5) EBIT growth (%) 9.3 91.4 (45.1) (29.5) Net income growth (%) (5.1) 129.2 (43.9) (30.5) EPS growth (%) (3.6) 132.9 (41.4) (27.6) EBITDA margin (%) 40.0 48.5 39.3 33.0 EBIT margin (%) 25.8 37.0 25.2 18.8 Pretax profit margin (%) 19.8 35.9 24.0 17.4 Net income margin (%) 15.1 25.9 18.0 13.3

Valuation 12/16A 12/17E 12/18E 12/19E

EV/Sales (x) 2.6 1.8 2.3 2.5 EV/EBITDA (x) 6.5 3.7 5.9 7.6 EV/EBIT (x) 10.0 4.9 9.2 13.3 Dividend yield (%) 4.06 8.16 5.41 3.94 P/E (x) 14.8 6.3 10.8 14.9

Credit ratios (%) 12/16A 12/17E 12/18E 12/19E

Net debt/equity (%) 21.0 6.9 14.6 17.2 Net debt to EBITDA (x) 0.7 0.2 0.5 0.7 Interest coverage ratio (x) 8.5 34.6 20.2 13.4

Company Background

Rio Tinto Limited is engaged in minerals exploration, development, production and processing. The Company’s product groups include aluminum, copper, diamonds and minerals, energy, and iron ore.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (p) (from 4200.00) 4800.00

Our Blue Sky valuation reflects the scenario that iron ore prices remain elevated through 2018 (at above $65/tonne), Chinese intervenes in the aluminium market causing a 30% increase in prices for 12 months, and $3bn of non-core assets are sold with 100% of proceeds passed to shareholders (via buybacks / dividends)

Our Grey Sky Scenario (p) 1450.00

China hits a hard landing and iron ore prices fall below $30/tonne.

Share price performance

The price relative chart measures performance against the FTSE ALL SHARE

INDEX which closed at 4014.7 on 01/03/17

On 01/03/17 the spot exchange rate was £.86/Eu 1.- Eu.95/US$1

Source: FTI, Company data, Thomson Reuters, Credit Suisse Securities (EUROPE) LTD. Estimates

3 March 2017

Global Mining 2020 Capex 19

Americas/Canada Diversified Metals & Mining

Teck Resources Ltd (TECKb.TO) Rating OUTPERFORM [V] Price (01-Mar-17, C$) 28.08 Target price (C$) 43.00 52-week price range (C$) 35.02 - 9.08 Market cap (C$ m) 15,936.71 Target price is for 12 months.

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Ralph M. Profiti, CFA

416 352 4563

Yan Truong, CFA

416 352 4584

Strong cash flows & diversification pave the way

■ Capex outlook: Capex peaked in 2013 (at C$2.6bn) and, in an effort to protect its balance sheet in a weak commodities price environment, Teck embarked on a cost-cutting programme reducing capex by 10% pa through to 2016. During this period, production saw limited growth. With the recent recovery in metal prices (most notably coking coal), Teck is budgeting for FY17 capex of C$2.2bn (+16% YoY), of which C$1.2bn will be spent on sustaining capital and capitalised stripping – a partial catch up on previous deferrals. With the completion of Fort Hills (in late-2017) and absent a sanctioning decision at QBII, we forecast Teck's capex to normalise at ~C$1.2bn pa by 2020. From 2020, we estimate production (on a copper-equivalent basis) will decline at an average rate of -2% pa to 2030 assuming

no capex is invested into brownfield/greenfield projects (i.e. QBII).

■ To maintain production volume flat post-2020, we estimate Teck would

require capex to return to ~C$2.0bn pa, or ~8% above 2016 levels. In order

to grow volumes at an average +2% pa, we estimate capex of C$2.5bn pa

(~34% above 2016 levels) based on a copper-equivalent capex intensity of

$18,000/t. Alternatively, successful permitting and sanctioning of QBII would

offset the 2% pa production decline at a project cost of ~C$4.5bn (spent

between 2018-2022).

■ Catalysts and risks: i) China policy on coal working day restriction (mid-

March); (ii) 2Q17 benchmark HCC price settlement (April); (iii) potential for debt rating agencies to upgrade to investment grade (2H17); (iv) potential increase in dividend (2H17); and (v) completion and first oil at Fort Hills (late-

2017).

■ Investment overview and valuation: We estimate Teck is trading at an

equity-implied coking coal benchmark price of US$120/t (at US$2.60/lb

copper, US$1.25/lb zinc and CAD$0.76). While Teck shares are not immune

to volatility in spot coking coal prices, we see compelling long-term valuation

support based on cash generation and deleveraging catalysts, with potential

reflation of the steelmaking cost curve supporting coking coal prices.

Share price performance

On 01-Mar-2017 the S&P/TSX Composite closed at

15599.68

Daily Mar02, 2016 - Mar01, 2017, 03/02/16 = C$9.51

Quarterly EPS Q1 Q2 Q3 Q4 2015A 0.11 0.14 0.05 0.03 2016E 0.03 0.01 0.26 1.61 2017E 1.37 1.23 1.18 0.97

Financial and valuation metrics

Year 12/15A 12/16E 12/17E 12/18E EPS (CS adj.) (C$) 0.33 1.91 4.75 2.26 Prev. EPS (C$) - - - - P/E (x) 86.1 14.7 5.9 12.4 P/E rel. (%) 401.9 85.7 39.1 93.1 Revenue (C$ m) 8,259.0 9,300.0 12,815.8 10,745.9 EBITDA (C$ m) -872.0 3,369.0 6,125.8 3,931.3 OCFPS (C$) -1.62 5.31 9.36 6.24 P/OCF (x) -3.3 5.3 3.0 4.5 EV/EBITDA (current) -27.0 7.0 3.8 6.0 Net debt (C$ m) 7,771 6,941 4,310 2,947 ROIC (%) -6.84 5.18 12.28 6.77

Number of shares (m) 567.55 IC (current, C$ m) 24,409.00 BV/share (Next Qtr., C$) 30.3 EV/IC (x) .9 Net debt (Next Qtr., C$ m) 6,936.0 Dividend (current, C$) - Net debt/tot eq (Next Qtr.,%) 39.4 Dividend yield (%) - Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 20

Teck Resources Ltd (TECKb.TO)

Price (23 Feb 2017): C$27.29; Rating: OUTPERFORM [V]; Target Price: C$43.00; Analyst: Ralph Profiti

Income Statement 12/15A 12/16E 12/17E 12/18E

Revenue (C$ m) 8,259.0 9,300.0 12,815.8 10,745.9 EBITDA (872) 3,369 6,126 3,931 Depr. & amort. (1,366) (1,385) (1,332) (1,301) EBIT (C$) (2,238) 1,984 4,794 2,630 Net interest exp (314) (341) (440) (548) Associates (10) (10) (10) (10) Other adj. 0 0 0 0 PBT (C$) (2,562) 1,633 4,344 2,072 Income taxes 836 (587) (1,607) (767) Profit after tax (1,726) 1,046 2,737 1,305 Minorities 10 (10) 1 (3) Preferred dividends - - - - Associates & other 1,904 63 0 0 Net profit (C$) 188 1,099 2,737 1,303 Other NPAT adjustments (2,662) (63) 0 0 Reported net income (2,474) 1,036 2,737 1,303

Cash Flow 12/15A 12/16E 12/17E 12/18E

EBIT (2,238) 1,984 4,794 2,630 Net interest (314) (341) (440) (548) Cash taxes paid - - - - Change in working capital 180 (360) 0 0 Other cash & non-cash items 1,437 1,778 1,041 1,514 Cash flow from operations (935) 3,061 5,395 3,596 CAPEX (2,244) (1,912) (2,314) (1,618) Free cashflow to the firm (3,179) 1,149 3,080 1,978 Aquisitions - - - - Divestments 810 0 59 0 Other investment/(outflows) 330 74 (0) 0 Cash flow from investments (1,104) (1,838) (2,256) (1,618) Net share issue(/repurchase) 0 8 0 0 Dividends paid (395) (44) (58) (58) Issuance (retirement) of debt (448) (993) (64) (29) Other 1,217 700 (386) (529) Cashflow from financing activities 374 (329) (507) (616) Effect of exchange rates 304 (64) 0 0 Changes in Net Cash/Debt (1,361) 830 2,631 1,362 Net debt at start 6,410 7,771 6,941 4,310 Change in net debt 1,361 (830) (2,631) (1,362)

Net debt at end 7,771 6,941 4,310 2,947

Balance Sheet (C$) 12/15A 12/16E 12/17E 12/18E

Assets Cash & cash equivalents 1,888 1,402 3,969 5,303 Account receivables 1,298 1,682 1,682 1,682 Inventory 1,620 1,673 1,673 1,673 Other current assets 0 0 0 0 Total current assets 4,806 4,757 7,324 8,658 Total fixed assets 26,791 27,595 28,519 28,836 Intangible assets and goodwill 1,127 1,127 1,127 1,127 Investment securities - - - - Other assets 1,965 2,145 2,145 2,145 Total assets 34,689 35,624 39,115 40,766 Liabilities Accounts payables 1,673 2,101 2,101 2,101 Short-term debt 25 0 0 0 Other short term liabilities 28 99 99 99 Total current liabilities 1,726 2,200 2,200 2,200 Long-term debt 9,606 8,244 8,180 8,151 Other liabilities 6,719 7,584 8,460 8,892 Total liabilities 18,051 18,028 18,840 19,243

Shareholder equity 16,408 17,437 20,116 21,364 Minority interests 230 159 159 159 Total liabilities and equity 34,689 35,624 39,115 40,766 Net debt 7,771 6,941 4,310 2,947

Per share 12/15A 12/16E 12/17E 12/18E

No. of shares (wtd avg) 576 576 576 576 CS adj. EPS 0.33 1.91 4.75 2.26 Prev. EPS (C$) - - - - Dividend (C$) 0.30 0.10 0.10 0.10 Dividend payout ratio 91.95 5.25 2.11 4.42 Free cash flow per share (5.52) 1.99 5.34 3.43

Earnings 12/15A 12/16E 12/17E 12/18E

Sales growth (%) (4.0) 12.6 37.8 (16.2) EBIT growth (%) (326.7) 188.7 141.6 (45.1) Net profit growth (%) (58.4) 484.5 149.1 (52.4) EPS growth (%) (58.4) 484.3 149.1 (52.4) EBITDA margin (%) (10.6) 36.2 47.8 36.6 EBIT margin (%) (27.1) 21.3 37.4 24.5 Pretax margin (%) (31.0) 17.6 33.9 19.3 Net margin (%) 2.3 11.8 21.4 12.1

Valuation 12/15A 12/16E 12/17E 12/18E

EV/Sales (x) 2.82 2.41 1.54 1.72 EV/EBITDA (x) (26.5) 6.9 3.8 5.9 EV/EBIT (x) (10.4) 11.3 4.1 7.0 P/E (x) 83.6 14.3 5.7 12.1 Price to book (x) 1.0 0.9 0.8 0.7 Asset turnover 0.2 0.3 0.3 0.3

Returns 12/15A 12/16E 12/17E 12/18E

ROE stated-return on (%) (14.1) 6.1 14.6 6.3 ROIC (%) (0.1) 0.1 0.1 0.1 Interest burden (%) 1.14 0.82 0.91 0.79 Tax rate (%) 25.3 35.9 37.0 37.0 Financial leverage (%) 0.59 0.48 0.41 0.39

Gearing 12/15A 12/16E 12/17E 12/18E

Net debt/equity (%) 46.7 39.4 21.3 13.7 Net Debt to EBITDA (x) Net

Cash 2.1 0.7 0.7

Interest coverage ratio (X) (7.1) 5.8 10.9 4.8

Quarterly EPS Q1 Q2 Q3 Q4

2015A 0.11 0.14 0.05 0.03 2016E 0.03 0.01 0.26 1.61 2017E 1.37 1.23 1.18 0.97

Share price performance

On 23-Feb-2017 the S&P/TSX Composite closed at 15781.2

Daily Feb25, 2016 - Feb23, 2017, 02/25/16 = C$7.67

Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 21

Americas/Brazil Diversified Metals & Mining

Vale (VALE) Rating NEUTRAL [V] Price (01-Mar-17, US$) 10.69 Target price (US$) 9.00 52-week price range (US$) 11.52 - 3.54 Market cap (US$ m) 55,941.21 Enterprise value (US$ m) 73,932.09 Target price is for 12 months.

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Ivano Westin

55 11 3701 6318

Renan Criscio

55 11 3701 6210

Rafael Cunha

55 11 3701 6320

Capex on a downward path ■ Summary: The combination of lower capex, divestment of non-core assets,

cost-cutting, and current momentum for commodities prices recently contributed to an improvement in Vale's balance sheet. Net debt to EBITDA dropped to 2.1x in 4Q16 from 2.9x in 3Q16 and 3.6x in 4Q15, while the gross debt-to-EBITDA ratio moved from 4.1x in 4Q15 and 3.6x in 3Q16 to 2.4x. The ramp-up of S11D should provide additional support for deleveraging, all else equal. We estimate ND/EBITDA at 1.2x YE 2017.

■ Capex on a downward path: Vale is the only major in this report for which we expect 2020 capex to be materially below 2015-16 due to the growth expected from S11D over the next 3-4 years and capex close to conclusion. In 2020 we forecast capex of $3.6bn compared with $8.4/$5.5bn in 2015/16 and we estimate $3.6-4.0bn should be sufficient to keep volumes stable post 2020. To grow volumes at 2% pa post 2020 based on our methodology of copper-focused growth at capex intensity of $16,000/t could mean capex climbing back to the $5.5-6.0bn range, a scenario which we estimate unlikely to materialize, given our base case of no increase in copper asset base.

■ Iron ore outlook: Vale expects steel demand in 2017 to be better than 2016

whereas seaborne iron ore supply should be lower and is seeing a restocking movement from mills ahead of increasing demand in the spring. High inventories at the port are not a major concern for the company as the bulk of the ore is low quality, for which demand is lower. For 2018, Vale reinforced that it will be responsible for ~50% of the additional seaborne supply volume and will always operate with the end-goal of margin optimisation.

■ Dividends: Reduction of net debt to the USD15bn target remains the company's primary focus, but we expect dividends to be at robust levels in CY17 (CSe ~ 5% dividend yield).

■ Vale's agenda – short to mid-term: Vale mentioned the current agenda is not completed and still needs to conclude: (i) ramp-up of all projects, especially S11D, (ii) leverage reduction, (iii) shareholder restructuring at Vale, and (iv) cost reduction. Once all these projects are concluded, Vale might consider new projects that could be explored. Vale intends to increase cash return to shareholders at the right time.

Share price performance

On 01-Mar-2017 the S&P 500 INDEX closed at 2395.96

Daily Mar02, 2016 - Mar01, 2017, 03/02/16 = US$3.63

Quarterly EPS Q1 Q2 Q3 Q4 2016A - - - - 2017E - - - - 2018E - - - -

Financial and valuation metrics

Year 12/16A 12/17E 12/18E 12/19E Revenue (US$ m) 29,366.7 38,396.1 31,305.6 27,791.5 EBITDA (US$ m) 12,184.7 18,821.6 12,348.9 8,388.0 EBIT (US$ m) 8,153.7 14,262.4 7,844.2 3,823.7 Net Income (US$ m) 3,985.7 8,234.5 3,955.2 762.6 EPS (CS adj.) (US$) 0.77 1.60 0.77 0.15 Prev. EPS (US$) 0.71 1.00 0.68 0.37 Dividend yield (%) 1.0 5.3 3.6 1.4 P/E (x) 13.8 6.7 13.9 72.2 EV/EBITDA 6.6 3.9 5.5 8.0 P/B (x) 1.41 1.24 1.19 1.19 ROE stated-return on equity 11.0 19.7 8.7 1.6 ROIC (%) 9.32 16.51 9.53 4.70 Net debt (US$ m) 25,060 17,991 12,532 11,576 Net debt/EBITDA (12/16E, %) 61.1 38.4 25.5 23.4 Capex (US$ m) -5,469 -4,513 -4,504 -4,101

Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 22

Vale (VALE)

Price (01 Mar 2017): US$10.69; Rating: NEUTRAL [V]; Target Price: US$9.00; Analyst: Ivano Westin

Income Statement 12/16A 12/17E 12/18E 12/19E

Revenue (US$ m) 29,366.7 38,396.1 31,305.6 27,791.5 EBITDA 12,185 18,822 12,349 8,388 Depr. & amort. (3,834) (4,397) (4,359) (4,319) EBIT (US$) 8,154 14,262 7,844 3,824 Net interest exp (2,542) (2,866) (2,616) (2,548) Associates - - - - Other adj. 3,185 (584) (351) (365) PBT (US$) 8,797 10,812 4,878 911 Income taxes (2,151) (2,703) (1,219) (228) Profit after tax 6,646 8,109 3,658 683 Minorities 6 441 421 185 Preferred dividends - - - - Associates & other (2,666) (316) (124) (106) Net profit (US$) 3,986 8,234 3,955 763 Other NPAT adjustments 0 0 0 0 Reported net income 3,986 8,234 3,955 763

Cash Flow 12/16A 12/17E 12/18E 12/19E

EBIT 8,154 14,262 7,844 3,824 Net interest (2,542) (2,866) (2,616) (2,548) Cash taxes paid - - - - Change in working capital (1,991) (773) 704 203 Other cash & non-cash items 7,140 8,767 8,016 7,767 Cash flow from operations 10,761 19,390 13,948 9,245 CAPEX (5,469) (4,513) (4,504) (4,101) Free cashflow to the firm 5,292 14,877 9,444 5,145 Aquisitions - - - - Divestments - - - - Other investment/(outflows) 770 2,053 2,232 0 Cash flow from investments (4,699) (2,460) (2,272) (4,101) Net share issue(/repurchase) 0 0 0 0 Dividends paid (543) (2,895) (1,978) (763) Issuance (retirement) of debt (740) (353) 0 0 Other (4,577) (6,612) (4,240) (3,426) Cashflow from financing activities (5,860) (9,861) (6,217) (4,188) Effect of exchange rates - - - - Changes in Net Cash/Debt 202 7,069 5,459 956 Net debt at start 25,262 25,060 17,991 12,532 Change in net debt (202) (7,069) (5,459) (956)

Net debt at end 25,060 17,991 12,532 11,576

Balance Sheet (US$) 12/16A 12/17E 12/18E 12/19E

Assets Cash & cash equivalents 4,262 11,857 17,612 18,867 Account receivables 3,663 4,010 3,309 3,102 Inventory 3,349 4,385 4,282 4,436 Other current assets 10,930 10,930 10,930 10,930 Total current assets 22,204 31,182 36,133 37,335 Total fixed assets 55,419 55,535 56,077 56,253 Intangible assets and goodwill 6,871 6,871 6,474 6,080 Investment securities - - - - Other assets 14,157 11,626 9,125 8,774 Total assets 98,651 105,214 107,809 108,442 Liabilities Accounts payables 3,630 4,240 4,140 4,289 Short-term debt 1,660 1,660 1,660 1,660 Other short term liabilities 5,942 5,589 5,589 5,589 Total current liabilities 11,232 11,489 11,389 11,538 Long-term debt 27,662 28,188 28,484 28,783 Other liabilities 19,096 19,096 19,096 19,096 Total liabilities 57,990 58,772 58,969 59,416

Shareholder equity 39,042 44,381 46,359 46,359 Minority interests 1,982 2,423 2,845 3,029 Total liabilities and equity 99,014 105,577 108,172 108,805 Net debt 25,060 17,991 12,532 11,576

Per share 12/16A 12/17E 12/18E 12/19E

No. of shares (wtd avg) 5,153 5,153 5,153 5,153 CS adj. EPS 0.77 1.60 0.77 0.15 Prev. EPS (US$) 0.71 1.00 0.68 0.37 Dividend (US$) 0.11 0.56 0.38 0.15 Dividend payout ratio 13.62 35.16 50.00 100.00 Free cash flow per share 1.03 2.89 1.83 1.00

Earnings 12/16A 12/17E 12/18E 12/19E

Sales growth (%) 14.6 30.7 (18.5) (11.2) EBIT growth (%) 197.3 74.9 (45.0) (51.3) Net profit growth (%) 132.9 106.6 (52.0) (80.7) EPS growth (%) 132.9 106.6 (52.0) (80.7) EBITDA margin (%) 41.5 49.0 39.4 30.2 EBIT margin (%) 27.8 37.1 25.1 13.8 Pretax margin (%) 30.0 28.2 15.6 3.3 Net margin (%) 13.6 21.4 12.6 2.7

Valuation 12/16A 12/17E 12/18E 12/19E

EV/Sales (x) 2.76 1.93 2.19 2.43 EV/EBITDA (x) 6.6 3.9 5.5 8.0 EV/EBIT (x) 9.9 5.2 8.7 17.7 P/E (x) 13.8 6.7 13.9 72.2 Price to book (x) 1.4 1.2 1.2 1.2 Asset turnover 0.3 0.4 0.3 0.3

Returns 12/16A 12/17E 12/18E 12/19E

ROE stated-return on (%) 11.0 19.7 8.7 1.6 ROIC (%) 0.1 0.2 0.1 0.0 Interest burden (%) 1.08 0.76 0.62 0.24 Tax rate (%) 37.0 25.0 25.0 25.0 Financial leverage (%) 0.75 0.67 0.65 0.66

Gearing 12/16A 12/17E 12/18E 12/19E

Net debt/equity (%) 61.1 38.4 25.5 23.4 Net Debt to EBITDA (x) 2.1 1.0 1.0 1.4 Interest coverage ratio (X) 3.2 5.0 3.0 1.5

Quarterly EPS Q1 Q2 Q3 Q4

2016A - - - - 2017E - - - - 2018E - - - -

Share price performance

On 01-Mar-2017 the S&P 500 INDEX closed at 2395.96

Daily Mar02, 2016 - Mar01, 2017, 03/02/16 = US$3.63

Source: Company data, Thomson Reuters, Credit Suisse estimates

3 March 2017

Global Mining 2020 Capex 23

Companies Mentioned (Price as of 01-Mar-2017) Anglo American Plc (AAL.L, 1310.0p, NEUTRAL[V], TP 1400.0p) BHP Billiton (BLT.L, 1353.5p, NEUTRAL[V], TP 1380.0p) Fortescue Metals Group Ltd (FMG.AX, A$6.6) Glencore (GLEN.L, 337.75p, OUTPERFORM[V], TP 400.0p) Kumba Iron Ore (KIOJ.J, R222.15) Rio Tinto (RIO.L, 3406.0p, OUTPERFORM, TP 4000.0p) Teck Resources Ltd (TECKb.TO, C$28.08, OUTPERFORM[V], TP C$43.0) Vale (VALE.N, $10.69, NEUTRAL[V], TP $9.0)

Disclosure Appendix

Analyst Certification The analysts identified in this report each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for Anglo American Plc (AAL.L)

AAL.L Closing Price Target Price

Date (p) (p) Rating

31-Mar-14 1526.50 1800.00 O

15-May-14 1608.00 1850.00 N

23-Jun-14 1470.50 1800.00

10-Oct-14 1325.50 1800.00 O

15-Dec-14 1098.50 1600.00

09-Apr-15 1024.00 1400.00 N

23-Jun-15 996.70 1350.00

15-Jul-15 874.40 1350.00 O

27-Jul-15 772.60 1200.00

04-Sep-15 668.50 R

17-Sep-15 749.30 1200.00 O

22-Sep-15 648.10 900.00 N

09-Nov-15 516.00 750.00

15-Dec-15 271.10 320.00

17-Feb-16 468.05 470.00

07-Apr-16 506.10 500.00

30-Jun-16 726.90 630.00

18-Jul-16 832.00 700.00

29-Jul-16 830.50 870.00

09-Aug-16 879.00 890.00

19-Sep-16 860.90 950.00

14-Oct-16 1006.00 970.00

17-Nov-16 1126.50 1300.00

07-Dec-16 1252.00 1400.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

REST RICT ED

3 March 2017

Global Mining 2020 Capex 24

3-Year Price and Rating History for BHP Billiton (BLT.L)

BLT.L Closing Price Target Price

Date (p) (p) Rating

13-Mar-14 1668.56 2097.36 N

19-Aug-14 1831.69 1864.32 U

14-Oct-14 1572.09 1864.32 N

26-Nov-14 1496.58 1724.49

09-Apr-15 1354.43 1305.02 U

16-May-15 1429.00 1350.00

24-Jun-15 1373.50 1350.00 N

21-Sep-15 1076.00 1250.00

21-Oct-15 1096.50 1350.00

10-Nov-15 946.50 1100.00

15-Dec-15 686.90 900.00 O

14-May-16 822.80 1050.00

18-Jul-16 976.80 1150.00

20-Jul-16 926.40 1050.00

19-Sep-16 1022.50 1150.00

13-Oct-16 1184.00 1300.00

07-Dec-16 1362.00 1380.00 N

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

U N D ERPERFO RM

O U T PERFO RM

3-Year Price and Rating History for Glencore (GLEN.L)

GLEN.L Closing Price Target Price

Date (p) (p) Rating

05-Mar-14 330.51 397.97 O

31-Mar-14 307.23 378.07

14-Aug-14 358.82 378.07 N

15-Dec-14 278.58 338.27

02-Mar-15 299.02 338.27 O

09-Apr-15 287.38 318.38

23-Jun-15 274.90 310.00

11-Aug-15 191.00 235.00

22-Sep-15 106.35 175.00

10-Dec-15 88.90 R

16-Dec-15 84.35 130.00 O

02-Mar-16 135.40 155.00

06-Apr-16 140.10 R

09-Jun-16 145.70 155.00 O

30-Jun-16 152.85 160.00

18-Jul-16 186.40 200.00 N

09-Aug-16 195.95 210.00

19-Sep-16 196.50 220.00 O

14-Oct-16 228.25 250.00

10-Nov-16 285.00 300.00

02-Dec-16 277.90 320.00

07-Dec-16 296.75 340.00

30-Jan-17 321.55 380.00

24-Feb-17 327.50 400.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

REST RICT ED

3 March 2017

Global Mining 2020 Capex 25

3-Year Price and Rating History for Rio Tinto (RIO.L)

RIO.L Closing Price Target Price

Date (p) (p) Rating

31-Mar-14 3337.50 4200.00 O

23-Jun-14 3127.00 4000.00

24-Nov-14 2976.50 3600.00

15-Dec-14 2616.50 3400.00

12-Feb-15 3039.50 3400.00 N

09-Apr-15 2852.50 2800.00

21-Sep-15 2274.50 2500.00

04-Nov-15 2370.50 2400.00

15-Dec-15 1879.50 2100.00

18-Jul-16 2462.50 2300.00

03-Aug-16 2423.00 2100.00

19-Sep-16 2359.00 2300.00

14-Oct-16 2596.00 2750.00

07-Dec-16 3221.50 3600.00 O

08-Feb-17 3377.50 4000.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

3-Year Price and Rating History for Teck Resources Ltd (TECKb.TO)

TECKb.TO Closing Price Target Price

Date (C$) (C$) Rating