section ii t c port sector - cc · in march 1990, law nbr. 18,032 was superseded by law nbr....

TRANSCRIPT

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

10

Dresdner Kleinwort BensonSouth Andes Ltda.

2.1 Background

In 1960, the Chilean Government created Empresa Portuaria de Chile or “EMPORCHI”, an autonomous state body responsible for the management, exploitation and preservation of the system of publicly-owned ports. By 1997 EMPORCHI owned the assets of the State’s ten principal commercial ports: Arica, Iquique, Antofagasta, Coquimbo, Valparaíso, San Antonio, Talcahuano-San Vicente, Puerto Montt, Chacabuco and Punta Arenas.

While EMPORCHI was responsible for the development of the state-owned ports, the private sector also began to build and operate new terminals, in particular to meet the import and export requirements of developing industries, such as forestry, mining and petrochemicals.

The speed of development of ship design, in particular in terms of ship size, rapidly made Chile’s port facilities inadequate. This problem was exacerbated by the considerable growth of trade that resulted from Chile’s economic policies in the 1970s. Consequently, by the late 1970s, there was an urgent need to modernise the Chilean port system.

In 1981 the government implemented a new policy (through law Nbr. 18,032) focused on improving existing labour practices and introducing competitive practices in stevedoring. EMPORCHI was obliged to abandon cargo handling operations on land, and private associations of stevedores were allowed to perform these tasks. This permitted EMPORCHI’s ports to increase throughput considerably, even with the limited investments made in infrastructure since that time.

In March 1990, law Nbr. 18,032 was superseded by law Nbr. 18,966, which established that EMPORCHI could neither load or unload ships, nor could it store or transport cargo between vessels and warehouses, leaving those activities to the private sector.

2.2 Industry structure

The following chart summarises the main forces interacting in the sector.

Entry Barriers

Substitutes

Customers SuppliersNatural barriers, expertise, capital requirements

Air, roads, railways

Export/importcompanies

Transportcompanies

Shipping lines

Shippingagencies

Governmentregulators

LocalCommunities

Constructioncompanies

Equipmentproviders

Workforce

Stevedoringcompanies

Tugboatcompanies

Competition within

the industry

Privately-owned ports for public use

Privately-owned ports for private use

State-owned ports for public use

Figure 2.1: Industry structure

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

11

Dresdner Kleinwort BensonSouth Andes Ltda.

2.2.1 Competition within the industry

There are 35 ports along the Chilean coast, of which 24 are privately-owned and the remainder state-owned. These ports can be categorised as follows:

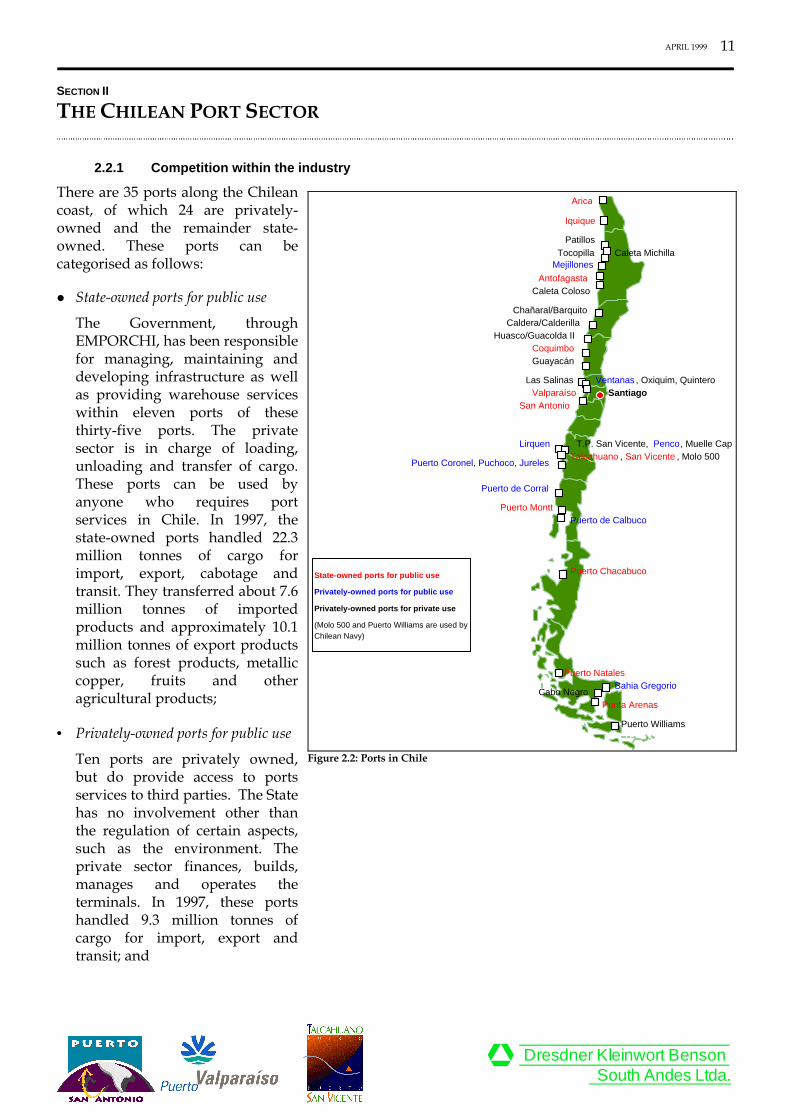

� State-owned ports for public use

The Government, through EMPORCHI, has been responsible for managing, maintaining and developing infrastructure as well as providing warehouse services within eleven ports of these thirty-five ports. The private sector is in charge of loading, unloading and transfer of cargo. These ports can be used by anyone who requires port services in Chile. In 1997, the state-owned ports handled 22.3 million tonnes of cargo for import, export, cabotage and transit. They transferred about 7.6 million tonnes of imported products and approximately 10.1 million tonnes of export products such as forest products, metallic copper, fruits and other agricultural products;

• Privately-owned ports for public use

Ten ports are privately owned, but do provide access to ports services to third parties. The State has no involvement other than the regulation of certain aspects, such as the environment. The private sector finances, builds, manages and operates the terminals. In 1997, these ports handled 9.3 million tonnes of cargo for import, export and transit; and

Arica

Iquique

PatillosCaleta MichillaTocopilla

Mejillones

AntofagastaCaleta Coloso

Chañaral/BarquitoCaldera/Calderilla

Huasco/Guacolda IICoquimboGuayacán

Las Salinas

San AntonioValparaíso

Ventanas , Oxiquim, QuinteroSantiago

T.P. San Vicente, Penco, Muelle CapLirquenTalcahuano , San Vicente , Molo 500

Puerto Coronel, Puchoco, Jureles

Puerto de Corral

Puerto MonttPuerto de Calbuco

Puerto Chacabuco

Puerto NatalesBahia Gregorio

Punta ArenasCabo Negro

Puerto Williams

State-owned ports for public use

Privately-owned ports for public use

Privately-owned ports for private use

(Molo 500 and Puerto Williams are used bytheChilean Navy)

Figure 2.2: Ports in Chile

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

12

Dresdner Kleinwort BensonSouth Andes Ltda.

• Privately-owned ports for private use

The remaining fourteen terminals have been constructed by private sector companies for their own operations. In general, third parties are not allowed to use the services at these terminals. These ports handled 21.1 million tonnes of cargo for import, export and transit in 1997.

The main imported products handled by the privately-owned ports, for both public and private use, are solid and liquid bulk, fertilisers, and chemicals. The principal export products transferred through privately-owned ports included ores, other metal products, forest products and fertilisers.

Although there are these three distinct sets of ports in Chile, only state-owned ports and privately-owned ports for public can be considered to be direct competitors for market share. This competition is principally in evidence in the II, V and VIII Regions, where a total of five state-owned ports and seven privately-owned ports for public use compete.

The following graph shows the market share of state-owned ports and privately-owned ports for public use in terms of cargo handled in Chile in 1997.

Chilean port systemCargo hand led in 1997

State-owned ports/ public use

71%

Privately-owned ports/ public use

29%

Source: DIRECTEMAR and EMPORCHI

The globalisation of the economy, materialised by international trade agreements signed by the Chilean Government, generates increasing business. Appendix B - Trading overview - gives an insight into the trends of Chilean foreign trade and its increasing number of trading partners. Foreign trade volume is expected to experience significant growth helped by the development of bi-oceanic corridors, with Chile also representing an ideal platform for trade between South America and the Far East as well as the other countries of the Pacific basin (e.g. Canada, U.S., Mexico, Central American countries, Australia and New Zealand).

Below is a breakdown of tonnage transferred through Chilean ports by destination of cargo in 1997. The subsequent map shows in detail the most commonly used maritime routes to and from Chile.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

13

Dresdner Kleinwort BensonSouth Andes Ltda.

Table 2.1: Cargo traffic by destination

Destination Tonnage transferred (million tonnes)

Far East 16.9

USA (Pacific Coast, Atlantic Coast, and Gulf Coast) 9.1

Northern Europe 5.3

South America (West Coast) 3.3

South America (East Coast) 3.2

Rest of the World 13.2

Total 51.0

Source: Cámara Marítima y Portuaria de Chile A.G.

Durban

Luanda

Capetown

Rio de JaneiroSantos

MontevideoBuenos Aires

Paranagua

Punta Arenas

TalcahuanoSantiago

Valparaíso

AntofagastaIquiqueArica

Callao

GuayaquilEsmeralda

Puerto Rico

Los Angeles

Philadelphia

Panama

Houston

New YorkNorfolkKuwait

Bergen

Liverpool

Helsinki

HamburgRotterdam

Hong Kong

Singapore

Regular routes of Chilean shipping lines

Regular routes for transit withforeign shipping lines

Legend

Yokohama

Nagoya

Pusan

Kobe

Keelung

Pto. Covadonga

Charleston

Miami

Savannah

Puerto Cortés

Veracruz

La Guaira

NaplesGenoa

Stockholm

Valencia

Bilbao

MarseillesAntwerp

Figure 2.3: Maritime routes Source: Instituto Geográfico Militar, Chile, 1998

As a result of Chile’s openness towards foreign trade and investment, exports have steadily grown from US$4 billion in 1984 to US$17 billion in 1997. Currently, exports account for 25 per cent. of Chile’s GDP.

Imports reached US$18 billion in 1997, meaning Chile has the highest level (US$) of imports per capita of all Latin America countries. This expansion of Chilean foreign trade has important implications for the development of the transportation system.

Geographic location plays an important role in the Chilean transport system and therefore has a significant impact on its economy. More than 90 per cent. of Chilean foreign trade is performed through ports. This level can be expected to broadly remain constant, since other means of transportation only compete efficiently with the service offered by ocean shipping only for certain types of cargo.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

14

Dresdner Kleinwort BensonSouth Andes Ltda.

13,514

21,771

13,968

26,737

14,509

27,546

18,159

29,528

18,547

30,144

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

'000

tonn

es

1993 1994 1995 1996 1997

Foreign Trade: Volume handled by Chilean ports

Imports

Exports

Source: Cámara Marítima y Portuaria de Chile A.G.

2.2.2 Entry barriers

There are four significant barriers to entry to the Chilean ports sector:

� geographical limitations of the Chilean coastline;

� initial capital expenditure requirements;

� ongoing maintenance and development expense; and

� experience in port operations

A number of natural and geographical barriers limit the development of new ports in Chile. The main impediment is the low number of naturally-protected bays and sheltered waters with the potential to be developed into profitable port operations.

The extent of capital expenditure requirements, already high for port infrastructure, is exacerbated in Chile by the history of seismic activity, with significant additional construction necessary in order to ensure the viability of port facilities. Additional capital expenditure may also be required in order to comply with environmental standards, with both local communities and regulatory bodies able to exert influence over the port industry.

Maintenance of the port assets is critical to ensure their efficient operation and ability to meet the growing demand from increasing trade. In order to remain competitive, port operations will require continuing investment in modern technology.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

15

Dresdner Kleinwort BensonSouth Andes Ltda.

2.2.3 Substitutes

The alternatives to ports for the transfer of cargo are mainly:

� air;

� road; and

� railway.

Air cargo is usually only economically efficient for low volumes of perishable or high value goods.

With the Andes acting as a natural barrier, road and railway systems are limited in terms of quality, reliability and cost. Although there are several roads to Argentina through the Andes, even the most reliable of routes, the Libertadores Tunnel (north-east of Santiago), is commonly closed in times of heavy mountain snowfalls.

Recently, due to the economic reforms applied by neighbour countries, foreign trade within the Southern Cone of South America has significantly increased. Consequently, both Chile and Argentina will consider improving existing routes and opening new ones through the Andes.

The longest highway in Chile is the Pan-American Highway, stretching from Panama (Central America) to Puerto Montt in the south of Chile. The physical barriers constituted by rainforest and the Andes in the northern part of Latin America limits the efficiency of cross-border transportation by road. In Chile, a number of sections of the Pan-American Highway have recently been concessioned to private operators.

A lack of investment in recent years has generally characterised the railway network in Chile. The network can not be considered well developed and does not cover a significant part of the Chilean territory. The majority of the cargo railways are concessioned to private operators, such as Ferrocarriles del Pacífico S.A. (FEPASA) and Ferrocarriles del Norte S.A.(FERRONOR).

2.2.4 Customers

Chilean exporters and importers have limited bargaining power dependent on their geographical location and type of cargo.

However, large customers, such as integrated forestry product companies and fruit exporters produce sufficient volumes to negotiate charter freights.

2.2.5 Suppliers

Prior to 1981, labour unions had strong influence over human resources policy in the ports, particularly regarding, work rules, recruitment, compensation and other contractual terms. The restructuring of the port industry at the beginning of the 1980’s eliminated much of the power of the unions, thereby significantly reducing the workers’ bargaining power in labour negotiations. The existence of numerous private associations of port workers and of competition between these associations has further contributed to reduction in labour influence.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

16

Dresdner Kleinwort BensonSouth Andes Ltda.

Through their ability to establish regulations, government bodies and local communities are also important players in the Chilean ports industry.

2.3 Key Competitors: Ports in V and VIII Regions

In the V and VIII Regions, the key competitors to the former EMPORCHI ports are the privately-owned ports for public use. These main competitors are briefly described below.

Puerto Ventanas (V Region)

Puerto Ventanas S.A. is a private sector company responsible for the administration and operation of the Port of Ventanas facilities at Quintero Harbour, in the V Region. Puerto Ventanas is located 41 km north of Valparaíso, and 160 km from Santiago. The facilities consist of a finger type pier with four berths. Berths Nbr. 1, Nbr. 3 and Nbr. 5 on the North side have a maximum draft of 8.2m, 11.5m and 14.3m respectively. Berth Nbr. 2 on the south side has an average draft of 9.5m. Berths Nbr. 1 and Nbr. 2 are 164.2m long. Berth Nbr. 3 is 180m long and berth Nbr. 5 is 84m long. Its services are mainly the loading, unloading, transfer, portage and storage of bulk cargo.

In 1997, Ventanas handled 2,496,000 tonnes of cargo. However, 34 per cent. of this cargo was coal for an electricity generator, GENER, which is also the controlling shareholder of Ventanas. This coal is used in the thermo-electric plant owned by GENER, located alongside the port, effectively representing captive demand.

Compañía Puerto Coronel (VIII Region)

The Port of Coronel is located in the bay of Coronel in the Gulf of Arauco. The location provides a protected bay, an acceptable draft, and availability of space for landside facilities, storage units, collecting yards and access ways.

The port consists of a single pier with two berths; a 336m long, 10m wide access bridge connected to a 172m long, 31m wide sea end of the dock. The maximum draft is equal to 12.8m. Coronel is primarily used for the export of forestry products and fishmeal.

Puerto Coronel has development projects currently under consideration, including the future expansion of its existing terminal and the construction of a second terminal.

Puerto Lirquén (VIII Region)

The Port of Lirquén is Chile's largest privately-owned port, located in the bay of Concepción. It is able to handle most types of cargo, but is principally used for the transfer of fertilisers and forestry products such as pulp, logs and lumber.

The port includes two piers, of which one is 615m long with four berths and a draft of 12.5m and the other 712m long with two berths and with a draft of 16.1m. Under a development plan currently under consideration this quay would be lengthened by an additional 234m to provide two more berths.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

17

Dresdner Kleinwort BensonSouth Andes Ltda.

The following table shows the volume of cargo handled by these three ports in 1997:

Table 2.2: Cargo transferred by Coronel, Lirquén and Ventanas (‘000 tonnes)

Port 1993 1994 1995 1996 1997 1998

Puerto Coronel - - - 313 1,098 907

Puerto Lirquén 2,305 2,717 2,543 2,745 2,429 2,130

Puerto Ventanas* 650 558 772 1,328 1,590 1,412

Total 2,955 3,275 3,315 4,386 5,117 4,449

Year on year change 10.8 1.2 32.3 16.7 -13.0 Source: Puerto Coronel, Puerto Lirquén, Puerto Ventanas * Excluding the coal transferred to GENER

2.4 Main users

The principal users of port services in Chile are:

� full service companies generally composed of a shipping line, a shipping agency and a stevedoring company

� international shipping lines and integrated companies

� smaller independent stevedoring companies and agencies

� large exporters and importers of goods, such as forestry products and mining companies

Set out below are some summary details of the principal users of Chilean ports.

Chilean companies

A.J. Broom y Cía. S.A.C./Portuaria Andes

A.J. Broom is a Chilean shipping agency providing the following services: chartering and brokerage, intermodal services, ship chandling in all Chilean ports. It has established its own stevedoring company and a company specialised in handling containers (repairing equipment and storage). It has offices with local partners in Ecuador, Bolivia, Perú and Argentina. It owns, in conjunction with Maersk, the stevedoring company Portuaria Andes which mainly operates in the ports of Valparaíso and San Antonio.

Compañía Sudamericana de Vapores (CSAV) / Sudamericana Agencias Aéreas y Marítimas (SAAM)

CSAV is a local shipping company, which has established itself as a regional carrier that covers many of the routes between South America and the rest of the world. It operates with an average of 50 ships and is actively involved in the general cargo, bulk, reefer and vehicle markets.

An intermodal service has been established by the Company, as well as other operations which complement its core activities, such as the management of storage areas and pier services. This "one-stop-shop" service, to any destination, is generally implemented in combination with CSAV's principal

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

18

Dresdner Kleinwort BensonSouth Andes Ltda.

subsidiaries: the shipping agency, Sudamericana Agencias Aéreas y Marítimas S.A. (SAAM), and COSAN, a container terminal situated in Santiago.

Empresas Navieras (CCNI/AGUNSA/Cabo Froward)

CCNI, AGUNSA and Cabo Froward are all subsidiaries of one of Chile’s three large maritime groups, Empresas Navieras S.A.

CCNI is the group’s shipping line, offering regular services, for both general and bulk cargo, from South America’s West Coast countries to the rest of the World.

AGUNSA, the holding company’s local shipping agency, has branch offices in each of the main Chilean ports. The company has expanded overseas, with investments in shipping agencies in Argentina, Perú, Colombia, Ecuador and Brazil.

The third subsidiary, Portuaria Cabo Froward, owns and operates ports. At present it controls two piers for loading wood chips on the northern side of Coronel Bay in the VIII Region.

Enseporpa Ltda./Enseporpa S.A.

Established in 1910, Enseporpa’s operations are principally in the Port of San Antonio, specialised in dry bulk activities.

The most relevant services provided by Enseporpa are stevedoring, storage and packaging of dry bulk products.

Ian Taylor

Ian Taylor is a shipping agency with offices in each of Chile’s main ports. It also has established offices in Perú (Callao and Lima), offering a wide range of services such as chartering, stevedoring, tallying, ship operating and tug and launch services.

Ian Taylor represents the following shipping companies: Polameriaca Joint Stick, Naviera Universal (Uniline), Hyundai Merchant Marine Co., Scaldis Reefer Chartering NV, Seatrade Parcel Service and ZIM Israel Navigation Co.

Jorge Carle y Cia.

Jorge Carle was established in 1974. It mainly operates in the Ports of San Antonio, Valparaíso and Coquimbo as a shipping agency and a stevedoring company.

Marítima de Valparaíso Chile S.A. (MARVAL)

MARVAL is a private company mainly focused on shipping activities related to liner and bulk services, covering the main Chilean ports.

The company was established in 1989. The most relevant services provided by MARVAL at Chilean ports can be summarised as follows: ocean freight, chartering, stevedoring, shipping agency, container terminal services and launch services. Additionally, it represents the following shipping companies: Seabord Marine Ltd., Consorcio Naviero de Occidente, Coastal Petroleum N.V. and Empremar.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

19

Dresdner Kleinwort BensonSouth Andes Ltda.

Pormar S.A.

Pormar S.A. was established in 1989. It mainly operates in the Port of San Antonio as a shipping agency, stevedoring company, multimodal operator and container terminal operator. Additionally, it provides storage services, consolidation and deconsolidation of products and containers, as well as stacking of a wide range of products. It annually serves approximately 100 ships, including container ships, car carriers and general cargo ships and handles annual total cargo of around 500,000 tonnes in the Port of San Antonio.

Sociedad Naviera Ultragas Ltda./ Transmares/Ultramar Agencia Marítima Ltda./Ultraport

This Chilean group includes two shipping lines (Ultragas and Transmares), one shipping agency (Ultramar) and a stevedoring company (Ultraport).

It provides the following services: port agents for foreign and national flag carriers, inland haulage, stevedoring, port facilities and equipment for the handling of all cargo types, in-port stacking facilities, tugboat services, crew support services, ship chandlers and warehousing of dry and refrigerated cargoes.

SOMARCO

SOMARCO is a local shipping agency initially focused on the shipping business, but later the company diversifying into an integrated range of maritime services. Today, it has contracts with several companies, most of them copper mines (it operates the bulk terminal of the mining company, Disputada de Las Condes, which is located in San Antonio) to operate dedicated terminals. It also operates tugboats.

Foreign companies

COSCO (China Ocean Shipping Company)

COSCO group is a Chinese conglomerate with shipping as its core business as well as other activities such as shipping agency, freight forwarding, terminals and warehousing, trade, industry, financial services, insurance and real estate. It has established representative offices in 38 countries or regions of the world, and has its own agents in 1,100 ports in 150 countries around the world.

COSCO Pacific, COSCO’s subsidiary, is mainly involved in the container leasing and terminal operation. The company is also a shareholder of container terminals in Shanghai, Qingdao, Zhangjiagang and Yantian.

Gearbulk

Gearbulk is a United Kingdom shipping line specialising in forestry and non-ferrous metal transport and operating open hatch gantry craned ships. The ships are designed and equipped to transport unitised cargoes, generally consisting of forest products (principally wood pulp, newsprint and different type of paper and paperboard) and non-ferrous metals (principally aluminium, copper, lead and zinc). The fleet operates primarily under one to ten years contracts of affreightment. In addition, Gearbulk charters conventional and semi-open hatch ships for short and medium term use.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

20

Dresdner Kleinwort BensonSouth Andes Ltda.

Hamburg Süd - Columbus Line

Since its constitution in 1871, the Hamburg Süd Shipping Group has developed into a world-wide marine transport and logistic management organisation, currently with a fleet of 66 ships, specialising in Northern/Southern traffic.

J. Lauritzen

J. Lauritzen A/S is a Danish shipping company operating globally. Its principal services are reefer operations, LPG and petrochemical gas distribution and bulk carriers operations (through Lauritzen Reefers and Lauritzen Kosan Tankers). Lauritzen Reefers' main business is the frozen transportation of perishable commodities such as fruit, vegetables, meat, fish and dairy products. In addition, it has interests in terminals and land transportation companies throughout South America.

Kawasaki Kisen Kaisha, Ltd. (“K” Line)

“K” Line was established in 1919 and is now one of Japan’s premier marine transportation companies. The worldwide liner service network of “K” Line concentrates on North American, European, and intra-Asia routes, while its bulk carrier services focus on the transportation of iron ore and coking coal for steel production. It also runs vehicle transport services, transferring more than 1.1 million vehicles annually.

Grupo Libra

Grupo Libra is a Brazilian conglomerate with businesses covering most of the maritime sector. The group operates a shipping line, a shipping agency and a stevedoring company.

With a fleet of more than twenty ships - either owned, chartered or operated in consortium - Grupo Libra provides both regular liner services and weekly container services in the trade between Brazil and other countries of the Americas, as well as between Brazil and Europe.

Since 1995, it has been operating container terminals in the Port of Santos (Terminal 37) and in the Port of Rio de Janeiro (TECON 1).

Mediterranean Shipping Co. (MSC)

MSC is one of the largest shipping lines in the world, serving five continents and calling at 112 ports.

Maersk / A.P. Moeller Group

Maersk Line is part of the A.P. Moeller Group with headquarters in Copenhagen, Denmark. The A.P. Moeller fleet comprises about 150 ships with a total dead-weight tonnage of about 7 million tonnes which include container ships, bulk, tankers and special ships, supply ships and drilling rigs. The A.P. Moeller group is also engaged in logistics, and offers a full range of logistic solutions from simple consolidation to management of the entire supply chain.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

21

Dresdner Kleinwort BensonSouth Andes Ltda.

NYK Sudamerica

Nippon Yusen Kabushiki Kaisha (NYK Line) is an integrated intermodal transporter and has more than 400 ships serving ports around the world.

P & O Nedlloyd/Agencia Marítima Nedlloyd Chile

P&O Nedlloyd is a global container shipping company, that resulted from the merger of P&O Containers Ltd. of London and Nedlloyd Lines B.V. of Rotterdam.

It operates a global network of 77 trade lanes connecting more than 250 main ports plus a larger number of additional ports through other feeder services. It has a fleet of 112 owned and chartered ships, and controls 540,000 owned and leased containers.

Transportadora Marítima Mexicana

Transportadora Marítima Mexicana is a Mexican shipping line. Historically a shipping line, the company offers today a multimodal transport service, including railway, road and sea transport. There are three specialised services where it is especially active: refrigerated cargo, liquid cargo and car carriers.

APRIL 1999

SECTION II

THE CHILEAN PORT SECTOR

22

Dresdner Kleinwort BensonSouth Andes Ltda.

2.5 Current tariff structure

The tariff structure currently in force at the State ports will soon change as envisaged by the terms of Concession Process. This current structure and the associated charges are set out below:

TARIFFTARIFFTARIFFTARIFFState-owned ports

EMPRESA PORTUARIA

Use of Infrastructure

DIRECTEMAR

Lighting and pilotage services

STEVEDORING

COMPANIES

- US$ amount per metre of ship per hour;

- US$ amount per metric tonne of cargo; and

- US$ amount per metric tonne of cargo and per day

(or per cubic metre and per day) for storage.

- a tariff for the transfer from the ship to the quay; and

- a tariff for the transport from the quay

to the storage areas or to the exit of the portTransfer of cargo

TUGBOAT COMPANIES

Figure 2.4: Current port tariff structure

Tariffs currently charged at the state-owned ports are as follows:

Table 2.5: Current Port Companies’ tariffs

Port

Ship tariff

(US$ per metre of ship per hour of stay)

General cargo tariff

(US$ per tonne of cargo transferred)

Bulk tariff

(US$ per tonne of cargo transferred)

Arica 0.40 1.35 0.84

Iquique 0.35 1.35 0.92

Antofagasta 0.70 1.98 1.12

Coquimbo 0.35 0.77 0.51

Valparaíso 0.75 1.97 1.35

San Antonio 0.75 1.97 1.41

Talcahuano 1.40 1.25 1.41

San Vicente 1.50 1.25 1.41

Puerto Montt 0.35 0.55 0.34

Chacabuco 0.45 0.55 0.34

Punta Arenas 0.45 1.24 0.78

Source: EMPORCHI