section 4a the power of compounding pages 210-222

TRANSCRIPT

Section 4ASection 4AThe Power of The Power of CompoundingCompoundingPages 210-222Pages 210-222

4-A

4-A

ExampleExample4-A

4-A

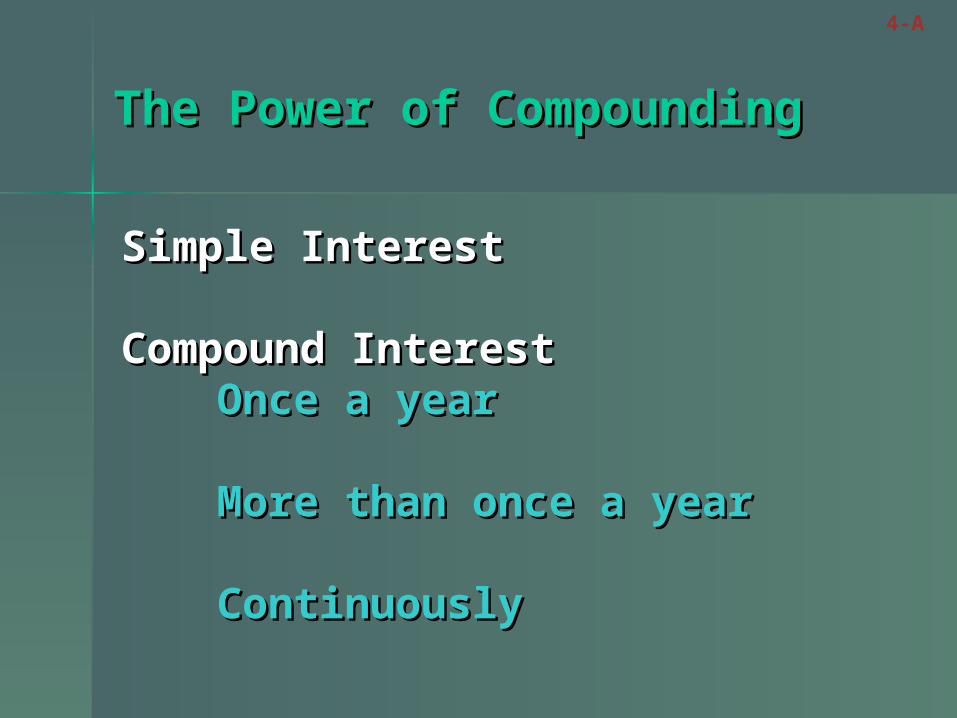

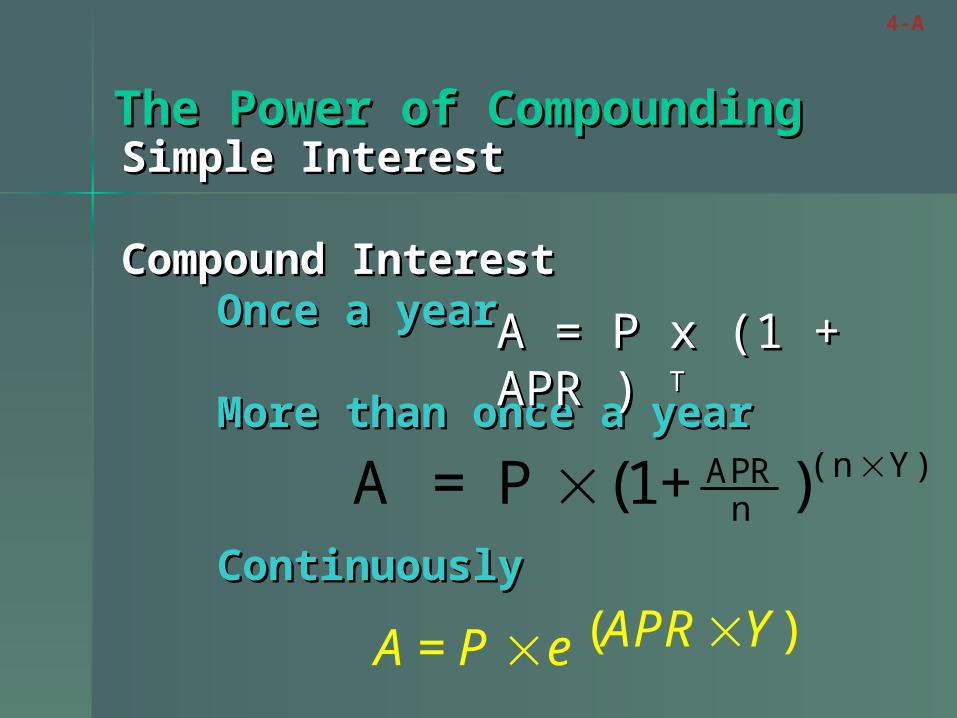

The Power of The Power of CompoundingCompounding

Simple InterestSimple Interest

Compound InterestCompound InterestOnce a yearOnce a year

More than once a yearMore than once a year

ContinuouslyContinuously

4-A

DefinitionsDefinitions

The The principal in financial formulas is the in financial formulas is the initial amountinitial amount upon which interest is paid. upon which interest is paid.

Simple interest is interest paid only on is interest paid only on the original principal, and not on any the original principal, and not on any interest added at later dates.interest added at later dates.

Compound interest is interest paid on is interest paid on both the original principal and on all both the original principal and on all interest that has been added to the original interest that has been added to the original principal.principal.

4-A

35/225 Yancy invests $500 in an account that 35/225 Yancy invests $500 in an account that earns earns simple interestsimple interest at an annual rate of 5% at an annual rate of 5% per year. Make a table that shows the per year. Make a table that shows the performance of this investment for 5 years. performance of this investment for 5 years.

Principal Time (years)

Interest Paid Total

$500$500 0 $0$0 $500$500

$500$500 1 (500x.05)=$2(500x.05)=$255

$525$525

$500$500 2 $25$25 $550$550

$500$500 3 $25$25 $575$575

$500 $500 4 $25$25 $600$600

$500$500 5 $25$25 $625$625

4-A

Principal

Time (years

)

Interest Paid Total

$500$500 0 $0$0 $500$500

$500$500 1 (500x.05) = $25(500x.05) = $25 $525$525

$525$525 2 (525 x .05)= $26.25(525 x .05)= $26.25 $551.25$551.25

$551.2$551.255

3 (551.25 x .05)= (551.25 x .05)= $27.56$27.56

$578.81$578.81

$578.8$578.811

4 (578.81 x .05) = (578.81 x .05) = $28.94$28.94

$607.75$607.75

$607.7$607.755

5 (607.75 x .05) = (607.75 x .05) = $30.39$30.39

$638.14$638.14

35/225 Samantha invests $500 in an account 35/225 Samantha invests $500 in an account with with annual compoundingannual compounding at a rate of 5% per at a rate of 5% per year. Make a table that shows the year. Make a table that shows the performance of this investment for 5 years. performance of this investment for 5 years.

4-A

Time (years)

TotalSimple

TotalCompoun

d

00 $500$500 $500$500

11 $525$525 $525$525

22 $550$550 $551.25$551.25

33 $575$575 $578.81$578.81

44 $600$600 $607.75$607.75

55 $625$625 $638.14$638.14

35/225 Compare Yancy’s and 35/225 Compare Yancy’s and Samantha’s balances over a 5 year Samantha’s balances over a 5 year period.period.

The POWER OF COMPOUNDING!The POWER OF COMPOUNDING!

4-A

A general formula for compound A general formula for compound interestinterest

4-A

Year 1: new balance is 5% more than old balance Year1 = Year0 + 5% of Year0

Year1 = 105% of Year0 = 1.05 x Year0

Year 2: new balance is 5% more than old balance Year2 = Year1 + 5% of Year1 Year2 = 105% of Year1 Year2 = 1.05 x Year1 Year2 = 1.05 x (1.05 x Year0) = (1.05)2 x Year0

Year 3: new balance is 5% more than old balance Year3 = Year2 + 5% of Year2 Year3 = 105% of Year2 Year3 = 1.05 x Year2 Year3 = 1.05 x (1.05)2 x Year0 = (1.05)3 x Year0

Balance after year T is Balance after year T is (1.05)(1.05)TT x x Year0Year0

Time (years)

Accumulated Value

0 $500$500

1 1.05 x 500 = $5251.05 x 500 = $525

2 (1.05)(1.05)2 2 x 500 = $551.25x 500 = $551.25

3 (1.05)(1.05)3 3 x 500 = $578.81x 500 = $578.81

4 (1.05)(1.05)4 4 x 500 = $607.75x 500 = $607.75

5 (1.05)(1.05)5 5 x 500 = $638.15x 500 = $638.15

10 (1.05)(1.05)1010x 500 = $814.45x 500 = $814.45

35/225 Samantha invests $500 in an account 35/225 Samantha invests $500 in an account with with annual compoundingannual compounding at a rate of 5% per at a rate of 5% per year. Make a table that shows the year. Make a table that shows the performance of this investment for 5 years. performance of this investment for 5 years.

4-A

Compound Interest Compound Interest FormulaFormula

(for interest paid once a year)(for interest paid once a year)

4-A

A = accumulated balance after T years P = starting principal i = interest rate (as a decimal) T = number of years

A = P x (1 + i ) T

4-A

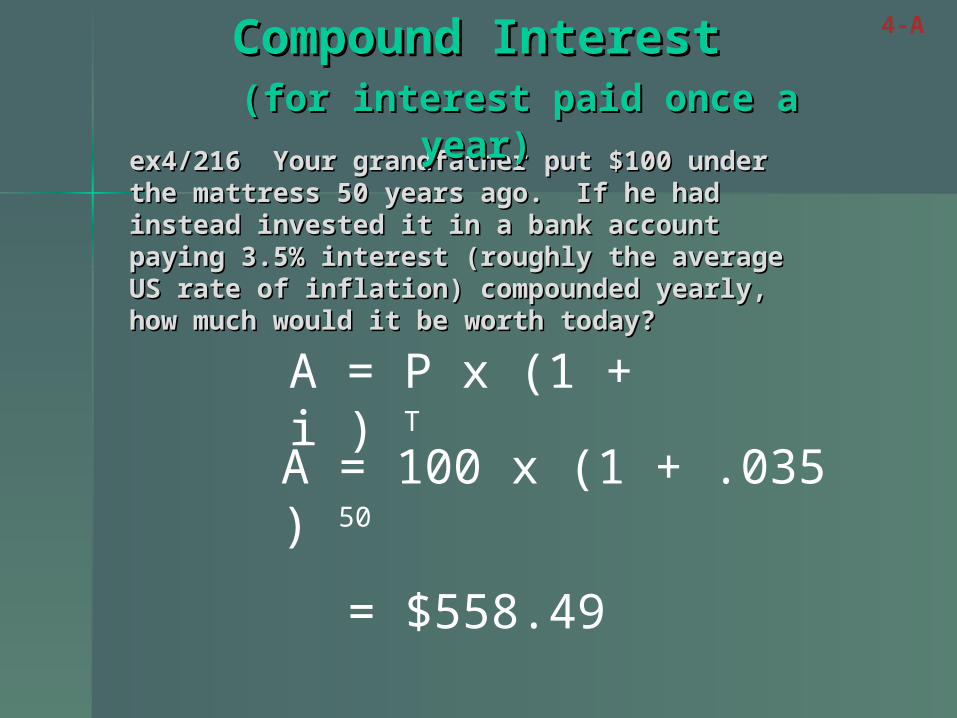

ex4/216 Your grandfather put $100 under ex4/216 Your grandfather put $100 under the mattress 50 years ago. If he had instead the mattress 50 years ago. If he had instead invested it in a bank account paying 3.5% invested it in a bank account paying 3.5% interest (roughly the average US rate of interest (roughly the average US rate of inflation) compounded yearly, how much inflation) compounded yearly, how much would it be worth today? would it be worth today?

A = P x (1 + i ) T

A = 100 x (1 + .035 ) 50

= $558.49

Compound InterestCompound Interest (for interest paid once a year)(for interest paid once a year)

4-A

pg 221 Suppose you have a new baby and pg 221 Suppose you have a new baby and want to make sure that you’ll have $100,000 want to make sure that you’ll have $100,000 for his or her college education in 18 years. for his or her college education in 18 years. How much should you deposit now at an How much should you deposit now at an interest rate of 7% compounded annually? interest rate of 7% compounded annually?

Planning Ahead with Planning Ahead with Compound InterestCompound Interest

A = P x (1 + i ) A = P x (1 + i ) TT

100000 = P x (1 + .07 ) 100000 = P x (1 + .07 ) 1818

100000/(1.07)100000/(1.07)1818 = P = P $29,586 = P $29,586 = P

ExampleExample4-A

Compounding Interest Compounding Interest (More than Once a Year)(More than Once a Year)

ex5/218 You deposit ex5/218 You deposit $5000$5000 in a bank in a bank account that pays an account that pays an APR of 3%APR of 3% and and compounds interest compounds interest monthlymonthly. How . How much money will you have after 1 much money will you have after 1 year? 2 years? 5 years?year? 2 years? 5 years?

APR is APR is annualannual percentage rate percentage rate

APR of 3% means monthly rate is 3%/12 APR of 3% means monthly rate is 3%/12 = .25%= .25%

4-A

Time Accumulated Value

0 m $5000$5000

1 m 1.0025x 5000 1.0025x 5000

2 m (1.0025)(1.0025)2 2 x 5000 x 5000

3 m (1.0025)(1.0025)3 3 x 5000 x 5000

4 m (1.0025)(1.0025)4 4 x 5000 x 5000

5 m (1.0025)(1.0025)5 5 x 5000x 5000

6 m (1.0025)(1.0025)6 6 x 5000 x 5000

7 m (1.0025)(1.0025)77x 5000 x 5000

8 m (1.0025)(1.0025)8 8 x 5000 x 5000

9 m (1.0025)(1.0025)9 9 x 5000 x 5000

10 m (1.0025)(1.0025)10 10 x 5000x 5000

11 m (1.0025)(1.0025)11 11 x 5000x 5000

1 yr = 12 m (1.0025)(1.0025)1212x 5000 = x 5000 = $5152.08$5152.08

2 yr = 24 m (1.0025)(1.0025)2424x 5000 = x 5000 = $5308.79$5308.79

5 yr = 60 m (1.0025)(1.0025)6060x 5000 = x 5000 = $5808.08$5808.08

4-A

Compound Interest Compound Interest FormulaFormula

((Interest Paid Interest Paid nn Times per Year) Times per Year)

4-A

AA = accumulated balance after = accumulated balance after YY years years PP = starting principal = starting principalAPR = annual percentage rate (as a APR = annual percentage rate (as a decimaldecimal)) nn = number of compounding periods per year = number of compounding periods per year YY = number of years (may be a fraction) = number of years (may be a fraction)

( n Y)APRnA = P (1+ )

45/225 You deposit $5000 at an APR of 5.6% 45/225 You deposit $5000 at an APR of 5.6% compounded quarterly. Determine the compounded quarterly. Determine the accumulated balance after 20 years.accumulated balance after 20 years.

( n Y)APRnA = P (1+ )

( 4 20).0564A = 5000 (1+ )

A = 5000 x (1.014)80 = 5000 x 3.04 = $15,205.70

4-A

Ex9/222 Suppose you have a new baby and Ex9/222 Suppose you have a new baby and want to make sure that you’ll have want to make sure that you’ll have $100,000$100,000 for his or her college education in 18 years. for his or her college education in 18 years. How much should you deposit now in an How much should you deposit now in an investment with an investment with an APR of 10%APR of 10% and and monthly monthly compoundingcompounding??

( n Y)APRnA = P (1+ )

( 12 18).1012100000 = P (1+ )

100000 = P x (1.0083)100000 = P x (1.0083)216216

100000 = P x 5.962100000 = P x 5.962

100000/5.962 = P100000/5.962 = P

$16772.90 = P$16772.90 = P

4-A

ex6’/219 You have $1000 to invest for a ex6’/219 You have $1000 to invest for a year in an account with APR of 3.5%. year in an account with APR of 3.5%. Should you choose yearly, quarterly, Should you choose yearly, quarterly, monthly or daily compounding?monthly or daily compounding?

Compounded

Formula Total

yearlyyearly $1035$1035

quarterlyquarterly $1035.46$1035.46

monthlymonthly $1035.57$1035.57

dailydaily $1035.62$1035.62

(4).0351000 1 +

4

(1).0351000 1 +

1

(12).0351000 1 + 12

(365).0351000 1 + 365

4-A

DefinitionDefinition

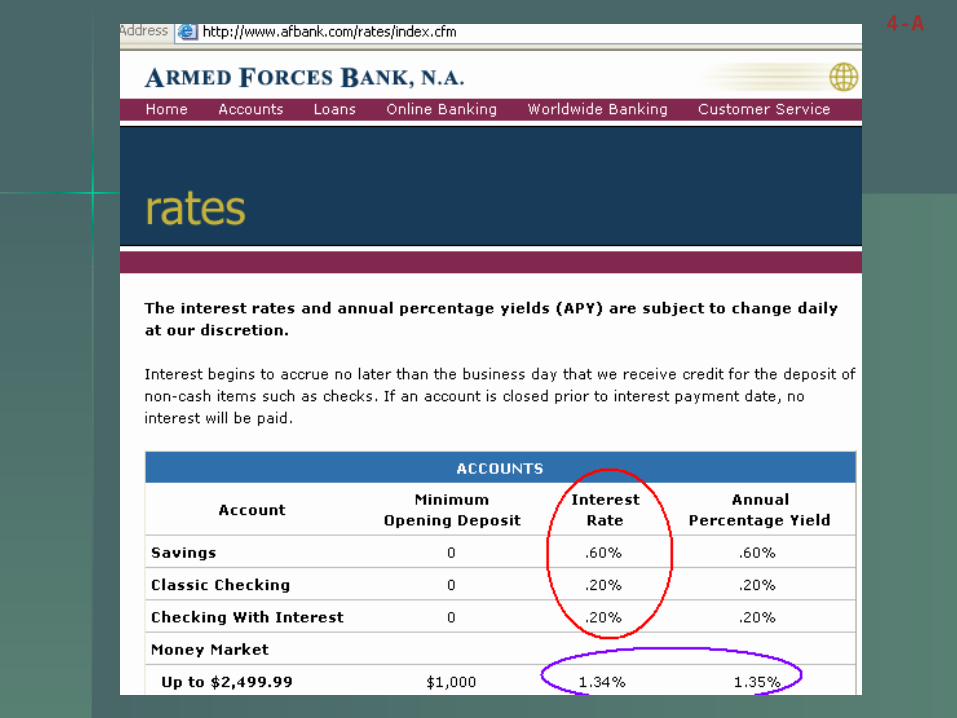

The The annual percentage yield(APY) is the is the actual percentage by which a balance actual percentage by which a balance increases in one year.increases in one year.

value after 1 year - principal amountAPY =

principal amount

4-A

APY calculations forAPY calculations for$1000 invested for 1 year at $1000 invested for 1 year at 3.5%3.5%

Compounded

Total Annual Percentage Yield

annuallyannually $1035$1035 3.5%3.5%**

quarterlyquarterly $1035.46$1035.46 3.546%3.546%

monthlymonthly $1035.57$1035.57 3.557%3.557%

dailydaily $1035.62 $1035.62

3.562%3.562%

* (1035 – 1000) / (1000)* (1035 – 1000) / (1000)

4-A

APR vs APYAPR vs APY

When compounding When compounding annuallyannually

APR = APYAPR = APY

When compounding When compounding more frequentlymore frequently, , APY > APRAPY > APR

4-A

Euler’s Constant eEuler’s Constant e

4-A

Investing $1 at a 100% APR for one year, the following table of amounts — based on number of compounding periods — shows us the evolution from discrete compounding to continuous compounding.

n = number of compoundings A = accumulation 1 = year 2.0 4 = quarters 2.44140625 12 = months 2.6130352902236 365 = days 2.7145674820245 365•24 = hours 2.7181266906312 365•24•60 = minutes 2.7182792153963 365•24•60•60 = seconds 2.7182824725426 infinite number of compoundings e 2.71828182846

Leonhard Euler(1707-1783)

( n 1)1.0nA = $1 (1+ )

Compound Interest FormulaCompound Interest Formula(Continuous Compounding)(Continuous Compounding)

4-A

( ) = APR YA P e

P = principal

A = accumulated balance after Y years

e = Euler’s constant or the natural number -an irrational number approximately equal

to 2.71828…

Y = number of years (may be a fraction)

APR = annual percentage rate (as a decimal)

ExampleExample4-A

4-A

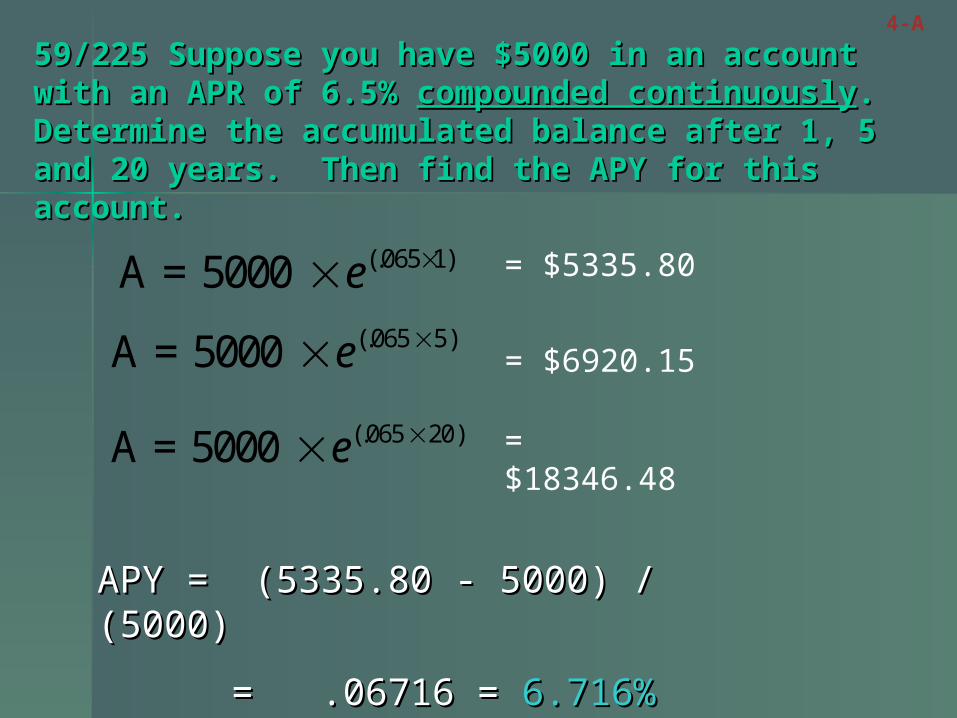

59/225 Suppose you have $5000 in an account with an 59/225 Suppose you have $5000 in an account with an APR of 6.5% APR of 6.5% compounded continuouslycompounded continuously. Determine the . Determine the accumulated balance after 1, 5 and 20 years. Then find accumulated balance after 1, 5 and 20 years. Then find the APY for this account.the APY for this account.

(.065 1)A = 5000 e

APY = (5335.80 - 5000) / (5000) APY = (5335.80 - 5000) / (5000)

= .06716 = = .06716 = 6.716%6.716%

(.065 5)A = 5000 e

(.065 20)A = 5000 e

= $6920.15

= $5335.80

= $18346.48

The Power of The Power of CompoundingCompoundingSimple InterestSimple Interest

Compound InterestCompound InterestOnce a yearOnce a year

More than once a yearMore than once a year

ContinuouslyContinuously

4-A

A = P x (1 + A = P x (1 + APR ) APR ) TT

( n Y)APRnA = P (1+ )

( ) = APR YA P e

More PracticeMore Practice

39/22539/225

45/22545/225

51/22551/225

55/22555/225

63/22563/225

65/22565/225

4-A

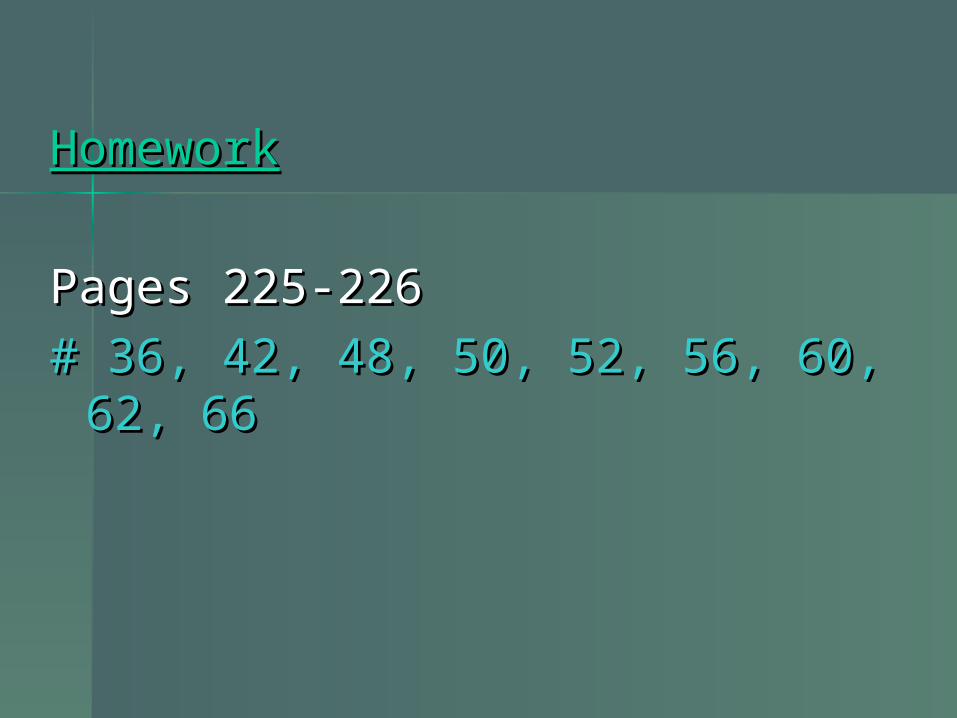

HomeworkHomework

Pages 225-226Pages 225-226

# 36, 42, 48, 50, 52, 56, 60, 62, # 36, 42, 48, 50, 52, 56, 60, 62, 6666