second to none: the role, value and potential of secondary

TRANSCRIPT

Please silence all cell phones.This session is being recorded.

Second to None: The Role, Value and Potential of Secondary Markets

Moderator:Noble Carpenter, Cassidy Turley

Panelists: Lawrence Bizjak, Garrison Investment GroupRobert G. Byron, Blue Vista Capital ManagementDoug Kintzle, Principal Real Estate InvestorsGlenn Mueller, PhD, Dividend Capital

2

Noble Carpenter, Executive Managing DirectorCassidy Turley

• Leads Cassidy Turley Capital Markets Group Nationally

• 26 Years of Global Capital Markets Experience

• Over $14 billion in investment sales and finance transactional experience

3

iPhone or iPadGo to the session Agenda Details and tap the feedback bubble in the lower right of your screen.

Android DeviceGo to the session Agenda Details and tap the thumbs up icon in the lower right of your screen.

Give Us Your Feedback for this Session!

Please silence all cell phones.This session is being recorded.

Second to None: The Role, Value and Potential of Secondary Markets

Moderator:Noble Carpenter, Cassidy Turley

Panelists: Lawrence Bizjak, Garrison Investment GroupRobert G. Byron, Blue Vista Capital ManagementDoug Kintzle, Principal Real Estate InvestorsGlenn Mueller, PhD, Dividend Capital

5

Glenn R. Mueller, Ph.D.

• Professor, University of Denver Franklin L. Burns School or Real Estate & Construction Management

• Real Estate Investment Strategist, Dividend Capital Research

6

Doug Kintzle, Managing DirectorPrincipal Real Estate Investors

• PrinREI Private Equity Quadrant– 124 million square feet managed

(including 15,000 multi-family units– $19.5 billion client portfolio value– $3.9 billion current active

development portfolio (land, construction and leasing)

– More than $12 billion of joint venture investments over the last decade.

7

Robert Byron, ChairmanBlue Vista Capital

• Cofounder of Blue Vista• Over 35 years of real estate investment

management and transaction experience, completed over $11 billion in real estate transactions in his career.

• Blue Vista has participated in direct investments and joint ventures representing over $5.25 billion across all real estate asset classes.

8

Lawrence Bizjak, Managing DirectorGarrison Investment Group

• Joined Garrison in 2007• Responsible for originating and

executing real estate transactions at all levels of the capital structure

• Leads a team responsible for acquisition and asset management of Garrison's real estate debt and equity positions, focused on opportunistic and special situation investments instruments throughout the United States.

9

Glenn R. Mueller, Ph.D

10

Market Cycle Quadrants

11

Historic National Office Rental Growth

12

Office Market Cycle Forecast Q2 2015 Estimates

13

Industrial Market Cycle ForecastQ2 2015 Estimates

14

Apartment Market Cycle ForecastQ2 2015 Estimate

15

Retail Market Cycle ForecastQ2 2015 Estimate

16

Hotel Market Cycle ForecastQ2 2015 Estimate

17

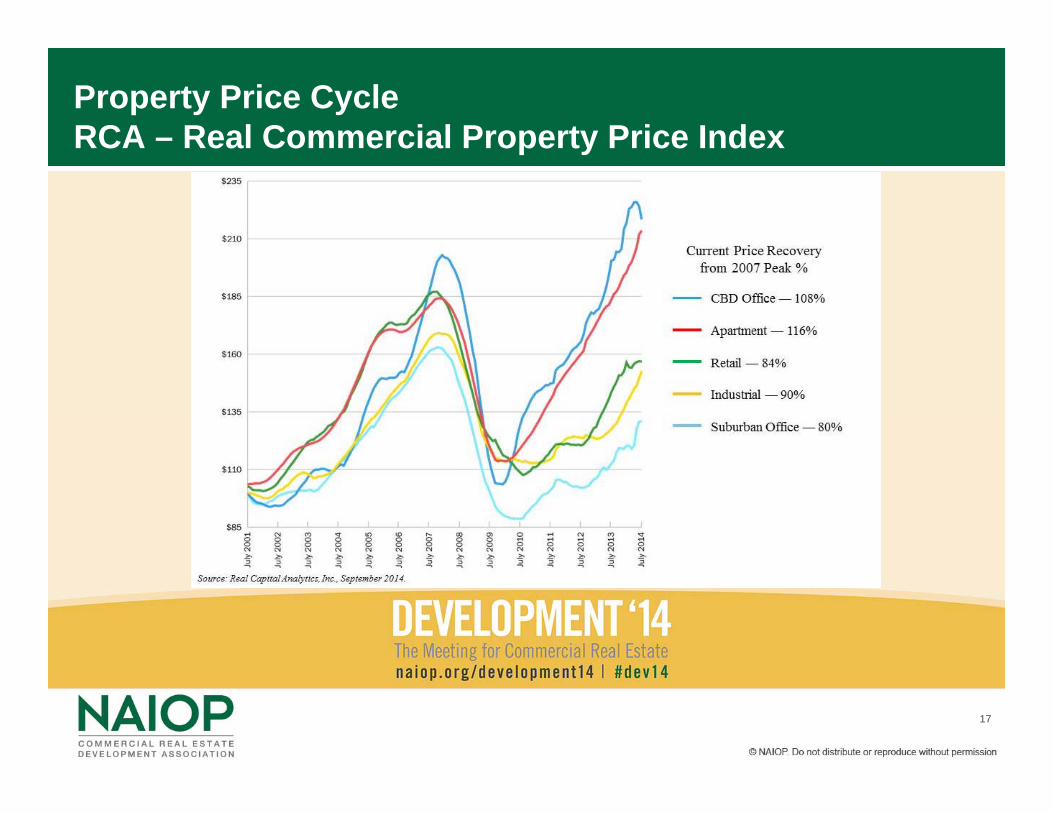

Property Price CycleRCA – Real Commercial Property Price Index

18

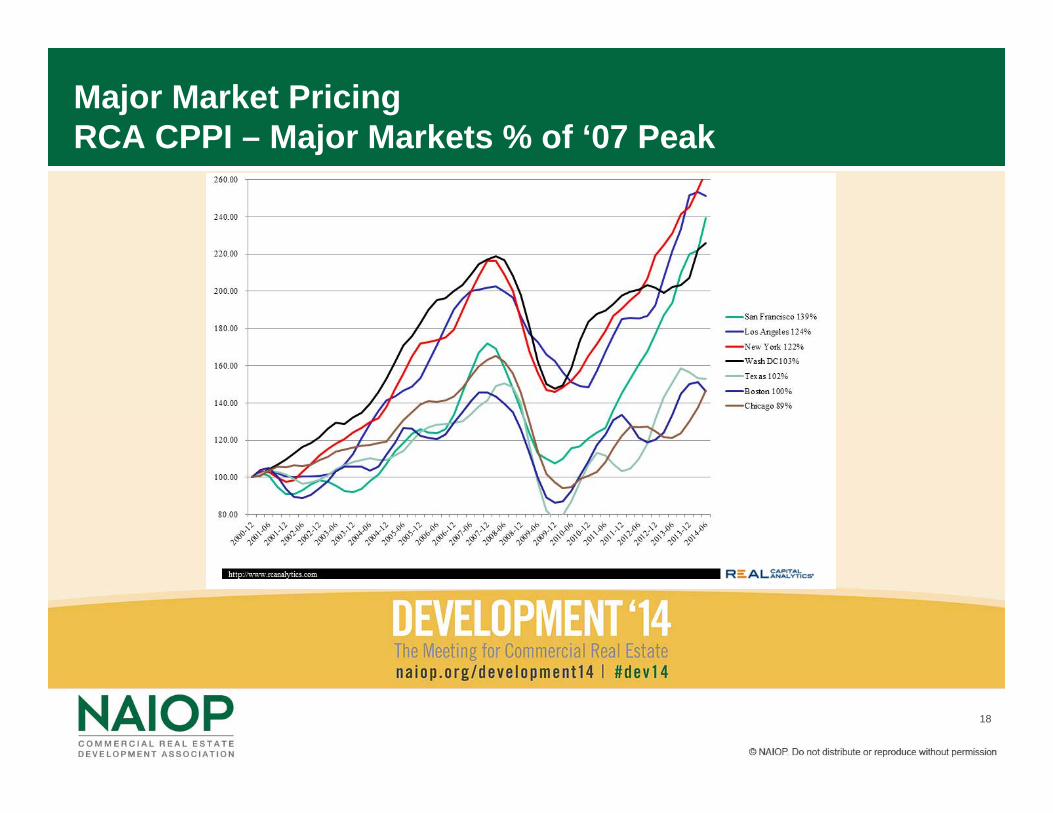

Major Market PricingRCA CPPI – Major Markets % of ‘07 Peak

19

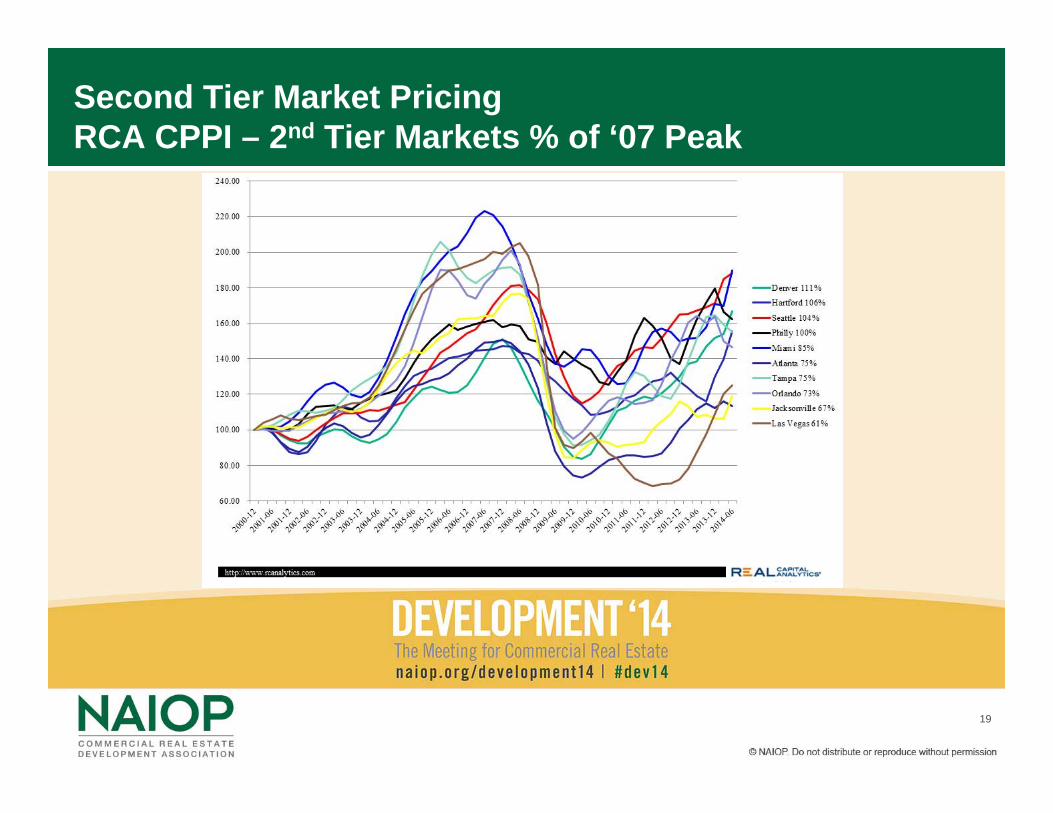

Second Tier Market PricingRCA CPPI – 2nd Tier Markets % of ‘07 Peak

20

Doug KintzleManaging Director

Principal Real Estate Investors

21

• Search for yield has caused increase in “bid-ask spread” between core and value-add properties

• In addition to “immediate core,” consider “lease-to-core” and “build-to-core” strategies that can provide:

– 200 - 300 bp increase in initial yield on cost

– 500 - 700 bp total return premium relative to unlevered core

• Focus on buying or building high-quality assets in primary markets with strong fundamentals.

• Consider larger secondary markets with return premium and liquidity (ex. office)

• Utilize moderate leverage (up to 50% LTV) to enhance returns and portfolio diversification

• Where economically feasible, pursue LEED or Energy Star certifications that can improve operating results and increase the bandwidth of potential tenants and buyers

• Seek to provide investors with a 4% - 6% annual dividend yield and a 10% - 12% total return (levered, after fee) over a 5 year investment period

Alternative “Means-to-Core” Strategy

22

Current Deals

Property: Cherry Creek ApartmentsDenver, CO

Deal Type: Multi-family

Year Built: Under Construction

Description: 175 market-rate multi-family units in one 12-story concrete/steel frame building with 5,488 sf of ground level retail. LEED Gold will be pursued.

Location: Located in the prestigious Cherry Creek North neighborhood southeast of downtown Denver. The site is across the street from Cherry Creek Shopping Center, one of Denver’s premier shopping centers.

Investment Thesis: Build trophy apartment project in the most coveted submarket in Denver MSA.

Gross Target IRR: Under developmentProjected Development Asset IRR: 14% to 15%

23

Current Deals

Property: Legacy 101San Jose, CA

Deal Type: Office

Year Built: Under Construction

Description: 199,175 square foot Class A, six story office building on just over 8 acres. A minimum LEED Silver Certification will be pursued.

Location: Located within the North San Jose office submarket in Silicon Valley, a block away from the VTA Light Rail, and offers freeway visibility for tenants.

Investment Thesis: Build high quality office for a build-to-core strategy. The site is shovel ready in a supply competitive environment. Timing of delivery matches well with current tenant market demand.

Gross Target IRR: Under developmentProjected Development Asset IRR: 16.0%

24

Current Deals

Property: Park Ladera IndustrialPhoenix, AZ

Deal Type: Industrial

Year Built: Under Construction

Description: Project will consist of three Class A tilt wall light distribution industrial buildings totaling 219,521 square feet with target tenant sizes ranging from 5,000 to 85,000 square feet.

Location: Located within the Deer Valley industrial market in Northern Phoenix with excellent access to the 1010 Freeway.

Investment Thesis: Build high quality industrial to generate higher risk-adjusted returns for a build-to-core strategy.

Gross Target IRR: Under developmentProjected Development Asset IRR: 13.0 to 13.5%

25

Robert ByronChairman

Blue Vista Capital

26

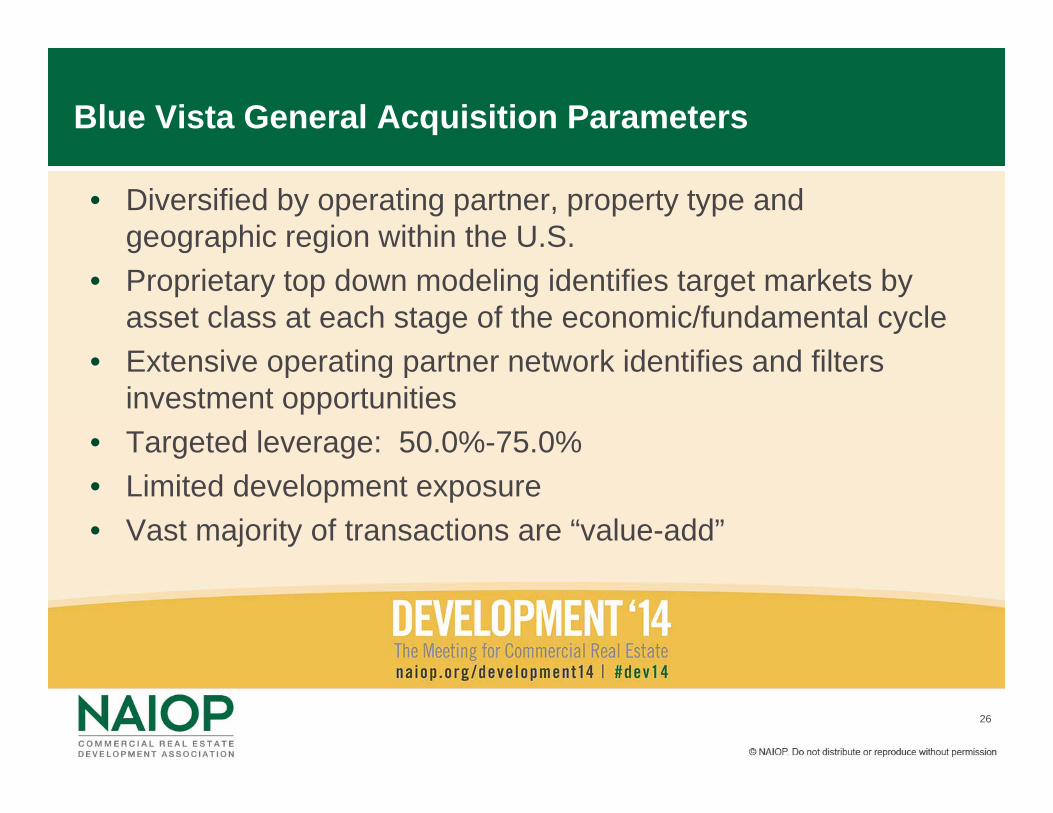

Blue Vista General Acquisition Parameters

• Diversified by operating partner, property type and geographic region within the U.S.

• Proprietary top down modeling identifies target markets by asset class at each stage of the economic/fundamental cycle

• Extensive operating partner network identifies and filters investment opportunities

• Targeted leverage: 50.0%-75.0%• Limited development exposure• Vast majority of transactions are “value-add”

27

Blue Vista Current Investment Strategies

• Multifamily development opportunities (minimum ROC to cap rate spreads of 150 bps)

• Low price per pound suburban office investments• Operationally inefficient limited service hotels• Well located grocery anchored retail • Self storage value-add/development• Co-GP core/core-plus investments with carried interest

participation• Platform Aggregation Strategies

28

Lawrence BizjakManaging Director

Garrison Investment Group

29

Garrison Overview

Post Crisis Price Recovery (As of 6/30/2014)

Index Peak TroughPeak to Trough

% Above (Below)

Prior PeakY/Y

Change

OfficeCBD Office - Major Mkts Dec-07 Sep-09 -47.6% 16.4% 14.7%CBD Office - Secondary Markets Dec-07 Dec-09 -53.9% -5.7% 23.5%Suburban OfficeSuburban Office - Major Markets Dec-07 Jun-10 -47.4% -18.6% 7.0%Suburban Office - Secondary Markets Sep-07 Mar-10 -44.7% -24.3% 23.0%IndustrialIndustrial - Major Markets Dec-07 Dec-09 -33.6% -6.0% 16.2%Industrial - Secondary Markets Sep-07 Mar-11 -35.5% -16.1% 18.8%

Source: Moody's RCA/CPPI & Garrison

• Garrison is a fund manager with approximately $4.0B of AUM. The real estate team focuses on opportunistic investments nationwide.

• One of the most active secondary market investors over the past several years, especially in the middle-market ($10MM-$50MM)

• From a macro-perspective, we think secondary markets offer the best risk/reward

• In our experience, secondary markets have better supply/demand dynamics, valuations, and, often, economic growth.

30

Core Markets vs.. Secondary Markets:Another Way to Look at Risk

Office Cap Rates Current

"Normal" Market

(2001-2004)

Increase in NOI Req'd to

BreakevenCore MarketsLos Angeles 5.81% 8.30% 42.8%New York 4.54% 7.41% 63.1%San Francisco 5.14% 8.29% 61.2%Washington DC 5.78% 8.16% 41.3%

Super Secondary MarketsAustin 6.61% 8.82% 33.4%Denver 7.04% 8.87% 26.0%Miami 5.44% 8.62% 58.6%Orange County 6.42% 8.47% 32.0%Phoenix 6.59% 8.91% 35.2%Salt Lake City 6.48% 8.35% 28.9%Seattle 6.47% 8.59% 32.8%

Secondary MarketsCharlotte 7.86% 8.30% 5.6%Nashville 7.40% 8.59% 16.2%Orlando 9.45% 9.05% -4.2%Pittsburgh 7.68% 8.40% 9.4%Raleigh 7.03% 8.10% 15.3%St Louis 9.82% 9.19% -6.4%

Low interest rates have distorted primary market valuations andcertain property sectors being driven by debt markets.

Primary markets provide limited downside protection. In recentmonths, interests in several NYC office buildings have beenoffered at 3-4% cap rates with valuations exceeding $1500psf.

From these cap rate levels, NOI must double or better tobreakeven in a “Normal” environment. For example, Rent =$100psf, Expenses = $30psf, NOI = $70psf. You would need toachieve rents of $170psf ($170-$30=$140, which is 2x $70psf)

Question: What is the probability of outperforming the abovescenario (assume you want to make money vs. breakeven)?

Washington DC is a similar story. Just substitute finance andWall Street for government and GSA.

The profile is much different in secondary markets, wheremodest NOI growth is required to breakeven, and fundamentalscan be stronger (i.e. energy and technology).

NYC and DC are great markets. This is merely a thoughtexperiment about risk, not a prediction.

31

This is your opportunity to make this session exactly what you need it to be – Ask the question.

Please note that this session is being recorded, so before speaking, please either proceed to a standing microphone or raise your hand and wait until a mic runner reaches you.

Thank you!

Q&A

32

Thank You!

Noble CarpenterExecutive Managing Director, PrincipalCassidy [email protected]

Lawrence BizjakManaging DirectorGarrison [email protected]

Robert G. ByronChairmanBlue Vista Capital [email protected]

Glenn Mueller, PhDReal Estate Investment StrategistDividend [email protected]

Doug KintzleManaging DirectorPrincipal Real Estate [email protected]