second sample answer and examiners’ comments full

TRANSCRIPT

© The ICAEW 2021 Page 1 of 10

SECOND SAMPLE ANSWER AND EXAMINERS’ COMMENTS

The commentary below follows the order and numbering of the script, with reference to the topics in the marking key. It should be read in conjunction with the review of the First Sample Answer and full Examiners’ Report for this session. Line numbers have been inserted on the script for ease of reference and are included where appropriate in this commentary.

Examiners’ comments – overview This script failed the exam. Although it addresses some of the key issues and contains some good sections, overall it has not gained enough passing grades (Clearly Competent (CC) and Sufficiently Competent (SC)).

Overall, the candidate earned 23 passing grades, more than half of which were SC. Of the 23, 5 (from a total of 7 available) were achieved for the Executive Summary and Overall Assessment Criteria (OAC). The remaining 18 were spread across the report, with sufficient passing grades obtained in Requirement 1 but not in Requirements 2 and 3. This is consistent with the lengths of each section – though that is not always a reliable indicator of relative quality. For professional skills, the 18 passing grades were divided as follows: 7 out of 9 boxes for Assimilating and Using Information (A&UI); 7 out of 9 for Structuring Problems and Solutions (SP&S); 3 out of 9 for Applying Judgement (AJ); 1 out of 6 for Conclusions and Recommendations (C&R). This weighting towards the left-hand side of the marking key is a common profile of failing scripts. With stronger development of what was often good analysis, this candidate could have passed. Executive summary

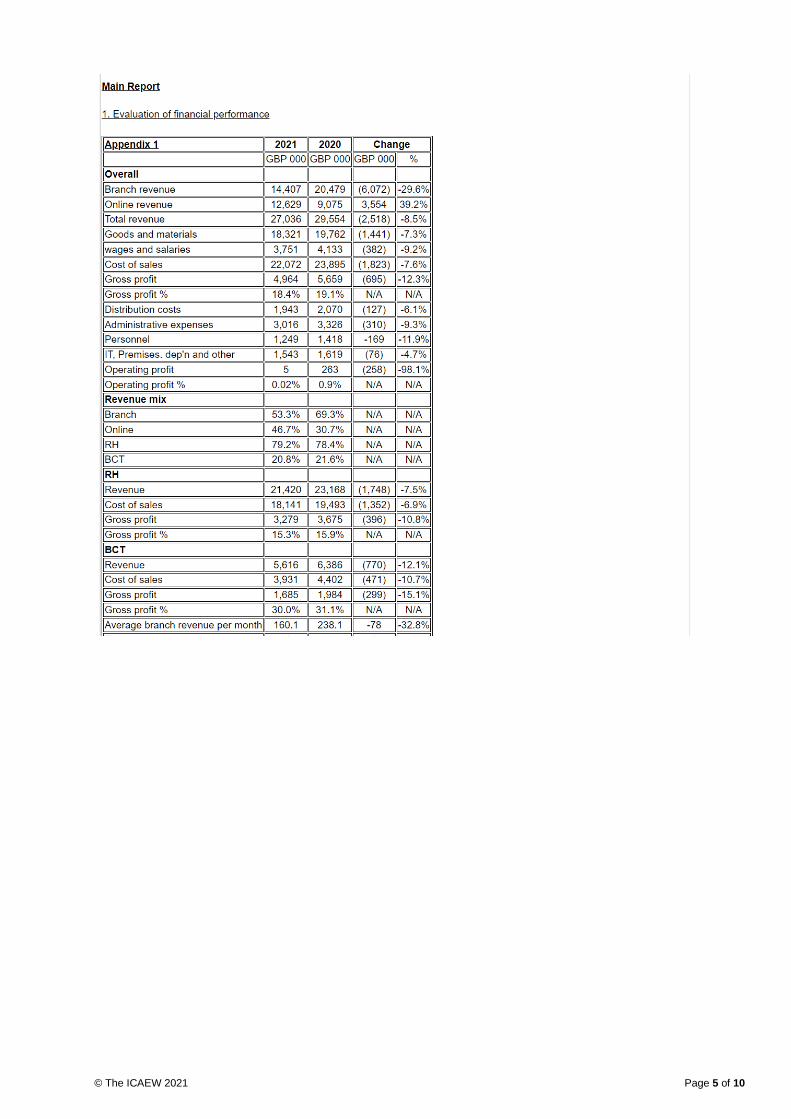

The executive summary contains a paragraph for each of the three main requirements. In all cases, it is an appropriate summary of the related section of the main report. For Requirement 1, the candidate has included detailed numerical analysis. However, there is no mention of the results by division and/or channel. There is also too much emphasis on the issue of trade receivable impairments and there is very little by way of recommendations. The section on Requirement 2 is the best part of the executive summary, especially in identifying the critical assumption (staff cost savings). It addresses most of the key areas, making sound commercial observations and providing relevant financial data. For Requirement 3, the candidate begins with a financial headline and goes on to make a clear recommendation not to proceed. However, there is some misplaced focus on the impact on HP’s relationship with Orko at the expense of other, more central issues that could have been raised. Overall Assessment Criteria The report begins with an inappropriate disclaimer (this is an internal report). The overall structure within the body of the report is adequate, with suitable headings/subheadings, but the appendices also require clear descriptive headings rather than just being numbered. The language is mostly appropriate but there are some careless lapses that undermine the overall presentation. (Where extracts from the script have been quoted, they have as necessary been corrected for ease of the flow of this commentary.) Review of HP’s financial performance [Requirement 1] The candidate has scored well for A&UI and SP&S, by identifying the (£ and %) movements in the main captions from the accounts and performing initial calculations, and by providing some good basic commentary. The appendix covers the core financial information, with appropriate segmental analysis and a correct calculation of average branch revenue per month. The candidate has in general made due reference to Exhibit 17, and to the wider business context, when discussing HP’s performance. Evaluation is less strong.

© The ICAEW 2021 Page 2 of 10

Grades for AJ were easily the weakest for this section. Specific shortcomings in evaluation include:

• Not making any reference to click-and-collect revenue, especially the way in which it is classified.

• Mentioning several times the lost revenue from two branches that were shut for three months without recognising that this is stated as having been partly diverted to other branches.

• Not linking divisional profits to the discounts given to RH and BCT customers respectively.

• Not considering the revenue and cost impact from Phase 1 of the ERP project. Under C&R, the recommendations are clear and relevant but the conclusions comprise mainly factual statements about the results without offering any comment. In addition, only overall revenue is included – there is no summary of the figures by channel or by division. Overall, this was a good section of the report – albeit with some missed opportunities to make it even better (see further under Requirement 2 below). The constant repetition of the phrase “We note

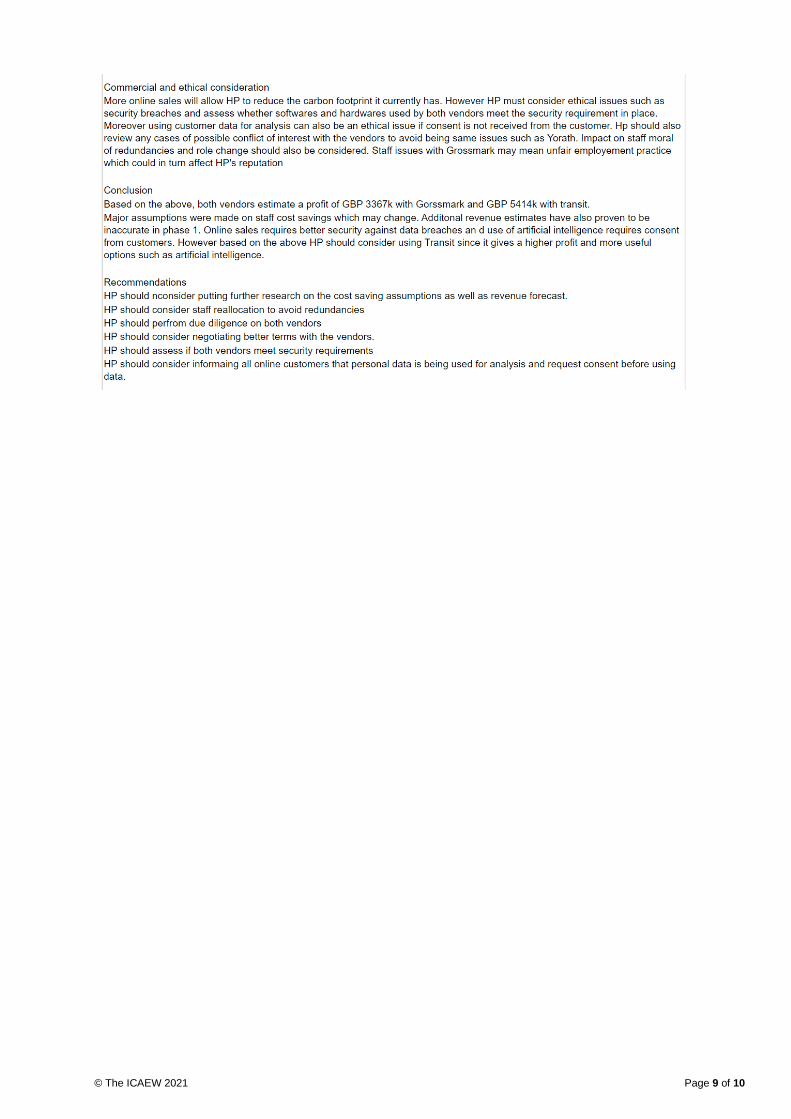

that …” is unnecessary, irritating and – more importantly – using up valuable writing time that could have been spent earning enough further marks to pass the exam. Evaluation of ERP Phase 2 vendors [Requirement 2] The answer to Requirement 2 gained fewer than 50% passing grades and was weaker than for most of the cohort. A fundamental reason for this is that the candidate has not read the requirement properly and so, rather than treating the warehouse issue as a separate topic, he/she has attempted to integrate it into the main part of the answer. In the appendix, the candidate has failed to apply any gross margin to the incremental revenue (see below) and has therefore ended up with inflated profits – and a heightened differential between Transit and Grossmark. He/she has also factored in some figures from the second part of the requirement (loss on disposal, loss of revenue), although these were not part of the vendor decision. In addition, there are no workings or footnotes to show how figures have been derived. When assessing the bids, the candidate has first considered the financial aspects and then the non-financial ones. There is in effect one long paragraph on each – not an advisable exam technique as it tends to impair clarity of thought. Bizarrely, the candidate has calculated his/her own profit margins (67.8% and 48.2%) and then benchmarked them against HP’s reported 18% for 2021 (the figure that he/she should have actually used), without seeming unduly surprised by this huge improvement! He/she has displayed higher skills on occasion, eg, “Cost savings are the key determinants of the

breakeven point of this project” [5:15]; it is a shame that this didn’t occur more often. Likewise, it is a shame that the sentiment that immediately follows (“As seen with Phase 1, additional revenues have not

been as high as estimated”) was not also included in the Requirement 1 commentary as an explanation for changes in revenue. With regard to non-financial considerations, the candidate has again frustratingly used data from Exhibit 17 that could and should have been incorporated into the answer to Requirement 1 as well as being referred to here, such as outages (5:21). There is good coverage of some other issues, such as the importance of IT development and maintenance problems with Grossmark. However, the candidate has overlooked some key issues in the discussion, such as the useful lives of the new equipment, the proposed parallel run period and Transit’s credentials from its work with Greg & Sons (the last one is a strange omission given that there are two other references to Greg & Sons in the answer). The candidate has included a section on ethical issues. These were not asked for at Requirement 2 and, while they have earned the odd mark in passing (eg, cybersecurity), they have done little more than waste further precious minutes out of the 240 allocated to the exam. However, what was asked for was a discrete discussion of the issues relating to HP’s proposed conversion of two branches to warehouses, and this is completely missing. As well as mistakenly including the warehouse disposal costs in the calculation, the candidate has also embedded the topic inappropriately in the narrative

© The ICAEW 2021 Page 3 of 10

(“… using Transit will allow absorption of lost revenue from closure of Warrington and Preston branches” [5:12]). Conclusions and recommendations are adequate but could both have been improved through tackling the warehouse situation in the right way – a failing that has pervaded the answer to Requirement 2 and contributed significantly to its overall low grades profile.

Evaluation of exclusive arrangement with Carey [Requirement 3] Requirement 3 is a curious mix of the very good and the less good. The calculation of revenue and gross profit is appropriate and correct. It could have benefited from better labelling, for example to show how the revenue from heating products was determined. The inclusion of lost revenue from Orko is an interesting extra element, which then gets picked up in the following narrative. There is no mention of possible extra costs such as distribution and additional administration or a comparison of the resulting revenue and profit with HP’s 2021 earnings. The candidate has also not touched on the wider strategic background, for example HP’s bank balance (which could be severely threatened by the payment terms being demanded by Carey) or the demographic impetus for HP’s further expansion into this sector. The ‘Financial analysis’ paragraph is striking in the way in which it skilfully weaves a wide range of points from across the case material (eg, dependence on a single customer [Risk Tracker], past project overruns, HP’s credit control system) into an all-too-short section that reveals sound commercial thought that is unfortunately absent from much of the rest of the script. For operational and strategic issues, in contrast, the candidate has dwelt too long on a small number of issues and has not identified some of the more pertinent ones. In particular, the sentences about buying group membership mostly repeat content from the AI and exam without relating them to the specifics of HP’s current needs. The key point to be made is that HP has to source suppliers for some of the items that Carey needs, and the candidate has not addressed this. He/she has also taken the misguided view that HP will have to lose Orko as a customer if it takes on Carey: there is certainly a delicate issue to address in respect of the publicity message being requested but this is a grey area rather than a black-or-white one. What would be a more germane point here is the potential value of HP’s experience with Orko in deciding whether or not to accept the approach from Carey.

The candidate has identified most of the ethical issues and addressed them adequately – though not necessarily under the ‘Ethical issues’ heading. Conclusions include the key figures and other items from the preceding narrative, ending with the advice to reject the proposal. Recommendations are satisfactory. In summary, the candidate has shown signs of quality through this section but not with enough consistency to achieve the grades that were possible.

© The ICAEW 2021 Page 4 of 10

© The ICAEW 2021 Page 5 of 10

© The ICAEW 2021 Page 6 of 10

© The ICAEW 2021 Page 7 of 10

© The ICAEW 2021 Page 8 of 10

© The ICAEW 2021 Page 9 of 10

© The ICAEW 2021 Page 10 of 10