second edition · second edition may 2008 149. fast ... fast facts computer systems ltd suresh...

TRANSCRIPT

As amended by Finance Act, 2008

Second Edition

May 2008

149

Fast Facts Computer Systems Ltd.

Price : Rs. 225

This book is based on the law as amended by Finance Act, 2008

Published By

Fast Facts Computer Systems LtdB-10, Sai Prasad, Telli Galli Cross RoadAndheri EastMumbai 400 069

Printed atPrint Tech46, Bomanji Lane,Near Fort Fire Station,Fort, Mumbai - 400 001.

All efforts have been made to avoid errors or omissions in this book. Nevertheless, errors may happen.Neither the publishers, nor the authors or sellers will be responsible for any damage or loss of action to any one, of any kind, in any manner. Readers are therefore advised to cross check all the facts, law and contents with the original Government publication, notification or circular.

No part of this book may be reproduced or copied in any form or by any means without the written permission of the publishers

For defects of missing pages, binding or misprints publisher's liability is limited to free replacement . Such replacement must be claimed within one month of purchase, for which all expenses will have to be borne by the purchaser only.

All disputes subject to Mumbai jurisdiction

About Authors

D K Tejwani is a Fellow member of The Institute of Chartered Accountants of India. He is Managing Director of Fast Facts Computer Systems Ltd., a software product company specializing in tax compliance related applications. He is editor of Fast Facts Bulletin a monthly newsletter about tax law updates. He is a regular speaker at various seminars and study circles.

Suresh Agrawal is a Fellow member of The Institute of Cost and Works Accountants of India, an Associate member of The Institute of Company Secretaries of India and a Law graduate. He has vast experience of more than two decades in industry in the field of Accounts, Finance, Budget and Cost control, Taxation and Internal Audit. He has been contributing articles to various professional journals and bulletins.

Page No.

1. Story of a TDS Transaction.......................................................1

2. TDS- Concept and Process .......................................................5

3. Deductor and Deductee..........................................................13

4. Tax Deduction Account No : TAN ........................................17

5. TDS Deduction.........................................................................22

6. TDS Rates..................................................................................31

7. TDS Payment............................................................................34

8. TDS Certificates .......................................................................42

9. eTDS Statements ......................................................................48

10. eTDS Correction.......................................................................57

11. TDS on Salaries ........................................................................60

12. Income from Salary: Computation........................................66

12. TDS on other payments ..........................................................80

13. TDS on payment to non-residents ......................................104

14. Tax Collection at Source........................................................110

15. Using Online Facilities..........................................................113

16. Consequences of Non Compliance .....................................121

17. TDS Accounting.....................................................................131

18. TDS in figures.........................................................................135

Annexure 1 :Sections ............................................................................137

Annexure 2 :Rules .................................................................................139

Annexure 3 :Circulars...........................................................................141

Annexure 4 :Forms................................................................................143

Annexure 5 :Date Calendar .................................................................146

Annexure 6 :TDS Rate Chart ...............................................................149

Index of Charts

Figure No. 1 TDS transaction ..................................................................4

Figure No. 2 TDS Process.......................................................................12

Figure No. 3 TDS Deduction Process ...................................................22

Figure No. 4 Filling up Challan No. 281..............................................41

Figure No. 5 Filling up TDS certificate 16A .......................................47

Figure No. 6 Control Totals in Form no. 27A......................................53

Figure No. 7 eTDS statements filing process ......................................56

Figure No. 8 Action to be taken in case of inconsistency ..................58

CONTENTS

This book is about complying with TDS provisions. Provisions of TDS i.e. Tax Deduction at Source are perceived to be difficult, tedious and at times confusing. This confusion is further compounded by frequent changes brought about by annual Finance Acts and notifications and circulars issued by Income Tax Department from time to time.

With the introduction of electronic TDS return filing, it took a definitive turn towards better compliance. With road map for dematerialization of TDS certificate already in place, the importance of TDS compliance will only grow.

We have made efforts to help Deductors understand the provisions in an easy manner.

Who should read this book

This book is meant for deductors, persons responsible for deducting tax at source. The provisions related to deductees or payees are not dealt with prominently. We recommend this book to:

• The financial controller / Head of accounts, who is responsible for the TDS compliance in the organization.

• The accounts executive who is actually doing accounting, payments and statement filing work.

• The student pursuing professional course.

This books is NOT meant for:

• The taxation expert - for legal nuances.

• Tax consultants/advocates.

What is unusual about this book

This book has following unique features:

• This book believes in the power of plain English. For this we are greatly influenced by a movement called “Plain English Movement”. More details can be viewed at www.plainenglish.co.uk. The basic idea behind this is to let the reader concentrate more on the message rather than the language. This is achieved by:

Preface

• Use of simple words, rather than complicated language.

• Small sentences.

• Avoiding use of technical jargon.

• We have not reproduced any section, rule, circular notification or form. 100% pages in this book are our contents and not reproduction. However, you can view all these references at our web site www.tdspac.com.

• We hate repetition. So a concept described once is not repeated anywhere.

• We believe in slim and trim. Hence 140 pages and not a bulk of 400 pages.

How is this book organized

• Each chapter has sufficient details for the topic.

• At the end of each chapter is “Practical Issues” where there can be differing opinions.

• The focus of the book is TDS Deductor.

• Many provisions pertain to both Tax deduction at source and Tax collection at source. But for the sake of convenience, we have always referred to Tax deduction at source.

• All the details pertain only to the financial year 2008-2009. Hence, no past provisions are given any where in the book.

• Circulars, notifications have been completely avoided.

Acknowledgements

We would like to thank many people who directly and indirectly contributed to this book . Special thanks to the reviewers of this book, who have taken efforts to critically review the book and provide valuable feedback.

We need your feedback

Please send your comments, criticism, & suggestions either by post or by email.

Dated May 15, 2008 D K Tejwani

Address for correspondence [email protected]

Fast Facts Computer Systems Ltd Suresh Agrawal

B-10, Sai Prasad [email protected]

Telli Galli Cross Road

Andheri (East)

Mumbai - 400 069

Mr. Deepak completed his masters degree in computer science. Although he was offered many jobs during placement, he decided to start his consulting venture offering consulting on blue tooth and wireless technologies.

He was lucky to get his first assignment from High Tech Retails Enterprises and the fees was fixed at Rs. 2,50,000 /-. The amount was to be paid as Rs. 100,000 towards advance and balance after completion of assignment.

May 17, 2005

He received a call from Mr. Desai, the accountant at High Tech informing him to collect his advance cheque. The date was May 17, 2005. When he read his first cheque, the amount was not Rs. 1,00,000 but Rs. 94,900 /- . “But the advance amount was supposed to be Rs. 100,000 “ he questioned Mr. Desai. “ The difference, my dear, is TDS @ 5.1% . I also need your PAN so if you do not have one, please get one fast “. A TDS Transaction was borne.

June 6, 2005

Mr. Desai was busy summing up the amounts he had deducted at source on several payments during May, 2005. He prepared Challans for such deductions and attached cheque with each one of them. He made sure that the TAN of High Tech is mentioned clearly on the challans. He checked the time and rushed to HDFC Bank across the lane.

June 6, 2005

Joe 's job at HDFC is to handle government payments. Today and tomorrow there will be huge rush at the counters as people rush to make their TDS payments. Mr. Desai was next in the queue. He slid two challans.

One of the challans was for Rs. 5,100/-. So the tax deducted from Deepak's technical fees is now going to the government.

Joe checked the challan carefully for TAN, accepted it and put the rubber stamp on it . Mr. Desai checked the rubber stamp it had date, BSR Code and Serial Number. Perfect.

June 6, 2005

HDFC bank was part of the online network covered under OLTAS which

1

Chapter 1

reported the tax collections to the Tax Information Net Work - TIN. Joe, at the end of day, prepared a consolidated file of all tax challans and transmitted it to the bank's Nodal Office from where it will travel to the Link Branch, which will finally upload this to the TIN.

June 17, 2005

Deepak realizing the necessity of a PAN had applied for one at the nearest TIN-Facilitation centre and was surprised to receive a PAN Card within 6 days . He immediately emailed the PAN to Mr. Desai.

June 30, 2005

Mr. Desai sat down to issue TDS certificate for all the deductions he has made in the month of May 2005. He prepared all such certificates. One of the certificate was for Rs. 5,100 issued to Mr. Deepak. He verified all the details mentioned in the certificate and couriered the same to Deepak. The certificate contained the PAN, name and address of Deepak. TAN, name and address of High Tech. It also had details of Rs. 1,00,000 and Rs. 5100/- .

July 12, 2005thMr. Desai checked his diary and reckoned that it is no point waiting for 15 to

submit eTDS statement for the quarter. Last moment rush must be avoided. So he started the software, entered all the details of TDS deductions made during April-June 2005, created the eTDS file . copied it on a CD and went to the nearest TIN-Facilitation Centre to submit the same.

July 12, 2005

Avinash manages a TIN Facilitation Centre on behalf of Alankit Assignments Ltd. A company which is authorized by NSDL the organization that manages TIN on behalf of income tax department. He accepted the CD from Mr. Desai and loaded the same in his software. The software checked the file and flashed Ok message. He verified the contents of Form that was given alongwith the CD, asked Mr. Desai to pay uploading charges and issued him a Receipt.

July 13,2005

Avinash consolidated all the eTDS returns collected yesterday and transmitted online to Alankit Head Office .

The Alankit Head office, will in turn consolidate all such files received from all the branches across India, verify and transmit it to the TIN Server.

Story of a TDS Transaction 2

Somewhere in the TIN, Rs. 5100 TDS of Mr. Deepak sits smugly.

June 7, 2006

Deepak is sitting with Mr. Bushan, his tax consultant who is preparing his income tax return. The first year was really satisfying . His total income for the year was Rs. 3.25 Lacs On which total tax liability was Rs. 48450. Bushan prepared a tax challan of Rs.43,350 /- after deducting Rs. 5100 for the TDS certificate .

After preparing his income tax return, he attached the proof of tax payment

Paid through challan 43,350

TDS Certificate 5,100

Total 48,450

So here is what we learnt from the story

Deepak

Deepak, a tax payer, must pay his tax on his earning . For this he has to work out his earnings at the year end, calculate tax and pay to the income tax department.

But part of his tax was paid by High Tech by deducting the amount from consultancy fees payable to him.

Deepak matched his accounts by working out total tax liability, attaching TDS certificate and paying the balance amount in bank.

High Tech

High tech matched its accounts by first deducting the amount from Deepak's payment and later paying the amount to income tax department by depositing the challan in bank.

TIN System

TIN system on receiving the eTDS statement from High Tech and bank challan details from HDFC, matched the details.

In this process, a whole lot of persons, Desai of High Tech, Joe of HDFC Bank, Avinash of TIN-FC and some more unseen persons, the person at the Nodal Office of HDFC, the person at the Link Office of HDFC, the person at the head office of Alankit devoted their time and efforts.

3 Story of a TDS Transaction

4

TDS Transaction

Story of a TDS Transaction 4

Payeror

Tax Deductor

Payeeor

Tax Deductee

Tax deduction at source

Issue of TDS certificate

Income Tax Department

Cross verification Assessingunit

TDS unitNSDLDigitisation

Processing

Payment ofTDS into Bank

Remittance into Govt. account

TSt

ee

eD

S at

mnt

Tl

a

OL

AS

Ch

al

n

Figure No. 1

Chapter 25

TDS defined

A taxpayer pays income tax on the income earned during the year. For this the taxpayer must compute the taxable income for the year and tax payable at the end of year. Due to this rule the tax collection is delayed till the completion of the year.

To receive tax collections regularly during the year, the tax department has provided for the following :

Advance tax

Tax deduction at source

Tax collection at source

Tax deduction at source or TDS as it is popularly known is one of the methods of tax collections and ensures regular cash flow to the government.

Tax deduction at source means recovering the tax at the time of income generation. So the person who makes the payment which is an income for the receiver is asked to deduct the tax and pay only the balance amount to the recipient.

The task of tax recovery is done by the person making payment and not by government.

Income concealment and thereby under recovery of tax is a big problem with governments all over the world. Making a person other than the taxpayer responsible for tax deduction, ensures that income concealment is reduced to some extent. Also, since the details of tax deductions are available to the government, these can be used to track incidences of tax avoidance.

Tax deduction at source is one of the methods of reducing incidences of income escaping tax, hence improving tax collections.

TDS- Concept and Process 6

To summarise,

• tax deduction at source is one of the methods employed by government to collect tax.

• It also serves the purpose of increase in tax revenues by widening the tax net.

• What is more, tax collection responsibility is passed on to the persons making payment.

TDS by other names

TDS is also known by other terms in different countries.

In most of the countries it is known as Withholding tax . The principle of a withholding tax is that it is withheld (retained) by the payer and given directly to the taxation authorities. The payee is given only the balance. The primary motivation is to reduce tax evasion or failure to pay..

In Australia it is known as PAYG (or pay-as-you-go) and is used for withholding taxation from employees, and other payees, in their regular payments from employers, and other payers.

PAYE (or pay-as-you-earn) is a payroll deduction system in which tax is deducted from a person's income when paid by the employer. It is so known in UK and New Zealand.

The European Union withholding tax, more commonly known as the EU withholding tax is a withholding tax which is deducted from interest earned by European Union residents on investments in another member state. Its aim is to ensure that they do not avoid taxation by depositing funds in tax havens with strong bank secrecy laws.

TDS : Income Tax Act, 1961

In the Income Tax Act 1961, one full chapter is devoted to tax deduction at source. Chapter XVII titled “Collection and recovery of tax “ . It has following parts.

Part A - General

Part B - Deduction at Source

Part BB - Collection at Source.

Section 192 to 206A deal with various provision pertaining to tax deduction at source.

TDS : Income tax Rules 1962

Part VI of Income tax Rules pertain to Deduction of Tax at Source.

TDS : More

Apart from the Act and Rules, a person has to keep track of :

• Notifications.

• Circulars.

• Finance Bill.

• Decisions by Supreme Court / High Court / Tribunals.

If all this seems a difficult task, this book will help you to understand the practical aspects in a simpler manner, thereby making it easier for you.

Before we proceed, it will be prudent to know some definitions, as these terms will be used frequently in the coming chapters.

Some Important Definitions

• Previous Year

The Financial Year in which the income is earned is known as the previous year. Any financial year begins from 1st of April and ends on subsequent 31st March. The financial year beginning on 1st of April 2007 and ending on 31st March 2008 is the previous year for the assessment year 2008-2009.

• Assessment Year :

The financial year following a previous year is known as the assessment year For example for the previous year from 1st April 2007 to 31st March 2008, the assessment year shall be the next financial year i.e. 1st April 2008 to 31st March 2009. Means the period of twelve months commencing on the 1st day of April every year.

• Deductor

Income-tax Act requires specified persons to deduct tax on a particular type of payment being made by them. The person who deducts tax is called a Deductor.

• Deductee :

The person who is getting the payment after deduction of tax at source is called a deductee.

• Tax Information Network (TIN),

A repository of nationwide Tax related information. TIN is an initiative by Income tax department for the modernisation of the current system

7 TDS- Concept and Process

for collection, processing, monitoring and accounting of direct taxes using information technology.

• TAN :

Every deductor has to apply for and get an identification number called Tax Deduction Account No. This is for easy identification of the deductor.

• PAN :

Permanent Account Number is allotted by income tax department to each taxpayer.

Deductor's burden

The person deducting the tax from specified payments, remits the amounts so deducted to the government and the persons from whose payment tax was so deducted, gets credit in his tax dues.

To complete this cycle, the following steps are carried out by deductor:

• Deduction of tax at source by deductor.

• Remitting deducted amount to government.

• Issuing TDS certificate to the deductee.

• Submitting quarterly TDS return to the income tax department.

All the above steps are performed by the deductor. If the task was unpleasant enough, it has been made onerous by:

• Making a time frame for all the tasks.

• Interest / penalty for non compliance or late compliance.

• Prosecution for non-compliance.

• Disallowance of expenses during tax computation due to non compliance.

There are some more responsibilities cast upon the deductor:

• Receive self declarations for No Deduction from deductee.

• Submit a copy of such declarations to income tax department.

• Obtain a Tax Deduction Account Number.

• Obtain PAN from all deductees.

• provide compliance details to auditors.

Is deductor defined under the Income Tax Act ?

No, deductor is the term we are using to refer to the person responsible for deducting tax at source.

8TDS- Concept and Process

TDS Process

Now let us see the TDS Process in brief.

Deduction of tax at source

This is where all the action begins. The questions that the deductor has to decide at this stage are:

• What is nature of payment being made or credited ?

• Is this payment covered under the provisions of TDS and if yes then under what section ?

• Check if you are covered under that section ?

• Is the person to whom payment is being made, exempt from the provisions of TDS ?

• Is the total amount paid less than the threshold or it has crossed the limit ?

• What is the rate applicable for TDS ?

• Has the person to whom payment is being made, given a certificate for lower rate or self declaration for NIL rate ?

Once all these questions are decided, then TDS will be computed and deducted.

Remitting deducted amount to government

This is the second stage after the deductions have been made. This is a very objective process and not much decision making is involved here.

• Segregate all the payments TDS section wise

• Within TDS section further segregate payments made to companies and other than companies.

• Fill up / prepare a challan No 281 for each such segregated amount.

• Give break up of TDS, surcharge and education cess.

• Prepare a cheque or arrange cash for the challan amounts.

• If you are a corporate or covered under mandatory tax audit, then make e-Payment. Otherwise go to the nearest bank branch, which accepts government receipts.

• After making the payment, ensure that the bank has put the Challan Identification Number Stamp on the challan.

Issuing TDS certificate to the deductee

This again is a simple step in the TDS process and outlined clearly.

• Every month, segregate the TDS deductions for which monthly

9 TDS- Concept and Process

certificates are required to be given.

• Check if the deductee has asked for a consolidated yearly certificate, if yes segregate these deductees.

• Arrange all TDS deductions for a deductee.

• Further arrange TDS deductions for the deductee, TDS section wise.

• Find out the Form in which TDS certificate is to be prepared.

• Prepare one certificate for each TDS section separately.

• Get the certificate signed by an authorised signatory.

• Put a proper certificate number on the certificate.

• Deliver the TDS certificate to the payee.

• At the year end, segregate all TDS deductions for which annual certificate are to be given . Prepare separate certificate for each deductee and deliver the same.

Submitting quarterly TDS return to the income tax department

At the end of each quarter, every deductor has to prepare quarterly TDS statement and deliver the same to the income tax department:

• Check if you are liable for mandatory filing of electronic TDS return ?

• If yes, then acquire / download software for eTDS return preparation

• Find out the number of returns to be filed, based on the TDS sections under which deductions are made.

• Prepare the return and submit.

10TDS- Concept and Process

How costly it is to comply with TDS

The National Institute of Public Finance and Policy (NIPFP) conducted a study for the Planning Commission in 2002 regarding cost of TDS compliance. Some very interesting figures have come to light in this revealing study. It says that the average annual cost incurred for TDS compliance for Salaries is 11.68% of the total income tax deducted at source for employees. Annually, on average the Rs.1.04 lacs are incurred for TDS compliance for deduction of around Rs.8.92 lacs of TDS for employees.

Average annual cost incurred towards fees of tax advisors has been estimated at Rs.3000 p.a. Following is the data regarding time spent for different activities of TDS compliance:

Activity Time spent per annum

a. Completing and submitting TDS return 20 man days

and depositing TDS

b. Computer and data processing related to TDS 30 man days

c. Completion & submission of Form 16 2.2 man daysfor employees

d. Preparation of Form 16 for one employee 15 min per form

If this is the scenario for TDS compliance for Salaries, we can very well imagine the cost figures for other heads of TDS where transactions, hassles and processing is much more, compared to the amount of income tax deducted. So the cost as a percentage of tax deducted will be significantly higher.

Moreover with the introduction of electronic filing of TDS returns, online

payment of TDS and online submission and matching of TDS certificates the

TDS compliance cost will further increase for software training and

competent staff and internet expenses etc.

11 TDS- Concept and Process

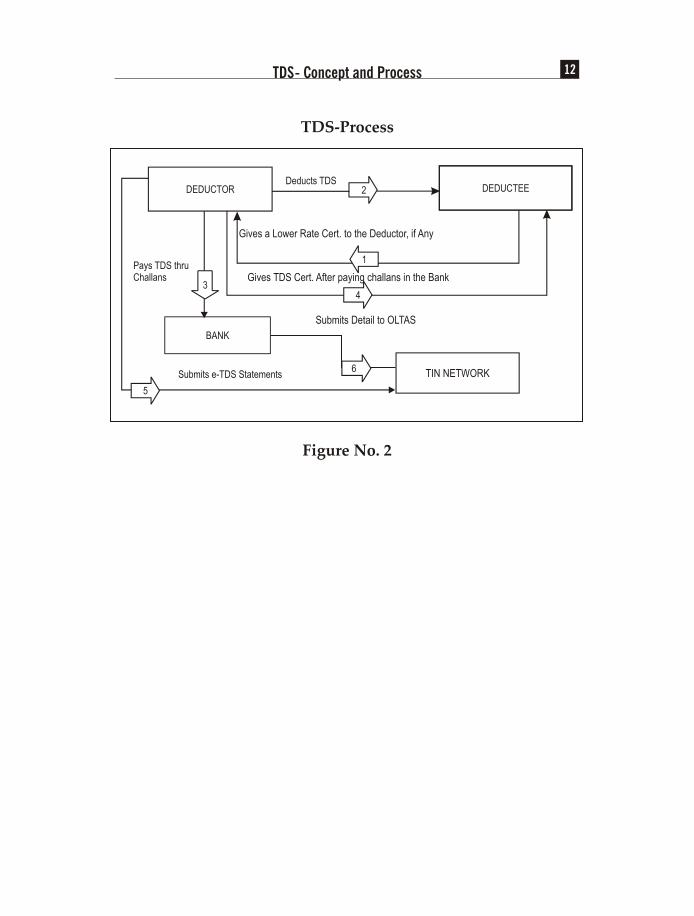

DEDUCTORDeducts TDS

DEDUCTEE

Gives a Lower Rate Cert. to the Deductor, if Any

Gives TDS Cert. After paying challans in the Bank

Submits Detail to OLTAS

TIN NETWORK

BANK

Submits e-TDS Statements

Pays TDS thruChallans

3

5

4

2

1

TDS- Concept and Process 12

TDS-Process

6

Figure No. 2

Deductor

Income-tax Act requires specified persons to deduct tax on a particular type of payment being made by them. The person who deducts tax is called a Deductor.

Deductee

The person who is getting the payment after deduction of tax at source is called a deductee.The type of deductee is very important as it will determine.

• the rate of TDS.

• the applicability of surcharge.

Different types of deductees

Company

• any Indian company registered under the Companies Act, 1956.

• a foreign company, registered under a law outside India.

Firm

A firm refers to a partnership firm which is a "relationship between persons

who have agreed to share the profits of business carried on by all or any of

them acting for all".

Association of Persons (AOP) or Body of Individuals (BOI)

• An association of persons (AOP) means two or more persons who join for

a common purpose with a view to earn an income.

• The association need not be on the basis of a contract. Therefore, if two or

more persons join hands to carry on a business but do not constitute a

partnership they may be assessed as an AOP.

• But, an AOP does not mean any and every combination of persons. It is

only when they associate themselves in an income-producing activity

that they become an association of persons.

• Body of individuals (BOI) means a conglomeration of individuals who

carry on some activity with the objective of earning some income.

Chapter 313

• It would consist only of individuals.

• Entities like companies or firms cannot be members of a body of

individuals.

Distinction between an AOP and BOI:

• An AOP may consist of non-individuals but a BOI has to consist of

individuals only.

• If two or more persons (like firm, company, HUF, individual etc) join

together, it is called an AOP. But if only individuals join together then it is

called a BOI.

• An AOP implies a voluntary getting together for a common design or

combined will to engage in an income producing activity, whereas a BOI

may or may not have common design or will.

Local Authority

• Panchayat

• Municipality

• Municipal Committee and District board, or

• Cantonment Board

Artificial juridical persons

• It includes entities which are not natural persons but are separate entities

in the eyes of law. Though they may not be sued directly in a court of law

but they can be sued through persons managing them.

• Example: God, idols and deities are artificial persons. Though they may

not be sued directly they can be legally sued through the priests or the

managing committee of the place of worship, etc.

• Similarly, all other artificial persons, with a juristic personality, will also

fall under this category, if they do not fall within any of the preceding

categories of persons e.g. University of Delhi is an artificial person as it

does not fall in any of the above categories. This is thus a residuary

classification and therefore it does not cover those falling within any of

the preceding classifications.

Deductor and Deductee 14

Individual

The word individual means only a natural person i.e. a human being.

Trustees of a discretionary trust have to be assessed in status of individual

and not in status of association of persons.

Hindu Undivided Family (HUF)

An HUF, as per the Hindu law, means a family which consists of all persons

lineally descended from a common ancestor and includes their wives and

unmarried daughters. Profits made by a joint Hindu family are chargeable to

tax as income of the HUF.

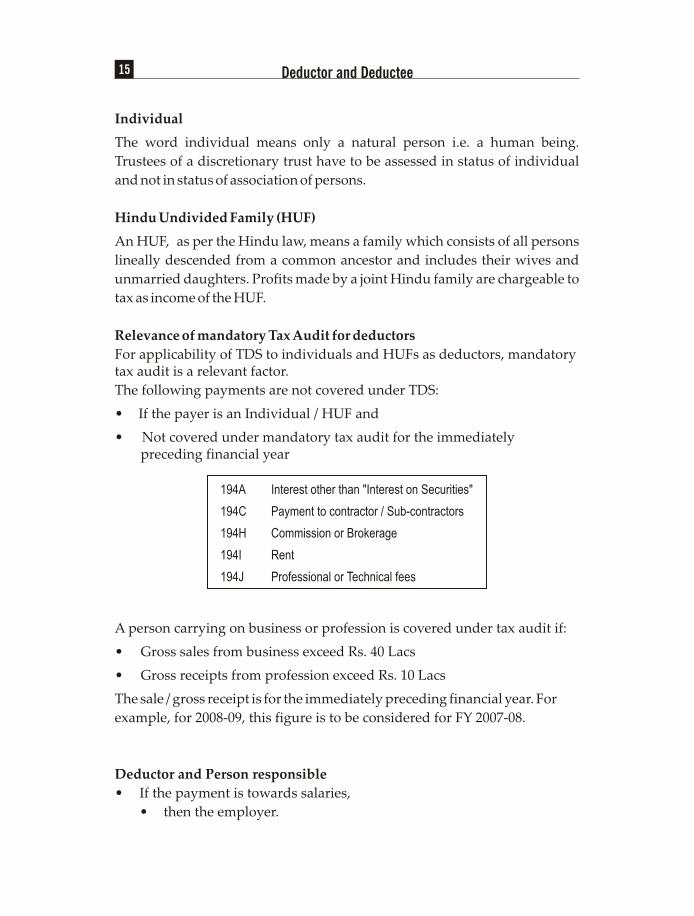

Relevance of mandatory Tax Audit for deductors

For applicability of TDS to individuals and HUFs as deductors, mandatory tax audit is a relevant factor.

The following payments are not covered under TDS:

• If the payer is an Individual / HUF and

• Not covered under mandatory tax audit for the immediately preceding financial year

194A Interest other than "Interest on Securities"

194C Payment to contractor / Sub-contractors

194H Commission or Brokerage

194I Rent

194J Professional or Technical fees

A person carrying on business or profession is covered under tax audit if:

• Gross sales from business exceed Rs. 40 Lacs

• Gross receipts from profession exceed Rs. 10 Lacs

The sale / gross receipt is for the immediately preceding financial year. For

example, for 2008-09, this figure is to be considered for FY 2007-08.

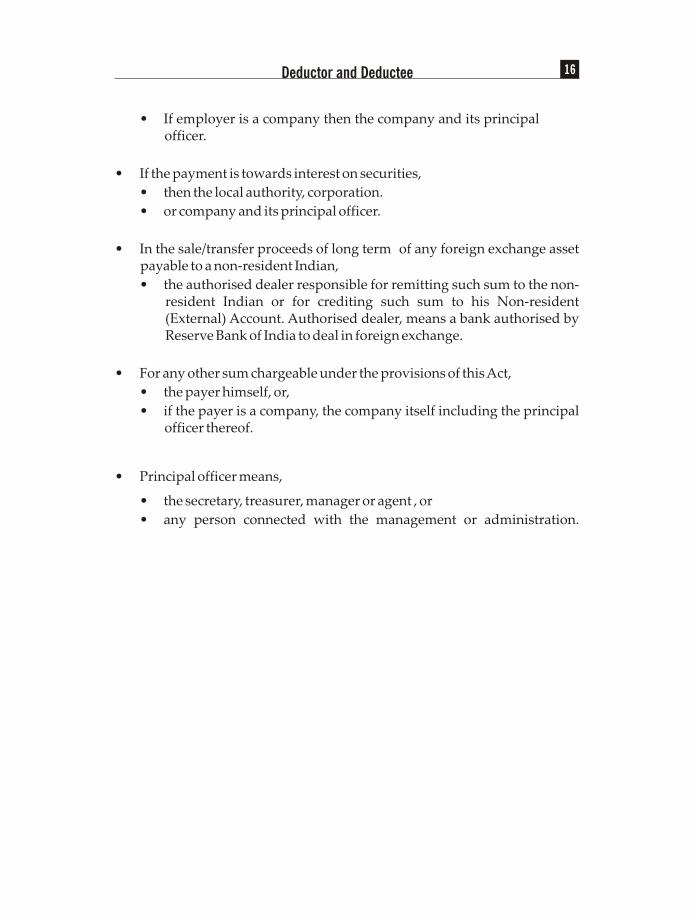

Deductor and Person responsible

• If the payment is towards salaries,

• then the employer.

15 Deductor and Deductee

• If employer is a company then the company and its principal officer.

• If the payment is towards interest on securities,

• then the local authority, corporation.

• or company and its principal officer.

• In the sale/transfer proceeds of long term of any foreign exchange asset payable to a non-resident Indian,

• the authorised dealer responsible for remitting such sum to the non-resident Indian or for crediting such sum to his Non-resident (External) Account. Authorised dealer, means a bank authorised by Reserve Bank of India to deal in foreign exchange.

• For any other sum chargeable under the provisions of this Act,

• the payer himself, or,

• if the payer is a company, the company itself including the principal officer thereof.

• Principal officer means,

• the secretary, treasurer, manager or agent , or

• any person connected with the management or administration.

16Deductor and Deductee

TAN is the unique number, with which each deductor is identified by the income tax department. Every deductor must apply for and get a TAN and must quote the same in all documents pertaining to TDS.

Format of TAN

• TAN is a 10 digit alpha numeric number.

• The valid format of TAN is AAA*99999A, where * is the first character of the name of the organization. Example TAN of Fast Facts is MUMF03364E.

• Earlier TAN numbering was not uniform. Once the electronic filing of eTDS return started, the OLD TANs were automatically allotted new TANs.

Applying for TAN

• Every person responsible for making payments which are subject to TDS, must apply for a TAN.

When to apply

• Application for TAN must be made within one month from the month, in which tax was deducted or collected for the first time.

TAN for a multi branch organisation

• It is not necessary for a multi branch organization to have a single TAN. Each branch can opt for a separate TAN. e.g. branches of a bank

Form No. 49B

• The application for TAN must be made in Form No. 49B.

• The form is freely downloadable on the income tax web site www.incometaxindia.gov.in.

• The instructions for filling up 49B are also given in the form as well as on the site.

Chapter 417

1 (a)

1 (b)

1 (c)

1 (d)

1 (e)

1 (f)

1 (g)

Name - Central / State Government

Name - Statutory / Autonomous Bodies

Name - Company

Branch of a company

Name- Individual / Hindu Undivided Family (Karta)

Branch of Individual Business(Sole Proprietorship concern)/ Hindu Undivided Family (HUF)

Firm/Association of persons/Association of persons (Trusts)/ Body of Individuals/ Artificial Juridical Person

This column is meant for Central Government, State Government, Local Authority (Central Govt), Local Authority (State Govt.). e.g. Directorate of Income Tax (systems) in Income Tax Department

e.g. Bandra office of Brihanmumbai Municipal Corporation

This category is to be filled by the company if it is applying TAN for the company as whole. In case company wants to apply different TANs for different divisions/branches point 1(d) should be filled. Abbreviations should not be used. Full words, 'Private Limited' or 'Limited' must be written

If Branch/division of a Company is applying for its separate TAN, it will mention the Name and Location of the Branch (in whose name TAN is sought) in this field. Different Branches of a company applying for separate TANs will fill this field.

If a Sole Proprietor/HUF wants to obtain a single TAN in his/her name for all businesses run by him/her/it, then he/she/it shall fill name in this field. First Name is Mandatory. Name of the deductor / collector should be written in full and not in abbreviated form . No prefix like Mr. Mrs. Dr is allowed in the name field.

This field will be filled only if TAN is being applied for branch of Individual Business (Sole Proprietorship Concern)/Hindu Undivided Family . Hence, the name of the concern will be filled in the field for Name/Location of Branch.

The Name of the F i rm/Assoc ia t ion of persons/Association of persons (Trusts)/Body of Individuals/ Artificial Juridical Person will be written in full in the field provided.

I t e m No.

Item Details Guidelines for filling up the form

Filling up Form 49B

1 Name:

The Name must be filled in one of the 8 separate headings. If you fill in name

under more than one headings then the application will be rejected.

Tax Deduction Account No. : TAN 18

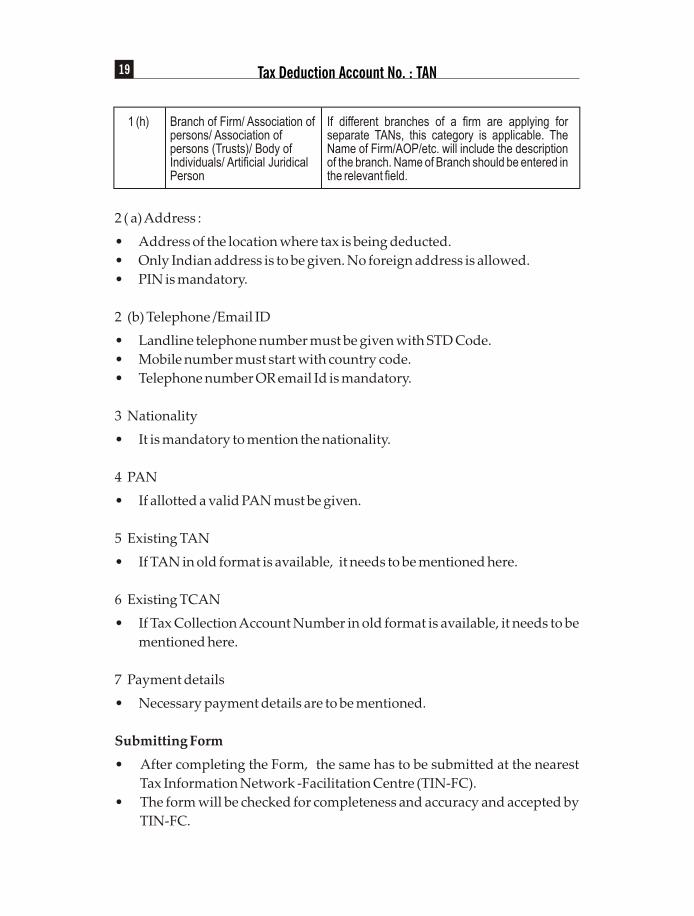

1 (h) Branch of Firm/ Association of persons/ Association of persons (Trusts)/ Body of Individuals/ Artificial Juridical Person

If different branches of a firm are applying for separate TANs, this category is applicable. The Name of Firm/AOP/etc. will include the description of the branch. Name of Branch should be entered in the relevant field.

2 ( a) Address :

• Address of the location where tax is being deducted.

• Only Indian address is to be given. No foreign address is allowed.

• PIN is mandatory.

2 (b) Telephone /Email ID

• Landline telephone number must be given with STD Code.

• Mobile number must start with country code.

• Telephone number OR email Id is mandatory.

3 Nationality

• It is mandatory to mention the nationality.

4 PAN

• If allotted a valid PAN must be given.

5 Existing TAN

• If TAN in old format is available, it needs to be mentioned here.

6 Existing TCAN

• If Tax Collection Account Number in old format is available, it needs to be

mentioned here.

7 Payment details

• Necessary payment details are to be mentioned.

Submitting Form

• After completing the Form, the same has to be submitted at the nearest

Tax Information Network -Facilitation Centre (TIN-FC).

• The form will be checked for completeness and accuracy and accepted by

TIN-FC.

19 Tax Deduction Account No. : TAN

• You also have to pay necessary fees to the TIN-FC. You will get an

acknowledgement Number.

• On the basis of application, TAN will be allotted by income tax

department.

• You will get intimation regarding TAN by post.

• You can also apply online for TAN.

• You can track your application status via web site or SMS.

Where the TAN is to be mentioned

• Challan No 281.

• TDS certificates.

• TCS Certificates.

• Quarterly TDS statement.

• Correspondence with income tax department.

What if TAN is not available

• You may be liable to pay a penalty of Rs. 10,000.

• The bank will not accept Challan for payment.

• The eTDS statement file will not be accepted by TIN-FC.

Online Resources pertaining to TAN

On the NSDL web site, you can use the following tools pertaining to TAN.

• TAN Search

TAN number search is very powerful and one can find out the TAN based

on first few characters of the name. Search is also possible based on Old

TAN.

• Online Application for TAN

If you do not want to visit a TIN-FC for submitting Form 49B, use online

application. The payment can be made by a Credit Card or a Demand

Draft can be attached later . Once form is submitted an acknowledgement

number will be generated. A print out of this acknowledgement

alongwith payment details can be couriered to NSDL. It will get

processed in the normal way.

20Tax Deduction Account No. : TAN

• Online Application for Changes Or Correction in TAN Data for TAN

allotted

If there is any change in the particulars mentioned in the original TAN

application form, this tool can be used to apply for the same. This can

similarly be used for cancellation of TAN .

• Track your TAN application status

By entering the acknowledgement number, name and date of

incorporation, the status of application can be enquired on line.

21 Tax Deduction Account No. : TAN

TDS Deduction is the first step in the process. Every person responsible for deducting TDS has to follow these simple steps for TDS deduction.

TDS DEDUCTION PROCESS

YES NO

NO YES

YESAmount CrossingThreshold

Limit

NO

NO

Deduct at Standard RateDeduct at Lower Rate/ NIL Rate

YES

IsDeducteeExempted

LowerRate / NilRate Cert.submitted

Payment liable

ToTDS

Chapter 5

No TDS Deduction

No TDS Deduction

No TDS Deduction

22

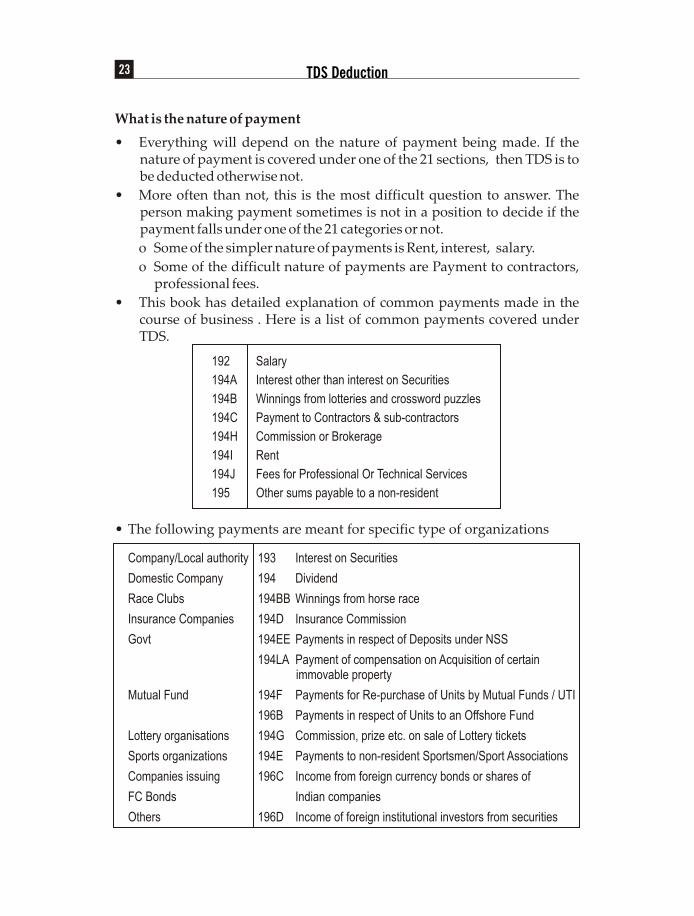

What is the nature of payment

• Everything will depend on the nature of payment being made. If the nature of payment is covered under one of the 21 sections, then TDS is to be deducted otherwise not.

• More often than not, this is the most difficult question to answer. The person making payment sometimes is not in a position to decide if the payment falls under one of the 21 categories or not.

o Some of the simpler nature of payments is Rent, interest, salary.

o Some of the difficult nature of payments are Payment to contractors, professional fees.

• This book has detailed explanation of common payments made in the course of business . Here is a list of common payments covered under TDS.

192 Salary

194A Interest other than interest on Securities

194B Winnings from lotteries and crossword puzzles

194C Payment to Contractors & sub-contractors

194H Commission or Brokerage

194I Rent

194J Fees for Professional Or Technical Services

195 Other sums payable to a non-resident

• The following payments are meant for specific type of organizations

Company/Local authority 193 Interest on Securities

Domestic Company 194 Dividend

Race Clubs 194BB Winnings from horse race

Insurance Companies 194D Insurance Commission

Govt 194EE Payments in respect of Deposits under NSS

194LA Payment of compensation on Acquisition of certain immovable property

Mutual Fund 194F Payments for Re-purchase of Units by Mutual Funds / UTI

196B Payments in respect of Units to an Offshore Fund

Lottery organisations 194G Commission, prize etc. on sale of Lottery tickets

Sports organizations 194E Payments to non-resident Sportsmen/Sport Associations

Companies issuing 196C Income from foreign currency bonds or shares of

FC Bonds Indian companies

Others 196D Income of foreign institutional investors from securities

TDS Deduction23

Who is covered as a deductor under a particular section

Any Income tax payer is called an assessee. Income Tax Act defines an assessee as a person as any of the following:

(i) an individual(ii) a Hindu undivided family (iii) a company (iv) a firm (v) an association of persons or a body of individuals, whether incorporated or not, (vi) a local authority, and (vii) every artificial juridical person, not falling within any of the preceding sub-clauses.

However, even a person not liable to pay income tax, is covered under the provision of tax deduction at source . e.g Government department .

In the normal course of business, the following are covered under provisions of TDS:

All persons for:

• Payment of Salaries.

• Payment of winning from lotteries.

• Payment of winning from horse race.

• Payment to non residents.

For remaining payments, all persons except:

• Individual whose gross receipts from profession is less than 10 Lacs.

• Individual / HUF whose gross receipts from business is less than 40 lacs.

Is the person to whom payment is being made, exempt from the provisions of TDS

The person or the organization to whom payment is being made may be exempt from the provisions of deduction of tax.

Complete Exemption

The following are completely exempt from provisions of TDS:

• The government.

• Reserve Bank of India.

• A corporation established by a state or central act which is under any law in force, exempt from tax on its income.

• A Mutual Fund.

Specific exemptions

There are specific exemptions under each section. An example is given below:

24TDS Deduction

Other Interest payable to:

• Banks

• Financial institutions

• LIC

• UTI

• Insurance Company

• Notified Institutions

• Notified Schemes

• Partners by firms

• members by a co-operative society

• saving/current and recurring deposits accounts by banks

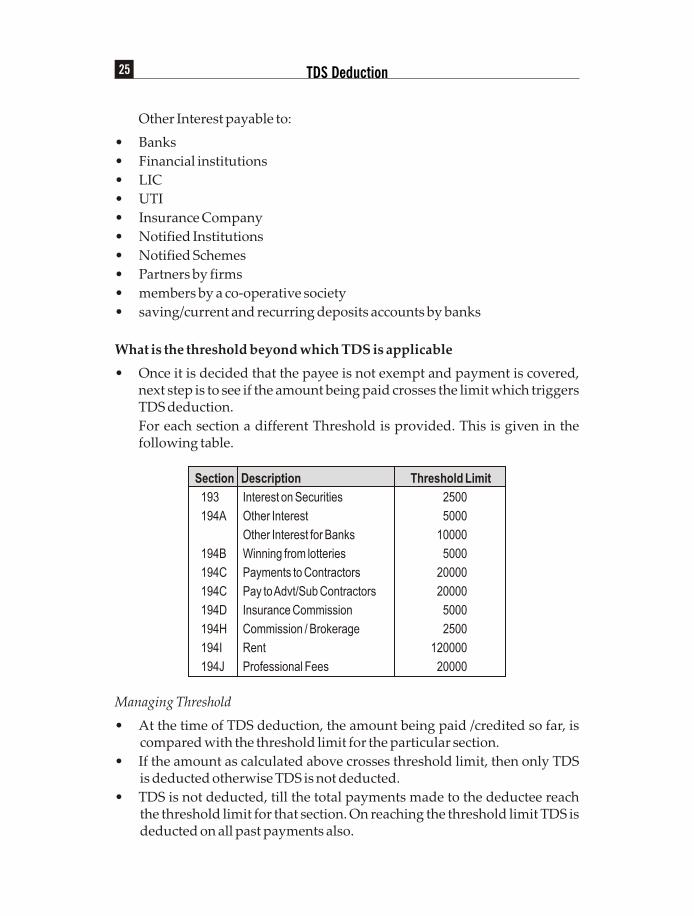

What is the threshold beyond which TDS is applicable

• Once it is decided that the payee is not exempt and payment is covered, next step is to see if the amount being paid crosses the limit which triggers TDS deduction.

For each section a different Threshold is provided. This is given in the following table.

Section Description Threshold Limit

193 Interest on Securities 2500

194A Other Interest 5000

Other Interest for Banks 10000

194B Winning from lotteries 5000

194C Payments to Contractors 20000

194C Pay to Advt/Sub Contractors 20000

194D Insurance Commission 5000

194H Commission / Brokerage 2500

194I Rent 120000

194J Professional Fees 20000

Managing Threshold

• At the time of TDS deduction, the amount being paid /credited so far, is compared with the threshold limit for the particular section.

• If the amount as calculated above crosses threshold limit, then only TDS is deducted otherwise TDS is not deducted.

• TDS is not deducted, till the total payments made to the deductee reach the threshold limit for that section. On reaching the threshold limit TDS is deducted on all past payments also.

25 TDS Deduction

Case Past Payments + TDS to be On what AmtCurrent Payment deducted

A < Threshold No -

B > Threshold and Crossing Yes Past Payment +threshold for the first time Current Payment

C > Threshold and has already Yes Current PaymentCrossed threshold in the past

What is the rate applicable for TDS

• TDS Rate comprises of Basic Rate of TDS, Surcharge and Education cess

• Surcharge is an additional rate of tax that is calculated on the tax at basic rate, when certain conditions are fulfilled.

• Cess is the tax charged on the total tax to be paid i.e on the amount of tax at basic rate plus surcharge. This is used for specific purposes like education, floods etc. Cess is levied on each tax-paying person.

• Surcharge is calculated on basic rate whereas cess is calculated on Basic rate + surcharge.

• Currently there is a 2% Education cess applicable plus Secondary and Higher education cess of 1%

• Rate of surcharge is 10% for payments made to deductees in India.

• TDS Rate computation is illustrated below:

Basic Rate 20%

Surcharge 10% i.e. 20*10% = 2

Education Cess 2%+1%=3% i.e. (20+2) * 3% = 0.66

TDS Rate 20+2+0.66 = 22.66

• Surcharge is mandatory if the deductee is

o AJP(Artificial Juridical Person).

• Surcharge is NOT applicable if the deductee is

o Co-operative Society

o Local Authority

• Surcharge is conditional in the case of Individual / HUF

o Applicable only in cases where total payment to deductee under all sections taken together exceeds Rs.10 Lakhs during the financial year

o Not applicable in other cases

• Surcharge is conditional in case of Companies/firms also

o Applicable only in cases where total payment to deductee under all sections taken together exceeds Rs.1 Crore during the financial year

o Not applicable in other cases

26TDS Deduction

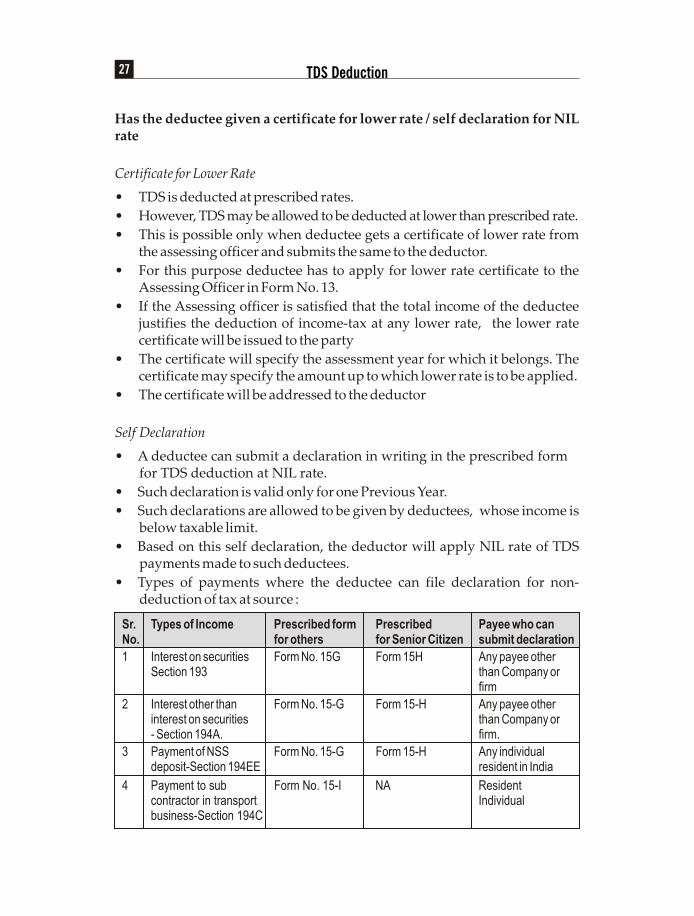

Has the deductee given a certificate for lower rate / self declaration for NIL rate

Certificate for Lower Rate

• TDS is deducted at prescribed rates.

• However, TDS may be allowed to be deducted at lower than prescribed rate.

• This is possible only when deductee gets a certificate of lower rate from the assessing officer and submits the same to the deductor.

• For this purpose deductee has to apply for lower rate certificate to the Assessing Officer in Form No. 13.

• If the Assessing officer is satisfied that the total income of the deductee justifies the deduction of income-tax at any lower rate, the lower rate certificate will be issued to the party

• The certificate will specify the assessment year for which it belongs. The certificate may specify the amount up to which lower rate is to be applied.

• The certificate will be addressed to the deductor

Self Declaration

• A deductee can submit a declaration in writing in the prescribed form for TDS deduction at NIL rate.

• Such declaration is valid only for one Previous Year.

• Such declarations are allowed to be given by deductees, whose income is below taxable limit.

• Based on this self declaration, the deductor will apply NIL rate of TDS payments made to such deductees.

• Types of payments where the deductee can file declaration for non-deduction of tax at source :

Sr. Types of Income Prescribed form Prescribed Payee who canNo. for others for Senior Citizen submit declaration

1 Interest on securities Form No. 15G Form 15H Any payee otherSection 193 than Company or

firm

2 Interest other than Form No. 15-G Form 15-H Any payee otherinterest on securities than Company or- Section 194A. firm.

3 Payment of NSS Form No. 15-G Form 15-H Any individualdeposit-Section 194EE resident in India

4 Payment to sub Form No. 15-I NA Resident contractor in transport Individualbusiness-Section 194C

27 TDS Deduction

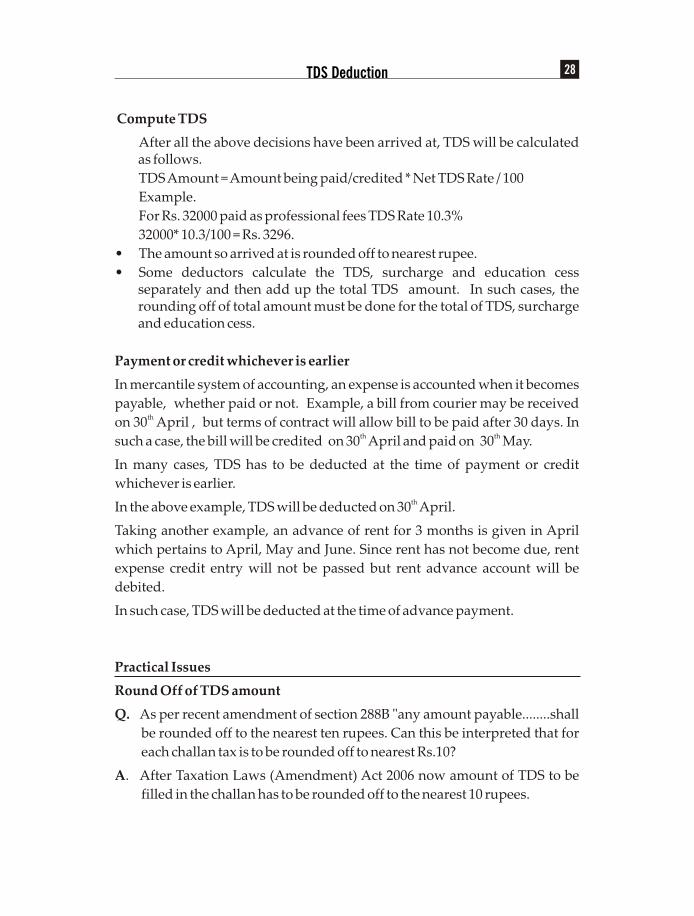

Compute TDS

After all the above decisions have been arrived at, TDS will be calculated as follows.

TDS Amount = Amount being paid/credited * Net TDS Rate / 100

Example.

For Rs. 32000 paid as professional fees TDS Rate 10.3%

32000* 10.3/100 = Rs. 3296.

• The amount so arrived at is rounded off to nearest rupee.

• Some deductors calculate the TDS, surcharge and education cess separately and then add up the total TDS amount. In such cases, the rounding off of total amount must be done for the total of TDS, surcharge and education cess.

Payment or credit whichever is earlier

In mercantile system of accounting, an expense is accounted when it becomes

payable, whether paid or not. Example, a bill from courier may be received thon 30 April , but terms of contract will allow bill to be paid after 30 days. In

th thsuch a case, the bill will be credited on 30 April and paid on 30 May.

In many cases, TDS has to be deducted at the time of payment or credit

whichever is earlier. thIn the above example, TDS will be deducted on 30 April.

Taking another example, an advance of rent for 3 months is given in April

which pertains to April, May and June. Since rent has not become due, rent

expense credit entry will not be passed but rent advance account will be

debited.

In such case, TDS will be deducted at the time of advance payment.

Practical Issues

Round Off of TDS amount

Q. As per recent amendment of section 288B "any amount payable........shall

be rounded off to the nearest ten rupees. Can this be interpreted that for

each challan tax is to be rounded off to nearest Rs.10?

A. After Taxation Laws (Amendment) Act 2006 now amount of TDS to be

filled in the challan has to be rounded off to the nearest 10 rupees.

28TDS Deduction

TDS Reversal

Q. Can TDS remittance be adjusted against the TDS reversal of particular

month/quarter/financial year? Example:

• TDS liability in respect of payment to "A" - Rs. 1000

• TDS reversal in respect of cheque cancellation of 'B' made in last

quarter - Rs.200.

• Net liability for the month - Rs.800.

Is it allowed? If yes, then how to report the same in eTDS statement, as the

same does not accept negatives. If no, how to claim TDS remitted?

A.

• In our view, TDS once deducted and deposited belongs to the

government. It cannot be reversed.

• Therefore the TDS of Rs.200 in respect of cancelled cheque of "B" can

neither be adjusted with any other TDS payments nor can any refund be

claimed from the government.

• However, a TDS certificate should be issued to "B" who can very well

claim the credit for the TDS of Rs.200 wrongly deducted.

Deduction seems to fall under two sections

Q. At times there is confusion regarding classifying a transaction in a

particular section. It may appear to fall under more than one section. For

example, a payment may appear to be a contract as well as payment for

technical services.

Whereas rate for TDS on contractor is 2%, it is 10% for technical services.

If lower of the two rates is applied and later during TDS assessment, a

different view is taken by office, the deductor is subjected to interest and

penalty proceedings. What to do in such cases?

A. In such cases, practical view is to take the higher rate with the consent of

payee.

Keeping track of threshold for deduction

Q. Threshold limit exemption is easier to work out in the case of one time

payments e.g. payment of crossword puzzle. But tracking this limit for

normal business transactions is a difficult task e.g. payment to

contractors, professionals. Even if such task is automated by software,

29 TDS Deduction

• TDS deduction will have to be done on past transactions.

• Such past transaction will have to be shown in eTDS Statements.

As such what is the correct approach for compliance which is practical

also?

A. To avoid this, deductors may take a practical view and deduct TDS

without considering threshold limit.

Difficulty in estimating total payment for surcharge purpose

Q. Surcharge applicability in the case of individual / HUF will depend on

total payment being more than 10 lacs.

• The limit of 10 lacs is payment under all sections

• If at first, the estimated payments are less than 10 lacs and during the year

the amounts exceed 10 lacs, surcharge will have to be deducted on past

transactions also.

Then how to practically keep track of the payments for surcharge

applicability purposes?

A. For this, a realistic estimation of total amount must be made right in the

beginning.

30TDS Deduction

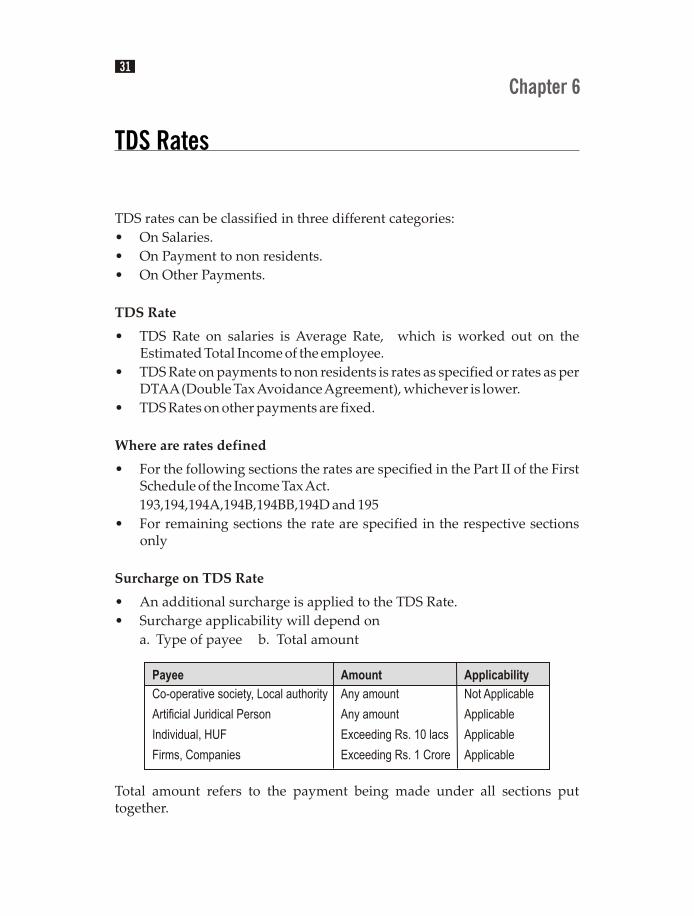

TDS rates can be classified in three different categories:

• On Salaries.

• On Payment to non residents.

• On Other Payments.

TDS Rate

• TDS Rate on salaries is Average Rate, which is worked out on the Estimated Total Income of the employee.

• TDS Rate on payments to non residents is rates as specified or rates as per DTAA (Double Tax Avoidance Agreement), whichever is lower.

• TDS Rates on other payments are fixed.

Where are rates defined

• For the following sections the rates are specified in the Part II of the First Schedule of the Income Tax Act.

193,194,194A,194B,194BB,194D and 195

• For remaining sections the rate are specified in the respective sections only

Surcharge on TDS Rate

• An additional surcharge is applied to the TDS Rate.

• Surcharge applicability will depend on

a. Type of payee b. Total amount

Payee Amount Applicability

Co-operative society, Local authority Any amount Not Applicable

Artificial Juridical Person Any amount Applicable

Individual, HUF Exceeding Rs. 10 lacs Applicable

Firms, Companies Exceeding Rs. 1 Crore Applicable

Total amount refers to the payment being made under all sections put together.

Chapter 631

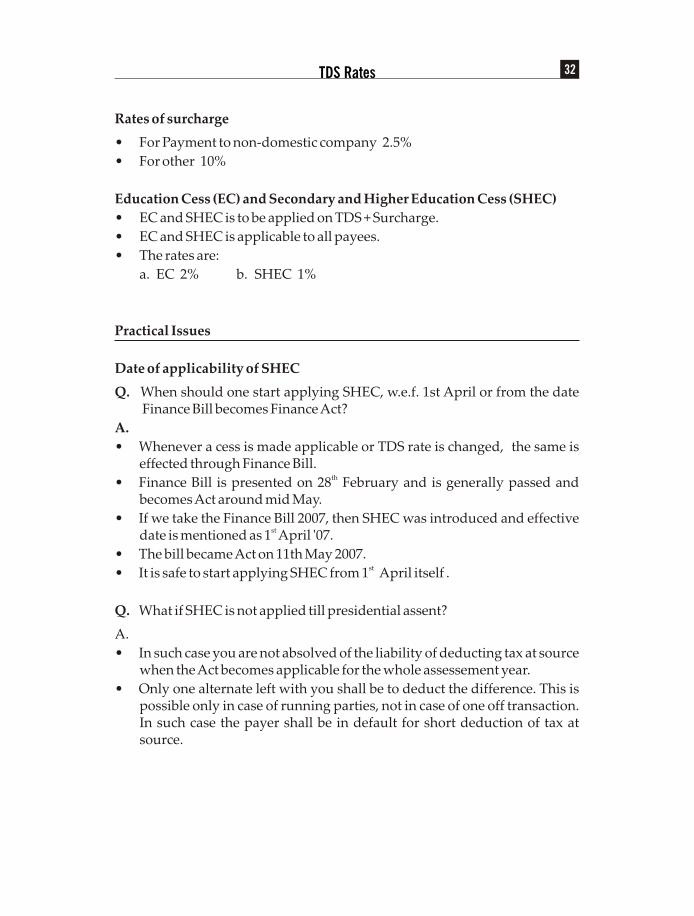

Rates of surcharge

• For Payment to non-domestic company 2.5%

• For other 10%

Education Cess (EC) and Secondary and Higher Education Cess (SHEC)

• EC and SHEC is to be applied on TDS + Surcharge.

• EC and SHEC is applicable to all payees.

• The rates are:

a. EC 2% b. SHEC 1%

Practical Issues

Date of applicability of SHEC

Q. When should one start applying SHEC, w.e.f. 1st April or from the date Finance Bill becomes Finance Act?

A.

• Whenever a cess is made applicable or TDS rate is changed, the same is effected through Finance Bill.

th• Finance Bill is presented on 28 February and is generally passed and becomes Act around mid May.

• If we take the Finance Bill 2007, then SHEC was introduced and effective stdate is mentioned as 1 April '07.

• The bill became Act on 11th May 2007.st• It is safe to start applying SHEC from 1 April itself .

Q. What if SHEC is not applied till presidential assent?

A.

• In such case you are not absolved of the liability of deducting tax at source when the Act becomes applicable for the whole assessement year.

• Only one alternate left with you shall be to deduct the difference. This is possible only in case of running parties, not in case of one off transaction. In such case the payer shall be in default for short deduction of tax at source.

TDS Rates 32

Surcharge applicability

Q. How to decide about the applicability of the surcharge on TDS for

payment exceeding Rs.10 lacs for individuals (and Rs.1 crore for

companies /Firms )? Is it based on payment or net income of the payee?

A..

• Surcharge is based on amount being paid to the individual and not on

individual's income. Payer cannot assess the income of the payee. Hence

criterion remains payment only.

• The words used in the Act are where the 'income paid or likely to be paid

exceeds Rs.10 lacs. If you are paying any individual an amount exceeding

Rs. 10 lacs then only the question of levy of surcharge arises.

• If for instance, Rs.8 lacs have been paid so far in the year then surcharge

need not be levied.

• However if further Rs.3 lacs are to be paid to the same individual then

TDS has to be deducted with surcharge on entire amount of 11 lacs.

33 TDS Rates