sec priorities and enforcement trends · •ocie national examination program ... •consistent...

TRANSCRIPT

2016 In House Counsel Conference

SEC PRIORITIES AND

ENFORCEMENT TRENDS

Presenters:

• Kimberly Burke – Senior Counsel, Novocure

• Andrew J. Brady – Akin Gump, Corporate & Securities

• Jeffery A. Dailey – Akin Gump, SEC Enforcement and

Litigation

2

Overview• Proxy Access Developments

• Shareholder Proposal Trends

• Say-on-Pay Results and Strategies

• Audit Committee Governance and Disclosure Issues

• Shareholder Activism

• Compensation Litigation Update

• Cybersecurity

• SEC Rulemaking

• OCIE National Examination Program

• SEC Enforcement Trends

• Whistleblower Considerations

3

PROXY ACCESS

DEVELOPMENTS

4

Proxy Access – Defining Issue in 2015

• Proxy access was the defining issue of the 2015 proxy season

• 115 companies received shareholder proposals requesting a bylaw

amendment to permit large, long-standing shareholders to include

their director nominees in the company proxy materials

• Up from 18 in 2014

• Due largely to the Boardroom Accountability Project of the NYC

Comptroller

• Comptroller submitted 75 proxy access proposals that requested proxy

access for shareholders that

• owned 3% of the company’s stock

• for at least 3 years

• for up to 25% of the board

• 95 proposals went to vote

• 60% of the proposals passed, up from 28% in 2014

• Average support was 54%, up from 34% in 2014

5

Proxy Access – Where Are Now?

• ~130 issuers (27% of the S&P 500) have adopted proxy

access bylaws or committed to do so

6

Proxy Access – Where Are Now?

• Most company bylaws track the 3% for 3 years ownership

thresholds of the SEC’s voided rule

• Nearly all set limits for the number of board seats

• Greater of 20% or 2 board seats is the most common

• Nearly all set shareholder aggregation limits

• 20 shareholder limit is the most common

• Second tier limitations prevalent

• Resubmission and post-meeting holding requirements most

common

7

Proxy Access – Remains Center Stage

in 2016• 2016 expected to feature as many/more proxy access proposals than

2015

• Through January, ~120 proxy access shareholder proposals have

been submitted

• The debate is moving from whether to adopt proxy access to when to

adopt and with what terms

• Debate on terms rapidly moving away from ownership thresholds,

nominee caps and aggregation limits to second tier/fine print

limitations

• Advance notice deadlines

• Calculating qualifying ownership

• Nominee resubmission limitations

• Continued ownership requirements

• Third party compensation limitations

8

SHAREHOLDER

PROPOSAL TRENDS

9

Shareholder Proposals – What to

Expect• In 2015, shareholders submitted 950 shareholder

proposals

• 2016 is expected to be equally as busy

• If past is prologue, popular shareholder proposals in 2016

will include:

• Proxy access

• Independent chair proposals

• Environmental and social proposals

• Corporate political activity proposals

1

0

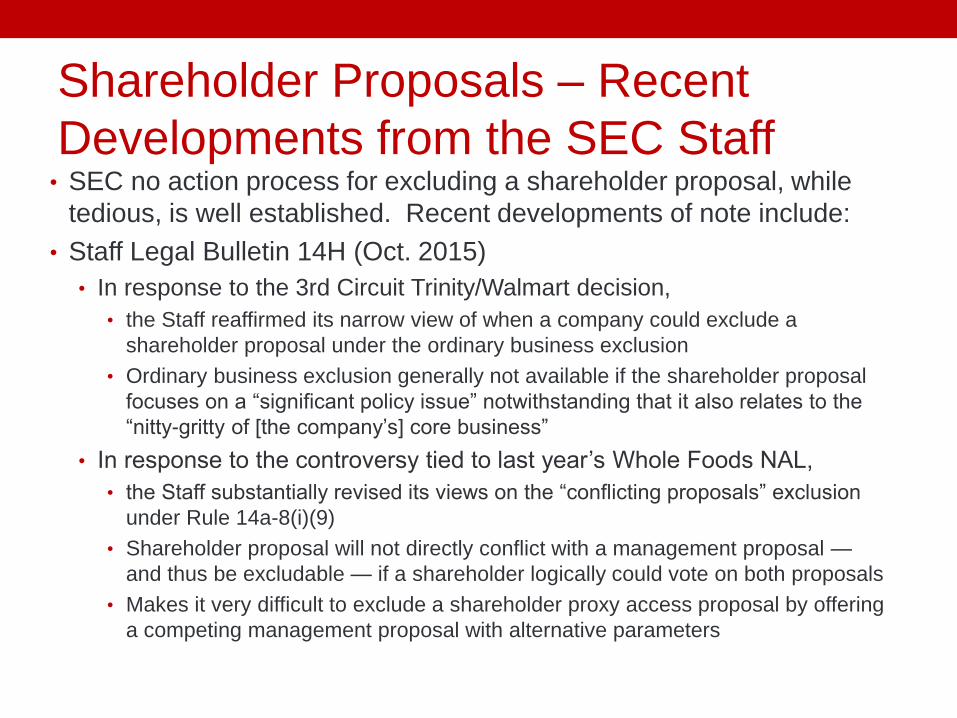

Shareholder Proposals – Recent

Developments from the SEC Staff• SEC no action process for excluding a shareholder proposal, while

tedious, is well established. Recent developments of note include:

• Staff Legal Bulletin 14H (Oct. 2015)

• In response to the 3rd Circuit Trinity/Walmart decision,

• the Staff reaffirmed its narrow view of when a company could exclude a

shareholder proposal under the ordinary business exclusion

• Ordinary business exclusion generally not available if the shareholder proposal

focuses on a “significant policy issue” notwithstanding that it also relates to the

“nitty-gritty of [the company’s] core business”

• In response to the controversy tied to last year’s Whole Foods NAL,

• the Staff substantially revised its views on the “conflicting proposals” exclusion

under Rule 14a-8(i)(9)

• Shareholder proposal will not directly conflict with a management proposal —

and thus be excludable — if a shareholder logically could vote on both proposals

• Makes it very difficult to exclude a shareholder proxy access proposal by offering

a competing management proposal with alternative parameters

1

1

Shareholder Proposals – Recent

Developments from the SEC Staff• In February 2015, the Staff granted no-action relief to 15 of 18 companies that sought to exclude

proxy access shareholder proposals under Rule 14a-8(i)(10) on the basis that the company had

substantially implemented the proposal via an existing access bylaw

• The letters outline the boundaries of substantial implementation under various fact patterns. As

summarized below, the companies’ access bylaws differed from the shareholder proposals in

multiple ways, and the Staff refused no-action relief only where a bylaw provided proxy access for

shareholders owning 5% of the shares, and the shareholder proposal sought a 3% ownership

threshold

1

2

Issue Shareholder Proposal Company Bylaw No-Action Relief

Ownership Threshold 3% 5% Refused

Number of Nominees Greater of 25% or 2 Greater of 20% or 2 Granted

Nominating Shareholder

Group SizeUnlimited 20 Granted

Limitation on Nominees

No additional

limitations that do not

apply to board

nominees

Nominees receiving less than 25% of the vote

prohibited in the following two years;

additional restrictions such as nominees may

not serve as an officer or director of a

competitor or be the subject of a criminal

proceeding

Granted

SAY-ON-PAY RESULTS AND

STRATEGIES

13

Say-on-Pay – 2015 Results

• With respect to say-on-pay (SOP) proposals during the

2015 proxy season, approximately:

• 77% passed with more than 90% support

• 15% passed with between 70.1% and 90% support

• 5% passed with between 50% and 70% support

• 3% (54 companies) obtained less than 50% support

• Overall, the results reflect slightly higher levels of support

than during the 2014 proxy season

1

4

Say-on-Pay – Continued Vigilance in

2016 is Critical• Nearly 75% of companies that failed the SOP vote last year had a

passing vote in 2014

• Sudden reversals typically tied to year-over-year changes in ISS or

Glass Lewis recommendations

• Reasons for negative recommendation:

• “Pay for performance disconnect” (as determined by ISS/Glass Lewis

methodology)

• Emphasis on time-based equity awards as compared to performance-

based

• Retention bonuses and mega equity grants

• Insufficiently challenging performance goals

• Termination and severance payments to outgoing CEO, particularly in a

“friendly” termination

• Negative recommendation typically lowers investor support by almost

30%1

5

Say-on-Pay – Key Drivers of a

Successful Result• Companies need to educate themselves on what pay

practices will be problematic

• Regular engagement with all significant shareholders and

proxy advisors on pay practices

• If necessary, proactively address any pay-for-performance

disconnect tied to changes in the company’s

compensation programs and/or poor performance

• Make clear in proxy why changes are, or are not, being

made

1

6

AUDIT COMMITTEE

GOVERNANCE AND

DISCLOSURE ISSUES

17

Audit Committee Governance and

Disclosure Issues• Overload

• In December 2015 speech, SEC Chair White expressed concern about the recent

trend of assigning duties to audit committees beyond their core regulatory

obligations

• Concern is that increased workload will dilute the amount of time the Audit

Committee can spend on its core duties

• Audit Committee Composition

• Chair White also questioned whether directors who serve on multiple boards,

including multiple audit committees, can fulfill their core duties effectively

• Audit Committee Report

• Increasing numbers of companies are including more robust proxy statement

disclosure regarding the appointment, compensation and oversight of the

independent auditor

• Chair White has strongly supported expanded Audit Committee Report disclosure

that addresses not only whether the Audit Committee satisfied its mandated duties

but how it did so

1

8

SHAREHOLDER

ACTIVISM

19

Shareholder Activism

• Shareholder “activism,” which has exploded in the past decade,

represents a range of activities by one or more of a publicly traded

corporation’s shareholders that are intended to result in some change

in the corporation

• The activities fall along a spectrum based on the significance of the

desired change and the assertiveness of the investors’ activities,

ranging from hedge fund activists seeking a significant change to a

company’s strategy, financial structure, management, or board to

individual shareholders seeking a “say on pay” advisory vote

• Activist investors have evolved from “corporate gadflies” to powerful

and increasingly dominant forces as they have gained support and

credibility from institutional investors

• According to a recent survey of more than 350 mutual fund

managers, half had been contacted by an activist in the past year,

and 45% of those contacted decided to support the activist

2

0

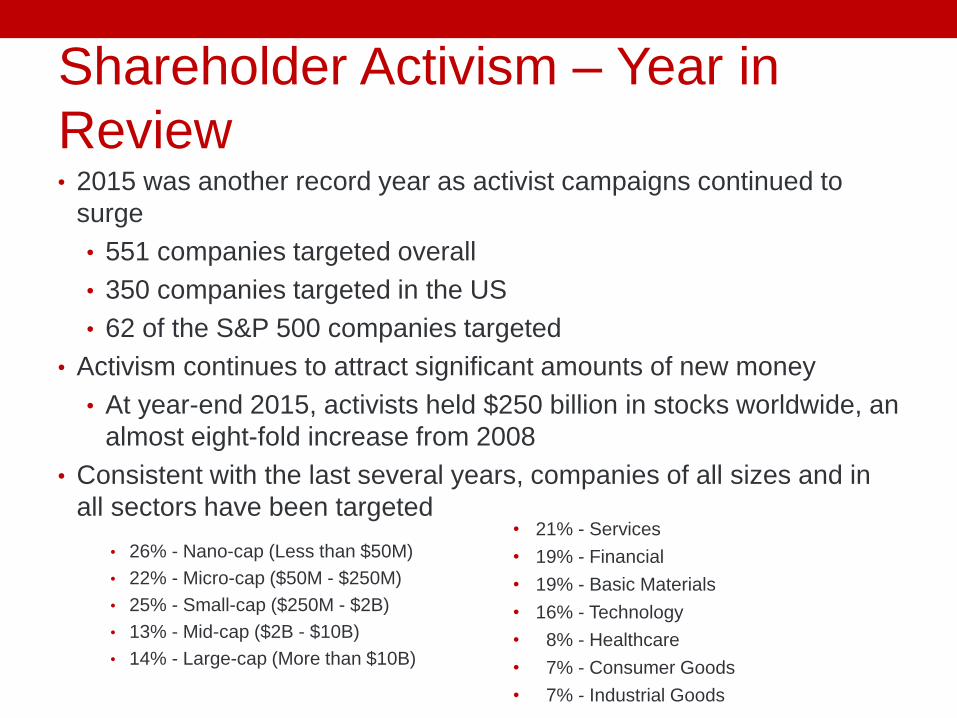

Shareholder Activism – Year in

Review• 2015 was another record year as activist campaigns continued to

surge

• 551 companies targeted overall

• 350 companies targeted in the US

• 62 of the S&P 500 companies targeted

• Activism continues to attract significant amounts of new money

• At year-end 2015, activists held $250 billion in stocks worldwide, an

almost eight-fold increase from 2008

• Consistent with the last several years, companies of all sizes and in

all sectors have been targeted

21

• 26% - Nano-cap (Less than $50M)

• 22% - Micro-cap ($50M - $250M)

• 25% - Small-cap ($250M - $2B)

• 13% - Mid-cap ($2B - $10B)

• 14% - Large-cap (More than $10B)

• 21% - Services

• 19% - Financial

• 19% - Basic Materials

• 16% - Technology

• 8% - Healthcare

• 7% - Consumer Goods

• 7% - Industrial Goods

Shareholder Activism – Year in Review

• Activist demands remained largely the same from prior

years

• 50% - Board-related

• 20% - Mergers & acquisitions

• 12% - Balance sheet

• 9% - Operational

• Activist campaigns experienced increasingly successful

campaigns in 2015

• 60.7% success rate globally

• 68.6% success rate in the US

• However, activist-targeted US stocks were down 7.7% on

an annualized basis for the year

2

2

Shareholder Activism – Looking Ahead

• Expected to remain a major concern for Boards in 2016

• 2016 brings certain wildcards not seen in recent years

• underwhelming performance by many activist funds in 2015

• volatile, and until recently, negative market indices in 2016

• If these factors persist, look for a drop in the number of

activist campaigns and a slowdown in the inflows to

activist funds (or maybe net outflows)

2

3

Shareholder Activism – How to Prepare

• Corporate preparedness and consistent, proactive

shareholder engagement are critical to successfully

addressing activism in all forms

• Preparedness in 3 steps:

• Conduct vulnerability assessments and identify likely strategies that

activists might use to “unlock value”

• Create “response teams” to develop a game plan that addresses

various activist scenarios

• Engage shareholders and prepare a shareholder support analysis

2

4

Shareholder Activism – Shareholder

Engagement• Must articulate a clear strategic plan and vision for

creating shareholder value (dually useful for performing

vulnerability assessments)

• Engagement should be consistent and sustained; not

limited to proxy season, earnings calls and investor days

• Companies should consider developing, adopting and

disclosing a formal shareholder engagement program

• Engagement building blocks include:

• One-on-one meetings and calls

• Governance roadshow (one on-one and/or group meetings)

• Responding to letters from shareholders

• Director involvement

• Enhancing proxy disclosure2

5

COMPENSATION LITIGATION

UPDATE

26

Compensation Litigation Update

• Recent years have seen numerous lawsuits alleging breaches of

fiduciary duties in connection with allegedly inadequate proxy

statement disclosure related to Say-on-Pay votes and Equity Plan

Proposal votes

• These claims appear to have run their course

• Plaintiffs are testing fiduciary duty claims related to purported

excessive director compensation

• In the recent Calma v. Templeton and Espinoza v. Zuckerberg litigation, the

Delaware Chancery Court has refused to apply the business judgment rule

with respect to stock awards granted to non-employee directors under

stock incentive plans that did not include a specific limit on grants to non-

employee directors

• Facebook very recently announced a settlement of its litigation after the

Chancery Court disagreed that Zuckerberg’s informal ratification of Non-

Employee Director compensation (he controlled 61% of the vote) was

sufficient to shift the review to the BJR presumption2

7

Compensation Litigation Update

• The Facebook settlement requires:

• Amendments to the Compensation & Governance Committee

Charter

• Shareholder votes at the 2016 meeting on separate proposals

related to Non-Employee Directors compensation:

• a proposal to ratify prior grants

• a proposal to approve the Non-Employee Director compensation plan,

which includes specific limits on annual equity grants and annual

retainer fees going forward

• Action item

• Strongly consider new provisions to add meaningful limits to the

size of awards and retainer fees to non-employee directors in new

or amended equity incentive plans

2

8

CYBERSECURITY

29

Cybersecurity – Disclosure Landscape

• No existing disclosure requirement refers specifically to cybersecurity

risks or cyber incidents

• But via CF Disclosure Guidance, Topic 2, dated October 2011, the

Staff has expressed it views regarding disclosure obligations relating

to cybersecurity risks and cyber incidents:

• Risk Factors. Disclose cybersecurity risks, taking into account the

occurrence, frequency and severity of prior cybersecurity incidents, as well

as the potential costs and other consequences associated with such

incidents

• MD&A. Consider whether the costs or other consequences associated

with known data breaches or the risk of such events could require MD&A

disclosure.

• Description of Business. Disclose any cyber incidents that materially

affect the company's products, services, relationships with customers or

suppliers or competitive conditions

• Legal Proceedings. Disclose any material pending legal proceeding that

relates to a cybersecurity incident 3

0

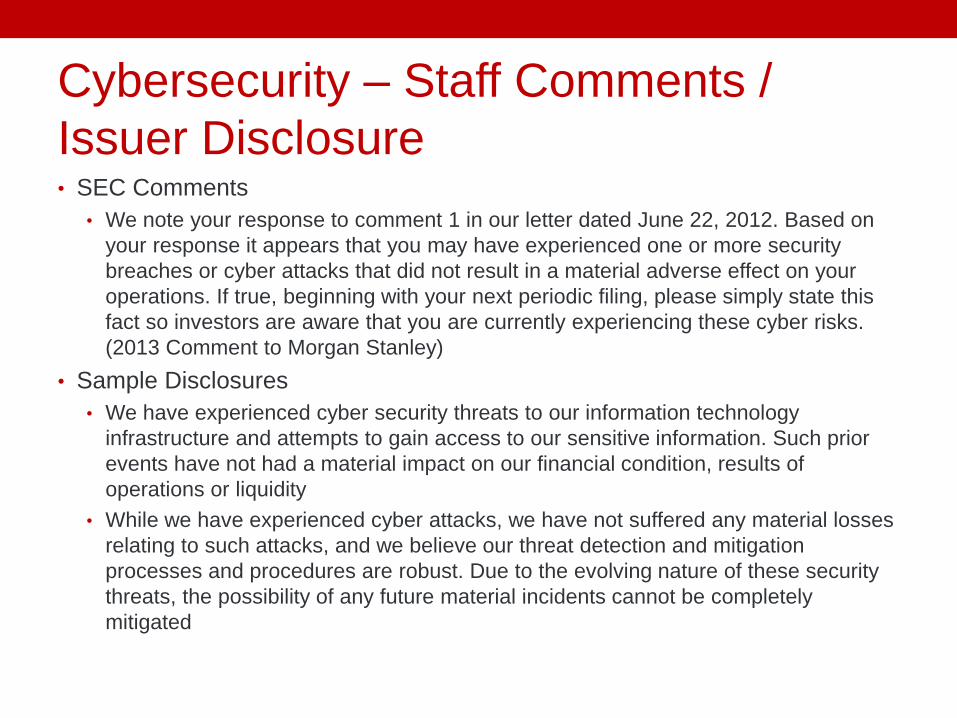

Cybersecurity – Staff Comments /

Issuer Disclosure• SEC Comments

• We note your response to comment 1 in our letter dated June 22, 2012. Based on

your response it appears that you may have experienced one or more security

breaches or cyber attacks that did not result in a material adverse effect on your

operations. If true, beginning with your next periodic filing, please simply state this

fact so investors are aware that you are currently experiencing these cyber risks.

(2013 Comment to Morgan Stanley)

• Sample Disclosures

• We have experienced cyber security threats to our information technology

infrastructure and attempts to gain access to our sensitive information. Such prior

events have not had a material impact on our financial condition, results of

operations or liquidity

• While we have experienced cyber attacks, we have not suffered any material losses

relating to such attacks, and we believe our threat detection and mitigation

processes and procedures are robust. Due to the evolving nature of these security

threats, the possibility of any future material incidents cannot be completely

mitigated

3

1

Cybersecurity – Disclosure Controls

and Procedures• Disclosure Controls and Procedures Definition

• “Controls and other procedures designed to ensure that (i)

information required to be disclosed by the Company in reports

filed or submitted under the Securities Exchange Act of 1934, as

amended, is recorded, processed, summarized and reported

accurately and on a timely basis and (ii) information is accumulated

and communicated to management of the Company, including the

Certifying Officers, as appropriate to allow timely decisions

regarding such required disclosure.” (Rule 13a-14)

• Cybersecurity Implications

• Failure to provide appropriate disclosure regarding material

security breaches could reflect ineffective disclosure controls and

procedures

3

2

Cybersecurity – Internal Control Over

Financial Reporting

• Internal Control Over Financial Reporting Definition

• A process to provide, among other things, “reasonable assurance

regarding prevention or timely detection of unauthorized

acquisition, use or disposition of the issuer's assets that could have

a material effect on the financial statements.” (Rule 13a-15(f))

• Cybersecurity Implications

• The failure to prevent the unauthorized acquisition, use, and/or

disposition of customer data, intellectual property, or other

company assets stored on a company's information systems may

constitute a material weakness in a company's internal control over

financial reporting

3

3

Cybersecurity – SEC Enforcement

Lurking• SEC reportedly is pursuing several enforcement actions involving

companies that have experienced cyber security breaches

• In these cases, the SEC is pursuing several theories of potential

liability, including the theory that the companies violated their

disclosure obligations and had shortcomings in their disclosure

controls in connection with their failure to adequately disclose cyber

security breaches and related matters

• The SEC is also pursuing companies based on perceived

shortcomings of their internal control over financial reporting to the

extent that unauthorized persons are able to access, steal, or destroy

material assets on their information technology systems

• In February 2016, Deputy Director of Enforcement, Stephanie

Avakian publicly acknowledged that the Enforcement staff was

“focusing” on cyber failures, further putting public companies on

notice

3

4

SEC RULEMAKING

35

CEO Pay Ratio Disclosure – Final Rule

• August 2015: SEC adopted final rules to implement the “CEO Pay

Ratio” requirements mandated by Dodd-Frank

• Covered public companies must disclose:

• The median of the annual total compensation of all employees, except the

CEO

• The annual total compensation of the CEO

• The ratio of these two amounts

• Covered companies include:

• All companies that are required to provide summary compensation table

disclosures pursuant to Item 402(c) of Regulation S-K

• EGCs, SRCs, FPIs, MJDS filers and registered investment companies,

none of which are subject to Item 402(c), are exempt

• Compliance date: January 1, 2017. For calendar year companies,

the pay ratio disclosure will not appear until the 2018 proxy statement

(covering FY ended 2017)3

6

CEO Pay Ratio Disclosure – Final Rule

• Transition periods for certain covered companies

• New public companies must provide pay ratio disclosure for the first full FY after the

company has (i) been subject to the Exchange Act reporting requirements for at

least 12 calendar months beginning on or after January 1, 2017, and (ii) filed at least

one annual report that does not contain the pay ratio disclosure

• Companies that cease to qualify as a SRC or EGC must provide pay ratio disclosure

in the first full fiscal year after they exit SRC or EGC status (but not for any FY

commencing prior to January 1, 2017)

• Covered Filings

• Annual reports on Form 10-K, registration statements, and proxy and information

statements that require executive compensation disclosure under Item 402(c) of

Regulation S-K

• Not required for an IPO on Form S-1 or Form S-11 or in an initial registration

statement on Form 10

• Liability

• Pay ratio disclosure will be treated as “filed” (rather than “furnished”) for purposes of

the Securities Act and Exchange Act

3

7

CEO Pay Ratio Disclosure – Action

Items • Brief the Board and/or Compensation Committee on the

new rules

• Organize an internal team to comply with the new rules

• Evaluate alternative methods (e.g., statistical sampling) for

identifying median employee

• Select a testing date for employee population/median employee

• Identify median employee once every three years

• Determine whether certain non-US employees may be excluded

• Consider COLA adjustments to align median employee to CEO

jurisdiction

• 2017 proxy season “test drive”

• Dry run the numbers and begin to develop internal and external

messaging discussing the results

3

8

Pay-for-Performance Disclosure –

Proposed Rule• April 2015: SEC proposed rules that would require new tabular and

narrative disclosure in a proxy statement or information statement in

which executive compensation is required

• The new table would require:

• Total compensation reported in the Summary Compensation Table for the

PEO and the average of the reported amounts of total compensation for

the remaining NEOs identified in the SCT

• Compensation actually paid the PEO plus the average compensation

actually paid to all other NEOs

• Compensation actually paid is the total compensation adjusted to include (i) for

pension benefits, only the annual pension service cost for services rendered

during the applicable year, and (ii) for equity awards, only the fair value of the

awards that vested during the year

• The company’s annual total shareholder return (TSR) for the last five years

• The TSR of the company’s peer group

3

9

Pay-for-Performance Disclosure –

Proposed Rule

4

0

Pay-for-Performance Disclosure –

Proposed Rule• Narrative disclosure: a clear description of the relationship between

the compensation actually paid to the PEO and other NEOs and the

company’s TSR

• Narrative or graphic disclosure: a comparison of the relationship

between the company’s TSR and the TSR of the company’s identified

peer group

• Covered companies

• All public companies that file proxy or information statements would be

subject to the proposed rule

• EGCs, FPIs, and registered investment companies are exempt

• Phase-in / transitional relief

• For companies other than SRCs, the proposed rule would be phased in

over three years, with three years of disclosure initially required and five

years of disclosure eventually required

• SRCs initially would be required to disclose two years of information and

three years of information thereafter 4

1

Pay-for-Performance Disclosure –

Implementation Issues and Compliance

Dates• Staff is aware of significant external debate on the use of

TSR as the performance indicator against which pay

should be measured

• Staff is trying to craft a rule that permits comparability

among companies by standardizing the way companies

report the pay-for-performance in the CD&A

4

2

Pay-for-Performance Disclosure –

Action Items• Begin internal dialogue (Compensation Committee,

Board, HR)

• Onboard compensation consultants or external counsel

early if necessary

• Prepare to revalue equity awards each year from the

grant date until the time of vesting (i.e., the definition of

“earned compensation actually paid” includes an

incremental compensation earned concept)

• Begin to develop shell proxy table and language

• Company’s historical discussion around pay and performance may

be highly compatible with the proposed rules or significant

reordering may be required

4

3

Clawback Policy – Proposed Rule

• July 2015: SEC proposed rules that would require companies with stock

exchange listed securities to adopt “clawback” policies to recover incentive-

based compensation following certain accounting restatements

• Required policy. Must provide that the company will recover incentive-

based compensation from current and former executive officers who received

such compensation during the three fiscal years preceding the date on which

the company is required to prepare an accounting restatement resulting from

material noncompliance with any financial reporting requirement

• No fault. Recovery would be required on a “no fault” basis, i.e., without

regard to whether any misconduct occurred (by anyone) and without regard

to an executive officer’s responsibility for the erroneous financial statements

• Incentive-based compensation. Any compensation that is granted, earned

or vested based wholly or in part on the attainment of any financial reporting

measure

4

4

Clawback Policy – Proposed Rule

• Financial reporting measure. Includes (i) measures that are based on the

accounting principles used in preparing the company’s financial statements,

(ii) any measures derived wholly or in part from such financial information,

and (iii) stock price and total shareholder return

• Amounts subject to be recovered. The amount of incentive-based

compensation that exceeds what the executive officer would have received

had the incentive-based compensation been determined based on the

restated results

• Discretion not to recover. If (i) direct third-party expenses would exceed

the amount to be recovered, (ii) for FPIs, recovery would violate home

country law, or (iii) after a reasonable attempt to recover, the Comp.

Committee or a majority of independent directors concludes recovery is

“impracticable”

• Issuers subject to the proposed rules. All listed issuers, including FPIs,

EGCs, SRCs, controlled companies and registered investment companies

with listed securities

4

5

Clawback Policy – Action Items

• Begin internal dialogue (Comp Comte, Board, HR,

Finance)

• Review existing clawback policies, if any, for any

necessary conforming changes.

• Review current plans, programs, agreements with

executive officers that provide for incentive compensation

tied to financial metrics

• Consider adding clawback language to incorporate final

rules into any new plans, grants, agreements

• Develop messaging that will communicate the company’s

policy to executive officers

4

6

Hedging Policy Disclosure – Proposed

Rule• February 2015: SEC proposed rules that would require disclosure regarding

whether directors, officers and other employees are permitted to hedge or

offset any decrease in the market value of equity securities granted by the

company as compensation or held, directly or indirectly, by employees or

directors

• Relevant Disclosure Document. Proxy and information statements filed with

respect to the election of directors

• Disclosure or Prohibition Against Hedging. The proposed rule would

require disclosure regarding whether a company permits any employees or

directors to engage in hedging but the rule would not prohibit such

transactions. Rather, the disclosure would identify the categories of persons

covered by the hedging policy (and those not covered), as well as the

categories of transactions that are permitted (and those that are not)

• Note, public companies, other than SRCs, EGCs, FPIs, and registered investment

companies, already are required to disclose in the CD&A section of their proxy

statements any company policies on hedging by their NEOs, if material

4

7

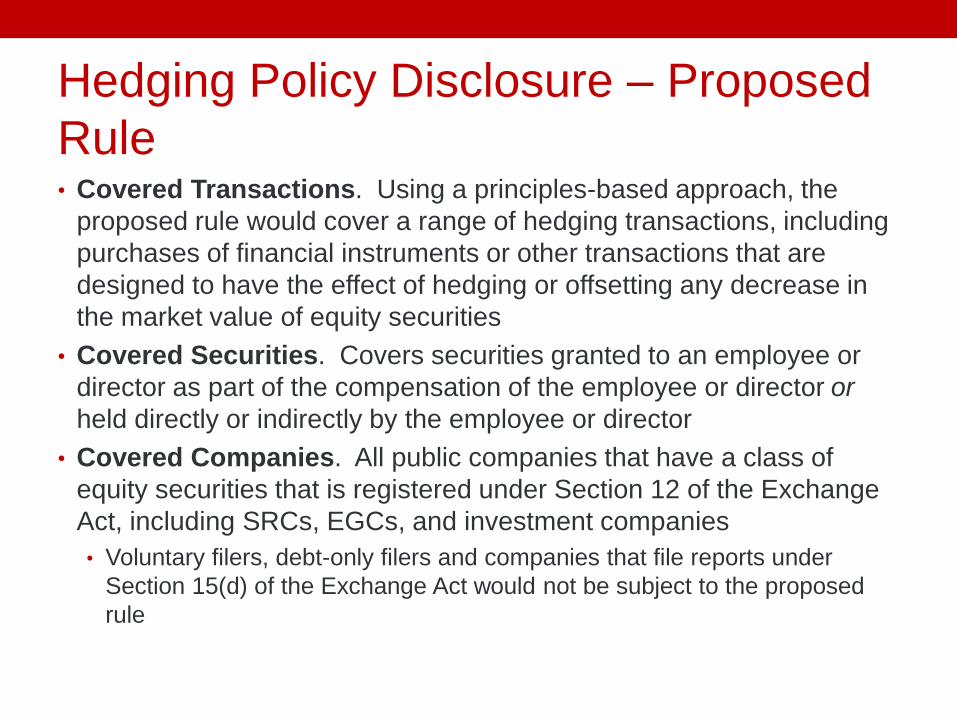

Hedging Policy Disclosure – Proposed

Rule• Covered Transactions. Using a principles-based approach, the

proposed rule would cover a range of hedging transactions, including

purchases of financial instruments or other transactions that are

designed to have the effect of hedging or offsetting any decrease in

the market value of equity securities

• Covered Securities. Covers securities granted to an employee or

director as part of the compensation of the employee or director or

held directly or indirectly by the employee or director

• Covered Companies. All public companies that have a class of

equity securities that is registered under Section 12 of the Exchange

Act, including SRCs, EGCs, and investment companies

• Voluntary filers, debt-only filers and companies that file reports under

Section 15(d) of the Exchange Act would not be subject to the proposed

rule

4

8

Hedging Policy Disclosure – Action

Items• With the negative light that ISS and Glass Lewis have

cast on hedging (and pledging) by executive officers, an

increasing number of companies already have adopted

policies that prohibit hedging and, pursuant to existing

CD&A requirements, disclosed such policies in their proxy

statements

• Companies should consider the additional proposed

disclosure requirements in connection with any review of

their existing hedging policies or any determination to

adopt a hedging policy

4

9

NATIONAL EXAMINATION

PROGRAM - OCIE

50

OCIE Exam Priorities

• “In general, the priorities reflect certain practices and

products that OCIE perceives to present potentially

heightened risk to investors and/or the integrity of the U.S.

capital markets.”

• Priorities organized around same three thematic areas as

in 2015:1. “Examining matters of importance to retail investors, including investors

saving for retirement”;

2. “Assessing issues related to market-wide risks”; and

3. “Using our evolving ability to analyze data to identify and examine

registrants that may be engaged in illegal activity.”

5

1

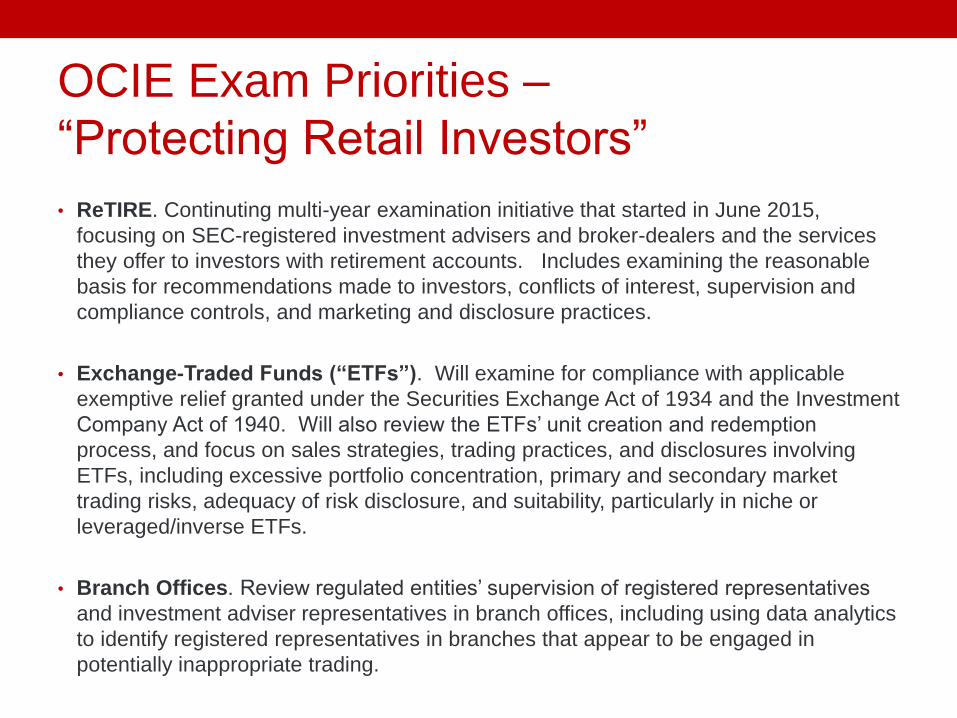

OCIE Exam Priorities –

“Protecting Retail Investors”

• ReTIRE. Continuting multi-year examination initiative that started in June 2015,

focusing on SEC-registered investment advisers and broker-dealers and the services

they offer to investors with retirement accounts. Includes examining the reasonable

basis for recommendations made to investors, conflicts of interest, supervision and

compliance controls, and marketing and disclosure practices.

• Exchange-Traded Funds (“ETFs”). Will examine for compliance with applicable

exemptive relief granted under the Securities Exchange Act of 1934 and the Investment

Company Act of 1940. Will also review the ETFs’ unit creation and redemption

process, and focus on sales strategies, trading practices, and disclosures involving

ETFs, including excessive portfolio concentration, primary and secondary market

trading risks, adequacy of risk disclosure, and suitability, particularly in niche or

leveraged/inverse ETFs.

• Branch Offices. Review regulated entities’ supervision of registered representatives

and investment adviser representatives in branch offices, including using data analytics

to identify registered representatives in branches that appear to be engaged in

potentially inappropriate trading.

5

2

OCIE Exam Priorities –

“Protecting Retail Investors” (con’t)

• Fee Selection and Reverse Churning. Will examine the variety of fee arrangements

(e.g., asset-based fees, hourly fees, wrap fees, commissions), and focus on

recommendations of account types and whether the recommendations are in the best

interest of the retail investor at the inception of the arrangement and thereafter,

including fees charged, services provided, and disclosures made about such

arrangements.

• Variable Annuities. Will examine the suitability of sales of variable annuities to

investors (e.g., exchange recommendations and product classes), as well as the

adequacy of disclosure and the supervision of such sales.

• Public Pension Advisers. Will examine advisers to municipalities and other

government entities, focusing on pay-to-play and certain other key risk areas related to

advisers to public pensions, including identification of undisclosed gifts and

entertainment.

5

3

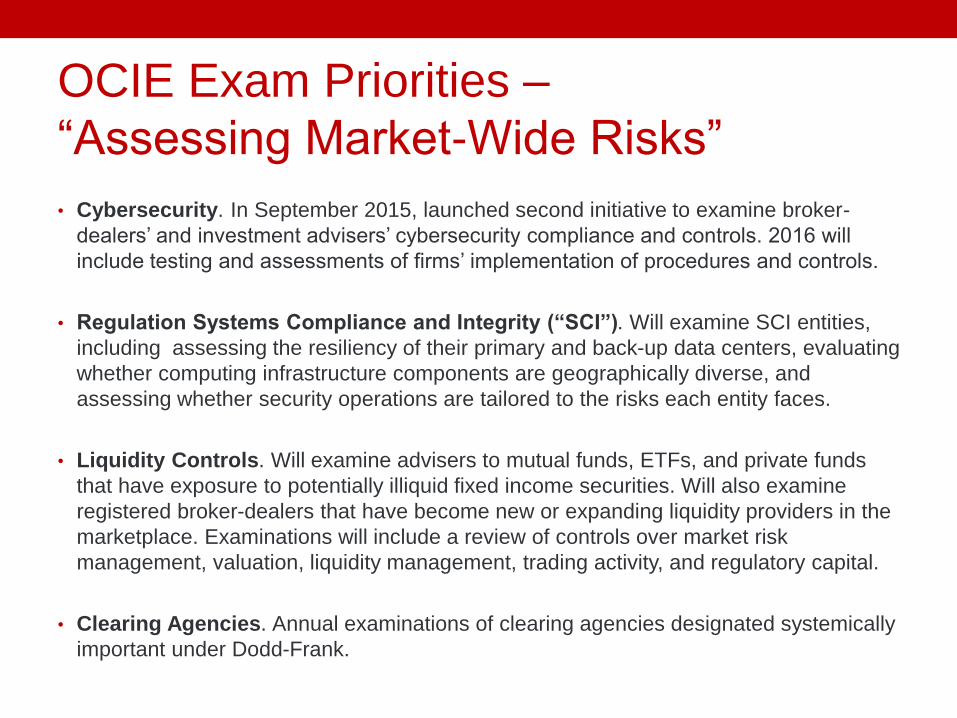

OCIE Exam Priorities –

“Assessing Market-Wide Risks”

• Cybersecurity. In September 2015, launched second initiative to examine broker-

dealers’ and investment advisers’ cybersecurity compliance and controls. 2016 will

include testing and assessments of firms’ implementation of procedures and controls.

• Regulation Systems Compliance and Integrity (“SCI”). Will examine SCI entities,

including assessing the resiliency of their primary and back-up data centers, evaluating

whether computing infrastructure components are geographically diverse, and

assessing whether security operations are tailored to the risks each entity faces.

• Liquidity Controls. Will examine advisers to mutual funds, ETFs, and private funds

that have exposure to potentially illiquid fixed income securities. Will also examine

registered broker-dealers that have become new or expanding liquidity providers in the

marketplace. Examinations will include a review of controls over market risk

management, valuation, liquidity management, trading activity, and regulatory capital.

• Clearing Agencies. Annual examinations of clearing agencies designated systemically

important under Dodd-Frank.

5

4

OCIE Exam Priorities –

“Using Data Analytics”

• Recidivist Representatives and their Employers. Identify individuals with a track

record of misconduct and examine the firms that employ them. Will assess the

compliance oversight and controls of investment advisers that have employed such

individuals after they have been disciplined or barred from a broker-dealer.

• Anti-Money Laundering (“AML”). Will focus on firms that have not filed the number of

suspicious activity reports (“SARs”) that would be consistent with their business models

or have filed incomplete or late SARs. Will continue to assess broker-dealers’ AML

programs, with a particular emphasis on (1) the adequacy of the independent testing

obligation, to ensure that these programs are robust and are targeted to each firm’s

specific business model, and (2) the extent to which firms consider and adapt, as

appropriate, their programs to current money laundering and terrorist financing risks.

5

5

OCIE Exam Priorities –

“Using Data Analytics” (con’t)

• Microcap Fraud. Will look for activities that indicate broker-dealers and

transfer agents may be engaged in, or aiding and abetting, pump-and-dump

schemes or market manipulation. Will assess whether broker-dealers are

complying with their obligations under the federal securities laws when

publishing quotes for or trading securities in the over-the-counter markets.

• Excessive Trading. Will analyze data, including from clearing brokers, to

identify and examine firms and their registered representatives that appear to

be engaged in excessive or otherwise potentially inappropriate trading.

• Product Promotion. Will focus on detecting the promotion of new, complex,

and high risk products and related sales practice issues to identify potential

suitability issues and potential breaches of fiduciary obligations.

5

6

SEC ENFORCEMENT

TRENDS

57

SEC Enforcement Trends – Financial

Reporting and Audit Task Force• In July 2013, the SEC established the Financial Reporting and Audit Task Force to

identify and prosecute securities law violations relating to false and misleading financial

statements and disclosures

• Task Force uses traditional investigation methods but also technology based tools,

such as analytic accounting quality models and data mining programs

• In December 2015, Chair White gave a speech to AICPA reminding preparers, auditors,

audit committee members, and their advisors of their essential roles in the preparation

of a company’s financial statements and disclosures and warned that SEC would hold

these parties accountable for their actions and inactions

• In February 2016, Chair White touted the “unprecedented number of enforcement

cases” brought by the SEC in 2015 and said that the SEC will continue to focus on

financial reporting and bring enforcement actions relating to missing or inadequate

internal corporate controls

• In March 2016, the SEC settled charges against Magnum Hunter Resources and

several individuals, including audit engagement partner and company consultant, for

deficient evaluation of the company’s ICFR, and failures to maintain ICFR

5

8

SEC Enforcement Developments –

Broken Windows• “Broken windows” enforcement strategy dates to October 2013

speech by Chair White

• “Minor violations that are overlooked or ignored can feed bigger ones, and,

perhaps more importantly, can foster a culture where laws are increasingly

treated as toothless guidelines—and so, I believe it is important to pursue

even the smallest infractions.”

• Broken windows enforcement strategy has resulted in:

• Settled actions in March 2015 against eight officers, directors, or major

shareholders for failing to update Schedules 13D and 13G to reflect

material changes, including steps to take the companies private

• Settled actions in November 2014 against 10 companies for failure to file

current reports on Form 8-K related to the execution of financing

arrangements resulting in dilution to existing shareholders

• Settled actions in September 2014 against 28 officers, directors and major

shareholders for violations related to Schedules 13D and 13G and Forms

3, 4 and 5 filings

5

9

CHIEF COMPLIANCE OFFICERS

• In the Matter of Blackrock Advisers, LLC (April 20, 2015)

• Alleged failure to disclose conflict of interest involving the outside business

activity of a portfolio manager. The portfolio manager had personally

invested $50 million in a Company that had a joint venture with a company

held in the BlackRock funds he managed.

• BlackRock knew of his involvement , the investment and the joint venture,

but failed to disclose the conflict of interest to the BlackRock funds’ boards

of directors or to BlackRock advisory clients.

• BlackRock also failed to adopt and implement written compliance policies

and procedures designed to prevent violations of the Advisers Act and

rules, concerning the outside activities of its employees, including how they

should be assessed and monitored for conflict purposes, and when the

outside activity should be disclosed.

60

CHIEF COMPLIANCE OFFICERS

(Con’t)• In the Matter of Blackrock Advisers, LLC (April 20, 2015) (con’t)

• CCO and others learned no later than January 2007 that the portfolio manager

had formed and funded the entity in violation of Blackrock’s private investment

policy, but concluded that no conflict exited.

• When told in 2010 that the portfolio manager wanted to serve on the Board of

the joint venture, the Legal and Compliance Department did not recall its review

from 2007 and issued a memorandum that concluded that there were potential

conflicts of interest raised by these activities.

• Blackrock allowed him to continue managing the stock positions held, with some

restrictions on his participation with the underlying entities. Blackrock did not

provide any disclosure to the funds’ boards or to advisory clients and did not

follow up to monitor or reassess the portfolio manager’s activities.

• In June of 2012, WSJ published a series of articles detailing the connection

between the portfolio manager and his simultaneous connection to the company

and as portfolio manager at BlackRock.

61

CHIEF COMPLIANCE OFFICERS

(Con’t)• In the Matter of SFX Financial Advisory Management Enter., Inc. (June

15, 2015)

• SFX provided advisory and financial management services to current and former

athletes, including management of investment portfolios, bill payment, financial

planning and tax consultation.

• SFX’s President allegedly misappropriated $670,000 in assets from 3 client accounts

by writing check to “cash” and wired money to himself.

• SEC stated that SFX’s compliance policies and procedures were not reasonably

designed, and were not effectively implemented, to prevent misappropriation.

• SEC also stated that the policies were not designed to prevent circumventing

secondary review of payments, and SFX did not implement required review of “cash

flows in client accounts” for bill paying services.

• SFX’s Form ADV disclosed that these were reviewed several times each week by

senior management for accuracy and appropriateness.

• Failed to conduct annual review of its compliance program in 2011.

62

CHIEF COMPLIANCE OFFICERS

(Con’t)• Statement by Commissioner Daniel M. Gallagher (June 18, 2015)

• “I have long called on the Commission to tread carefully when bringing

enforcement actions against compliance personnel. These recent actions

fly in the face of my admonition, and I feel compelled to explain the

rationale for dissenting.”

• “Both settlements illustrate a Commission trend toward strict liability for

CCOs under Rule 206(4)-7. Actions like these are undoubtedly sending a

troubling message that CCOs should not take ownership of their firm’s

compliance policies and procedures, lest they be held accountable for

conduct that, under Rule 206(4)-7, is the responsibility of the adviser itself.

Or worse, that CCOs should opt for less comprehensive policies and

procedures with fewer specified compliance duties and responsibility to

avoid liability when the government plays Monday morning quarterback.”

63

CHIEF COMPLIANCE OFFICERS

(Con’t)• Statement by Commissioner Luis A. Aguilar (June 29, 2015)

• “…the dissent, and the resulting publicity, has left the impression that the

SEC is taking too harsh of an enforcement stance against CCOs, and

that CCOs are needlessly under siege from the SEC.”

• …”it has been my experience that the Commission does not bring

enforcement actions against CCOs who take their jobs seriously and do

their jobs competently, diligently, and in good faith to protect investors.”

• “…the Commission has brought relatively few cases targeting CCOs

relating solely to their compliance-related activities…Estimates show”

that “enforcement cases brought against these CCOs, compared to

enforcement cases brought against investment advisers and investment

companies” between 2009 and 2014, ranged between 6-11%, except in

2013 when they were 19%.

64

CHIEF COMPLIANCE OFFICERS

(Con’t)• Statement by Commissioner Luis A. Aguilar (June 29, 2015)

(con’t)

• “The vast majority of these cases involved CCOs who ‘wore more

than one hat’…In fact, since the adoption of Rule 206(4)-7 [in

December 2003], enforcement actions against individuals with

CCO-only titles and job functions have been rare…over the last

11 years, the Commission brought only eight cases against such

CCOs.”

• Aguilar cited examples where compliance rules broken, but no

action against CCO because CCO attempted to do job.

65

CHIEF COMPLIANCE OFFICERS

(Con’t)• Other Notable Matters Involving Chief Compliance Officers:

• December 2014 – U.S. Treasury Department’s Financial Crimes

Enforcement Network fined former Chief Compliance Officer of

MoneyGram International for failing to ensure the Company

followed anti-money laundering laws.

• April 2014 – The Financial Regulatory Authority fined former

Chief Compliance Officer at Brown Brothers Harriman for failing

to ensure anti-money laundering rules were followed.

• Some commentators note that other agencies may follow suit

because financial services is the “leading edge” of enforcement

trends that happen before they happen in other industries.

66

WHISTLEBLOWER

CONSIDERATIONS

67

SEC Whistleblower Program

• Monetary awards to eligible individuals who provide

original information about violations of the federal

securities laws resulting in a Commission enforcement

action involving more than $1 million in sanctions.

• Awards can range from 10% to 30% of the money

collected.

• Office of the Whistleblower has established an online

portal that makes it relatively easy for informers to contact

the agency and provide information.

68

SEC Whistleblower Program (con’t)

• According to the WSJ, the SEC has received confidential

information from more than 6,500 people, leading to 5

cases based on information from 8 whistleblowers that

resulted in $150 million in restitution and fines.

• The SEC has doled out more than $15 million to

whistleblowers, including a $14 million award to a single

tipster.

• 0.1% of tips lead to claims.

69

Responding to Whistleblower Complaints

• Responding promptly to allegations from an employee that comes

forward with allegations of securities laws violations, will provide an

opportunity for the company to be proactive and take charge of an issue,

which will put the company in a better position if there is an SEC inquiry.

• Reactive changes to a whistleblower’s status may lead to charges of

retaliation and make the company look defensive.

• Anti-retaliation provisions apply to employees who report securities law

violations internally, but do not contact the SEC.

• SEC Interpretation of the SEC’s Whistleblower Rules Under Section 21F of the

Securities Exchange Act of 1934, Release No. 34-75592 (Aug. 2015)

• Berman v. Neo@Ogilvy LLC (2d Cir.) (Sept. 2015)

• But See, Asadi v. GE Energy United States, LLC (5th Cir, 2013) (Holding that

Dodd-Frank does not protect whistleblowers who only report internally).

70

Retaliation

• $2.2 million settlement

• Hedge fund advisory firm that had allegedly retaliated against a

whistleblower who had contacted the SEC.

• SEC noted that this was the first time it had exercised its

authority to bring an anti-retaliation enforcement action.

• The SEC had alleged that the firm and its principal engaged in

transactions with conflicts of interest without adequate

disclosure and consent, in violation of Section 206(3) of the

Investment Advisors Act of 1940.

• SEC also alleged that the firm had violated Section 21F(h) of

the Securities Exchange Act of 1934 by retaliating against its

head trader after he disclosed that he had reported the

conflicted transactions to the SEC.

71

Implications of Employment Contracts to

Keep Whistleblowing In-House• Whistleblower Chief Sean McKessy has stated that the

SEC is keeping an eye out for creatively drafted contracts

attempting to incentivize company whistleblowers from

bringing alleged company wrongdoing to the agency’s

attention.

• Has stated that SEC will go after Companies and

attorneys who draft such agreements.

72