se 4 q14 slides final v2

TRANSCRIPT

2014 FOURTH QUARTER EARNINGS UPDATE

February 4, 2015

Spectra Energy Growth from a Position of Strength

2014 Fourth Quarter Update | Growth from a position of strength

Safe Harbor Statement

Some of what we’ll discuss today concerning future company performance will

be forward-looking information within the meanings of the securities laws.

Actual results may materially differ from those discussed in these forward-

looking statements, and you should refer to the additional information

contained in Spectra Energy and Spectra Energy Partners’ Forms 10-K and other

filings made with the SEC concerning factors that could cause those results to

differ from those contemplated in today’s discussion. As this is a joint

presentation, the terms “we,” “our,” and “us” refer to Spectra Energy and/or

Spectra Energy Partners, as appropriate.

Reg G Disclosure

In addition, today’s discussion will include certain non-GAAP financial measures

as defined under SEC Regulation G. A reconciliation of those measures to the

most directly comparable GAAP measures is available on our websites.

2

2014 Fourth Quarter Update | Growth from a position of strength

4Q14 Results – EBITDA

3

Spectra Energy Partners Distribution Western Canada Field Services

• Increased earnings from expansions, mainly related to TEAM 2014 and TEAM South placed into service

• Continued ramp up of volumes on Sand Hills and Southern Hills

• Higher crude transportation revenue, mainly due to increased tariff rates on Express

• Decreased earnings from weaker Canadian dollar

• Lower customer usage due to warmer weather

• Higher Empress earnings mainly due to non-cash MTM gains on commodity risk management program, partially offset by lower NGL sales prices

• Higher G&P revenues • Partially offset by weaker

Canadian dollar

• Decreased earnings from: – Lower NGL and crude prices – Increased NCI as a result of

the MTM effect of hedges and growth from dropdowns at DPM

– Partially offset by increased earnings from expansions

PERFORMANCE DRIVERS FOR THE QUARTER:

Ongoing Segment EBITDA ($MM) 4Q14 4Q13 YTD 2014 YTD 2013

Spectra Energy Partners (1) $444 $369 $1,669 $1,440

Distribution 132 156 552 574

Western Canada 250 215 754 736

Field Services (2) (18) 72 229 343

Other 2 (14) (58) (59)

Ongoing SE EBITDA $810 $798 $3,146 $3,034

Ongoing SEP EBITDA(1) $424 $352 $1,591 $1,391 (1) EBITDA for SEP is different than the EBITDA reported for the Spectra Energy Partners segment within SE. The difference is because SEP reports its own Corporate Other when SEP is reported standalone.

These amounts represent the costs of services rendered by SE in support of SEP. These amounts are included in SE’S Corporate Other at the SE level.

(2) Represents equity earnings of DCP + gains from DPM equity issuances. DCP standalone EBITDA (100%) = $246 for 4Q14 & $307 for 4Q13; $1,182 YTD 2014 & $1,157 YTD 2013

2014 Fourth Quarter Update | Growth from a position of strength 4

Spectra Energy: Distributable Cash Flow

(1) Excludes reimbursable expenditures.

SE Distributable Cash Flow ($MM) 4Q14 4Q13 YTD

2014 YTD

2013 Ongoing EBITDA $810 $798 $3,146 $3,034

LESS: Special items – 11 12 34

Reported EBITDA $810 $787 $3,134 $3,000

ADD:

Equity in earnings of unconsolidated affiliates (24) (100) (361) (445)

Distributions from unconsolidated affiliates 107 116 416 348

Empress non-cash items (60) - (60) -

Other (28) (8) (19) 6

LESS:

Interest expense 158 181 679 657

Distributions to noncontrolling interests 47 40 175 144

Maintenance capex (1) 280 229 751 668

Equity AFUDC 20 16 53 105

Net cash paid/(refund) for income taxes (16) 14 (8) 43

Total Distributable Cash Flow $316 $315 $1,460 $1,292

2014 Fourth Quarter Update | Growth from a position of strength

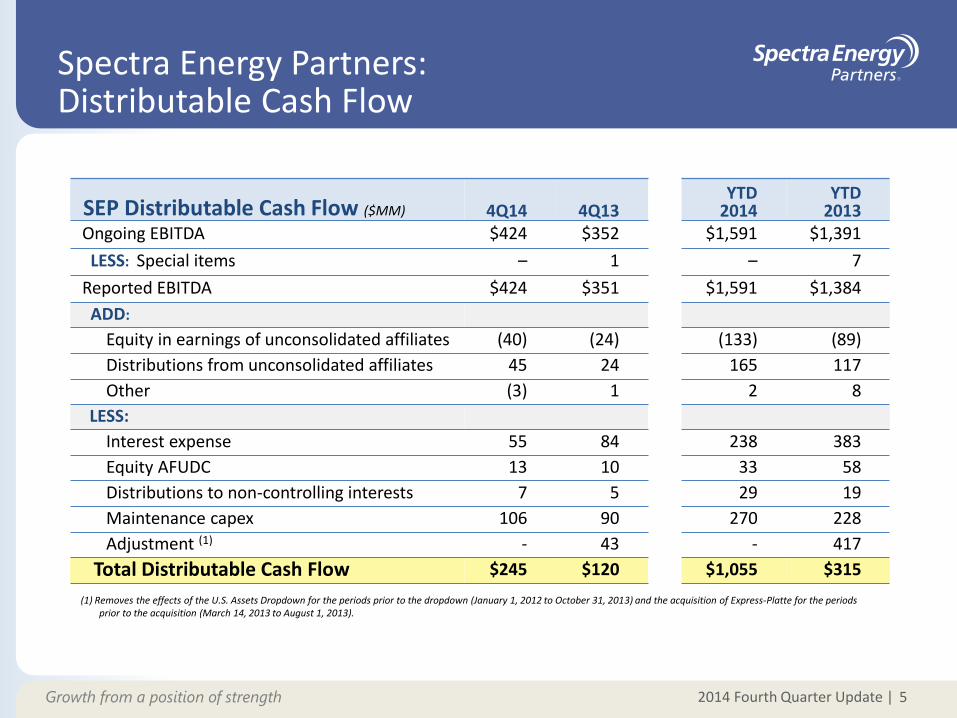

Spectra Energy Partners: Distributable Cash Flow

5

SEP Distributable Cash Flow ($MM) 4Q14 4Q13 YTD

2014 YTD

2013 Ongoing EBITDA $424 $352 $1,591 $1,391

LESS: Special items – 1 – 7

Reported EBITDA $424 $351 $1,591 $1,384

ADD:

Equity in earnings of unconsolidated affiliates (40) (24) (133) (89)

Distributions from unconsolidated affiliates 45 24 165 117

Other (3) 1 2 8

LESS:

Interest expense 55 84 238 383

Equity AFUDC 13 10 33 58

Distributions to non-controlling interests 7 5 29 19

Maintenance capex 106 90 270 228

Adjustment (1) - 43 - 417

Total Distributable Cash Flow $245 $120 $1,055 $315

(1) Removes the effects of the U.S. Assets Dropdown for the periods prior to the dropdown (January 1, 2012 to October 31, 2013) and the acquisition of Express-Platte for the periods prior to the acquisition (March 14, 2013 to August 1, 2013).

2014 Fourth Quarter Update | Growth from a position of strength

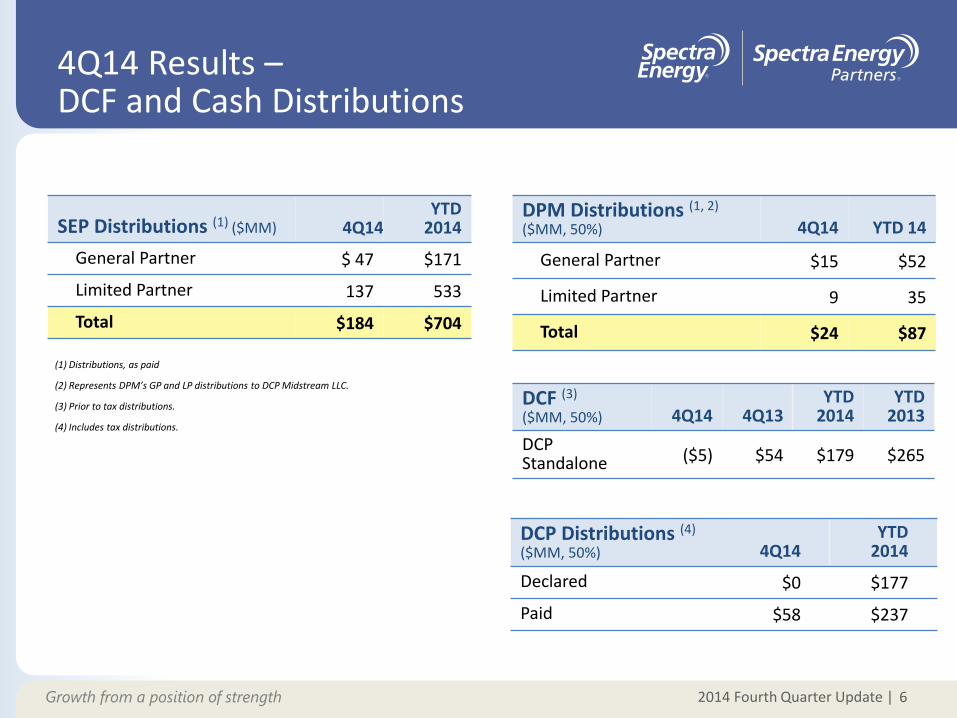

4Q14 Results – DCF and Cash Distributions

6

DPM Distributions (1, 2) ($MM, 50%) 4Q14 YTD 14

General Partner $15 $52

Limited Partner 9 35

Total $24 $87

DCF (3)

($MM, 50%) 4Q14 4Q13 YTD

2014 YTD

2013

DCP Standalone ($5) $54 $179 $265

(2) Represents DPM’s GP and LP distributions to DCP Midstream LLC.

(1) Distributions, as paid

SEP Distributions (1) ($MM) 4Q14 YTD

2014

General Partner $ 47 $171

Limited Partner 137 533

Total $184 $704

DCP Distributions (4) ($MM, 50%) 4Q14

YTD 2014

Declared $0 $177

Paid $58 $237

(4) Includes tax distributions.

(3) Prior to tax distributions.

2014 Fourth Quarter Update | Growth from a position of strength

Strong Finish to 2014

• Solid fee-based businesses continue to perform well

• Strong financial position to enter 2015:

– Strong cash coverage

– Excellent credit metrics

– Investment grade balance sheet

– Multiple financing vehicles to fund growth capex

7

Continued confidence in dividend growth

2014 Fourth Quarter Update | Growth from a position of strength

Financial strength and flexibility & solid growth projects provide solid platform for 2015 and beyond

Exceptional 2014 Results Strongly Position SE for 2015

8

2014 PLAN

$1,460 Distributable

Cash Flow

$3.5B Projects secured with fee-based contracts

1.6x Coverage

at SE

$0.14 Dividend

growth at SE

$1,230 Distributable

Cash Flow

$3.0B Projects secured with fee-based contracts

1.4x Coverage

at SE

$0.12 Dividend

growth at SE

2014 RESULTS