scotiamocatta precious metals forecast 20 10 · pdf filegold jewellery consumption, ... given...

TRANSCRIPT

ScotiaMocatta

Precious Metals Forecast 2010 PGM

w w w . s c o t i a m o c a t t a . c o m

Executive Summary • The PGM’s fall last year was a reality check, but the steady rebound across the

metals now looks more sustainable and justified by the fundamentals. Expect Platinum to trade in a $1,100-$1,900/oz range, Palladium between $250/oz and $420/oz and Rhodium between $1,400/oz and $3,000/oz.

• High levels of buying through the ETFs shows strong investor interest, which is likely to continue as the longer term outlooks for the PGMs remain bullish.

• Fund interest has also ballooned, but that may be in anticipation of PGM ETFs being launched in the US.

• Industrial demand for all metals is expected to recover slowly to start with, but then to gain momentum as 2010 progresses.

• South African issues will likely determine whether sufficient Platinum and Rhodium supply is seen, while Russia will remain key for Palladium supply.

Introduction Platinum had a very volatile time in 2008: prices were ramped up on the back of supply concerns following power shortages in South Africa, only to tumble as the financial crisis unfolded and the global economy went into recession. As 2009 started, a rebound was under way and prices have trended consistently higher, but at a steady pace with a few short- lived corrections along the way. The down turn in the economy saw all sectors of demand initially hit, including investment, but as 2009 progressed investment demand has rebounded strongly and considerable pent-up demand for Platinum jewellery has been unleashed in China. The lower prices at the start of the year also attracted strong long term investor interest and indeed if you can look past the current economic downturn, the supply and demand fundamentals for Platinum look bullish. Near term however, with prices up 77% from their lows last October, traders may be wary of chasing the market higher. In recent months, the fund long position has increased rapidly, but we feel that this may be more to do with the possibility that PGM ETFs may be launched in the US, rather than the funds being bullish for purely fundamental reasons. The net fund long position averaged 7,844 contract in Q2’09, since when it has raced up to 18,224 contracts, a third higher than seen at the recent peaks in 2007 and 2008. So although we are bullish for Platinum prices in the longer term, we feel the combination of spare production capacity and lack of clear evidence that a sustainable recovery is underway, may hold Platinum prices back and see the Platinum-Gold spread narrow.

Precious Metals Forecast 2010_PGM October 2009

2

Industrial demand falls heavily Platinum demand comes from industry, jewellery manufacturers and investors. Within the industrial category the manufacture of autocatalysts consumes the most, followed by its use in the electrical, chemical, glass and petroleum, industries. This diverse demand for the metal provides Platinum with a broad base of consumption, which has certainly helped cushion the drop in demand during the recent recession. Platinum’s industrial demand between 2004 and 2007 grew at an average 7.3% per annum, but in 2008 dropped 8% and in 2009 is expected to drop some 13%. However, these significant falls have been lessened by stable jewellery demand and growing investment interest. When these other sectors are taken into account, overall demand is likely to have fallen by around 6.7% in 2009, half the level that industrial demand suffered on its own. Looking forward, Platinum demand is likely to rebound strongly once global recovery gets underway. Initially demand should do well as much of it is geared up to growth in Asia, but as the chart opposite shows, the US and Europe collectively still consume 50% of consumption and demand for big ticket items like cars may take some time to recover. However, when one takes into account the level of destocking within industry, there is also likely to be strong demand from restocking, if only when sustainable recovery is anticipated. Platinum’s penetration into existing and new markets is likely to continue, helped by ever more stringent environmental legislation that is set to see pollution control equipment fitted to an ever increasing variety of machines. However, Platinum is losing market share to Palladium in petrol-driven engines and Palladium has started to replace some Platinum in diesel catalytic convertors. Therefore, Platinum is suffering on two fronts: it is losing market share within the auto industry and demand is down in line with the depressed state of auto sales in Europe and the US. Auto sales recovered slightly backing the wake of government ‘cash for clunkers’ incentive schemes, but sales are likely to dip once these schemes have run their course, as they did in the US, since the incentives schemes will have encouraged future purchases to have been brought forward. However, auto sales in China are rising very strongly - again boosted by government incentives - but this was likely to happen anyway as demand for vehicles was growing fast before the economic slowdown , due to the large pool of potential first time buyers waiting on the horizon. Other industrial uses The outlook for non-emission control applications, which account for some 31% of Platinum’s industrial consumption and which include use in the glass, electronics, petroleum and chemical industries, should respond well when a return to growth is seen. Collectively this sector was growing at a steady 6% per annum between 2004 and 2007. Demand fell 4.8% in 2008 and is expected to drop 10% in 2009, but this area of Platinum’s use is likely to recover well. For example demand for flat-TV and display screens have suffered as a result of the recession, but these are the type of items that will pick-up smartly once consumer spending starts again and

Europe37%

Japan17%

N.America13%

China18%

RoW15%

Regional Consumption of Platinium(average 2005-2008)

Precious Metals Forecast 2010_PGM October 2009

3

companies start to hire again (more computers on desks). However, in 2010, with only a slow recovery expected later in the year, this sector may only see slow growth, say 3% next year. Jewellery demand expected to take up some of the slack Demand for Platinum from the jewellery industry has proved to be price elastic in recent years and as a result it has become something of a swing factor for Platinum demand. The climb of Platinum prices over most of the past decade saw demand fall to 1.365Moz in 2008, from a peak of 2.88Moz in 1999. Indeed jewellery in 2008 accounted for 21% of Platinum demand, compared to 51% in 1999. High prices on the back of shortages of metal meant Platinum jewellery became the reserve of the bridal market. However, despite the recession, the sell-off in price has seen demand from the jewellery sector hold steady, which, given the sharp drop in Gold jewellery consumption, is noteworthy. Geographically, jewellery demand has held up well in Europe, has fallen in the US, fallen heavily in Japan, but grown strongly in China, where growth was 9% in 2008 and looks set to be surpassed this year. What is interesting is that, even with a strong rally in prices, Chinese imports remain high. As there is considerable scope for growth to expand in China and Asia, ex-Japan, we feel prices below $1,500/oz will continue to prompt strong jewellery buying. As such, we expect jewellery demand to remain flat in 2009, but to grow 15% in 2010. Supply In 2008, Platinum supply fell 9.5%, principally in South Africa and Russia, while other areas saw a small increase. The big disruptions were seen in South Africa where power shortages, shutdowns after accidents and industrial unrest, led to a production fall of 540,000 oz, a drop of 10.6%. After the sharp price falls in H2’08, most South African producers cut production schedules and have been reluctant to raise output in the short term. However, if higher prices continue, producers are likely to review their production levels for 2010. In Russia, output has slowed as lower ore grades have been encountered, while output in North America in 2008 was unchanged from 2007. Somewhat surprisingly, given all its political unrest, Zimbabwe’s output been picking up. In 2009, global mine output is expected to fall 3% to 5.79Moz. The issues affecting supply next year are likely to revolve around price and physical restraints on production, such as further strikes, safety closures, electricity availability and production costs. With South Africa’s power utility Eskom’s electricity costs rising 31% between July 2009 and March 2010, Platinum producers are likely to be more reluctant to raise output and may also be more responsive should PGM prices fall again. Changes in the exchange rate are another factor, with the dollar weakness reducing the South African Rand price of the PGMs they are selling. In this environment, producers have to try to reduce production costs to keep profit margin steady. This in turn does not make for good labour relations. Under these conditions, it is difficult for producers to allocate much money for project expansions, which, could create problems in the future, once currently spare production capacity is exhausted. In Russia, output has been falling. In 2008 production was 820,000 oz, down from 915,000 oz in 2007 and a peak of 1.3 Moz in 2001. Output continued to fall in the first half of 2009, with production at some operations falling 11%. For 2009, output as a whole is expected to fall to 790,000 oz, but is likely to edge higher, back towards 810,000 oz in 2010 as stronger base metals and PGM prices provide the incentive to increase production. Production in other regions grew 1.7% in 2008 to 295,000 oz and is likely edge higher this year and next, as higher base metal prices prompt the a pick-up in mining output.

Precious Metals Forecast 2010_PGM October 2009

4

Investment demand – The chart shows the heavy redemptions seen in the London ETF in the second half of 2008. This was the result of a massive reduction in risk appetite and selling on the fear that physical demand for Platinum would be hit hard by the down turn in the auto industry. However, given the extent of the sell-off, investor demand soon picked up on the back of bargain hunting and safe-haven buying. By early April 2009, the ETFs had grown to new highs and have continued to grow steadily since. Indeed, since the end of August 2009, there has been another acceleration in demand for Platinum ETFs, which comes on the back of fresh weakness in the dollar and perhaps on concern that the equity rally might be running out of steams, thereby encouraging money to flow from equities to precious metals. In 2008, the size of the ETFs grew by 104,049 oz, a gain of 53%. In the January to September period of 2009, the ETFs have grown 226,936 oz, a gain of 89%. Given a sustainable recovery in the auto industry, (we think the aftermath of ‘cash for clunkers’ shows such a recovery has not started yet) the medium-to- long term demand outlook for Platinum remains good and that should encourage ongoing investor interest. In addition, there is a distinct possibility that PGM ETF’s will be launched in the US, (currently awaiting regulatory approval from the SEC) and, if they are, it is likely the amount of Platinum held in ETFs will rise by another order of magnitude. With the ETFs now holding a large volume of metal, which is extremely liquid as was seen by the pace of redemption in the H2’08, the market needs to be aware that a heavy spell of redemptions could prompt a significant price sell-off. However, with the worst of the recession hopefully behind us and with industrial users likely to have destocked last year, the prospects for good demand ‘further out’ are likely to see investors hold on to their ETFs holdings. Fund position races higher The net long fund position has climbed rapidly in recent months to a new record level, far above previous peaks. At first sight this seems strange, as the fundamentals are not as bullish now as they were in 2007 and 2008. However, the sudden increase may well be more tied into the possible launch of PGM ETFs in the US and the run up in fund buying is in anticipation of the ETF having to buy if it gets the regulatory approval. The same thing happened on two occasions ahead of both the delayed launch and then the actual launch of the Silver ETF in the US. If this is the case, this run up in fund interest may be for mechanical rather than fundamental reasons. We would expect the net fund position to deflate if the ETF is given the go ahead and perhaps deflate even more rapidly if the regulators say “No”.

Precious Metals Forecast 2010_PGM October 2009

5

Technical The correction in Platinum’s price last year was vicious with prices falling 67% from the highs at $2,300/oz in March 2008 to lows at $745/oz in October 2008. By comparison the rebound has been steady, with prices recently reaching the 38.2% Fibonacci retracement line. Prices are now approaching former resistance seen in 2007 during the bull market and before the power disruptions in South Africa and which has now capped the market three times since 2006. Gold’s move up into new high ground is bound to prompt further buying in Platinum and the stochastics have crossed higher again too, but it may end up taking Platinum to levels that are not sustainable in the current environment. With the up trend line at $1,200/oz, there is room on the downside for prices to consolidate at lower numbers without damaging the overall chart picture. Overall we expect the up trend line to guide prices higher at a steady pace, which will include pull backs to the up trend line, which in turn are likely to provide good scale down buying opportunities. Conclusion and Forecast Platinum has been on a rollercoaster ride since the start of 2008, but the sell-off in the second half of last year gave the market a reality check. Since then the rally has been orderly with steady long term ETF buying providing direction. In addition, the lower prices enabled jewellery manufacturers, especially in China, to restock as the margin on Platinum jewellery became more favourable for fabricators and retailers. More recently, fund buying has accelerated, but we think that is in anticipation of a US based ETF, more than on the back of any particular bullish development in the fundamentals. Long term industrial demand looks set to gradually recover and there may be considerable scope for restocking in the auto industry as recovery gets underway, although it is probably too early to anticipate that now. Jewellery demand is also likely to remain strong while prices are below the $1,500/oz level, but once again we feel that when prices do go higher, jewellery will become a negative swing factor. Other reasons for not expecting a fast price rise are that there is spare production capacity, which can be utilised when demand does rise and on the demand side, Palladium is taking market share from Platinum in the autocatalyst market. In the short term, we expect prices to remain buoyant on the back of fund buying and general investment buying now that Gold has headed higher. Likewise we remain long term bullish as once a sustainable economic recovery gets going demand is likely to recover. Until then, we would not be surprised if the broader markets, after the strong rallies seen since March this year, suffered either further consolidation, or possibly even another sell-off. Overall we feel Platinum prices will trade in the $1,100/oz to $1,900/oz range between now and the end of 2010.

Precious Metals Forecast 2010_PGM October 2009

6

Palladium

Palladium prices spiked higher in 2008 to reach $592/oz only to then slump back to $156/oz a few months later. Since then prices have been climbing higher at a steady pace, which over the medium-to- long term seems set to continue. Short term there is potential for a pull back across all the markets and that is likely to affect Palladium too, but generally Palladium’s fundamentals are bullish. There are some potentially very bullish developments, but these are not expected to come into play over the next twelve months and, overall, the outlook will improve once a sustainable recovery is underway. We expect dips to be well supported and look for the overall uptrend to continue over the forecast period. Auto catalysts In line with the down turn in the global economy and the slump in the auto industry, demand from auto catalyst dropped 3.6%, although the regional differences were more extreme with North America (the largest market with 31% of demand) seeing consumption drop around 20%, while demand climbed by: 3% in Europe, 3.7% in Japan, 18.5% in China and 8.3% across other countries. In 2009, the recession will see demand fall further, but demand for Palladium in auto-catalysts should recover well as the regions likely to experience the strongest recovery are Brazil, Russia, India and China (‘BRIC’) and the trend in these countries is for petrol-driven cars, which tend to use Palladium based autocatalysts, rather than the Platinum ones used for diesel vehicles. That said, Palladium’s use in this sector is expected to drop around 9% in 2009. It should recover in 2010 as vehicle production recovers around the globe, albeit slowly in the mature Western markets. Taking into account a pick-up in demand, the introduction of tighter legislation in Europe, Palladium’s greater use in the diesel sector and the likelihood of all the above coinciding with restocking, could lead to a rebound in demand of between 12-15% in 2010. Other industrial uses Palladium’s other industrial uses include electronics, chemicals and other emission control equipment for factories and petrol-powered machinery, such as garden equipment. The electronics sector has suffered significantly from the economic slowdown, however, the high rate of technological change in electrical equipment and in computer memory and processing should mean this sector undergoes a strong resurgence when sustainable economic recovery gets going. Also, emission control equipment for factories is a growth market as it is fitted to new plants and retrofitted to existing operations. Jewellery demand Demand for Palladium jewellery, like Silver jewellery, has faired better than Gold jewellery demand because the cheaper price appealed to cash-strapped buyers. It also appealed to fabricators as they could write in bigger profit margins as Palladium jewellery was still considerably cheaper than Gold or Platinum items. In addition, as Palladium jewellery is still relatively new it is still benefitting from geographical growth as it makes inroads into the North American and European markets. However in Japan, Palladium jewellery has not become popular and the metal’s jewellery role is to be used to blend with Gold to make white-Gold. Interestingly, the practice of incorporating a bigger profit margin seems to be back-firing in Asia as when customers try to trade in old jewellery for new, the resale value is not good and therefore, the jewellery is not seen as an investment. However, as consumer become accustomed to the metal fabricators are likely to have to cut their margins, or face losing sales.

Precious Metals Forecast 2010_PGM October 2009

7

As it is, the sharp pull back in Platinum prices in late 2008 has seen some swing back towards Platinum jewellery anyway. In time, it would not be surprising if Palladium jewellery finds a more stable outlet in North America and Europe where there are traditionally larger mark-ups and the practice of swapping old jewellery for new is rare. Supply Russia is the dominant supplier of Palladium on two counts. Firstly, it mines 43% of the World’s output, compared to South Africa’s 38% and, secondly, Russia keeps the market roughly in balance by making sales from stockpile that have averaged 1.2Moz per annum in recent years. In 2008, Russia supplied 50% of total supply (mine output and metal from stocks), with South Africa providing 33%, North America 12% and other countries 5%. In 2008, production in South Africa fell 12% on the back of power shortages, safety issues and shutdowns, while in Russia lower ore grades, adverse weather and various maintenance shutdowns lead to an 11.5% drop in production. North American output dropped in late 2008 as producers closed some mines and made cutbacks at others; which led to an output fall of 8%. In Zimbabwe output increased 6.5% as expansions became operational, which, considering all the political turmoil there, is noteworthy. In 2009, global Palladium supply is expected to drop in North America as some mines have remained on care and maintenance for the whole year and as poor weather and low ore grades have impact Russian production. In South Africa, some producers have expanded, but overall output is expected to be down 5%. Although the energy shortage seems to have disappeared as the recession has reduced overall demand for electricity, producers’ margins do not seem strong enough to encourage a rise in output. Palladium production is expected to fall 5% in 2009 before rebounding in 2010 as higher prices encourage the reactivation of idle capacity, with output then expected to grow around 4%. Russian sales from stockpile remain all important Russian sales from stockpile in recent years have prevented the Palladium market from being in a supply deficit. Between 2005 and 2008 sales from stockpile have averaged around 1.2Moz per annum, which equates to some 20% of annual demand. At some stage Russian stockpiles will be exhausted and when they are, the Palladium market is likely to become very interesting. However, Russian PGM stockpiles are a state secret and the size of the stockpile is not in the public domain. In recent years, the level of sales from inventory has fallen, but this may well be due to the lower prices and the fall in demand. In 2008, shipments from Russia to Switzerland were high but not all of the metal was thought to have been sold. However, since March this year, Russia shipments to Switzerland have, effectively, fallen to zero. This might reflect the higher level of shipments in 2008, or else be the result of another administrative reorganisation. Overall, the market remains in deficit, in 2008, the production / demand deficit was around 0.5Moz and in 2009 the deficit is likely to be 0.6Moz. So with Russian sales from stockpile likely to be around the 0.9Moz level, the market will be heading into surplus - a surplus which will be more than absorbed by investment demand. In 2010, we have to assume that Russian stockpiles will continue, but would advise vigilance for any signs that suggest stockpile sales are dwindling. Once that happens then Palladium’s fundamentals are likely to become significantly more bullish. That said, with large stockpiles in Switzerland, thought to be around the 8Moz level, there is no danger of an immediate shortage.

Precious Metals Forecast 2010_PGM October 2009

8

Investment demand grows steadily Investors’ interest in Palladium has grown steadily in 2008 and 2009. In 2008, combined holdings climbed 380,000 oz a rise of 136% over the year and up until September 2009, they had grown a further 417,814 oz, an increase of 63%, within nine months. More to the point, the accumulation in the Palladium ETFs has been steady, with few redemptions. Given the structural deficit in the market and years of stockpile sales by Russia (which can not go on forever), plus a good long term demand outlook for the metal, it would not be surprising to see the ETFs continue to grow steadily. Fund activity reaches record levels Unlike the ETFs’ performance, the funds view on Palladium is more erratic. However, since March the funds have been bullish as seen by the net fund long position reaching a record high of 13,164 contracts. Some of this we feel is on the back of rotation out of equities and the dollar and into the PGM’s as a safe-haven, but we would not be surprised if a good proportion of the increased buying is in anticipation of a US Palladium ETF being launched. If an ETF is launched then we may well see the net fund position come down, but without too much of a pull back in price as metal moves from Futures to the ETF. On its own the record high net fund long position is worrying some commentators, but we would say this is only going to be the case if the regulations rule against a US Palladium ETF. Technical This long term chart of Palladium shows how devastating the pull back was last year, albeit from a spike higher. From highs at $592/oz in March prices have plunged to $156/oz. Since then prices have climbed steadily to $320/oz, just short of the 38.2% Fibonacci retracement line at $322/oz. Prices are now approaching the bottom of the trading band seen on the left hand side of the chart, which dominated trading before the rally caused by

Precious Metals Forecast 2010_PGM October 2009

9

the South Africa power shortage started to drive the market. Given that sustained economic recovery does not seem underway yet, we would be surprised if prices managed to trade above this former trading band that runs between $310/oz and $384/oz, so that is our upside target for the year ahead, with the underlying up trend line around $250/oz likely to provide support and generally guide prices higher. Although we remain bullish, we feel there will be pull backs, but we expect any such pull backs to encounter good support. Conclusion and Forecast Palladium’s medium-to- long term outlook is bullish, the market is in a structural deficit with the deficit being made up from Russian stockpiles sales, which at some stage are going to be depleted. Palladium is also gaining market share from Platinum in the autocatalyst market and with the main growth region for vehicles expected to be in Asia, where petrol- fuelled vehicles dominate, Palladium demand should increase faster than that of Platinum. Likewise Palladium has also made strong inroads into the jewellery market, which is a relatively new and growing source of offtake. As such, the outlook is bullish, although, as with all the metals, Palladium is unlikely to really benefit until sustainable economic recovery gets underway. Given the price gains already seen this year and with the possibility of a broad base market correction still present, we do expect a relatively large pull back in prices at some stage, but we also expect any dips to attract a good level of investment buying. Overall we look for prices to spend the bulk of time between now and the end of 2010, trading in the $250-$420/oz range.

Rhodium Outlook

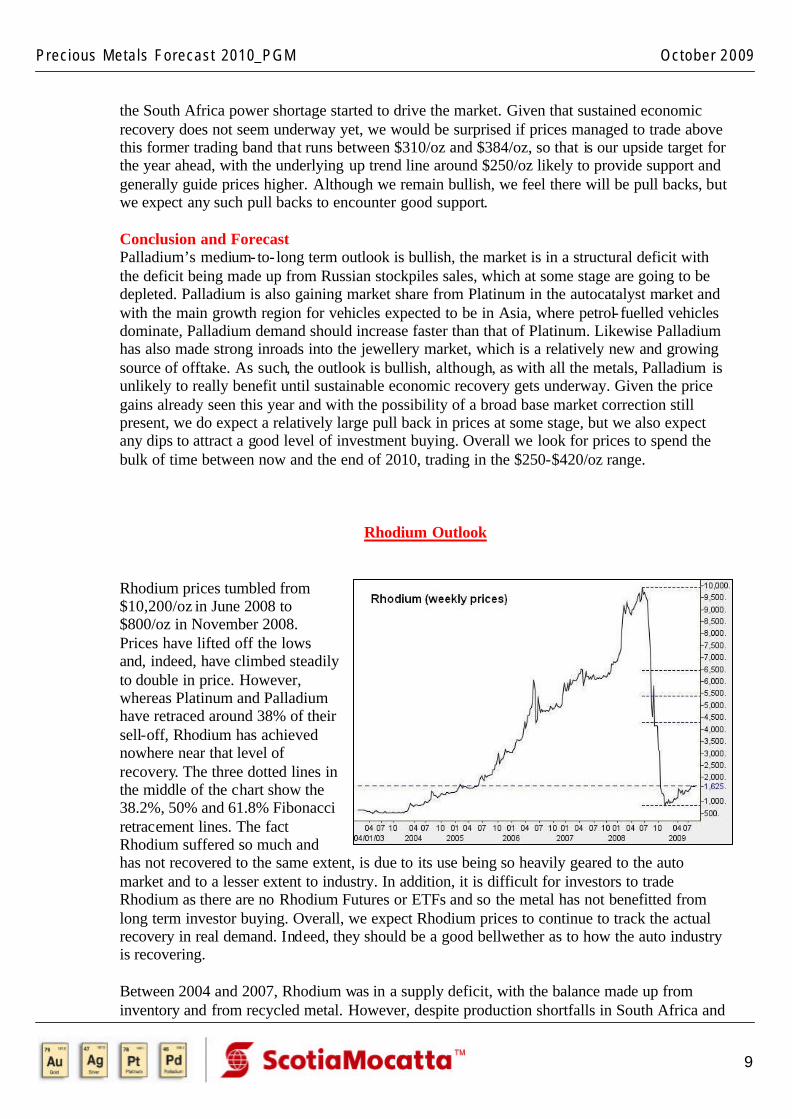

Rhodium prices tumbled from $10,200/oz in June 2008 to $800/oz in November 2008. Prices have lifted off the lows and, indeed, have climbed steadily to double in price. However, whereas Platinum and Palladium have retraced around 38% of their sell-off, Rhodium has achieved nowhere near that level of recovery. The three dotted lines in the middle of the chart show the 38.2%, 50% and 61.8% Fibonacci retracement lines. The fact Rhodium suffered so much and has not recovered to the same extent, is due to its use being so heavily geared to the auto market and to a lesser extent to industry. In addition, it is difficult for investors to trade Rhodium as there are no Rhodium Futures or ETFs and so the metal has not benefitted from long term investor buying. Overall, we expect Rhodium prices to continue to track the actual recovery in real demand. Indeed, they should be a good bellwether as to how the auto industry is recovering. Between 2004 and 2007, Rhodium was in a supply deficit, with the balance made up from inventory and from recycled metal. However, despite production shortfalls in South Africa and

Precious Metals Forecast 2010_PGM October 2009

10

a 15.7% drop in supply, demand dropped more, falling 18.3%, which left the market with a small supply surplus. Demand Rhodium demand is predominantly focused on the autocatalyst market which absorbs 85% of supply. The glass and chemical industries in recent years both accounted for 6% of global demand, although in 2008, the glass industry’s share fell to 4%, while the chemical industry’s share climbed to 8%. Generally, demand from these industries is price inelastic, but what was noticeable in the glass industry is that after a surge in glass making capacity in recent years, some old capacity was closed which released Rhodium back into the market. However, during the last recession in 2001, then the only sector that suffered a significant drop in rhodium demand was the autocatalyst industry, which saw a fall of 28%, so whether offtake in 2009 has dropped to the same extent remains to be seen. All in all, we expect Rhodium demand to recover in line with the general economic recovery, but especially in line with the recovery in auto production, which in the West is likely to be sluggish, but which should recover strongly in Asia and especially China. Supply In 2008, Rhodium supply dropped heavily in South Africa as output at PGM operations were affected by power outages and shutdowns. Output in Russia and in North America also declined, albeit at a lesser rate. With South Africa producing 84% of the world’s Rhodium, any disruptions to production by strikes or power shortages will have a noticeable affect on supply, but generally South African supply is set to grow as much of the new capacity coming on stream is set to produce Rhodium-rich ores. High prices in 2005 to 2008 made it attractive to recycle Rhodium from old catalysts, but the rapid sell-off in prices and the relatively low prices so far in 2009, has seen the amount of recycled metal fall. However ,with the various incentive schemes to swap used cars for new cars, more modern cars are now being recycled and that should boost the amount of metal available for recycling. Recycled metal accounted for 18% of total supply in 2007, grew to 23% in 2008 and after a lull in 2009, is likely to increase again in 2010. Conclusion Demand in 2009 is expected to suffer heavily, which is likely to see another year of surplus and with high Rhodium ore grades set to be mined as production expands and with a build up of metal waiting to be recycled, supply is likely to overhand the market for a while. However, as a global recovery is likely to get underway as 2010 progresses demand should pick-up too; slowly at first, but then gain momentum as recovery becomes more widespread. Overall, we expect Rhodium prices to slowly edge higher, but with such a high percentage of production coming from South Africa the risk to this outlook no doubt lies to the upside. With the fundamentals likely to improve slowly we would look for prices to trade in the $1,400-$3,000/oz trading range between now and the end of 2010.

Precious Metals Forecast 2010_PGM October 2009

11

SCOTIAMOCATTA is a global leader in metals trading, brokerage and finance. As part of Scotia Capital and a member of the Scotiabank Group, clients can access a full range of financial products and services. To obtain additional information on ScotiaMocatta products and services, call one of the offices listed below.

CANADA Toronto Scotia Plaza 40 King Street West Box 4085, Station ‘A’ Scotia Plaza Toronto, Ontario M5W 2X6

Andy Montano [email protected] Tel: 1-416-866-7835 Fax: 1-416-866-6897 UNITED KINGDOM London Scotia House 33 Finsbury Square London EC2A 1BB

David Wilkinson [email protected] Tel: 44-20-7826-5931 Fax: 44-20-7826-5948 UNITED STATES New York One Liberty Plaza 165 Broadway New York, N.Y. 10006

Tim Dinneny [email protected] Tel: 1-212-225-6200 Fax: 1-212-225-6248 MEXICO Mexico City Blvd. M. Avila Camacho #1, Piso 11 Col. Chapultepec Polanco Colonia Polanco 11560 Mexico

Jose Maria Tapia [email protected] Tel: 52 55 9179 5142 Fax: 52 55 5325 3527 INDIA Mumbai 11-13 Maker Chambers VI 1st Floor 220 Nariman Point Mumbai 400021

Rajan Venkatesh [email protected] Tel: 91-22-2288-0994 (Direct) Fax: 91-22-2288-1078

New Delhi Upper Ground Floor Dr. Gopal Das Bhavan 28 Barakhamba Road New Delhi 110001

Prem Nath [email protected]

Tel: 91-11-5535-2420 Fax: 91-11-2335-9342

Bangalore 25/2 S.N. Towers M.G. Road Bangalore 560001

Mahendran Krishnamurthy [email protected]

Tel: 91-80-2532-5325 Fax: 91-80-2558-1435

Coimbatore Classic Towers 1547 Trichy Road Coimbatore 641018

Shankara Subramanian [email protected] Tel: 91-422-2301-595 Fax: 91-422-2301-596 HONG KONG SAR 25th Floor, United Centre 95 Queensway Hong Kong

Alice Lam [email protected] Tel: 852-2861-4788 Fax: 852-2573-7869 SINGAPORE 1 Raffles Quay #20-01, North Tower One Raffles Quay Singapore, 048583

Swee Kiang Teo [email protected] Tel: 65-6536-3683 Fax: 65-6534-7825 UNITED ARAB EMIRATES Dubai 302, 3rd Floor Precinct Building 03 Dubai International Financial centre Dubai UAE

Pramod Mohan [email protected] Tel: 97 14 3711 777 Fax: 97 14 228 9090

Precious Metals Forecast 2010_PGM October 2009

12

This report has been prepared on behalf of ScotiaMocatta and is not for the use of private individuals. The ScotiaMocatta trademark represents the precious metals business of The Bank of Nova Scotia. The Bank of Nova Scotia, a Canadian chartered bank, is incorporated in Canada with limited liability. Opinions, estimates and projections contained herein are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither the Bank of Nova Scotia, its affiliates, employees or agents accepts any liability whatsoever for any loss arising from the use of this report or its contents. The Bank of Nova Scotia, its affiliates, employees or agents may hold a position in the products contained herein. This report is not a direct offer financial promotion, and is not to be construed as, an offer to sell or solicitation of an offer to buy any products whatsoever. This market commentary is regarded as a marketing communication. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The Bank of Nova Scotia is authorised and regulated by The Financial Services Authority.