scope of total income (section 5) - home | magni profs

TRANSCRIPT

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 1

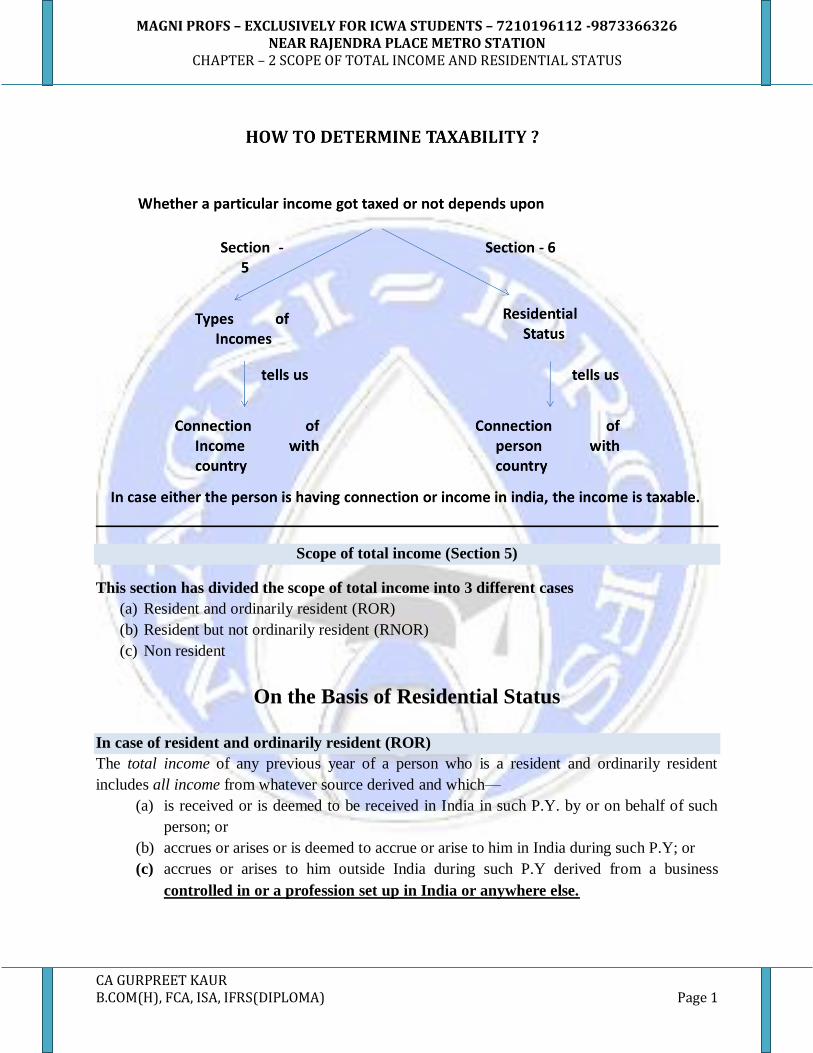

Scope of total income (Section 5)

This section has divided the scope of total income into 3 different cases

(a) Resident and ordinarily resident (ROR)

(b) Resident but not ordinarily resident (RNOR)

(c) Non resident

On the Basis of Residential Status

In case of resident and ordinarily resident (ROR)

The total income of any previous year of a person who is a resident and ordinarily resident

includes all income from whatever source derived and which—

(a) is received or is deemed to be received in India in such P.Y. by or on behalf of such

person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such P.Y; or

(c) accrues or arises to him outside India during such P.Y derived from a business

controlled in or a profession set up in India or anywhere else.

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 2

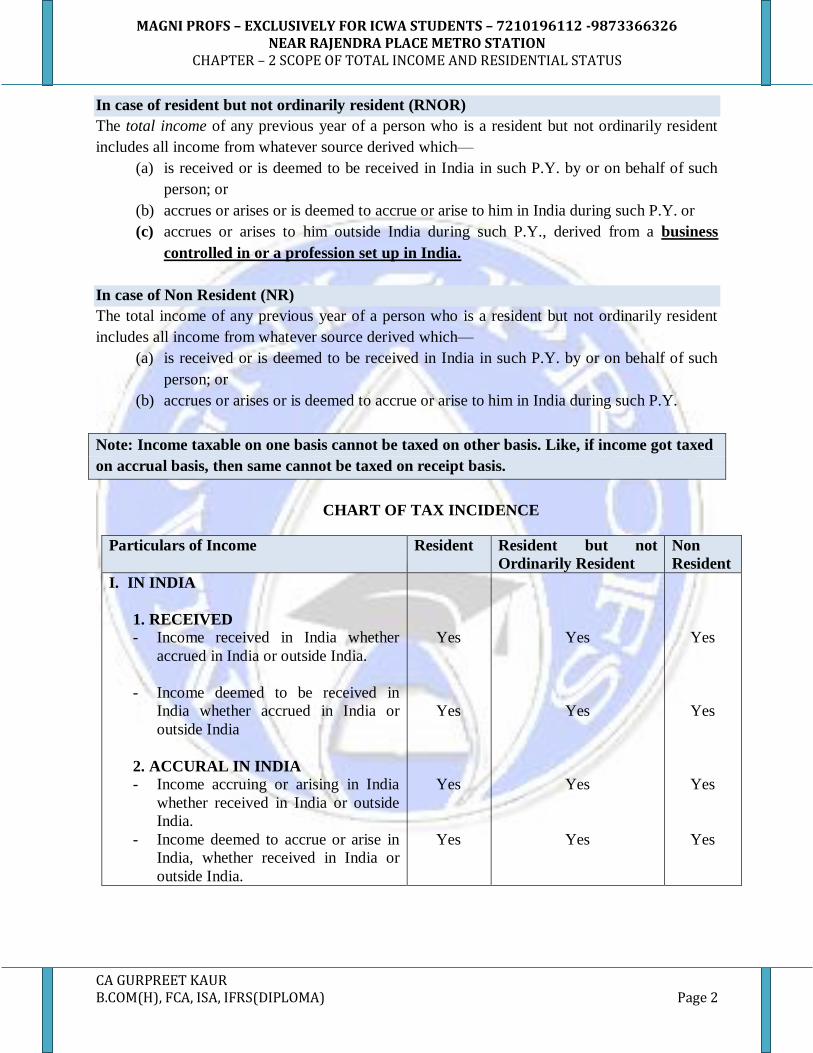

In case of resident but not ordinarily resident (RNOR)

The total income of any previous year of a person who is a resident but not ordinarily resident

includes all income from whatever source derived which—

(a) is received or is deemed to be received in India in such P.Y. by or on behalf of such

person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such P.Y. or

(c) accrues or arises to him outside India during such P.Y., derived from a business

controlled in or a profession set up in India.

In case of Non Resident (NR)

The total income of any previous year of a person who is a resident but not ordinarily resident

includes all income from whatever source derived which—

(a) is received or is deemed to be received in India in such P.Y. by or on behalf of such

person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such P.Y.

Note: Income taxable on one basis cannot be taxed on other basis. Like, if income got taxed

on accrual basis, then same cannot be taxed on receipt basis.

CHART OF TAX INCIDENCE

Particulars of Income Resident Resident but not

Ordinarily Resident

Non

Resident

I. IN INDIA

1. RECEIVED

- Income received in India whether

accrued in India or outside India.

- Income deemed to be received in

India whether accrued in India or

outside India

2. ACCURAL IN INDIA

- Income accruing or arising in India

whether received in India or outside

India.

- Income deemed to accrue or arise in

India, whether received in India or

outside India.

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 3

II. OUTSIDE INDIA

- Income received and accrued outside

India from a business controlled or

profession set up in India.

- Any other Income

Yes

Yes

Yes

No

No

No

Residential Status (Section 6)

According to Section 5, taxability of a person depends upon its residential status. Therefore it is

important to ascertain the residential status of a person to find out which income will be taxable

in India under this Act. Section 6 guide us how to determine the residential status of a person.

Steps for Determining residential status

Step 1 First find out whether a person is resident or non resident

Step 2 If a person is resident, than find out whether it is ROR or RNOR

Note: Only individuals and HUF can be RNOR; rest all other persons can be only resident

(ROR) or non resident

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 4

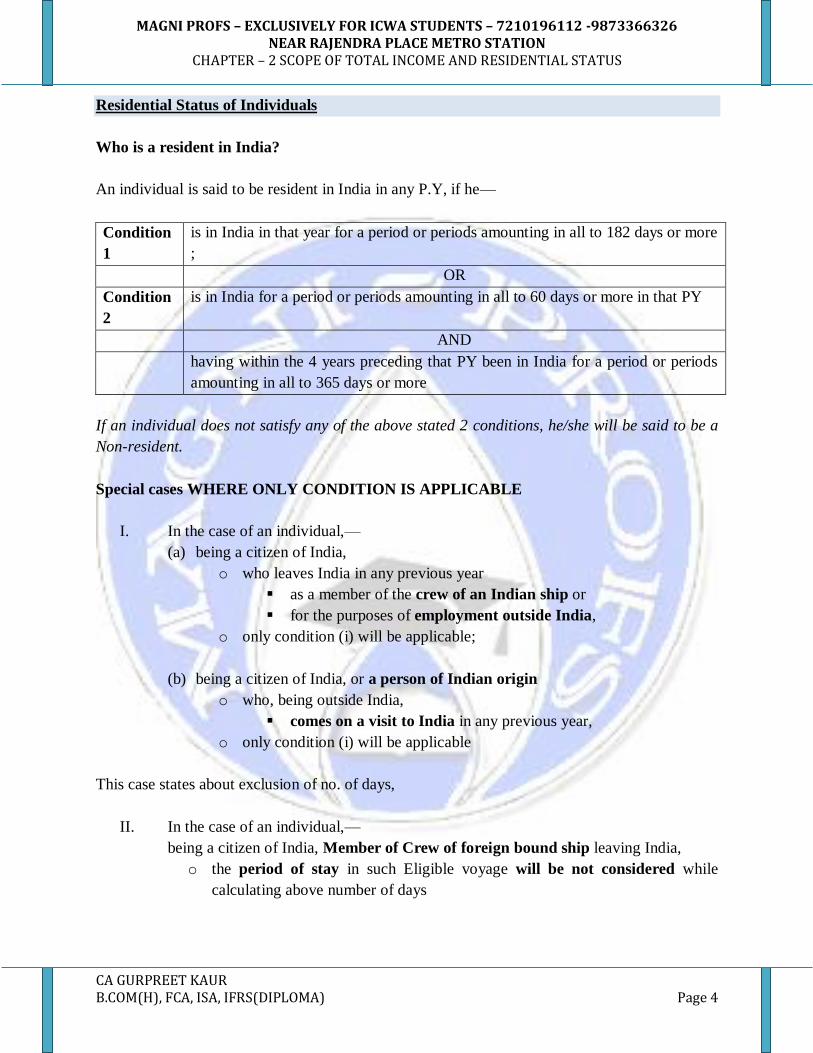

Residential Status of Individuals

Who is a resident in India?

An individual is said to be resident in India in any P.Y, if he—

Condition

1

is in India in that year for a period or periods amounting in all to 182 days or more

;

OR

Condition

2

is in India for a period or periods amounting in all to 60 days or more in that PY

AND

having within the 4 years preceding that PY been in India for a period or periods

amounting in all to 365 days or more

If an individual does not satisfy any of the above stated 2 conditions, he/she will be said to be a

Non-resident.

Special cases WHERE ONLY CONDITION IS APPLICABLE

I. In the case of an individual,—

(a) being a citizen of India,

o who leaves India in any previous year

as a member of the crew of an Indian ship or

for the purposes of employment outside India,

o only condition (i) will be applicable;

(b) being a citizen of India, or a person of Indian origin

o who, being outside India,

comes on a visit to India in any previous year,

o only condition (i) will be applicable

This case states about exclusion of no. of days,

II. In the case of an individual,—

being a citizen of India, Member of Crew of foreign bound ship leaving India,

o the period of stay in such Eligible voyage will be not considered while

calculating above number of days

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 5

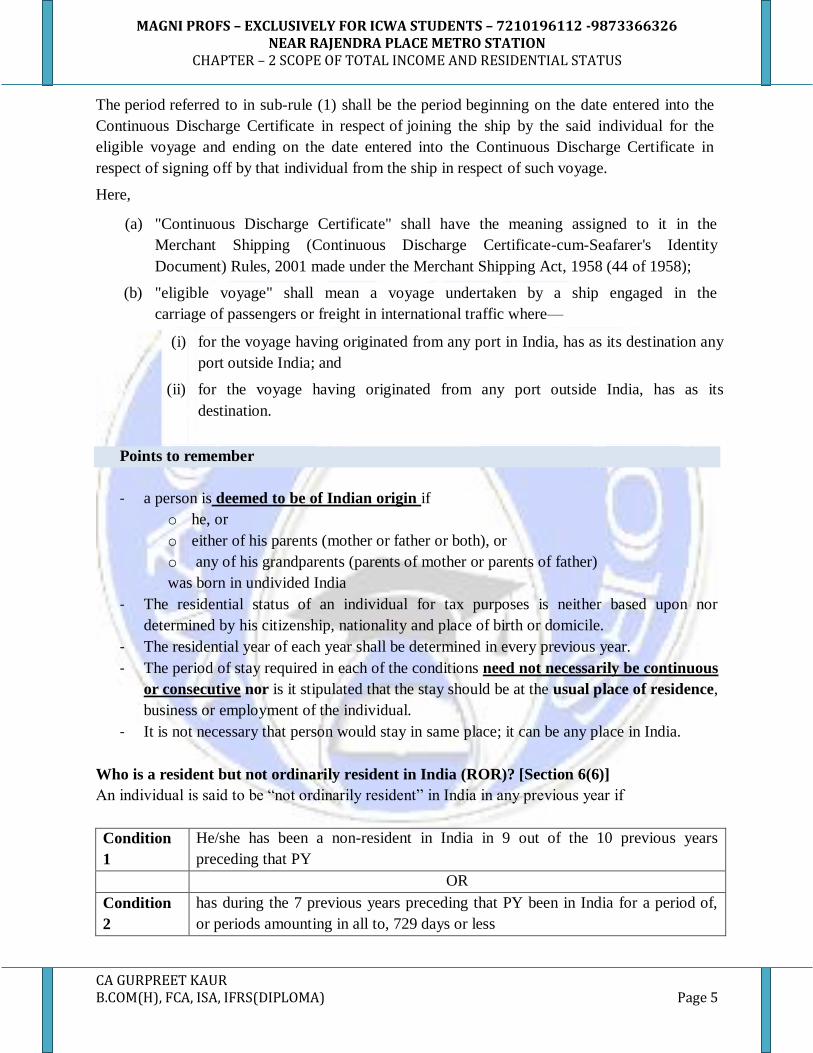

The period referred to in sub-rule (1) shall be the period beginning on the date entered into the

Continuous Discharge Certificate in respect of joining the ship by the said individual for the

eligible voyage and ending on the date entered into the Continuous Discharge Certificate in

respect of signing off by that individual from the ship in respect of such voyage.

Here,

(a) "Continuous Discharge Certificate" shall have the meaning assigned to it in the

Merchant Shipping (Continuous Discharge Certificate-cum-Seafarer's Identity

Document) Rules, 2001 made under the Merchant Shipping Act, 1958 (44 of 1958);

(b) "eligible voyage" shall mean a voyage undertaken by a ship engaged in the

carriage of passengers or freight in international traffic where—

(i) for the voyage having originated from any port in India, has as its destination any

port outside India; and

(ii) for the voyage having originated from any port outside India, has as its

destination.

Points to remember

- a person is deemed to be of Indian origin if

o he, or

o either of his parents (mother or father or both), or

o any of his grandparents (parents of mother or parents of father)

was born in undivided India

- The residential status of an individual for tax purposes is neither based upon nor

determined by his citizenship, nationality and place of birth or domicile.

- The residential year of each year shall be determined in every previous year.

- The period of stay required in each of the conditions need not necessarily be continuous

or consecutive nor is it stipulated that the stay should be at the usual place of residence,

business or employment of the individual.

- It is not necessary that person would stay in same place; it can be any place in India.

Who is a resident but not ordinarily resident in India (ROR)? [Section 6(6)]

An individual is said to be “not ordinarily resident” in India in any previous year if

Condition

1

He/she has been a non-resident in India in 9 out of the 10 previous years

preceding that PY

OR

Condition

2

has during the 7 previous years preceding that PY been in India for a period of,

or periods amounting in all to, 729 days or less

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 6

Thus an individual is said to be “ordinarily resident” in India in any previous year if :-

Condition

1

He/she has been a resident in India in 2 out of the 10 previous years preceding

that PY

AND

Condition

2

He/she has been in India for 730 days or more during the 7 previous years

preceding that PY

Practical Problems

Determine the Residential Status

Ques1. Mrs. Clinton, an American citizen comes to India for the first time in previous year

2008-09 for 120 days. During the following year he stayed in India:-

2009-10 100 2012-13 120

2010-11 150 2013-14 190

2011-12 100 2014-15 94

2015-16 90

Ques2. Indian citizen and Business man Shri Raj Gopal, who resided in Jaipur, went to Germany

for purposes of employment on 15-08-14 and came back to India on 10-11-2015. He has never

out of India before it. Determine his Residential Status for the Asstt Year 2016-17.

What if, he has gone for his leisure trip?

Ques3. R an Indian citizen left India for the first time on 21-09-14 for employment in Germany.

During the previous year 2015-16 he comes to India on 5-5-15 for 150 days. Determine the

Residential Status of R.

Ques4. K was born in Lahore in 1946, he has been staying in England since 1972. He comes to

visit on 2-10-15 and returns on 31-3-16. Determine its residential status on assessment year 16-

17.

Ques5. K was born in England in 1966. His Father had been born in America in 1936. “K”

Grandfather had been born in Lahore 1916.

Will K be a resident in India, if he made visits to India for 180 days every year? Determine his

residential during the previous year 2015-16.

Ques6. During the previous year 2015-16, K a foreign citizen, stayed in India for just 69 days.

Determine his residential status for the assessment year 2016-17 on the basis of following

information.

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 7

- During 14-15, he was not present in India but during 13-14 he came to India for 276

days.

- During 12-13, K was present in India for 90 days.

- During 11-12 & 2010-11, K was in India for 389 days & 348 days respectively.

- Earlier 10-11, he had been equally coming to India for 100 days every year.

_________________________________________________________________________

Residential Status of HUF

Who is a resident in India (ROR)? (sub-section 2)

A Hindu undivided family, firm or other association of persons is said to be resident in India in

any previous year in every case except where during that year the control and management of

its affairs is situated wholly outside India.

Meaning of Place of control and management

It is the place from decisions and directions are issued but not the places where from the business

is carried on.

In case of H.U.F.:

(a) In the case of a H.U.F., the control and management of its affairs is normally said to be

from the place where the karta resides and issues directions.

(b) There may be chances that HUF is managed by member or co parceners, in that case we

will not considered the place where the karta resides and issue directions. For e.g. A &

Sons (HUF) is managed by the Mr.S, elder son of Mr.A who is Karta of A & Sons

(HUF), due to his age factor. Now, Place of Mr. S will be considered for determining the

place of control and management.

Who is a resident but not ordinarily resident in India (ROR)? (sub-section 6)

A HUF is said to be “not ordinarily resident” in India in any previous year if

Condition

1

Its Karta has been a non-resident in India in 9 out of the 10 previous years

preceding that PY

OR

Condition

2

Its Karta has, during the 7 previous years preceding that PY, been in India for a

period of, or periods amounting in all to, 729 days or less

If the control and management of the affairs of a HUF is Residential Status

1. Wholly or partly in India Resident

2. Wholly outside India Non-resident

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 8

Note:

Where, during the last ten years the karta’s of the H.U.F. had been different from one

another, the total period of stay of successive karta’s of the same family should be

aggregated to determine the residential status of the karta’s and consequently the H.U.F.

The residential status of the members of HUF is generally irrelevant for determining the

residential status of the HUF

Practical Problems

Ques1. During the previous year 15-16, Sachin Kumar & sons (HUF) was partly controlled from

India by its Karta, who is a citizen of India but stay outside India. For the purpose of managing

the affairs of the HUF, Sachin Kumar has been regularly visiting India. Determine the residential

status of the HUF for the assessment year 2016-17 in following cases :-

- Sachin Kumar has been visiting India for 100 days for the last 12 years

- Sachin Kumar has been visiting India for 110 days for the last 12 years.

- Sachin Kumar has been visiting India for the last 12 years. During last 4 previous years

he stays for 50 days and earlier 200 days.

Residential Status of Firm or AOP or AJP

Who is a resident in India (ROR)? (Sub-Section 2)

A firm or other association of persons is said to be resident in India in any previous year in every

case except where during that year the control and management of its affairs is situated wholly

outside India.

If the control and management of the affairs of a

FIRM/AOP/LLP Every other Person [other than

Individual, HUF & Company]

Residential Status

1. Wholly or partly in India Resident

2. Wholly outside India Non-resident

Place of Control And Management Person In-charge

1. Partnership Firm Active Partners

2. Limited Liability Partnership Designated Partners

3. Association of Person Head of Governing Body

4. Artificial Judicial Person Head of Governing Body

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 9

Residential Status of company

Who is a resident in India (ROR)? (Sub-Section 3)

A company is said to be resident in India in any previous year, if—

(i) it is an Indian company ; or

(ii) Its place of effective management, in that year, is in India.

1. Indian company Resident

2. Other Companies- Control and management of the

affairs of a company is:

(a). Wholly in India Resident

(b). Wholly or partly outside India Non-resident

Note:

POEM is the place where key management and commercial decision that are necessary for the

conduct of the business of an entity as a whole, are in substance made.

After deciding the Residential Status, we will establish connection of Income with India, as

summarized in Section 5.

Particulars ROR RNOR NR

In India

Earn

- Accure or arise in India

- Deemed to accure or arise in India [ Section

9]

Taxable

Taxable

Taxable

Taxable

Taxable

Taxable

Received

- received in India

- Deemed to receive in India [ Section 7]

Taxable

Taxable

Taxable

Taxable

Taxable

Taxable

Outside India

- Business or Profession controlled from India

- Any other Source

Taxable

Taxable

Taxable

Not Taxable

Not Taxable

Not Taxable

Income Accrue/Arise or Due

Accrue refers to the right to receive income, whereas due refers to the right to enforce payment

of the accrued income. Therefore, income can be said to be accrue when it becomes due.

For example Interest on FDR accrues every day, but will become due on the maturity of the

FDR.

Income deemed to accrue or arise in India (Section 9)

This section refer all those Income are covered which are deemed to accrue or arise in India.

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 10

(i) Any income accruing or arising to an assessee at any place outside India, whether directly or

indirectly,:

- through or from any business connection in India,

- through or from any property in India, - (Rental Income)

- through or from any asset or source of income in India, (Dividend)

- through the transfer of a capital asset situated in India. – (Capital Gain)

Business connection includes all the activities carried out through a person who, acting on

behalf of the non-resident like:-

a) Person habitually exercises, an authority to conclude contracts except purchase of goods

for exports

b) Having no authority as stated above, but habitually maintains a stock of goods and

makes regular delivery of products on behalf of the non resident.

c) Habitually secures order in India, mainly or wholly for the non resident or for that non

resident or other non resident subject to common control of non resident

NOTE

An asset or a capital asset being any share or interest in a company or entity registered or

incorporated outside India shall be deemed to be and shall always be deemed to have been

situated in India, if the share or interest derives, directly or indirectly, its value substantially from

the assets located in India.

When asset deemed to be gets its value derived from India,

i. When the value of asset of the entity

(a) Exceed Rs. 10 Crore AND

(b) At least 50% of total of the asset

On Specific Date

ii. Specific Date

As on date of Transfer – (15% increase in the value of BV of asset as on last date of

Accounting period)

Or

As on last date of accounting period before the date of transfer.

iii. Accounting period

(a) Ending on 31st March

(b) But if different 12 month period is considered by entity to comply with

statutory requirement then same can be taken.

Exception to above rule

i. In case asset are directly owned by the company or entity and there is no right to

management or control or holding voting powers or share capital or interest

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 11

exceeding 5% of total voting power or share capital or interest during last 12

months prior to the transfer.

ii. In case asset are Indirectly ( along with its associated enterprise) owned by the

company or entity and there is no right to management or control or holding voting

powers or share capital or interest exceeding 5% of total voting power or share

capital or interest during last 12 months prior to the transfer.

Exception to Deemed to be Earn

Income not deemed to accrue/arise in India

(a) in the case of a business of which all the operations are not carried out in India,

o the income of the business shall not be deemed to accrue or arise in India to extent

the operations of such business carried outside in India;

(b) in the case of a non-resident,

o no income shall be deemed to accrue or arise in India to him through or from

operations which are confined to the purchase of goods in India for the purpose

of export ;

(c) in the case of a non-resident,

o being a person engaged in the business of running a news agency or of

publishing newspapers, magazines or journals,

o no income shall be deemed to accrue or arise in India to him through or from

activities which are confined to the collection of news and views in India for

transmission out of India;

(d) in the case of a non-resident, being—

(1) an individual who is not a citizen of India ; or

(2) a firm which does not have any partner who is a citizen of India or who is resident in

India ; or

(3) a company which does not have any shareholder who is a citizen of India or who is

resident in India,

no income shall be deemed to accrue or arise in India to such individual, firm or company

through or from operations which are confined to the shooting of any cinematograph

film in India.

(ii) Income, which falls under the head ‘Salaries’, if it is earned in India i.e. if services are

rendered in India.

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 12

Note:

- Any income under the head ‘Salaries’ payable for rest period or leave period which is

preceded and succeeded by services rendered in India, and forms part of the service

contract of employment, shall be regarded as income earned in India.

(iii)Income from ‘Salaries’

which is payable by the Indian Government

to a citizen of India

for services rendered outside India

(However, allowances and perquisites paid outside India by the Government are exempt).

(iv) Dividend paid by an Indian company outside India.

(v) Income by way of interest payable by—

(a) the Government ; or

(b) a person who is a resident, (except where the interest is payable in respect of any debt

incurred, or moneys borrowed and used,

for the purposes of a business or profession carried on by such person outside

India or

for the purposes of making or earning any income from any source outside

India) ; or

(c) a person who is a non-resident, where the interest is payable in respect of any debt

incurred, or moneys borrowed and used,

for the purposes of a business or profession carried on by such person in India.

(vi) Income by way of royalty payable by—

(a) the Government; or

(b) a person who is a resident, (except where the royalty is payable in respect of any right,

property or information used or services utilised

for the purposes of a business or profession carried on by such person outside

India or

for the purposes of making or earning any income from any source outside

India); or

(c) a person who is a non-resident, where the royalty is payable in respect of any right,

property or information used or services utilised

for the purposes of a business or profession carried on by such person in India

or

for the purposes of making or earning any income from any source in India.

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 13

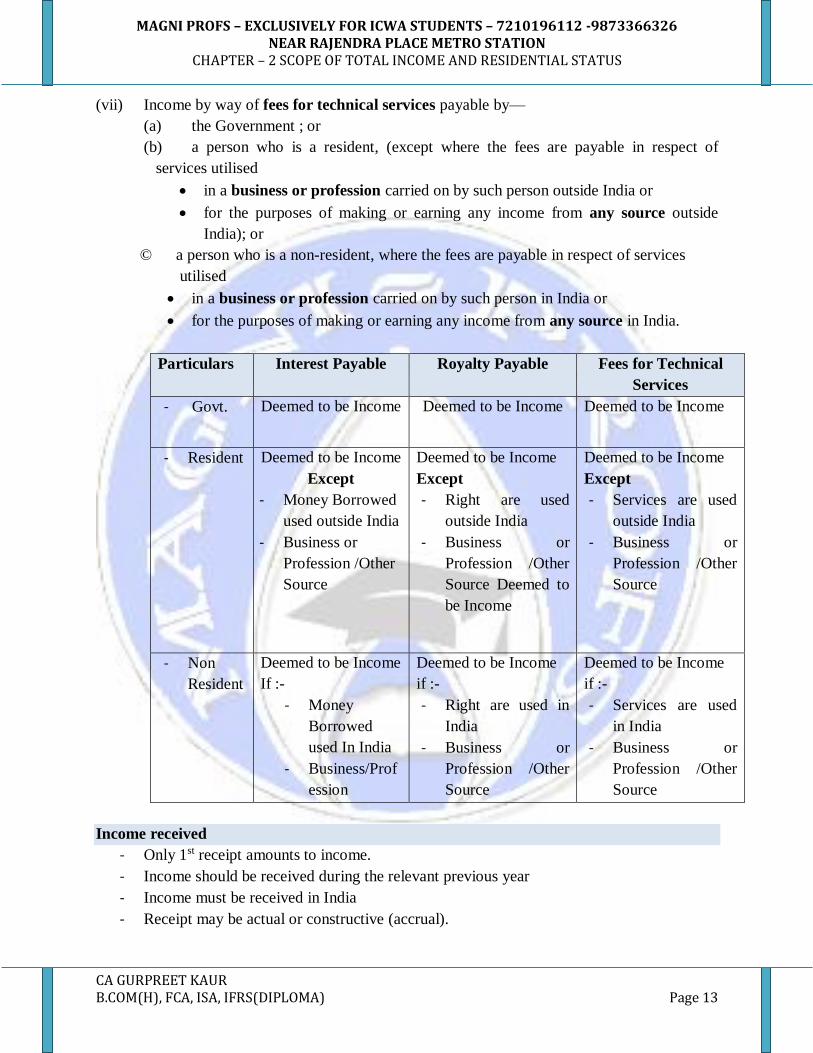

(vii) Income by way of fees for technical services payable by—

(a) the Government ; or

(b) a person who is a resident, (except where the fees are payable in respect of

services utilised

in a business or profession carried on by such person outside India or

for the purposes of making or earning any income from any source outside

India); or

© a person who is a non-resident, where the fees are payable in respect of services

utilised

in a business or profession carried on by such person in India or

for the purposes of making or earning any income from any source in India.

Particulars Interest Payable Royalty Payable Fees for Technical

Services

- Govt. Deemed to be Income Deemed to be Income Deemed to be Income

- Resident Deemed to be Income

Except

- Money Borrowed

used outside India

- Business or

Profession /Other

Source

Deemed to be Income

Except

- Right are used

outside India

- Business or

Profession /Other

Source Deemed to

be Income

Deemed to be Income

Except

- Services are used

outside India

- Business or

Profession /Other

Source

- Non

Resident

Deemed to be Income

If :-

- Money

Borrowed

used In India

- Business/Prof

ession

Deemed to be Income

if :-

- Right are used in

India

- Business or

Profession /Other

Source

Deemed to be Income

if :-

- Services are used

in India

- Business or

Profession /Other

Source

Income received

- Only 1st receipt amounts to income.

- Income should be received during the relevant previous year

- Income must be received in India

- Receipt may be actual or constructive (accrual).

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 14

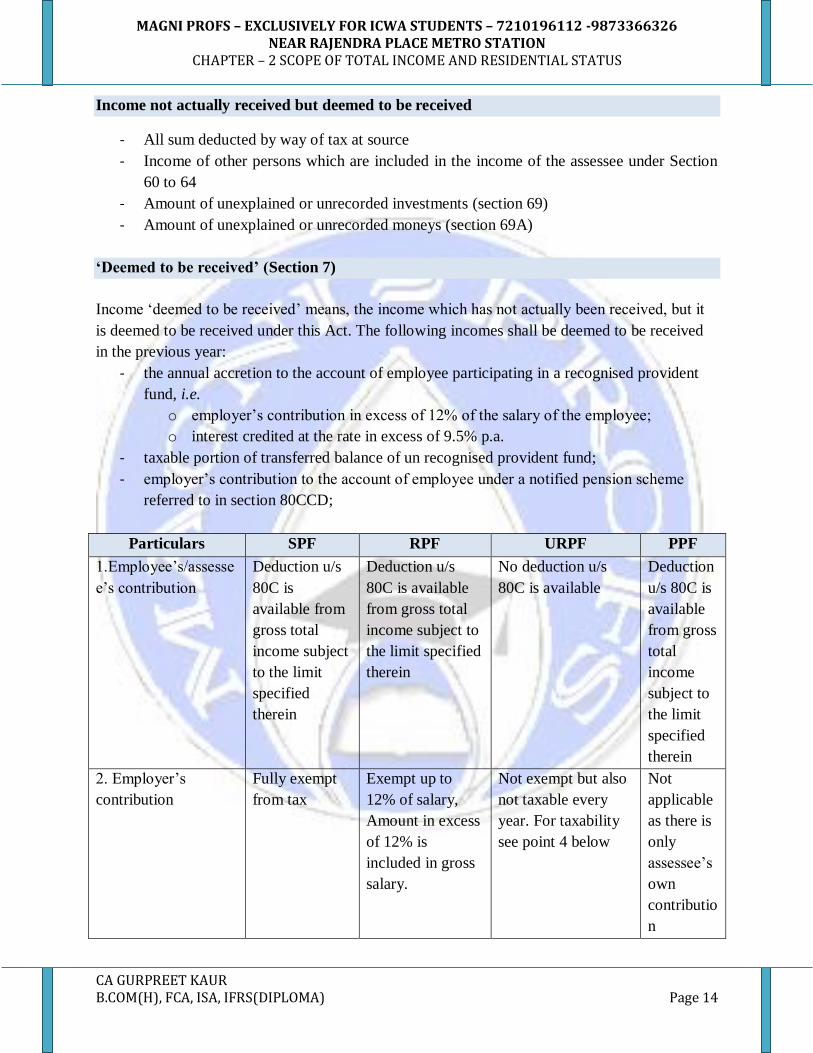

Income not actually received but deemed to be received

- All sum deducted by way of tax at source

- Income of other persons which are included in the income of the assessee under Section

60 to 64

- Amount of unexplained or unrecorded investments (section 69)

- Amount of unexplained or unrecorded moneys (section 69A)

‘Deemed to be received’ (Section 7)

Income ‘deemed to be received’ means, the income which has not actually been received, but it

is deemed to be received under this Act. The following incomes shall be deemed to be received

in the previous year:

- the annual accretion to the account of employee participating in a recognised provident

fund, i.e.

o employer’s contribution in excess of 12% of the salary of the employee;

o interest credited at the rate in excess of 9.5% p.a.

- taxable portion of transferred balance of un recognised provident fund;

- employer’s contribution to the account of employee under a notified pension scheme

referred to in section 80CCD;

Particulars SPF RPF URPF PPF

1.Employee’s/assesse

e’s contribution

Deduction u/s

80C is

available from

gross total

income subject

to the limit

specified

therein

Deduction u/s

80C is available

from gross total

income subject to

the limit specified

therein

No deduction u/s

80C is available

Deduction

u/s 80C is

available

from gross

total

income

subject to

the limit

specified

therein

2. Employer’s

contribution

Fully exempt

from tax

Exempt up to

12% of salary,

Amount in excess

of 12% is

included in gross

salary.

Not exempt but also

not taxable every

year. For taxability

see point 4 below

Not

applicable

as there is

only

assessee’s

own

contributio

n

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 15

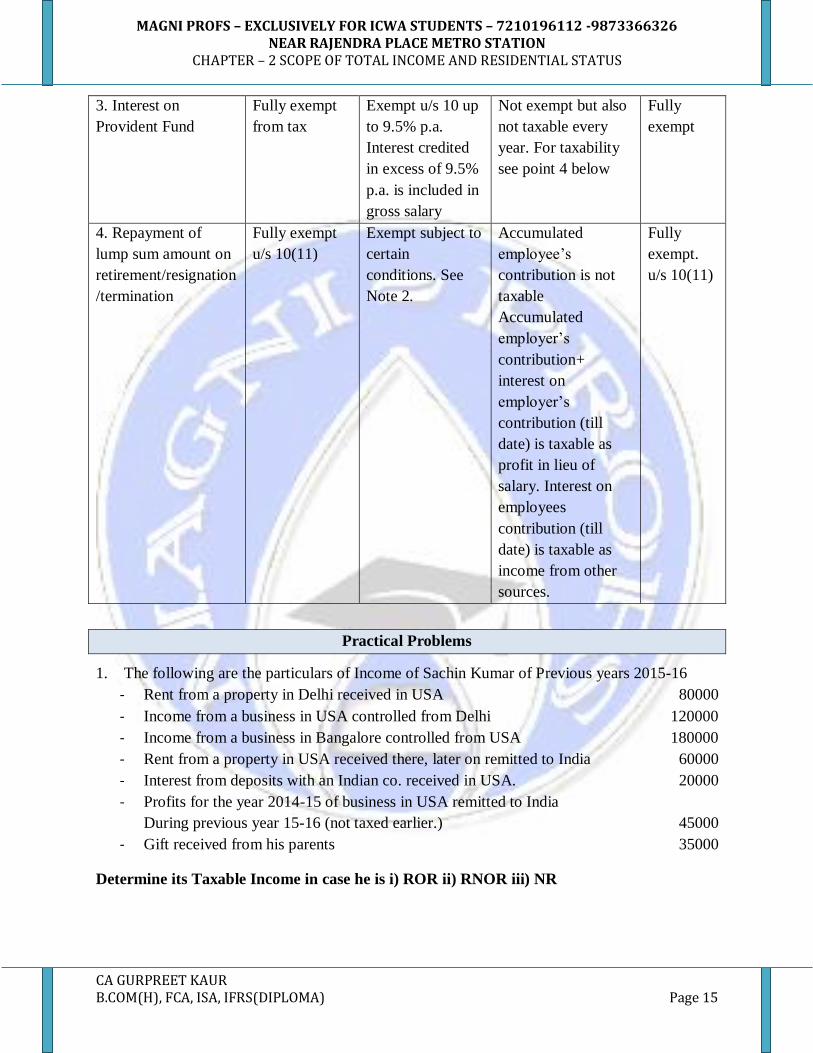

3. Interest on

Provident Fund

Fully exempt

from tax

Exempt u/s 10 up

to 9.5% p.a.

Interest credited

in excess of 9.5%

p.a. is included in

gross salary

Not exempt but also

not taxable every

year. For taxability

see point 4 below

Fully

exempt

4. Repayment of

lump sum amount on

retirement/resignation

/termination

Fully exempt

u/s 10(11)

Exempt subject to

certain

conditions. See

Note 2.

Accumulated

employee’s

contribution is not

taxable

Accumulated

employer’s

contribution+

interest on

employer’s

contribution (till

date) is taxable as

profit in lieu of

salary. Interest on

employees

contribution (till

date) is taxable as

income from other

sources.

Fully

exempt.

u/s 10(11)

Practical Problems

1. The following are the particulars of Income of Sachin Kumar of Previous years 2015-16

- Rent from a property in Delhi received in USA 80000

- Income from a business in USA controlled from Delhi 120000

- Income from a business in Bangalore controlled from USA 180000

- Rent from a property in USA received there, later on remitted to India 60000

- Interest from deposits with an Indian co. received in USA. 20000

- Profits for the year 2014-15 of business in USA remitted to India

During previous year 15-16 (not taxed earlier.) 45000

- Gift received from his parents 35000

Determine its Taxable Income in case he is i) ROR ii) RNOR iii) NR

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 16

2. Mr. Kartar Singh earns the following of during the financial year 2015-16:

- Interest from an Indian Co. Received in Malaysia 120000

- Pension from former employer in India received in Singapore 180000

- Profits earned from a business in Paris which is controlled in India, 200000

half of the profits being received in India.

- Income from agriculture in China and remitted to India. 125000

- Income from property in London received there. 400000

- Past foreign income bought to India. 10000

- Profits from business in Pakistan received in India. 500000

- Income from HP in Kuwait received in India. 120000

- Income from HP in Sri Lanka deposited in bank there. 180000

- Profits of business established in Sri Lanka deposited in bank, 200000

There business is controlled in India (out of 200000, a sum of

Rs.100000 is remitted in India)

- Income from profit in India but received in England 240000

- Profit earned from business in Chennai. 160000

- Income from of an England, it all spent on the end of children in 270000

London.

Determine its Taxable Income in case he is i) ROR ii) RNOR iii) NR

3. During the previous year 2015-16, Ranvijay, a foreign citizen, stayed in India for just 69

days. Determine his residential status for the assessment year 2016-17 on the basis of the

following information:

i. During 2015-16, he was not present in India but during 2014-15 he came to India for

276 days.

ii. During 2013-14, Ranvijay was present in India for 90 days.

iii. During 2010-11 and 2009-10, Ranvijay was in India for 359 and 348 days

respectively.

iv. Earlier to 2009-10 he had been regularly coming to India for 100 days every year.

4. X is a citizen of Bangladesh. His grandmother was born in a village near Dhaka in 1940. He

came to India for the first time since 1981 on 31.10.2015 for a visit of 190 days. Find out the

residential status of X for the assessment year 2016-17 on the assumption that wife of X is a

resident but” not ordinarily resident in India” for the same year.

5. Sanskar ltd, a German company, which is non-resident in India, earned the following

incomes by way of fee for technical services. Advise about the taxability of such income in

the hands of Sanskar ltd. in India:

a) Govt. of India paid Rs. 2,00,000 under an agreement, to be used for a project in India.

b) Amitabh ltd, an Indian company, paid Rs.3,00,000 for the know-how to be used in India.

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 17

c) Dharmender ltd, an Indian company, paid Rs.4000000 for know-how acquired in

Germany to be used in China.

d) Jitender ltd, a non-resident company paid Rs. 2400000 for acquiring know-how to be

used in India for carrying on certain manufacturing business.

6. During the financial year 2015-16 Kamal Kumar had the following income:

a) Salary income received in India for services rendered in Sweden Rs.390000

b) Income from profession in India, but received in Hongkong Rs.360000

c) Property income in Uganda (out of which Rs.240000 was remitted to India.) Rs.500000

d) Profits earned from business in Bangalore. Rs.150000

e) Agricultural income in Kenya. Rs.160000

f) Profits from a business carried on at Nepal but controlled from India. Rs.220000

Compute the income of Kamal Kumar for the assessment year 2016-17 if he is

resident and ordinarily resident,

Not ordinarily resident, and

Non-resident in India

7. Mr. Shikhar Dhawan earns the following income during the financial year 2015-16:

a) Income from house property in London, received in India. 60000

b) Profits from business in Japan and managed from there (received in Japan) 900000

c) Dividend from foreign company, received in India. 30000

d) Dividend from Indian company, received in England. 50000

e) Profits from business in Kenya, controlled from India, profits 300000

received in Kenya.

f) Profits from business in Delhi, managed from Japan. 700000

g) Capital Gains on Transfer of shares of Indian companies, sold in 200000

USA and gains were received there.

h) Pension from former employer in India, received in Japan. 50000

i) Profits from business in Pakistan, deposited in bank there 20000

j) Profit on sale of asset in India but received in London. 8000

k) Past untaxed profits of UK business of 2015-16 brought into India 90000

in 2016-17.

l) Interest on Govt. securities accrued in India but received in Paris. 80000

m) Interest on USA Govt. securities, recd. in India. 20000

n) Salary earned in Bombay, but received in UK. 60000

o) Income from property in Paris, received there 100000

(Presume all the above incomes are computed incomes)

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 18

Determine the gross total income of Mr. Shikhar Dhawan if he is

- resident and ordinarily resident,

- resident but not ordinarily resident,

- non- resident in India, during the financial year 2015-16.

8. Krishna Systems, Partnership firm, has an income of Rs.3 lakhs in India and income

accruing/arising and also received abroad Rs.23 lakhs. It consists of two partners. Mr. Mohit

Sharma who is in active partner, is staying outside India throughout the year. Mr. Nakul

Sharma is a dormant partner and is staying in India throughout the year.

Compute tax liability of the partnership firm in India for the assessment year 2016-17.Also

compute tax liability of the firm if Mr. Nakul Sharma is also an active partner.

9. Punit Kumar, a foreign citizen (not being a person of India origin) came to India for the first

time on 2nd December, 2015 for a visit of 210 days. Punit Kumar had the following income

during the previous year ended 31st March, 2016:

a) Salary (received in India for three months) 100000

b) Income from house property in London (received there) 275200

c) Amount brought into India out of the past-untaxed profit earned in 80000

Germany.

d) Income from agriculture in Sri lanka, received and invested there. 12300

e) Income from business in Nepal, being controlled from India. 35000

f) Income from house property in USA received in USA 86000

(Rs. 76,000 is used in Canada for meeting the educational expenses

of Punit’s daughter and Rs. 10,000 is later on remitted in India)

You are required to compute his total income for the assessment year 2016-17.

10. Mr. David, a Government employee serving in the Ministry of External Affairs, left India for

the first time on 31.03.2015 due to his transfer to High Commission of Canada. He did not visit

India any time during the previous year 2015-16. He has received the following income for the

Financial Year 2015-16:

S.No. Particulars ` Amount

(i) Salary 5,00,000

(ii) Foreign Allowance 4,00,000

(iii) Interest on fixed deposit from bank in India 1,00,000

(iv) Income from agriculture in Pakistan 2,00,000

(v) Income from house property in Pakistan 2,50,000

Compute his gross total income for Assessment Year 2016-17.

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 19

11. Mr. Shyam, an Indian citizen, left India on 21.08.2015 for the first time to work as an officer

of a company in UK.

Determine the residential status of Ram for the assessment year 2016-17 and explain the

conditions to be fulfilled for the same under the Income-tax Act, 1961.

12. Miss Vineeta paid an amount of 10000 USD to Mr. K, a management consultant practising in

UK, specializing in project financing. The payment was made in UK. Mr. Kulasekhara is a non-

resident. The consultancy is related to a project in India with possible Ceylonese collaboration. Is

this payment chargeable to tax in India in the hands of Mr. K, since the services were used in

India?

Question Asked in Examination

Dec 2012

State the difference between the residential Status of a Company and that of Others.

Dec 2009

A Company which has its head office in India operated in Pakistan declared dividend subject to

remittance from Pakistan. During the previous year relevant to the Assessment year, the

remittance could not be covered from Pakistan. What is the tax liability in the hands of

Shareholder? Discuss

June 2015

Mr. Bharat, an engineering graduate, born and bought up in India, got employment in USA in

August 2015. By what date he should leave India, in order to become a non resident? By what

date he should leave India, in order to become a non resident? By that Tax advantage he will get?

December 2006

‘Y’, a foreign citizen (not being a person of Indian Origin) comes to India, for the first time in

the last 30 years on 20 March, 2015. On 1st September 2015, he leaves India for Nepal on a

business trip. He comes back on 26 Feb, 2016. Determine his residential Status under the Income

Tax Act, 1961 for the assessment year 2016-17.

December 2008

Kamlesh was working as crew member on an India Ship Plying in Foreign Waters. During the

year ended 31.03.2016, the ship did not touch the Indian Coast, except for 180 days. State the

MAGNI PROFS – EXCLUSIVELY FOR ICWA STUDENTS – 7210196112 -9873366326

NEAR RAJENDRA PLACE METRO STATION CHAPTER – 2 SCOPE OF TOTAL INCOME AND RESIDENTIAL STATUS

CA GURPREET KAUR B.COM(H), FCA, ISA, IFRS(DIPLOMA) Page 20

residential status for the assessment year. State the residential status for the assessment year

2016-17 and taxability of his salary.

December 2009

X got an employment in Singapore during the previous year 2015-16. He left for Singapore on

August 9, 2015. He is an Indian Citizen. Determine the residential status for the Asstt year 2016-

17.

Dec 2010

Following are the details of income of Mr. Subramani for the Financial Year 2015-16 :

Income from property in Srilanka remitted by the tenant to the assessee in India

through SBI 210000

Profit from business in India 100000

Dividend form shares in Foreign Companies received outside India 60000

Interest on deposit in India Companies 120000

Loss from business in SriLanka ( whose control and management of business

Wholly remained in India) 80000

Determine the total income in terms of the Income Tax Act, 1961 in the following situations:

i. Resident and ordinarily resident of India

ii. Resident but not ordinarily resident of India

iii. Non Resident

Dec 2015

X Limited is an Indian Company, however it carries on business in USA. All the

shareholders are resident of USA. The Board Meetings and Annual General Meeting are

held outside India. What is the Residential Status of X Limited?

Mr. Dravid, a citizen of Spain came to India for the first time in previous year 2011-12

and stayed for 100 days in that year. During the previous year 2012-13 2013-14, 2014-15

and 2015-16, he stayed in India for 120 days, 110 days, 80 days and 90 days respectively.

What is the residential Status of Mr. Dravid for the assessment year 2016-17?