scomi engineering bhd · scomi engineering bhd (111633-m) level 17, ... block d13, pusat dagangan...

TRANSCRIPT

Scomi Engineering Bhd (111633-M)

Level 17, 1 First Avenue, Bandar Utama47800 Petaling Jaya, Selangor Darul Ehsan, Malaysia

Tel: +603 7717 3000Fax: +603 7727 7935

www.scomiengineering.com.my

Sco

mi E

ngineering

Bhd

(111633-M

)A

nnual Report 2011

NEW OPPORTUNITIES. MOVING AHEAD.Annual Report 2011Annual Report 2011

Scomi Engineering Bhd

CONTENTS2 Key Financial Highlights

3 Corporate Structure

4 Corporate Statement of Scomi Group

5 Corporate Information

8 Profile of Directors

12 Management Team

14 Chairman’s Statement

22 Chief Executive Officer’s Review of Operations

30 Corporate Social Responsibility

38 Statement on Corporate Governance

44 Statement on Internal Control

46 Audit and Risk Management Committee Report

50 Additional Information

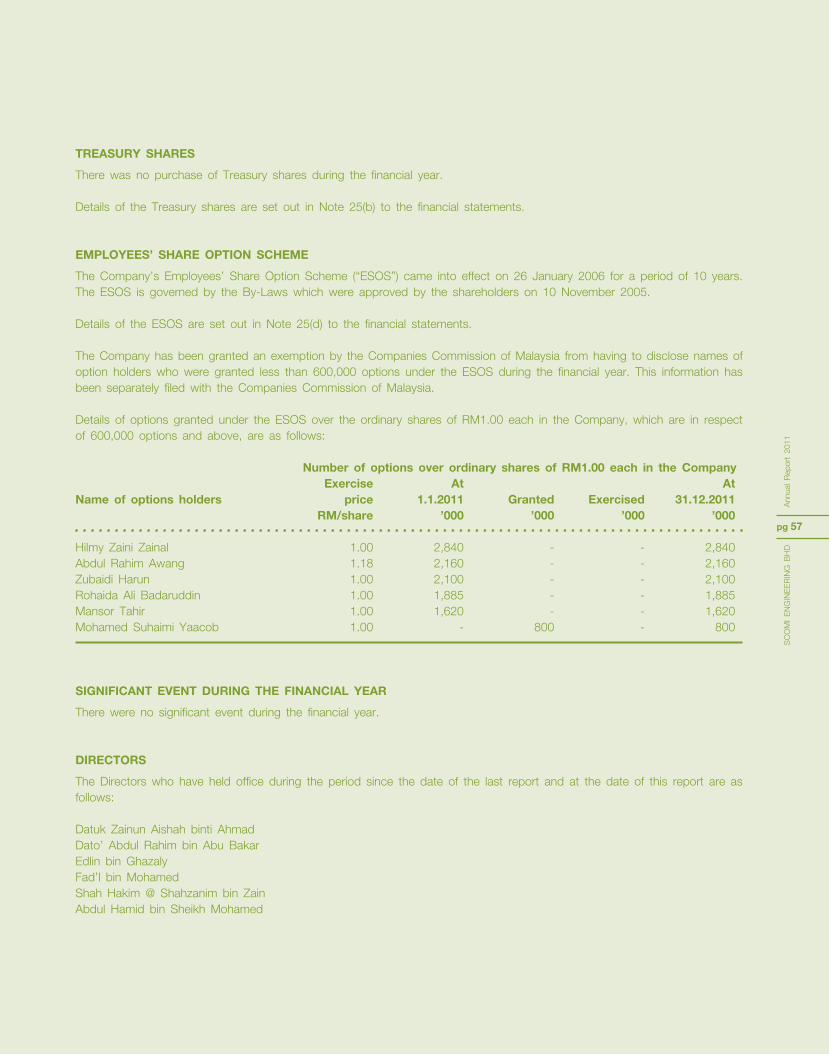

51 Information in Relation to Employees’ Share Option Scheme

52 Statement on Directors’ Responsibility

55 Financial Statements

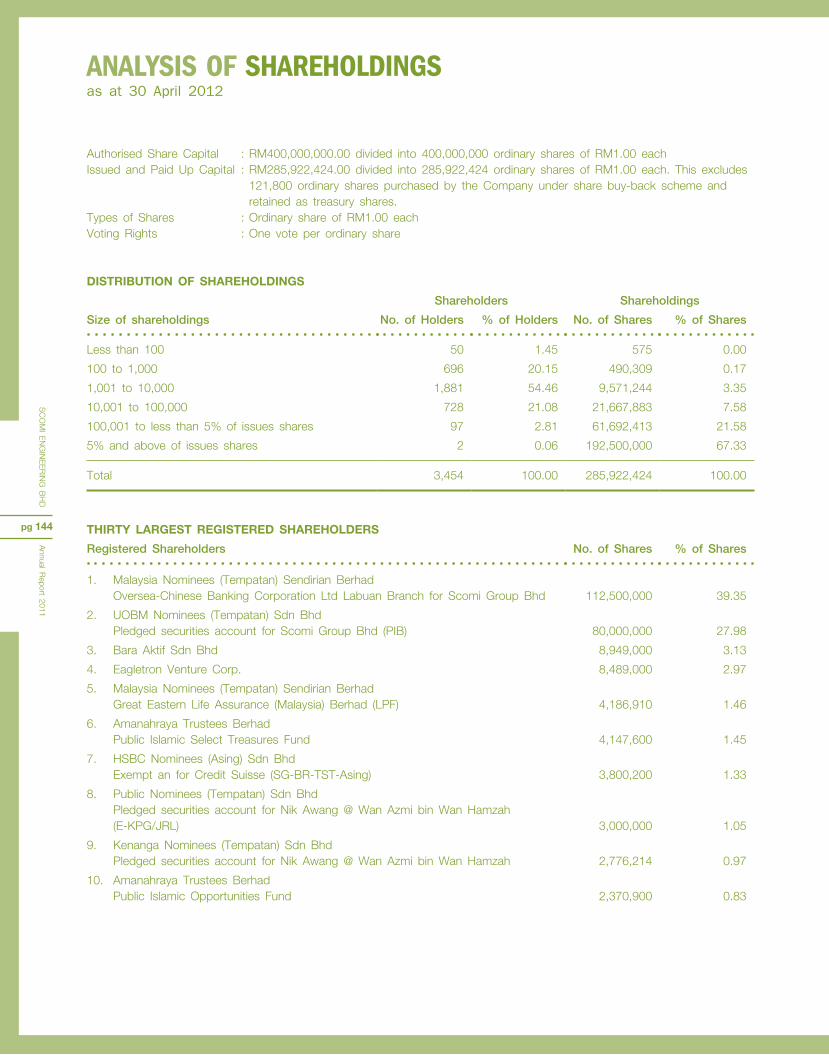

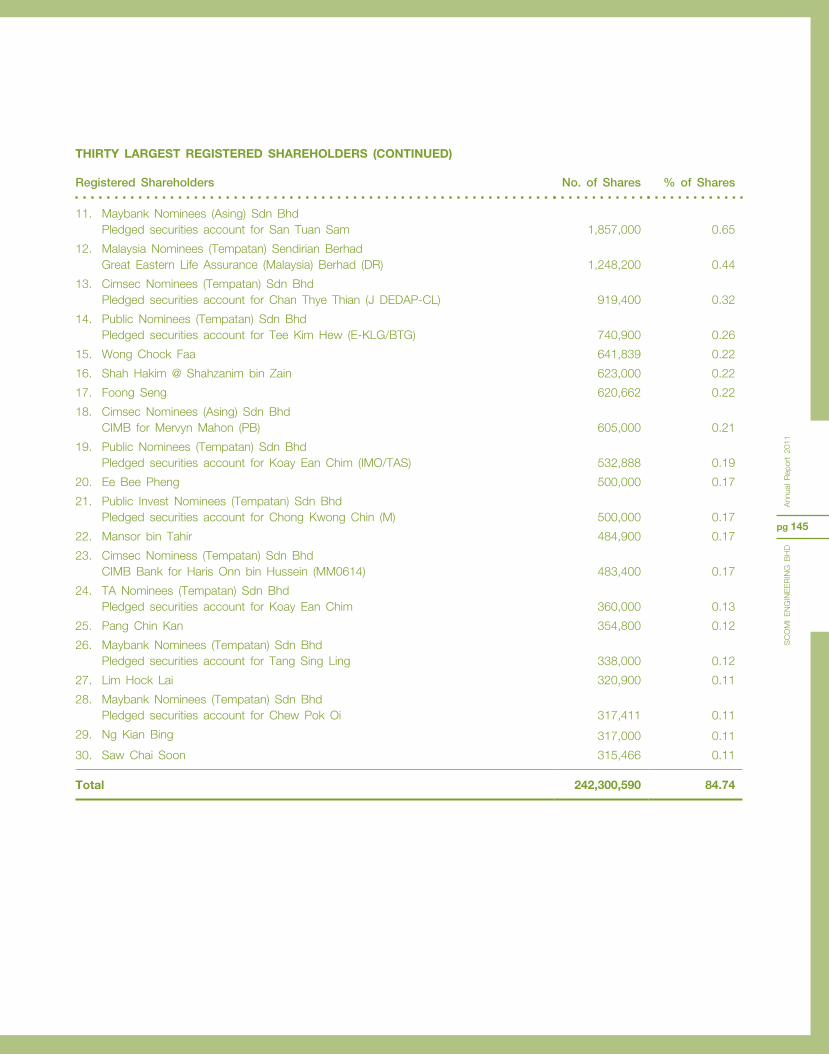

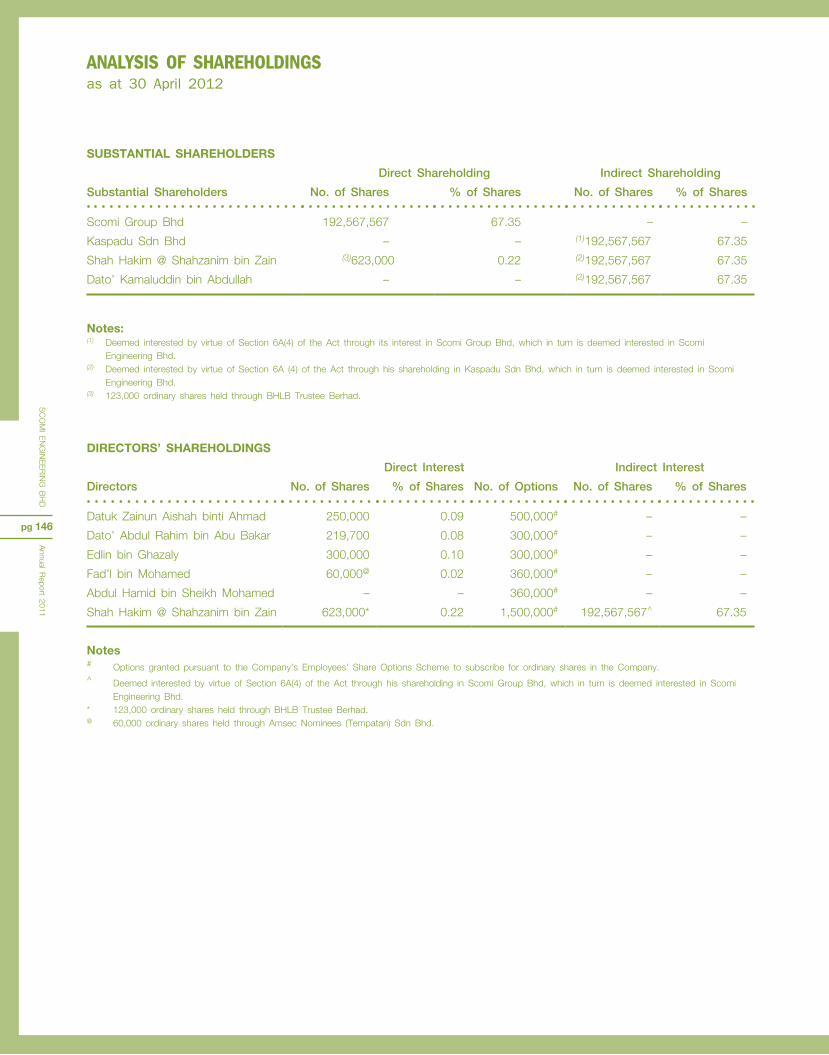

144 Analysis of Shareholdings

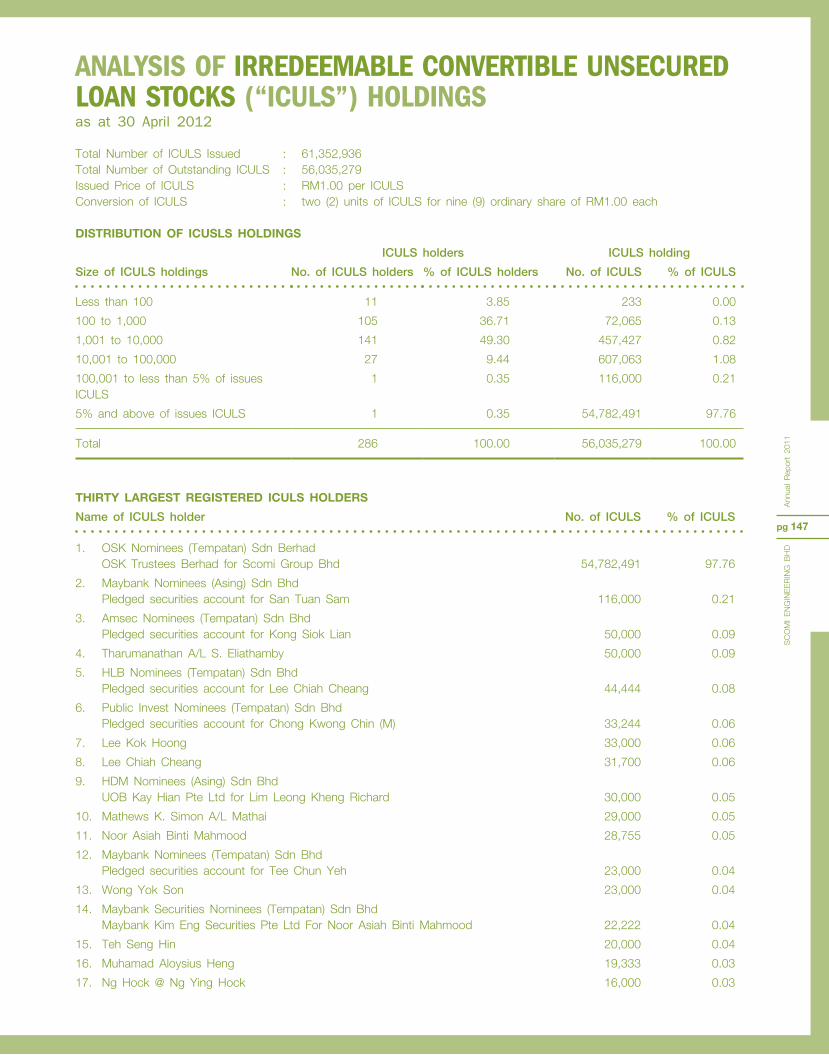

147 Analysis of Irredeemable Convertible Unsecured Loan Stocks (“ICULS”) Holdings

149 List of Property

150 Corporate Directory

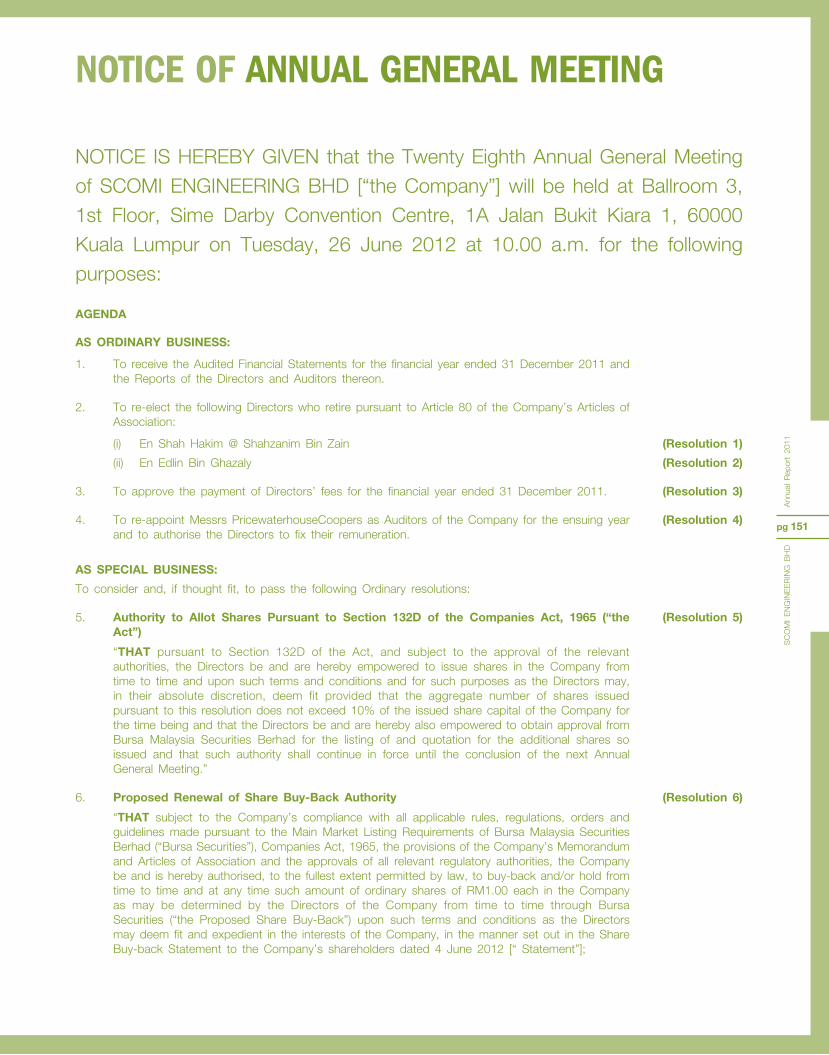

151 Notice of Annual General Meeting

154 Statement Accompanying Notice of the Twenty Eighth Annual General Meeting

• Form of Proxy

New Opportunities. Moving Ahead.

With a presence in 27 countries, Scomi Group is an accomplished global technology enterprise. Entrusted with numerous high-profile projects, Scomi’s achievements have reinforced its position as a world-class service provider and technology owner in oilfield services, transport solutions and energy logistics.

By consolidating operations and building on its strengths, Scomi will continue to seek out new opportunities in both the domestic and global market. Moving ahead, Scomi will keep delivering value to its stakeholders and making a difference in the communities it helps shape.

28th ANNUAL

GENERAL MEETING

Ballroom 3 1st Floor, Sime Darby Convention Centre 1A Jalan Bukit Kiara 1 60000 Kuala Lumpur

on 26 June 2012 at 10.00 a.m.

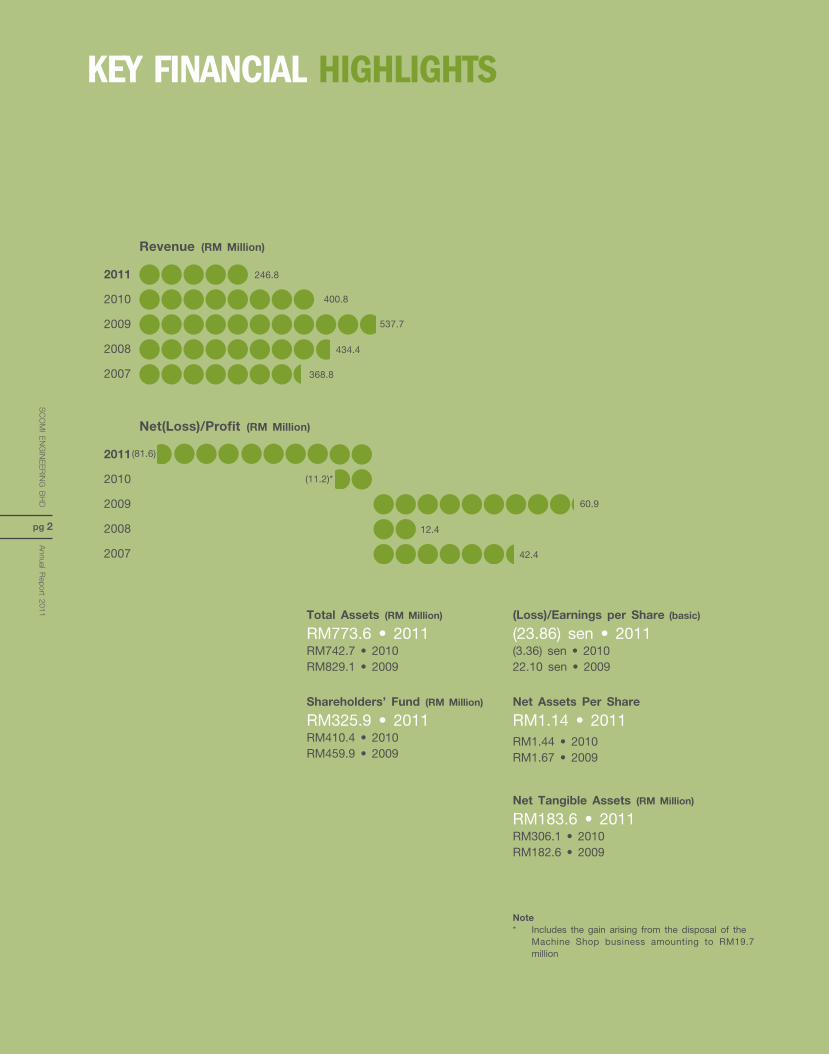

Total Assets (RM Million)

RM773.6 • 2011RM742.7 • 2010RM829.1 • 2009

Shareholders’ Fund (RM Million)

RM325.9 • 2011RM410.4 • 2010RM459.9 • 2009

(Loss)/Earnings per Share (basic)

(23.86) sen • 2011(3.36) sen • 201022.10 sen • 2009

Net Assets Per Share

RM1.14 • 2011RM1.44 • 2010RM1.67 • 2009

Net Tangible Assets (RM Million)

RM183.6 • 2011RM306.1 • 2010RM182.6 • 2009

Note* Includes the gain arising from the disposal of the Machine Shop business amounting to RM19.7

million

Revenue (RM Million)

2011

2010

2009

2008

2007

246.8

400.8

537.7

434.4

368.8

Net(Loss)/Profit (RM Million)

2011

2010

2009

2008

2007

(11.2)*

60.9

12.4

42.4

(81.6)

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 2

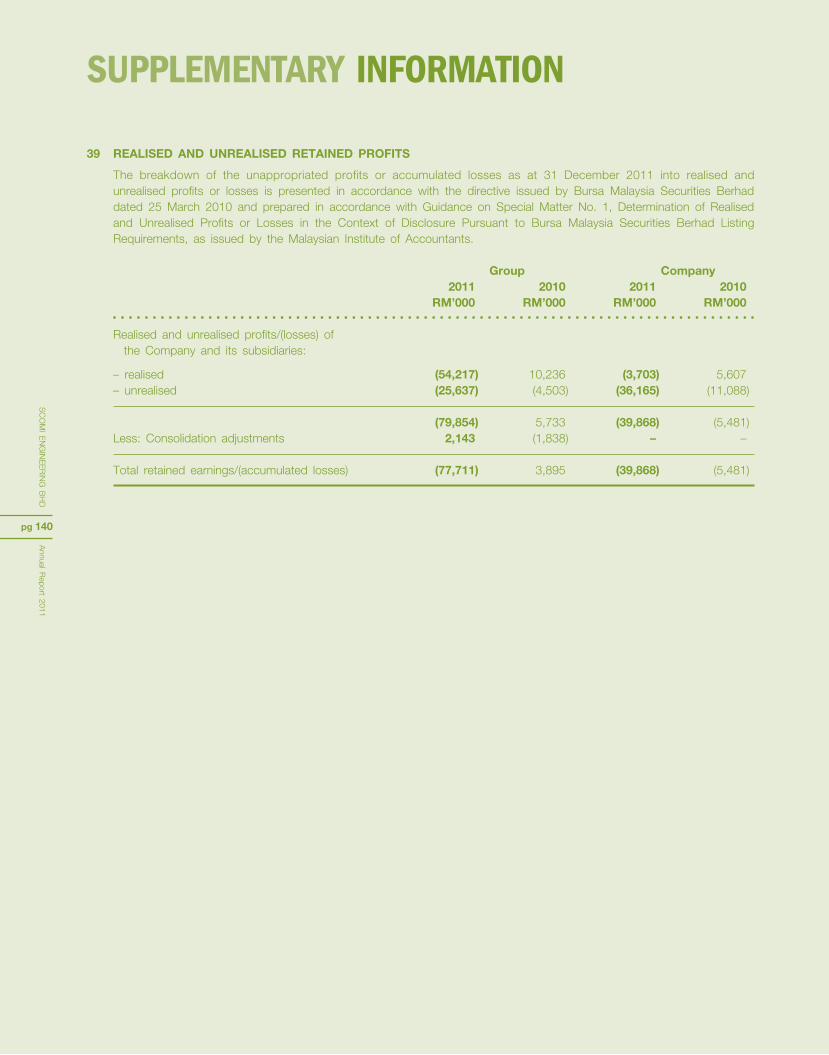

KEY FINANCIAL HIgHLIgHts

100% British Virgin Islands

India

Malaysia

Brazil

SCOMIENGINEERING

BHD

Scomi OMS Oilfield Services Ltd

Urban Transit Servicos Do Brasil Ltda**(formerly known as Trams Servicos Mercadologicos De Consultoria Ltda)

Urban Transit Pvt Ltd *

Scomi Special Vehicles Sdn Bhd

Scomi Transit Projects Sdn Bhd

Scomi Transportation Systems Sdn Bhd ***

Scomi Transit Projects Brazil (Sao Paulo) Sdn Bhd

Scomi Transit Projects Brazil Sdn Bhd

Scomi Trading Sdn Bhd

Scomi Coach Sdn Bhd

Scomi Coach Marketing Sdn Bhd

Scomi Rail Bhd

* Includes 0.001% held by Scomi Rail Bhd.** includes 1 quota (“share”) held by Scomi Rail

Bhd.*** Malaysia Nominees (Tempatan) Sdn Bhd

(“MNTSB”) is the registered shareholder in Scomi Transportation Systems Sdn Bhd (MNTSB is holding in Trust for SEB)

Notes

i. Except as otherwise expressly stated, all companies in this structure are incorporated in Malaysia.

ii. Except as otherwise expressly stated, all companies in this structure are wholly owned by their respective holding companies.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 3

sComI ENgINEErINg CorporAtE struCturEas of 31 December 2011

With a presence in 52 locations across 27 countries, the Scomi group of companies is a global technology enterprise in the energy and logistics industries.

WE ARE A GLOBAL TECHNOLOGy ENTERPRISE.

Our global reach, capabilities and talent provide us with the necessary resources to develop and own new technology in all areas of our business.

W E F O C U S O N E N E R G y & LOGISTICS.

All of our 3 business units are focused on the Energy and/or Logistics sectors with the ability to compete globally. All of us in the Scomi family should remember that any new initiatives we undertake will focus on these areas of business.

W E P R O v I D E I N N O v A T I v E SOLUTIONS.

We innovate to respond to an evolving env i ronment . Our products and operations meet today’s needs while ant ic ipat ing tomorrow’s. We are committed to developing competitive and innovative solutions to create efficiency, add value and grow with our customers to shape our future.

WE AIM TO REALISE POTENTIAL FOR OUR STAKEHOLDERS.

• Our customers: We will develop and offer customers innovative and competitive products and services that help them grow their business.

• Our shareholders: We are committed to providing long-term superior returns to our shareholders.

• Our people: We aim to provide our employees with developmental opportunities so they can succeed on personal and professional levels.

• Our suppliers: We will treat our suppliers as our partners in the mutual interest of business growth.

• Our society/environment: As a good corporate citizen, we will give back to the communities we operate in worldwide.

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 4

CorporAtE stAtEmENt oF sComI group

DIRECTORS

Datuk Zainun Aishah Binti Ahmad Chairman

Dato’ Abdul Rahim Bin Abu Bakar

Edlin Bin Ghazaly

Fad’l Bin Mohamed

Abdul Hamid Bin Sheikh Mohamed

Shah Hakim @ Shahzanim Bin Zain

AUDIT AND RISK MANAGEMENT COMMITTEE

Dato’ Abdul Rahim Bin Abu Bakar Chairman

Edlin Bin Ghazaly

Fad’l Bin Mohamed

Abdul Hamid Bin Sheikh Mohamed

NOMINATION AND REMUNERATION COMMITTEE

Datuk Zainun Aishah Binti Ahmad Chairman

Dato’ Abdul Rahim Bin Abu Bakar

Edlin Bin Ghazaly

OPTIONS COMMITTEE

Edlin Bin GhazalyChairman

Dato’ Abdul Rahim Bin Abu Bakar

Shah Hakim @ Shahzanim Bin Zain

REGISTERED OFFICE

Level 17, 1 First AvenueBandar Utama47800 Petaling JayaSelangor Darul Ehsan, MalaysiaT +603 7717 3000F +603 7727 7935

ADMINISTRATIvE AND CORRESPONDENCE ADDRESS

Level 17, 1 First AvenueBandar Utama47800 Petaling JayaSelangor Darul Ehsan, MalaysiaT +603 7717 3000F +603 7727 7935w www.scomiengineering.com.myE [email protected]

REGISTRAR

Symphony Share Registrars Sdn BhdLevel 6, Symphony HouseBlock D13, Pusat Dagangan Dana 1Jalan PJU 1A/4647301 Petaling JayaSelangor Darul Ehsan, MalaysiaT +603 7841 8000F +603 7841 8008

ADvOCATES & SOLICITORS

Albar & PartnersAdvocates & Solicitors6th Floor, Faber Imperial CourtJalan Sultan Ismail50250 Kuala Lumpur, Malaysia

COMPANy SECRETARIES

Chua Hooi Sian (MAICSA 7014565)Catherine Mah Suik Ching (LS 01302)

AUDITORS

PricewaterhouseCoopers (AF: 1146)Chartered AccountantsLevel 10, 1 SentralJalan Travers, Kuala Lumpur SentralP O Box 10192, 50706 Kuala LumpurMalaysia

PRINCIPAL BANKERSUnited Overseas Bank (Malaysia) BerhadMenara UOB, Jalan Raja LautPO Box 1121250738 Kuala Lumpur, Malaysia

CIMB Bank BerhadBangunan CIMB, Jalan SemantanDamansara Heights50490 Kuala Lumpur, Malaysia

Malayan Banking BerhadMenara Maybank100, Jalan Tun Perak50050 Kuala Lumpur, Malaysia

OCBC Bank (Malaysia) BerhadMenara OCBC18, Jalan Tun Perak50050 Kuala Lumpur, Malaysia

Standard Chartered Bank Malaysia BerhadMenara Standard Chartered30 Jalan Sultan Ismail50250 Kuala LumpurMalaysia

Export-Import Bank of Malaysia BerhadLevel 1, EXIM BankJalan Sultan Ismail 50250 Kuala LumpurMalaysia

STOCK ExCHANGE LISTING

Main Board of Bursa MalaysiaSecurities BerhadStock Name: ScomienStock Code: 7366

CURRENCy

Ringgit Malaysia (RM)

SC

OM

I E

NG

INE

ER

ING

BH

D

pg 5

Ann

ual

Rep

ort

2011

CorporAtE INFormAtIoN

Reinventing ourselves to realise opportunitiesWe continue to recognise the importance of re-inventing

ourselves, re-evaluating our endeavours and following

through with strategies that will increase our opportunities

in the global market.

Datuk Zainun Aishah Binti AhmadChairman, Independent Non-Executive Director

Datuk Zainun Aishah, a Malaysian, aged 65, was appointed to the Board on 15 December 2005. She is also the Chairman of the Company’s Nominat ion and Remuneration Committee.

Datuk Zainun Aishah graduated from University of Malaya with an Honours Degree in Economics. Datuk Zainun Aishah began her career with Malaysian Industrial Development Authority (“MIDA”), the Malaysian government’s principal agency for the promotion and coordination of industrial development in the country where she worked for 35 years. In her years of service, she held various key positions in MIDA as well as in some of the country’s strategic council, notably her pivotal role as National Project Director in the formulation of Malaysia’s first Industrial Master Plan. She was the Director-General of MIDA for 9 years and Deputy Director-General for 11 years.

Datuk Zainun Aishah was a Director of Tenaga Nasional Berhad, Kulim Hi-Tech Park and Malayan Banking Berhad.

Currently Datuk Zainun Aishah’s other directorships in public companies are, Microlink Solutions Berhad, Degem Bhd, Pernec Corporation Bhd, Berjaya Media Berhad, Berjaya Food Bhd, Shell Refinery Company (Federation of Malaysia) Bhd and British American Tobacco (Malaysia) Berhad.

Datuk Zainun Aishah attended all ten (10) Board Meetings of the Company held during the financial year ended 31 December 2011.

Datuk Abdul Rahim Bin Abu BakarIndependent Non-Executive Director

Dato’ Rahim, a Malaysian, aged 66, was appointed to the Board on 15 December 2005. He is the Chairman of the Company’s Audit and Risk Management Committee. He is also a member of the Company’s Options Committee and Nomination and Remuneration Committee.

Dato’ Rahim graduated from the Brighton College of Technology, United Kingdom with B.Sc (Hon) Electrical Engineering in 1969. Dato’ Rahim is a member of the Institute of Engineers Malaysia (“MIEM”) and is a Professional Engineer, Malaysia (P.Eng). He also holds the Electrical Engineer Certificate of Competency Grade 1. Dato’ Rahim began his career in 1969 with the then National Electricity Board. He was attached to the organisation for 10 years in various technical and engineering positions before he moved on to the private sector. From 1979 to 1983, he served with Pernas Charter Management Sdn Bhd, a management company for the tin mining industry. Then, from late 1983 to 1991, he was attached to Malaysia Mining Corporation Berhad (“MMC”) in various senior positions. Later from 1991 to 1995, he moved on to MMC Engineering Services Sdn Bhd and subsequently to MMC Engineering Group Berhad as the Managing Director. In May 1995, he joined Petronas to assume the position of Managing Director of Petronas Gas Berhad (“PGB”) and subsequently moved on to Petronas as its Vice President, in charge of the Petrochemical Business in 1999. He retired from Petronas on 31 August 2002.

Dato’ Rahim’s other directorships in public companies are Telekom Malaysia Bhd, Scomi Group Bhd and Global Maritime Ventures Bhd. Save for Global Maritime Ventures Bhd, all the other companies are listed on the Bursa Malaysia Securities Berhad. He is also a director of a public listed company in India, Infrastructure Development Finance Corporation Ltd.

Dato’ Rahim attended Nine (9) out of Ten (10) Board Meetings of the Company held during the financial year ended 31 December 2011.

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 8

proFILE oF DIrECtors

Encik Fad’l holds an Honours Degree in Law from the University of London, and a Certified Diploma in Accounting and Finance (Association of Chartered Certified Accountants). He started his career as a lawyer in Messrs. Rashid & Lee in 1991 to 1993.

He then joined the Securities Commission in 1993 to serve in the Take-Overs and Mergers Department and subsequently in the new Product Development Department. Between 1996 and 1999, he was attached to the Kuala Lumpur offices of Dresdner Kleinwort Benson, a global investment bank, providing cross-border M&A advice and other corporate advisory services to Malaysian and foreign corporations. He is currently the founder and Managing Director of Maestro Capital Sdn Bhd, a licensed corporate finance advisor providing corporate finance advisory services in the areas of mergers and acquisition and capital raising.

Encik Fad’l is a director of CIMB-Principal Asset Management Berhad and holds directorships in various private companies. He is also an independent investment committee member of CIMB-Principal Asset Management Berhad and CIMB Nasional Equity Fund.

Encik Fad’l attended all ten (10) Board Meetings of the Company held during the financial year ended 31 December 2011.

Edlin Bin GhazalyIndependent Non-Executive Director

Fad’l Bin MohamedIndependent Non-Executive Director

Encik Edlin, a Malaysian, aged 47, was appointed to the Board on 20 December 2004. He is the Chairman of the Company’s Options Committee. He is also a member of the Company’s Nominat ion and Remuneration Committee and Audit and Risk Management Committee.

Encik Fad’l, a Malaysian, aged 44, was appointed to the Board on 15 December 2005. He is a member of the Company’s Audit and Risk Management Committee.

Encik Edlin read law at the International Islamic University (IIU), graduating in 1989, and was admitted to the Malaysian Bar in 1990. Over the past 22 years, he has established a notable career in the legal profession and set up his own practice in 1994.

Encik Edlin attended all ten (10) Board Meetings of the Company held during the financial year ended 31 December 2011.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 9

Abdul Hamid Bin Sheikh MohamedIndependent Non-Executive Director

Encik Abdul Hamid, a Malaysian, aged 47, was appointed to the Board on 24 February 2010. He is a member of the Company’s Audit and Risk Management Committee.

Encik Abdul Hamid, a Fellow of the Association of Chartered Certified Accountants, is currently the Executive Director of Symphony House Berhad. He started his career in the accounting firm Messrs Lim Ali & Co/Arthur Young, before moving on to merchant banking with Bumiputra Merchant Bankers Berhad. He later moved on to the Amanah Capital Malaysia Berhad Group, an investment banking and finance group, where he led the corporate planning and finance functions until 1998 when he joined the Kuala Lumpur Stock Exchange (“KLSE”), now known as Bursa Malaysia Berhad. During his five years with the KLSE Group, he held diverse roles and had experience in strategy, corporate finance, business transformation, finance and administration, treasury, external affairs and public relations. He led KLSE’s acquisitions of KLOFFE and COMMEX and their merger to form MDEX, and the acquisition of MESDAQ. He also led KLSE’s demutualisation exercise.

Encik Hamid’s other directorships in public companies are Symphony House Berhad, SILK Holdings Bhd and MMC Corporation Berhad.

Encik Hamid attended eight (8) of ten (10) Board Meetings of the Company held during the financial year ended 31 December 2011.

Shah Hakim @ Shahzanim Bin ZainChief Executive Officer/ Non-Independent Executive Director

Encik Shah Hakim, a Malaysian, aged 47, was appointed to the Board as Non-Independent Executive Director on 15 December 2005 and as Chief Executive Officer on 1 August 2011. He is also a member of the Company’s Options Committee.

Encik Shah Hakim started his career as an auditor with Ernst & Young and was subsequently promoted as Consulting Manager, responsible for servicing large corporations. He went on to be appointed as Executive Director of a regional packaging manufacturer in 1992, with direct operational responsibility. He currently sits on the Board of Sapura Industrial Berhad, Scomi Marine Bhd, Scomi Group Bhd and KMCOB Capital Berhad.

Encik Shah Hakim attended all ten (10) Board Meetings of the Company held during the financial year ended 31 December 2011.

Notes:None of the Directors have:

• Any family relationship with any Director and/or substantial shareholder of Scomi Engineering Bhd

• Any conflict of interest with Scomi Engineering Bhd; and• Any conviction for offences within the past 10 years (other than

traffic offences, if any)

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 10

proFILE oF DIrECtors

Shah Hakim ZainChief Executive Officer

Suhaimi yaacobPresident – Rail

Mastura MansorVice President

Group Human Resource

Zubaidi HarunVice President

Business Development

Radhi MohamadChief Financial Officer

mANAgEmENttEAm

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 12

Mansor TahirHead – Commercial Vehicles

Abdul Wahab Mohamed Khalid

Head – Engineering

Chee Chiak yangHead – Turnkey Services

yan Siew ChingGroup Financial Controller

Revantha SinnetambyHead – Legal & Secretarial

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 13

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 13

CHAIRMAN’SstAtEmENt

Datuk Zainun Aishah Binti AhmadChairman

The year 2011 proved to be eventful with significant progress accomplished in on-going projects and a number of new contracts being signed in our Rail segment. Consequently, I have great pleasure in presenting our audited financial statement for the year ended 31 December 2011.

Dear Stakeholders,

Although the operating environment was extremely challenging for global businesses, given the continuing economic crises in the US and Europe, there were some bright spots, mainly in emerging markets that have been kept afloat by strong internal demand.

Public investment into urban transport in particular remained strong in rapidly developing nations such as Brazil and India, where Scomi Engineering has been focusing our energies. Our years of groundwork in Brazil came to fruition when we were awarded two significant monorail projects – in the cities of Sao Paolo and Manaus. In India, we continued to make progress on the Mumbai monorail project and took part in various other tenders for monorail development in other major cities.

In Malaysia, too, there is a resurgence in interest in urban public transport, particularly in conjunction with the Greater Kuala Lumpur/Klang Valley i n i t i a t i ve unde r t he Econom ic Transformation Programme. We are already playing a part in this, following the award in December 2010 by Syarikat Prasarana Negara Bhd (SPNB) to expand the KL Monorail. However, we are confident we can play a bigger role in transforming public transport in

the Greater KL/KV and have submitted tenders for more projects under this National Key Economic Area (NKEA).

FINANCIAL PERFORMANCE

Our revenue for the year of RM246.8 million was lower than the RM350.0 million achieved in 2010 mainly as a result of delays in our monorail project in Mumbai, India. Most of this revenue was derived from our Rail segment, which contributed RM202.2 million, or 81.9%, of the total. The remaining RM44.6 million was contributed by our Coach and Special Purpose Vehicles (SPV) segment.

We made a net loss of RM81.6 million as compared to RM30.9 million in 2010 (excluding the gain of RM19.7 million from the disposal of our machine shop businesses in June 2010). This was due to lower work done and project cost revisions, mainly from the Mumbai monorail delays. However, as we have been given an extension on time for this project, we expect future losses to be minimised and our project costs to be mitigated. Along with our partner, Larsen & Toubro, we are doing our best to expedite completion of this eagerly anticipated urban transport system in India’s commercial capital.

Because of the losses incurred and our projected expansion in the coming years, the Board of Directors has decided not to pay a dividend for the year under review.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 15

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 16

CHAIrmAN’s stAtEmENt

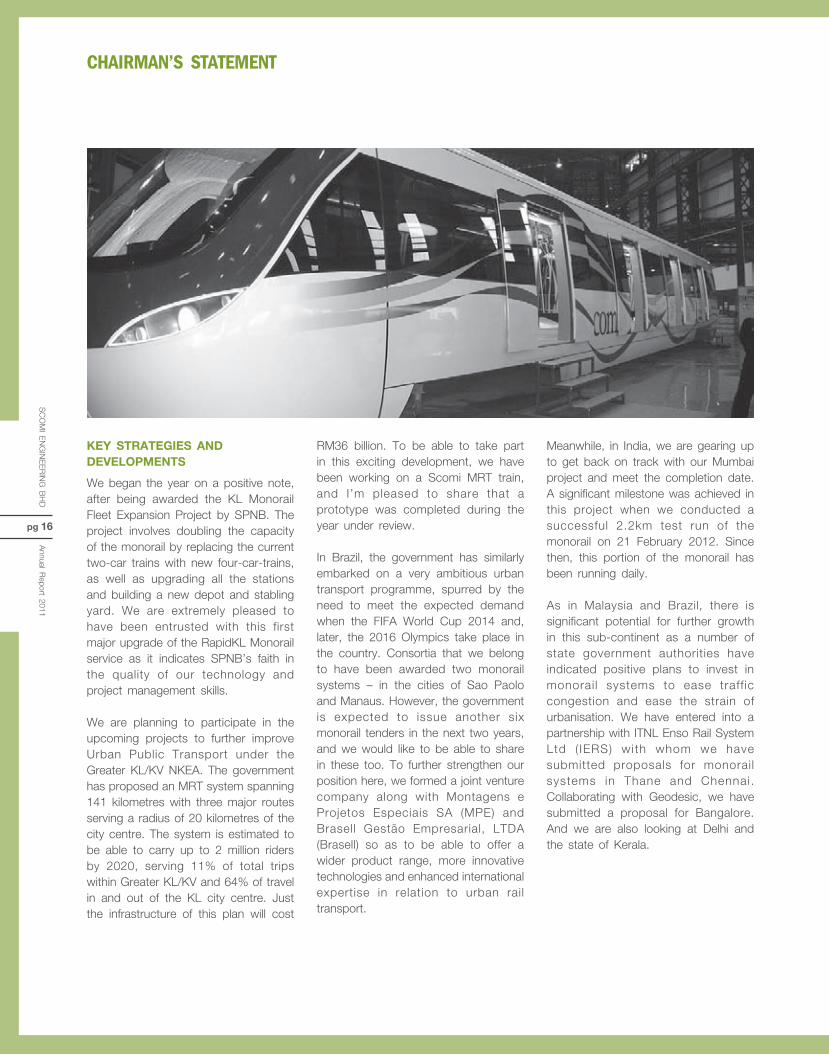

KEy STRATEGIES AND DEvELOPMENTS

We began the year on a positive note, after being awarded the KL Monorail Fleet Expansion Project by SPNB. The project involves doubling the capacity of the monorail by replacing the current two-car trains with new four-car-trains, as well as upgrading all the stations and building a new depot and stabling yard. We are extremely pleased to have been entrusted with this first major upgrade of the RapidKL Monorail service as it indicates SPNB’s faith in the quality of our technology and project management skills.

We are planning to participate in the upcoming projects to further improve Urban Public Transport under the Greater KL/KV NKEA. The government has proposed an MRT system spanning 141 kilometres with three major routes serving a radius of 20 kilometres of the city centre. The system is estimated to be able to carry up to 2 million riders by 2020, serving 11% of total trips within Greater KL/KV and 64% of travel in and out of the KL city centre. Just the infrastructure of this plan will cost

RM36 billion. To be able to take part in this exciting development, we have been working on a Scomi MRT train, and I’m pleased to share that a prototype was completed during the year under review.

In Brazil, the government has similarly embarked on a very ambitious urban transport programme, spurred by the need to meet the expected demand when the FIFA World Cup 2014 and, later, the 2016 Olympics take place in the country. Consortia that we belong to have been awarded two monorail systems – in the cities of Sao Paolo and Manaus. However, the government is expected to issue another six monorail tenders in the next two years, and we would like to be able to share in these too. To further strengthen our position here, we formed a joint venture company along with Montagens e Projetos Especiais SA (MPE) and Brasell Gestão Empresarial, LTDA (Brasell) so as to be able to offer a wider product range, more innovative technologies and enhanced international expertise in relation to urban rail transport.

Meanwhile, in India, we are gearing up to get back on track with our Mumbai project and meet the completion date. A significant milestone was achieved in this project when we conducted a successful 2.2km test run of the monorail on 21 February 2012. Since then, this portion of the monorail has been running daily.

As in Malaysia and Brazil, there is significant potential for further growth in this sub-continent as a number of state government authorities have indicated positive plans to invest in monorai l systems to ease traff ic congestion and ease the strain of urbanisation. We have entered into a partnership with ITNL Enso Rail System Ltd ( IERS) with whom we have submitted proposals for monorail systems in Thane and Chennai. Collaborating with Geodesic, we have submitted a proposal for Bangalore. And we are also looking at Delhi and the state of Kerala.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 17

Our successes to date in Brazil and India can be attributed to strategic planning that has seen us partner with strong players in these countries, such as Larsen & Toubro (L&T), Geodesic Techniques, IERS, Infrastructure Leasing & Financial Services Limited (IL&FS) and Engineering Project (India) (EPI) Ltd in India; and CR Almeida and AG in Brazil.

At the same time, we have been relentless in our focus on R&D to ensure our products are comparable to the best in the global marketplace. In 2011, in addition to the new MRT train we were also working on a better and more ef f ic ient Gen 2.1 SUTRA prototype. Our constant attention to reliability, quality and cost has allowed us to constantly innovate on our products to satisfy global standards and al low us to be competit ive internationally.

Our customers have always been at the heart of our business operations, and we regularly re-evaluate our customer engagement practices in order to ensure the highest standards of serv ice and project del ivery. Accordingly, last year, we embarked on several initiatives to further improve our systems and processes to simplify procedures so as to be a preferred service or business partner.

We are confident that our Rail unit will continue to grow in 2012 and beyond. The year under review was a little slow for our Coach & SPV unit, but with improved efficiencies, better cost management and aggressive marketing, we are posit ive of seeing some substantial returns from it in the near future.

As we expand our global footprint, Scomi Engineering will continue to prioritise excellence in product quality and project execution, while maintaining strict cost control. We believe the future holds many opportunities for our further growth, and in order to capitalise on t h e s e , w e w i l l e n h a n c e o u r competitiveness by strengthening our design and manufacturing capabilities so that our best-in-class offerings meet our global and local customers’ demands.

PROSPECTS

As I mentioned earlier, the global economic downturn is not affecting all countries equally. A number of emerging economies have been able to continue with their development plans, driven by internal forces of demand for products and services. Along with economic development, these countries are experiencing greater urbanisation which in turn creates a need for greater and more efficient public transport. We believe we are in a position to meet the urban transport needs of these emerging markets with our proven monorail technology. Our R&D team at the Engineering, Technology and Innovation Centre (ETIC), located in the Malaysian capital has been working assiduously on better, more cost effective and environment-friendly designs which will help tremendously in overpopulated and dynamic cities.

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 18

CHAIrmAN’s stAtEmENt

ACKNOWLEDGEMENTS

On behalf of the Board of Directors, I would like to acknowledge all our stakeholders who have made possible the successes that we achieved. We thank our highly valued shareholders for their continued trust in our vision and strategies. We would like to extend our appreciation to our customers, particularly the governments of Brazil, India and Malaysia, for giving us the opportunity to contribute to urban transport development in their countries. We are deeply grateful to our business partners, suppliers and financiers who share the same vision as us and who have made possible our growth and geographic expansion.

I would like to take this opportunity to acknowledge my fellow Board members for their wisdom and guidance. And, finally, I wish to express my sincere gratitude to the management and staff of Scomi Engineering for their hard work and commitment to the company.

Sincerely,

Datuk Zainun Aishah Binti AhmadChairman

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 19

Ensuring sustainability through strategic actionsSustainability is a major focus for our businesses. As

such, we have embarked on various key initiatives and

strategic measures to add value, realise potential and

fortify our balance sheet.

CHIEF ExECutIvE oFFICEr’s rEvIEW oF opErAtIoNs

Shah Hakim ZainChief Executive Officer

OvERvIEW

Even as growth of the global economy dropped from 5.1% in 2010 to 4.3% in 2011, emerging and developing nations maintained a relatively high growth of 6.6%, with the greatest activity seen in China (9.6%) and India (8.2%). In other words, economic growth around the world was unbalanced, with the scales definitely tipped in favour of Asia and other developing regions.

Along with rapid development in these areas, there is a concomitant increase in urbanisation. According to the World Bank, in China and India alone, more than 500 million people are expected to migrate by 2020 to urban areas that already have one million residents or more. The World Bank goes on to note that if there isn’t any efficient and environment-friendly public transport, there will be serious repercussions in terms of traff ic congestion, road accidents and pollution. Already, in many Chinese and Indian cities, motor vehicle ownership rates are rising faster than population and income.

Acknowledging the potentially explosive situation, governments in a number of emerging nations have embarked on massive transformation of their public transport systems. Infrastructure spend over the next two decades in Asia, the

Gulf and South America has been estimated to lie in the region of USD871 billion, of which USD400 billion will be in Asia, USD300 billion in the Middle East and USD171 billion in South America.

Although there has been a slowdown in infrastructure development in the Middle East due to the political turmoil that unfolded in the spring of 2011, as well as in some countries in Southeast Asia – such as Indonesia, Thailand and Vietnam, where other national agendas have taken precedence over urban transport – there is still abundant scope for the monorail systems for which Scomi Engineering has developed niche expertise. This is especially true in countries we have targeted, namely Brazil, India and Malaysia.

In preparation for the FIFA World Cup 2014, the Brazilian Government has set aside a budget of BRZ Real 104.5 billion for projects related to transport, and is expected to float at least another 20 tenders in the next 24 months of which five or six are projected to be monorail systems. In India, there are plans for nine monorail networks spanning a total of 184km. In Malaysia, m e a n w h i l e , t h e E c o n o m i c Transformation Programme (ETP) unveiled by the Government in 2010

Dear Stakeholders, It’s been an eventful year of many exciting starts and a few unexpected stops for Scomi Engineering Berhad (“Scomi Engineering”, “the Group” or “the Company”). Taken as a whole, the events that unfolded have been promising and we have every reason to believe we are on the right track in our journey towards becoming a global transport solutions provider. It gives me great pleasure to report on our achievements for the year ended 31 December 2011.

focuses on the Greater Kuala Lumpur/Klang Valley as one of 12 National Key Economic A reas , under wh ich approximately RM47 billion has been earmarked to develop an Integrated Urban Mass Rapid Transit System. Of this, RM36 billion is expected to be invested in infrastructure alone.

There is, therefore, a huge market for the Scomi Urban Transport Rai l Application, better known as SUTRA, which is not only safe, reliable, cost-efficient and energy efficient, but also ideal for crowded cities because it runs on elevated lines. We have been marketing SUTRA extensively in various developing and emerging economies over the last few years. Given the positive responses we’ve been getting and the immense potential we’ve seen for our global transport solutions, in 2010 we made the strategic decision to focus more intently on this high-growth business by disposing of our machine shops. It was a bold step to take, but it’s been validated by events in 2011 as they unfolded. Year 2011 was in no uncertain terms the year of SUTRA. And it all happened on the other side of the world – in Brazil.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 23

FINANCIAL PERFORMANCE

Scomi Engineering comprises two main units – Rail and Coaches & Special Purpose Vehicles (SPV). In 2011, our Rail unit achieved total revenue of RM202.2 million. Despite winning two significant contracts in Brazil, this was lower than the revenue of RM276.7 million in 2010 mainly because of the lower value of work done on the Mumbai monorail project, which was stalled by continuing delays in civil works and approvals. We have, however, been given an extension of time by our client – the Mumbai Metropolitan Region Development Authority – and are pulling all stops to expedite the project’s completion.

Revenue from our Rail unit, which was our main income generator, was also affected by the declining value of the Indian Rupee against the Ringgit.

Meanwhile, our Coach & SPV unit, which offers products ranging from city and inter-city to mini-range buses, achieved revenue of RM44.6 million. This was lower than its revenue of RM73.3 million in 2010, mainly as a result of a lower volume of orders following a freeze on new permits in the first half of the year which was gradually lifted in the second half.

Consequently, the Group’s revenue dropped from RM350.0 million in 2010 to RM246.8 million. The Group posted a higher net loss of RM81.6 million as compared to RM30.9 million in 2010 (excluding the gain of RM19.7 million from the disposal of the machine shop businesses in June 2010).

HIGHLIGHTS OF THE yEAR

The highlight of the year was definitely the award of two major monorail projects in Brazil. On 30 July 2011, the Consortium Monotrilho Integracao to which we belong – comprising also Andrade Gutierrez S.A. (AG Group), CR Almeida S.A. Engenharia de Obras and Montagens e Projetos Especiais SA (MPE) – was awarded the Line 17-Gold monorail project in Sao Paulo. The project covers the design works, manufacture, supply and implementation of the monorail system for a 17.6-km line to be served by 18 stations.

Our scope of work involves the supply of 24 train sets of three cars each which are expected to carry some 252,000 passengers per day. The award is valued at BRZ Real 1.4 billion (RM2.6 billion). Work began as per schedule in July 2011 and is expected to be completed in 42 months. Other than the rolling stock, we will also be supplying the vehicle management system (VMS), the design for switches, system integration and system assurance, as well as testing and commissioning.

Quick on the heels of this Sao Paulo award came our second Brazilian win – announced on 5 August 2011 – for a 20km monorail line in the city of Manaus. This BRZ Real 1.46 billion (RM2.56 billion) project was awarded to a Consortium comprising Scomi, CR Almeida S/A Engenharia De Obras (CR Almeida), Mendes Junior Trading E Engenharia S/A (Mendes Junior) and Serveng-Civ i lsan S/A Empresas Associadas De Engenharia (Serveng).

The Manaus Monorail will consist of nine stations, and involve the supply of 10 train sets of six cars each. The project is expected to be completed in 40 months, with six months assisted maintenance, to provide efficient access

to key locations in the city, in advance of the 2014 World Cup hosted by Brazil. Once completed, the monorail line will be able to carry some 35,000 passengers per hour per direction.

Together, both projects are expected to bolster our coffers. But more than the financial gain, we are extremely pleased about these projects as they reflect confidence in the Group’s capabilities as well as our track record in managing sizeable and multi-faceted urban transportation endeavours on an international scale. We do, also, have to acknowledge the strength of our consortium partners who no doubt played key roles in these wins.

CHIEF ExECutIvE oFFICEr’s rEvIEW oF opErAtIoNs

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 24

The AG Group and CR Almeida are both well-established and highly-proven construction brands not only in Brazil but more generally in South America. Their credentials and technical skills-sets will be invaluable in our further expansion in the region.

To further strengthen our position in Brazil, and to facilitate in the supply of rolling stock and other components for the two projects, on 7 December 2011 we signed a Memorandum of Understanding with MPE and Brasell Gestão Empresarial, LTDA (Brasell) to set up a joint venture company (JVC) to serve as our manufacturing arm and to pursue other rai l related services projects.

During the year we also embarked on the KL Monorail Fleet Expansion Project (KL MFEP) which was awarded to us by Syarikat Prasarana Negara Berhad in December 2010. In this project, valued at RM494 million, we will replace the existing 12 sets of two-car trains with a new fleet of 12 sets of four-car trains, to double its passenger capacity as the current system is running at 35% over-capacity. We are also upgrading the Electrical & Mechanical Systems and ensuring the 11 stations served are able to accommodate the longer trains. In addition, we have been entrusted with building a new depot and stabling yard for the project, which is scheduled for completion by July 2013.

Our Mumbai monorail project, as I mentioned earlier, has been lumbered with unavoidable delays. However, our team continued to work hard and conducted a successful 2.2km test run o f t he sys tem i n Mumba i on 21 February 2012. With continued efforts to increase the momentum of this project, we are targeting to commence operations of the first phase in 2012.

KEy INITIATIvESOur success in taking our urban transport solutions international can be distilled to two main factors: excellent product reliability and quality backed by strong R&D capabi l i t ies; and continuous efforts to engage with customers so as to enhance our relationships with them.

Our Engineering, Technology and Innovation Centre (ETIC), located in the Malaysian capital, has recently been awarded world-class quality standards certification – the ISO 9001:2008 certification for quality management s y s t e m , O H S A S 1 8 0 0 1 : 2 0 0 7 certification for occupational health and safety management system and ISO 14001 :2001 fo r env i ronmen ta l management system. It is here that our

Centre of Excel lence is housed, complete with a dedicated research team that developed the very first SUTRA prototype and where work is on-going to create the Gen 2.1 model which will be bigger, yet just as fuel-efficient. We believe strongly that to maintain an edge in the competitive global transport solutions market we need to invest in innovation, hence a significant amount of the Group’s profits is channeled back into ETIC for this purpose.

It is also at this facil ity that we manufacture and test our rolling stock and other components for our own monorails as well as for transport units as required by customers, such as locomotives, mass rapid transit (MRT) vehicles and coaches. Most recently, our team has been working on a new MMX bus model, comprising a 12m single deck coach powered by a Euro 2 engine, which we plan to make our flagship coach in the coming years.

To take our innovative products and technologies overseas, we have formed synergistic partnerships with leading companies in the fast-growing countries targeted, such as Larsen & Toubro (L&T), Geodesic Techniques, IERS,

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 25

and capacity of urban rail. It has put forward plans for the MRT system within the Greater Kuala Lumpur/Klang Valley area to span 141km with three major routes serving a radius of 20km of the city centre. The system is estimated to be able to carry up to 2 million riders by 2020, serving 11% of total trips within Greater KL/KV and 64% of travel in and out of the KL city centre. This presents a mine of opportunit ies for urban transport solutions providers such as Scomi, and we aspire to participate in the exciting transformation of Greater KL/KV by lending our growing expertise.

At the same time, we are not deterred by the delays experienced in Mumbai. If anything, we are more determined than ever to take on more projects in the vast Indian subcontinent where we have made the most critical step of gaining market entry and now face the much easier task of growing our presence. We have formed a consortium with Geodesic with whom we have proposed to build a 60km monorail in Bangalore, the capital of the Indian state of Karnataka. In June 2011, we were able to sign on ITNL Enso Rail System Ltd (IERS), a subsidiary of IL&FS Transportation Network Limited (ITNL), as our financier in this project. This is yet another very exciting venture as it represents the first

Infrastructure Leasing & Financial Services Limited (IL&FS) and Engineering Project (India) (EPI) Ltd in India; and CR Almeida and AG in Brazil.

We also form strategic alliances with leading technology partners on a project by project basis such as Siemens, Thales and Bombardier. Having experienced the advantages of these partnerships, we will continue to operate along these lines to further expand our business in the global arena.

While we have made significant strides in terms of product innovation, we realise there is a need also to focus on the processes and procedures that support our rapidly expanding business. In order to ensure quality operations and a high level of customer satisfaction, we have embarked on an Improvement Plan which will see concerted efforts made in the three areas of reliability, quality and cost. Towards this end, we will be investing more in better testing equipment, upgrading our test tracks and improving our endurance tests. We will also be enforcing stricter quality controls to improve our manufacturing capabilities. Finally, in terms of better cost control, we will make concerted efforts to reduce and recover costs while monitoring our procurement practices more closely. In terms of quality, the Improvement Plan has

already yielded positive results in the overall performance and standards of our monorail car.

We also believe strongly that the customer has to be placed foremost in all our plans and programmes. With this in mind, in 2011 we launched several customer engagement initiatives to maintain close relationship with our customers as well as business partners. In addition, as part of efforts to create closer rapport with our customers, we regularly arrange for visits to our NKLF, where guests are given a comprehensive brief on the production and process flow of our monorail technology.

PROSPECTS

Despite predictions of a further slow-down in the global economy in 2012, we are confident of accelerating the growth of our business and especially that of our urban transport solutions both in Malaysia and internationally.

In Malaysia, the Government is targeting to increase the public transport modal share (namely the percentage of commuters who use public transport) in the Klang Valley from just 12% (as of 2009) to over 50%, to match that of more developed nations. This is to be supported by an increase in coverage

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 26

CHIEF ExECutIvE oFFICEr’s rEvIEW oF opErAtIoNs

Public Private Partnership (PPP) for urban transport in India under the Swiss Challenge procurement process. We are awaiting final guidelines from the Karnataka Government before proceeding in this endeavour.

Together with IERS we also submitted a proposal for a 300km monorail system in Chennai, after the Chief Minister announced plans to introduce such a system to ease transport in this traffic-choked city of about 4.6 million people. The first phase, stretching 111km, is expected to be completed within two to three years. Along with our financial partners, we have also been pre-qualified for a monorail project proposed by the Thane Municipal Corp. of Maharashtra. In addition, we have stated our interest in the Kerala state government’s plans to develop monorail systems in the fast growing cities of Thiruvananthapuram and Kozhikode. The state authorities have set aside Rs5,100 crore for these projects and are awaiting a detailed project report before proceeding. We are also eyeing the capital Delhi, where the government has approved in principle an 11.5km-long elevated monorail corridor with 12 stations.

Neighbouring Bangladesh faces the same challenges of urbanisation and congestion as does India and we have capitalised on opportunities here by proposing a monorail in Dhaka, the national capital, to connect the Hazrat Shahjalal International Airport to the suburbs.

In Brazil, meanwhile, the government is expected to issue tenders for four more major monorail projects in the next 12 months. Needless to say, we will be pursuing these in collaboration with our partners.

We are also optimistic of our Coach & SPV unit where, again, we feel the way forward is to form strategic partnerships with key players. In December 2010, we had s igned a co-operat ion agreement with Zonda Bus Co Ltd in China to leverage on each other’s strengths and undertake the supply of chassis, parts and body kits as well as the supply of SKD/CKD buses as part of integrated urban transport systems in other overseas markets. Our team is engaging actively with their counterparts in Zonda and we hope to see some positive outcomes in the near future.

Indeed, we feel fort i f ied by the milestones achieved in 2011 and look forward to reinforcing our international reputation by strengthening our design and manufacturing capabilities while maintaining the highest level of project and service delivery, at reasonable costs, to make further progress as a global transport solutions provider in 2012 and beyond.

Thank you,

Sincerely,

Shah Hakim ZainChief Executive Officer

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 27

Reaching out through sustainable practices We aim to contribute positively towards the advancement

of the communities we operate in. Towards this end, we

are involved in various projects and initiatives such as

conservation activities, philanthropy and volunteerism,

amongst others.

CorporAtE soCIAL rEspoNsIBILItY

In today’s competitive corporate world, companies are judged not only on their financial performance but also on their contributions to society and to the preservation of the environment. At Scomi Engineering, we acknowledge our responsibility to the lives we touch either directly or indirectly, and are committed to making a positive impact in the communities where we have a presence while further strengthening our corporate reputation via upholding a culture of integrity and transparency.

We also realise that, given the nature of urban transport solutions business, we can make a positive impact on the env i ronment w i th our monora i l technology, a low-carbon transport alternative. Hence, we invest significantly in R&D to develop ‘green’ products that are efficient, cost-effective and, most importantly, that protect the environment and leave a minimal imprint.

Over the years, we have progressed along with the Group towards a more ho l i s t ic approach to corporate responsibility (CR), which has evolved from individual acts of philanthropy to becoming a mindset that influences our every decision and strategy. The Group ensures that this mindset is shared among al l employees by

reinforcing the principles of integrity and corporate citizenry in training modules and internal communication, and encouraging a spirit of volunteerism across its operations globally.

THE MARKETPLACE

Our marketplace initiatives encompass efforts to engage with our stakeholders and to better serve our customers. Via our investor relations programme, we hold investor briefings and meetings. W e a l s o m a k e i m m e d i a t e announcements to Bursa Malaysia on material activities and events, and distribute a quarterly Letter to our Shareholders. Group updates are further captured in our quarterly newsletter, Focus, which is shared with customers,

partners, suppliers, employees and other s takeholders. Meanwhi le , comprehensive information on the Group is easily accessible via our website and other electronic channels, as well as our Annual Report.

Our investment in R&D and our quest to continuously innovate led to Scomi Engineering being honoured with the Special Award for Product Excellence under the Innovative Product category at the Malaysian Ministry of International T rade and Indus t r y ’ s I ndus t r y Excellence Awards 2010 held on 24 March 2011. The award recognised the cutting-edge technology behind our SUTRA monorail system.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 31

Towards further strengthening our relationship with customers and the general public, we regularly invite key stakeholders to our Engineering, Technology and Innovation Centre (ETIC) in Rawang, Malaysia, where the SUTRA monorail was first developed and where we continue to invest in R&D to further improve our prototypes. We also take part in exhibitions, and from 8-10 November 2011 set up booths along with our Brazi l ian manufacturing partner Montagen E Projetos Especiais SA at the Negocios Nos Trihos (Business on Rails) 2011 held in São Paolo, Brazil. And we organised a KL Monorail Expansion Project (KL MEP) futsal tournament for all parties involved in this endeavour on 9 December 2011 at the rooftop of One Utama New Wing, which attracted six teams – two from Prasarana and Scomi and one each from KL StarRail and Microconsult.

We also engaged posit ively with corporate Malaysia by taking part in The Edge Bursa Malaysia Kuala Lumpur Rat Race, held on 20 September 2011. Meanwhile Group CEO Shah Hakim Zain was a panellist at several high-level conferences held in Malaysia and abroad. He contributed to a discussion on Corporate Sector Wish List: What Would Get Malaysian Businesses to Invest More in Malaysia? at the Perdana Leadership Foundation CEO Forum 2011 on 23 June 2011; and was also a panelist discussing issues facing a rapidly urbanising Mumbai at the India E c o n o m i c S u m m i t , o r g a n i s e d by the World Economic Forum, from 12-14 November 2011. Later, on 17 December 2011, he shared Scomi’s experiences in India at the 3rd Annual Young Corporate Malaysians (YCM) Summit in Kuala Lumpur.

We take seriously our commitment to creating cleaner, more efficient urban centres and fully support the Group’s introduction of a blog, Ideas For Tomorrow at which creates a platform for individuals around the world to discuss issues relating to urban development.

THE WORKPLACE

We realise that Scomi Engineering is only as good as our strongest asset, our people. We are therefore committed to nurturing a workplace that attracts the best talents and motivates them to excel. We do this by creating a culture that values and rewards performance while also reinforcing a sense of belonging to the Group. In order to bring out the best in our employees, they are constantly challenged to stretch their abilities via projects and assignments of increasing responsibility and complexity. At the same time, employees are given training and professional development opportunities to acquire relevant knowledge and skills for their career progression. All executives are required to attend a minimum of 40 hours of training a year, while non-executives need to fulfil at least 20 hours of training a year.

In order to create Group unity, we have various programmes that stamp Scomi’s unique identity and which draw the participation of our employees. We also create a sense of belonging and ownership by interacting with our employees and maintaining effective communication with them.

GLAD

Talent DevelopmentScomi Group has a dedicated Group Learning and Development (GLaD) team that conducts training programmes for staff across i ts internat ional operations. GLaD is responsible for addressing the identified skills and knowledge gaps, and for managing the Group ’s comprehens i ve t a l en t development programme, which comprises the following initiatives:

• The Work @ Scomi & Induction Programme. This two-day training is mandatory for all new employees, introducing them to the Scomi business, culture and brand. It offers the recruits an insight into what Scomi stands for, what it expects from its employees and, conversely, what employees can expect from the company.

• T h e M a n a g e m e n t T r a i n e e Programme. A imed at f resh graduates who are recruited into Scomi, this 18-month programme exposes the new recruits to all facets of the Group’s operations. During this time, the trainees are attached to different departments to enable them to pick up relevant skills that will set them on the right track for further development in Scomi.

• The Execu t i ve Management Programme. This programme brings together mid-level management from our global operations, and is geared towards enhancing their leadership skills while allowing them to meet and network with their global counterparts. In 2011, an Executive Management Programme was held in Kuala Lumpur drawing the participation of managers worldwide.

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 32

CorporAtE soCIAL rEspoNsIBILItY

• The Management Leadership Development Programme. This aims to develop future leaders for the Group, hence the high-level t ra in ing focuses on ef fect ive management and leadership skills. In 2011, the programme was held in Kuala Lumpur, attended by senior managers from our global operations.

• Global Executive Learning (GEL). Th i s i s a two-day l ea rn ing programme for senior management and is normally held in conjunction with GEM, a conference of senior management from Scomi’s global operations.

• Mentoring Programme. One-to-one mentoring is offered to managers who have demonstrated leadership potential, to help them deal with challenges and issues as they move up the leadership ladder. It is geared towards ensuring a secure leadership pipeline and forms part of Scomi’s succession plan.

• Pro jec t Genera t ing Amaz ing Engineers (GAME). This 12-month programme has been developed by Scomi Engineering to nurture well-rounded young engineers. Project GAME exposes the engineers to various aspects of rail engineering, manufacturing, product assurance and project delivery, in addition to soft skills training, which are crucial for future management positions.

Employee EngagementScomi believes that open communication across the Group – within and between all levels – acts as a cohesive force that is especially important given the international nature of its organisation. Hence, a variety of platforms and tools are used to engender an inclusive culture in which every employee matters and every voice is heard.

• Open Communication Sessions. The Group promotes the sharing of knowledge, strategic information, business direction, performance status and updates across all our businesses via teleconferences and webcast facilities. The Group CEO himself conducts staff briefings to present the Group’s quarterly results and to announce any special update. In addition, Town Hall sessions are held at which groups of about 15 employees have private sessions with the Group CEO or Presidents of the Business Units at which they are at liberty to bring up any issue for c lar i f icat ion or discussion.

• Internal Communication. All operations Group-wide are connected by an intranet, through which employees are kept updated on projects, initiatives and corporate activities. The Group recently launched Vengo+, which enables members of Scomi’s global operations to communicate with each other more easily, by sharing working files, ideas and experiences.

• Global Executive Meetings (GEM). This is an annual conference of senior management from each of Scomi’s Business Units, where the global heads review and brainstorm Group strategies. GEM 2011 was held in Melaka, Malaysia, from 2-6 October, attended by 45 members of the senior management.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 33

• Open Days. Every year, the different Divisions within Scomi Group hold Open Days to create a better sense of understanding among employees of what their colleagues in other divisions do. In 2011, Scomi Engineering held our Open Day at ETIC on 18 March.

• Hari Raya Celebration. ETIC held a Hari Raya open house on 26 September, at which in-house band, Audacious, performed Raya songs. Some 300 Scomi employees attended the celebration. The KL Monorail Expansion Project (KL MEP) team, meanwhile, organised its Hari Raya open house at the KL Monorail Depot in Brickfields on 23 September 2011, attended by 200 guests that included staff from Wisma Monorail and KL Monorail Station.

Work-Life BalanceThe Group promotes a healthy work-life balance and encourages the families of all employees to feel as if they, too, are part of the extended Scomi family. Towards this end, Scomi’s Sports Club Malaysia organises a Family Day every year, and this year brought together 500 staff and their families at the national Zoo in Kuala Lumpur.

In 2011, the head office in Kuala Lumpur also introduced flexi-hours to allow our employees to better manage their work and family obligations. They can now opt to work from either 7.30am-4.30pm, 8.00am-5.00pm, 8.30am-5.30pm or 9.00am-6.00pm. As an added bonus to Malaysian employees, the management extended the lunch hour to two hours on Friday. This enables staff to carry out important personal errands, or just to enjoy a rejuvenating break from work with colleagues or counterparts.

Performance ReviewIn 2011, the Group unveiled a new Performance Assessment & Capability Enhancement (PACE) to replace ACE, the previous performance management tool. With PACE, employees are assessed on Scomi’s three leadership capabilities, namely People Leadership, Personal Leadership and Business Leadership. Its objective is not just to evaluate performance but also to highlight areas of improvement for personal development. Via PACE, employees are engaged in a discussion to explore their strong points and agree on areas in which they can improve as well as to map a career plan that will allow them to realise their potential.

PACE also allows the management to identify employees with high potential who are provided the opportunity to fast-track their careers.

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 34

CorporAtE soCIAL rEspoNsIBILItY

Safety at WorkScomi places the highest priority on maintaining best practices in Quality, Health, Safety and Environment (QHSE) in our workplaces because we value the well-being of our employees and contractors, and are also driven to safeguard the assets of our customers. At Scomi Engineering, we have QHSE teams that function to ensure all personnel, contractors, suppliers and even visitors are aware of our well-defined QHSE policies, and to enforce these. Every employee is expected to meet basic QHSE requirements and this is taken into account in performance appraisals.

Our Mumbai office reached a milestone during the year, when it did the Group proud by completing three years without a single lost time incident on 26 July 2011. Various programmes were run to reinforce the team’s QHSE awareness and skills. The Rolling Stock team underwent a fire drill and training on using the fire extinguishers, while staff at the Wadala Project Office went through a HSE Refresher Training session. Topics included Work-site Accidents, Safe Access On-Site, Working at Height, Ladders and Crane Safety as well as Traffic Vehicles, Electricity and Safety Success.

Meanwhile a half-day Safety Talk, Fire Dri l l and First Aid Training was organised by the management of the Project Office of the KL Monorail Fleet Expansion Project on 26 July 2011 with the aim of keeping all staff aware of and trained in safety measures.

THE ENvIRONMENTAs a responsible corporate citizen, Scomi is concerned about environmental issues and takes every measure we can to minimise the wasteful use of resources as well as to protect the env i ronment i n pos i t i ve ways . Employees at our corporate offices are committed to the green cause and have implemented various programmes to reduce our environmental footprint. At our R&D centres, preservation of the environment is always factored into product development, right from the stage of design.

Our new global headquarters in 1 First Avenue in Bandar Utama, Selangor, Malaysia, has further cemented our commitment to the environment, making us immediately a very low-carbon, high-efficiency company as our new home is a certified Green Building. In this new office, we have also implemented a number of environment-friendly initiatives, such as reducing the number of printing machines, restricting colour printing as well as implementing a 3R programme to reuse, reduce and recycle.

Energy-Efficient ProductsSUTRA, or Scomi Urban Transport Rail Application, has been developed to be environment friendly. An improved direct-drive propulsion system, combined with lower vehicle weight, translates into an energy-efficient monorail system. In addition, the monorail promotes use of public transport which reduces the use of private vehicles, thus reducing carbon emissions.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 35

THE COMMUNITy

Scomi Group believes strongly that all corporate organisations have a duty to give back to the communities that support them. This is a principle the Group has adhered to from the beginning, and which has seen its involvement in the community intensify over the years. In 2005, the Group’s foundation Scomi was established. It runs a structured programme to extend help, financially or otherwise, to the underprivi leged, marginalised and needy.

At the same time, our own employees have joined forces to make a difference to society, via Project Pyramid, our flagship social responsibility (CSR) programme that has seen the involvement of employees from across our global operations. Project Pyramid in Malaysia is led by the captains of the Blue, Green, Yellow and Red Houses of the Scomi Sports Club. These captains are provided with Seed Funds and, gu ided by cer ta in parameters, carry out CSR projects of their own choosing. All staff are required to take part in their house projects, their involvement earning them points under PACE.

Project Pyramid 2011In 2011, the Yellow Team invited the World Wildlife Fund Malaysia (WWF) to present a talk on endangered wildlife to the staff at Scomi’s Global HQ and launched an interactive educational website where visitors can acquire facts and knowledge relevant to the projects accomplished by the Yellow Team.

The Red Team invited the Women’s Aid Organisation of Malaysia to present a talk at the Global HQ on violence against women. Red Team members in Kemaman, meanwhile, donated a bicycle and 40 school bags to underprivileged children. They also visited a centre for disabled children, where a talk was given to not only the kids but also their parents. They concluded the visit by presenting the children with gifts.

The Blue Team invited a medical practitioner to deliver a talk on breast cancer, covering topics from the early symptoms to effective prevention measures. Held at the Global HQ, the session emphasised that there is hope for breast cancer patients. The Blue Team also cleaned the beach at Kampung Aru in Labuan, East Malaysia.

The Green Team treated Scomi staff at the Global HQ to free 10-minute shoulder massages. They also visited the children’s cancer unit at Hospital Universiti Kebangsaan Malaysia (HUKM), and donated eight LCD TVs to UKM’s Paediatric and Oncology Ward to create a livelier atmosphere for the young patients. In Terengganu, the Green Team donated Year 6 textbooks and school tables to Sekolah Islam Darul Taqwa in Kemaman. With the help of other volunteers, they also painted the classrooms and raised RM2,000 to purchase additional books for the students.

No-Hunger GAMEThe final stage of Project GAME was a CSR project called Feed the Street, which aimed at raising awareness among Scomi staff of the problem of homelessness in Malaysia and creating an opportunity for the young engineers to prepare and distribute food packages to the homeless.

To raise funds for this project, the Team set up a booth at the Scomi Family Day in Zoo Negara to run various fundraising activities, and managed to raise more than RM7,000. On 21 July, the Team operated a carwash booth at the North Kuala Lumpur Facility to give the staff there the opportunity to contribute to this cause. In total, they collected RM8,100 for Feed the Street.

Collaborating with Reach Out Malaysia, GAME members along with more than 300 Scomi volunteers finally ‘fed the street’ at a Cook and Reach activity held at Sekolah Kebangsaan Sungai Way in Petaling Jaya on 24 July 2011. In addition to the food, a total of 150 dry packs containing small towels, vitamin C tablets, soap, toothbrushes and toothpaste, were distributed to the homeless.

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 36

CorporAtE soCIAL rEspoNsIBILItY

Yayasan ScomiYayasan Scomi continued to take on various acts of philanthropy to help those in need. Among its programmes, the foundation has been running an annual blood donation activity since its formation in 2005. Last year, i t organised its Blood Donation Drive together with the University Malaya Medical Centre on 10 March at Scomi’s Global HQ.

Yayasan Scomi also runs an outreach programme involving 11 families it has adopted in Malaysia. They include 10 families in Baling, Kedah and another in the remote area of Selama, Perak. Every year, the foundation extends financial assistance to these families to help them meet their education, nutrition, health and shelter needs. The foundation also offers counselling to the children in these communities and monitors them closely to ensure they are coping with school and community life.

In 2011, volunteers from across the Scomi Group of Companies visited the 11 families to evaluate their progress. Following these visits, they made

recommendations on how Yayasan Scomi can provide further assistance to the families. While helping the families, the visits also afford the volunteers a glimpse of the living conditions of those in remote, poverty-stricken areas.

Other activities undertaken by Yayasan Scomi during the year included a visit to the museum and KL Bird Park organized for kids from Wake One House, a talk on dyslexia, visit to Rumah Lindungan Kasih, a welfare home in Tampin, Negeri Sembilan, various Ramadhan visits to the poor

and needy, and a breaking of fast with orphans in Lipis, Pahang. Yayasan Scomi also supported GAME’s Feed the Street project.

Meanwhile, Scomi Group continued with its tradition of supporting the MERCY Malaysia Humanitarian Fund by participating in its fund-raising dinner held at the Istana Hotel, Kuala Lumpur on 7 October 2011.

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 37

A Statement on Corporate Governance communicates to stakeholders the philosophy, the policies, the practices and the operating culture adopted by an organisation in pursuit of its objectives and goals. Towards this purpose, the Board of Directors (“the Board”) of Scomi Engineering Bhd (“the Company”) sets out below the various frameworks that were adopted with regards to the governance of the Company and its subsidiaries (the “Group”). In developing its governance framework, the Board was guided by the Malaysian Code on Corporate Governance (“the Code”).

The Board is committed to ensuring that the highest standards of integrity are maintained throughout the Group and that the managers and employees of Group companies are cognisant of the interests of the stakeholders. The goal is always to ensure that the Group remains at the forefront of good governance and is recognised as an exemplary organisation in this respect.

This Statement sets out the practices which the Group has undertaken with respect to key principles and the extent of its compliance with best practices under the Code.

THE BOARD OF DIRECTORS

The BoardThe Company is led and controlled by an effective Board. The Board consists of the Chairman and five (5) Directors who are committed to guiding the Company along its path of sustainable value creation. The composition of the Boa rd r e f l e c t s a d i v e r s i t y o f backgrounds, skills and experiences in the areas of business, economics, finance, legal, general management and strategy.

The Board meets at least 5 times a year, with special meetings convened when necessary. The Board is responsible for setting the goals of the Group and in reviewing and approving medium and long term strategic plans. Timely and periodic review of the G r o u p ’ s p e r f o r m a n c e a n d implementation of the strategic plans are conducted by the Board to assess the progress made towards achieving the overall goals of the Group.

The Board is of the opinion that its current composition and size makes it an effective Board, and that the Independent Non-Executive Directors are of the calibre necessary to bring objectivity to Board decision-making.

The role of the Chairman of the Board (“ the Chairman”) and the Chief Executive Officer (“CEO”) are separated with each having a clear scope of dut ies and responsib i l i t ies. The Chairman is responsible for ensuring the Board’s effectiveness whilst the CEO has the overall responsibility for opera t iona l and o rgan isa t iona l effectiveness and implementation of Board policies, directives, strategies and decisions.

A brief description of the background of each Director is presented within the Profile of Directors section as set out on pages 8 to 10 of this Annual Report.

Board CommitteesThe Board has establ ished and delegated specific responsibilities to three (3) Committees of the Board which operate within clearly defined written Terms of Reference. The Board Committees deliberate the issues on an in-depth basis before making recommendations to the Board for approval.

The Board Committees are:

• Audi t and Risk Management Committee;

• Nomination and Remuneration Committee; and

• Options Committee. S

CO

MI E

NG

INE

ER

ING

BH

DA

nnual Report 2011

pg 38

stAtEmENt oN CorporAtE govErNANCE

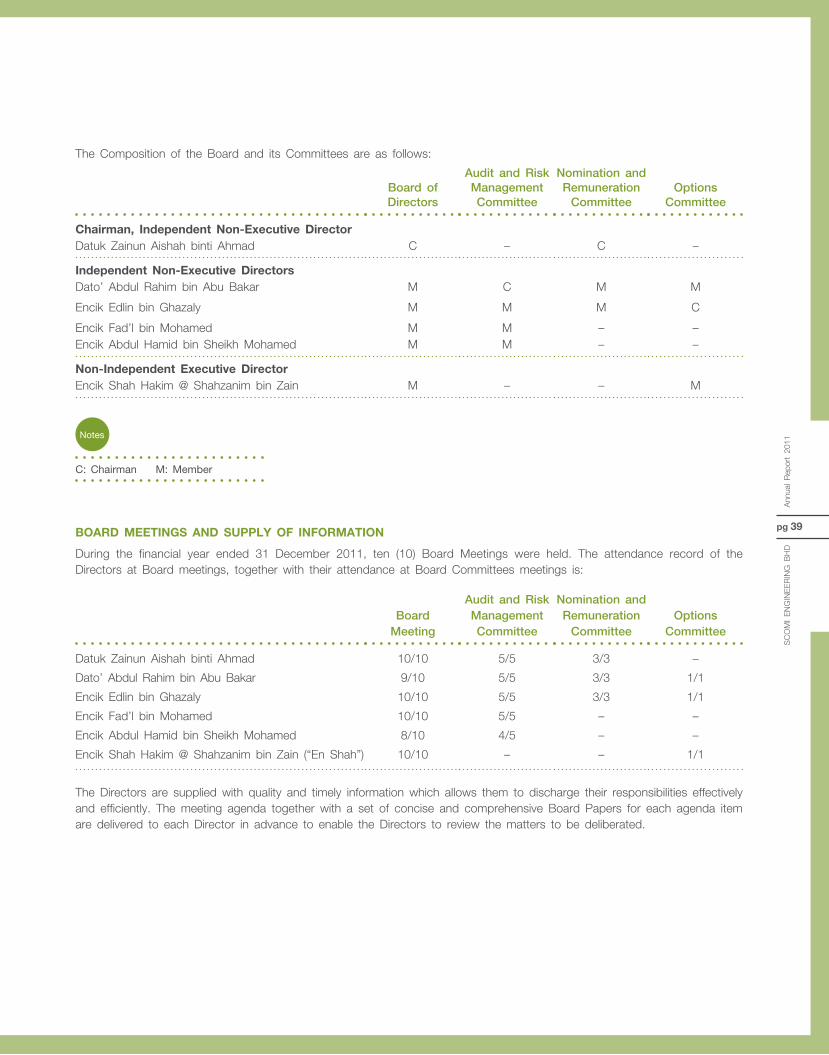

The Composition of the Board and its Committees are as follows:

Board of Directors

Audit and Risk Management Committee

Nomination and Remuneration

CommitteeOptions

Committee

Chairman, Independent Non-Executive DirectorDatuk Zainun Aishah binti Ahmad C – C –

Independent Non-Executive DirectorsDato’ Abdul Rahim bin Abu Bakar M C M M

Encik Edlin bin Ghazaly M M M C

Encik Fad’l bin Mohamed M M – –Encik Abdul Hamid bin Sheikh Mohamed M M – –

Non-Independent Executive DirectorEncik Shah Hakim @ Shahzanim bin Zain M – – M

BOARD MEETINGS AND SUPPLy OF INFORMATION

During the financial year ended 31 December 2011, ten (10) Board Meetings were held. The attendance record of the Directors at Board meetings, together with their attendance at Board Committees meetings is:

Board Meeting

Audit and Risk Management Committee

Nomination and Remuneration

CommitteeOptions

Committee

Datuk Zainun Aishah binti Ahmad 10/10 5/5 3/3 –

Dato’ Abdul Rahim bin Abu Bakar 9/10 5/5 3/3 1/1

Encik Edlin bin Ghazaly 10/10 5/5 3/3 1/1

Encik Fad’l bin Mohamed 10/10 5/5 – –

Encik Abdul Hamid bin Sheikh Mohamed 8/10 4/5 – –

Encik Shah Hakim @ Shahzanim bin Zain (“En Shah”) 10/10 – – 1/1

The Directors are supplied with quality and timely information which allows them to discharge their responsibilities effectively and efficiently. The meeting agenda together with a set of concise and comprehensive Board Papers for each agenda item are delivered to each Director in advance to enable the Directors to review the matters to be deliberated.

Notes

C: Chairman M: Member

SC

OM

I E

NG

INE

ER

ING

BH

DA

nnua

l R

epor

t 20

11

pg 39

APPOINTMENT TO THE BOARD

The Nomination and Remuneration Commit tee ( “ the NRC” ) , wh ich comprises of 3 Independent Non-Executive Directors, is delegated with the responsibility to ensure the Board has the requisite mix of skills and experience to guide the Company, and has an effective process for assessment of directors and selection of new directors to the Board. The NRC is additionally responsible for making recommendations to the Board on the re-election of Directors.

The NRC is also responsible for reviewing candidates for appointment to Board Committees, and makes appropriate recommendations thereon to the Board for approval. It is also tasked with assessing the effectiveness of the Board and Board Committees and the performance of individual directors.

The salient Terms of Reference of the NRC include:

(a) To:

• recommend to the Board potent ia l cand idates fo r directorships to be filled by the shareholders or the Board, giving consideration to:-

• the requirements of the Group;

• the candidates’ ski l ls, knowledge, expertise and experience;

• t h e c a n d i d a t e s ’ professionalism;

• the candidates’ integrity; and

• in the case of candidates f o r t h e p o s i t i o n o f Independent Non-Executive Directors, their ability to d i s c h a r g e s u c h responsibilities/functions as expected from Independent Non-Executive Directors;

• consider, in making its r e c o m m e n d a t i o n s , candidates for directorships p r o p o s e d b y t h e Management, any Director or shareholder; and

• recommend to the Board, Directors to fill the seats on Board Committees.

(b) To conduct an annual review of the required mix of skills and experience and other qualities, including core competencies which non-executive directors should bring to the Board.

(c) To assess, on an annual basis, the effectiveness of the Board as a whole, the Committees of the Board and the contributions of each individual director, including Independent Non-Execut i ve Directors, as well as the CEO and to ensure that all assessments and evaluations carried out in the discharge of this function are properly documented.

(d) From time to time, to examine the size of the Board with a view to present recommendations to the Board on the optimum number of Directors on the Board to ensure its effectiveness.

(e) To ensure that new appointees to the Board undergo an orientation and education programme.

(f) To make recommendations to the Board concerning the re-election by shareholders of any Directors under the retirement by rotation provisions in the Company’s Articles of Association.

(g) Annually, to review and assess the training needs of individual Directors and propose suitable t ra in ing programmes to be attended.

(h) To establish and recommend to the Board a fair and transparent Remuneration Policy framework for Executive Directors designed to attract, retain and motivate individuals of the highest quality. The key e l emen ts o f t h i s framework, which would form the basis of deliberations on the remuneration to be awarded, are:

• The Company’s f inancia l per fo rmance wh ich may include financial indicators such as turnover, profitability, market capital isat ion and achievement of these indicators v i s -à-v is p re-dete rmined goals;

• T h e s k i l l s , k n o w l e d g e , expertise, performance and relative experience of the Executive Directors;

• The duties and responsibilities borne by the Execut i ve Director; and

• The nature of the Company’s business e.g. international/ regional business presence.

(i) To conduct, on an annual basis (or when the need arises as in the case of proposing remuneration for a new Executive Director), a review and thereon provide advice and recommendations to the Board on all aspects of reward structure accorded to Executive Directors in terms of the following components:

SC

OM

I EN

GIN

EE

RIN

G B

HD

Annual R

eport 2011

pg 40

stAtEmENt oN CorporAtE govErNANCE

• Basic salaries and basis of i ncrement app l ied (as a percentage of basic salary, f i xed quan tum o r mer i t increment);