sbi etf it - mutual fund india

TRANSCRIPT

NFO Start Date:

6th October, 2020

NFO Close Date:

13th October, 2020

Exchange Traded Funds and their advantages

Exchange Traded Funds – What are they?

ETF’s are the perfect combination of two great investment ideas brought together

ETFs

DiversifiedTradable during the day

Diversified funds that trade like stocks

Mutual FundStock

3

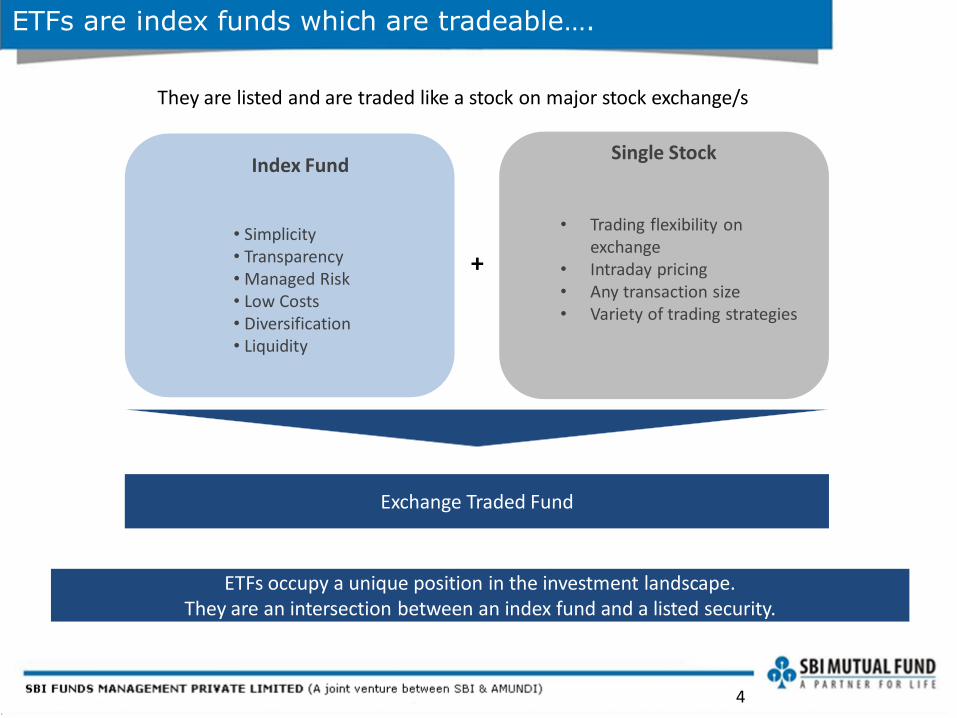

ETFs are index funds which are tradeable….

They are listed and are traded like a stock on major stock exchange/s

Single Stock

• Trading flexibility on exchange

• Intraday pricing• Any transaction size• Variety of trading strategies

Index Fund

• Simplicity• Transparency• Managed Risk • Low Costs• Diversification• Liquidity

Exchange Traded Fund

+

ETFs occupy a unique position in the investment landscape.They are an intersection between an index fund and a listed security.

4

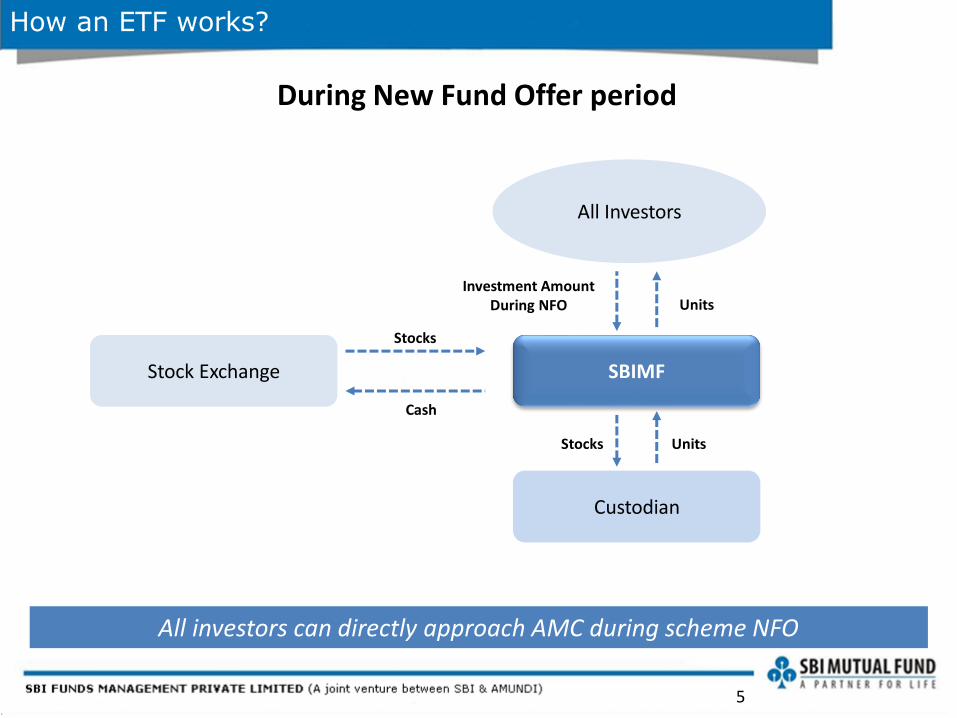

During New Fund Offer period

How an ETF works?

All investors can directly approach AMC during scheme NFO

SBIMFStock Exchange

Custodian

All Investors

Stocks

Cash

Investment Amount During NFO Units

UnitsStocks

5

During Continuous Offer Period

How an ETF works?

Redemption process will be vice versa for both retail and large investors

Large Investors / AP’s (trading in creation unit size)

Retail Investors

SBIMF

Custodian

Units

Units

UnitsStocksStock Exchange

Basket of Index Stocks/

CashCash

UnitsCash

Units

R&T

AP – Authorised ParticipantR&T – Registrar and Transfer Agents

6

Large Investor/

Authorized Participants

FULLY REPLICATED

ETF

Security A

Security B

Security C

Security D

INDEX

Security A

Security B

Security C

Security D

=

Cash/ Portfolio Deposit + Cash

component

Index Returns

(-) Expenses (+) Revenues

How an ETF works? Cont.…

ETFs act as an investment vehicle that endeavors to replicate the index and seeks to deliver returns that closely correspond to that of the index

7

Advantages of ETFs

Transparency • Investors know the ETF holdings, price and costs

Liquidity

• ETFs offer two sources of liquidity:

o Traditional liquidity measured by secondary market trading volume

o Authorized participants boost the liquidity of ETFs

Diversification

• ETFs provide immediate exposure to a basket or group of securities for instant diversification

• Broad range of asset classes including equities, bonds, commodities, investment themes, etc.

Flexibility

• ETFs are listed on exchanges and can be traded at any time the market is open

• Pricing is continuous throughout the day

Cost effectiveness • ETFs offer a cost-effective route to diversified market exposure

8

Why ETFs?

Benefits of ETFs

Return

CostRisk

Returns that closely correspond to that of the underlying index

Risk management as ETFs offer diversification, tradability & transparency

Achieves cost efficiency as compared to other mutual fund schemes

10

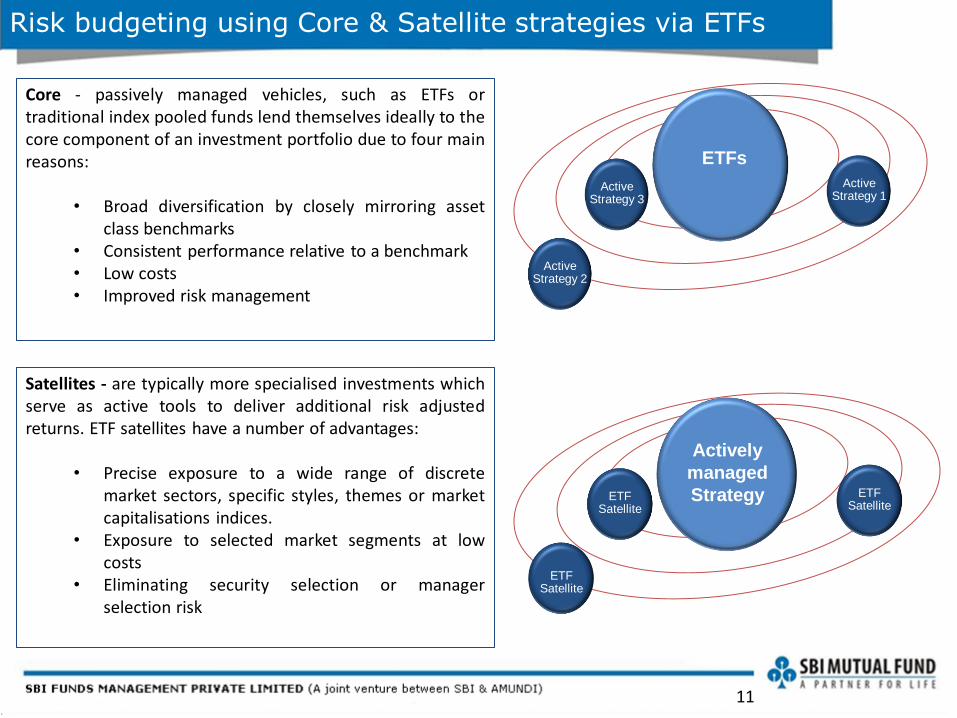

Risk budgeting using Core & Satellite strategies via ETFs

Core - passively managed vehicles, such as ETFs ortraditional index pooled funds lend themselves ideally to thecore component of an investment portfolio due to four mainreasons:

• Broad diversification by closely mirroring assetclass benchmarks

• Consistent performance relative to a benchmark• Low costs• Improved risk management

Active Strategy 2

Active Strategy 3

Active Strategy 1

ETFs

ETF Satellite

ETF Satellite

ETFSatellite

Actively

managed

Strategy

Satellites - are typically more specialised investments whichserve as active tools to deliver additional risk adjustedreturns. ETF satellites have a number of advantages:

• Precise exposure to a wide range of discretemarket sectors, specific styles, themes or marketcapitalisations indices.

• Exposure to selected market segments at lowcosts

• Eliminating security selection or managerselection risk

11

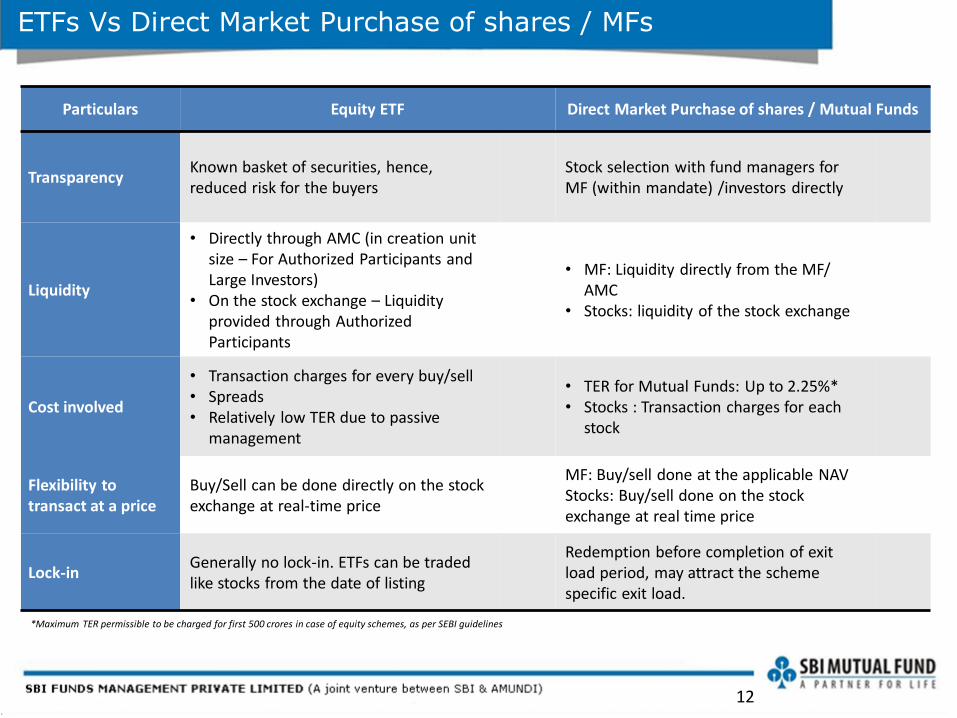

ETFs Vs Direct Market Purchase of shares / MFs

12

Particulars Equity ETF Direct Market Purchase of shares / Mutual Funds

Transparency Known basket of securities, hence, reduced risk for the buyers

Stock selection with fund managers for MF (within mandate) /investors directly

Liquidity

• Directly through AMC (in creation unit size – For Authorized Participants and Large Investors)

• On the stock exchange – Liquidity provided through Authorized Participants

• MF: Liquidity directly from the MF/ AMC

• Stocks: liquidity of the stock exchange

Cost involved

• Transaction charges for every buy/sell• Spreads• Relatively low TER due to passive

management

• TER for Mutual Funds: Up to 2.25%*• Stocks : Transaction charges for each

stock

Flexibility to transact at a price

Buy/Sell can be done directly on the stock exchange at real-time price

MF: Buy/sell done at the applicable NAVStocks: Buy/sell done on the stock exchange at real time price

Lock-inGenerally no lock-in. ETFs can be traded like stocks from the date of listing

Redemption before completion of exit load period, may attract the scheme specific exit load.

*Maximum TER permissible to be charged for first 500 crores in case of equity schemes, as per SEBI guidelines

Sector Review:Information Technology

Evolution of Sector in India

Pre 1995

1995-2000

2000-2005

2005-20152015-2020

• By early 90s, US basedcompanies began tooutsource work on low-cost and skilled talent poolin India

• IT Industry started tomature

• Increased Investment inR&D and infrastructurestarted

• India increasingly seen asa product developmentdestination

• The number of Firms in Indiagrew in size and started offeringcomplex services such asproduct management and go-tomarket strategies

• Western firms set up a numberof captives in India

• Firms in India becamemultinational companies withdelivery centres across the globe.

• Indian IT-BPM revenue was USD146.5 bn in FY15.

• India’s IT sector was at aninflection point, moving fromenterprise servicing to enterprisesolutions.

• India emerging as hub for “DigitalSkills”. The country spent USD 1.6bn annually on training workforcein the sector.

• IT industry is the largest employerwithin private sector.

• India transforming into digitaleconomy with over 450mn plusinternet subscribers, only secondto China.

• The industry increased its costcompetitiveness, with approx. 3-4times cost effective than US.

Source: NICCT, Invest India

14

Sector Highlights

Revenues $ 191 Bn*Growth 7.7%

Exports $ 147 Bn*Growth 8.1%

Domestic $ 44 Bn*Growth 6.5%

Digital Share 26-28%*

Direct Employees* 4.4 Mn

Market Size$191 Bn (2020E)$350 Bn (2025E)

Contributes 8% to India’s GDP

46% share in Total Services exported in 2020

#1 destination in Asia for new Innovation Centres

(2nd Globally)

2nd Fastest growing Data center region in Asia

Pacific

Source: Invest India report (September 2019), NASSCOM *FY2020E NASSCOMMap not to scale. The map has been used for design and representational purpose only, it does not depict the geographical boundaries of the country

Global IT Spend as of

2019 $ 1.5 TrillionGrowth 5.6%

15

54%

23% 23%

47%

22%

8%

7%

3%3%

10%CADM

IMS

Testing

Support & Training

System Integration

IT Consulting

Others

43%

32%

25%

39%

22%

22%

13%2%

1%1%

Drivers for Export of IT services

Source: NASSCOM

16

ExportsFY 2020E $ 147 bn.

IT ServicesGrowing on Digital Momentum

Key drivers for IT Services:• Demand for cloud-native apps, legacy applications

modernization and agile• Telecom demand and 5G roll out• Automation, growth in connected devices, focus on user

experience and demand for information security• Integrating diverse devices and applications across varied

environments – hardware, cloud, etc.• Demand for SaaS services and on premise software

ExportsFY 2020E $ 79 bn.

BPM

ExportsFY 2020E $ 33 bn.

Key drivers for BPM Services:• Transforming from voice-enabled

service to personalized, omni-channel experiences, enabled byincreased adoption ofconversational AI solutions

• Increased demand for cloud-based (SaaS) and predictiveanalytics solutions, rapidadvances in adoption of IoT, AI,deep learning algorithms drivers

Engineering R & D

BPM – Business Process Management, IoT – Internet of Things, AI – Artificial Intelligence,CIS - Customer Interaction, F&A - Finance & Accounting, SaaS – Software as a Service

ExportsFY 2020E $ 31 bn.

Key drivers for ER&D Services:• Technologies like cognitive

computing, microservices,blockchain driving growth.

• Increasing deployments of IoT;edge devices that are smartenabled with analytic capabilities

• Data driven engineering and datamonetization opportunities withaccess to growing volumes ofdata

ExportsFY 2020E $ 31 bn.

ER&D – Engineering Research & Development, PES – Product EngineeringIoT – Internet of Things

CADM – Application Development & Maintenance IMS – Infrastructure Management, SaaS – Software as a Service

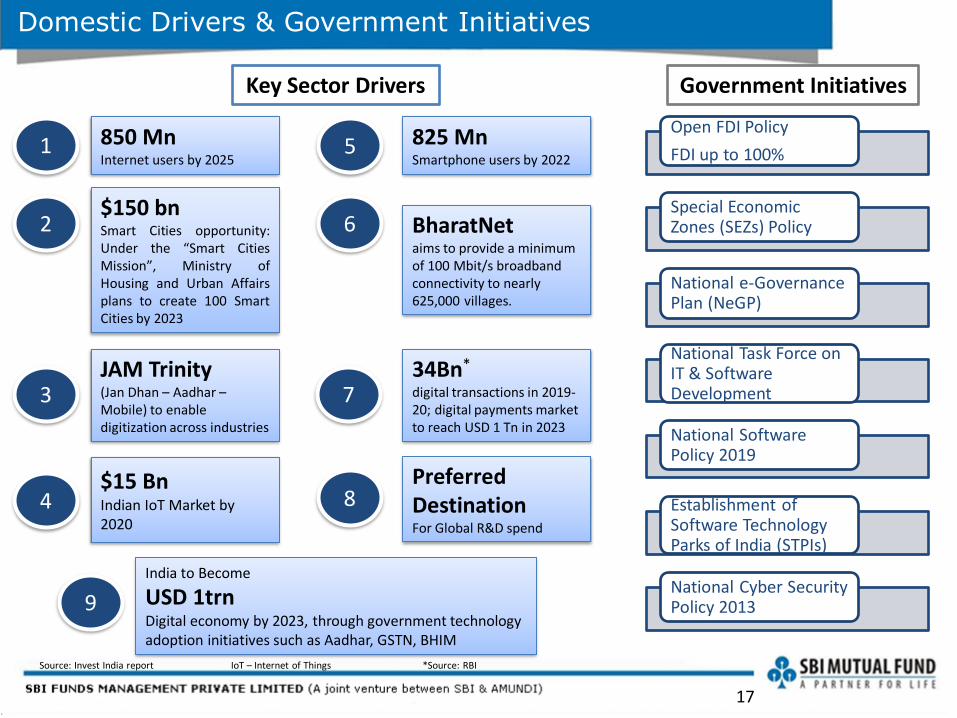

Domestic Drivers & Government Initiatives

Source: Invest India report IoT – Internet of Things *Source: RBI

1 850 MnInternet users by 2025

5 825 MnSmartphone users by 2022

2$150 bnSmart Cities opportunity:Under the “Smart CitiesMission”, Ministry ofHousing and Urban Affairsplans to create 100 SmartCities by 2023

4$15 BnIndian IoT Market by 2020

6 BharatNetaims to provide a minimum of 100 Mbit/s broadband connectivity to nearly 625,000 villages.

3JAM Trinity(Jan Dhan – Aadhar –Mobile) to enable digitization across industries

734Bn*

digital transactions in 2019-20; digital payments market to reach USD 1 Tn in 2023

8

India to Become

USD 1trnDigital economy by 2023, through government technology adoption initiatives such as Aadhar, GSTN, BHIM

9

Preferred DestinationFor Global R&D spend

Key Sector Drivers

Open FDI Policy

FDI up to 100%

Special Economic Zones (SEZs) Policy

National e-Governance Plan (NeGP)

National Task Force on IT & Software Development

National Software Policy 2019

Establishment of Software Technology Parks of India (STPIs)

National Cyber Security Policy 2013

Government Initiatives

17

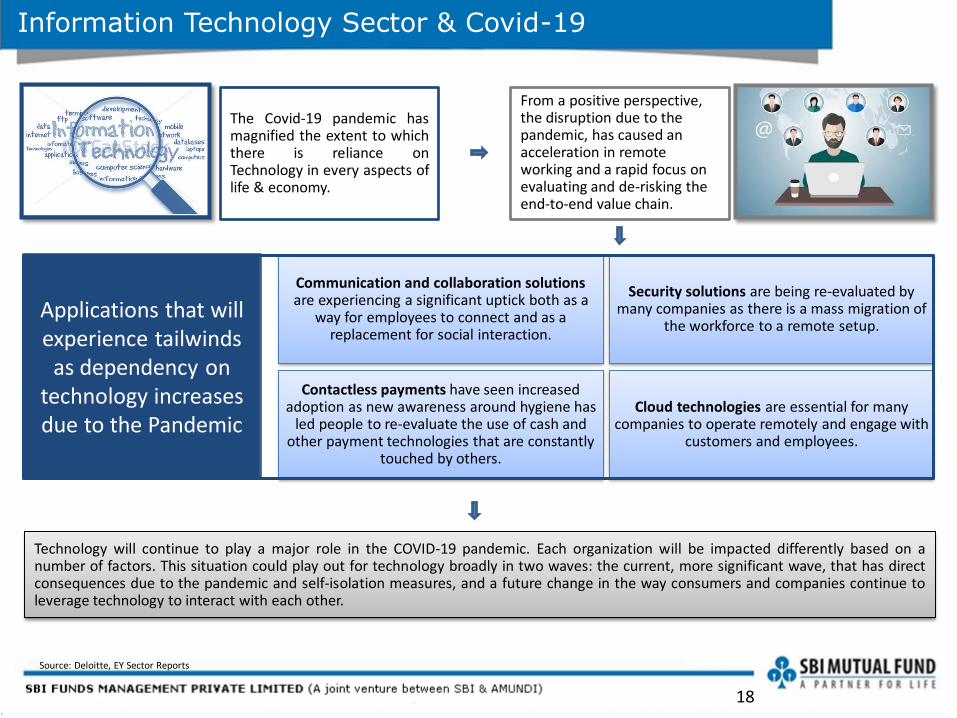

Information Technology Sector & Covid-19

Technology will continue to play a major role in the COVID-19 pandemic. Each organization will be impacted differently based on anumber of factors. This situation could play out for technology broadly in two waves: the current, more significant wave, that has directconsequences due to the pandemic and self-isolation measures, and a future change in the way consumers and companies continue toleverage technology to interact with each other.

The Covid-19 pandemic hasmagnified the extent to whichthere is reliance onTechnology in every aspects oflife & economy.

From a positive perspective, the disruption due to the pandemic, has caused an acceleration in remote working and a rapid focus on evaluating and de-risking the end-to-end value chain.

Communication and collaboration solutionsare experiencing a significant uptick both as a

way for employees to connect and as a replacement for social interaction.

Security solutions are being re-evaluated by many companies as there is a mass migration of

the workforce to a remote setup.

Contactless payments have seen increased adoption as new awareness around hygiene has

led people to re-evaluate the use of cash and other payment technologies that are constantly

touched by others.

Cloud technologies are essential for many companies to operate remotely and engage with

customers and employees.

Applications that will experience tailwinds

as dependency on technology increases due to the Pandemic

18

Source: Deloitte, EY Sector Reports

Key Themes driving the Sector

• Companies across the globe are investing in creation of mobile based platformsfor interaction with their customers, employees, distributors and suppliers.

• This means development of mobile apps for sales, implementation of apps thatenable employees to work remotely and apps for interacting with distributorsand suppliers.

• Websites and desktop applications are not sufficient anymore for engagement.

• Steady decline in prices of smartphones and crash in price of broadband isbringing millions of new Indians into the digital platforms.

• New internet-only companies are disintermediating traditional business modelsand creating value for shareholders.

• Industries like retail, real estate, education, finance and media are someexamples.

• Dramatic fall in cost of hardware and advancement in softwaretechniques over the last decade has enabled companies to developArtificial Intelligence models that can beat humans in several white-collared roles.

• Companies that supply chips and software platform for developmentof these models have a long runway for growth.

• Cloud platforms are the technology equivalent of dairy farms. Dairyfarms own cows, feed them and supply milk to consumers on a perlitre basis. Similarly, Cloud Platforms own and maintain data serversand applications.

• Their corporate customers use these assets and pay them on a per usebasis. It helps companies cut their cost.

Key Themes to drive the Technology Industry

Cloud Platforms

Enterprise Mobility

Increase in Internet

Adoption

Artificial Intelligence

19

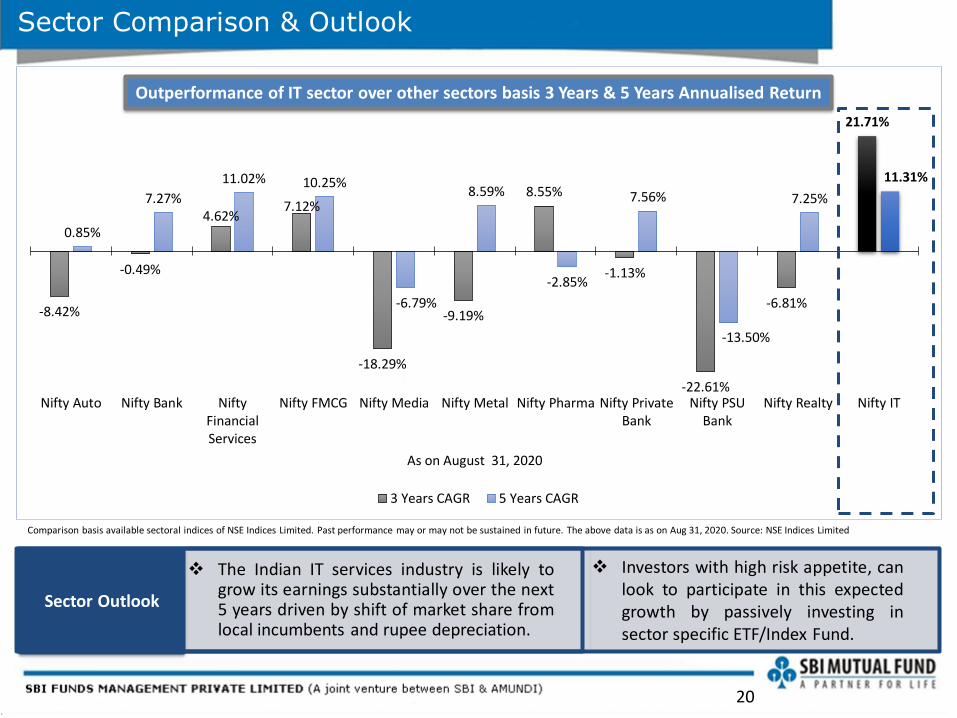

Sector Comparison & Outlook

❖ The Indian IT services industry is likely togrow its earnings substantially over the next5 years driven by shift of market share fromlocal incumbents and rupee depreciation.

Sector Outlook

-8.42%

-0.49%

4.62%7.12%

-18.29%

-9.19%

8.55%

-1.13%

-22.61%

-6.81%

21.71%

0.85%

7.27%

11.02% 10.25%

-6.79%

8.59%

-2.85%

7.56%

-13.50%

7.25%

11.31%

Nifty Auto Nifty Bank NiftyFinancialServices

Nifty FMCG Nifty Media Nifty Metal Nifty Pharma Nifty PrivateBank

Nifty PSUBank

Nifty Realty Nifty IT

As on August 31, 2020

3 Years CAGR 5 Years CAGR

Comparison basis available sectoral indices of NSE Indices Limited. Past performance may or may not be sustained in future. The above data is as on Aug 31, 2020. Source: NSE Indices Limited

20

Outperformance of IT sector over other sectors basis 3 Years & 5 Years Annualised Return

❖ Investors with high risk appetite, canlook to participate in this expectedgrowth by passively investing insector specific ETF/Index Fund.

NFO Start Date:

6th October, 2020

NFO Close Date:

13th October, 2020

Minimum Application

Amount in NFO:

₹ 5000/- & in multiples

of ₹ 1/- thereof

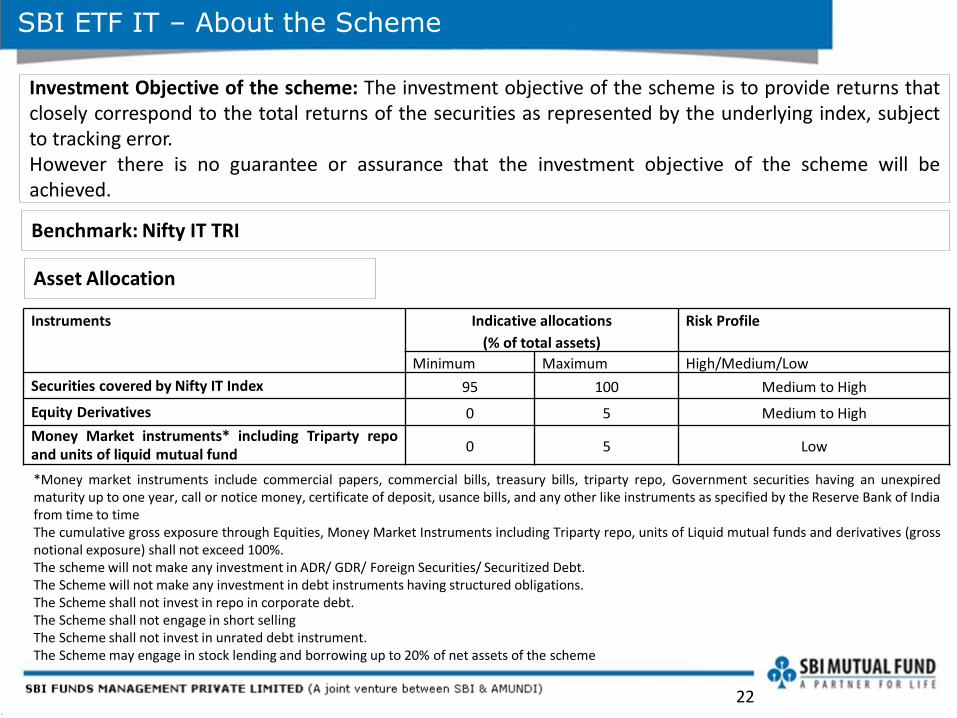

SBI ETF IT – About the Scheme

Investment Objective of the scheme: The investment objective of the scheme is to provide returns thatclosely correspond to the total returns of the securities as represented by the underlying index, subjectto tracking error.However there is no guarantee or assurance that the investment objective of the scheme will beachieved.

Asset Allocation

*Money market instruments include commercial papers, commercial bills, treasury bills, triparty repo, Government securities having an unexpiredmaturity up to one year, call or notice money, certificate of deposit, usance bills, and any other like instruments as specified by the Reserve Bank of Indiafrom time to timeThe cumulative gross exposure through Equities, Money Market Instruments including Triparty repo, units of Liquid mutual funds and derivatives (grossnotional exposure) shall not exceed 100%.The scheme will not make any investment in ADR/ GDR/ Foreign Securities/ Securitized Debt.The Scheme will not make any investment in debt instruments having structured obligations.The Scheme shall not invest in repo in corporate debt.The Scheme shall not engage in short sellingThe Scheme shall not invest in unrated debt instrument.The Scheme may engage in stock lending and borrowing up to 20% of net assets of the scheme

Benchmark: Nifty IT TRI

Instruments Indicative allocations

(% of total assets)

Risk Profile

Minimum Maximum High/Medium/Low

Securities covered by Nifty IT Index 95 100 Medium to High

Equity Derivatives 0 5 Medium to High

Money Market instruments* including Triparty repoand units of liquid mutual fund

0 5 Low

22

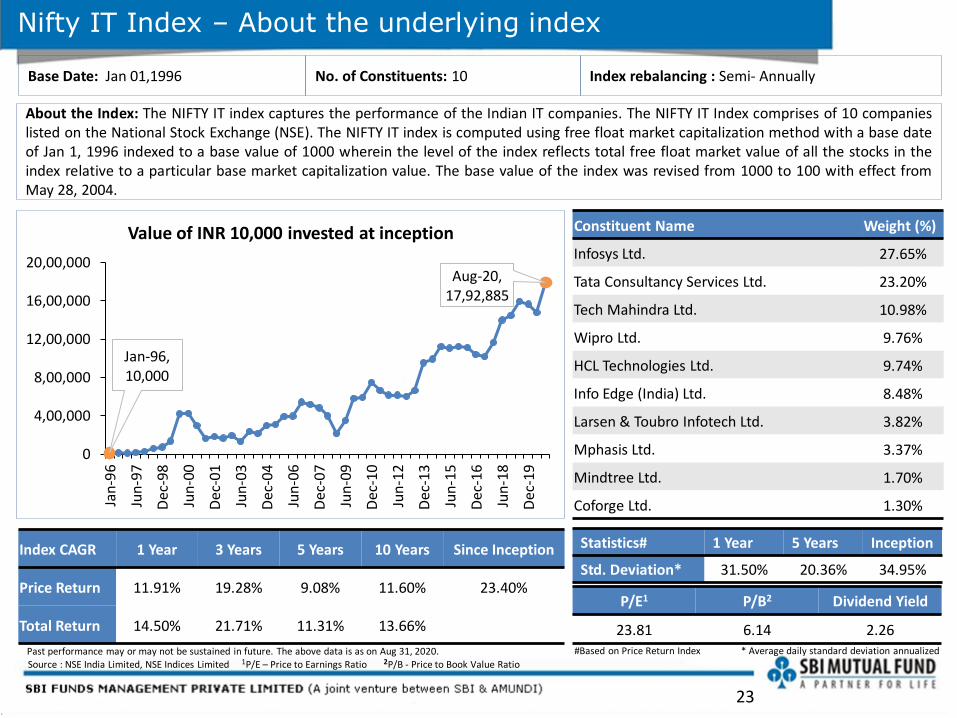

Nifty IT Index – About the underlying index

About the Index: The NIFTY IT index captures the performance of the Indian IT companies. The NIFTY IT Index comprises of 10 companieslisted on the National Stock Exchange (NSE). The NIFTY IT index is computed using free float market capitalization method with a base dateof Jan 1, 1996 indexed to a base value of 1000 wherein the level of the index reflects total free float market value of all the stocks in theindex relative to a particular base market capitalization value. The base value of the index was revised from 1000 to 100 with effect fromMay 28, 2004.

Base Date: Jan 01,1996 No. of Constituents: 10 Index rebalancing : Semi- Annually

Past performance may or may not be sustained in future. The above data is as on Aug 31, 2020.

Index CAGR 1 Year 3 Years 5 Years 10 Years Since Inception

Price Return 11.91% 19.28% 9.08% 11.60% 23.40%

Total Return 14.50% 21.71% 11.31% 13.66%

Constituent Name Weight (%)

Infosys Ltd. 27.65%

Tata Consultancy Services Ltd. 23.20%

Tech Mahindra Ltd. 10.98%

Wipro Ltd. 9.76%

HCL Technologies Ltd. 9.74%

Info Edge (India) Ltd. 8.48%

Larsen & Toubro Infotech Ltd. 3.82%

Mphasis Ltd. 3.37%

Mindtree Ltd. 1.70%

Coforge Ltd. 1.30%

P/E1 P/B2 Dividend Yield

23.81 6.14 2.26

Statistics# 1 Year 5 Years Inception

Std. Deviation* 31.50% 20.36% 34.95%

#Based on Price Return Index * Average daily standard deviation annualized

Source : NSE India Limited, NSE Indices Limited 1P/E – Price to Earnings Ratio 2P/B - Price to Book Value Ratio

Jan-96, 10,000

Aug-20, 17,92,885

0

4,00,000

8,00,000

12,00,000

16,00,000

20,00,000

Jan

-96

Jun

-97

Dec

-98

Jun

-00

Dec

-01

Jun

-03

Dec

-04

Jun

-06

Dec

-07

Jun

-09

Dec

-10

Jun

-12

Dec

-13

Jun

-15

Dec

-16

Jun

-18

Dec

-19

Value of INR 10,000 invested at inception

23

Nifty IT Index – About the underlying index

Internal Analysis basis Price Return Index Values sourced from NSE Indices. Past performance may or may not be sustained in future. The above data is as on Aug 31, 2020.

Calendar Year Wise Returns

Year Abs. Returns

2011 -18%

2012 -2%

2013 58%

2014 18%

2015 0%

2016 -7%

2017 12%

2018 24%

2019 8%

2020* 15%

Year Abs. Returns

2001 -38%

2002 4%

2003 23%

2004 25%

2005 33%

2006 39%

2007 -11%

2008 -55%

2009 166%

2010 29%*Implies YTD as on August 31, 2020

24

SBI ETF IT – Creation unit size

Portfolio ofNifty IT Index Stocks

CashComponent

SBI ETF IT Creation Unit4,000Units

25

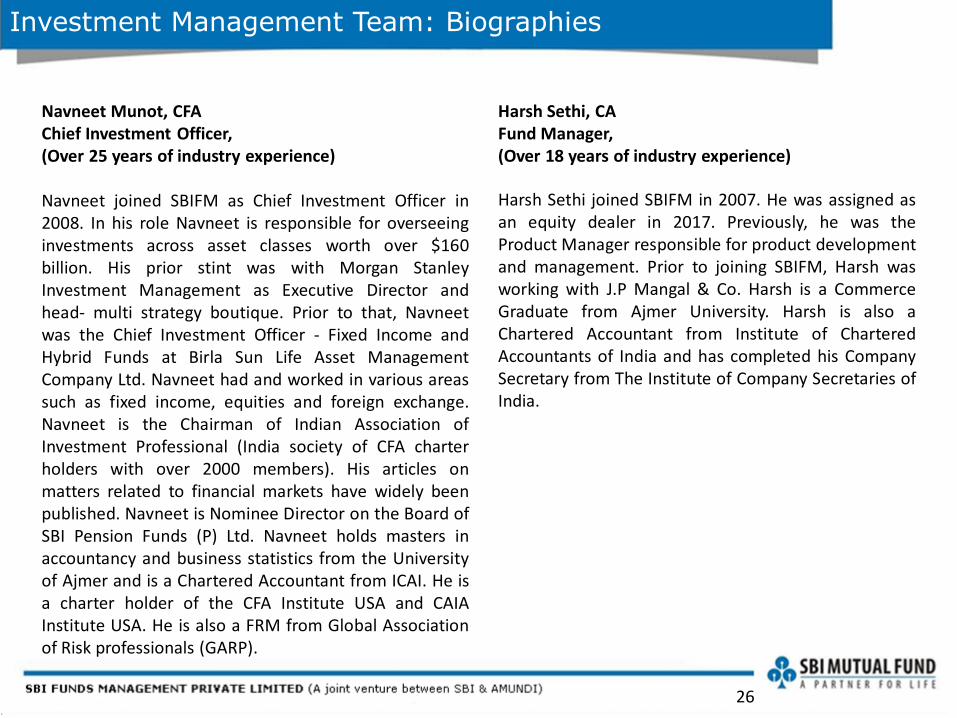

Harsh Sethi, CA Fund Manager,(Over 18 years of industry experience)

Harsh Sethi joined SBIFM in 2007. He was assigned asan equity dealer in 2017. Previously, he was theProduct Manager responsible for product developmentand management. Prior to joining SBIFM, Harsh wasworking with J.P Mangal & Co. Harsh is a CommerceGraduate from Ajmer University. Harsh is also aChartered Accountant from Institute of CharteredAccountants of India and has completed his CompanySecretary from The Institute of Company Secretaries ofIndia.

Investment Management Team: Biographies

Navneet Munot, CFA Chief Investment Officer,(Over 25 years of industry experience)

Navneet joined SBIFM as Chief Investment Officer in2008. In his role Navneet is responsible for overseeinginvestments across asset classes worth over $160billion. His prior stint was with Morgan StanleyInvestment Management as Executive Director andhead- multi strategy boutique. Prior to that, Navneetwas the Chief Investment Officer - Fixed Income andHybrid Funds at Birla Sun Life Asset ManagementCompany Ltd. Navneet had and worked in various areassuch as fixed income, equities and foreign exchange.Navneet is the Chairman of Indian Association ofInvestment Professional (India society of CFA charterholders with over 2000 members). His articles onmatters related to financial markets have widely beenpublished. Navneet is Nominee Director on the Board ofSBI Pension Funds (P) Ltd. Navneet holds masters inaccountancy and business statistics from the Universityof Ajmer and is a Chartered Accountant from ICAI. He isa charter holder of the CFA Institute USA and CAIAInstitute USA. He is also a FRM from Global Associationof Risk professionals (GARP).

26

27

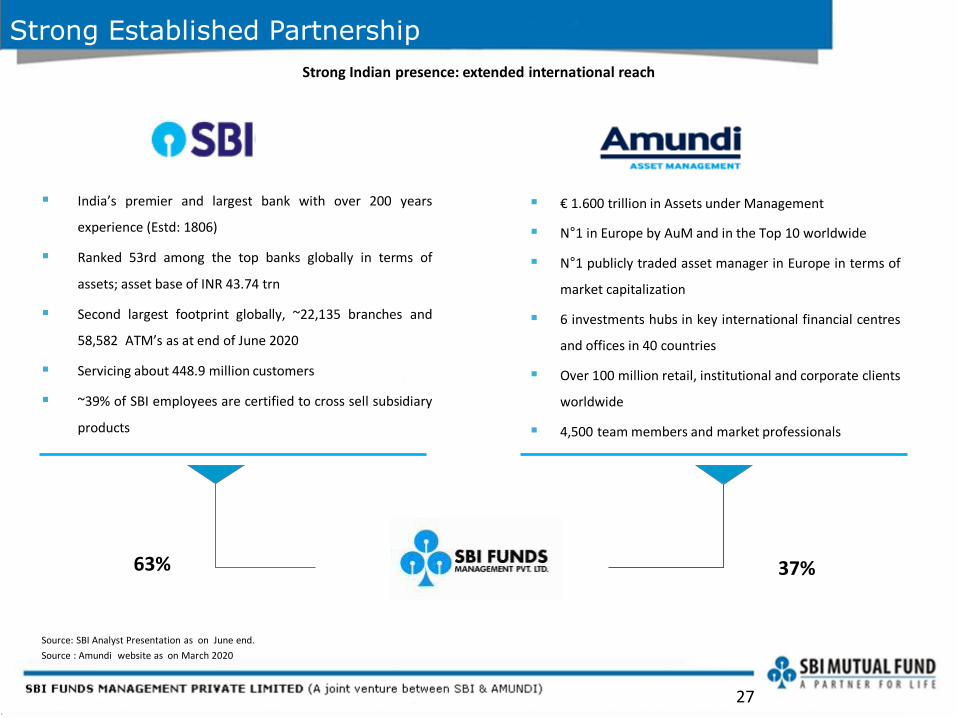

Strong Established Partnership

Strong Indian presence: extended international reach

Source: SBI Analyst Presentation as on June end.

Source : Amundi website as on March 2020

63% 37%

▪ India’s premier and largest bank with over 200 years

experience (Estd: 1806)

▪ Ranked 53rd among the top banks globally in terms of

assets; asset base of INR 43.74 trn

▪ Second largest footprint globally, ~22,135 branches and

58,582 ATM’s as at end of June 2020

▪ Servicing about 448.9 million customers

▪ ~39% of SBI employees are certified to cross sell subsidiary

products

▪ € 1.600 trillion in Assets under Management

▪ N°1 in Europe by AuM and in the Top 10 worldwide

▪ N°1 publicly traded asset manager in Europe in terms of

market capitalization

▪ 6 investments hubs in key international financial centres

and offices in 40 countries

▪ Over 100 million retail, institutional and corporate clients

worldwide

▪ 4,500 team members and market professionals

27

28

SBI Funds Management Pvt. Ltd.

Established in 1987: A leading asset manager in India

▪ INR 11.77 Trillion in AuM across mutual funds, segregated managed

accounts, domestic advisory and offshore advisory business

▪ Multiple asset classes ranging from equities and debt, money market to

ETFs and structured funds

▪ Investment team of 58 professionals with strong track record

▪ Broad customer base with ~ 10 million folios related to individual,

corporate and institutional investors

Broad Investor

Base

AUM INR 11.7 Trillion

Wide Distributio

n Network

Experienced Investment

Team

ExtensiveProductRange

Data as on August 31, 2020

28

This presentation is for information purposes only and is not an offer to sell or a solicitation to buy any mutual fund units/securities. Theseviews alone are not sufficient and should not be used for the development or implementation of an investment strategy. It should not beconstrued as investment advice to any party. All opinions and estimates included here constitute our view as of this date and are subject tochange without notice. Neither SBI Funds Management Private Limited, nor any person connected with it, accepts any liability arising fromthe use of this information. The recipient of this material should rely on their investigations and take their own professional advice.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

For complete details, refer Scheme Related Documents available on https://www.sbimf.com/

Disclaimer & Risk Factors

NSE Indices LimitedThe Product(s) are not sponsored, endorsed, sold or promoted by NSE INDICES LIMITED (formerly known as India Index Services &Products Limited ("IISL")). NSE INDICES LIMITED does not make any representation or warranty, express or implied, to the owners of theProduct(s) or any member of the public regarding the advisability of investing in securities generally or in the Product(s) particularly or theability of the product to track general stock market performance in India. The relationship of NSE INDICES LIMITED to the Issuer is only inrespect of the licensing of the Indices and certain trademarks and trade names associated with such Indices which is determined,composed and calculated by NSE INDICES LIMITED without regard to the Issuer or the Product(s). NSE INDICES LIMITED does not have anyobligation to take the needs of the Issuer or the owners of the Product(s) into consideration in determining, composing or calculating. NSEINDICES LIMITED is not responsible for or has participated in the determination of the timing of, prices at, or quantities of the Product(s) tobe issued or in the determination or calculation of the equation by which the Product(s) is to be converted into cash. NSE INDICES LIMITEDhas no obligation or liability in connection with the administration, marketing or trading of the Product(s).NSE INDICES LIMITED do not guarantee the accuracy and/or the completeness of the product or any data included therein and NSEINDICES LIMITED shall have not have any responsibility or liability for any errors, omissions, or interruptions therein. NSE INDICES LIMITEDdoes not make any warranty, express or implied, as to results to be obtained by the Issuer, owners of the product(s), or any other personor entity from the use of the product or any data included therein. NSE INDICES LIMITED makes no express or implied warranties, andexpressly disclaim all warranties of merchantability or fitness for a particular purpose or use with respect to the index or any data includedtherein. Without limiting any of the foregoing, NSE INDICES LIMITED expressly disclaim any and all liability for any claims ,damages orlosses arising out of or related to the Products, including any and all direct, special, punitive, indirect, or consequential damages (includinglost profits), even if notified of the possibility of such damages.An investor, by subscribing or purchasing an interest in the Product(s), will be regarded as having acknowledged, understood and accepted the disclaimer referred to in Clauses above and will be bound by it.

29