sbctac staff reportmeetings.sbcag.org/meetings/sbctac/2013/11 nov/item 4/item 4-tda... · sbctac...

TRANSCRIPT

SBCTAC STAFF REPORT

SUBJECT: Transportation Development Act Triennial Performance Audits

MEETING DATE: November 7, 2013 AGENDA ITEM: 4

STAFF CONTACT: Peter Imhof, Andrew Orfila

RECOMMENDATION:

Recommend that the Board approve the Triennial Performance Audits for FYs 2009/10-2011/12 for Santa Barbara Metropolitan Transit District (SBMTD), Santa Maria Area Transit (SMAT), City of Lompoc Transit (COLT), Santa Ynez Valley Transit (SYVT), City of Guadalupe Transit, Santa Barbara County Transit (Cuyama and Los Alamos), Easy Lift, the Santa Maria Organization of Transportation Helpers (SMOOTH), and SBCAG and authorize submittal to the State Controller.

SUMMARY:

The draft TDA triennial performance audits presented at last month’s meeting have been revised by PMC as necessary and appropriate to address comments received from TTAC, SBCTAC and transit operators. SBCTAC is asked to recommend that the SBCAG Board approve the audits and authorize submittal to the State Controller. The triennial performance audits have also been presented to the North County Subregional Committee and TTAC for recommendation to the SBCAG Board at their meetings earlier this month. Staff will update SBCTAC as to the action taken at these committees’ meetings.

California Public Utilities Code (PUC) Section 99246 requires regional transportation planning agencies (RTPAs) such as SBCAG to conduct performance audits every three years of its activities as well as the activities of the transit operators to which it allocates Transportation Development Act (TDA) funds. SBCAG allocates TDA funds to the Santa Barbara Metropolitan Transit District (MTD), Santa Maria Area Transit (SMAT), City of Lompoc Transit (COLT), Santa Ynez Valley Transit (SYVT), City of Guadalupe Transit, Santa Barbara County Transit (Cuyama and Los Alamos), Easy Lift, and the Santa Maria Organization of Transportation Helpers (SMOOTH). SBCAG contracted with PMC to conduct the TDA triennial performance audits for FYs 2009/10 through 2011/12. PMC reviewed compliance, implementation of prior audit recommendations, and agency functions, and made findings and recommendations. The findings and recommendations from the triennial performance audits of SBCAG and the transit operators are attached.

For the two local transit operators (COLT and SMAT) that do not currently meet required farebox recovery ratios, we will be returning next month with separate items to address Transportation Development Act compliance and allow the Board to consider options for providing temporary relief to avoid potential financial penalties for non-compliance. SBCAG staff has been in conversation with local transit staff and is committed to working together collaboratively to identify long-term solutions to address farebox recovery.

2

DISCUSSION:

Background

California Public Utilities Code (PUC) Section 99246 requires regional transportation planning agencies (RTPAs) such as SBCAG to conduct performance audits every three years of its activities as well as the activities of the transit operators to which it allocates Transportation Development Act (TDA) funds. SBCAG allocates TDA funds to the Santa Barbara Metropolitan Transit District (MTD), Santa Maria Area Transit (SMAT), City of Lompoc Transit (COLT), Santa Ynez Valley Transit (SYVT), City of Guadalupe Transit, Santa Barbara County Transit (Cuyama and Los Alamos), Easy Lift, and the Santa Maria Organization of Transportation Helpers (SMOOTH).

Preparing performance audits not only fulfills SBCAG’s legal requirements, but also provides for an independent, objective, and comprehensive review of the audited agencies. A performance audit evaluates an organization's effectiveness, efficiency, and economy of operation. The TDA audits evaluate compliance with TDA requirements and the status of implementing prior audit recommendations, and provide a review of agency functions. SBCAG’s performance audit describes how well SBCAG is meeting its administrative and planning obligations particularly as it relates to the TDA programs. Transit operator performance audits ensure accountability in the use of public transportation revenue and include calculations of transit service performance indicators. The audits conclude with findings and recommendations for improvement.

In December 2012, SBCAG issued a request for proposals (RFP) to conduct the triennial performance audits for fiscal years (FYs) 2009/10-2011/12. SBCAG formed an evaluation and selection committee of SBCAG and local transit operator staff to review the proposals. After reviewing the three proposals submitted, the committee recommended PMC. In February 2013, the SBCAG Board approved a contract with PMC to conduct the TDA triennial performance audits for FYs 2009/10-2011/12. Shortly thereafter PMC initiated work on the performance audits.

PMC submitted draft audits throughout September 2013. SBCAG and transit operator staff reviewed the drafts and worked with PMC to incorporate necessary changes into the final draft audits. The final triennial performance audits were submitted on October 25, 2013.

SBCTAC Comments

a. TDA Audit Recommendations: Required vs. Best Practice

At the October meeting, TTAC members requested that the audits be revised to distinguish between recommendations that are required and those that are based on best operator practice. This revision has been made in each of the audits within Section VI – Triennial Audit Recommendations. Each recommendation is listed as either a “Compliance Requirement” or an “Auditor Suggestion.”

b. Verify SMAT Ridership

SBCTAC members commented that the service changes implemented by SMAT should have resulted in a ridership increase in fiscal year 2012, rather than a decrease. The response to this comment is shown in Finding #6 on page 47 of the SMAT audit:

One of the major differences of the new transit network is that the routes are bi-directional, requiring less transfers which resulted in an artificial decrease in ridership, hence the increase in the cost per passenger.

3

c. Clarification regarding SMOOTH Service to Tri-Counties Regional Center

In order to address the comment raised regarding the Department of Developmental Services directive for the Tri-Counties Regional Center relative to SMOOTH service, the following caveat was added to Recommendation #2 of the SMOOTH audit on page 27:

Although it has been indicated that an incentive clause is likely difficult to incorporate due to the set pricing structure, the incentive could come into effect as an opportunity to offset any punitive measures assessed on SMOOTH.

d. Penalty for Noncompliance With Required Farebox Recovery Ratio

At the October meeting, SBCTAC members raised questions about compliance with the TDA statute and, in particular, options available and penalties that potentially ensue if a transit operator is not able to meet its farebox ratio required by statute.

SBCAG’s TDA Claims Manual outlines clear guidance for measures that need to be taken when an operator does not meet its farebox recovery ratio. It is allowable under PUC Section 99268.19 for an operator to utilize local funds (such as Measure A) to meet the ratio requirement. If an operator fails to achieve the farebox ratio requirement for two consecutive fiscal years, the operator’s eligibility for TDA funding is reduced by the difference between the required fare revenues and the actual fare revenues for the second fiscal year that the required ratio was not maintained. The table below describes the penalty timeline for noncompliance with the farebox requirements.

Table 1: Penalty Timeline for Noncompliance with Farebox Ratio Requirements

Grace Year (Year 0)

Noncompliance Year (Year 1)

Determination Year (Year 2)

Penalty Year (Year 3)

The first fiscal year for which an operator or transit service claimant does not maintain the required FBRR is the grace year. There is neither any penalty nor any loss of eligibility for TDA funds in this year.

The second fiscal year for which an operator or transit service claimant does not maintain the required FBRR is the noncompliance year. There is no loss of eligibility for TDA funds in this year; however, the future penalty will be based on audited figures from this year.

The fiscal year after the noncompliance year is the Determination Year. There is no loss of eligibility for TDA funds in this year. The audited amount of the difference between the required and actual FBRR as reported in the claimant’s fiscal and compliance audit for the noncompliance year must be determined in this year. In other words, the penalty that will be applied in the following fiscal year (Penalty Year) is calculated during this year (Determination Year) based on the previous year (Noncompliance year) audit.

In the third or penalty year, the operator’s or transit service claimant’s eligibility to receive TDA funds shall be reduced, for one year only, by the amount of the difference between the required fare revenues and the actual fare revenues in the Noncompliance Year. A claimant subject to the penalty in this section shall demonstrate to SBCAG how it will achieve the required ratio during any Penalty Year.

Source: SBCAG TDA Claims Manual & CCR 6633.9

e. Can the fare revenue generated from transit services not funded by TDA be credited towards farebox recovery ratio in the TDA Triennial Performance Audit?

As stated in the triennial performance audit, “stand-alone” transit services (such as the Clean Air Express) that are not funded with TDA are not counted towards the farebox recovery ratio in the TDA Triennial Performance Audit.

4

f. What is the minimum amount of TDA funding required in order for fare revenues to be credited towards farebox recovery ratio in the TDA Triennial Performance Audit?

The Transportation Development Act sets an upper limit of 50%, but does not set a lower limit.

g. Follow-up with transit operator staff prior to North County Subregional Planning Committee Meeting in November

SBCAG staff convened a meeting with SMAT staff and PMC via teleconference on October 21, 2013 to discuss the audit and SMAT comments. SBCAG staff met with COLT staff on October 22, 2013 to discuss the COLT audit recommendations and options for COLT moving forward.

We will be returning next month with separate items to address Transportation Development Act compliance and allow the Board to consider options for providing temporary relief to avoid potential financial penalties for non-compliance. SBCAG staff has been in conversation with local transit staff and is committed to working together collaboratively to identify long-term solutions to address farebox recovery.

TDA Triennial Performance Audits

The complete TDA triennial performance audits, submitted by Derek Wong from PMC on October 25, 2013, are included in Attachment 1, available with the SBCTAC agenda on the SBCAG website. The triennial performance audits address transit operator, SBCAG staff, SBCTAC, and TTAC comments and suggested revisions. The findings and recommendations for each audit are attached in Attachment 2.

Findings for SBCAG

PMC found that SBCAG conducts its management of the TDA program in a competent, professional manner while operating in a complex intergovernmental environment using limited staff resources. Some of SBCAG’s major accomplishments during the three-year audit period related to the adoption of a Strategic Plan, Measure A becoming effective in 2010; availability and use of Proposition 1B CMIA funding for interregional capacity-increasing projects on Highway 101; the continuing annual Unmet Transit Needs Assessment process; implementation of the Breeze 200 and Coastal Express Limited service; assignment of the Clean Air Express service contract to the City of Lompoc in FY 2009-10 and on to City of Santa Maria beginning in July 2010; adoption of the 2011 FTIP and 2010 and 2012 RTIPs; adoption of the Regional Transportation Plan-Sustainable Communities Strategy (which occurred outside of the audit period, but which included adoption of goals, objectives and performance measures, and development of a list of RTP projects during the audit period); and an update of the SBCAG Public Participation Plan to comply with SB 375.

Recommendations for SBCAG

PMC’s recommendations for SBCAG are summarized below. SBCAG responses follow.

1. Ensure process to keep staff and Board of Directors apprised of the [SBCAG] Strategic Plan.

SBCAG Response: Concur with recommendation.

2. Track completion of Short Range Transit Plans.

SBCAG Response: Concur with recommendation.

5

3. Update the Transit Resource Guide

SBCAG Response: Concur with recommendation, following completion of the North County Transit Plan update.

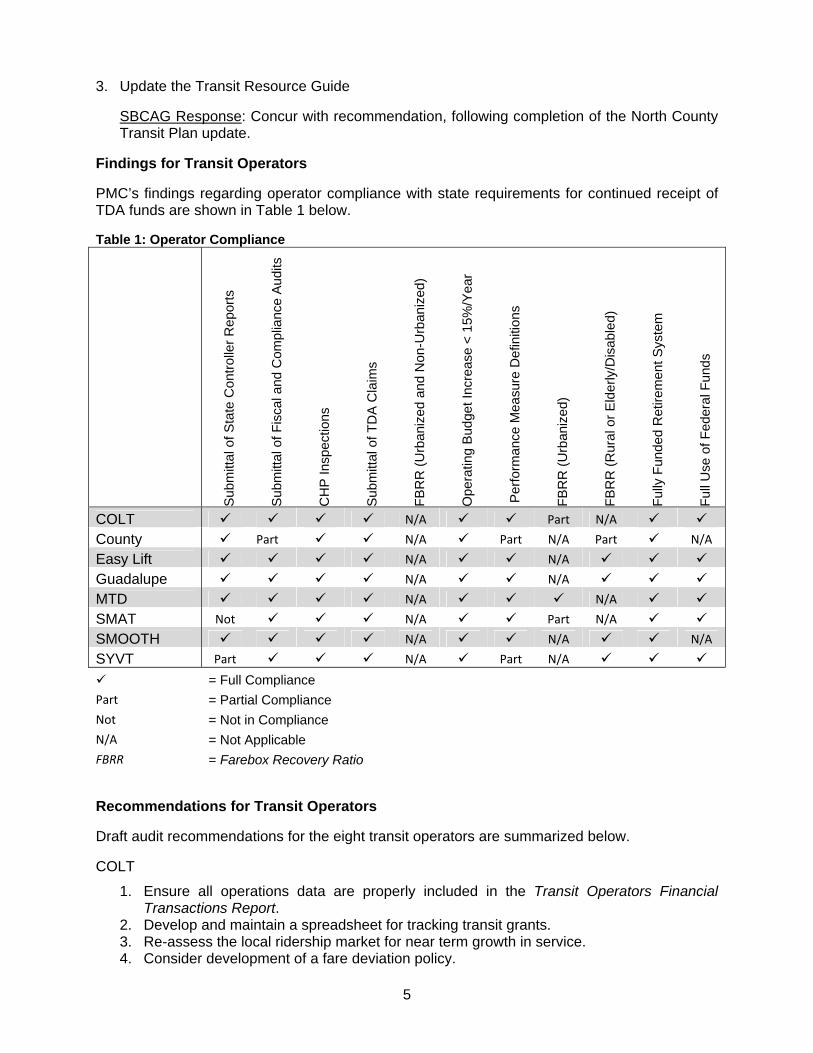

Findings for Transit Operators

PMC’s findings regarding operator compliance with state requirements for continued receipt of TDA funds are shown in Table 1 below.

Table 1: Operator Compliance

Sub

mitt

al o

f Sta

te C

ontr

olle

r R

epor

ts

Sub

mitt

al o

f Fis

cal a

nd C

ompl

ianc

e A

udits

CH

P In

spec

tions

Sub

mitt

al o

f TD

A C

laim

s

FB

RR

(U

rban

ized

and

Non

-Urb

aniz

ed)

Ope

ratin

g B

udge

t Inc

reas

e <

15%

/Yea

r

Per

form

ance

Mea

sure

Def

initi

ons

FB

RR

(U

rban

ized

)

FB

RR

(R

ural

or

Eld

erly

/Dis

able

d)

Ful

ly F

unde

d R

etire

men

t Sys

tem

Ful

l Use

of F

eder

al F

unds

COLT N/A Part N/A County Part N/A Part N/A Part N/A

Easy Lift N/A N/A Guadalupe N/A N/A MTD N/A N/A SMAT Not N/A Part N/A SMOOTH N/A N/A N/A

SYVT Part N/A Part N/A

= Full Compliance

Part = Partial Compliance

Not = Not in Compliance

N/A = Not Applicable

FBRR = Farebox Recovery Ratio

Recommendations for Transit Operators

Draft audit recommendations for the eight transit operators are summarized below.

COLT

1. Ensure all operations data are properly included in the Transit Operators Financial Transactions Report.

2. Develop and maintain a spreadsheet for tracking transit grants. 3. Re-assess the local ridership market for near term growth in service. 4. Consider development of a fare deviation policy.

6

5. Consider further options to address declining ridership and farebox ratio.

County

1. Assure the proper and accurate completion of State Controller Reports. 2. Develop a formalized agreement for the services to be provided by SMOOTH for the

new Cuyama Transit vehicle. (Carryover recommendation from prior audit) 3. Enclose annual CHP terminal inspection report for Cuyama Transit in County TDA

Claim.

Easy Lift

1. Report FTA Section 5310 revenue as capital in the State Controller Report. 2. Develop a technology plan that maximizes existing assets. 3. Complete Strategic Plan Process.

Guadalupe

1. Submit separate State Controller Reports for General Public and Specialized Services. 2. Report correct Full Time Equivalents for demand response service. 3. Closely monitor performance measures of ADA demand response.

MTD

1. Provide documentation of findings of TDA compliance in the annual MTD financial compliance audit. (Carryover recommendation from prior audit)

2. Fulfill strategic goals by advancing technology investment. 3. Complete Short Range Transit Plan Update. 4. Consider alternative bus operator training opportunities when feasible.

SMAT

1. Ensure State Controller Reports are submitted on time. (Carryover recommendation from prior audit)

2. Continue to improve upon the consistent reporting of financial and performance data. 3. Add interactive trip planning capability on SMAT website. 4. Consider options to address declining ridership and farebox ratio. 5. Use actual cost, rather than average cost, and develop cost measures for reporting

service operating costs to Breeze partners. 6. Consider strategies to reduce operating cost of the Breeze service.

SMOOTH

1. Develop a technology plan that maximizes existing assets. 2. Review the contract structure for Tri-Counties Regional Center. 3. Continue pursuit of opportunities to expand SMOOTH’s CTSA role. 4. Develop expanded performance standards for CTSA service efficiency and

effectiveness. SYVT

1. Calculate Full Time Equivalents according to the TDA definition. 2. Continue improvements in submitting the Transit Operators Financial Transactions

Reports to the State Controller within the statutory timeline. 3. Include local Measure “A” funds for SYVT in calculation of farebox recovery.

7

Conclusion

The findings and recommendations from the triennial performance audits are attached. Complete copies of the triennial performance audits are available on the SBCAG website. SBCTAC is asked to recommend that the SBCAG Board approve of the triennial performance audits for their submittal to the State Controller.

ATTACHMENTS:

1. Draft Transportation Development Act Triennial Performance Audits, FYs 2009/10-2011/12 (available via with the TTAC meeting agenda on the SBCAG website, hard copies are available upon request)

2. Draft Audit Findings and Recommendations:

a. SBCAG b. Santa Barbara Metropolitan Transit

District (MTD) c. Santa Maria Area Transit (SMAT) d. City of Lompoc Transit (COLT) e. Santa Ynez Valley Transit (SYVT) f. City of Guadalupe Transit

g. Santa Barbara County Transit (Cuyama and Los Alamos)

h. Easy Lift i. Santa Maria Organization of

Transportation Helpers (SMOOTH)

October 2013

Triennial Performance Audit 50

SBCAG

Section V

Findings

The following material summarizes the major findings obtained from the Triennial Audit

covering fiscal years 2010 through 2012. A set of audit recommendations is then provided.

1. SBCAG conducts its management of the TDA program in a competent, professional manner

while operating in a complex intergovernmental environment.

2. SBCAG retained 20 authorized positions with no significant changes to staffing levels. There

was turnover in some staff positions including in management from retirement of the long-

time Deputy Director for Planning in January 2011, who had served at SBCAG and its

predecessor agency for 34 years. There were three staff departures and three staff hires

over the past three years, including the Deputy Director for Planning and two transportation

planning positions.

3. SBCAG has satisfactorily complied with state legislative mandates for Regional

Transportation Planning Agencies. To its credit, SBCAG meets these mandates using limited

staff resources.

4. Four of the five prior performance audit recommendations have been fully implemented.

One prior recommendation pertaining to creating an SBCTAC agenda item to receive and

present transit performance data has been partially implemented. Staff raised the

possibility of a transit performance data agenda item with SBCTAC and some transit agency

staff asked for time to consider ways to make such an item more useful. Transit

performance data is included in the annual Transit Needs Assessment, which SBCTAC

reviews.

5. A significant achievement by SBCAG during the audit period was a high level review of its

management processes and ability to serve the Santa Barbara region. As a result, SBCAG

completed a Strategic Plan in September 2011 that supports prior efforts including an

organizational assessment conducted in December 2010. The annual Overall Work Program

describes specific work elements that will implement the goals and supporting strategies

articulated by the Strategic Plan in service of SBCAG�s mission.

6. Local Measure A transportation sales tax became effective in April 2010, replacing Measure

D. The first Measure A revenues were received by SBCAG in July 2010. Funds are allocated

to local jurisdictions and public transit operators according to the Investment Plan. The

Measure A Program of Projects for the five-year period covering FYs 2010-11 through 2015-

16 was adopted by the Board in June 2011.

Triennial Performance Audit 51

SBCAG

7. SBCAG prepares the annual Transit Needs Assessment in close consultation with the

SBCTAC, which serves as the statutorily required Social Service Transportation Advisory

Council (SSTAC). The Transit Needs Assessment fulfills the requirement of the TDA unmet

transit needs process and entails an assessment of transit-dependent and transit-

disadvantaged in the county, an evaluation of existing transit providers, public outreach,

and testing of public request for services against reasonableness to meet criteria.

8. The 2040 Regional Transportation Plan & Sustainable Communities Strategy was approved

in August 2013. Although adoption of the final plan was outside the audit period,

development of several key elements of the plan occurred during the audit timeframe. They

included adoption of goals, objectives and performance measures and development of a list

of RTP projects and project evaluation criteria for prioritizing project funding in the plan. In

August 2011, the SBCAG Board adopted a new Public Participation Plan as required by SB

375, laying out a process for public participation in adoption of the Sustainable

Communities Strategy and Regional Transportation Plan.

9. In recognition of the different needs between the north county jurisdictions and their south

county counterparts, and to efficiently address these diverse needs, local project delivery

assistance in the Programming and Project Delivery Division is divided between the north

and south county and assigned to separate staff. However, coverage is provided where

programming staff are cross-trained to handle each other�s responsibilities and provide

program support.

10. In March 2010 and then more recently in 2013, SBCAG updated its document Local

Transportation Fund and State Transit Assistance Fund Claim Manual. The purpose of the

TDA Manual is to clarify the TDA provisions and to serve as a convenient reference

document for TDA claimants and SBCAG in administering the TDA claims process. It also

serves as a technical reference document for stakeholders who are involved with

transportation planning in Santa Barbara County and with the unmet transit needs process.

11. Traffic Solutions set a goal to integrate technology and various tools such as mobile apps,

social media, website, and video into the promotion, awareness and communication of

alternative transportation. In 2011-2012 Traffic Solutions was awarded a federal highway

grant to launch a pilot Real Time Rideshare system in the South Coast as a Transportation

Demand Management tool. Real Time Rideshare uses smartphone technology to match

riders and drivers to facilitate casual carpooling for non-traditional commutes and

transportation trips. Environmental benefits are quantified from Traffic Solution programs

including reductions in auto trips, vehicle miles traveled, gasoline consumption, and

pollutants.

Triennial Performance Audit 52

SBCAG

Recommendations

1. Ensure process to keep staff and Board of Directors apprised of the Strategic Plan.

(Auditor Suggestion)

The strategic plan is a living document providing overarching values and goals and the

framework for SBCAG�s activities. The strategic plan recommended that updates be

undertaken annually by the staff and Board. This is conducted through the annual Overall

Work Program (OWP) and budget preparation. With new Board members that join SBCAG

on a fairly regular basis, staff is reminded of the need to keep all members updated on the

strategic goals. A defined process keeping both staff and the Board apprised of the strategic

plan initiatives should ensure that the goals and implementation strategies continue to

bring perspective to SBCAG work programs. Actions may include ensuring the strategic plan

components are articulated during Board member orientation and meetings, providing

annual updates on the status of meeting strategic plan goals, and setting a timetable for

revisiting each plan component as the agency and its responsibilities evolve in response to

regional and individual members� needs.

2. Track completion of Short Range Transit Plans.

(Auditor Suggestion)

Short Range Transit Plans guiding operations and capital projections are prepared by the

public transit operators on various schedules. With two SRTPs completed during the audit

period, there are three additional sets of SRTPs that will be developed including for Santa

Maria, Guadalupe and MTD. Similar to the tracking of TDA claims and other related

documents, SBCAG should continue to track the progress of each SRTP and ensure their

completion and consistency with the principles and objectives in the new Regional

Transportation Plan & Sustainable Communities Strategy. The program of projects

contained in the SRTPs provides the justification for their inclusion in regional and federal

transportation improvement plans.

3. Update the Transit Resource Guide.

(Auditor Suggestion)

The previous guide was last developed in 2009. Since then, several new and modified transit

services have been implemented along with new system connections. The Transit Resource

Guide should be updated following or concurrently with the update of several other

documents, including the North County Transit Plan, Short Range Transit Plans, and the

coordinated public transit-human services transportation plan. The Transit Resource Guide

should be made available electronically given the prevalence of technology use by the

public. The Traffic Solutions website currently contains links to each transit operator�s

schedules. It is suggested that the updated Transit Resource Guide be inserted within the

same webpage as the transit operator links on the Traffic Solutions website, as well on the

SBCAG publications site.

October 2013

Triennial Performance Audit 43

Santa Barbara Metropolitan Transit District

Section VI

Findings and Recommendations

The following material summarizes the major findings obtained from this triennial audit covering

FYs 2010 through 2012. A set of recommendations is then provided.

Triennial Audit Findings

1. Of the compliance requirements pertaining to MTD, the agency fully complied with all nine

requirements. Two additional compliance requirements did not apply to MTD (e.g.,

intermediate/rural farebox recovery ratios). MTD also fully implemented five of six prior audit

recommendations, with the one being carried forward in this audit.

2. Based on the annual fiscal audits, MTD complied with the farebox recovery ratio and the fare plus

local support ratio. Both ratios were relatively strong compared to the TDA thresholds. MTD

receives significant local support through various revenue sources including local Measure A,

property taxes, subsidies from local governments to buy down fares, and advertising. Local

support for the system has increased due primarily to implementation of Measure A, which

allowed MTD to become a direct recipient of the sales tax revenue.

3. MTD participates in the CHP Transit Operator Compliance Program in which the CHP has

conducted inspections within the 13 months prior to each TDA claim. The CHP inspection reports

submitted for review included minor findings made by the CHP in regard to vehicle condition and

driver records, but rated overall satisfactory.

4. MTD�s transit performance indicators over the past three years reflect a stable system

characterized by a relatively efficient operating cost structure that correlates with decreased

bus service and declines in passenger trips due to economic forces and available revenue.

Total operating costs increased marginally and below the rate of inflation (CPI). MTD froze

employee wage rates and reduced service slightly to offset changes in other expenses such as

diesel fuel prices. Other TDA performance indicators such as operating cost per passenger and

cost per hour increased only slightly for the three-year period. Passengers per hour declined by

a small margin as well.

5. Among the service changes include reduced service hours, elimination of the Carrillo

Commuter Lot Shuttle, the Valley Express intercommunity service from Solvang to Santa

Barbara, and booster service at Santa Barbara Senior and La Cumbre Jr. High Schools.

Additional changes were proposed to other services late in the audit period including to Lines

1, 2, 6, 11, 23 and 25. MTD held community meetings before the schedule change and

conducted outreach afterward to create greater awareness of the adjustments.

6. MTD engaged in negotiations with the Teamsters Union for a new contract to replace the one

that expired in June 2010. New contracts with both bargaining units were effective from July 1,

2010 through June 30, 2012 under different operating conditions from the past contract. An

Triennial Performance Audit 44

Santa Barbara Metropolitan Transit District

agreement in the contract was no wage scale increases that have significant helped the agency

control operating costs. As a result, a positive outcome was that there were no layoffs in spite

of reductions in transit services.

7. A decreasing trend in the number of complaints and commendations reflect to some degree

the decline in service hours and passenger trips. Improved customer service to address the

service changes and passenger awareness also helped to alleviate passenger behavior. The

performance measure of compliments per million passengers decreased by 59 percent, while

complaints per million passengers decreased by 45 percent. In May 2011, MTD developed a

complaint and compliment procedure file that outlines the steps for the intake and handling of

customer feedback including clarifying to whom within the agency the complaint is forwarded

for follow up.

8. Maintenance staff indicated that issues with hybrid vehicles have been fixed which have

allowed mechanics to refocus on diesel engines. The number of vehicle breakdowns more than

doubled during the audit period, resulting in a declining trend in the ratio of vehicle miles

between failures. Electric vehicles were one of the main causes of the trends in vehicle

breakdowns due to batteries. MTD separates vehicle breakdowns with and without electric

vehicles to show that the vehicle fleet meets the agency�s goal for miles between failures

when electric vehicles are not included.

9. MTD produces a series of detailed statistical reports that provide snapshots of route

performance. Data is collected through different means including probes of the GFI fareboxes

and analysis by staff. Performance measures such as ridership and related key indicators are

compared to historic data. Monthly data feeds into quarterly and annual statistics.

10. MTD adopted nine performance goals to provide a means to measure the success of meeting

its strategic goals. Systemwide statistics are compared against these nine agency goals in a

standalone Annual Performance Standard report as a gauge of system performance and for

strategic planning purposes. MTD met most performance standards for the three audit years

with exception of the internal goal for farebox recovery, and vehicles miles between

breakdowns with inclusion of electric vehicles.

11. A Transit Talk meeting held in April 2012 focused on schedule and service changes that went

into effect in August of that year. MTD develops an annual Report to the Community

highlighting some of the agency�s accomplishments and outreach efforts for the past fiscal

year. The report is designed with high level graphics to serve as a marketing piece in addition

to providing information to the community.

12. Although outside the audit period, it is worth noting that in November 2012, MTD�s Board of

Directors, working with staff, completed a new Strategic Plan for the agency. The purpose of

the Strategic Plan is to reflect the goals and values of MTD in providing direction on issues and

projects of importance to the Board and the community.

Triennial Performance Audit 45

Santa Barbara Metropolitan Transit District

Triennial Audit Recommendations

1. Provide documentation of findings of TDA compliance in the annual MTD financial compliance

audit.

(Auditor Suggestion)

As a carryover from the prior performance audit, MTD has made effort to implement the

recommendation. MTD is in communication with the auditor conducting MTD�s single audit and

with the triennial performance auditor to arrive at a resolution that is acceptable to all parties.

However, as described in Chapter III, the Compliance Reports prepared by the independent

fiscal auditor document incorrect compliance tasks. MTD�s fiscal auditor provides a

certification of TDA compliance. The recommendation suggests that further effort be made to

include the fiscal auditor�s findings, calculations, and conclusions for each of the 14 compliance

tasks in the compliance report as described in the California Code of Regulations Section 6667

(provided in the Caltrans TDA Statutes and California Code of Regulations). These tasks are

separate from those currently undertaken in the Compliance Reports and should replace the

tasks in those reports.

2. Fulfill strategic goals by advancing technology investment.

(Auditor Suggestion)

The recent MTD Strategic Plan identified four major trends affecting transit service delivery,

one of which is technology. The FY 2011-12 MTD budget called for capital investment in GPS

embedded digital radios, Automatic Vehicle Location (AVL) and estimated time of arrival

technology. This recommendation fully supports MTD�s efforts to continually embrace the use

of transit technology as a significant means of addressing efficiencies and local operating

conditions created by changing economic and demographic dynamics. Capital funding should

be prioritized to ensure technology advancement is attained. It is suggested that technology

investments made by MTD meet at least three outcomes: create efficiencies in service that

help control operations cost; enhance the data collection and planning process; and improve

customer experience through on-board and stationary safety-related devices (e.g., video

cameras) and availability of real time information.

3. Complete Short Range Transit Plan Update.

(Auditor Suggestion)

The MTD SRTP was last approved in May 2005 which covered the five-year period through

2010. During this audit period, work was undertaken for an update although more pressing

priorities inhibited its completion, including transitions of staff work roles and responsibilities,

and agencywide efforts to combat the effects of the economic recession. MTD indicated its

intention to complete the SRTP update that will provide guidance on near and mid-term policy,

service, and financial matters. The principles and actions contained in the recent Strategic Plan

will also play a strong role in the plan�s development.

Triennial Performance Audit 46

Santa Barbara Metropolitan Transit District

4. Consider alternative bus operator training opportunities when feasible.

(Auditor Suggestion)

MTD provides its operators with a good set of training tools that have maintained safety and

reduced risk as measured by various performance indicators. As a dual means to increase

training opportunities and possibly further enhance operating staff morale, it is suggested

MTD consider additional methods of skills testing and development through participation in

competitive events such as bus roadeos. Events include the Southern California Regional Bus

Roadeo, transit association bus roadeos (CalACT/CTA), and the APTA Bus Roadeo.

Alternatively, MTD may also consider developing its own local bus roadeo. Mechanics�

competitions are also staged at roadeos. While budget constraints among other factors have

limited the availability of events and participation of transit agencies, opportunities for

alternative training and showcasing of skills should be considered when feasible in venues that

also promote the image and visibility of the agency.

October 2013

Triennial Performance Audit 46

Santa Maria Area Transit (SMAT)

Section VI

Findings and Recommendations

The following material summarizes the major findings obtained from this triennial audit covering

FYs 2010 through 2012. A set of recommendations is then provided.

Triennial Audit Findings

1. Of the compliance requirements pertaining to Santa Maria Area Transit, the system fully

complied with seven of the nine requirements. Two additional compliance requirements did

not apply to Santa Maria (e.g., rural/intermediate farebox recovery ratios). The City was found

not in compliance with the timely submittal of its State Controller Reports and was in partial

compliance with the attainment of the minimum farebox recovery ratio. The City accounts for

the late submittal due to the City financial close-out procedures required to generate the

financial information required in the Controller�s Report. The City will explore methods with

the goal for timely submission of the State Controller Report.

2. Based on the available data from various sources including the annual financial audits,

National Transit Database, and SMAT Transit Contractor Reports, the farebox recovery ratios

were in partial compliance over the three year period. The systemwide ratio of 20 percent was

not met during the audit period. On a modal basis, the fixed route ratio of 20 percent was met

in FY 2010 only. For ADA Paratransit, the mode�s farebox ratio of 10 percent was met in FY

2011 and using Measure D/A revenues as a supplement allowable by TDA. Provisions in TDA

describe potential penalties for non-compliance with the farebox. However, other remedies

are available at the discretion of SBCAG including lowering the farebox recovery standard.

3. Santa Maria participates in the CHP Transit Operator Compliance Program in which the CHP

has conducted inspections within the 13 months prior to each TDA claim. The CHP inspection

reports submitted for review were found to be satisfactory. First Transit Inc. which took over

operations in 2009 and provides maintenance of the city owned transit vehicles. According to

the CHP, by definition of the California Vehicle Code Section 408, First Transit is the motor

carrier. Prior to First Transit, the previous contractor was not recognized as the motor carrier

given that vehicle maintenance was conducted by a separate vendor.

4. The operating budget did not increase by more than the TDA threshold of 15 percent. The

average annual budgetary increase during the audit period was 3 percent, with the largest

increase in FY 2011 of 7.8 percent.

5. Of the four prior audit recommendations, Santa Maria partially implemented two

recommendations while one was not implemented, and the other was no longer applicable.

The recommendation not implemented was the submission of State Controller Reports for

SMAT within the proper timelines. The recommendation that is no longer applicable relates to

SMAT and social media which is a decision by City leadership outside of the transit program.

Triennial Performance Audit 47

Santa Maria Area Transit (SMAT)

6. SMAT�s transit indicators show varied trends including both positive and negative results. For

example, a significant positive trend is the decline in operating cost per vehicle service hour

which is an indicator of cost efficiency. However, in contrast, a negative trend is the increase in

operating cost per passenger which is an indicator of cost effectiveness. One of the major

differences of the new transit network is that the routes are bi-directional requiring less

transfers which resulted in an artificial decrease in ridership, hence the increase in the cost per

passenger. The new network is better for the customer but artificially decreases ridership.

These trends affect other performance measures including passengers per hour, passengers

per mile, and farebox recovery.

7. SMAT implemented significant service adjustments in June 2011 coinciding with the opening

of the new Santa Maria Transit Center. The service changes were guided by the 2010 Short

Range Transit Plan and were designed to decrease the need for passenger transfers among

buses, thus the expected decline in ridership. The adjustments have improved service delivery

but also show a decline in ridership characterized by fewer transfers. Aside from the expected

ridership drop in FY 2012, operating costs for the local fixed route increased relatively steadily

in spite of growth in certain costs such as for fuel. Any reduction in ridership due to service

adjustments that eliminate the need to transfer reflects a service enhancement rather than a

service degradation. Although indicators based on ridership may suggest the latter, ridership

patterns typically take time to adjust to any significant change in service.

8. Outreach was conducted for the 2011 service changes including a half dozen community

workshops and open houses along with flyers in both English and Spanish. The operations

contractor First Transit assisted the City in the outreach effort. Given the large Hispanic

population in the service area, a significant effort has been made to reach that market.

9. At the beginning audit period, Santa Maria changed contract operators, having selected First

Transit effective July 1, 2009. The contract is for three years plus seven, one-year options (10

years total) that could carry the contract through June 2019. Annual cost increases in the

contract are based on a two-tier system, Tier 1 being a variable mileage rate and Tier 2 being a

fixed management fee. Tier 1 variable rates are similar for the local fixed route and ADA

Paratransit, while the Breeze and Clean Air Express have higher rates. The Tier 2 fixed rate

differs by mode with local fixed route having the highest fee followed by Breeze and then ADA

Paratransit (there is no fixed fee for Clean Air Express). A contract extension for at least the

next two fiscal years through June 2014 was signed in June 2012.

10. City transit management reports that First Transit has been responsive and more numbers-

oriented than the previous contractor. The First Transit General Manager position changed

over in the middle of the audit period, as did a few other management positions.

11. SMAT updated its Short Range Transit Plan (SRTP) in June 2010 that covers a 10-year period

through 2020. The SRTP provides a demographic analysis, an onboard and telephone survey,

and an assessment of existing services at the time the plan was developed and a projected

service plan that identifies specific capital and operations improvements. A major focus of the

SRTP was to revisit the fixed route network and identify modifications to achieve goals.

Triennial Performance Audit 48

Santa Maria Area Transit (SMAT)

12. SMAT maintains an Internet presence through its web site within the Santa Maria home site. In

its current form, the SMAT website lacks the interactive features more commonly available

through other public transit websites that tend to generate web traffic such as a trip planning

tool. Transit management indicated that when the City procures an AVL system with real time

capability, SMAT will be in a better position for on-line trip planning.

13. Transit operators do not use the same methodology to generate operating costs and cost

indicators. The City of Santa Maria accounts for operating cost by service whereas other

operators use an average systemwide hourly cost. The City demonstrated the difference

between the two methods and the incompatibility of conducting a comparison in reporting to

the Breeze funding partners. This inconsistency causes incompatibility issues when comparing

operating costs and cost indicators between operators. Failure to include actual costs leads to

a number of accounting inaccuracies and inaccurate financial reporting to the funding

partners.

Triennial Performance Audit 49

Santa Maria Area Transit (SMAT)

Triennial Audit Recommendations

1. Ensure State Controller Transit Operators Financial Transactions Reports are submitted on

time.

(Compliance Requirement)

This recommendation is carried over from the prior audit. The City submits separate reports

for its fixed-route (general public service) and demand response (specialized service)

operations. Pursuant to the Public Utilities Code, Section 99243, the City is required to submit

the reports to SBCAG and the State Controller within 90 days following the end of the fiscal

year (110 days for electronic filing). It is suggested that the Transit Services Manager and staff

work closely with the City Treasurer to design a schedule to complete, review, and submit the

State Controller Reports within the statutory timelines. A copy of the completed annual report

should also be transmitted to SBCAG as required by statute.

2. Continue to improve upon the consistent reporting of financial and performance data.

(Auditor Suggestion)

This recommendation is carried over from the prior audit and is prompted for full

implementation due to discrepancies found in the operational data elements contained in the

contractor reports and reports to external agencies. The Transit Manager cited changes in data

between the original NTD data and the NTD close out report due to additional scrutiny

provided by the FTA for the close out report. The original NTD data compares better to the

State Controller Report as both have not undergone the additional level of review. Other data

discrepancies include scheduled hours for Breeze service and reported hours by the

contractor. Transit management should cross check the figures at the time of the original

submissions and conduct more extensive review and trend analysis of monthly and quarterly

reports submitted by the contractor for discrepancies. Data by transit service and mode should

be checked for consistency as well as between contractor reports and reports provided to

partner agencies.

3. Add interactive trip planning capability on SMAT website.

(Auditor Suggestion)

As described earlier, the SMAT website which is under the domain of the City of Santa Maria

currently does not have the interactive features more commonly available by public transit

websites. These interactive tools such as trip planning through Google Transit tend to generate

web traffic. Transit management indicated that when the City procures an AVL system with

real time capability, SMAT will be in a better position for on-line trip planning. Follow up with

such an on-line tool, among other customer friendly amenities, would enhance the SMAT

website and potentially increase transit awareness and ridership. This recommendation could

also be considered in a larger context of a regional trip planning tool.

Triennial Performance Audit 50

Santa Maria Area Transit (SMAT)

4. Consider options to address declining ridership and farebox ratio.

(Auditor Suggestion)

SMAT staff should work with SBCAG staff to identify and discuss options for SMAT to address

declining local fixed route ridership and farebox ratio trends. The audit describes several issues

that should be discussed including potential penalties for non-compliance with farebox and

other remedies such as lowering the farebox recovery standard. City transit staff should

ensure that eligible methods to reduce operating costs such as capital cost of contracting and

service exemptions are included in audited financial statements in a timely manner and follow

TDA procedures. SMAT should also consider recommendations in the Short Range Transit Plan

update. SMAT has retained a consultant to review its local fixed route service. Other

operational and service options should be considered by SMAT and SBCAG as part of the North

County Transit Plan update.

5. Use actual cost, rather than average cost, and develop cost measures for reporting service

operating costs to Breeze partners.

(Auditor Suggestion)

Recommendations regarding the Breeze service have considered the input and review of the

audit by SBCAG. To ensure accurate cost information is provided to funding partners of the

Breeze service (City of Lompoc and the County), actual operating costs paid to the contractor

should be used for financial reports. Actual expenditures are necessary for financial planning

and projections, including amounts needed from each partner for capital replacement and

future operations. Cost metrics that accurately depict the service should also be developed

that are reflective of the payment to the contractor combined with performance of the

system. External reports should be amended as necessary to use the same cost metrics (e.g.,

cost per hour, cost per passenger, subsidy per passenger, farebox recovery) to allow direct

comparison and reduce potential for discrepancies in cost accounting.

6. Consider strategies to reduce operating cost of the Breeze service.

(Auditor Suggestion)

Trends for the cost of operating the Breeze service have increased dramatically over the last

several years. Over the last five fiscal years (FYs 2007-08 through 2011-12) the operating cost

rose from $117 per hour (as reported in the previous TDA audit) to approximately $191 per

hour, a 63 percent increase. The City should consider strategies for achieving cost savings

including soliciting cost proposals for operating the Breeze service from service providers, or

negotiating rates with the current provider.

October 2013

Triennial Performance Audit 35

City of Lompoc Transit (COLT)

Section VI

Findings and Recommendations

The following material summarizes the major findings obtained from this triennial audit covering

FYs 2010 through 2012. A set of recommendations is then provided.

Triennial Audit Findings

1. Of the compliance requirements pertaining to COLT, the operator fully complied with eight

of the nine applicable requirements. The operator was in partial compliance with regard to

the farebox recovery ratio, having partially met the modal farebox standard. Two

additional compliance requirements did not apply to COLT (e.g., intermediate and farebox

recovery ratios).

2. Pursuant to SBCAG requirements, COLT is held to a temporary farebox recovery standard

of 15 percent on a systemwide basis as an urban operator. Based on audited data, the

systemwide farebox recovery ratios for COLT were below the standard for the triennial

period. The FY 2010 farebox recovery ratio excludes the Clean Air Express commuter

service that was administered by Lompoc because it is not TDA funded. On a modal basis,

fixed-route is held to a 15 percent farebox recovery standard and Dial-a-Ride is held to a 10

percent standard. The respective standards were met for fixed route in FY 2011 and for

Dial-a-Ride in FY 2010 and FY 2012.

3. Through its contract operators, first AmericanStar Transportation and then Storer

Transportation Service, Lompoc participates in the CHP Transit Operator Compliance

Program and received vehicle inspections within the 13 months prior to each TDA claim.

Satisfactory ratings were made for all inspections conducted during the audit period.

4. The operating budget fluctuated significantly throughout the audit period. The FY 2010

budget increased 33.8 percent due to the City�s administration of the Clean Air Express.

The budget then decreased 24.7 percent the following year due to a change to a new

contract operator through a bid process and the relinquishing of the Clean Air Express

operation, resulting in lower cost. There was a slight decrease in FY 2012 of 0.2 percent.

5. Lompoc implemented the four prior audit recommendations which pertained to recording

actual fare revenues for each mode, conducting performance review and analysis on route

by route level, updating the SRTP and reporting Wine Country Express performance data

under the fixed-route mode.

6. Operating costs systemwide increased only 0.9 percent over the triennial period based on

audited data from the FY 2009 base year through FY 2012. The cost growth trends compare

well in relation to the Consumer Price Index (CPI). Using unaudited data derived from the

National Transit Database, fixed route operating costs decreased by 9.7 percent whereas

Dial-a-Ride operating costs decreased 35.6 percent. The largest increase in systemwide

Triennial Performance Audit 36

City of Lompoc Transit (COLT)

operating costs occurred between FYs 2010 and 2011 due to increases in transit labor costs

for the last year of the previous contractor. The new contractor has since lowered

operating costs.

7. Based upon contract operator data, systemwide ridership decreased 23 percent during the

audit period. Fixed route ridership decreased 22.5 percent and Dial-a-Ride ridership

decreased 27.8 percent. Ridership experienced the highest decrease in numbers during FYs

2010 and 2012, primarily on the fixed-route when the routes were modified. Systemwide

ridership declined from 207,380 in FY 2011 to 180,837 in FY 2012, a 12.8 percent decrease.

Further, Dial-a-Ride ridership decreased 22.1 percent in FY 2012. The decrease in ridership

is attributed to several occurrences, including fewer students using the transit system due

to the closure and consolidation of school campuses, and the elimination or realignment of

some local routes to gain efficiencies in meeting farebox recovery.

8. The provision of revenue hours and miles exhibited decreases systemwide and for both

modes during the audit period. Fixed route revenue hours and miles decreased 27.5 and

17.7 percent, respectively while DAR revenue hours and miles decreased 22.3 and 7.7

percent, respectively. Systemwide, vehicle service hours decreased 26.2 percent and

vehicle service miles decreased 16.2 percent.

9. Cost efficiency and effectiveness indicators showed negative trends from the service over

the past few years. Although operating cost increased only marginally, performance trends

for operating cost per passenger and per vehicle hour were unfavorable given that

ridership and vehicle hours declined.

10. The system underwent a change in contract operators. A single Request for Proposals (RFP)

was released in conjunction with Santa Ynez Valley Transit (SYVT) to receive bids for a new

service contract. Storer Transit Systems was selected and began operating COLT in July

2011 under a five-year contract (with two 1-year extensions).

11. The City initiated the process to develop an update of its Short-Range Transit Plan (SRTP) in

2011. The City Council accepted the draft SRTP in June 2011 and approved the first year

recommendations. They included the elimination of Route 2A and reduction of one

weekday hour in the evening from all routes. Route 1 was also realigned to serve Valley

Medical Center and the Wine Ghetto.

12. The 2012 COLT Short Range Financial Plan (SRFP) was commissioned and adopted in

October 2012. The SRFP was prepared using excerpts and recommendations from the draft

2011 SRTP and primarily focuses on farebox attainment strategies. A recommendation to

raise fares was denied by the City Council.

13. Grant funding allocated towards supporting transit services have been derived from local,

state and federal sources. The FTA Triennial Review conducted in 2012 found that the City

did not have on file records of all FTA-funded assets with the required FTA information.

Triennial Performance Audit 37

City of Lompoc Transit (COLT)

This could have an effect on the budgeting and tracking of local match requirements and

use of non-federal dollars.

Triennial Audit Recommendations

1. Ensure all operations data are properly included in the Transit Operators Financial

Transactions Report.

(Compliance Requirement)

Full Time Equivalents (FTEs) are required to be reported in the annual Transit Operators

Financial Transactions Report submitted to the State Controller. The State Controller Reports

compiled for COLT�s fixed route and dial-a-ride had omitted FTE data for a few of the audit

years. FTEs should include personnel hours from the contract operator and City personnel

responsible for monitoring the operating contract and preparing the State Controller Report. It

is suggested that time dedicated to the transit system be tracked as reasonably as possible and

tabulated properly since it feeds into the State Controller Reports. Operations data contained

in the State Controller Report should be reviewed by City transit management for accuracy and

completeness prior to submittal to the State by the Lompoc Finance Department. Proper

reporting of FTEs as well as all other required operations data will result in more accurate

performance indicators of productivity and responsiveness to the State.

2. Develop and maintain a spreadsheet for tracking transit grants.

(Auditor Suggestion)

The FTA Triennial Review conducted in 2012 found that the City did not have on file records of

all FTA-funded assets with the required FTA information including description, ID number,

acquisition date, cost, federal percentage, grant number, location, and vesting. This is also

inclusive of best practices procedures that ensure the proper tracking of grant awards. It is

suggested that City transit management and the Finance Department work closely to design

and utilize a spreadsheet tracking grants awarded toward the procurement, construction and

maintenance of transit assets and property. The tracking tool should also be used for the

budgeting and tracking of local match requirements and use of non-federal dollars.

3. Re-assess the local ridership market for near term growth in service.

(Auditor Suggestion)

Ridership declines have adversely impacted the farebox recovery returns for the transit

system. While the local school district has reduced school campuses, there is also reduced

school bus service which could provide opportunities for COLT. Although City transit

management indicated students have preferred to walk to school and that general local

conditions are difficult for the transit system, the City should take steps to re-assess local

ridership opportunities including students and other rider needs in the service area. Recent

new economic developments in the transit service area have increased some potential for

additional riders which should be monitored. Targeted marketing efforts could be focused on

these groups from the assessment. The next update to the SRTP could further study how COLT

Triennial Performance Audit 38

City of Lompoc Transit (COLT)

service can be designed to increase efficient service for student travel and new trip attraction

locations.

4. Consider development of a fare deviation policy.

(Auditor Suggestion)

A fare deviation policy is suggested to identify any variance of fare revenue between expected

fares and actual revenue collections. Expected fare revenue is based on ridership figures and

the type of fares paid. The policy, when implemented in regular intervals such as monthly or

quarterly, would provide information to the contractor and City transit management of any

revenue difference between expected and actual fares after the revenue is counted. The policy

would also assist in identifying when actual fare revenues fall outside of a specific range set by

the City such as beyond a 10 percent difference. As farebox recovery is a performance

standard for COLT, and given that the new contractor counts actual fares by service, the policy

will further strengthen the fare revenue reconciliation process developed by Lompoc and the

new contract operator. Implementation could be a simple data spreadsheet formula that

determines the difference between expected and actual fare revenue. A further step would be

a second formula that highlights or provides notification when the actual counted fare revenue

falls outside an expected range. It is suggested that this practice be continuous at a minimum

until automated fareboxes are installed on the buses.

5. Consider further options to address declining ridership and farebox ratio.

(Auditor Suggestion)

COLT staff should work with SBCAG staff to identify and discuss options for COLT to address

declining ridership and farebox ratio trends. As COLT�s farebox standard is already reduced to

15 percent, TDA does not allow further reductions or relaxing of the farebox ratio

requirements below 15 percent. The City has been, and continues, to implement system

changes in an effort to meet the required fair box recovery requirements. This includes

working with SBCAG on a temporary reduced farebox requirement, and working with the

County on using local support rather than TDA funds to pay for a portion of the services COLT

provides to the County. The City Council also has authorized the use of Measure A (local

support) funds to meet minimum farebox recovery requirements.

Failure to meet minimum farebox ratios results in certain penalties. As was discussed earlier,

Lompoc�s eligibility to receive TDA support could be reduced during a subsequent penalty year

by the amount of the difference between the required fare revenues and the actual fare

revenues for the fiscal year that the required ratio was not maintained. Lompoc would have to

demonstrate to SBCAG how it would achieve the required ratio of fare revenues during any

penalty year. These trends require examining operational changes that would increase overall

farebox by increasing ridership and/or fares or reducing costs. Other operational and service

options should be considered by COLT and SBCAG as part of the North County Transit Plan

update.

Triennial Performance Audit

Santa Ynez Valley Transit

October 2013

Triennial Performance Audit 31

Santa Ynez Valley Transit

Section VI

Findings and Recommendations

The following summarizes the major findings obtained from this Triennial Audit covering fiscal

years 2010 through 2012. A set of recommendations is then provided.

Triennial Audit Findings

1. Of the compliance requirements pertaining to SYVT, the operator fully complied with seven

out of the nine applicable requirements. The operator was in partial compliance with regard

to the timely submittal of its Transit Operator Financial Transactions Reports to the State

Controller and meeting the definitions of performance measures (e.g. FTEs). The City of

Solvang Finance Director at that time unexpectedly went out on medical leave and was

absent during most of FYs 2010-11 and 2011-12. Two additional compliance requirements

did not apply to SYVT (e.g., intermediate farebox recovery ratio under PUC 99270.1 and

urbanized farebox recovery ratio).

2. Pursuant to SBCAG requirements, SYVT is held to a 10 percent farebox standard either on a

systemwide basis or on a modal basis as a rural operator. Based on audited data, the farebox

recovery ratios for SYVT were 10.60 percent in FY 2010; 12.31 percent in FY 2011; and 11.24

percent in FY 2012. The average farebox ratio during the period was 11.38 percent. On a

modal basis, both fixed-route and Dial-a-Ride farebox recovery ratios exceeded the 10

percent standard during FY 2011 and FY 2012.

3. The Solvang City Council approved a reduction in the Dial-a-Ride fare from $2.25 to $1.75

that went into effect July 1, 2011. Local Measure A revenues are applied toward subsidizing

Dial-a-Ride fares. In addition, General Public Dial-a-Ride service was implemented on Sunday

in July 2011.

4. Through its contract operators, first AmericanStar Transportation and then Storer

Transportation Service, SYVT participates in the CHP Transit Operator Compliance Program

and received vehicle inspections within the 13 months prior to each TDA claim. Satisfactory

ratings were made for all inspections conducted during the audit period.

5. The operating budget exhibited modest fluctuations throughout the audit period. There were

decreases in FY 2010 and FY 2012 of 6.3 and 7.4 percent, respectively. For FY 2011, the

operating budget increased 7.7 percent to account for the last year of the contract for the

prior operator and transition to the new contractor.

6. SYVT implemented the two prior audit recommendations which pertained to recording actual

fare revenues for each mode and using a consistent allocation method for operating costs

between State Controller Report and internal SYVT system management reports.

Triennial Performance Audit 32

Santa Ynez Valley Transit

7. Operating costs systemwide increased 6.8 percent over the audit period, with fixed route

costs increasing by 5.4 percent and Dial-a-Ride by 13 percent. The growth in operating costs

slightly outpaced the increase in the regional Consumer Price Index (CPI). It is noted that the

change in contract operators in July 2011 resulted in a methodology change on how

operating cost by mode are derived. Whereas the prior contractor allocated costs based on

ridership, the new contractor allocates cost based on revenue hours.

8. Ridership increased 19.9 percent systemwide during the audit period. Ridership experienced

the highest increase in numbers during FY 2011 on the fixed-route, growing by 7,700

passengers in one year. In addition, Dial-a-Ride ridership increased 27.6 percent in FY 2012.

Increased usage by seniors, students and hospitality industry service workers is responsible

for the positive ridership trends.

9. Performance measures were mainly positive and reflect a fairly stable service. Systemwide

operating cost per passenger decreased 11 percent while passengers per vehicle service hour

increased 16 percent over the three period. Operating cost per hour increased only 3.3

percent systemwide for the audit period.

10. The system underwent a change in contract operators. A single Request for Proposals (RFP)

was released in conjunction with the City of Lompoc to receive bids for a new service

contract. Modesto-based Storer Transit Systems was selected and began operating SYVT in

July 2011 under a five-year contract (with two 1-year extensions).

11. With the implementation of StrataGen dispatching and scheduling software in conjunction

with Storer becoming the contract operator, SYVT has been able to accommodate more Dial-

a-Ride trips. The StrataGen dispatching software is configured to accept same-day

reservations and allows for open return reservations for passengers with medical

appointments.

12. The SYVT Short-Range Transit Plan (SRTP) was updated and adopted in September 2012.

Some of the findings contained in the 2012 SRTP include an emphasis on attracting �choice

riders�, targeting marketing efforts toward the region�s tourism industry, the need for

schedule adherence during peak commute hours, and maximizing the use of technology such

as GPS and the StraGen scheduling software.

13. SYVT conducted a bus stop survey as part of the SRTP and used the findings to make service

modifications and bus stop improvements. Some of the bus stops were converted to on-call

stops while fourteen new bus shelters were constructed with solar lighting. Also, routing

through the community of Los Olivos was streamlined and one full trip was eliminated in

order to attain schedule adherence.

14. On-time performance shows the fixed route buses tend to run late beginning midday. This is

attributed to increased afternoon traffic in Solvang and increased demand at on-call stops at

Triennial Performance Audit 33

Santa Ynez Valley Transit

the casino and Tribal clinic, compounded by the �tightness� of the current operating

timetable. The SRTP has made recommendations to improve on-time performance.

Triennial Performance Audit 34

Santa Ynez Valley Transit

Triennial Audit Recommendations

1. Calculate Full Time Equivalents according to the TDA definition.

(Compliance Requirement)

Full Time Equivalents (FTEs) are required to be reported in the annual Transit Operators

Financial Transactions Report submitted to the State Controller. The State Controller Reports

compiled for SYVT�s fixed route and dial-a-ride during the audit period do not properly

calculate FTEs, or the data is missing. For example, FTE data for Dial-a-Ride was missing for FY

2010 and was underreported in FY 2012. Also, FTEs for fixed-route in FY 2012 appear to

represent headcount rather than the formula of dividing total annual employee hours by

2,000.

Employee hours should include those from the contract operator and City personnel

responsible for monitoring the operating contract and preparing the State Controller Report.

It is suggested that time dedicated to the transit system be tracked as reasonably as possible

and tabulated properly since it feeds into the State Controller Reports. Operations data

contained in the State Controller Report should be reviewed by SYVT transit management for

accuracy and completeness prior to submittal to the State by the Solvang Finance

Department. Proper reporting of FTEs will result in more accurate performance indicators of

productivity and responsiveness to the State.

2. Continue improvements in submitting the Transit Operators Financial Transactions Reports

to the State Controller within the statutory timeline.

(Compliance Requirement)

The FY 2010 Transit Operator Financial Transactions Reports for both fixed route and dial-a-

ride were submitted to the State Controller beyond the statutory deadline. However, the two

subsequent reports in FYs 2011 and 2012 were submitted on time. Public Utilities Code

Section 99243 requires the reports to be filed 90 days after the close of the transit operator's

fiscal year (110 days for electronic filing). The purpose of the statewide report is to collect

specific financial related and statistical data information about public transit operations for

use by the State Legislature, transportation planners, and the public. The performance

auditor recognizes the improvement in timing of the reports by SYVT/Solvang and

encourages this trend to continue.

3. Include local Measure �A� Funds for SYVT in calculation of farebox recovery.

(Auditor Suggestion)

With reduced fares for seniors and disabled beginning in March 2012, the actual fare revenue

per passenger is lower which has an impact on farebox recovery. This reduction is

supplemented by Measure �A� funding that can be included along with fare revenues in the

farebox recovery ratio. The local measure funding should be included in the calculation of

farebox recovery in such reports as the annual financial audit and the State Controller

Triennial Performance Audit 35

Santa Ynez Valley Transit

Report. By including the measure revenue, the farebox is made whole in consideration of the

reduced fares.

October 2013

Triennial Performance Audit 32

City of Guadalupe Transit

Section VI

Findings and Recommendations

The following material summarizes the major findings obtained from this triennial audit covering

FYs 2010 through 2012. A set of recommendations is then provided.

Triennial Audit Findings

1. Of the compliance requirements pertaining to the City of Guadalupe, the City fully complied

with each of the nine requirements. Two additional compliance requirements did not apply to

Guadalupe (e.g., intermediate and urban farebox recovery ratios). Although the Full Time

Equivalents (FTE) figures contained in the annual State Controller Reports for ADA demand

response are not accurately reflected, the correct FTEs are calculated by SMOOTH in internal

documents provided for this audit. The correct FTEs should be included in the State Controller

Reports.

2. The City�s farebox recovery ratio remained well above the required 10 percent. There was a

fare increase in August 2008 (prior to the audit period) that has helped to increase the farebox

the last several years. The fare increase was intended to offset rising fuel prices and the

additional hours of service to extend the Flyer by an additional hour in the evening on

weekdays. The average systemwide farebox recovery ratio was 30.85 percent during the

triennial period.

3. Guadalupe participates in the CHP Transit Operator Compliance Program through the

contractor in which the CHP has conducted inspections at SMOOTH�s facility within the 13

months prior to each TDA claim. The CHP inspection reports submitted for review were found

to be satisfactory.

4. Five of the six prior audit recommendations were fully implemented. One recommendation

not implemented involved having the City to submit separate State Controller Reports for fixed

route and ADA services.

5. Guadalupe�s transit indicators reflect trends that have developed due to various forces

including impacts from a prior fare increase, increases in operations costs, and continued

economic strains. In spite of a fare increase, ridership remains relatively strong characterized

by the local demographics of Guadalupe. With several efficiency and effectiveness measures

trending downward, transit management should continue to monitor performance and

consider potential adjustments if warranted. The current high farebox recovery ratios provide

the City with a degree of assurance for the continued receipt of TDA funds.

6. Efforts to increase public awareness of ADA services available to eligible residents has been

successful. However, increased trip demand on the ADA demand response service should be

monitored due to its relatively higher cost of providing the service on a per passenger and per

Triennial Performance Audit 33

City of Guadalupe Transit

hour basis. Detailed assessment of ADA applications should continue as well as considerations

of opportunities for transitioning ADA riders onto fixed route when possible.

7. Review of performance figures for fixed route and demand response indicates very consistent

data among different State and federal transit reports. There are very minor discrepancies in

the performance data, generally between internal reports and reports submitted to external

agencies. Compared to the prior audit period, significant improvements have been made to

overall data consistency.

8. Guadalupe Transit has benefited from continued high ridership levels and is viewed as an

essential service to the residents of the city. Although ridership patterns show a leveling of

growth for the Flyer and Shuttle services during the three-year period, it remains relatively

stable. The drivers assigned to the Guadalupe bus routes have long tenure with the transit

system and are very familiar with the area and the passengers.

9. Small adjustments were made to the Guadalupe Flyer during the audit period. The route was

changed to start and end at the new Santa Maria Transit Center. Within the City, some bus

stops were either eliminated to enable the bus to travel on a straighter route, relocated to

more ideal spots along the route, or reconfigured. The result of these improvements was a

decrease in travel time for the Flyer route of about six minutes which is positive for

passengers.