sba your way - whitepaper th

TRANSCRIPT

THE SBA LENDING PARTNER

How Your Lending Institution Can Take Advantage

of SBA Lending

www.banc-serv.com

SBAWAY

your™

OVERVIEWEntrepreneurs and small business owners are vital to the strength of the U.S. economy. There are almost 28

million small businesses in the US, with over 50% of the working population employed with a small business.

Roughly 60% of debt financing to small businesses is through the help of lending institutions. Most small

businesses rely on conventional lending, personal lending, and outside equity investments for financing options.

One underutilized financing option for small businesses comes through lending programs established by the

Small Business Administration (SBA). SBA loan programs provide an excellent option for access to capital when

additional funding is not available through conventional lending methods. The proceeds from these loans can be

used for many business purposes, provided the small business meets certain eligibility requirements.

The SBA offers a variety of programs structured under 7(a) guidelines to banks, credit unions, and other

specialized lenders. This paper examines the reasons for including an SBA lending program as part of your

institution’s commercial loan portfolio. This paper assesses:

• 3 Biggest Myths of SBA Lending

• Challenges of SBA Lending

• Benefits of SBA Lending

• Finding the Right Partner to Handle SBA Lending

THE SBA LENDING PARTNER

The Small Business Administration (SBA) off ers numerous programs

that provide small businesses with an opportunity to start, manage,

and grow. Despite the tremendous boost SBA loans provide for a

small business, there are still many misconceptions that exist regard-

ing these government guaranteed programs.

3 MYTHS OF SBA LENDING

THE SBA LENDING PARTNER

The SBA is an avenue for lending institutions to extend capital to those

borowwers who are not strong enough to meet the institutions credit policy.

It is a resource and tool for those who are generally missing a small piece of

the eligibility puzzle, a piece that would have allowed them an opportunity to

receive a conventional loan otherwise. Whether it is a lower than average credit

score, a lack of full collateral, or less than perfect cash flow, the SBA can provide

assistance in troubled areas through a set of specially developed guidelines and

regulations. Understanding SBA guidelines, compliance, and regulation comes

with many years of training and dedication to the SBA process.

Borrowers with poor history (i.e., credit) can easily get a loan

3 BIGGEST MYTHS OF SBA LENDING

MYTH 1

THE SBA LENDING PARTNER

Cumbersome and Timely

3 BIGGEST MYTHS OF SBA LENDING

MYTH 2

Many of the SBA loan programs were traditionally associated with lengthy and complex

processing, making them a last resort option for borrowers. Though old perceptions still linger,

the SBA has developed significant changes. Over the years, the SBA has made substantial strides

by reducing redundancy, centralizing itself for consistency, and adding a staff of well trained

individuals. Many of the implemented efficiencies include streamlined forms, revised application

documents and regulations, and internally aligned protocol. Still, nothing plays a more important

role in change than the input and feedback from lenders and borrowers across the country.

THE SBA LENDING PARTNER

More Fees, Less ProfitBorrowers and lenders alike, more often than not, hesitate to travel down the SBA

path due to a misconceived notion that SBA loans are always more expensive for the

borrower and less profitable for the lender. In some cases, that scenario can be true.

However, that is not always the case. Cost of funds, pricing, and loan structure all play a

vital role in determining costs for all involved parties. It is important for lenders to work

through a full cost analysis before making a decision to move forward with an SBA loan.

In certain cases, borrowers can actually save money by rolling fees into the SBA loan.

Additionally, institutions can earn tremendous and immediate profit from selling

guaranteed portfions of SBA loans on the secondary market. Again, each loan is unique

and has its own set of possibilities. Because of this, it is always important to ask an

expert and work through your own analysis.

3 BIGGEST MYTHS OF SBA LENDING

MYTH 3

THE SBA LENDING PARTNER

CHALLENGES OFSBA LENDING

Many lending institutions shy away from taking advantage of the

SBA due to misconceptions. Typically, hesitation stems from an

unfamiliarity with the loan process or from a lack of knowledge

or experience with its programs. Understanding the basic fl ow

of an SBA loan can be a highly important step in taking on such

loans yourself. The following are the biggest challenges to take

into consideration when moving forward with an institution’s SBA

lending program:

• Expertise

• Effi ciency

• Due Diligence

THE SBA LENDING PARTNER

Expertise SBA Guidelines (SOP)

Lenders must have full working knowledge of the SBA’s Standard Operating

Procedures, otherwise known as the SOP. In an ever changing environment,

understanding the SOP guidelines will arm lenders with the expertise needed to

process quality loans more efficiently.

Business and Borrower Eligibility

There are many programs available through the SBA, most of which can help lenders

create a loan that is beneficial for both the borrower and lender. Loan parameters

and borrower requirements vary from program to program. Again, understanding the

SOP will help provide guidance on what is best for your borrower.

Loan Programs and Parameters

It is highly important for lenders to understand each loan program. Not only will

placing the loan within the right program benefit the borrower, it will also provide

your lending institution with the security it requires to ensure your loans reamain in

compliance and your guarantees stay intact.

CHALLENGES OF SBA LENDING

THE SBA LENDING PARTNER

Due DiligenceAn SBA loan is not complete simply becuase it was approved. Nurturing an SBA

loan through maturity is vital to maintaining the loan’s guarantee. It is important to

continually target and analyze items such as personal and business financials; tax

payment verification; life and commercial insurance verification; and debt service

analysis. Though those aren’t the only items to follow up on, they are a great place to

start.

EfficiencyDocumentation

A guarantee is one of the biggest benefits provided by an SBA loan. With the

ability to reduce risk comes the responsibility to document the loan and its process

correctly. It is not enough to simply move a loan through to the final approval stage.

Proper care and documentation should be taken every step of the way—from credit

analysis, packaging, closing, and selling to servicing, reporting, liquidation, and

annual due dillegence.

BENEFITS OF SBA LENDING

Despite the challenges involved with the SBA lending process, there is

tremendous profi tability and growth potential for a lending institution

who chooses to take advantage of SBA progrmas. An institution’s

objectives should ensure that assets are protected (soundness), that

a reasonable return on investment is provided to its shareholders

(profi tability), and that the needs of its community are continually

met (growth). When a lending institution chooses to proceed with

any endeavor, these key business drivers—soundness, profi tability,

and growth—must meet or exceed expectations. The following are the

biggest benefi ts to consider when building an SBA lending platform:

• Reduce Risk

• Increase Growth

• Increase Profi tability

THE SBA LENDING PARTNER

Reduce RiskThe SBA, depending on the program, provides a specific

guarantee on each individual loan, anywhere from 50% to 90%.

This reduced risk provides lenders with additional comfort when

moving forward with loans that otherwise wouldn’t have been

approved through conventional lending. Not only is the reduction

of risk important for the overall health of the institution, it also

allows lenders an opportunity to help support more borrowers in

their community.

BENEFITS OF SBA LENDING

THE SBA LENDING PARTNER

Each loan guaranteedanywhere from

50-90%

Increase GrowthDepending on your governing regulatory authority, a lending institution may

have the ability to record the full loan amount on their balance sheet or just the

unguaranteed portion. With capital requirements such an integral part of an

institution’s lending flexibility, this capability allows institutions the room they

need to increase their loan portfolio and provide additional long-term assistance

to their borrowers.

BENEFITS OF SBA LENDING

THE SBA LENDING PARTNER

The secondary market is one of the most underutilized areas in

the SBA loan process. Though not always the best route, selling

the guaranteed portion of a loan on the secondary market can

be a highly benefi cial profi t center for certain institutions. With

recently recorded premiums as high as 118, there has never been

a better time for lenders to consider taking advantage of reduced

exposure and increased liquidity.

Increase Profi tability (Interest & Secondary Market)

BENEFITS OF SBA LENDING

THE SBA LENDING PARTNER

118Recorded Premiums as High as

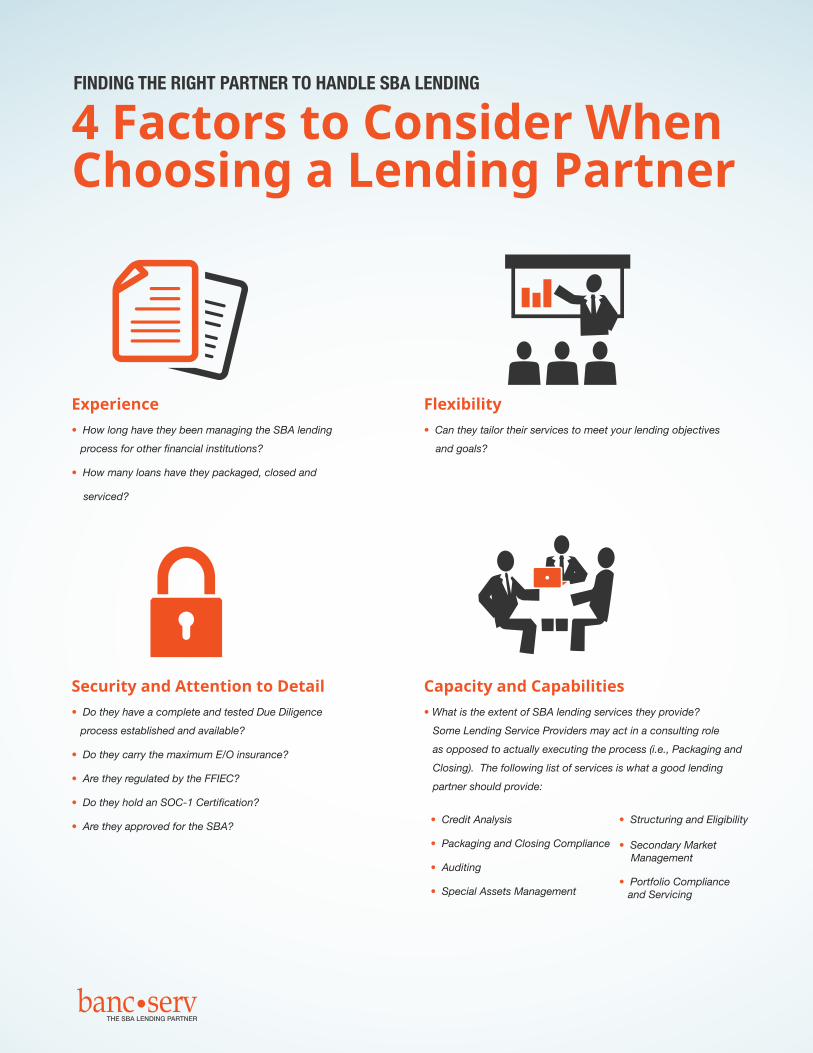

FINDING THE RIGHT PARTNER TO HANDLE SBA LENDING

Finding the right partner to handle your SBA loans can be a

challenging and time consuming eff ort. It is important to fi nd

a lender service provider that can provide your institution with

expertise and effi ciency in every aspect of the SBA lending process.

There are four main factors you should take into consideration when

choosing a lender service provider to handle your SBA portfolio:

• Experience

• Flexibility

• Security and Attention to Detail

• Capacity and Capabilities

THE SBA LENDING PARTNER

Experience• How long have they been managing the SBA lending process for other financial institutions?

• How many loans have they packaged, closed and

serviced?

Flexibility • Can they tailor their services to meet your lending objectives and goals?

Security and Attention to Detail• Do they have a complete and tested Due Diligence process established and available?

• Do they carry the maximum E/O insurance?

• Are they regulated by the FFIEC?

• Do they hold an SOC-1 Certification?

• Are they approved for the SBA?

Capacity and Capabilities• What is the extent of SBA lending services they provide? Some Lending Service Providers may act in a consulting role as opposed to actually executing the process (i.e., Packaging and Closing). The following list of services is what a good lending partner should provide:

FINDING THE RIGHT PARTNER TO HANDLE SBA LENDING

THE SBA LENDING PARTNER

4 Factors to Consider WhenChoosing a Lending Partner

• Credit Analysis

• Packaging and Closing Compliance

• Auditing

• Special Assets Management

• Structuring and Eligibility

• Secondary Market Management

• Portfolio Compliance and Servicing

SUMMARY

ABOUT BANC-SERVbanc-serv can become your SBA back office, instantly providing your institution with the expertise needed

to complete all aspects of the lending process. We have the ability to handle any path a loan may take. Any

particular model that we develop can be customized to your specific needs. Our experience and expertise enable

us to understand how to best move a loan through the SBA process as efficiently as possible.

Make the SBA your way today. Call 866-423-9503.banc-serv PARTNERS LLC | 777 E Main St, Westfield, IN 46074

“The SBA Lending Partner” may be a bold statement, but it is something that we can proudly back up. In

business as a Lender Service Provider (LSP) for over 14 years, banc-serv boasts an in-house staff of 40+

employees that work with 300+ institutions nationwide.

As we continue to grow and develop, we always seek to make the SBA program understandable, accessible, and

profitable because we have a passion for lending institutions and small businesses alike.

SBA lending programs can be a viable option for any lending institution and are underutilized financing options

for small businesses who need access to additional funding. Even though there are challenges involved with

the SBA lending process, there is tremendous profitability and growth potential for a lending institution who

chooses to take advantage of SBA programs. Whether an institution chooses to handle SBA lending internally

or outsource to an SBA lender service provider, it is vital to have expertise and efficiency in every aspect of the

process. Ensuring a lender service provider has experience, security, and flexibility will increase its probability of

adding greater volume and profitability to its current lending portfolio.

THE SBA LENDING PARTNER

© 2016 banc-serv PARTNERS LLC. All rights reserved.

Tucker HerringExecutive Vice President - National Sales Managero: [email protected]