savings goals and saving behavior from a...

TRANSCRIPT

129Journal of Financial Counseling and Planning Volume 26, Issue 2 2015, 129-147. © 2015 Association for Financial Counseling and Planning Education®. All rights of reproduction in any form reserved

Savings Goals and Saving Behavior From a Perspective of Maslow’s Hierarchy of NeedsJae Min Lee1, Sherman D. Hanna2

The purpose of this study was to examine associations between saving goals and saving behavior from a perspective ofMaslow’s Hierarchy. Using 1998-2007 Surveys of Consumer Finance datasets, we analyzed responses given to an openended saving reason question, and categorized responses into six saving goals. The retirement/security goal was the mostfrequently mentioned, and the self-actualization goal was the least frequently mentioned. We tested two models toascertain whether the order of response differed in the likelihood of saving, measured as whether households spent lessthan income. Model 1 tested the effects of whether particular goals were given as the first response to the open-endedquestion, and Model 2 tested the effects of whether particular goals were given as any response. In both analyses, selfactualization and retirement/security had the strongest associations with saving behavior.

Keywords: goal setting; Maslow hierarchy; saving goal; saving motive; Survey of Consumer Finances

Goal setting and the way a goal is established are important determinants for obtaining outcomes, not only in finance but in other areas, including learning, health, and organizational performance (Fujita, Trope, Liberman, & Levin-Sagi, 2006; Gómez-Mpiñambres, 2012; Ülkümen & Cheema, 2011). A number of studies have analyzed people’s tendencies in saving for retirement (Ando & Modigliani, 1963), saving for precautionary purposes (Leland, 1968), and saving for the purchase of a house (Hayashi, Ito, & Slemrod, 1988). Although examination of such traditional goals has been at the forefront of the academic debate regarding saving (Van Veldhoven & Groenland, 1993; Yuh & Hanna, 2010), empirical studies indicate that households may save for many other reasons related to psychological needs or for multiple reasons simultaneously (Fisher & Anong, 2012; Wärneryd, 1999; Xiao & Noring, 1994).

The simplest definition of “saving” that can be applied to all households is income minus consumption in a year (or other time period) (Browning & Lusard, 1996). The purposes and meanings of saving, however, are different for each household, and are determined not only by income, but by the need to accumulate consumable goods (Wärneryd, 1989). The projection of such psychological factors as needs and expectations into the need for saving distinguishes this paper from classic saving behavior studies (Ewing & Payne, 1998; Van Veldhoven & Groenland, 1993; Wärneryd, 1989). Accumulating money for a particular reason reflects specific personal values. Thus, the decision to save may not necessarily be related to a desire for financial safety or family prosperity

(Canova, Rattazzi, & Webley, 2005). To better understand the saving behavior of households, therefore, it is important to identify the attributes of each saving goal and the influence of human needs on the likelihood of saving. This will allow us to explore a model with greater applicability in empirical behavior to further study how to improve saving behavior. Focusing on psychological needs and the reasons for saving (beyond financial emergencies and retirement preparation) will expand the scope of saving behavior research by providing unique insights on the characteristics of household saving and the relative importance of certain saving goals.

This study has the following objectives: (a) to analyze the incidence of goals at the different levels of Maslow’s hierarchy of needs; (b) to examine patterns of first response versus any response of goals; and (c) to identify the relative importance of the saving goals categorized into Maslow’s hierarchy on the likelihood of saving. The contributions of this study include examining the effects of different hierarchal savings goals on the likelihood of saving, controlling for household characteristics and attitudes. This study is unique in its comparison of the effect of the most salient goal (first response) to whether particular goals were mentioned at all (any goal response) to obtain insights into whether the order of response is important. This study carefully identifies how savings objectives listed in the Survey of Consumer Finances (SCF) datasets were coded into hierarchal goals defined based on Maslow’s theory, therefore making it easier for future researchers to test alternative definitions of the hierarchal goals.

1 Department of Family Consumer Science, Minnesota State University, Mankato, 102 Wiecking Center, Mankato, MN 56001, 614-558-0018, [email protected] Human Sciences Department, The Ohio State University, 1787 Neil Avenue, Columbus, OH 43210, 614-292-4584, [email protected]

09795Text.indd 129 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015130

Related LiteratureSaving Goals: Why Do People Save?A goal is defined as a desired end state that people try to achieve through cognitive regulation (Ford, 1992). Saving goals are viewed as reasons or purposes that lead households to save and can be measured with the question of, “What is your most important reason for saving?” (Browning & Lusardi, 1996; DeVaney, Anong, & Whirl, 2007; Xiao & Noring, 1994). Keynes (1936) suggested the following eight saving goals, which are relatively stable and thereby influence the propensity to consume over a long period of time: precaution needs, foresight, calculation, improvement, independence, enterprise, pride, and avarice.

Many other authors have used a variety of approaches to discuss saving goals in household finance. Studies focusing on retirement or precautionary reasons based on classic models such as the permanent income hypothesis (Friedman, 1957) and the life cycle hypothesis (Ando & Modigliani, 1963) have led the discussion on saving decisions. Other researchers depended on behavioral or psychological approaches, such as Dusenberry (1949) who emphasized the influence of social peers on the consumption and saving of households, and Shefrin and Thaler (1988), who proposed the behavioral life cycle hypothesis, assuming impatience and bounded rationality, and using the concepts of self-control, mental accounting, and framing. Although such approaches have contributed to understanding household saving practices, they do not consider how multiple goals may differently affect saving behavior, nor do they focus on reasons for saving other than retirement and precautionary purposes (Fisher & Anong, 2012; Wärneryd, 1999; Xiao & Noring, 1994).

An alternative approach may serve better for analyzing the effects of multiple saving goals. For example, analyzing saving goals based upon a hierarchical structure hypothesizes that since each level in the structure consists of goals with similar characteristics, these different levels can coexist. While the number of levels in the hierarchy and the specific characteristics of those levels are different among various studies, in general, short-term basic financial needs are considered lower level saving goals, financial security needs are middle level, and self-actualization are at the top level. All of this remains consistent with Maslow’s theory (Canova et al., 2005; Lindqvist, 1981).

The relationship between shares (or types) of financial assets and needs, as well as the possibility of movement from lower to higher levels, are also analyzed in previous

research. Xiao and Anderson (1997) found that checking and savings accounts reflected lower level needs; whereas, bonds and stocks were related to higher level needs. As financial resources increased, households were more likely to pursue higher levels of financial needs. DeVaney et al. (2007) reported similar findings on household characteristics, in which the age of the head of household, family size, and length of the planning horizon were generally related to the likelihood of movement from lower to higher saving levels, and income, gender, race, education, health, and risk tolerance were also significant factors. This study therefore assumes that saving goals can be categorized into multiple hierarchical levels and focuses on the relative effects of each goal on saving decisions.

Importance of Goal Setting on Desired Outcomes Goal setting intensifies the motivation for achievement, affecting both the productivity and satisfaction of goal holders (Gómez-Miñambres, 2012). It is often noted, however, that there is a discrepancy between the goal’s intention and actual implementation (Soman & Zhao, 2011). The importance of clarifying the salient aspects of a goal has been emphasized in many areas, including better learning, job performance, mental health, and maintenance of behavioral change people planned for (Deci & Ryan, 2000; Gómez-Miñambres, 2012). Because goal-directed behavior regulates process, it thus positively affects desired outcomes. Specifically, goal clarification as a device for commitment controls long-term, time-inconsistent preferences to achieve desired outcomes (Ariely & Wertenbroch, 2002). Goal accuracy and direction boosts motivation, reasoning, and judgments based on the perceived relationship between saving goals and the prediction of spending. Peetz and Buehler (2009) found both predictions for sequential decisions and having a salient, directional goal can prompt individuals to process evidence selectively and thus consider desired conclusions as approachable. Due to this “desirability bias,” whereby people generate predictions corresponding to their preferences, saving goals create bias towards predictions for desired saving behavior. The goals themselves or the ways they were established also determine the effectiveness of outcomes. Intrinsic motivation increases active engagement with a task and promotes growth, which in turn leads to more predicted outcomes than external or controlled motivations (Deci & Ryan, 2000).

The relationship between goal specifications and anticipated outcomes depends upon the construal level at which a goal is identified or represented. For high-level construers who focus on the desirability and importance of the goal to specify saving

09795Text.indd 130 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 131

amounts, specific goals lead to greater anticipated savings. For low-level construers, however, nonspecific goals lead to greater anticipated savings (Ülkümen & Cheema, 2011). The relationship between construal level and anticipated outcomes is often understood as a matter of self-control: a higher construal level of purpose enhances self-control (Fujita et al., 2006). Goals can control present oriented impulsiveness, increasing persistence for predicted future selves (Ülkümen & Cheema, 2011). Setting specific goals, therefore, increases goal “commitment,” defined as one’s determination to reach a goal or the intention to put consistent effort towards goal achievement by clarifying the level of performance (Locke & Latham, 1994). Thus, this study assumes that goal commitment provides persistence in goal pursuit, or a disinclination to stop the goal (Hollenbeck & Klein, 1987). Having a better understanding of one’s own needs and specific saving goals, therefore, can improve the likelihood of household saving.

On the other hand, the order of goals or goal salience is also important on the desired outcomes. Prominence is defined by situations in which one attribute is valued of greater importance, or given more attention than, another attribute in terms of a criterion variable (Tversky, Sattath, & Slovic, 1988). The choice for a certain attribute is made from an evaluation over the rest of the attributes, so the subjective difference of a decision maker is reflected through that choice (Evangelidis & Levav, 2013). Therefore, the primary attributes, the first ones chosen by respondents, are weighted more than the rest of the attributes and affect the decisions (Fischer, Carmon, Ariely, & Zauberman, 1999).

Saving Goals and Saving BehaviorConsidering the positive relationship between goals and desired outcomes (as mentioned above), a specific saving plan or goal also contributes to financial progress and better preparation for an anticipated achievement (O’Neill, Xiao, Bristow, Brennan, & Kerbel, 2000). The chance of saving could increase with specific plans for the goal, e.g. deadline setting, setting regular principles for spending and saving, etc. (Ariely & Wertenbroch, 2002; Peetz & Buehler, 2009).

The importance of goals on the effectiveness and well-being of saving behavior has been empirically investigated. Studies examining the effect of saving goals on saving behavior have found that whether households had any saving goals influenced saving behavior (Hogarth & Angelov, 2003; Ülkümen & Cheema, 2011), whether households had specific saving goals had an effect (Fisher & Anong, 2012; Fisher &

Montalto, 2010; Rha, Montalto, & Hanna, 2006; Soman & Zhao, 2011; Wärneryd, 1989; 1999; Zhong & Xiao, 1995), and whether saving goals were hierarchically ordered had effects (Canova et al., 2005; Devaney et al., 2007; Xiao & Noring 1994). On the other hand, Fisher and Hsu (2012) found no significant effect of goals on saving behavior. Studies using saving goals as dependent variables have found that household characteristics had significant effects on whether respondents reported specific saving goals (Xiao & Anderson, 1997; Xiao & Fan, 2002).

Studies have examined single and multiple saving goals. In the SCF survey, respondents are asked to provide objectives for saving, and the SCF staff coded open-ended responses into categories (Table 1). Respondents provide one to six saving goals. Hogarth and Anguelov (2003) and Zhong and Xiao (1995) categorized the first response only, so that, for instance, if the respondent mentioned a retirement related goal as the first response, that household would be counted as having a retirement saving goal, but if the retirement related goal had been given as the second response, the household would not be counted as having a retirement related goal. Other researchers combined responses, so, for instance, if a respondent gave a response coded as retirement for the first, second, third, fourth, fifth, or the sixth response, that respondent would be considered to have a motive related to retirement (Devaney et al., 2007; Fisher & Anong, 2012; Fisher & Montalto, 2010; Rha et al., 2006; Xiao & Fan, 2002; Xiao & Noring, 1994).

Previous studies using Maslow’s theory as a theoretical framework categorized saving goals based on various assumptions in defined categories, but did not obtain consistent results. This study specifies saving goals based on Maslow’s theory and offers an explicit discussion of the rationales for assigning specific goals to Maslow’s hierarchal levels. This study also tests (a) a model based on the most salient (first response) saving goals and (b) a model based on each type of hierarchal goal as listed by the respondent, whether as the first or the sixth response.

Other Influencing FactorsSocio-demographic variables including age, ethnicity, presence of children, retirement status, human capital variables such as education and perceived health status, financial attitude variables, and economic variables, have all been linked to some aspects of saving decisions. Age is one of the most closely associated demographic determinants of saving. Household saving rates differed across age groups (Huggett & Ventura, 2000). Controlling for income and other

09795Text.indd 131 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015132

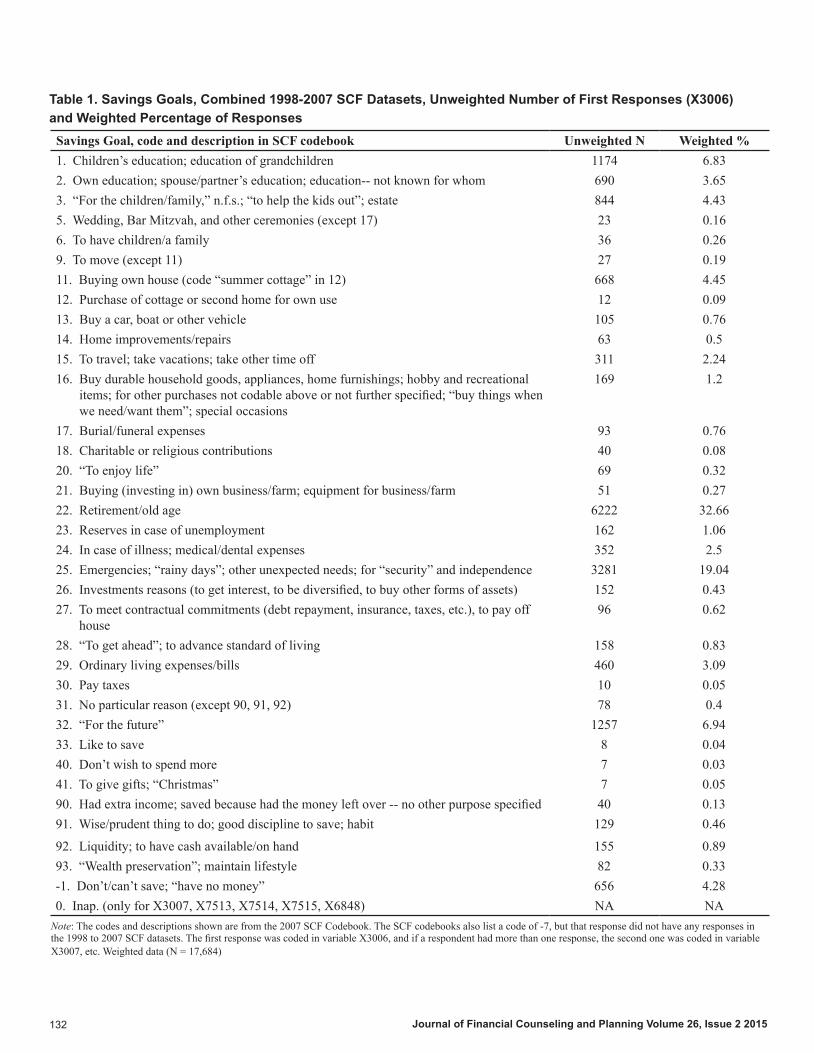

Savings Goal, code and description in SCF codebook Unweighted N Weighted %1. Children’s education; education of grandchildren 1174 6.832. Own education; spouse/partner’s education; education-- not known for whom 690 3.653. “For the children/family,” n.f.s.; “to help the kids out”; estate 844 4.435. Wedding, Bar Mitzvah, and other ceremonies (except 17) 23 0.166. To have children/a family 36 0.269. To move (except 11) 27 0.1911. Buying own house (code “summer cottage” in 12) 668 4.4512. Purchase of cottage or second home for own use 12 0.0913. Buy a car, boat or other vehicle 105 0.7614. Home improvements/repairs 63 0.515. To travel; take vacations; take other time off 311 2.2416. Buy durable household goods, appliances, home furnishings; hobby and recreational items; for other purchases not codable above or not further specified; “buy things when we need/want them”; special occasions

169 1.2

17. Burial/funeral expenses 93 0.7618. Charitable or religious contributions 40 0.0820. “To enjoy life” 69 0.3221. Buying (investing in) own business/farm; equipment for business/farm 51 0.2722. Retirement/old age 6222 32.6623. Reserves in case of unemployment 162 1.0624. In case of illness; medical/dental expenses 352 2.525. Emergencies; “rainy days”; other unexpected needs; for “security” and independence 3281 19.0426. Investments reasons (to get interest, to be diversified, to buy other forms of assets) 152 0.4327. To meet contractual commitments (debt repayment, insurance, taxes, etc.), to pay off house

96 0.62

28. “To get ahead”; to advance standard of living 158 0.8329. Ordinary living expenses/bills 460 3.0930. Pay taxes 10 0.0531. No particular reason (except 90, 91, 92) 78 0.432. “For the future” 1257 6.9433. Like to save 8 0.0440. Don’t wish to spend more 7 0.0341. To give gifts; “Christmas” 7 0.0590. Had extra income; saved because had the money left over -- no other purpose specified 40 0.1391. Wise/prudent thing to do; good discipline to save; habit 129 0.46

92. Liquidity; to have cash available/on hand 155 0.8993. “Wealth preservation”; maintain lifestyle 82 0.33-1. Don’t/can’t save; “have no money” 656 4.280. Inap. (only for X3007, X7513, X7514, X7515, X6848) NA NA

Note: The codes and descriptions shown are from the 2007 SCF Codebook. The SCF codebooks also list a code of -7, but that response did not have any responses in the 1998 to 2007 SCF datasets. The first response was coded in variable X3006, and if a respondent had more than one response, the second one was coded in variable X3007, etc. Weighted data (N = 17,684)

Table 1. Savings Goals, Combined 1998-2007 SCF Datasets, Unweighted Number of First Responses (X3006)and Weighted Percentage of Responses

09795Text.indd 132 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 133

characteristics, older households were less likely to save than were those with a household head under age 30 (Yuh & Hanna, 2010). There are racial/ethnic differences in saving behaviors as well. Ethnic groups share common cultural values and practices that form unique ways of perceiving, understanding, thinking, and behaving, which affect financial decisions (Danes, Lee, Stafford, & Heck, 2008). Rha et al. (2006) found racial/ethnic differences in the likelihood of saving. Specifically, Black households were less likely to save than otherwise similar White households. All other things equal, Asian households and Hispanic households were more likely to have a saving goal for college education for their children than were White households (Lee, Hanna, & Sireger, 1997). Household composition also affects saving decisions, such as the likelihood of saving and the dependent level on saving for unexpected expenses. Having a dependent child was related to a lower likelihood of saving (Yuh & Hanna, 2010). Households with children were less likely to depend on saving for unexpected expenses than those without children living with them (Lusardi, Schneider, & Tufano, 2011). When it comes to working status, Yuh and Hanna (2010) found that self-employed households were more likely to save than those not self-employed, and retired households were less likely to save than non-retired households. Hurd and Rohwedder (2003) found a decrease in consumption after retirement. Kennickell and Lusardi (2006) found a difference in desired precautionary saving between persons aged under 62 and those aged over 62.

Human capital variables, defined as the required knowledge, skills, abilities, and attitudes to produce professional services (Pennings, Lee, & Witteloostuijn, 1998), affect households’ financial decisions. Educational level is often assumed to represent financial literacy or cognitive ability to make financial decisions (Berry, Gruys, & Sackett, 2006). Fisher and Montalto (2011) and Yuh and Hanna (2010) found a positive relationship between education and the likelihood of saving. Health condition also affects total wealth accumulation and assets composition, often conditional on the availability of health insurance (Rosen & Wu, 2004; Starr-McCluer, 1996). Household heads in poor health without health insurance had higher out-of-pocket spending for health costs, leading to lower precautionary saving than their otherwise similar counterparts (Starr-McCluer, 1996).Financial attitudes, such as risk preference and planning horizon, affect household financial decisions, including saving and composition and allocation of an investment portfolio (Barsky, Juster, Kimball, & Shapiro, 1997). Greater uncertainty increases the incentive to save for risk averse

households as they seek to protect themselves against the higher likelihood of adverse outcomes and losses (Carroll, 1992). A greater aversion to risk leads to a greater saving demand (Heaton & Lucas, 1997). On the other hand, saving decisions are based on relative tradeoffs between costs and benefits at different points in time (Frederick, Loewenstein, & O’Donoghue, 2002). Time horizon, thus, is an important determinant of saving decisions, often captured as the marginal rate of substitution of current consumption for future consumption (Bryant & Zick, 2006).

Economic variables, including income and homeownership, determine saving decisions. Income and saving are closely related. In general, as household income or lifetime earnings increases, saving also increases (Chang, 1994; Rha et al., 2006; Yuh, & Hanna, 2010). Dynan, Skinner, and Zeldes (2004) found a positive relationship between the marginal propensity to save and lifetime income, as well as a positive correlation between saving rates and lifetime income. Yuh and Hanna (2010) noted that a normative model does not imply a positive relationship between income and the likelihood of saving, unless the effects of the social safety net are considered. Homeownership is also related to saving. Homeowners were more likely to save than non-homeowners (Fisher & Montalto, 2010; Yuh & Hanna, 2010). Based on the relationship found in the previous studies, this research controls for socio-demographic variables, human capital, financial attitude, and economic variables to examine the relationship between saving goals and saving decisions.

Theoretical Background and Hypotheses Maslow’s Hierarchical Theory of Human NeedsMaslow (1954) proposed that human needs can be captured in a hierarchical structure. The model he proposed is shaped like a pyramid, with the most basic levels of human needs for life, such as sufficiency needs, at the bottom, and the need for the most abstract desires at the top. The former includes physical needs, safety/security needs, love/belonging needs, and esteem needs, all of which are located in the lower levels. At the top there are self-actualization needs, which include cognitive needs, aesthetic needs, and self-transcendence needs. In order to move up to the higher levels, the lower level needs have to be met first. Since household saving can reflect human needs (DeVaney et al., 2007), the connection between the psychology of human nature and household saving needs in an economic model can open a broader discussion on how to specify human needs as saving goals, and how to introduce such goals in household saving behavior.

09795Text.indd 133 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015134

In classic models, concepts such as simultaneous saving goals and the relative hierarchy of human needs on saving decisions would not be identified. The life cycle hypothesis (Ando & Modigliani, 1963), one of the representative classic models on saving, assuming that households attempt to maximize their utility by selecting optimal consumption levels over their lifetime, focuses on retirement saving goal (Xiao, 1997). Under the idea of smooth consumption, which indicates an effort to keep the marginal utility of consumption stable (Yuh & Hanna, 2010), households tend to save for either retirement or wealth accumulation. Inter-temporal consumption decisions are based on the long term prediction on lifetime wealth and can be accomplished by saving when income is high and by dissaving when income is low. Thus, saving decisions are constrained by disposable income (Ewing & Payne, 1998) and factors related to retirement are important for saving decisions, including current age, expected retirement age, and life expectancy (Xiao, 1997).

Unlike classic models, an approach with such a psychological perspective would provide (a) a different theoretical background and (b) the determinants of various saving goals to test alternative definitions and the relative effects of hierarchical goals on saving decisions. Based on the related studies described above, the following research hypotheses are proposed to examine the incidence of goals at the different levels in Maslow’s hierarchy of needs, to examine patterns of first response versus any response of goals, to find whether the order of response is important, and to identify the relative importance of the saving goals categorized into Maslow’s hierarchy on the likelihood of saving. Six saving goals categorized hierarchically were generated and two models distinguishing the first response from any responses for saving reasons were used.

H1: Holding other factors constant, households with specific saving goals are more likely to save than those without specific saving goals.

H2: Holding other factors constant, the level of savings goals in a Maslow’s hierarchy will have different effects on the likelihood of saving.

H3: Holding other factors constant, there will be different effects on the likelihood of saving between goals based on the first response only and goals based on any responses from the first to the sixth answer.

MethodsDataThis study used a combination of four U.S. Survey of Consumer Finances datasets (1998, 2001, 2004, 2007). The triennial SCF survey has been conducted by the Federal Reserve Board of Governors since 1983 and provides reliable and detailed information on the broad financial circumstances of U.S. households (Bucks, Kennickell, Mach, & Moore, 2009). The individual household is defined as the primary economic unit (PEU), which consists of “an economically dominant single individual or couple (married or living as partners) in a household and all other individuals in the household who are financially interdependent with that individual or couple” (Kennickell, 2009). The survey data include information on a variety of aspects of household finances (including assets, debts, income, saving, and investments) and attitudes in financial decision making (such as risk preference, planning horizon, and saving goals) besides sufficient demographic background of each household (such as age, education level, and health status).

The combined dataset analyzed for this study contains 17,684 households (4,305 in 1998, 4,442 in 2001, 4,519 in 2004 and 4,418 in 2007). The proportions of households reporting some types of goals were small, for instance, less than 1% reported a self-actualization goal as the first response, so combining four SCF datasets was necessary to obtain robust estimates of effects. The proportions of households reporting that they saved (spent less than income) were quite stable over the 1998 to 2007 SCF datasets (Bucks, Kennickell, & Moore, 2006; Bucks, et al., 2009), ranging from 56% to 59%; whereas, the proportion of households reporting that they saved in the 2010 SCF dataset was substantially lower than any of the other survey years, 52%. Furthermore, other changes plausibly would have made patterns very different in that year. There may be many differences in financial decisions of households between before the Great Recession and after the Great Recession, including differences in saving goals and behavior. The purpose of this study is to consider various goals that have not been treated in the classic models. To compare before and after the Great Recession would be a different approach with a different research objective, which can be left to future research. Therefore, we did not include the 2010 dataset for the analysis.

Dependent VariableThe dependent variable was whether households reported saving, that is, spent less than income. This saving measure was constructed from the answer to the question (Rha et al.,

09795Text.indd 134 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 135

2006; Yuh & Hanna, 2010), “Over the past year, would you say that: your spending exceeded your income, that it was about the same as your income, or that you spent less than your income?” This variable is considered the difference between income and spending, with spending for vehicles, houses, or any investment excluded (Fisher & Montalto, 2010; Yuh & Hanna, 2010). Three SCF variables (X7508, X7509, and X7510) were used for this saving measure using SAS code provided by the Federal Reserve Board (Kennickell, 2009). A household was designated as a saver if the respondent answered that spending was less than income during the previous year. If the respondent responded that spending was about the same as income, but the spending included purchases for houses, vehicles, or any investments, the household was also considered as a saver (Yuh & Hanna, 2010).

Independent Variables Saving GoalsIn the SCF surveys, respondents are asked the following open-ended question: “Now, I’d like to ask you some questions about your attitudes about saving. People have different reasons for saving, even though they may not be saving all the time. What are your most important reasons for saving?” The SCF staff coded up to six open-ended responses into categories. The 35 valid categories for the 2007 SCF are shown in Table 1, along with the unweighted number of

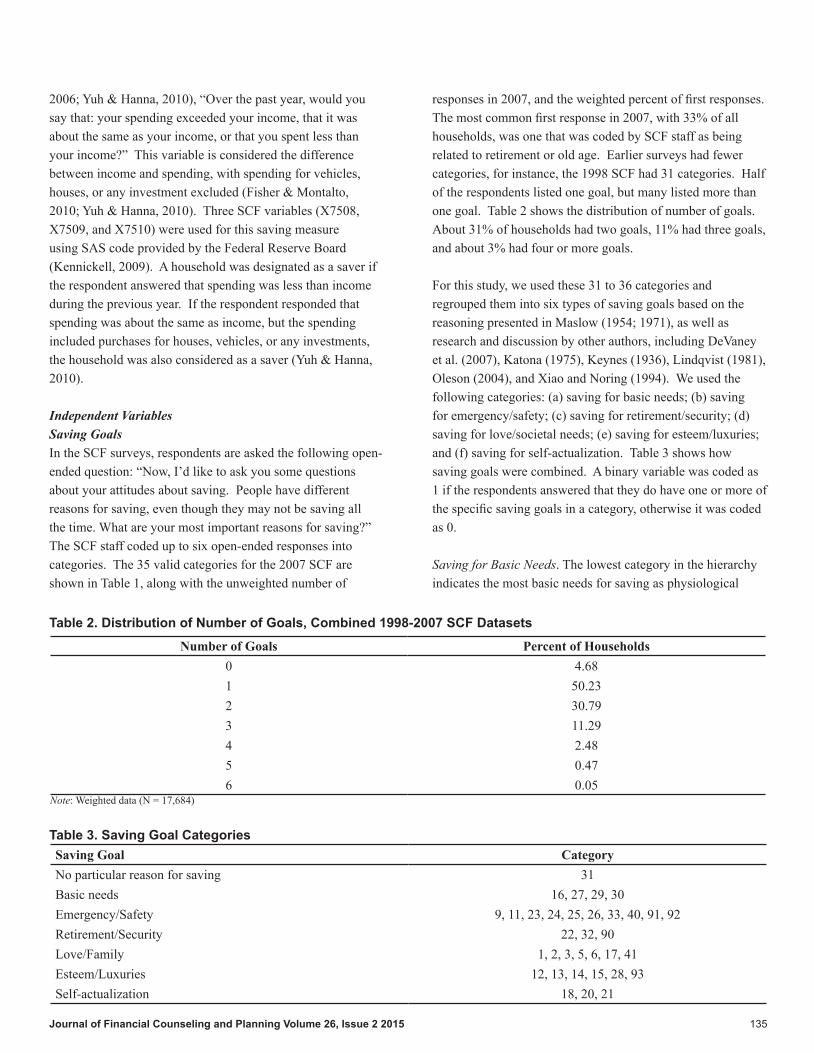

responses in 2007, and the weighted percent of first responses. The most common first response in 2007, with 33% of all households, was one that was coded by SCF staff as being related to retirement or old age. Earlier surveys had fewer categories, for instance, the 1998 SCF had 31 categories. Half of the respondents listed one goal, but many listed more than one goal. Table 2 shows the distribution of number of goals. About 31% of households had two goals, 11% had three goals, and about 3% had four or more goals.

For this study, we used these 31 to 36 categories and regrouped them into six types of saving goals based on the reasoning presented in Maslow (1954; 1971), as well as research and discussion by other authors, including DeVaney et al. (2007), Katona (1975), Keynes (1936), Lindqvist (1981), Oleson (2004), and Xiao and Noring (1994). We used the following categories: (a) saving for basic needs; (b) saving for emergency/safety; (c) saving for retirement/security; (d) saving for love/societal needs; (e) saving for esteem/luxuries; and (f) saving for self-actualization. Table 3 shows how saving goals were combined. A binary variable was coded as 1 if the respondents answered that they do have one or more of the specific saving goals in a category, otherwise it was coded as 0.

Saving for Basic Needs. The lowest category in the hierarchy indicates the most basic needs for saving as physiological

Number of Goals Percent of Households0 4.681 50.232 30.793 11.294 2.485 0.476 0.05

Table 2. Distribution of Number of Goals, Combined 1998-2007 SCF Datasets

Note: Weighted data (N = 17,684)

Saving Goal CategoryNo particular reason for saving 31Basic needs 16, 27, 29, 30Emergency/Safety 9, 11, 23, 24, 25, 26, 33, 40, 91, 92Retirement/Security 22, 32, 90Love/Family 1, 2, 3, 5, 6, 17, 41Esteem/Luxuries 12, 13, 14, 15, 28, 93Self-actualization 18, 20, 21

Table 3. Saving Goal Categories

09795Text.indd 135 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015136

needs, such as food, water, and warmth (Maslow, 1971). This category consists of the necessary budgets for a rudimentary quality of living and represents saving for daily expenses, such as ordinary living expenses/bills (SCF code number 29), paying taxes (30), buying durable households goods/appliances/home furnishing (16), and meeting contractual commitments (27).

Saving for Emergency/Safety. The second level of the saving goal category is saving for emergency/safety. This includes unexpected emergencies like, illness (24), unemployment (23), or investment reasons to get interest or to be diversified (26). Needs for freedom from fear are central to this safety goal, and savings are used for covering expenses on a sudden loss of income, as a buffer stock against unforeseen conditions in the future (Keynes, 1936). This goal also includes buying one’s own home (11), moving (9) or home repairs/improvements (25), which satisfy the needs of financial safety and physical safety. Cash management needs are also included in this category: to save (33), do not wish to spend more (40), wise/prudent thing to do (91), and liquidity/to have cash available on hand (92).

Saving for Retirement/Security. The third saving goal, saving for retirement/security, consists of saving for retirement/old age (22), for the future (32), and for having extra income (90). All these selected categories reflect the desire to reduce the financial difficulties that occur after retirement.

Saving for Love/Societal Needs. The fourth level is saving for love/societal needs, related to specific expenses to take care of family or children, including: just for the children or family (3), education for children or grandchildren (1), one’s own or spouse’s education, (2) to have children or a family (6), wedding and other ceremonies (5), funerals (17), and Christmas gifts (41). Maslow’s level of human needs, belonging needs for love with family or with friends, can be applied to this saving purpose.

Saving for Esteem/Luxuries. The fifth level is saving for esteem/luxuries associated with self-esteem needs in Maslow’s theory. According to his theory, individuals are eager to gain respect or recognition from others while they interact with and influence each other, and therefore behaviors of households can be interpreted within this social context. The fifth saving goal is composed of the following categories: purchase of cottage or second home for personal use (12), buying a car, boat or other vehicle (13), home improvements/repairs (14), to travel/take vacations (15), to get ahead or to advance standard

of living (28), and to maintain current lifestyle (wealth preservation) (93).

Saving for Self-Actualization. The highest level, self-actualization, is related to one’s effort to reach full potential in life, distinct from household levels. Self-actualization is defined as the full realization of one’s capabilities, or the full realization of one’s “true self” (Gleitman, Fridlund, & Reisberg, 2004). This goal level consists of a more personalized desire for one’s values in life, achieving a lifetime goal for a better self, or enhancing one’s emotional well-being. We judged that the following SCF categories applied to the self-actualization goal: to purchase a business (21), to enjoy life (20), and to make charitable or religious contributions (18). The goals in this category are not used as mediators to bring out other motivations or outcomes: self-actualization is a desire, not a driving force, which leads to realizing one’s potential, and encourages the individual to achieve their ambitions rather than determine one’s life (Maslow, 1971). It is plausible that one’s own education may be for self-actualization. Unfortunately, the SCF coding of education goals other than children (code 2) does not distinguish between one’s own education and the education of a spouse or unknown person other than one’s children. It could be argued that this category, as it applies to one’s own education, might be counted as self-actualization (c.f., DeVaney et al. 2007), but for the education goals other than the respondent, it does not seem to fit the self-actualization category. We have thus decided to conservatively classify the categories into each level of goals. Belonging needs for love with family or with friends may be more relevant to love/societal saving purposes, and thus we included the education category in the saving for love/societal level. It is also plausible that some people may travel for self-actualization, but we decided that travel to resorts, etc. might be more appropriately categorized as luxuries.

Some choose to start their own business as their lifetime goal. Some choose to help others through financial, emotional, or psychical support, which give providers psychosocial and emotional happiness or self-fulfillment (Aknin et al., 2013; Dunn, Aknin, & Norton, 2008; Schwartz & Sendor, 1999). Those who act altruistically acknowledge that their lives are changed for the better and filled with an improved satisfaction of both themselves and their life (Brunier, Graydon, Rothman, Sherman, & Liadsky, 2002; Dunn et al., 2008). Financial generosity, or using financial resources to help others, is also known to promote the provider’s emotional happiness and self-fulfillment (Aknin et al., 2013). Harbaugh, Mayr, and

09795Text.indd 136 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 137

Burghart (2007) found that donating to charity arouses neural responses in areas linked to the emotional reward, giving the donor an enhanced self-actualization. In this sense, these particular goals are not used as a driving force to achieve other reasons or motivations, such as basic needs or retirement. Households can have self-actualization goals just for realizing their own potential.

In sum, these different saving goal categories reflect not only the need to protect households from income uncertainty, but also personal desires influenced by social symbols, and by their own value beyond the functional usage of spending money by planned materialization, such as saving behavior (Wärneryd, 1989). A total of six different saving goals were used. Each of the saving goals were measured as dichotomous variables, coded as “1,” “having specific level of goals” if the respondents answered that they have any of designated saving reasons in each category of goals, otherwise it was coded as 0.

Control Variables Socio-demographic variables, human capital variables, financial attitude variables, economic variables, and time trend variables were used as control variables. Socio-demographic variables included age of the head, respondent’s racial/ethnic group, the presence of children, and work conditions. Age was classified by five categories: under 30 (reference category), 30-39, 40-49, 50-59, 60-69, and 70 and over. The race/ethnicity of the respondent had the four categories identified in the public dataset of the SCF, White (reference category), Black, Hispanic, and Asian/others. The presence of children (whether or not a household had a dependent child under 18 living in the home) and retirement status (whether or not the head was retired) were measured as dichotomous variables.

Human capital variables included educational attainment and the perceived health status of the head, measured as categorical variables. Our measure of educational attainment of the household head had five categorical variables: less than high school degree (reference category), high school degree, some college, bachelor degree, and post-bachelor degree. The assessment of health status of the head had four categories: poor (reference category), fair, good, and excellent health.

Household financial attitude variables included risk tolerance and planning horizon. The level of risk tolerance was measured as four categories: no risk (reference category), average, above, and substantial risk. We categorized planning horizon as four categories: next few months (reference

category), the next year, the next few years, the next 5 to 10 years, or longer than 10 years. Two binary variables were used to measure expectations, whether or not a household expected a substantial inheritance in the future and whether or not a household had a foreseeable expense in the next 5 to 10 years.

Economic variables were income and homeownership. Annual income in 2007 dollars was categorized into five levels: less than $10,000 (reference category), $10,000-$24,999, $25,000-$49,999, $50,000-$99,999, and $100,000 or more. Homeownership was whether or not the household owned a home. There was a dummy variable for each survey year, with 1998 as the reference category, in order to control for changes in the economic environment.

Data AnalysesAs mentioned above, respondents in the SCF survey may answer up to six reasons for saving so as to identify which one was the primary response for this question. It is plausible that the first response given by SCF respondents for saving goals is the most salient goal and more important than the rest of the choices. To examine this potential difference of effects of goals by the order of answering, we used two different models: whether a particular type of goal was mentioned in the first response, and whether a particular type of goal was mentioned in any response. In the SCF dataset, the first response given by the respondent is in variable X3006, and the second through sixth responses are in variables X3007, X7513, X7514, X7515, and X6848. Our multivariate analyses are designated Model 1 (first response) and Model 2 (any response).

To analyze the influence of independent variables on the dependent variable, which was dichotomous, two logistic regression analyses were implemented for each model. We conducted both reduced analyses and full analyses for each model.

Reduced Models. The reduced logistic regression for each model was conducted with only the saving goal variables, so as to ascertain the effect of each saving goal. In Model 1 (first response), the likelihood of saving is assumed to be a function of whether a household had one of the six saving goals as the first response. In Model 2 (any response), the likelihood of saving is assumed to be a function of whether a household had any of the six saving goals in any response. We estimated the reduced models using two logistic regressions.

09795Text.indd 137 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015138

Full Models. The logistic regression for each full model contained control variables in addition to the savings goal variables. In Model 1 (first response), the likelihood of saving was assumed to be a function of whether a household had any of the six saving goals in any response, plus control variables, including socio-demographic; human capital, financial attitude, economic, and time trend variables; and as an error term. The full model for Model 2 (any response) was estimated in the same way. For each categorical variable, the odds ratio can be interpreted as the ratio of the odds of saving for the given category relative to the reference category, controlling for other independent variables.

For descriptive results, weighted analyses averaged across all implicates were performed to represent nationwide sampling estimates. As suggested by Lindamood, Hanna, and Bi (2007), the logistic regressions were not weighted. For the logistic regression analysis, repeated imputation inference (RII) techniques were used to obtain inference of greater validity based on the variance estimates (Montalto & Sung, 1996). As suggested by Lindamood et al. (2007), in the multivariate analyses we present the exact significance levels of effects rather than the conventional thresholds (such as the 5% level).

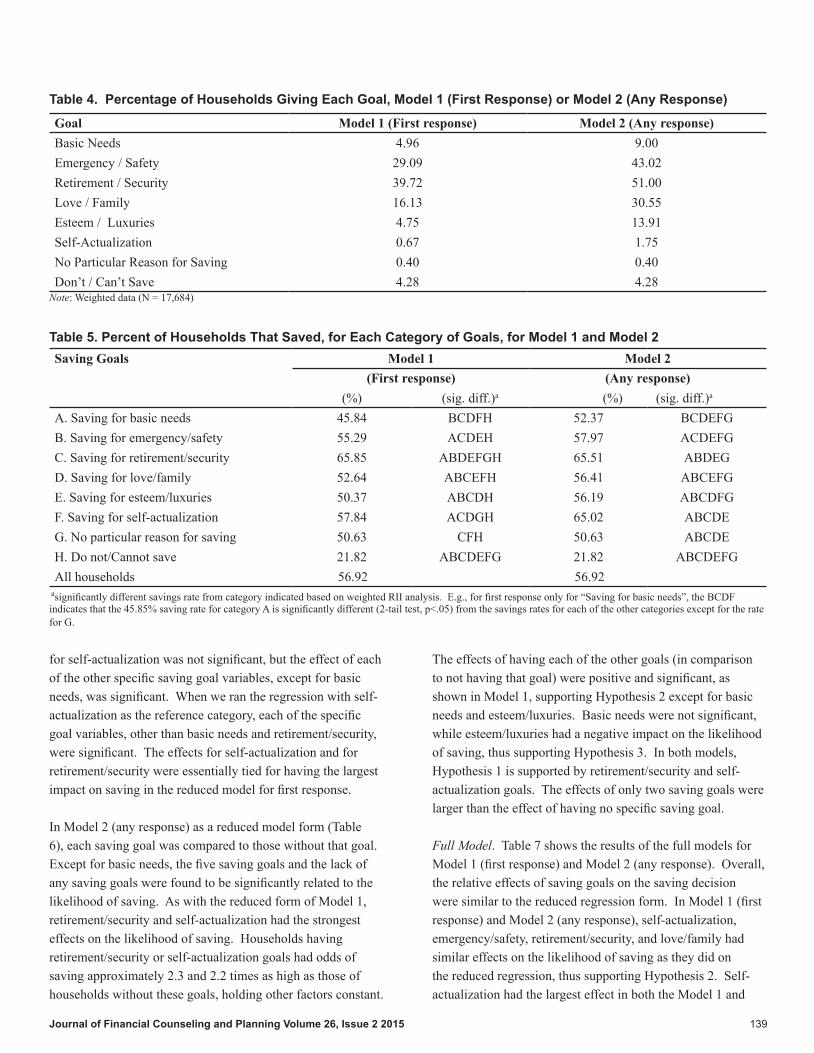

Results Descriptive Statistics Table 4 shows the frequency of each saving goal variable for the combined 1998 to 2007 SCF datasets for Model 1 (first response) and Model 2 (any response). Goals associated with retirement/security were the most frequent with about 40% of respondents giving that type of goal as their first response (Model 1), and 51% for any response (Model 2). The least frequent motive was the self-actualization goal, with less than 1% as the first response, and about 2% for any response. The actual unweighted number of households with self-actualization responses in the combined sample was 160 for the first response and 425 for any response. For both the first response and for any response, emergency/safety goal was ranked second, and love/family goal was third. There are differences in ranks between the fourth and fifth goals in the two models: in Model 1(first response), the frequency of esteem/luxuries goal was smaller than that of basic needs goal, but the ranking was reversed for Model 2 (any response).

Table 5 shows the descriptive patterns of saving (spending less than income) by saving goals. For Model 1 (first response), 66% of those with a retirement/security goal saved, compared to the overall sample frequency of 57%. For Model 2 (any

response), over 65% of those with a retirement/security goal and over 65% of those with a self-actualization goal saved. Based on the any response analyses, those who had a specific saving goal other than for basic needs had a saving frequency higher than the sample average, but those with a goal for basic needs and those who did not provide any particular reason for saving had lower frequencies than the overall sample mean. For the respondents answering the saving goal question with an answer indicating they could not or did not save, 22% spent less than income, so there was some inconsistency between the answers to the different questions. Overall, the any response patterns suggest that having a specific saving goal was associated with being more likely to save.

In both models, safety (e.g., emergency) and security (e.g., retirement) related goals were the most commonly stated goals. Goals related to basic needs were less common, but that may reflect typical patterns in an advanced economy with a social welfare system. Goals related to love/family were more frequent than goals related to esteem/luxury. Self-actualization was the least frequent of the six goals. On the other hand, the descriptive patterns in Tables 4 and 5 show some of the differences between Model 1 (first response) and Model 2 (any response), most notably in the higher frequencies for both self-actualization and other goals for any response (Table 4) and the higher percent of savers for any response of self-actualization (Table 5).

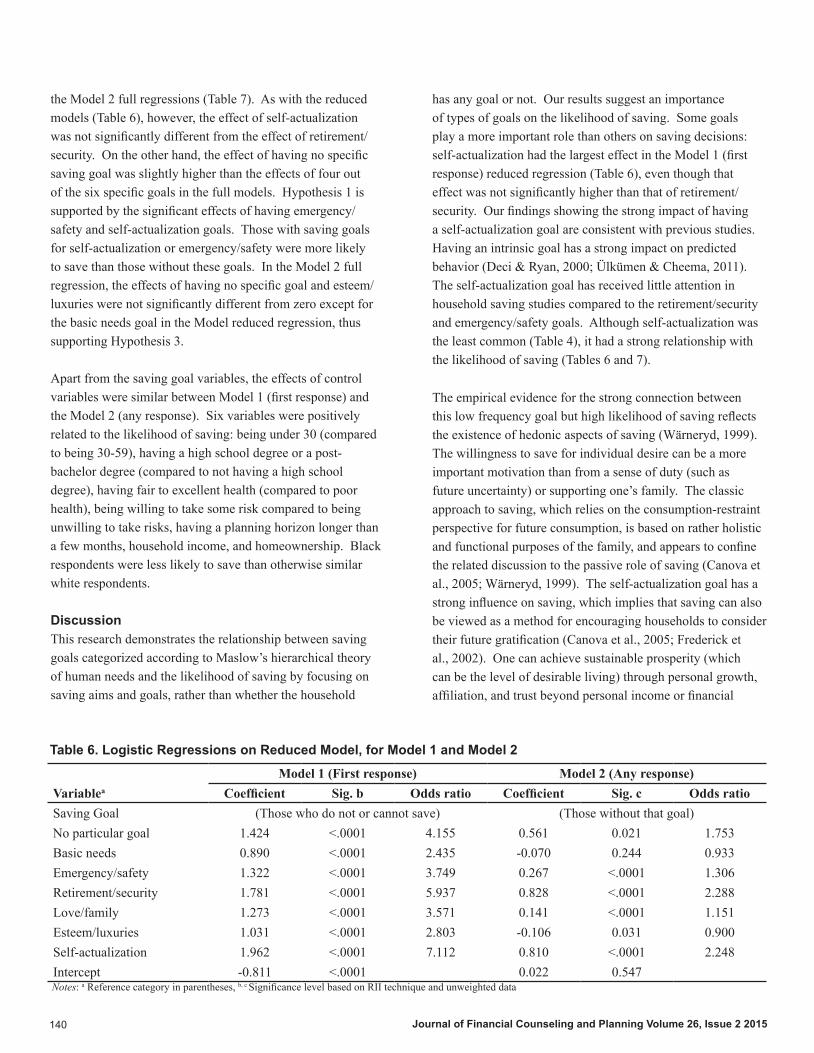

Multivariate StatisticsThe results of the two logistic analyses for Model 1 (first response) and Model 2 (any responses) on the likelihood of saving are presented in Table 6 and Table 7. Both models’ results contain the reduced regression and full regression analyses.

Reduced Model. Table 6 shows the results of reduced models, with only savings goals as the independent variables. The reduced model was used to show the impact that saving goals have on saving decisions. In Model 1 (first response), the effect of each saving goal (compared to stating that one was unable to save or did not save) on the likelihood of saving was positive and significant. This result is related to having “do not/cannot save” as the reference category, while magnitudes of the coefficients offer insight into relative effects of having different saving goals. Self-actualization was the most influential goal. Retirement/security, emergency/safety, love/family, esteem/luxuries, and basic needs followed, supporting Hypothesis 2. When we ran the same regression with retirement/security as the reference category, the coefficient

09795Text.indd 138 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 139

for self-actualization was not significant, but the effect of each of the other specific saving goal variables, except for basic needs, was significant. When we ran the regression with self-actualization as the reference category, each of the specific goal variables, other than basic needs and retirement/security, were significant. The effects for self-actualization and for retirement/security were essentially tied for having the largest impact on saving in the reduced model for first response.

In Model 2 (any response) as a reduced model form (Table 6), each saving goal was compared to those without that goal. Except for basic needs, the five saving goals and the lack of any saving goals were found to be significantly related to the likelihood of saving. As with the reduced form of Model 1, retirement/security and self-actualization had the strongest effects on the likelihood of saving. Households having retirement/security or self-actualization goals had odds of saving approximately 2.3 and 2.2 times as high as those of households without these goals, holding other factors constant.

The effects of having each of the other goals (in comparison to not having that goal) were positive and significant, as shown in Model 1, supporting Hypothesis 2 except for basic needs and esteem/luxuries. Basic needs were not significant, while esteem/luxuries had a negative impact on the likelihood of saving, thus supporting Hypothesis 3. In both models, Hypothesis 1 is supported by retirement/security and self-actualization goals. The effects of only two saving goals were larger than the effect of having no specific saving goal.

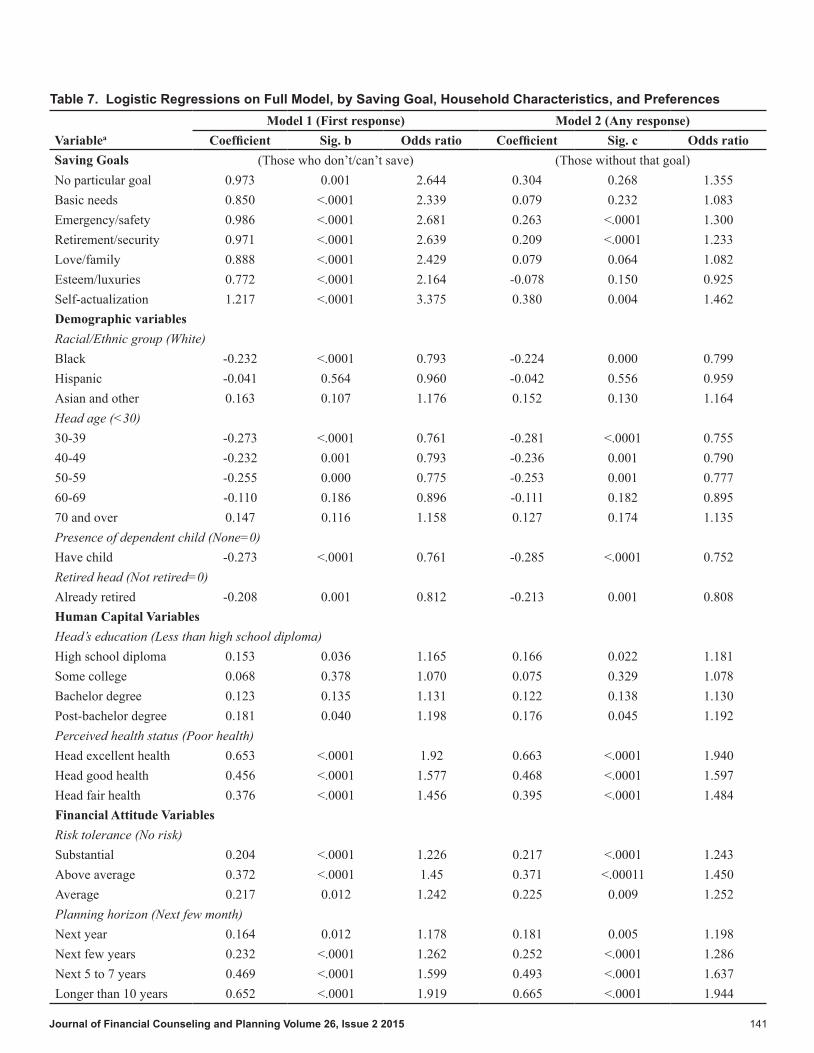

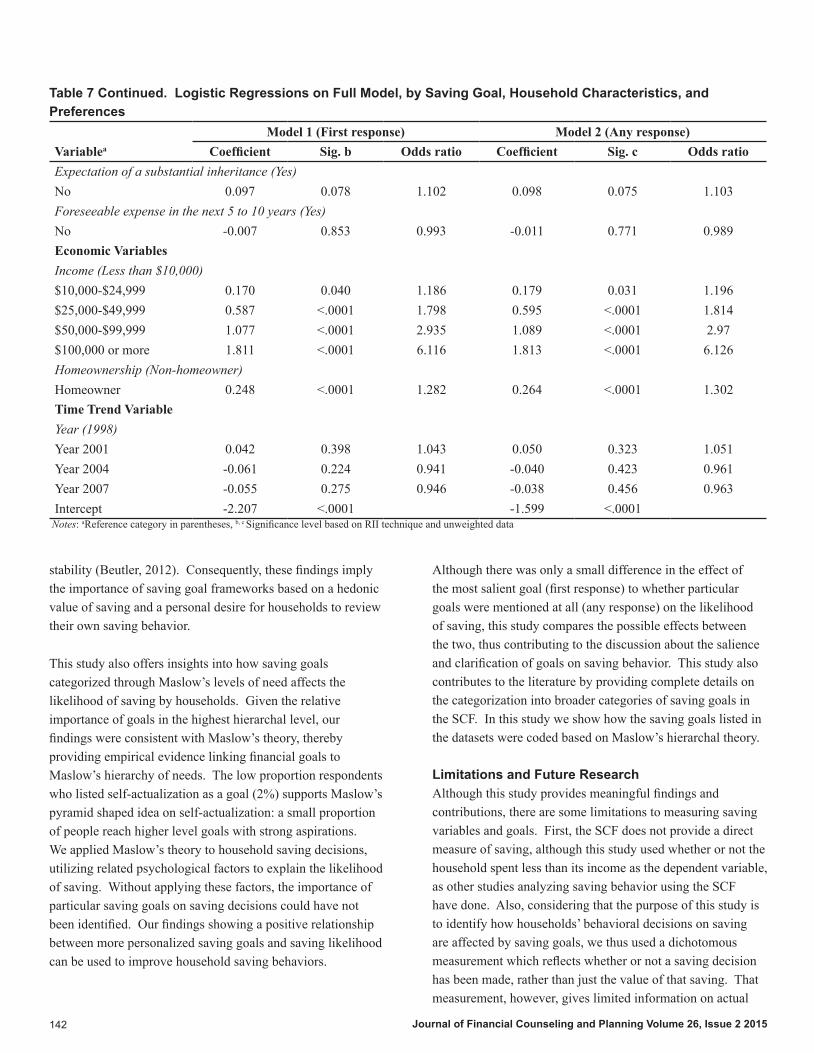

Full Model. Table 7 shows the results of the full models for Model 1 (first response) and Model 2 (any response). Overall, the relative effects of saving goals on the saving decision were similar to the reduced regression form. In Model 1 (first response) and Model 2 (any response), self-actualization, emergency/safety, retirement/security, and love/family had similar effects on the likelihood of saving as they did on the reduced regression, thus supporting Hypothesis 2. Self-actualization had the largest effect in both the Model 1 and

Goal Model 1 (First response) Model 2 (Any response)Basic Needs 4.96 9.00Emergency / Safety 29.09 43.02Retirement / Security 39.72 51.00Love / Family 16.13 30.55Esteem / Luxuries 4.75 13.91Self-Actualization 0.67 1.75No Particular Reason for Saving 0.40 0.40Don’t / Can’t Save 4.28 4.28

Table 4. Percentage of Households Giving Each Goal, Model 1 (First Response) or Model 2 (Any Response)

Note: Weighted data (N = 17,684)

Saving Goals Model 1 Model 2(First response) (Any response)

(%) (sig. diff.)a (%) (sig. diff.)a

A. Saving for basic needs 45.84 BCDFH 52.37 BCDEFGB. Saving for emergency/safety 55.29 ACDEH 57.97 ACDEFGC. Saving for retirement/security 65.85 ABDEFGH 65.51 ABDEGD. Saving for love/family 52.64 ABCEFH 56.41 ABCEFGE. Saving for esteem/luxuries 50.37 ABCDH 56.19 ABCDFGF. Saving for self-actualization 57.84 ACDGH 65.02 ABCDEG. No particular reason for saving 50.63 CFH 50.63 ABCDEH. Do not/Cannot save 21.82 ABCDEFG 21.82 ABCDEFGAll households 56.92 56.92

asignificantly different savings rate from category indicated based on weighted RII analysis. E.g., for first response only for “Saving for basic needs”, the BCDF indicates that the 45.85% saving rate for category A is significantly different (2-tail test, p<.05) from the savings rates for each of the other categories except for the rate for G.

Table 5. Percent of Households That Saved, for Each Category of Goals, for Model 1 and Model 2

09795Text.indd 139 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015140

the Model 2 full regressions (Table 7). As with the reduced models (Table 6), however, the effect of self-actualization was not significantly different from the effect of retirement/security. On the other hand, the effect of having no specific saving goal was slightly higher than the effects of four out of the six specific goals in the full models. Hypothesis 1 is supported by the significant effects of having emergency/safety and self-actualization goals. Those with saving goals for self-actualization or emergency/safety were more likely to save than those without these goals. In the Model 2 full regression, the effects of having no specific goal and esteem/luxuries were not significantly different from zero except for the basic needs goal in the Model reduced regression, thus supporting Hypothesis 3.

Apart from the saving goal variables, the effects of control variables were similar between Model 1 (first response) and the Model 2 (any response). Six variables were positively related to the likelihood of saving: being under 30 (compared to being 30-59), having a high school degree or a post-bachelor degree (compared to not having a high school degree), having fair to excellent health (compared to poor health), being willing to take some risk compared to being unwilling to take risks, having a planning horizon longer than a few months, household income, and homeownership. Black respondents were less likely to save than otherwise similar white respondents.

Discussion This research demonstrates the relationship between saving goals categorized according to Maslow’s hierarchical theory of human needs and the likelihood of saving by focusing on saving aims and goals, rather than whether the household

has any goal or not. Our results suggest an importance of types of goals on the likelihood of saving. Some goals play a more important role than others on saving decisions: self-actualization had the largest effect in the Model 1 (first response) reduced regression (Table 6), even though that effect was not significantly higher than that of retirement/security. Our findings showing the strong impact of having a self-actualization goal are consistent with previous studies. Having an intrinsic goal has a strong impact on predicted behavior (Deci & Ryan, 2000; Ülkümen & Cheema, 2011). The self-actualization goal has received little attention in household saving studies compared to the retirement/security and emergency/safety goals. Although self-actualization was the least common (Table 4), it had a strong relationship with the likelihood of saving (Tables 6 and 7).

The empirical evidence for the strong connection between this low frequency goal but high likelihood of saving reflects the existence of hedonic aspects of saving (Wärneryd, 1999). The willingness to save for individual desire can be a more important motivation than from a sense of duty (such as future uncertainty) or supporting one’s family. The classic approach to saving, which relies on the consumption-restraint perspective for future consumption, is based on rather holistic and functional purposes of the family, and appears to confine the related discussion to the passive role of saving (Canova et al., 2005; Wärneryd, 1999). The self-actualization goal has a strong influence on saving, which implies that saving can also be viewed as a method for encouraging households to consider their future gratification (Canova et al., 2005; Frederick et al., 2002). One can achieve sustainable prosperity (which can be the level of desirable living) through personal growth, affiliation, and trust beyond personal income or financial

Model 1 (First response) Model 2 (Any response)Variablea Coefficient Sig. b Odds ratio Coefficient Sig. c Odds ratioSaving Goal (Those who do not or cannot save) (Those without that goal)No particular goal 1.424 <.0001 4.155 0.561 0.021 1.753Basic needs 0.890 <.0001 2.435 -0.070 0.244 0.933Emergency/safety 1.322 <.0001 3.749 0.267 <.0001 1.306Retirement/security 1.781 <.0001 5.937 0.828 <.0001 2.288Love/family 1.273 <.0001 3.571 0.141 <.0001 1.151Esteem/luxuries 1.031 <.0001 2.803 -0.106 0.031 0.900Self-actualization 1.962 <.0001 7.112 0.810 <.0001 2.248Intercept -0.811 <.0001 0.022 0.547

Notes: a Reference category in parentheses, b, c Significance level based on RII technique and unweighted data

Table 6. Logistic Regressions on Reduced Model, for Model 1 and Model 2

09795Text.indd 140 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 141

Model 1 (First response) Model 2 (Any response)Variablea Coefficient Sig. b Odds ratio Coefficient Sig. c Odds ratioSaving Goals (Those who don’t/can’t save) (Those without that goal)No particular goal 0.973 0.001 2.644 0.304 0.268 1.355Basic needs 0.850 <.0001 2.339 0.079 0.232 1.083Emergency/safety 0.986 <.0001 2.681 0.263 <.0001 1.300Retirement/security 0.971 <.0001 2.639 0.209 <.0001 1.233Love/family 0.888 <.0001 2.429 0.079 0.064 1.082Esteem/luxuries 0.772 <.0001 2.164 -0.078 0.150 0.925Self-actualization 1.217 <.0001 3.375 0.380 0.004 1.462Demographic variablesRacial/Ethnic group (White)Black -0.232 <.0001 0.793 -0.224 0.000 0.799Hispanic -0.041 0.564 0.960 -0.042 0.556 0.959Asian and other 0.163 0.107 1.176 0.152 0.130 1.164Head age (<30)30-39 -0.273 <.0001 0.761 -0.281 <.0001 0.75540-49 -0.232 0.001 0.793 -0.236 0.001 0.79050-59 -0.255 0.000 0.775 -0.253 0.001 0.77760-69 -0.110 0.186 0.896 -0.111 0.182 0.89570 and over 0.147 0.116 1.158 0.127 0.174 1.135Presence of dependent child (None=0) Have child -0.273 <.0001 0.761 -0.285 <.0001 0.752Retired head (Not retired=0)Already retired -0.208 0.001 0.812 -0.213 0.001 0.808Human Capital VariablesHead’s education (Less than high school diploma)High school diploma 0.153 0.036 1.165 0.166 0.022 1.181Some college 0.068 0.378 1.070 0.075 0.329 1.078Bachelor degree 0.123 0.135 1.131 0.122 0.138 1.130Post-bachelor degree 0.181 0.040 1.198 0.176 0.045 1.192Perceived health status (Poor health)Head excellent health 0.653 <.0001 1.92 0.663 <.0001 1.940Head good health 0.456 <.0001 1.577 0.468 <.0001 1.597Head fair health 0.376 <.0001 1.456 0.395 <.0001 1.484Financial Attitude VariablesRisk tolerance (No risk)Substantial 0.204 <.0001 1.226 0.217 <.0001 1.243Above average 0.372 <.0001 1.45 0.371 <.00011 1.450Average 0.217 0.012 1.242 0.225 0.009 1.252Planning horizon (Next few month)Next year 0.164 0.012 1.178 0.181 0.005 1.198Next few years 0.232 <.0001 1.262 0.252 <.0001 1.286Next 5 to 7 years 0.469 <.0001 1.599 0.493 <.0001 1.637Longer than 10 years 0.652 <.0001 1.919 0.665 <.0001 1.944

Table 7. Logistic Regressions on Full Model, by Saving Goal, Household Characteristics, and Preferences

09795Text.indd 141 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015142

stability (Beutler, 2012). Consequently, these findings imply the importance of saving goal frameworks based on a hedonic value of saving and a personal desire for households to review their own saving behavior.

This study also offers insights into how saving goals categorized through Maslow’s levels of need affects the likelihood of saving by households. Given the relative importance of goals in the highest hierarchal level, our findings were consistent with Maslow’s theory, thereby providing empirical evidence linking financial goals to Maslow’s hierarchy of needs. The low proportion respondents who listed self-actualization as a goal (2%) supports Maslow’s pyramid shaped idea on self-actualization: a small proportion of people reach higher level goals with strong aspirations. We applied Maslow’s theory to household saving decisions, utilizing related psychological factors to explain the likelihood of saving. Without applying these factors, the importance of particular saving goals on saving decisions could have not been identified. Our findings showing a positive relationship between more personalized saving goals and saving likelihood can be used to improve household saving behaviors.

Although there was only a small difference in the effect of the most salient goal (first response) to whether particular goals were mentioned at all (any response) on the likelihood of saving, this study compares the possible effects between the two, thus contributing to the discussion about the salience and clarification of goals on saving behavior. This study also contributes to the literature by providing complete details on the categorization into broader categories of saving goals in the SCF. In this study we show how the saving goals listed in the datasets were coded based on Maslow’s hierarchal theory.

Limitations and Future Research Although this study provides meaningful findings and contributions, there are some limitations to measuring saving variables and goals. First, the SCF does not provide a direct measure of saving, although this study used whether or not the household spent less than its income as the dependent variable, as other studies analyzing saving behavior using the SCF have done. Also, considering that the purpose of this study is to identify how households’ behavioral decisions on saving are affected by saving goals, we thus used a dichotomous measurement which reflects whether or not a saving decision has been made, rather than just the value of that saving. That measurement, however, gives limited information on actual

Model 1 (First response) Model 2 (Any response)Variablea Coefficient Sig. b Odds ratio Coefficient Sig. c Odds ratioExpectation of a substantial inheritance (Yes)No 0.097 0.078 1.102 0.098 0.075 1.103Foreseeable expense in the next 5 to 10 years (Yes)No -0.007 0.853 0.993 -0.011 0.771 0.989Economic VariablesIncome (Less than $10,000)$10,000-$24,999 0.170 0.040 1.186 0.179 0.031 1.196$25,000-$49,999 0.587 <.0001 1.798 0.595 <.0001 1.814$50,000-$99,999 1.077 <.0001 2.935 1.089 <.0001 2.97$100,000 or more 1.811 <.0001 6.116 1.813 <.0001 6.126Homeownership (Non-homeowner)Homeowner 0.248 <.0001 1.282 0.264 <.0001 1.302Time Trend VariableYear (1998)Year 2001 0.042 0.398 1.043 0.050 0.323 1.051Year 2004 -0.061 0.224 0.941 -0.040 0.423 0.961Year 2007 -0.055 0.275 0.946 -0.038 0.456 0.963Intercept -2.207 <.0001 -1.599 <.0001

Notes: aReference category in parentheses, b, c Significance level based on RII technique and unweighted data

Table 7 Continued. Logistic Regressions on Full Model, by Saving Goal, Household Characteristics, andPreferences

09795Text.indd 142 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 143

household saving decisions, as it is conditional upon whether or not people report their spending as less than their income. For instance, in both models, having no saving goal had a stronger effect than some types of goals in the likelihood of saving. This puzzling result may imply some disparity between actual saving and the saving behavior measured in this study. Even if households did not have any saving goals or intention for saving behavior, they can still be considered to have saving behavior if their spending was less than their income.

Second, this study categorized each category provided by the SCF into six levels of saving goals using the theoretical background, related studies, and the implementation of the hierarchically ordered categories, which had not previously been statistically tested. Since our categorization was based on Maslow’s hierarchy, it would be inappropriate to use a non-theoretical statistical method—such as factor analysis—to define our categories. Moreover, the factor analysis categorization using dichotomized variables would not provide a reliable statistically interpretation. A factor analysis model assumes a linear relationship between a set of observed variables and latent trait variables, namely, common factors. If the survey items are related to a common factor via a nonlinear function—particularly likely for dichotomous variables—then the linear factor analysis model may produce mathematical artifacts (McDonald, 1985). Researchers can use the distribution of responses we provide in Table 1 to consider alternative groupings of the SCF coded responses to saving goals. We believe that our groupings of these original are consistent with Maslow’s framework, but acknowledge that other interpretations are possible, e.g., the DeVaney et al. (2007) approach that included coding SCF goal 2 as a self-actualization goal. If that goal is excluded from self-actualization (see our discussion in the Methods section) then the proportion of households with a self-actualization goal is very small, only about 1% for the first response (Model 1) and 2% for any response (Model 2).

Third, this study used demographic characteristics of households as control variables to focus on the role of saving goals in the likelihood of saving. It would be interesting to use an interaction model or to run the analyses on subsamples, such as by age, to see if the effect of savings goals on the likelihood of saving varied by household characteristics. However, due to the limited proportion of households with some goals such as self-actualization, we did not use an interaction model or sample segmentation. One of these approaches might be reasonable with a larger sample size, for

instance, with a combination of more survey years, though that approach would be based on the assumption that the effect of savings goals on the likelihood of saving did not vary over time. Further research refining these measures could improve theoretical applications to empirical evidence to gain a better understanding of the relationship between hierarchical saving goals and saving behavior.

ImplicationsThis study confirmed the important relationship between the psychological needs of human beings and their saving decision. Financial planners, educators, and policy makers can utilize these empirical results and the application of Maslow’s hierarchical theory of human needs to improve household saving decisions.

Financial planners and educators should thus focus on helping households clarify their saving goals, and develop a financial plan to achieve those goals. Saving requires self-regulation of spending impulses (Shefrin & Thaler, 1988), and specific goals have a positive impact on saving in the descriptive patterns (Table 5). The effect of commitment to a specific goal can be amplified through a voluntary imposition of constraints on one’s future choices. Beyond whether one has a goal or not, increasing goal commitment can be reliant upon how to set specific, measurable, achievable, relevant, and track-able goals (O’Neil et al., 2000). Households should be guided on how to clarify their saving goals and classify them according to their various needs. Having a saving goal reflects both the psychological needs of households and their ideas on the connectivity between those needs and saving. Changing the way households think about their savings and the connectivity between their needs and saving can influence saving decisions. Specific methods can start from framing goals, which is required for setting a goal. Specific goals are more beneficial than nonspecific goals, as people are more committed to specific goals than nonspecific goals (Wright & Kacmar, 1994). Being able to clarify which saving goal one has, and why that goal is important, matters for households, whether they rely on the professional help of financial planners and educators or try to plan by themselves.

Some goals (such as self-actualization) can be too abstract, however. In this case, combining those goals with detailed strategies, such as concrete budget setting or plans for implementing goals, could increase the predictive power of saving (Peetz & Buehler, 2009). For instance, specifying a goal should include specifying how much to save for a certain goal, “I need to save $1,000 for vacations‚” rather

09795Text.indd 143 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015144

than an unspecified amount, “I need to save as much as I can,” thinking about why to save, and how to save. These devices can be used to make households feel more responsible in managing their saving matters through goal setting and concrete plans.

To guide their saving plans and financial progress, financial planners and educators also need to understand what households are seriously pursuing from a holistic, long-term perspective. This includes getting to know clients better, identifying their various aspirations and personal goals, connecting goals to their financial and psychosocial circumstances, and suggesting detailed saving plans. At the same time, encouraging households to have more personalized saving goals is another way for financial planners and educators to implement our findings. This suggestion could be more important for young adult financial decisions: Beutler (2012) and Beutler, Beutler, and McCoy (2008) noted that middle school/high school youth and post-high school adults viewed their sustainable prosperity beyond high income or social fame. Young adults considered their personal growth as an aspiration to achieve autonomy—becoming fully achieved is important for their economic prosperity or financial well-being. In particular, educators can see students internalizing the idea of saving. Students need to understand their socio-psychological needs related to saving behavior through educators teaching the importance of saving by focusing on personal desires: describing individual dreams and connecting those dreams to saving decisions, practicing pursuing goals consistently, checking process, and sharing their ideas and difficulties together can help students learn healthy financial decisions as well as habitual ways of saving.

This does not necessarily imply, however, the sole importance of personal needs, disregarding the importance of other goals such as retirement/security and emergency/safety. Saving goals can be complementary and coexist (Fisher & Anong, 2012): for instance, less than 2% of households had self-actualization goals, indicating that these households simultaneously had other saving goals. Instead, financial planners and educators should note (a) that households can have multiple saving goals simultaneously, and (b) the relative effects of those goals on saving decisions. Specifically, financial planners can recommend that households have separate saving accounts for saving goals, which can increase goal commitment in terms of improved visualization of detailed plans and achievement of those goals.

Policy makers could benefit from this study as a tool to change perspectives on household saving policy. Encouraging households to pursue specific saving goals and participate in saving decisions can improve not only economic growth and stability, but also the psychological well-being of households. Garland (1983) suggested that even externally imposed goals can lead to better outcomes for individuals.

ReferencesAknin, L. B., Barrington-Leigh, C. P., Dunn, E. W., Helliwell,

J. F., Burns, J., Biswas-Diener, R.,…Norton, M. I. (2013). Prosocial spending and well-being: Cross-cultural evidence for a psychological universal. Journal of Personality and Social Psychology, 104(4), 635-652.

Ando, A., & Modigliani, F. (1963). The “life cycle” hypothesis of saving: Aggregate implications and tests. American Economic Review, 53(1), 55-84.

Ariely, D., & Wertenbroch, K. (2002). Procrastination, deadline, and performance: Self-control by precommitment. Psychological Science, 13(3), 219-224.

Barsky, R. B., Juster, F. T., Kimball, M. S., & Shapiro, M. D. (1997). Preference parameters and behavioral heterogeneity: An experimental approach in the health and retirement study. The Quarterly Journal of Economics, 112(2), 537-579.

Berry, C. M., Gruys, M. L., & Sackett, P. R. (2006) Educational attainment as a proxy for cognitive ability in selection: Effects on levels of cognitive ability and adverse impact. Journal of Applied Psychology, 91(3), 696-705.

Beutler, I. F. (2012). Connections to economic prosperity: Money aspiration from adolescence to emerging adulthood. Journal of Financial Counseling and Planning, 23(1), 17-32.

Beutler, I. F., Beutler, L. B., & McCoy, J. K. (2008). Money aspirations about living well: Development of adolescent aspirations from middle school to high school. Journal of Financial Counselling and Planning, 19(2), 67-82.

Browning, M., & Lusardi, A. (1996). Household saving: Micro theories and micro facts. Journal of Economic Literature, 34(4), 1797-1855.

Brunier, G., Graydon, J., Rothman, B., Sherman, C., & Liadsky, R. (2002). The psychological well-being of renal peer support volunteers. Journal of Advanced Nursing, 38(1), 40-49.

Bryant, W. K., & Zick, C. D. (2006). The economic organization of the household. New York: Cambridge University Press

Bucks, B. K., Kennickell, A. B., & Moore, K. B. (2006).

09795Text.indd 144 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015 145

Recent changes in U.S. family finances: Evidence from the 2001 and 2004 Survey of Consumer Finances. Federal Reserve Bulletin, 92, A1-A38.

Bucks, B. K., Kennickell, A. B., Mach, T. L., & Moore, K. B. (2009). Changes in U.S. family finances from the 2004 and 2007: Evidence from the Survey of Consumer Finances. Federal Reserve Bulletin, 95, A1-A55.

Canova, L., Rattazzi, A. M., & Webley, P. (2005). The hierarchical structure of saving motives. Journal of Economic Psychology, 26(1), 21-34.

Carroll, C. D. (1992). The buffer-stock theory of saving: Economic evidence. Brookings Papers on Economic Activity, 1992(2), 62-156.

Chang, Y. R. (1994). Saving behavior of U.S. households in the 1980s: Results from the 1983 and 1986 Survey of Consumer Finance. Journal of Financial Counseling and Planning, 5, 45-64.

Danes, S. M., Lee, J., Stafford, K., & Heck, R. K. (2008). The effects of ethnicity, families and culture on entrepreneurial experience: An extension of sustainable family business theory. Invited article for Journal of Developmental Entrepreneurship, Special Issue titled Empirical Research on Ethnicity and Entrepreneurship in the U.S., 13(3), 229-268.

Deci, E., & Ryan, R. (2000). The what and why of goal pursuits: Human needs and the self-determination of behavior. Psychological Inquiry, 11(4), 227-268.

DeVaney, S. A., Anong, S. T., & Whirl, S. E. (2007). Household savings motives and a hierarchy of needs. Journal of Consumer Affairs, 41(1), 174-186.

Dunn, E. W., Aknin, L. B., & Norton, M. I. (2008). Spending money on others promotes happiness. Science, 319, 1687-1688.

Dusenberry, J. (1949). Income, saving and the theory of consumer behavior. Cambridge, MA: Harvard University Press.

Dynan, K., Skinner, J., & Zedels, S. (2004). Household savings motives. The Journal of Affairs, 41, 174-186.

Evangelidis, I., & Levav, J. (2013). Prominence versus dominance: How relationships between alternatives drive decision strategy and choice. Journal of Marketing Research, 50(6), 753-766.

Ewing, B. T., & Payne, J. E. (1998). The long-run relation between the personal savings rate and consumer sentiment. Journal of Financial Counseling and Planning, 9(1), 89-96.

Fischer, G. W., Carmon, Z., Ariely, D., & Zauberman, G. (1999). Goal-based construction of preferences: Task goals and the prominence effect. Management Science,

45(8), 1057-1075.Fisher, P. J., & Anong, S. T. (2012). Relationship of saving

motives to saving habits. Journal of Financial Counseling and Planning, 23(1), 63-79.

Fisher, P. J., & Hsu, C. (2012). Differences in household saving between non-Hispanic white and Hispanic households. Hispanic Journal of Behavioral Sciences, 34(1), 137-159.

Fisher, P. J., & Montalto, C. P. (2010). Effect of saving motives and horizon on saving behaviors. Journal of Economic Psychology, 31(1), 92-105.

Fisher, P. J., & Montalto, C. P. (2011). Loss aversion and saving behavior: Evidence from the 2007 US Survey of Consumer Finances. Journal of Family and Economic Issues, 32(1), 4-14.

Ford, M. E. (1992). Human motivation: Goals, emotions, and personal agency belief. Newbury Park, CA: Sage.

Frederick, S., Loewenstein, G., & O’Donoghue, T. (2002). Time discounting and time preference: A critical review. Journal of Economic Literature, 40(2), 351-401.

Friedman, M. (1957). A theory of the consumption function. Princeton, NJ: Princeton University Press.

Fujita, K., Trope, Y., Liberman, N., & Levin-Sagi, M. (2006). Construal level and self-control. Journal of Personality and Social Psychology, 90(3), 351-367.

Garland, H. (1983). Influence of ability, assigned goals, and normative information on personal goals and performance: A challenge to the goal attainability assumption. Journal of Applied Psychology, 68(1), 20.

Gleitman, H., Fridlund, A.J., & Reisberg, D. (2004). Psychology. New York: Norton.

Gómez-Miñambres, J. (2012). Motivation through goal setting. Journal of Economic Psychology. 33(6), 1223-1239.

Harbaugh, W. T., Mayr, U., & Burghart, D. R. (2007). Neural responses to taxation and voluntary giving reveal motives for charitable donations. Science, 316(5831), 1622-1625.

Hayashi, F., Ito, T., & Slemrod, J. (1988). Housing finance imperfections, taxation, and private saving: A comparative simulation analysis of the United States and Japan. Journal of the Japanese and International Economics, 2(3), 215-238.

Heaton, J., & Lucas, D. (1997). Market frictions, savings behavior, and portfolio choice. Macroeconomic Dynamics, 1(1), 76-101.

Hogarth, J. M., & Anguelov, C. E. (2003). Can the poor save? Journal of Financial Counseling and Planning, 14(1), 1-18.

Hollenbeck, J. R., & Klein, H. J. (1987). Goal commitment

09795Text.indd 145 12/9/15 4:11 PM

Journal of Financial Counseling and Planning Volume 26, Issue 2 2015146

and the goal-setting process: Problems, prospects, and proposals for future research. Journal of Applied Psychology, 72, 212-220.

Huggett, M., & Ventura, G. (2000). Understanding why high income households save more than low income households. Journal of Monetary Economics, 45(2), 361-397.

Hurd, M., & Rohwedder, S. (2003). The retirement-consumption puzzle: Anticipated and actual declines in spending at retirement (No. w9586). National Bureau of Economic Research.

Katona, G. (1975). Psychological economics. New York: Elsevier.

Kennickell, A. B. (2009). Codebook for 2007 Survey of Consumer Finances. Washington, DC: Board of Governors of the Federal Reserve System.